Financial Markets

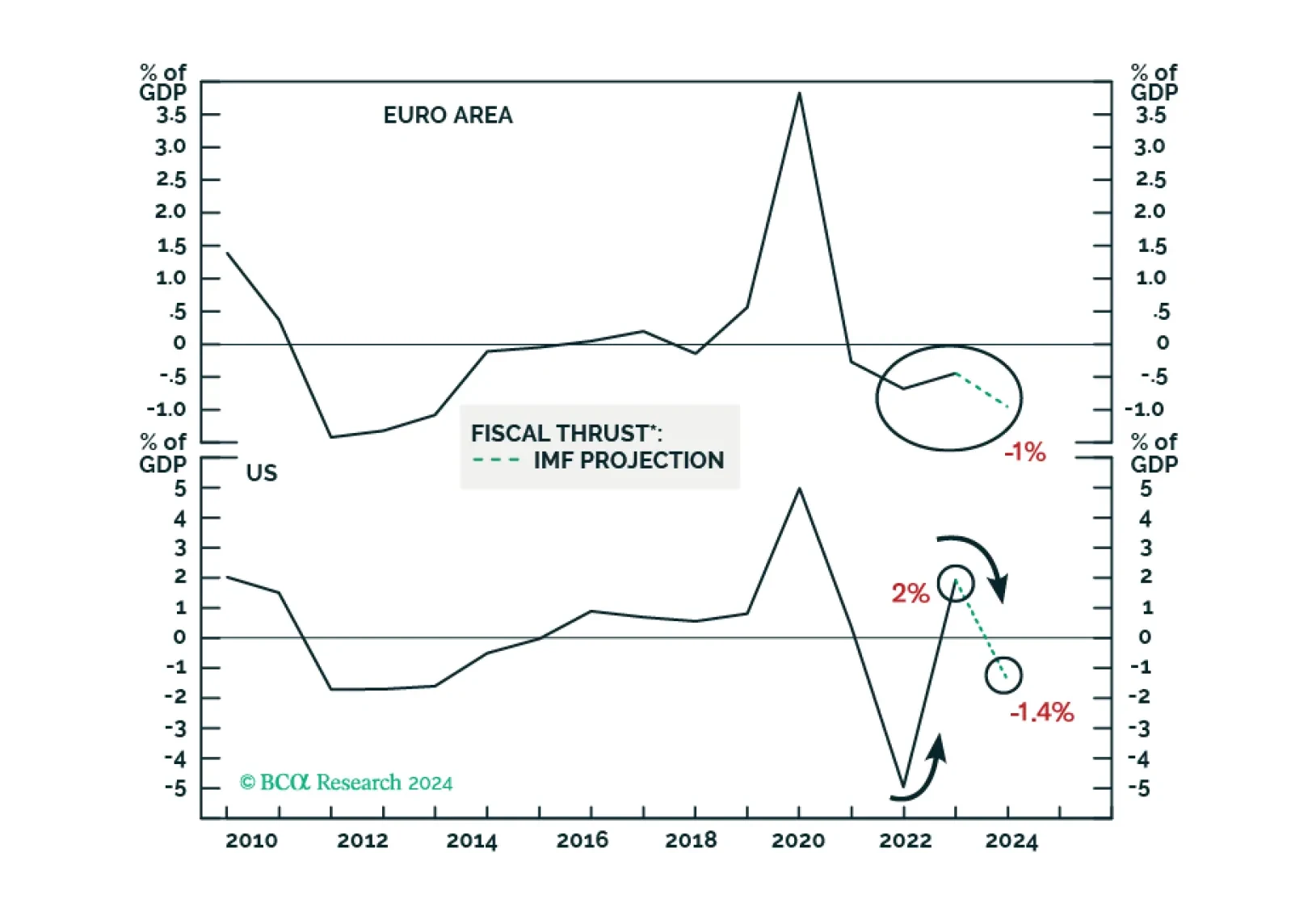

Despite a couple of rate cuts in H2 2024, borrowing costs will remain elevated in real terms amid lower inflation in the US and Europe. This and tightening fiscal policy will hinder domestic demand in advanced economies. Domestic demand in China and EM ex-China will remain very tepid, with risks skewed to the downside.

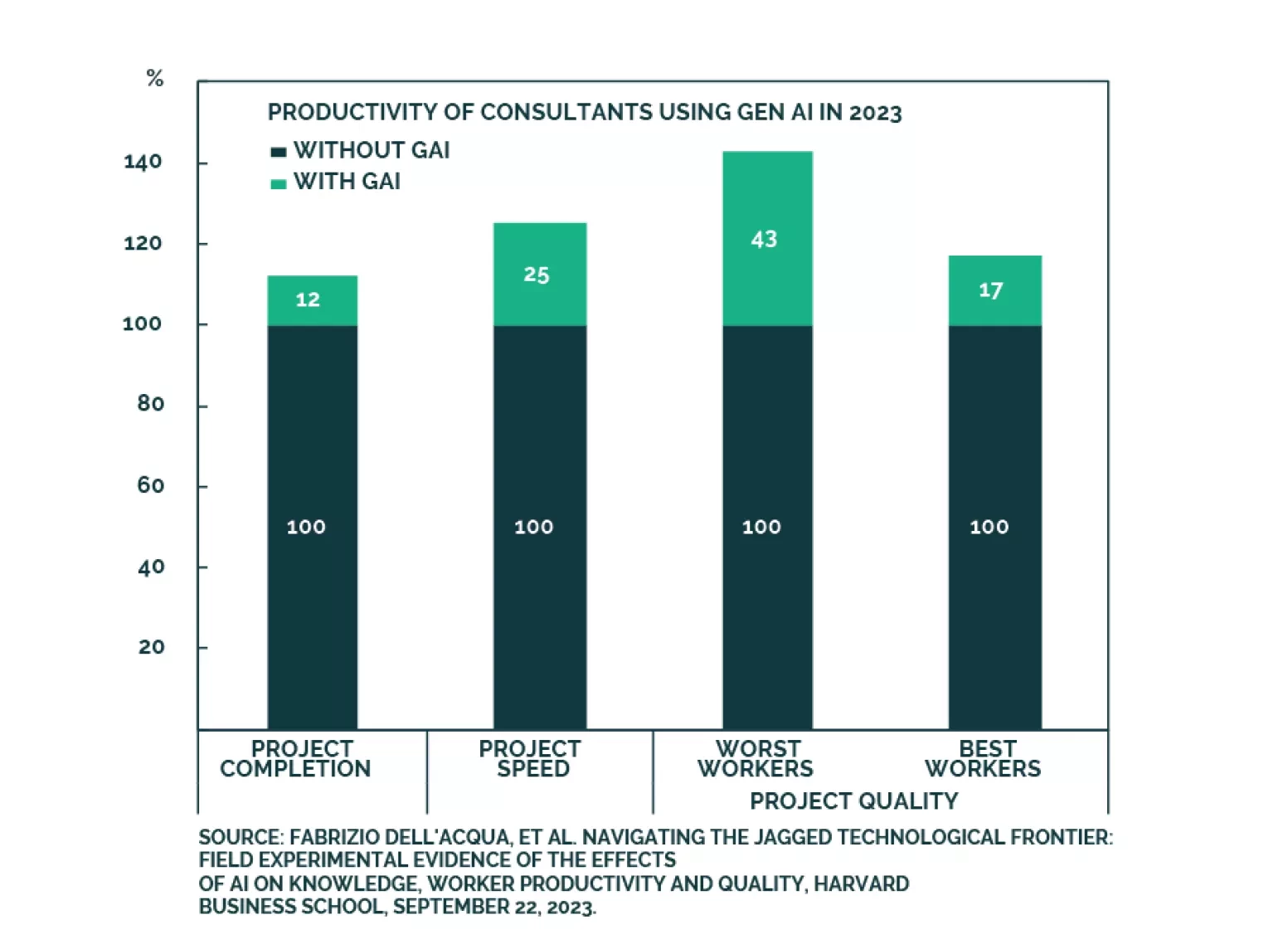

GAI technology has made tremendous gains over the past year. It has advanced from being a mere “curiosity” to becoming an everyday helper. While the promise of GAI is enormous, its effects are still limited: Companies are still struggling with monetization while productivity improvement is still at least a year away. In terms of evolution, the focus is shifting away from “picks and shovels” infrastructure companies toward model and application developers.

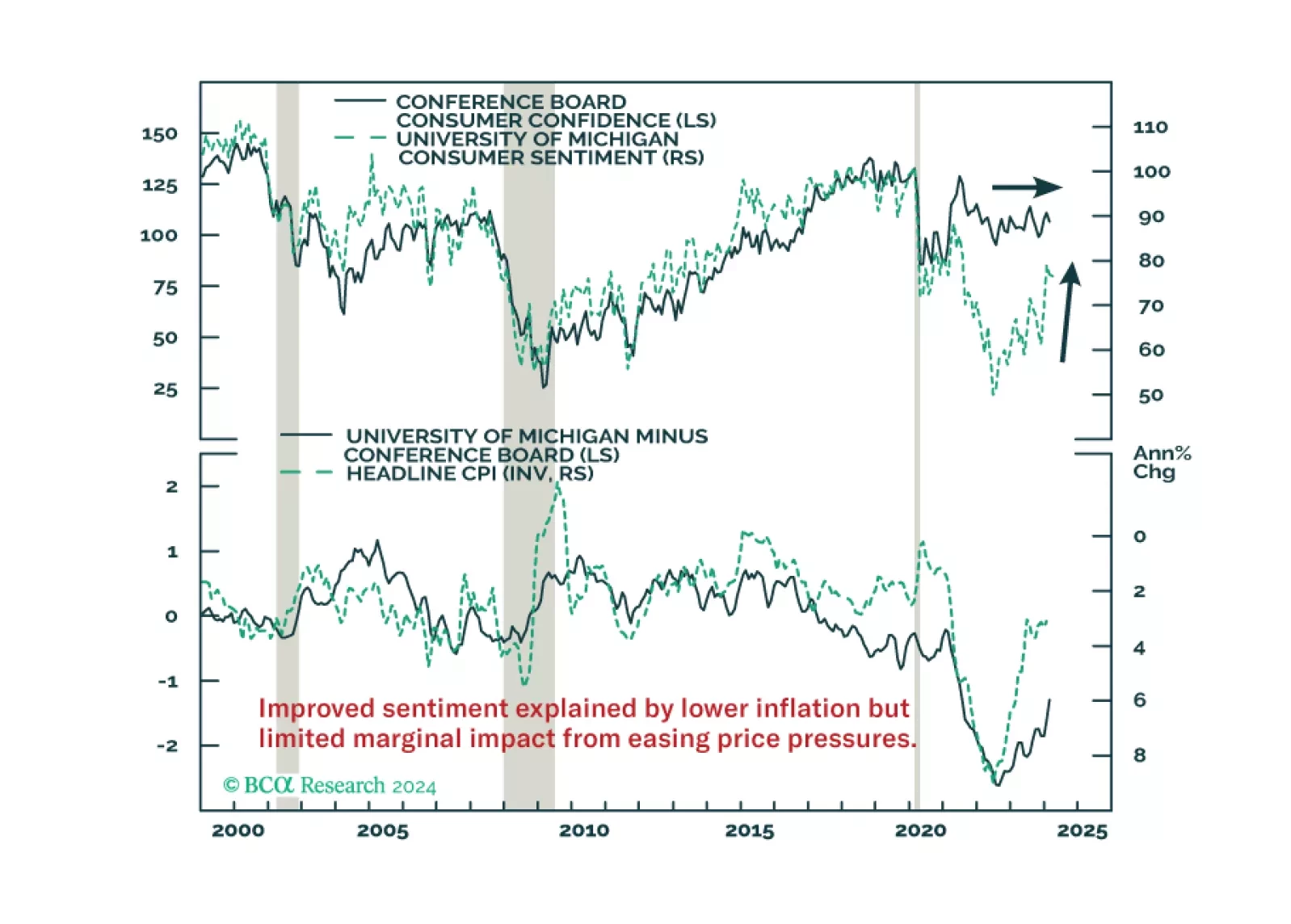

Improved consumer morale will not compensate for the fading tailwinds to consumption. Neither will the wealth effects from higher stocks and home prices.

We assess where emerging markets debt is on a strategic and cyclical basis. We find it has benefited from local central banks boosting their inflation-fighting credentials and governments improving financial stability. As a result, EM debt is behaving less like a risk-on asset, changing the role it plays in a global portfolio. We also expand our asset allocation playbook by assessing how the asset class behaves across the business cycle. While EM debt is more than a risk-on play, we suggest investors stay cautious on a cyclical horizon.

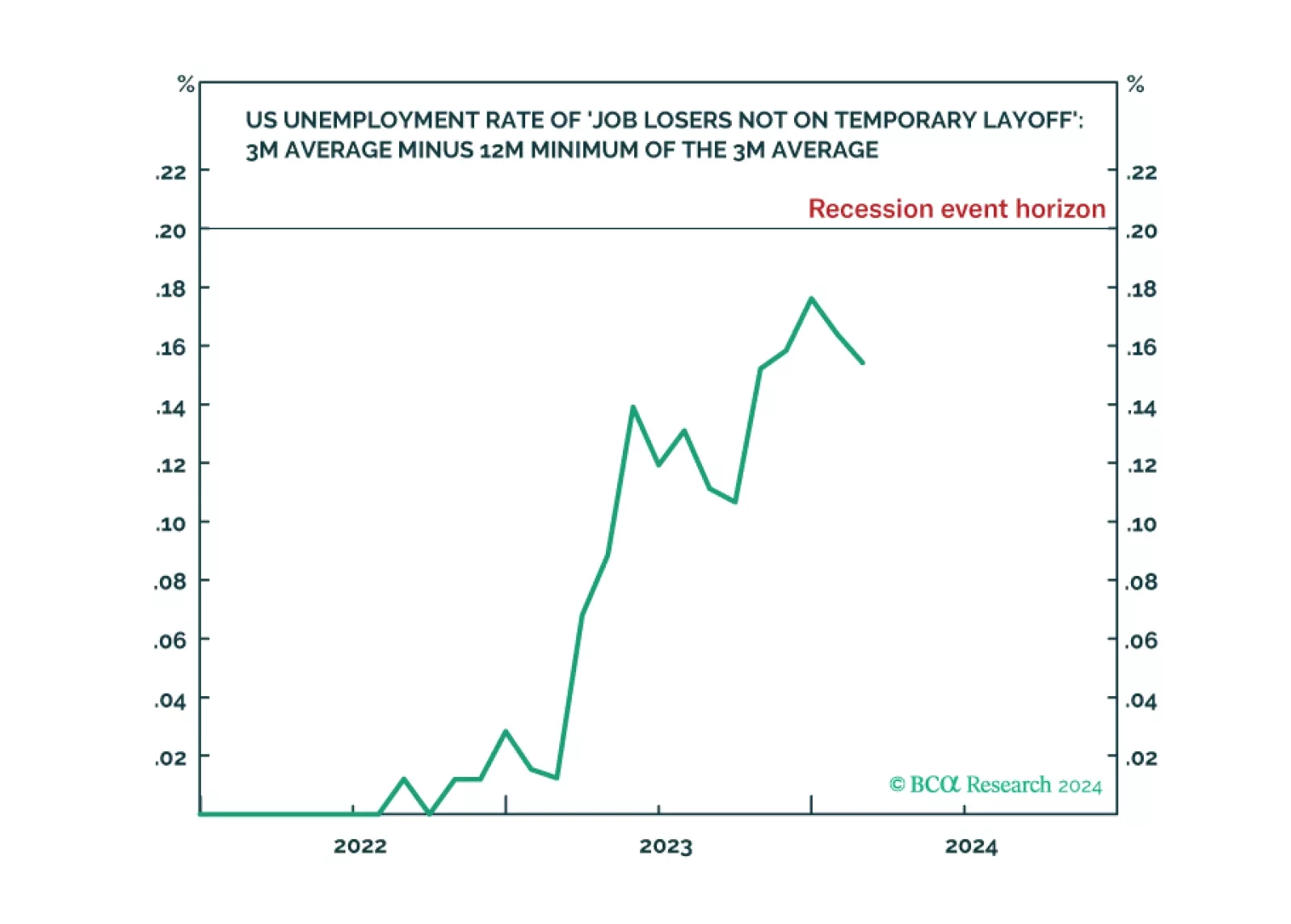

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).

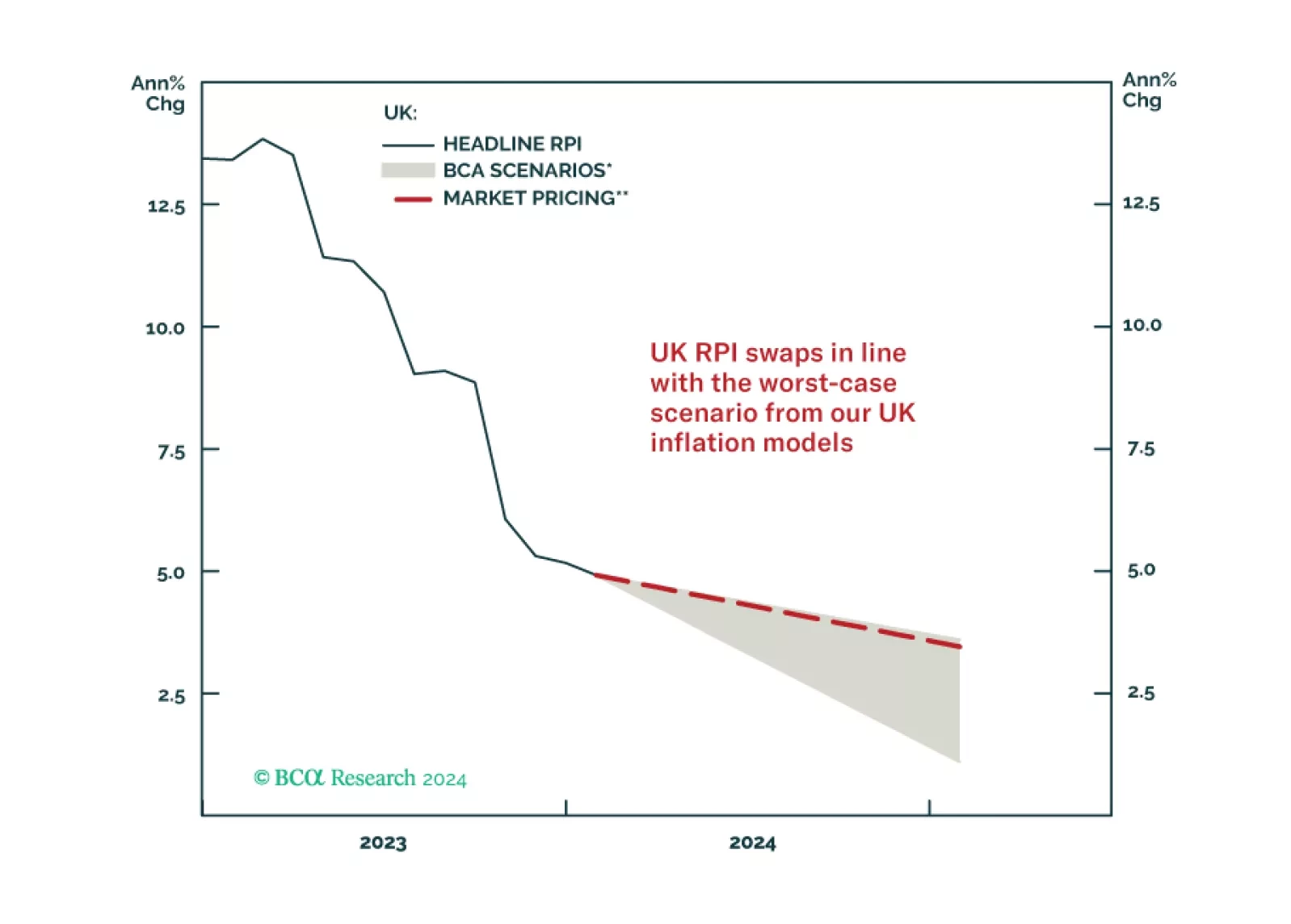

In this Special Report, we introduce our UK Linkers Golden Rule – a framework to profitably trade and invest in UK inflation-linked bonds versus nominal UK gilts. The Rule is currently signaling that nominal Gilts should outperform UK linkers over the next year as UK inflation slows.