Financial Markets

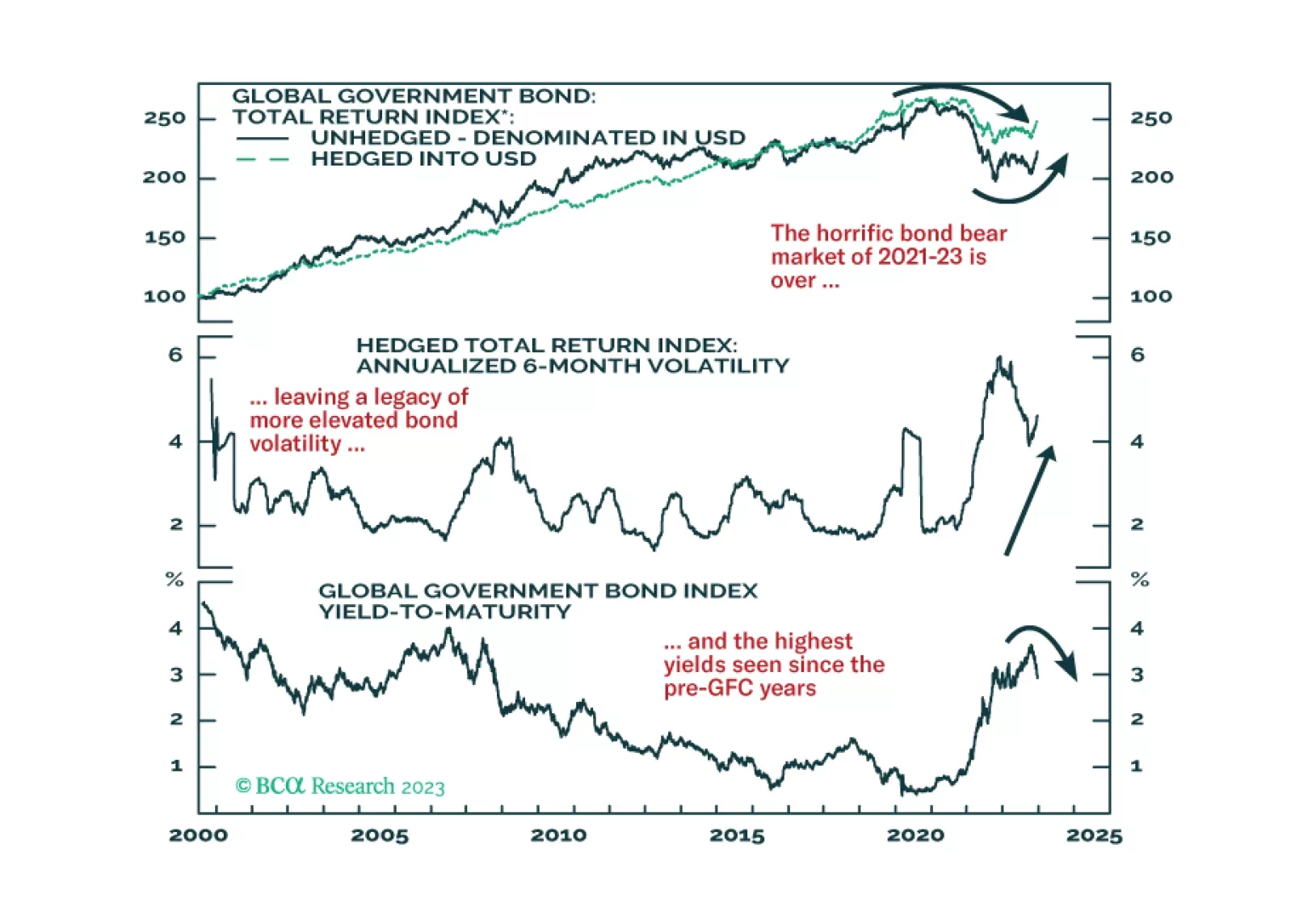

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

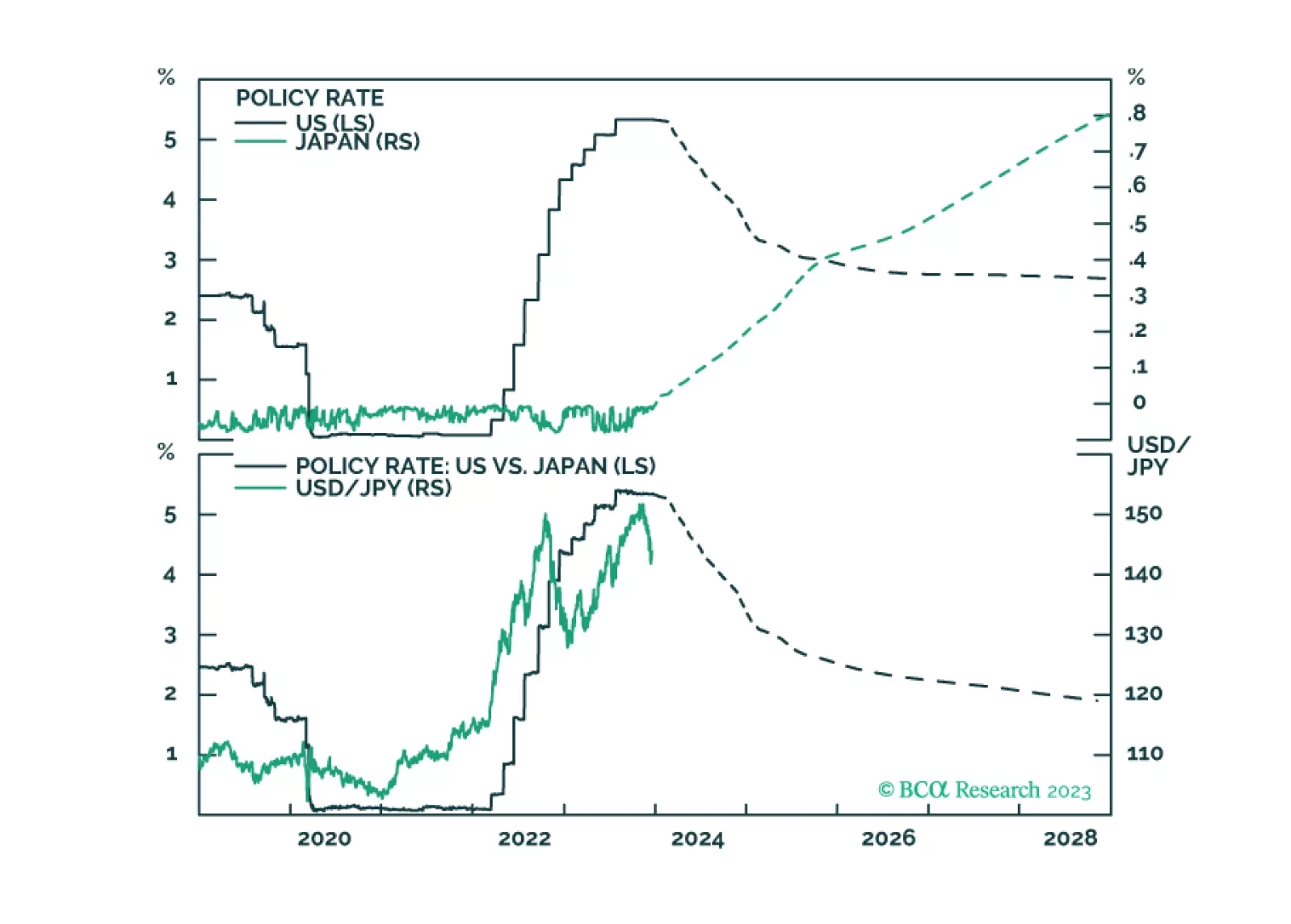

A post-mortem of our trades for the year, and also comments on future yen and sterling moves from the recent BoJ meeting, and the UK inflation report.

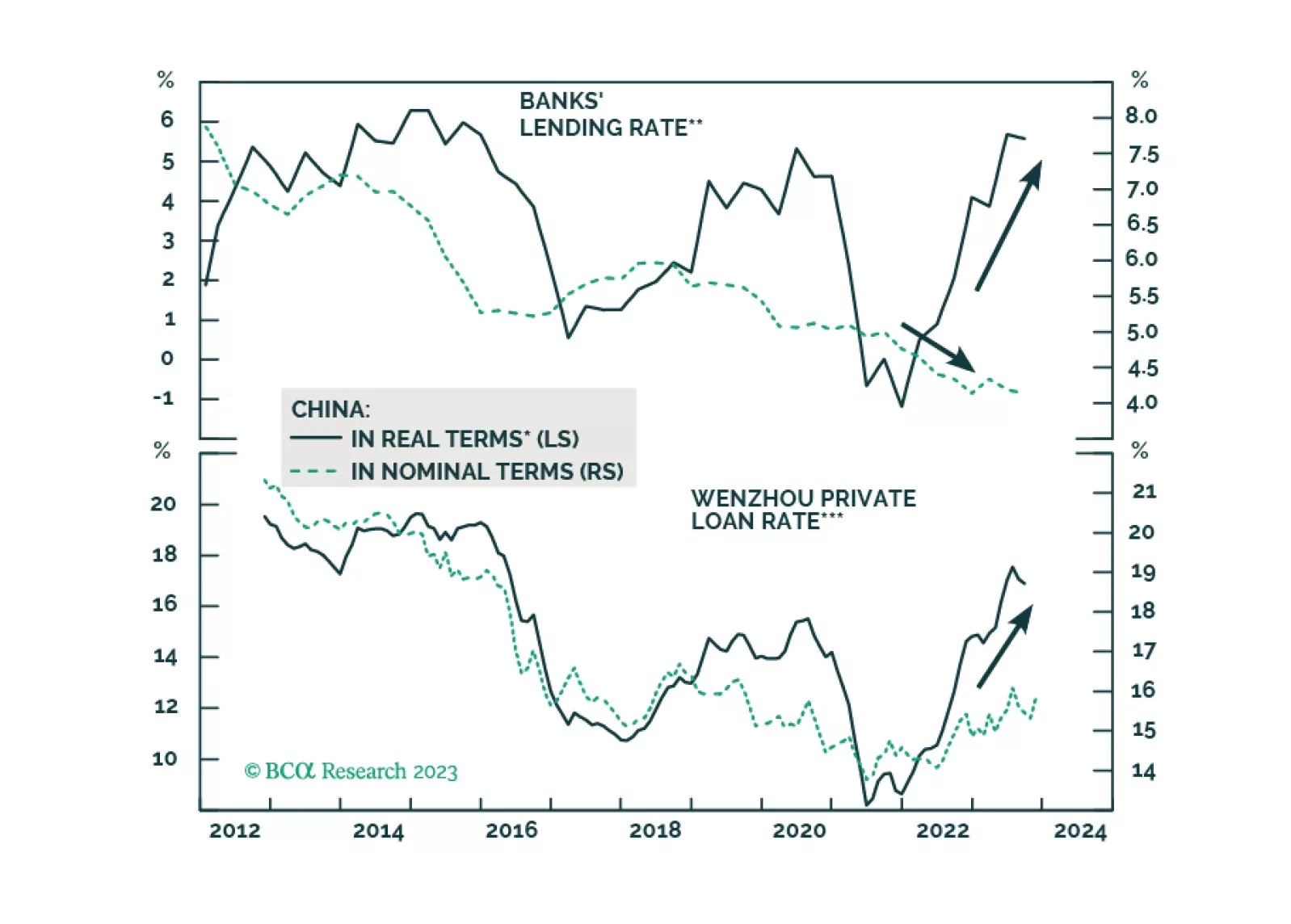

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

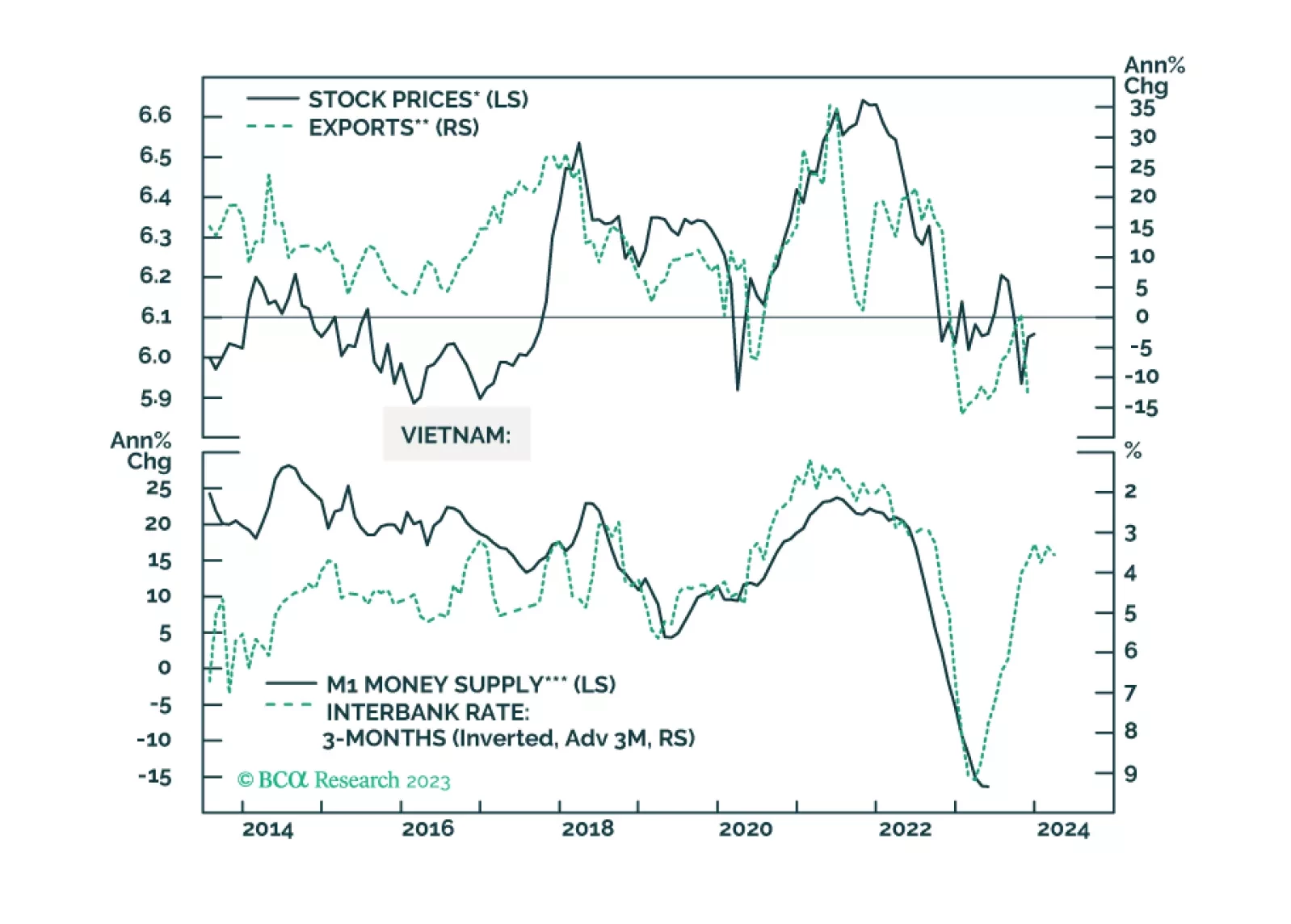

Vietnamese stocks may not see an immediate rally as global manufacturing and exports remain weak. But investors with longer-term horizons should stay overweight this market.

Our last publication of 2023 is an illustrated guide to our view that the economy will enter a recession around midyear. We expect equities will underperform Treasuries and cash over much of 2024, but we are waiting to turn tactically defensive until more investors are drawn into the soft-landing camp, capping the equity rally.