Financial Markets

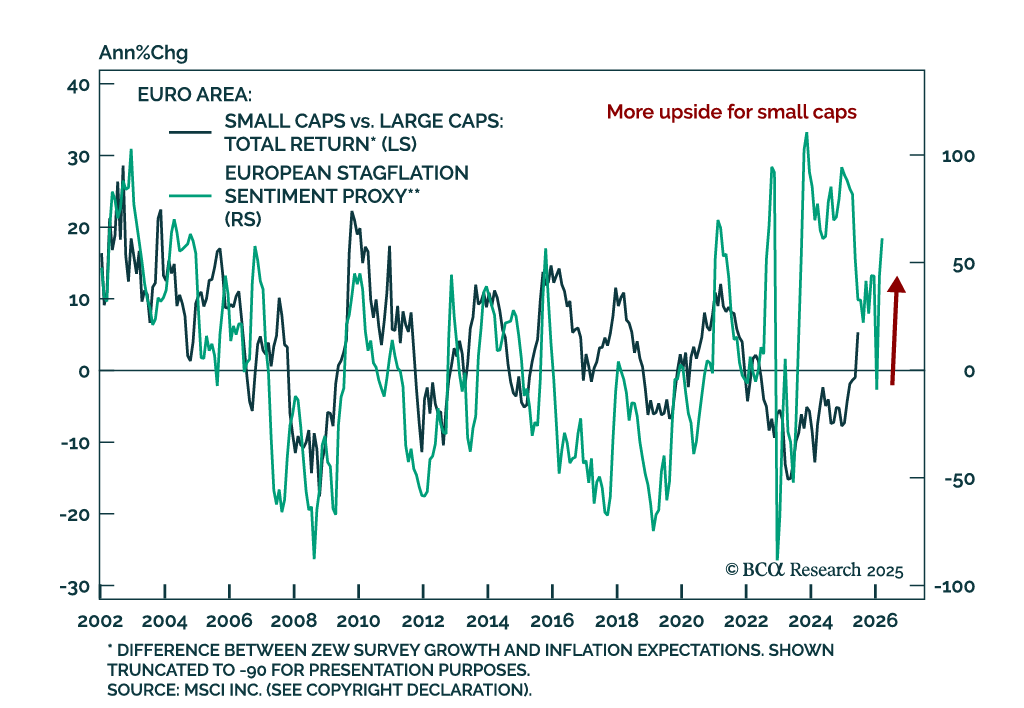

Our European Investment strategists upgrade small caps to maximum overweight, citing improving margins, supportive macro trends, and attractive valuations. They expect small caps to continue outperforming large caps over the next 12 to 18 months. With…

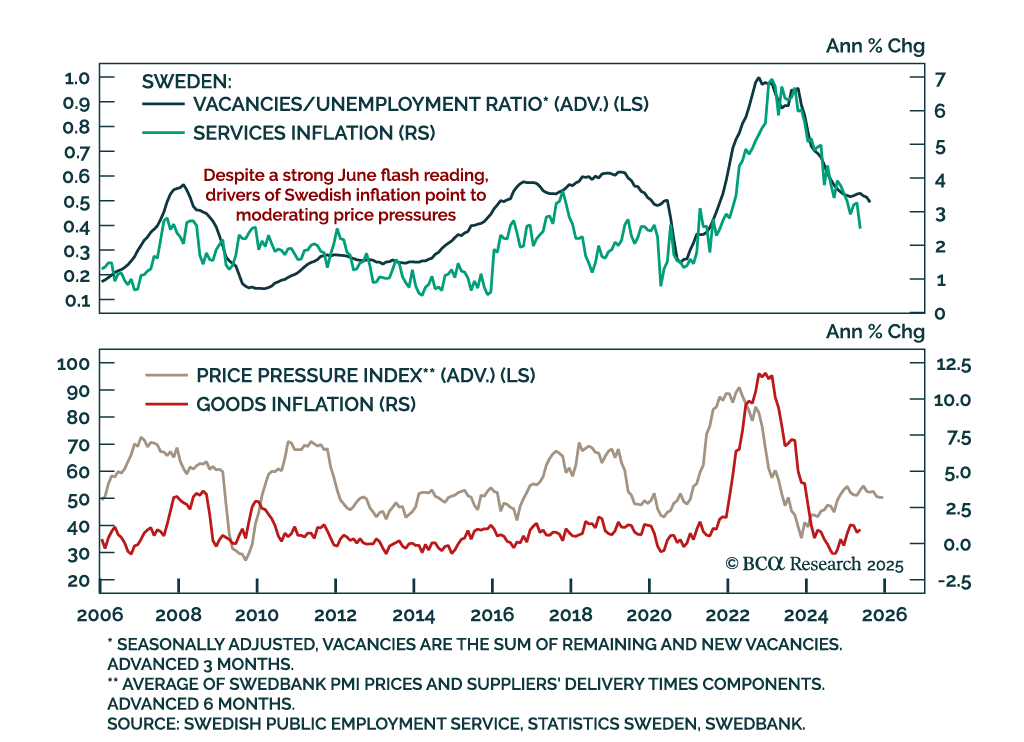

Stronger-than-expected June inflation will likely keep the Riksbank on hold in August, despite soft underlying trends. Headline inflation accelerated more than expected to 0.5% m/m (0.8% y/y), while CPI ex-housing rose to 2.9% y/y and core inflation to 3.3%…

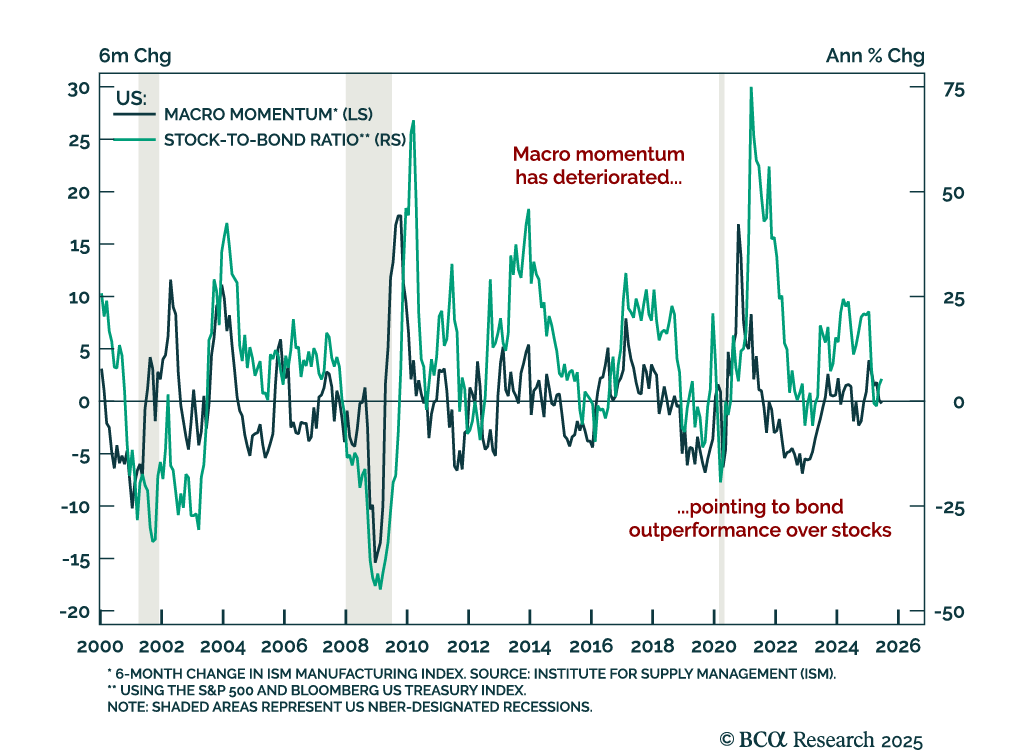

Deteriorating macro momentum supports a defensive asset allocation stance as hard data deteriorates. Last week’s ISM Manufacturing and Services PMIs confirmed that growth is slowing and price pressures are easing from a high level. The ISM Manufacturing index…

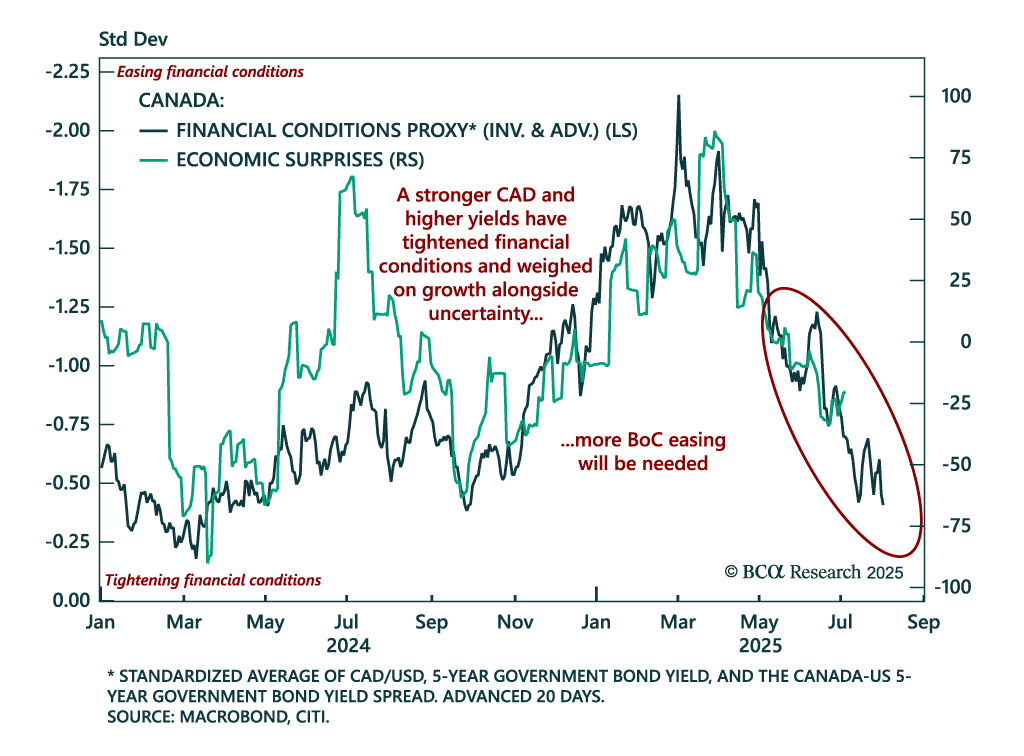

Canada’s stronger currency and tightening financial conditions point to further BoC easing and support long Canadian bond positions. The CAD has appreciated this year alongside the global push to diversify away from USD assets, which has weakened the US…

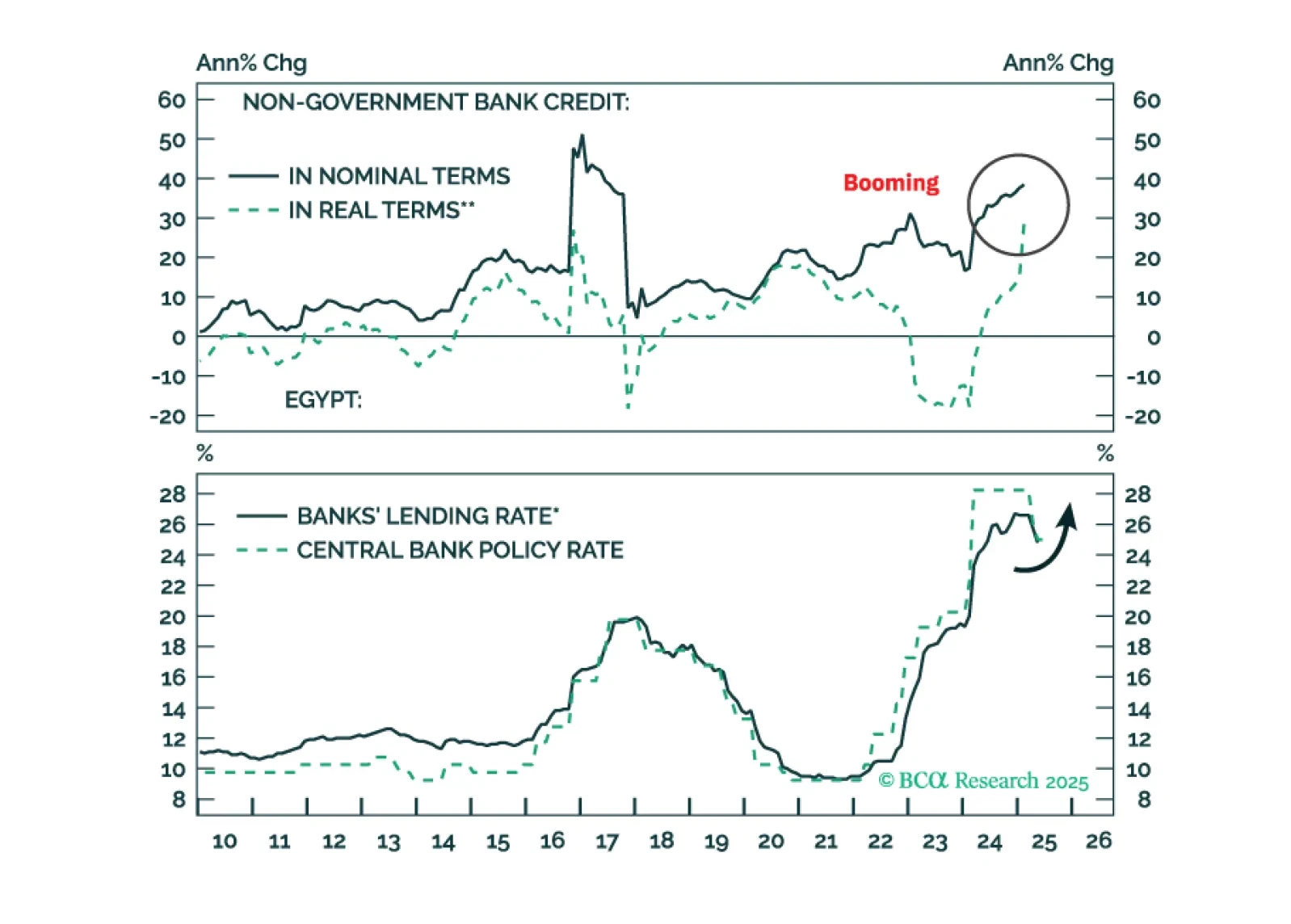

Downward pressure on the pound will rise in the coming months. Inflation will go up, so will bond yields. It’s time to book profits on Egyptian domestic bonds.

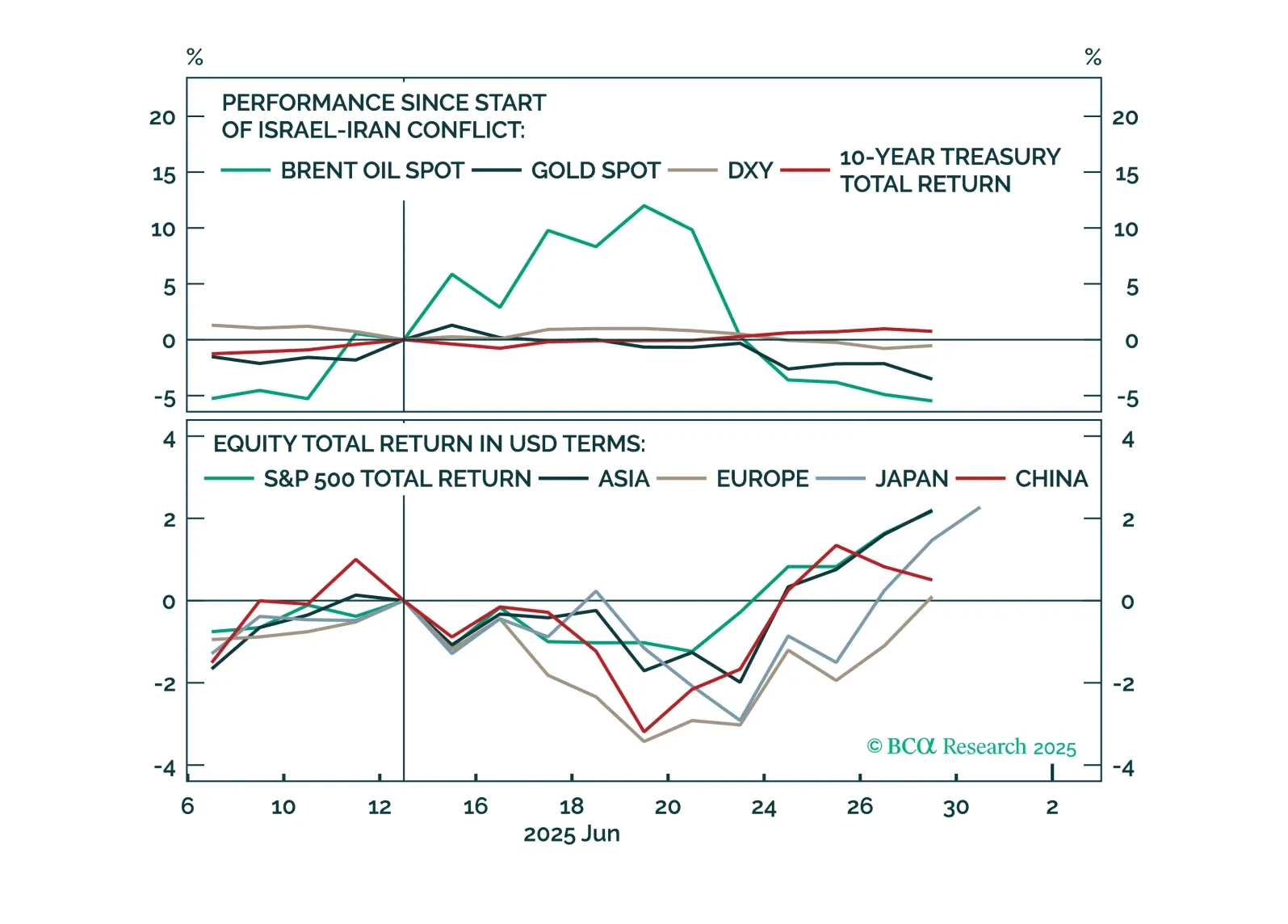

There is a thin line between geopolitical risk and Enlightenment, just ask Europe in the seventeenth century. The Middle East is exhibiting both. Investors are over-indexing on the negative – which has not impacted the investible universe – and ignoring the positives.

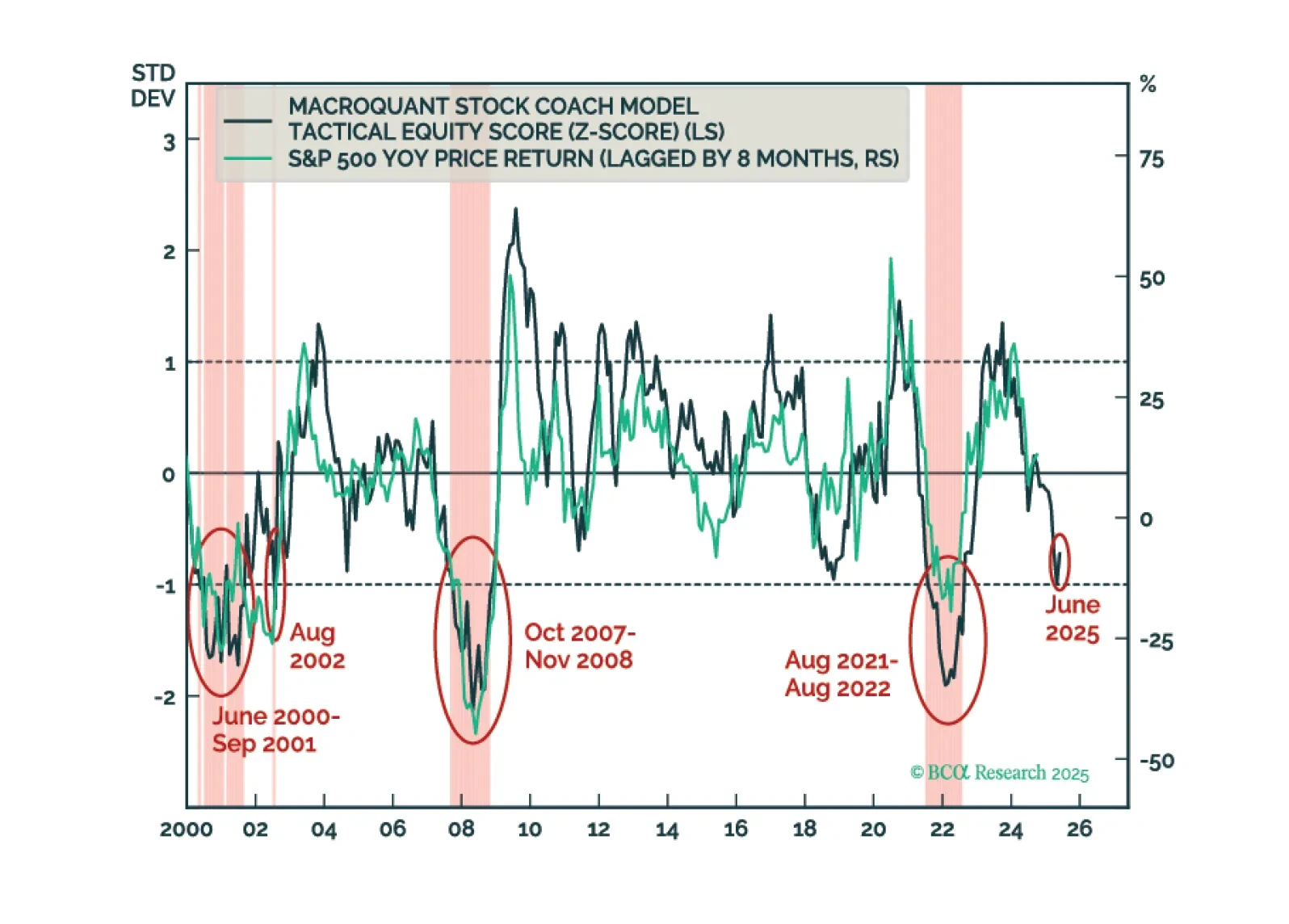

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.

Our US Bond strategists expect a modest narrowing of the Treasury/OIS spread, supporting a cyclical long-duration stance and 2s10s steepeners. Over the past year, the spread has added roughly 30 bps to the 10-year Treasury yield, driven by factors such as…

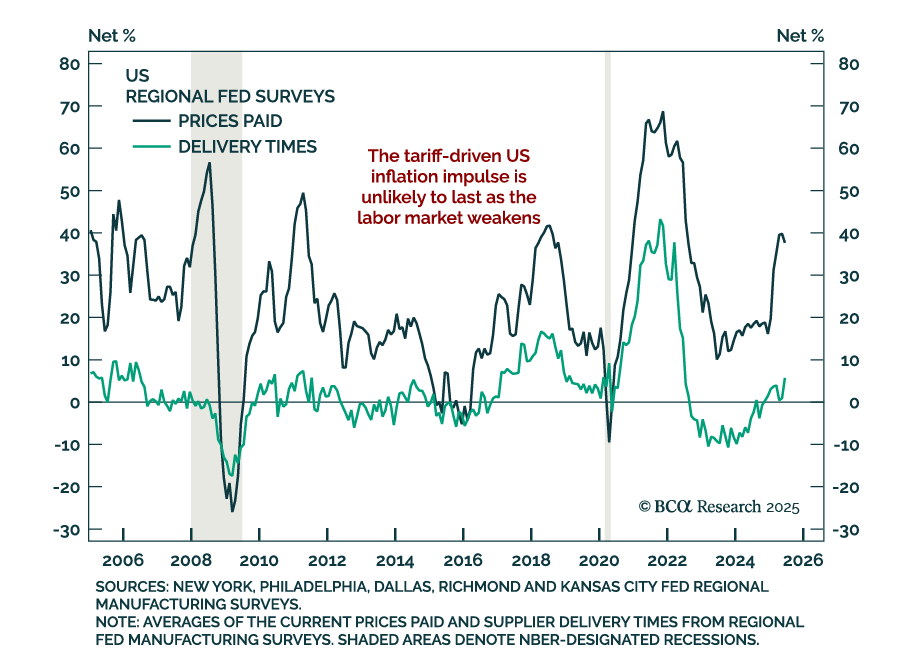

Regional Fed surveys confirm sluggish US manufacturing and tame inflation, supporting long duration positioning outside the US. The June Dallas Fed Manufacturing survey missed expectations, rising to -12.7 from -15.3, still deep in contraction. New orders…

Tech-led momentum is driving the S&P 500 to new highs despite weak growth and rising cyclical risks. The rally has accelerated following a de-escalation in geopolitical tensions and ongoing hopes for positive trade developments. Momentum signals confirm…