Financial Markets

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

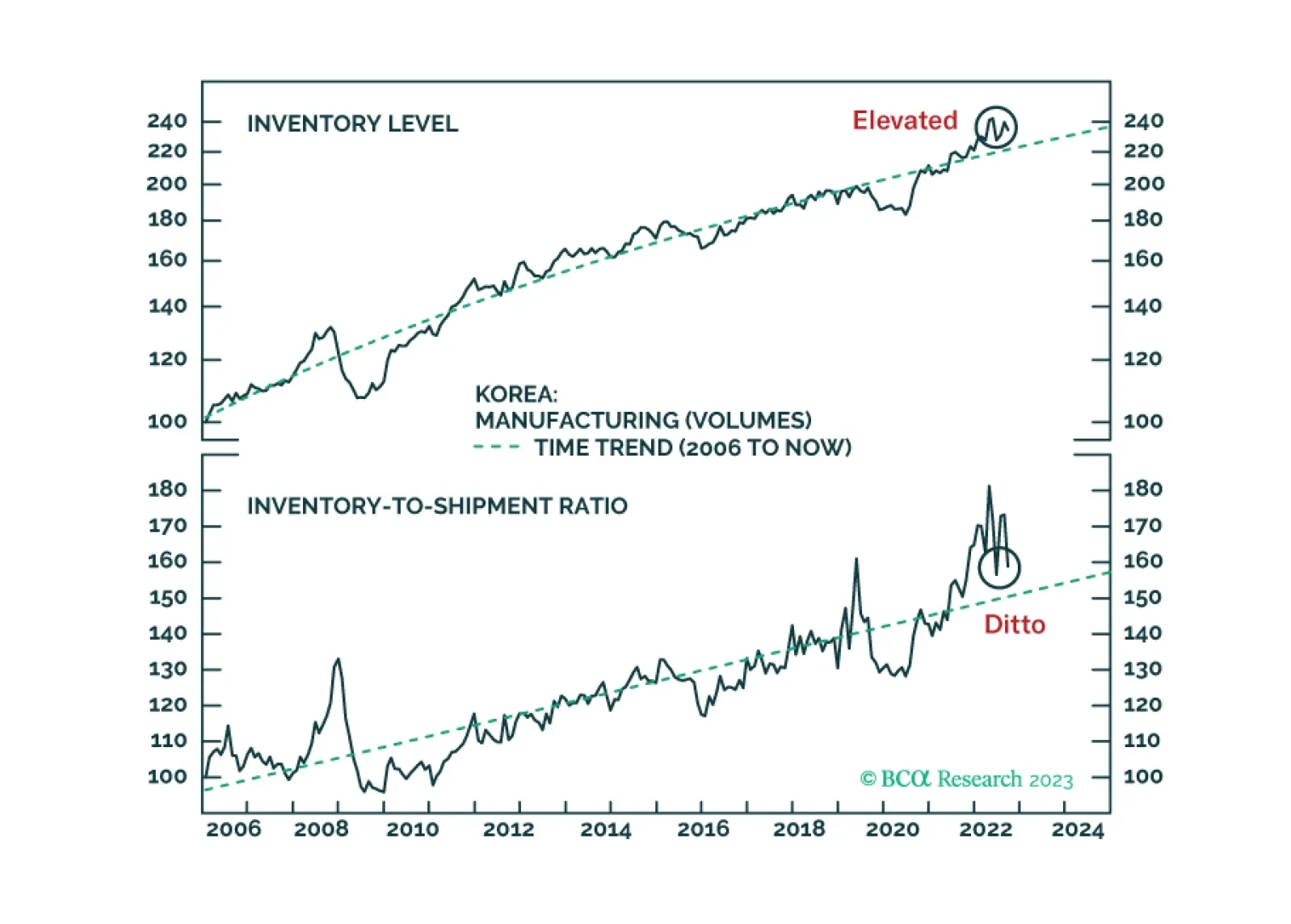

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

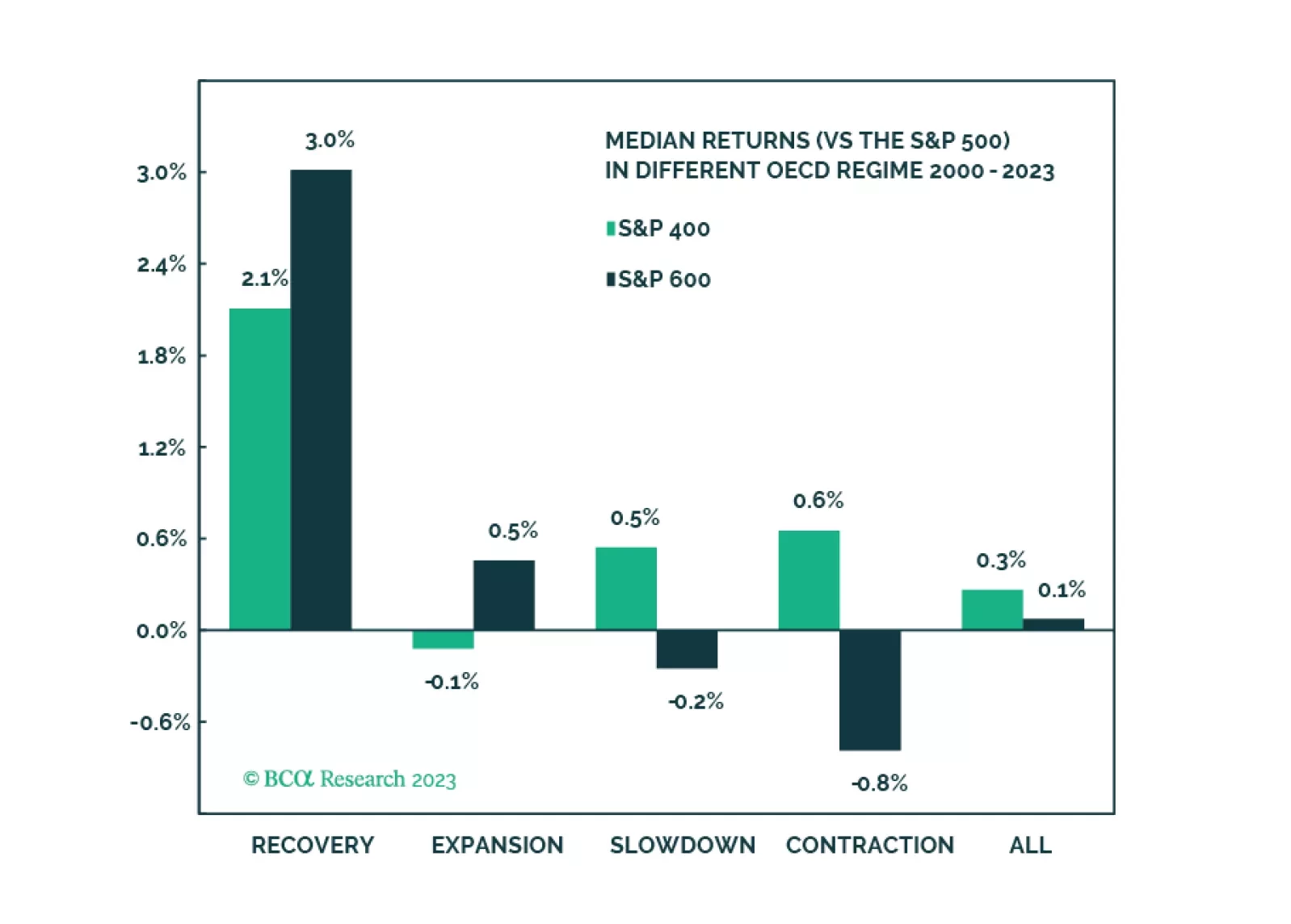

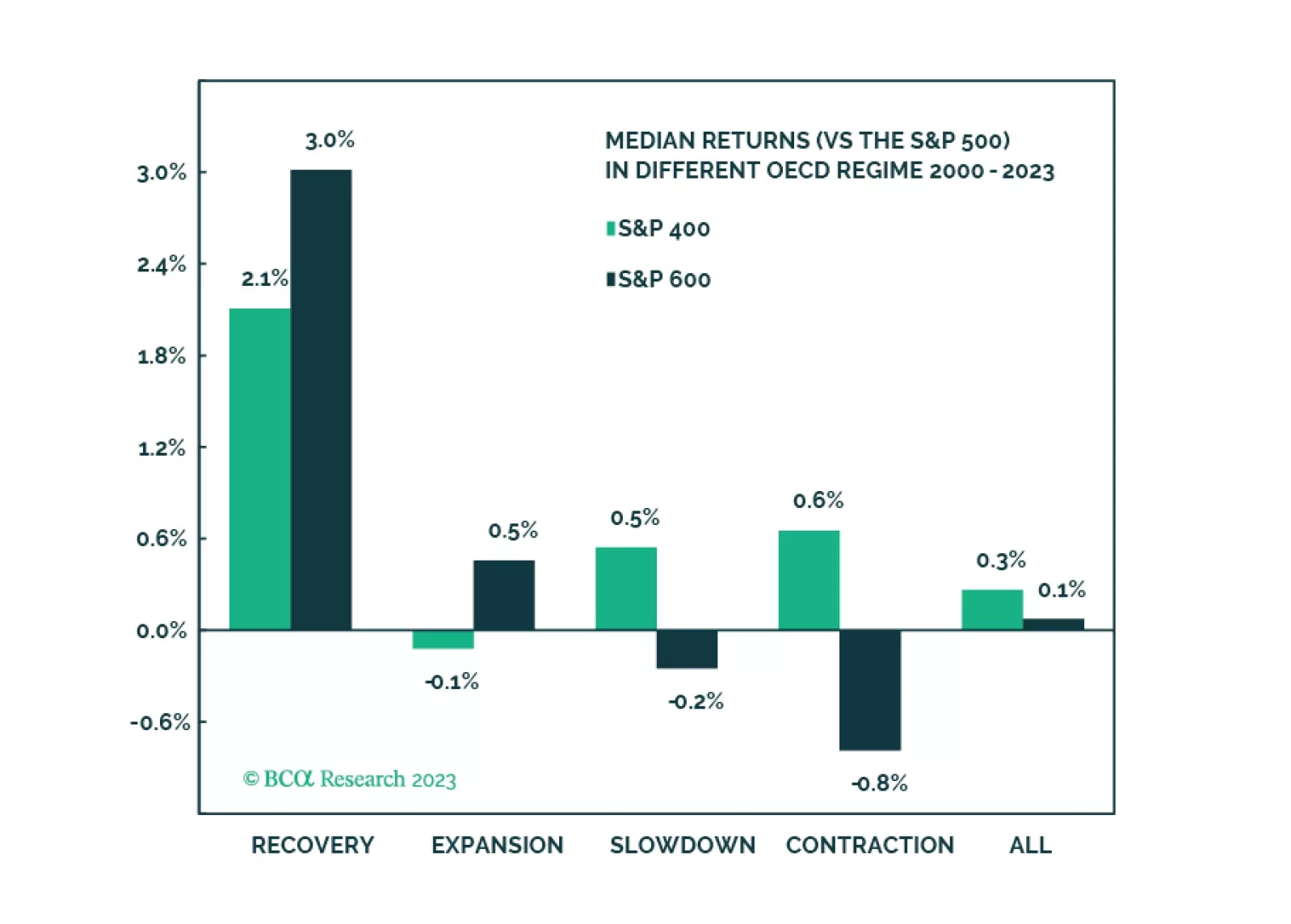

Mid-caps are the best of both worlds and are an excellent strategic overweight thanks to their size premium, but also better financial quality and higher dividend yield than Small. We are bullish on Mid near term and believe that this may be a great trade. We will initiate a position in the S&P 400 as a tactical overweight but will monitor it very closely.

Mid-caps are the best of both worlds and are an excellent strategic overweight thanks to their size premium, but also better financial quality and higher dividend yield than Small. We are bullish on Mid near term and believe that this may be a great trade. We will initiate a position in the S&P 400 as a tactical overweight but will monitor it very closely.

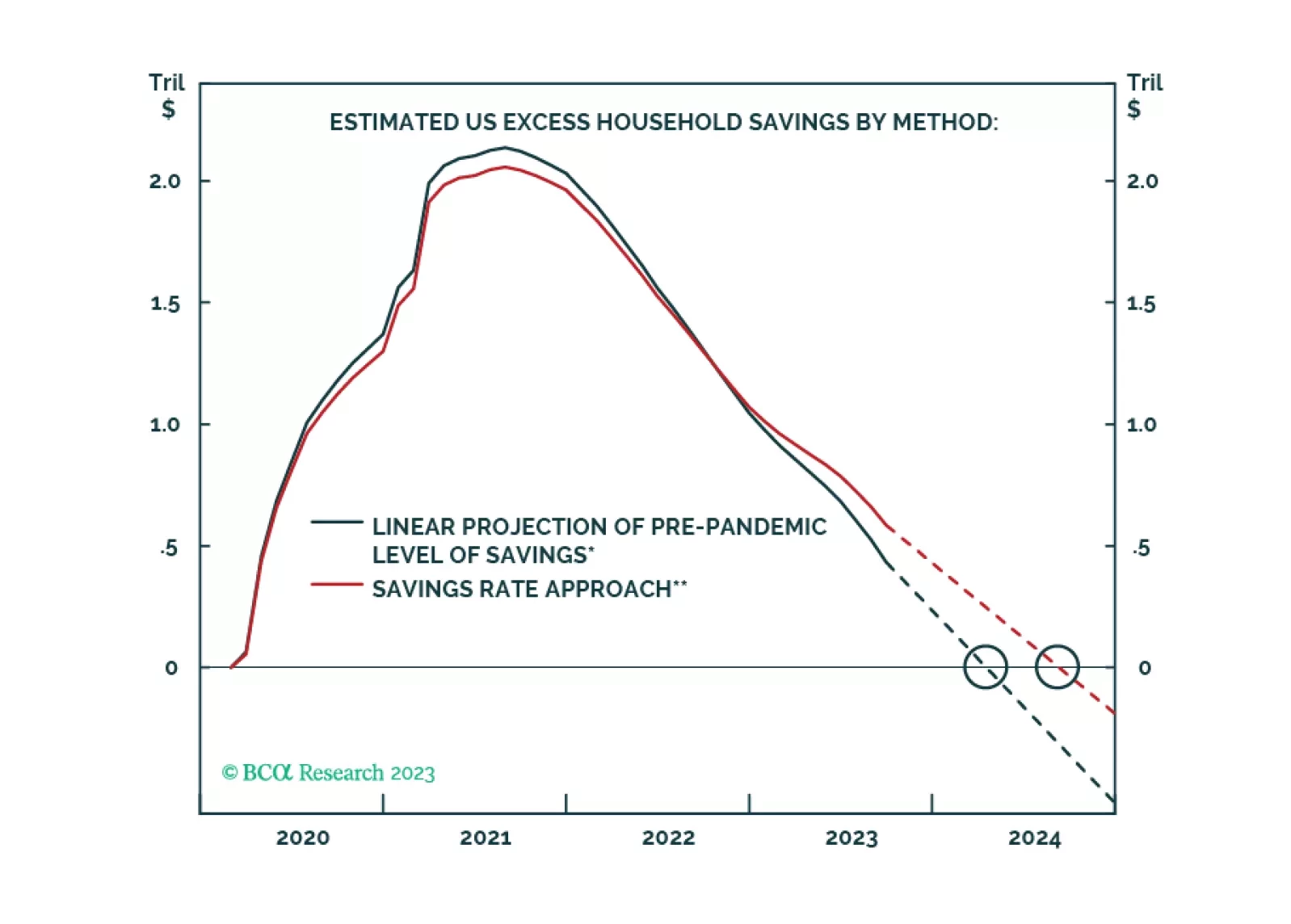

The soft-landing narrative has gotten nowhere at BCA but appears to be making some headway with broker-dealers and investors. We are preparing to lean against it once it pushes equity prices a little higher.