Financial Markets

In financial systems, cracks typically begin on the periphery and then expand to the center. Hence, the ruptures on the fringes often act as an early warning. These fissures tend to widen and spread to the core, causing a breakdown in the S&P 500. Investors should consider buying US Treasurys aggressively when the S&P 500 slips below 4,000.

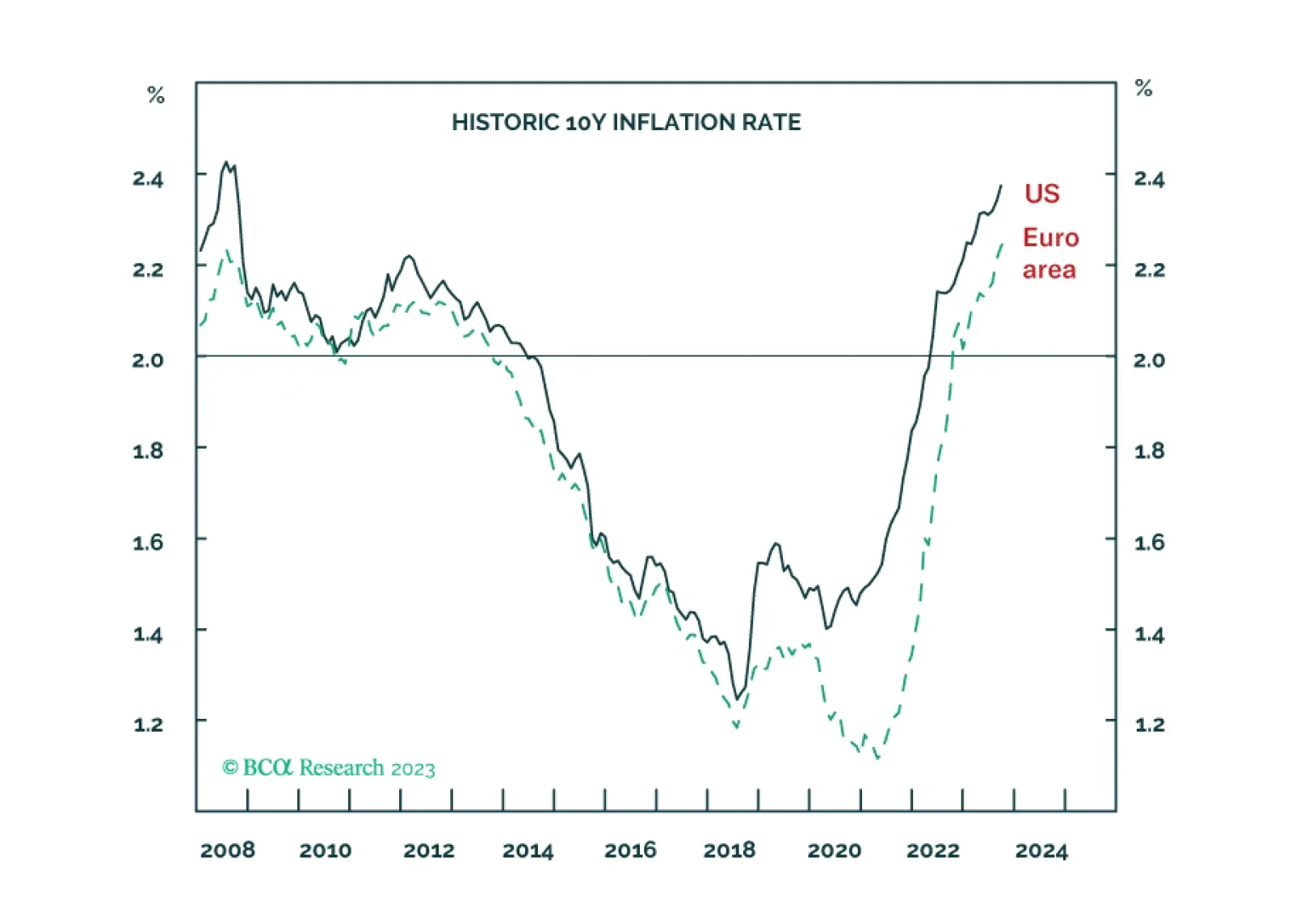

The fundamental component of long-term inflation expectations has climbed to its highest level since 2008 in both the US and the euro area. This means that both the Fed and the ECB will need to engineer inflation to undershoot 2 percent for an extended period if they are to maintain their 2 percent inflation targets. We explain what this means for investment strategy over the coming 6-12 months. Plus, we pinpoint what to focus on in this Friday’s US jobs report. And we identify food and beverages (PBJ) and the Indonesian rupiah (IDR/USD) as excellent rebound candidates.

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

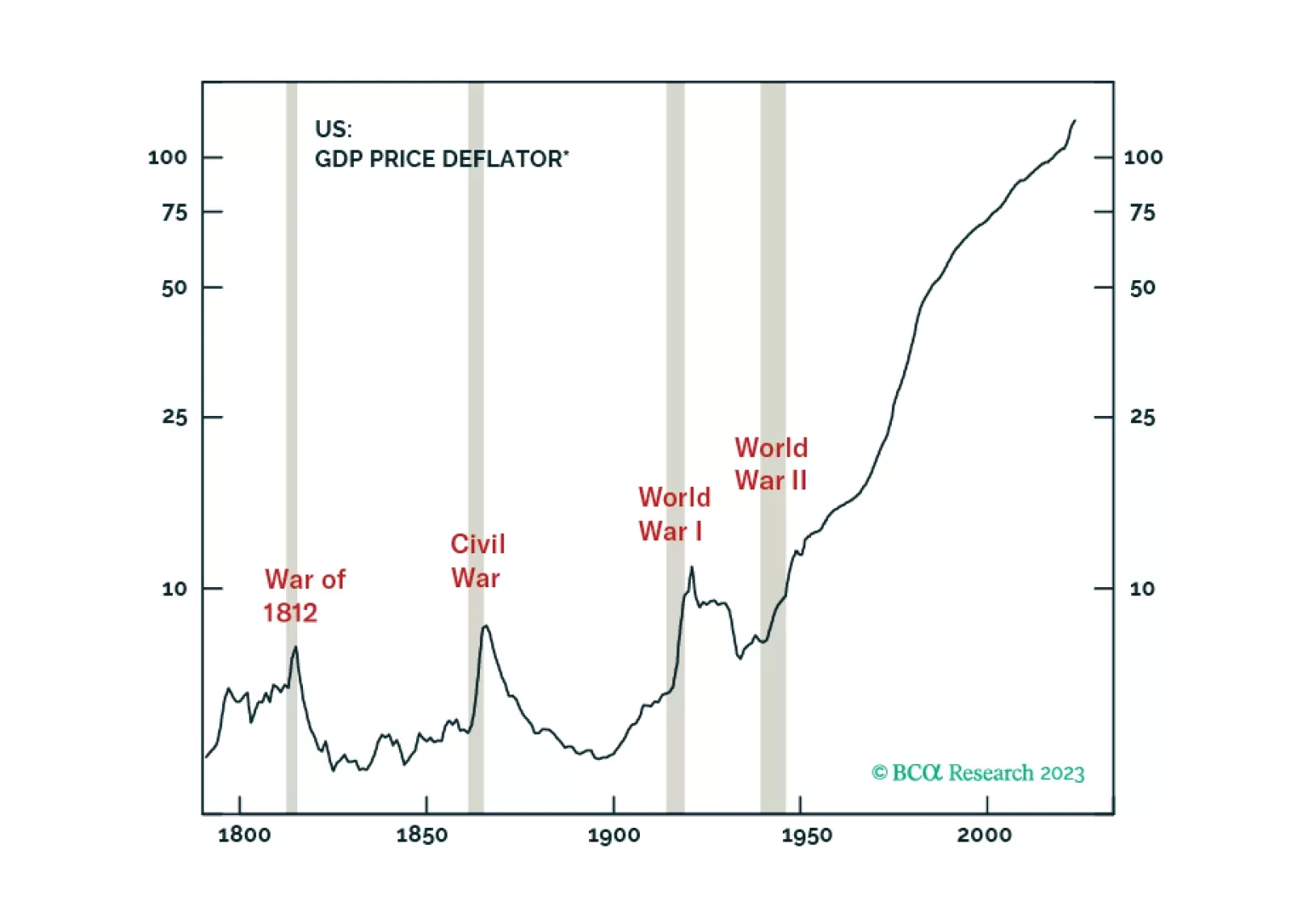

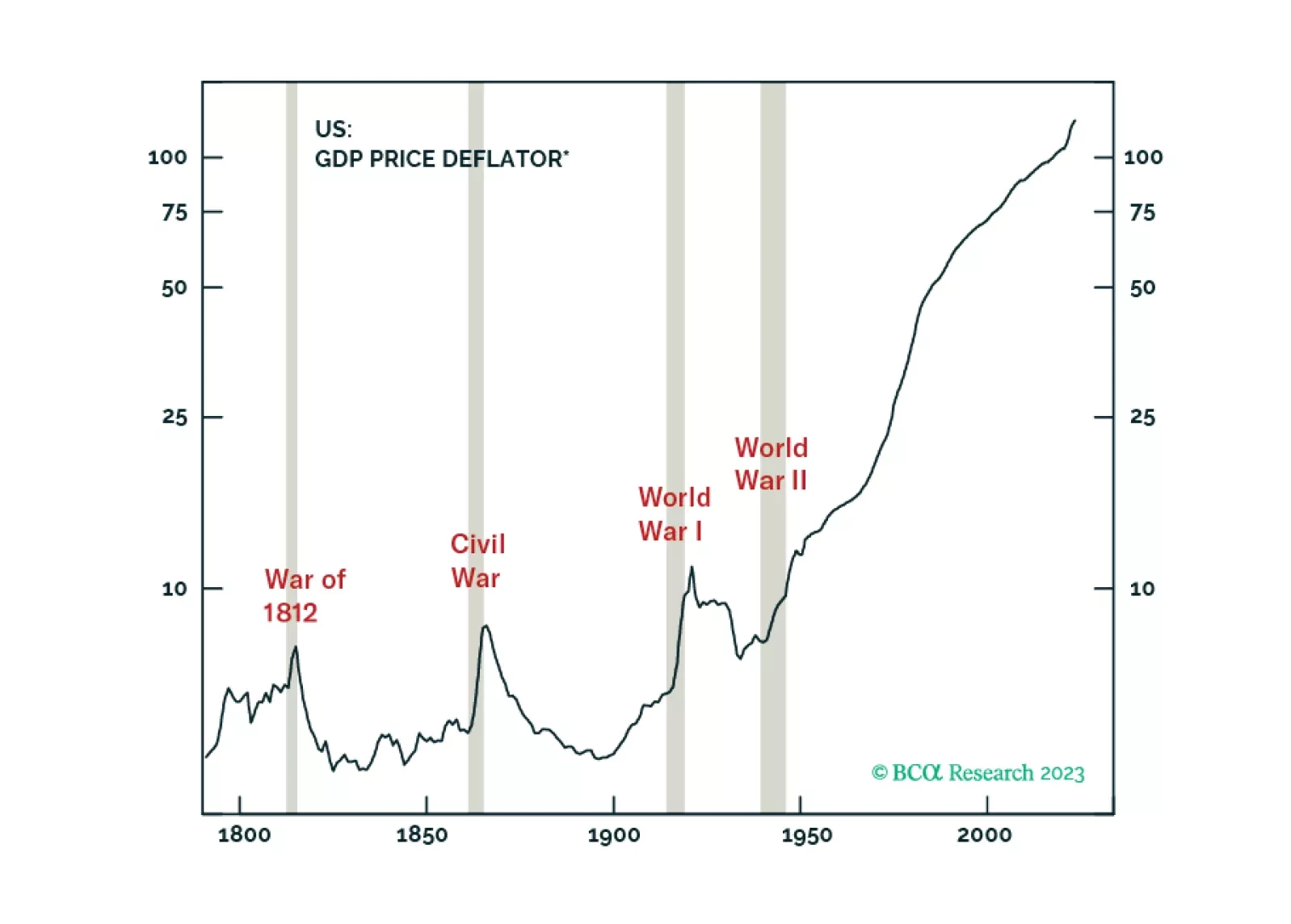

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

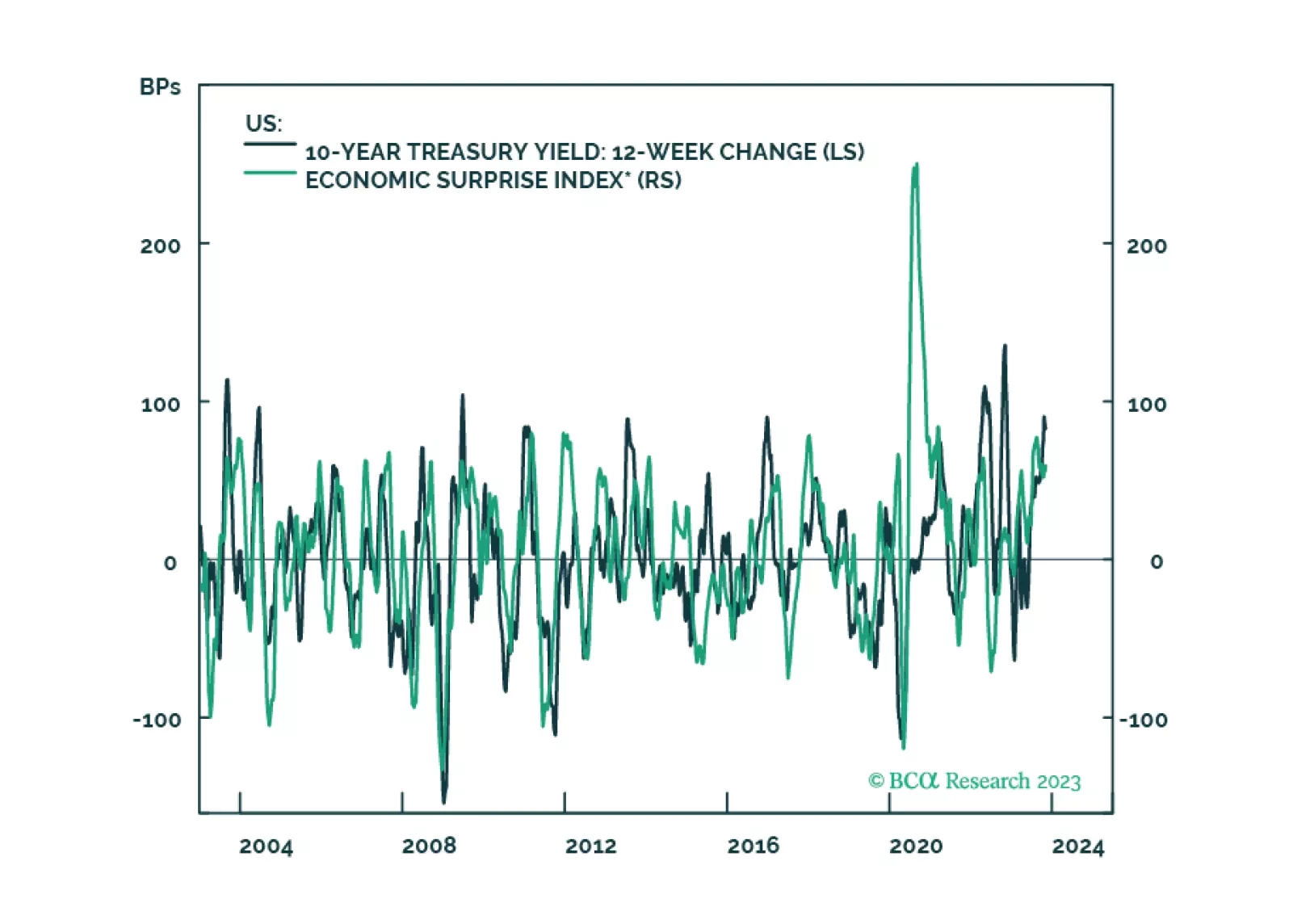

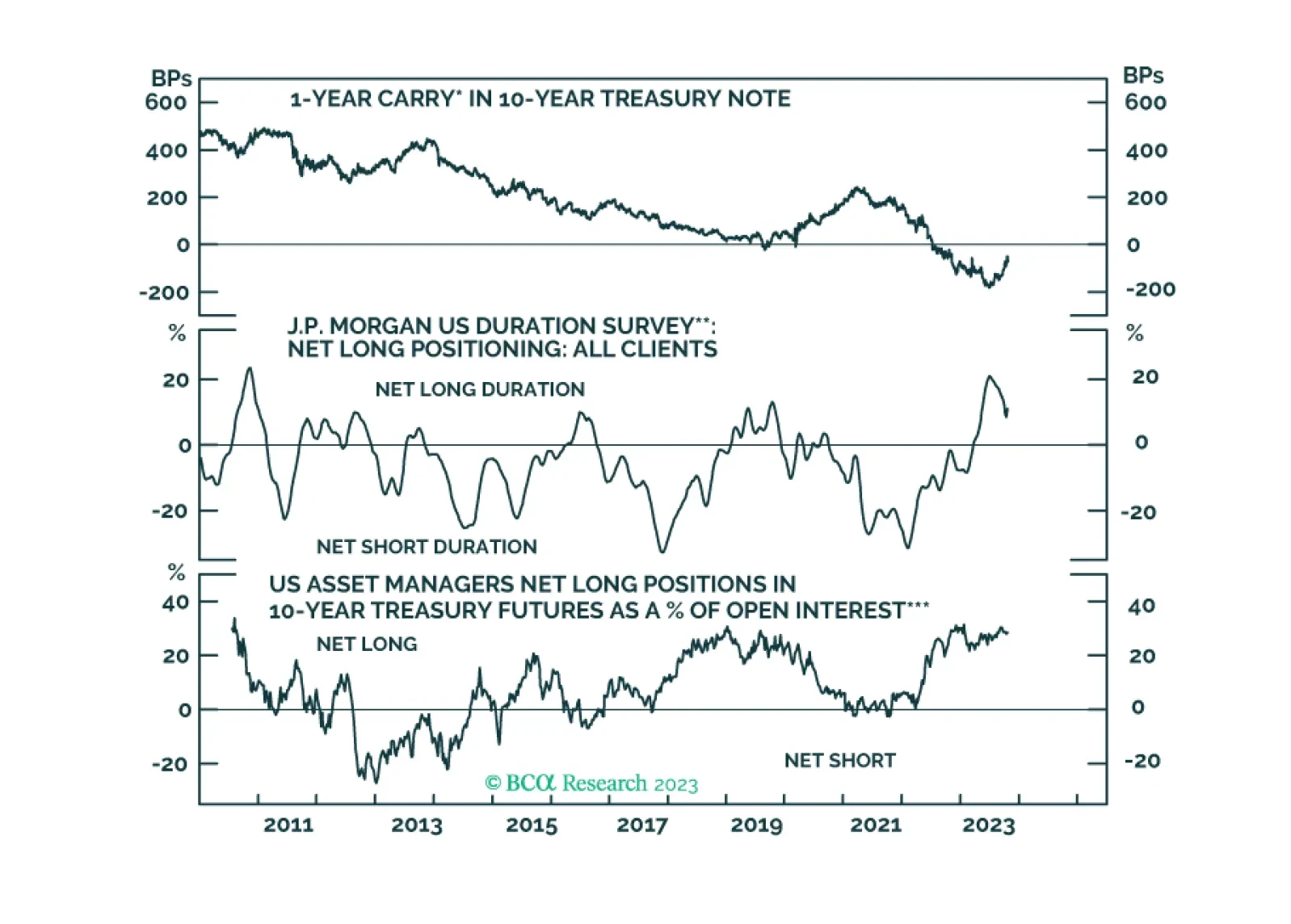

This week’s report contains an update on the Treasury curve’s recent bear-steepening trend and a look at different measures of long-maturity Treasury valuation.

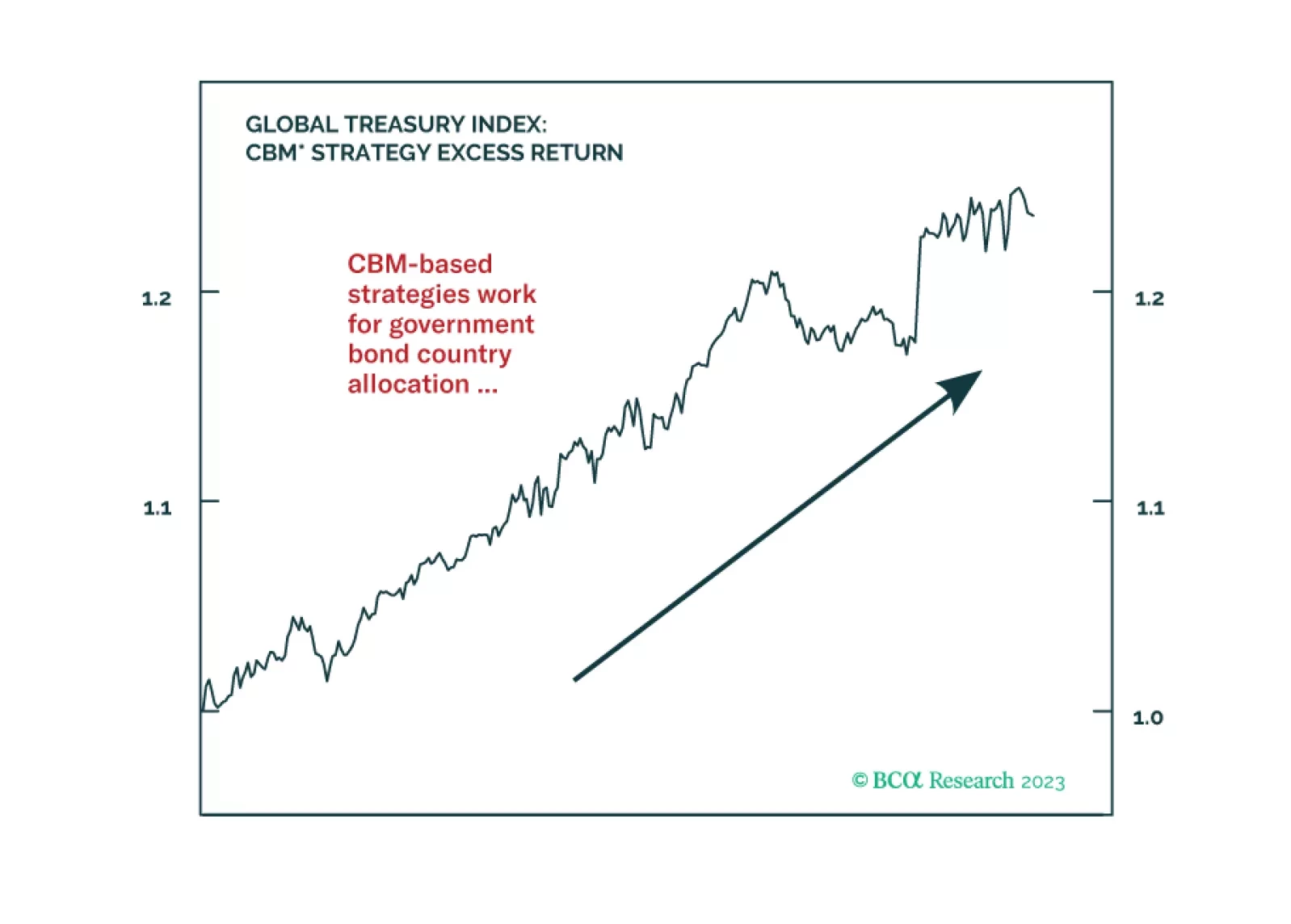

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.