Financial Markets

Fears of a hard landing are abating as growth has been surprising to the upside. New worries are emerging, such as the trajectory of disinflation, and the pace and timing of rate cuts. In this environment, it is important to build a resilient all-weather portfolio, which protects against a correction, rising rates, or stubborn inflation but also has exposure to the AI theme.

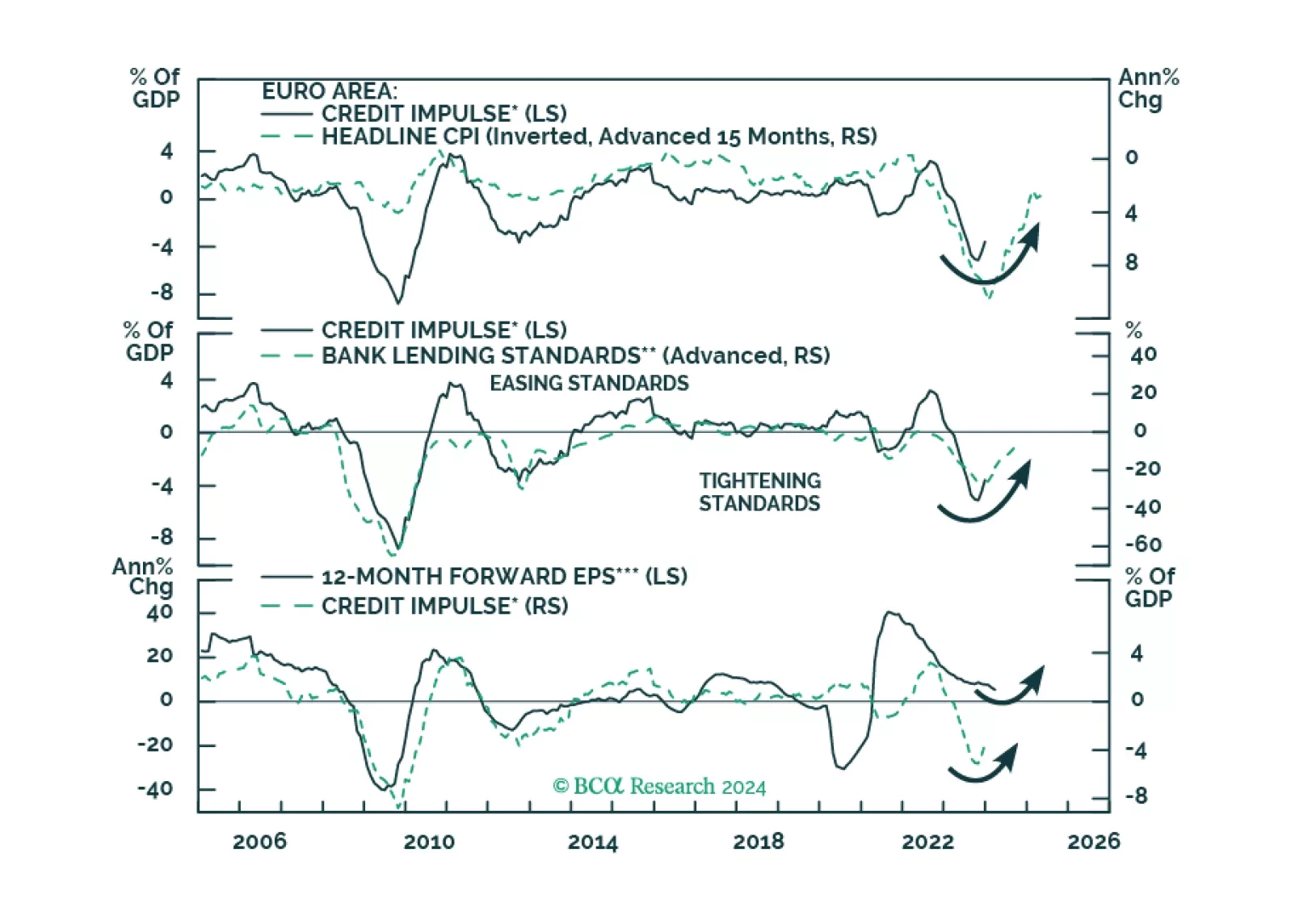

Europe credit flows are stabilizing, hence a major drag on the region’s growth will dissipate. What does this development imply for European equities?

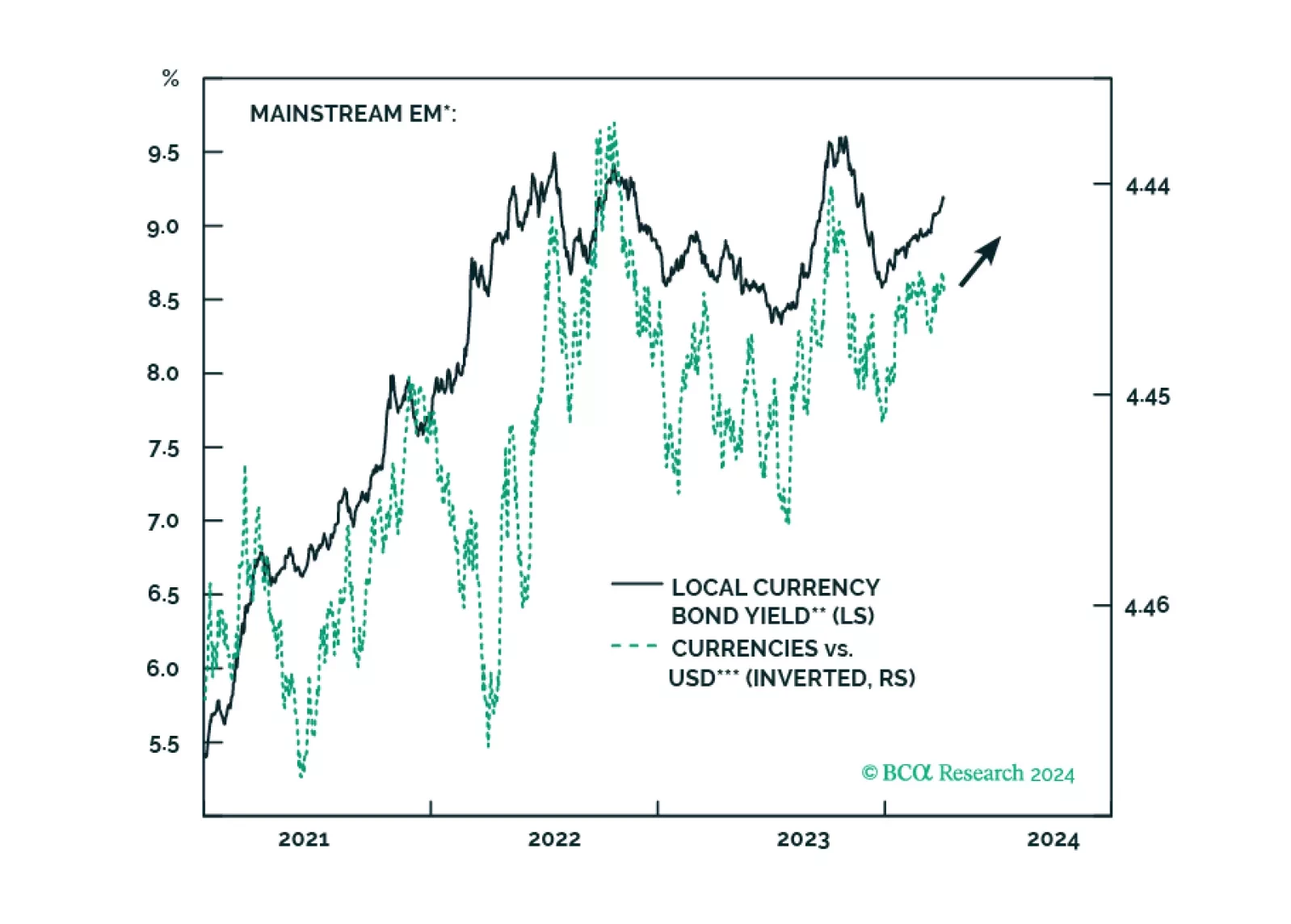

Climbing US bond yields, alongside higher oil prices, might spoil the party for global risk assets. There are budding cracks in EM domestic bonds, and even though we like this asset class in the long run, investors exposed to it should reduce their positions for now.

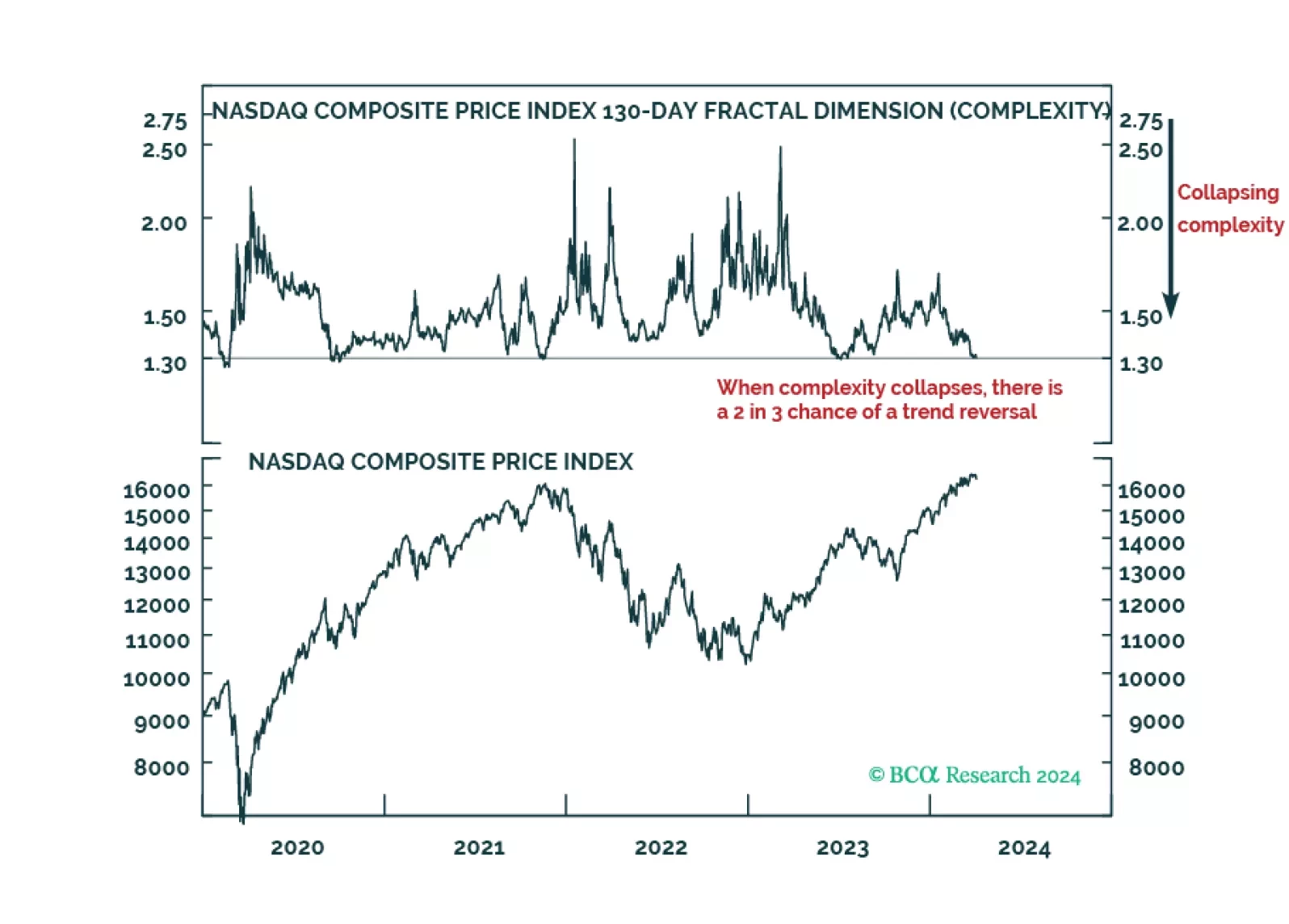

The analysis of complexity is a massive competitive advantage in investing, and from today, clients will be able to monitor the complexities of the world’s 17 major investments on our webpage in real-time.

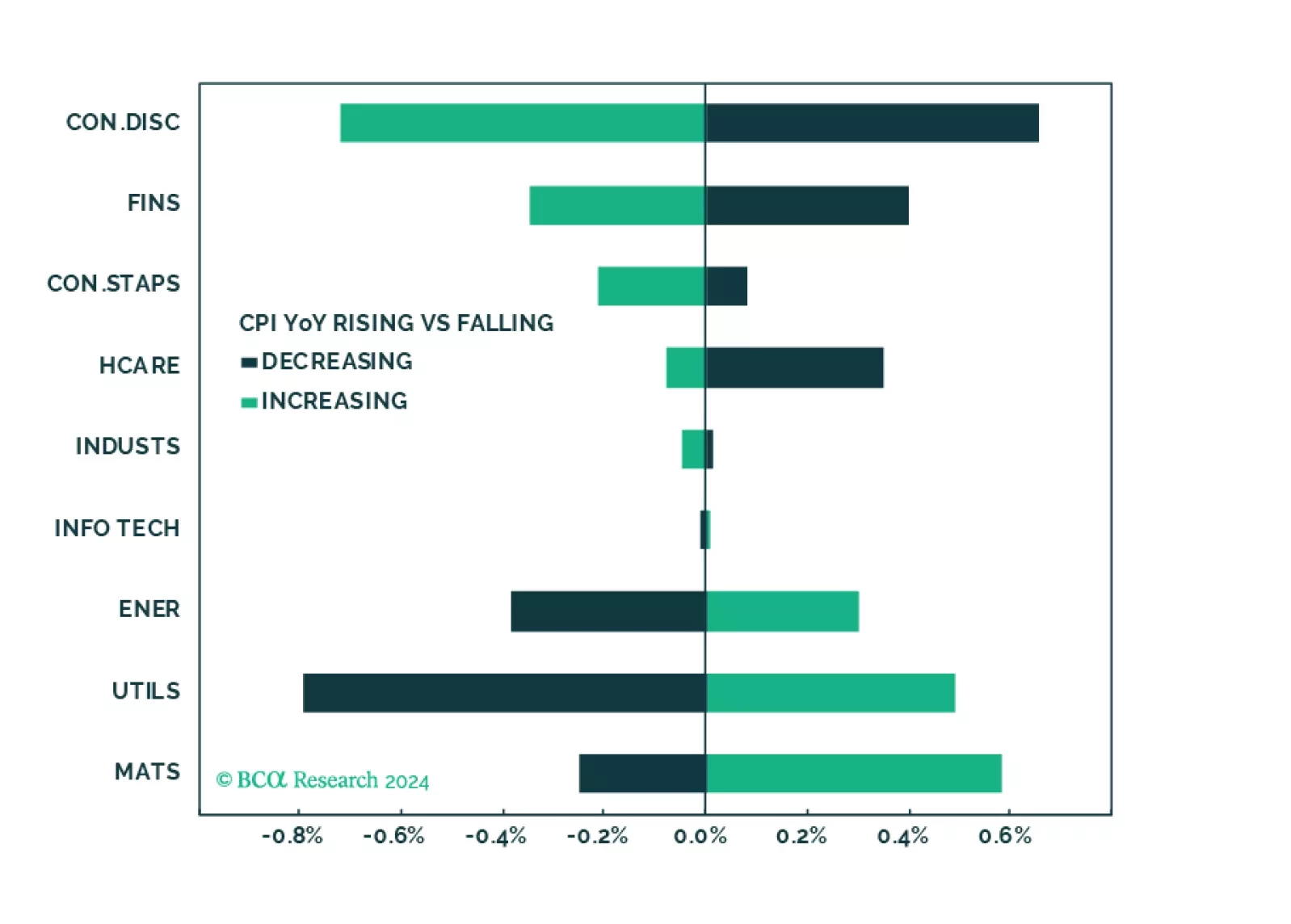

The equity rally extended into March as hard landing outcome was priced out. It has broadened, as money flowed into less over-loved pockets of the market. Our models signal that margins are about to stabilize, and earnings growth will accelerate as the year progresses. However, companies are raising prices again and the no-landing outcome and fewer than three rate cuts this year are increasingly likely.