Financial Markets

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.

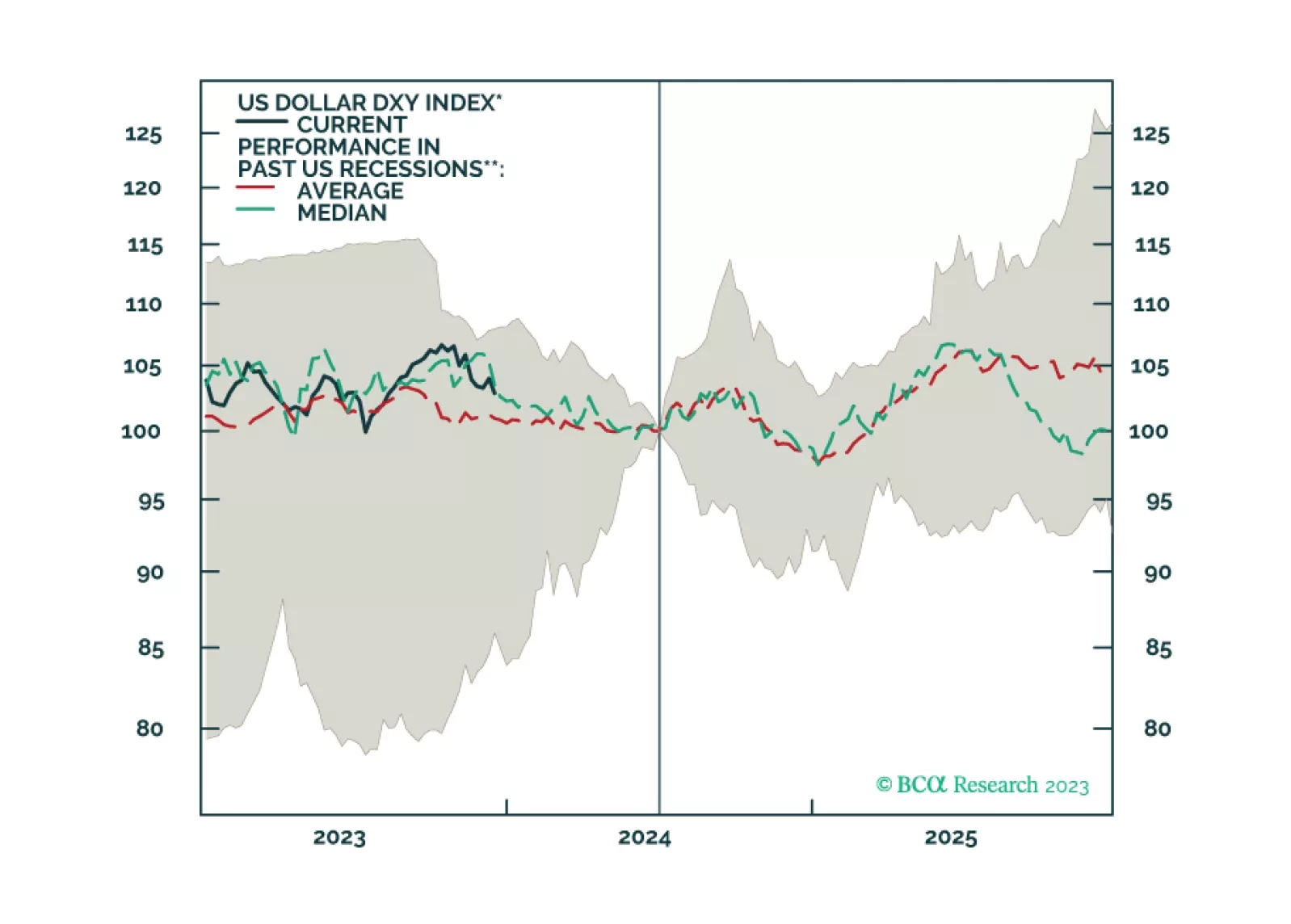

In this week’s report, we present our dollar view for 2024 and beyond, with a few trade ideas.

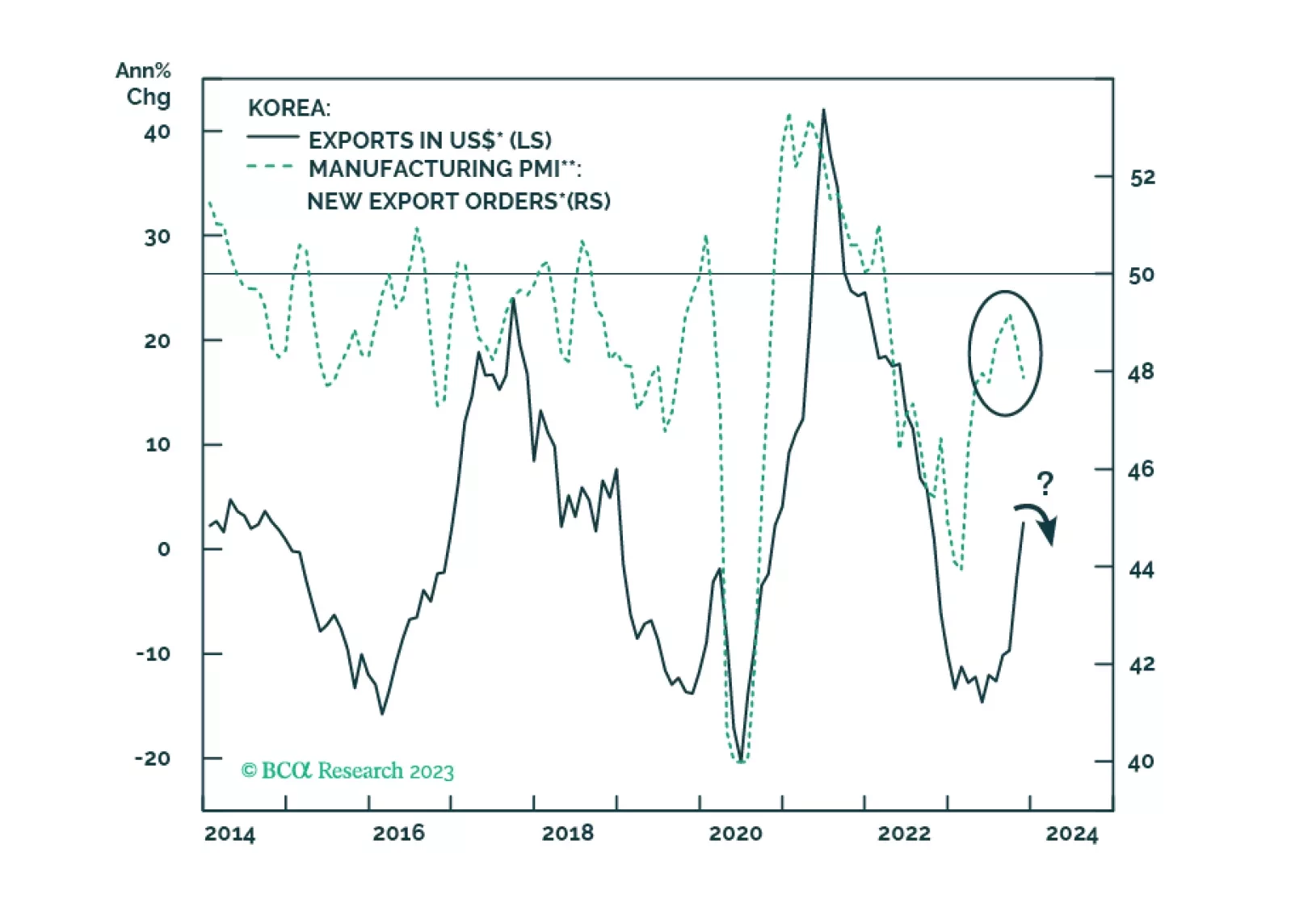

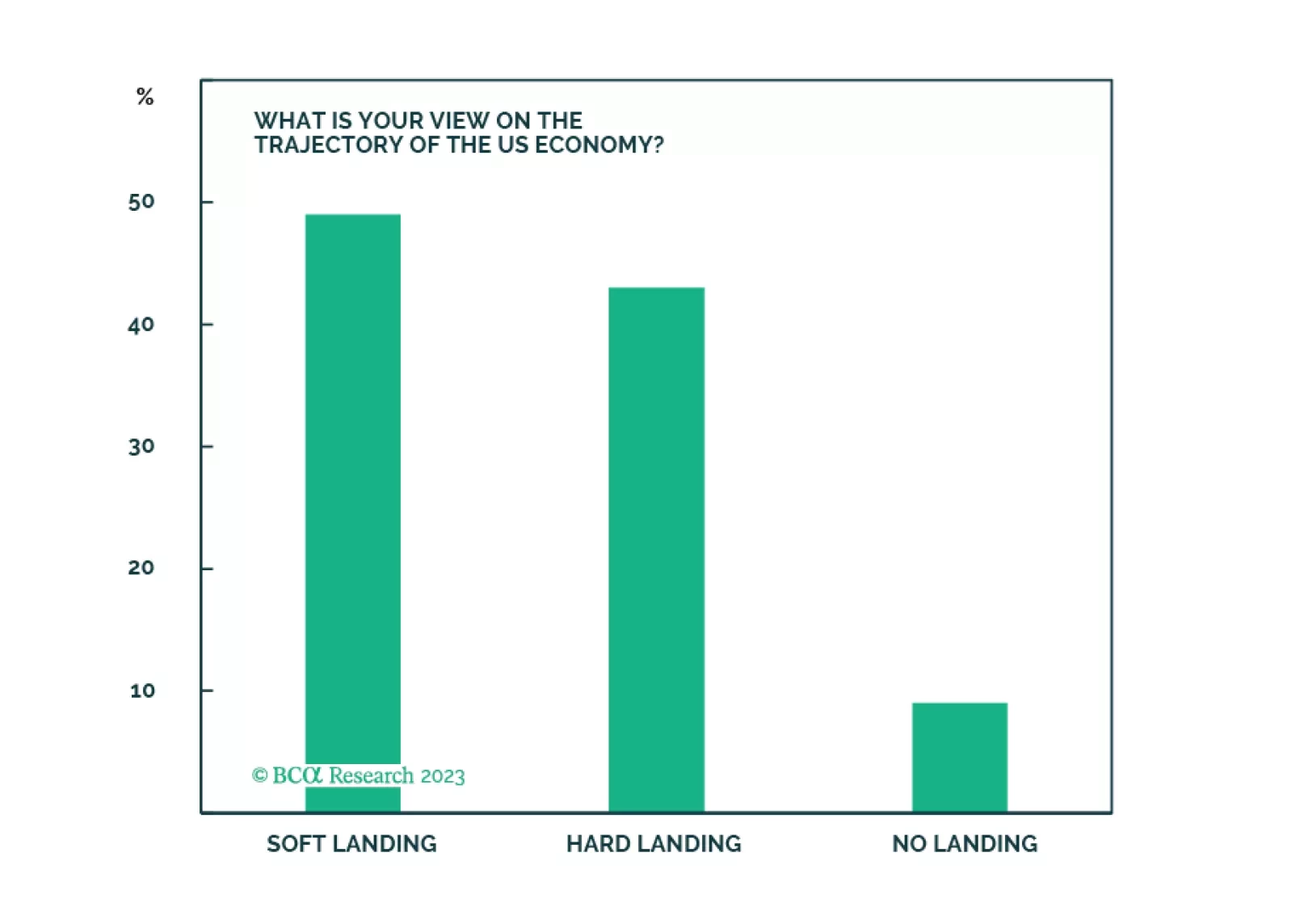

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

The Santa Claus rally is a repricing of the "soft landing" scenario as a likely economic outcome. Yet, many investors remain cautious, and harbor significant cash balances. Next year, repricing of various scenarios will continue, and volatility will be elevated. We remain in a "hard landing" camp and recommend defensive stance on a strategic investment horizon.

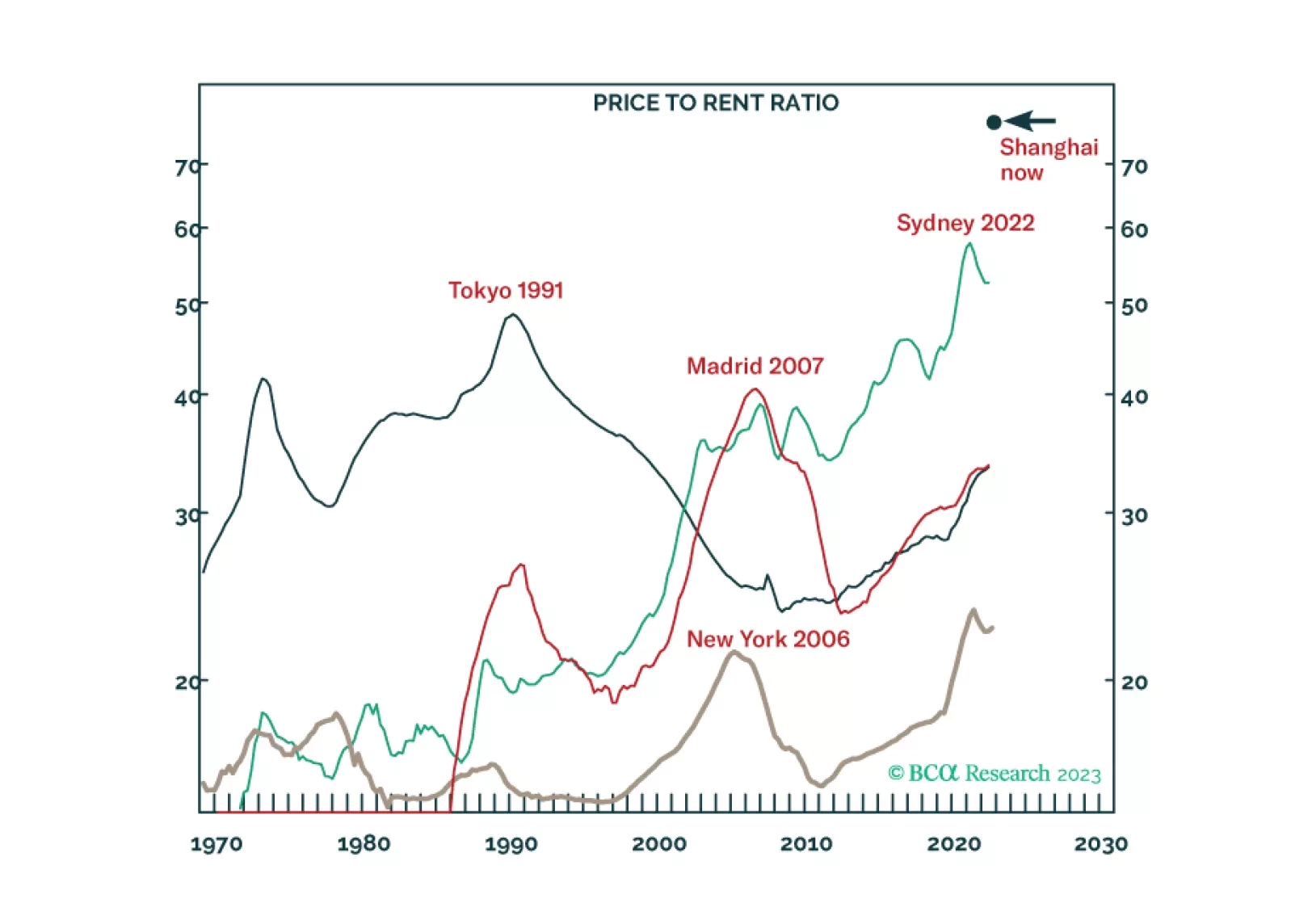

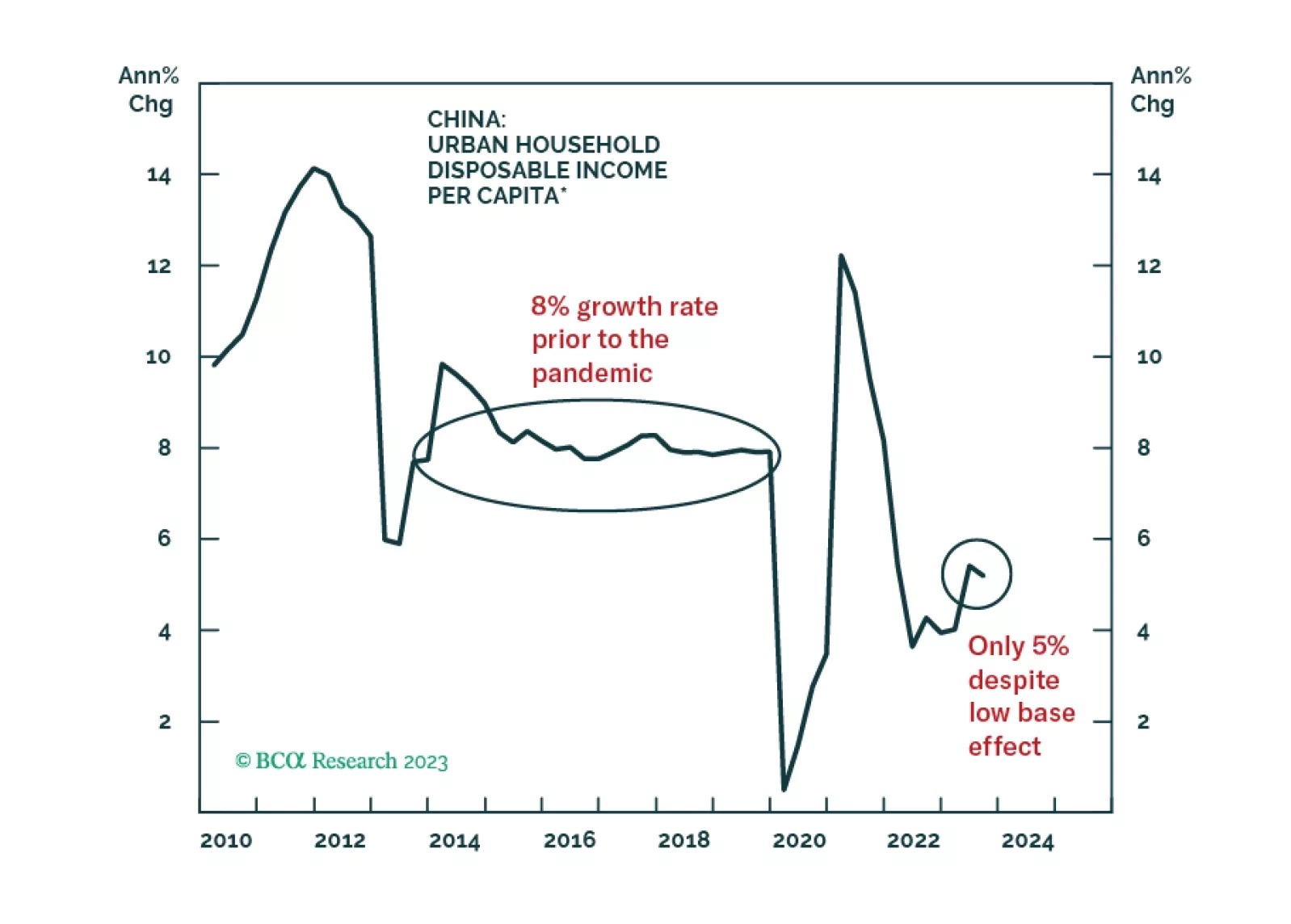

The overarching macro theme for China in 2024 will be deflation and its impact on the economy, macro policies, and financial markets. Widespread deflation, in combination with high debt levels and falling real estate prices, has unleashed debt deflation and balance sheet recession dynamics. The latter are rendering monetary policy inefficient.

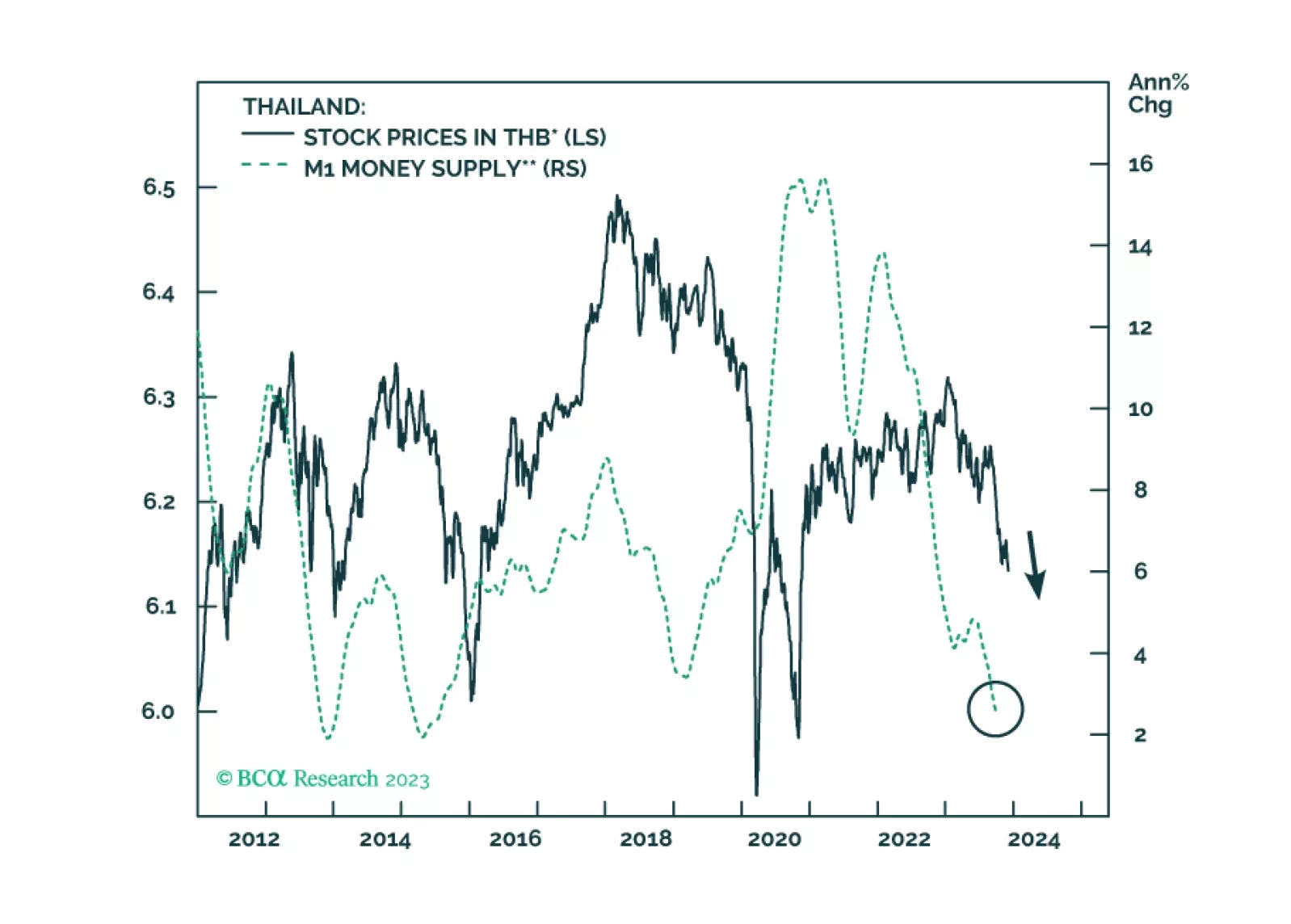

Meager credit growth and shrinking real wages will keep Thai inflation very low in the coming months. The currency will get support from an improving current account surplus. Fixed-income investors should upgrade Thailand from neutral to overweight within EM domestic bond portfolios.

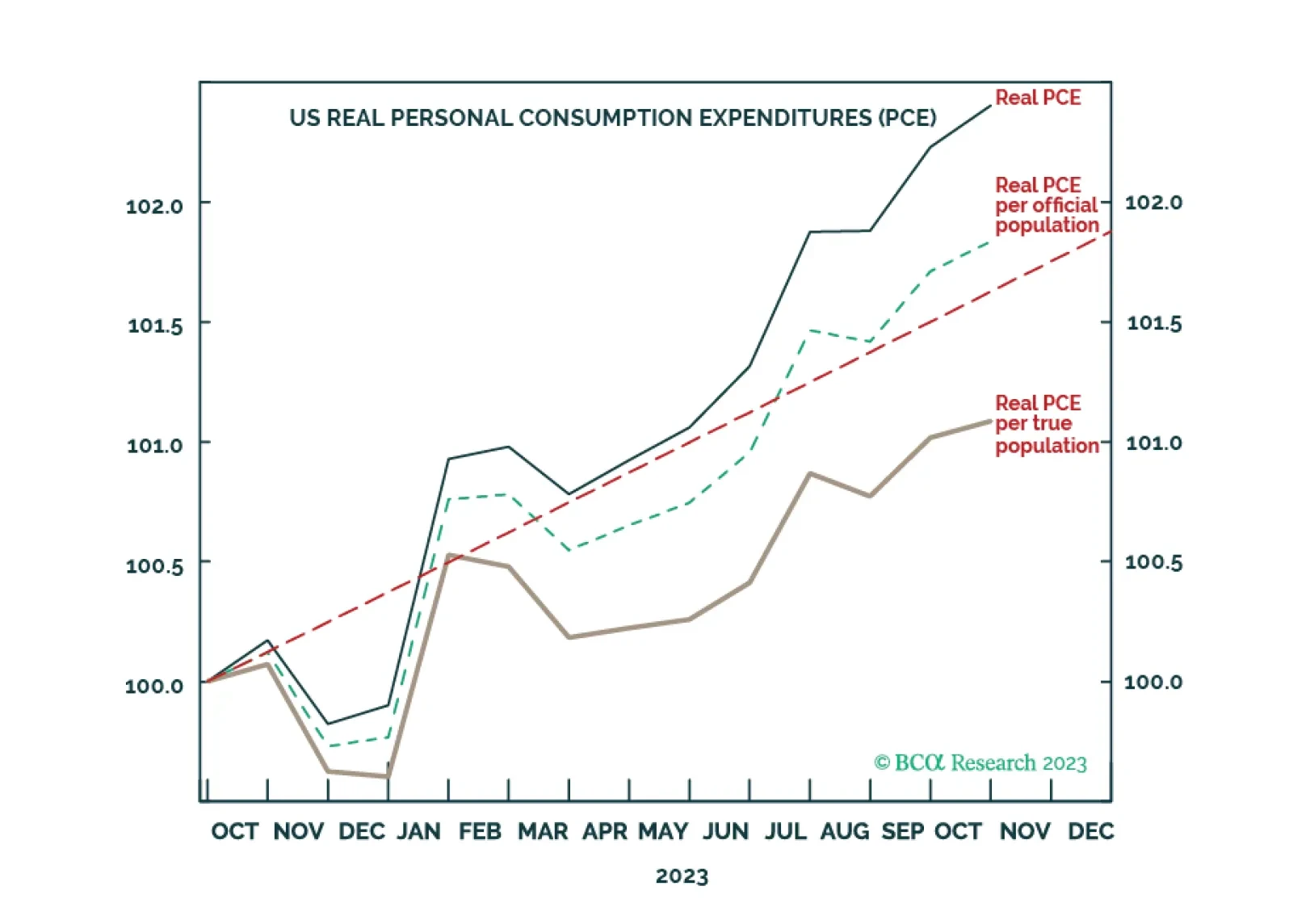

Illegal immigration into the US has skyrocketed to record levels. Correctly accounting for this, US real consumption growth on a per head basis is already fragile. Meanwhile, the real bond yield is only now approaching the pain point that typically triggers a recession. Ahead of the upcoming US jobs report, we point out what it would take for the Joshi rule real-time US recession indicator to breach its event horizon. And how to position in stocks and bonds, both tactically and cyclically. Plus: potential turning points in Biotech and Genome, ADBE, and Taiwan versus China.