Financial Markets

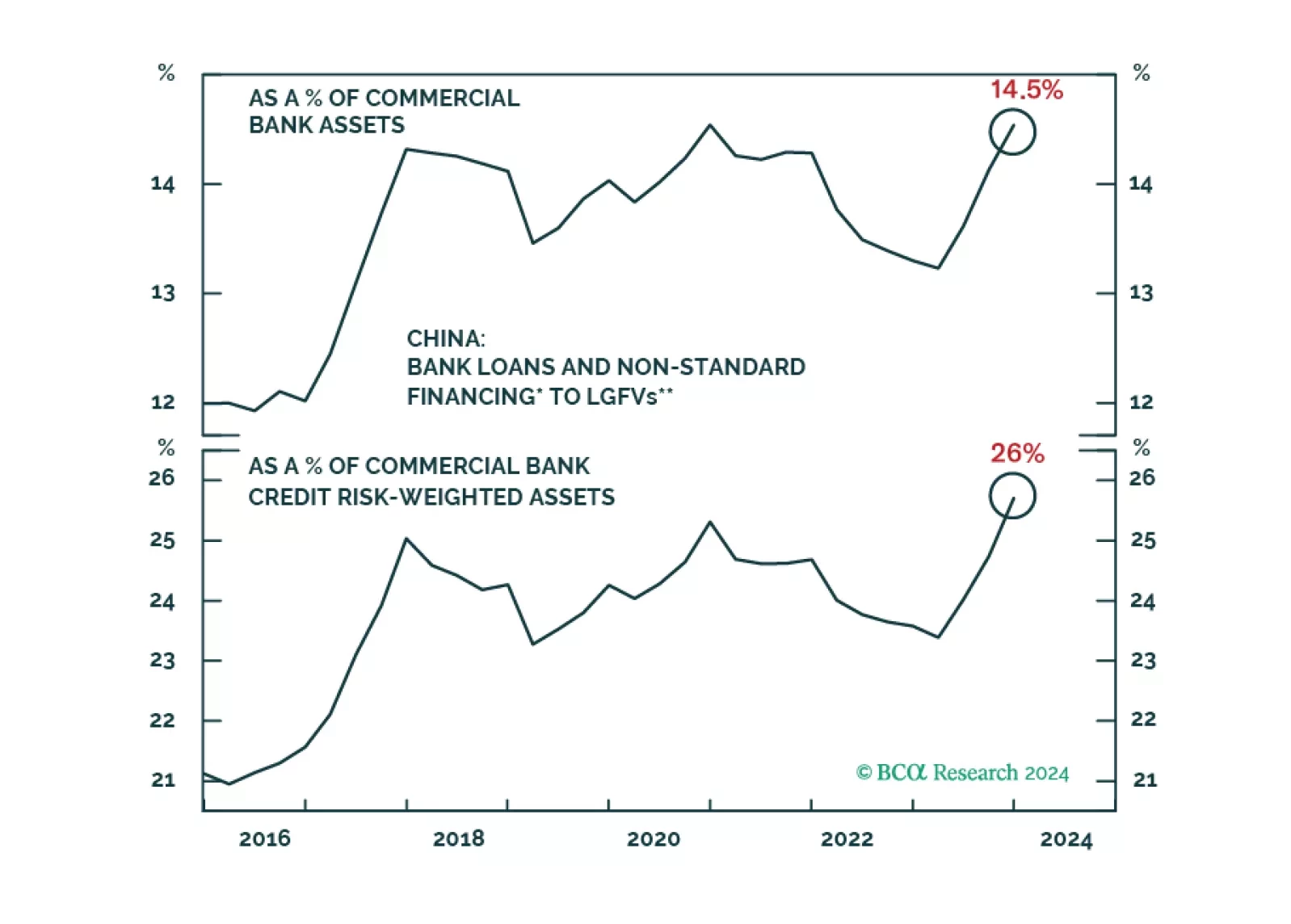

The odds of a “Minsky Moment” for the Chinese banking sector are low. They, however, will continue facing cyclical and structural headwinds, including a dismal asset quality and profit outlook. Bank stocks remain a value trap. Absolute-return investors should sell rebounds in Chinese bank stocks.

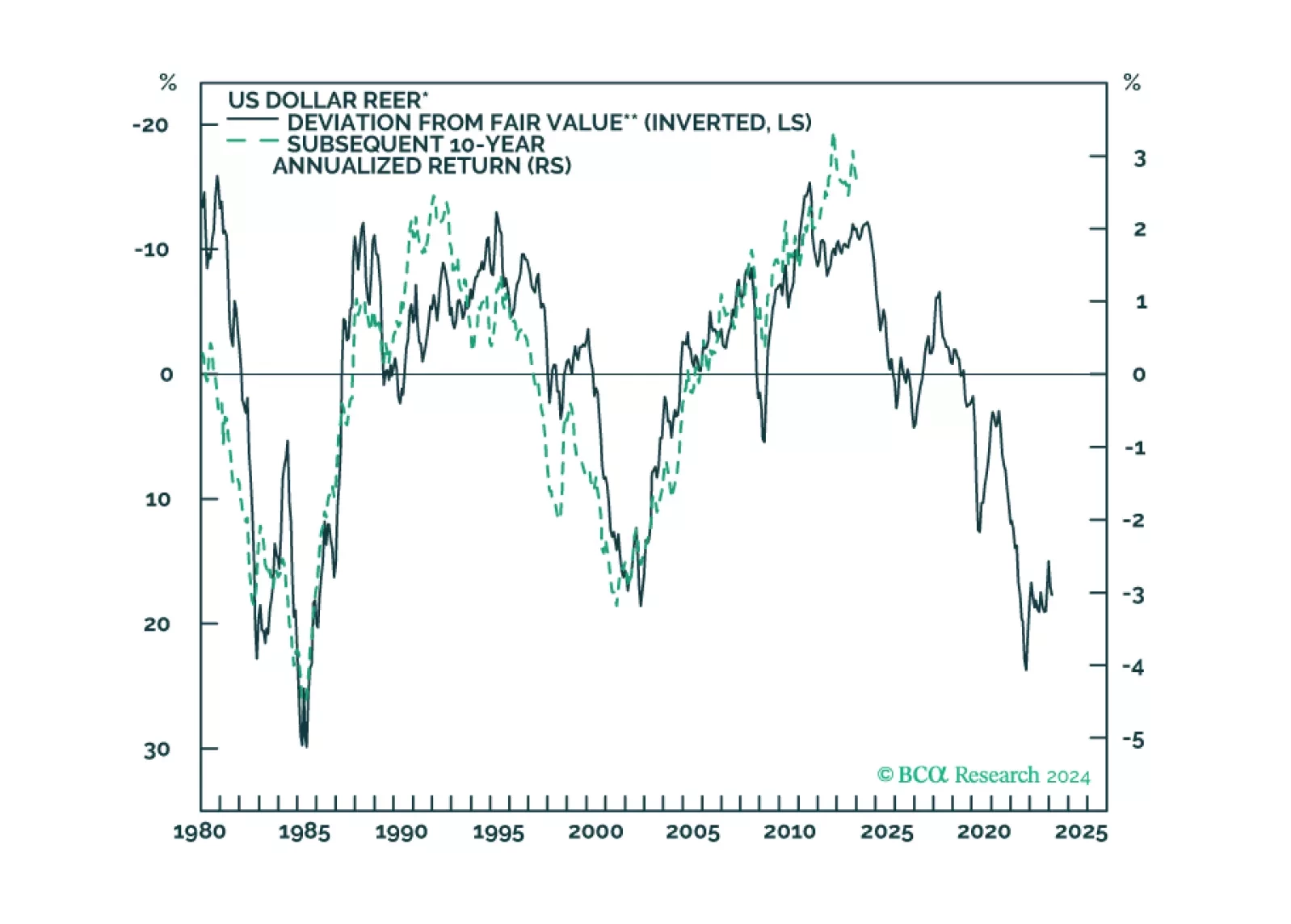

In this week’s report, we release an update to our long-term REER valuation model and expected future returns for major currencies.

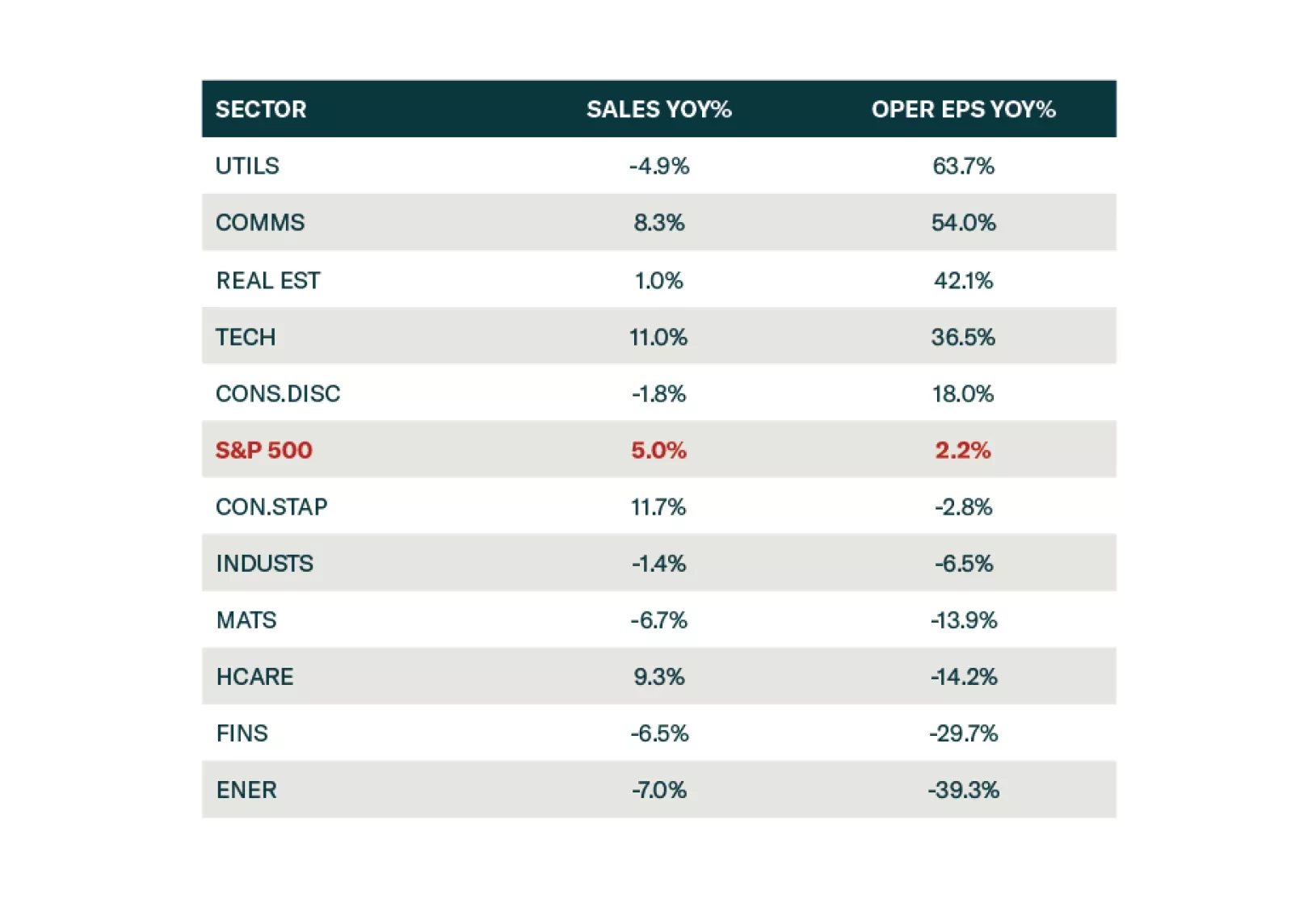

Reported earnings for Q4-2023 were rather underwhelming and prone to issues that we have identified over the past few months: Growth is concentrated in just a few sectors and companies, while the profitability of a broad swath of the equity market is under pressure from disinflation and sticky wages. Consumers are still spending, but less enthusiastically than before, while a switch from spending on services to spending on goods is in its very early innings. Downgrade Consumer Staples to neutral.

Households have ramped up their cash holdings since the end of 2019, but the absence of an empirical link between cash and consumption leads us to believe that we’ve modestly overestimated the risk of consumer-driven overheating.

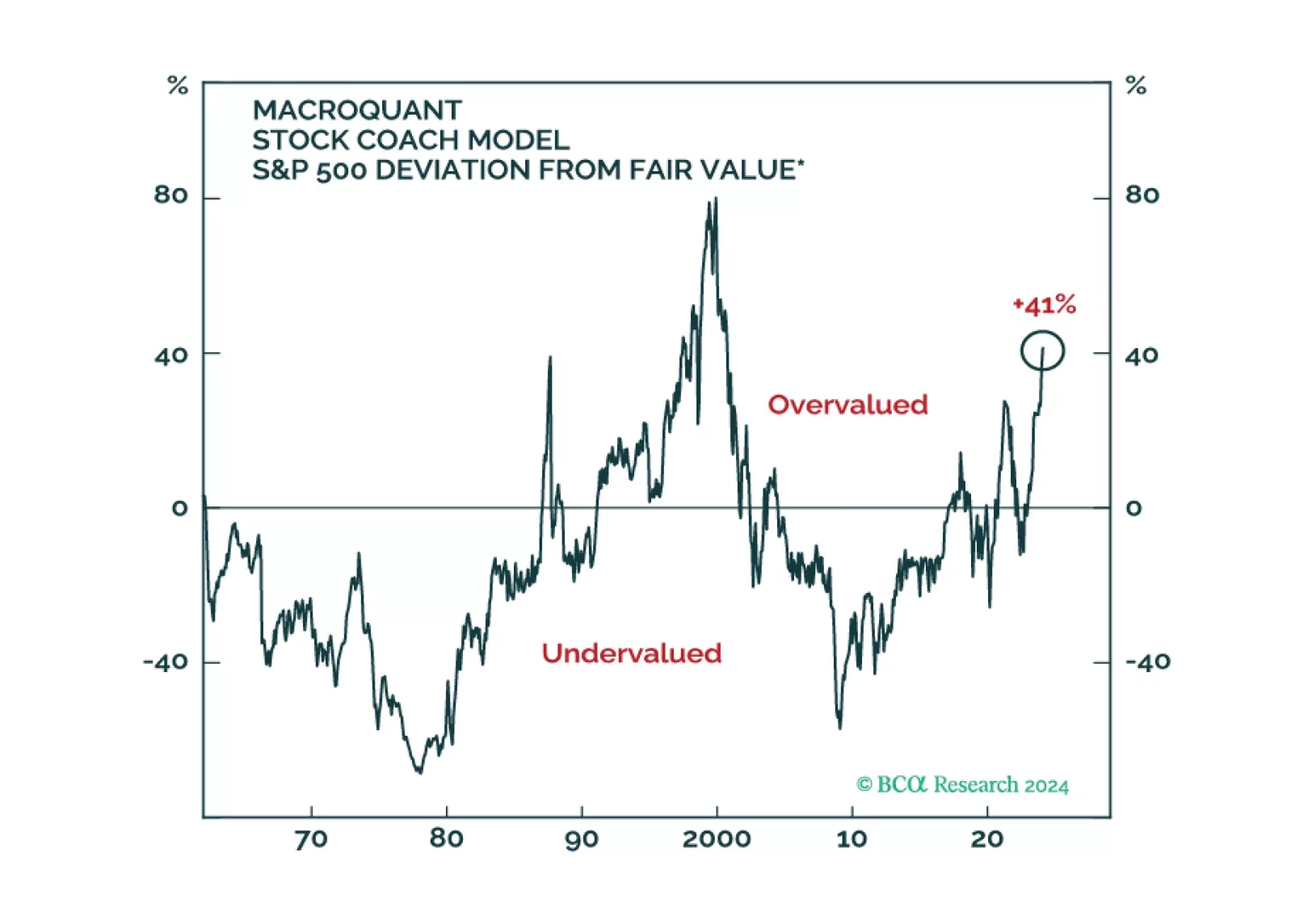

Recessions often begin seemingly out of the blue when the economy’s temperature falls enough to set in motion adverse feedback loops that cause unemployment to rise. We expect the US economy to suddenly freeze over towards the end of this year or in early 2025. For now, a benchmark allocation to equities is appropriate, but a more defensive stance will be necessary later this year.