Financial Markets

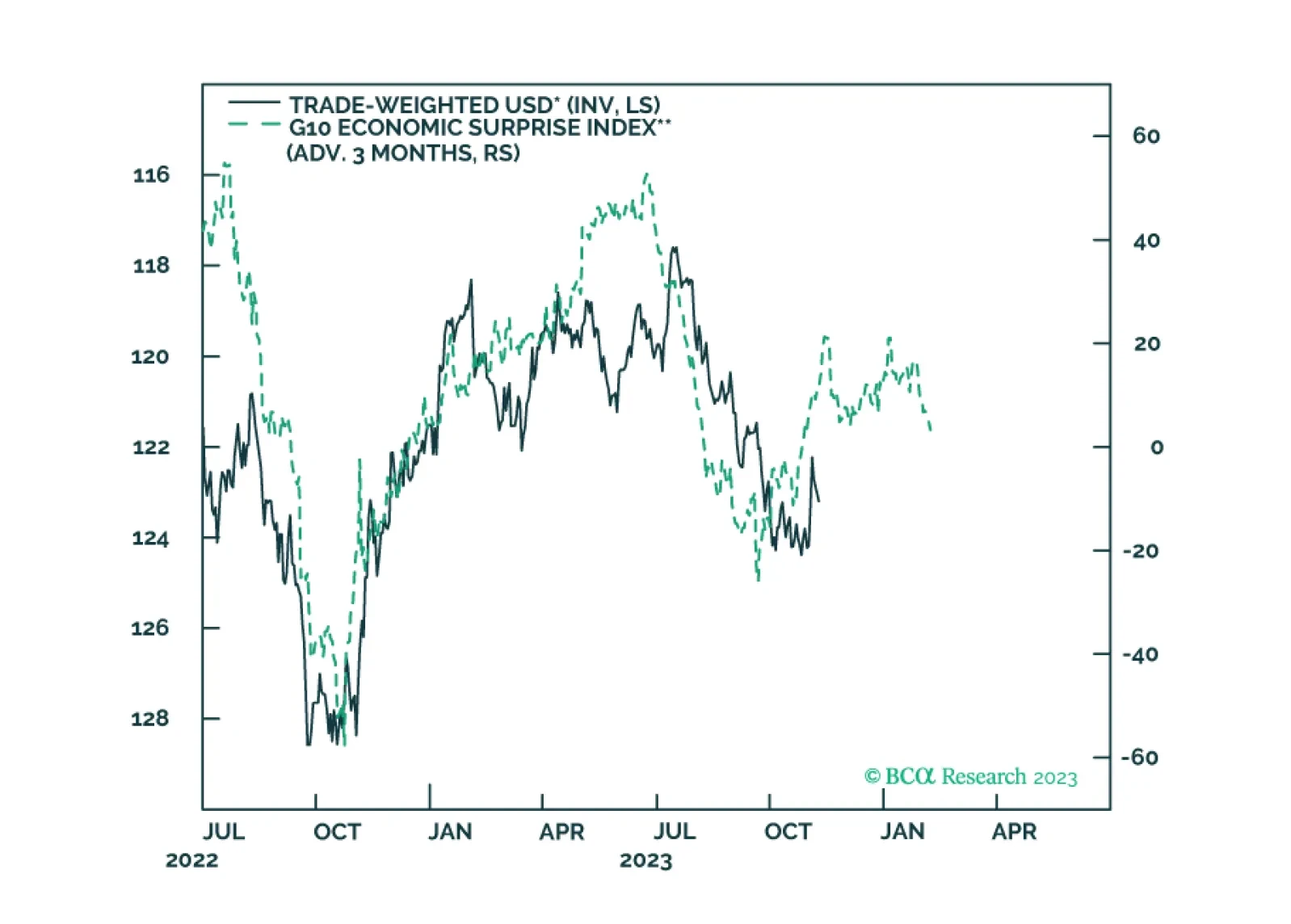

In this report, we go around the globe and survey the near-term outlook for G10 currencies. Our longer-term view on the dollar has been clear, we are sellers. In this report, we review if a tactical sell is also warranted given incoming data and the message from our models.

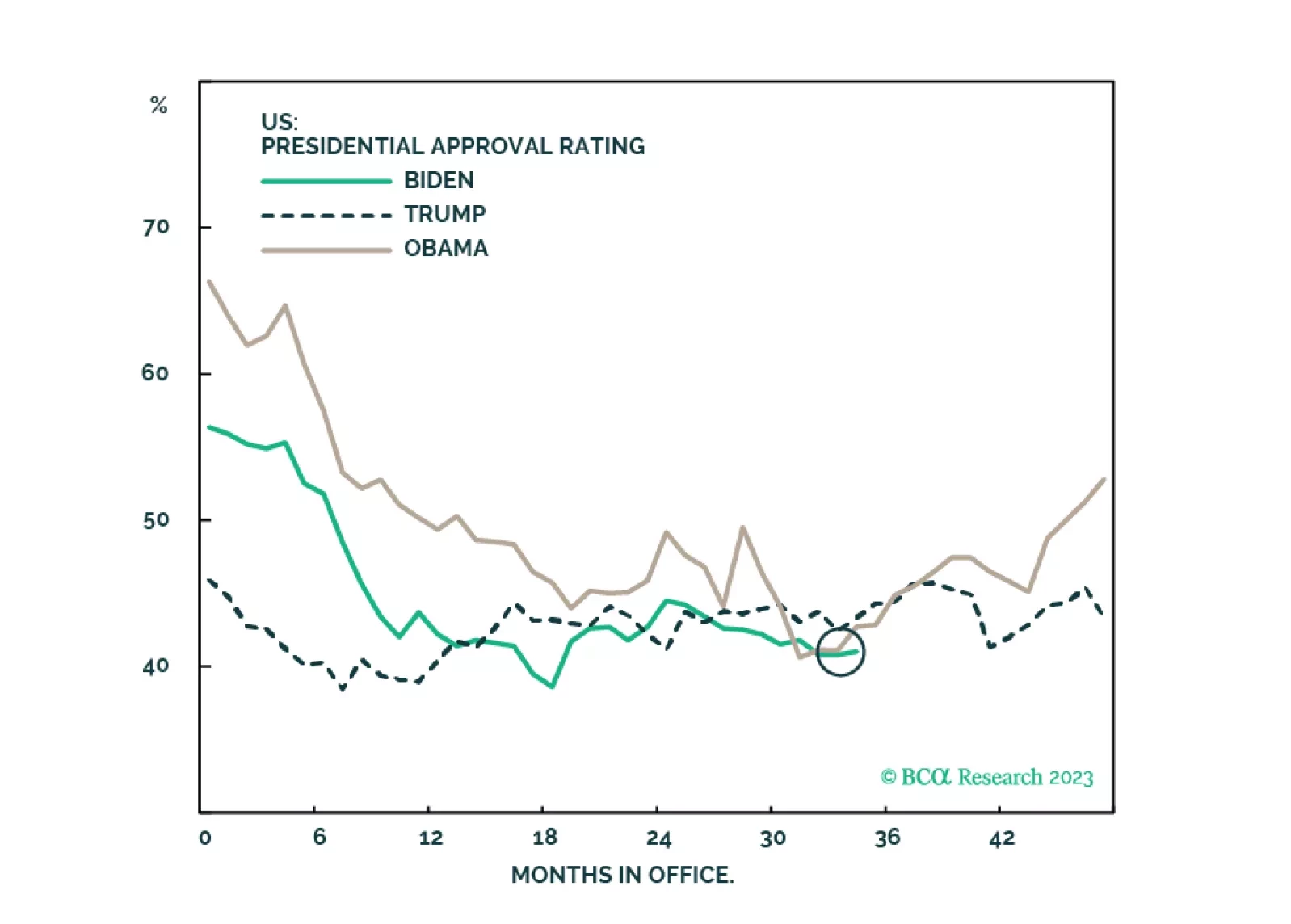

Results from Tuesday’s elections suggest that the Democrats are doing better than what their 2024 polling are showing. While the results are marginally positive for equities, investors should not overrate this off-year election, especially considering the slowing economy and the many foreign challenges facing the US.

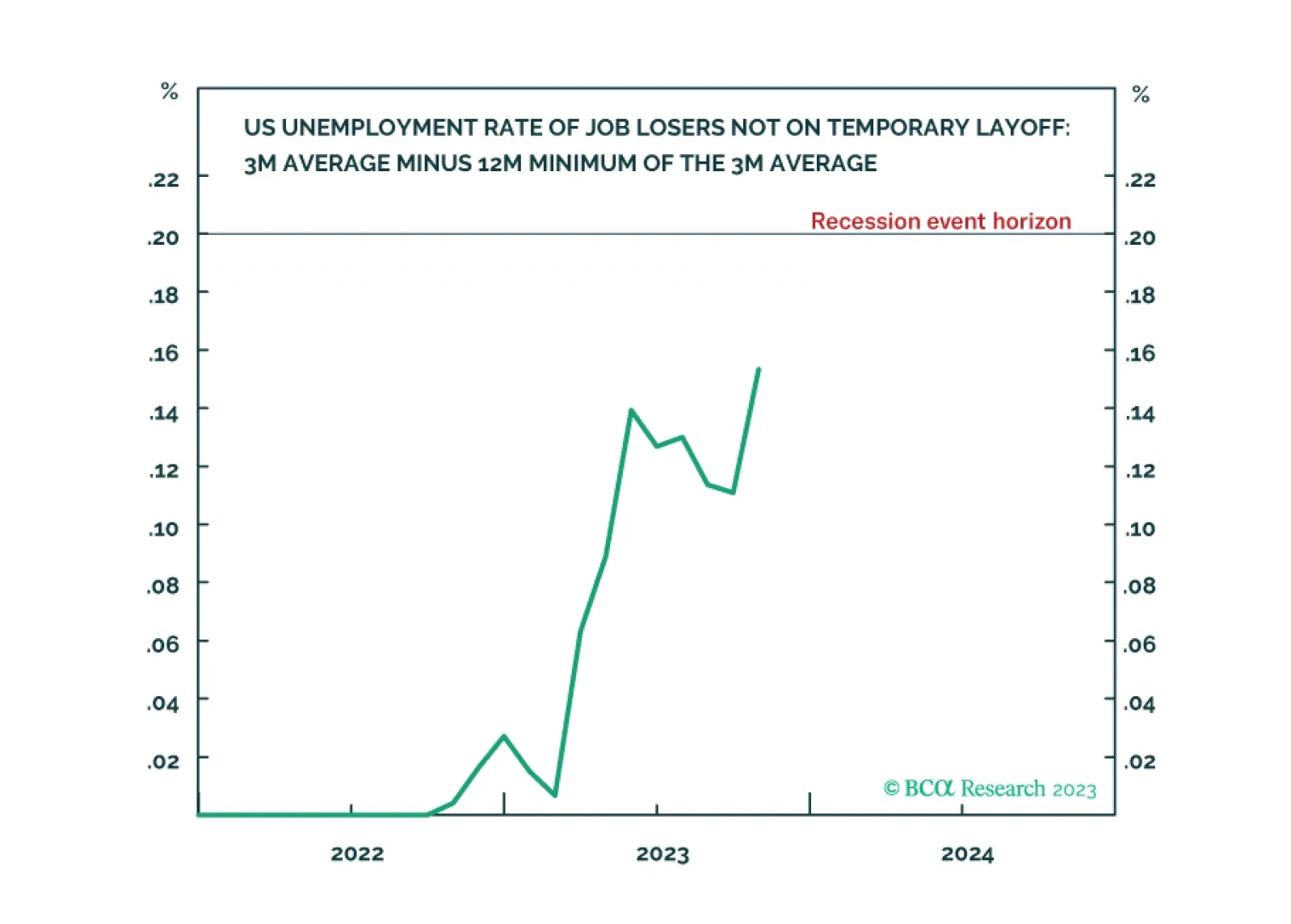

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.

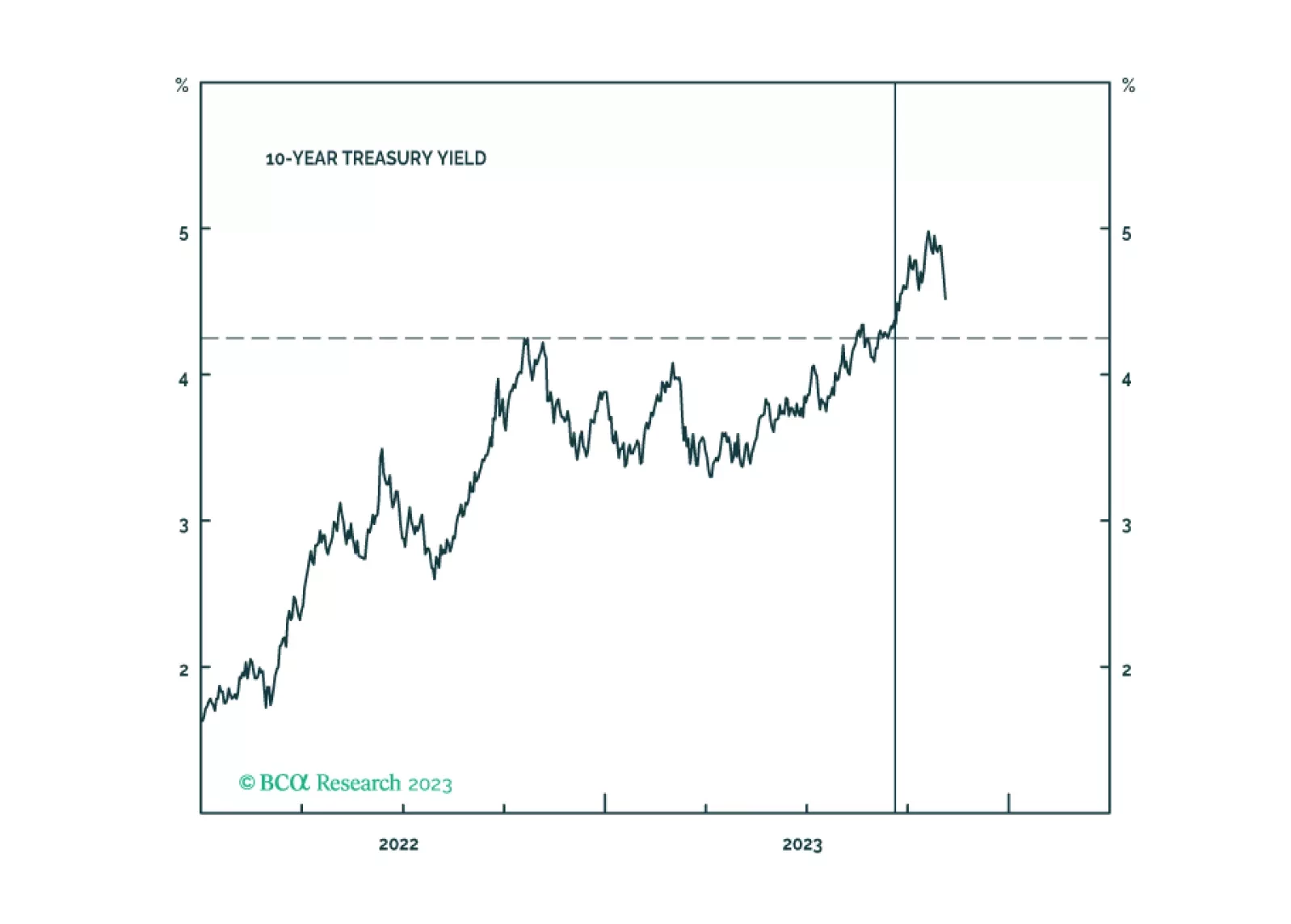

We consider several uncertainties in this week’s report, from the interest rate outlook to the source of the mountain of cash households have amassed since the pandemic began. We have not adjusted our tactical asset-allocation recommendations but will do so soon to align with the defensive cast of our cyclical recommendations.

Economic growth has little to no relationship with long-term country returns. But if GDP doesn’t drive long-term equity returns, then what does? To find out, we break down equity total returns of 33 countries from 1997 to 2022 into seven components. In line with other academic research, we find that, over our sample, net buybacks were a crucial factor for long-term country performance. Our research suggests that equity issuance is an underestimated driver of returns that investors should pay more attention to.