Financial Markets

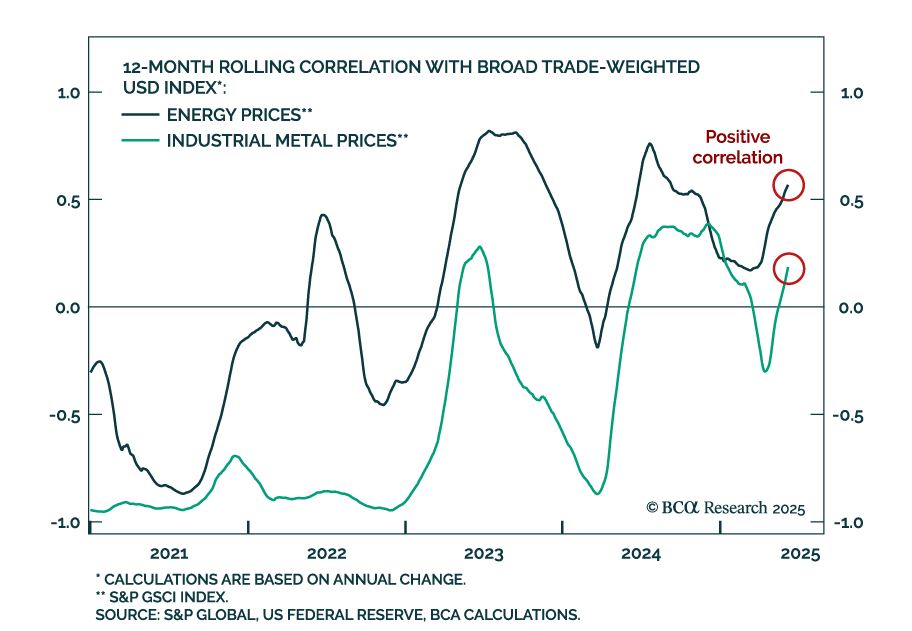

Our Commodity strategists see a breakdown of historical commodity correlations. The US dollar now shows a positive correlation with commodities, particularly energy, and a weaker dollar will no longer guarantee upside for commodity prices. Softening global…

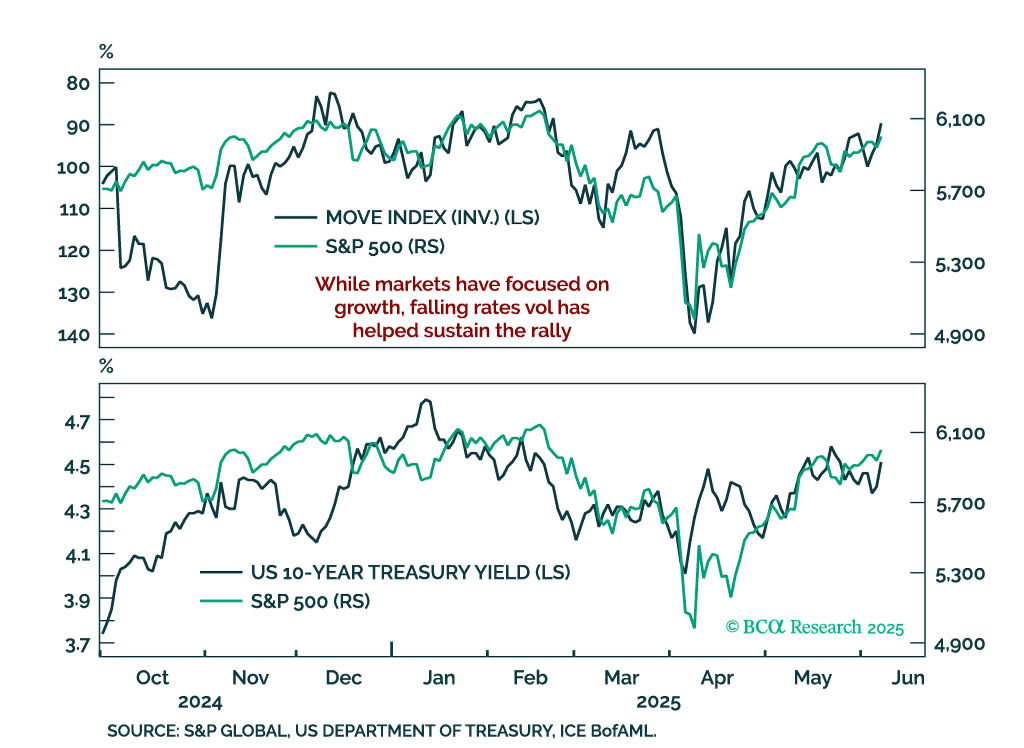

The equity rally faces two looming threats: Weakening growth expectations and a potential resurgence in rates volatility. Equities are vulnerable to any deterioration in growth sentiment. Economic surprises have turned lower and financial conditions are…

Our Counterpoint Strategists see no signs of recession or market fragility but remain skeptical of US superstar stocks. Winners of past tech cycles rarely lead the next, making Web 2.0 firms unlikely beneficiaries of the AI-driven rally. BCA’s Counterpoint…

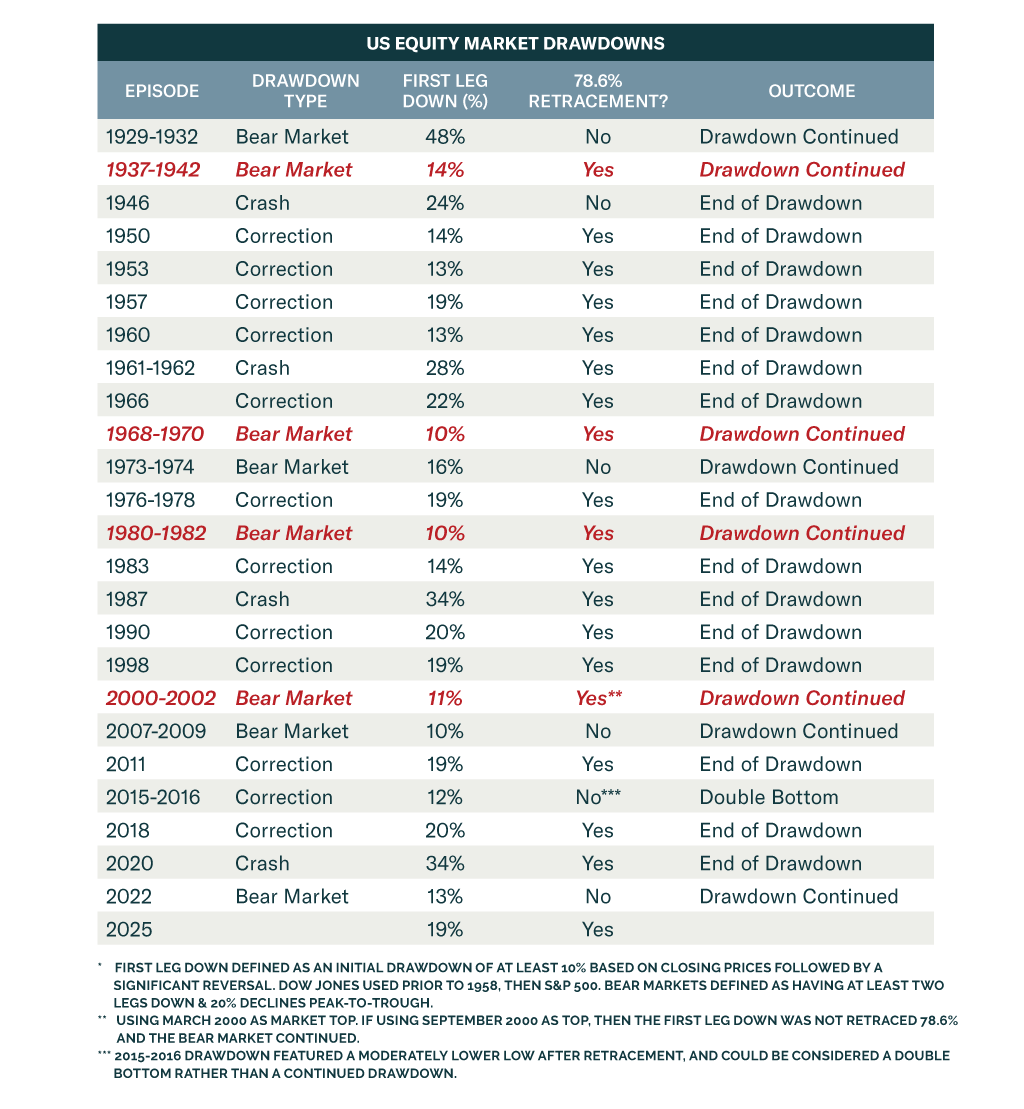

Despite a strong rebound in equities, we remain defensively positioned as recession risks persist and market history warns against premature optimism. The S&P 500 has retraced 78.6% of its initial drawdown, a level that typically signals the end of a…

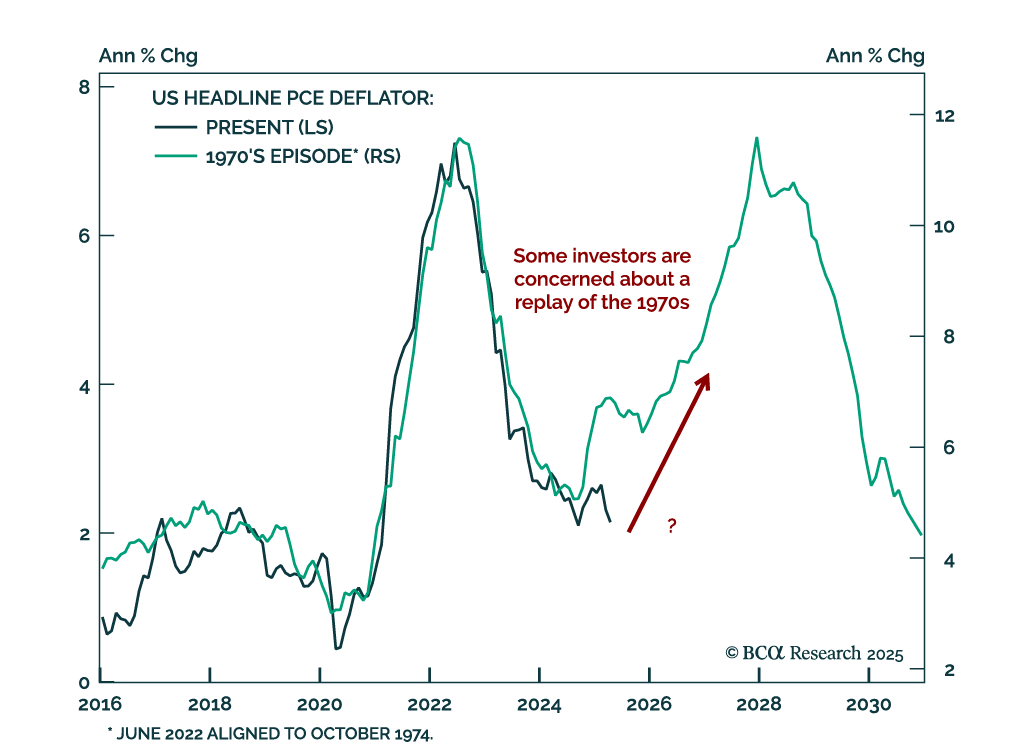

Our Special Reports Unit evaluates whether US inflation is likely to remain structurally elevated. While our base case is for inflation to hover around or modestly above 2% over the long run, there are several risks to that view. Demographics are the most…

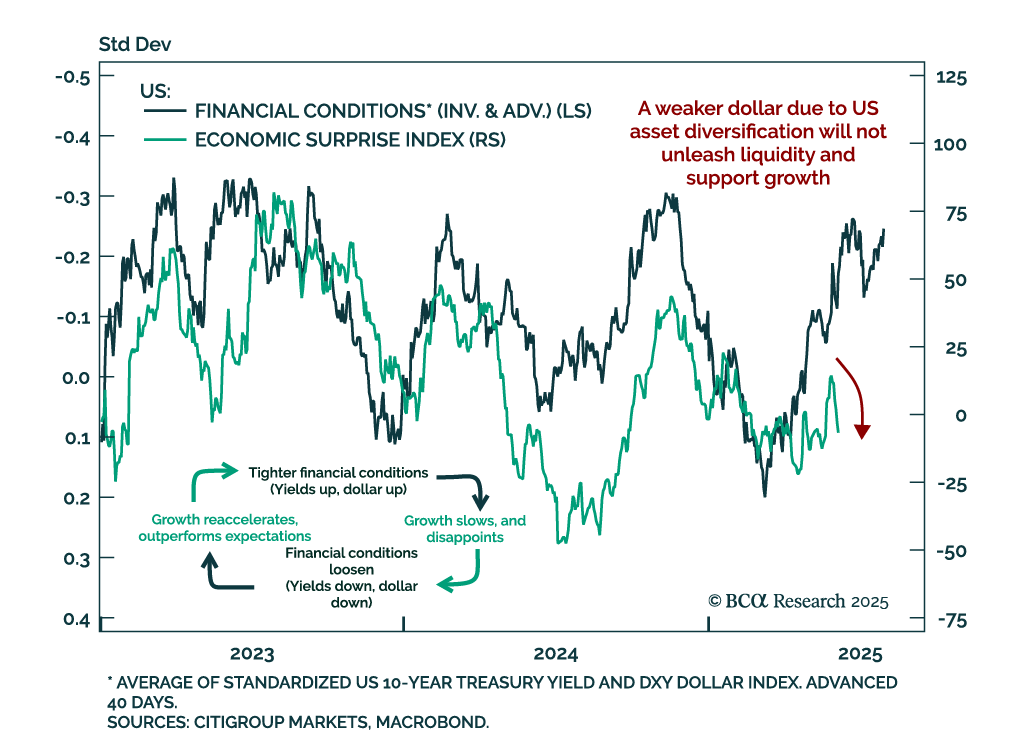

A falling dollar usually eases financial conditions, but recent dollar weakness is unlikely to reverse negative growth surprises, reinforcing our call to sell risk assets on strength. Our tactical framework tracks the reflexive loop between financial…

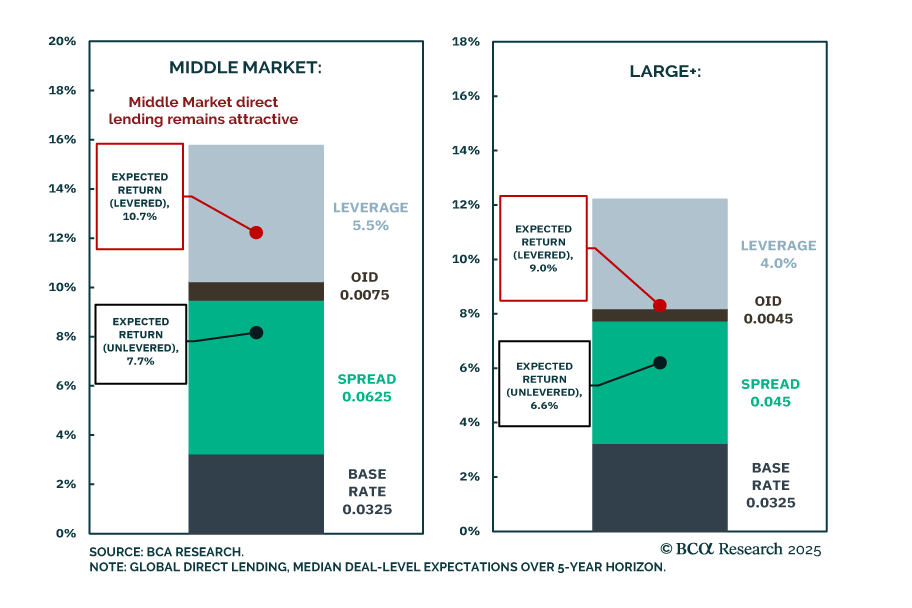

Our PMA strategists published Part 2 of their Capital Market Assumptions update, focusing on Direct Lending. They project gross annualized returns of 7.7% unlevered and 10.7% levered for Global Middle Market Direct Lending, and 6.5% and 8.7% respectively for…

Our Global Asset Allocation strategists remain underweight US equities and the dollar, as fiscal policy overtakes tariffs as the key market driver. The “One Big Beautiful Bill” may avoid worst-case scenarios, but rising US yields are already weighing on…

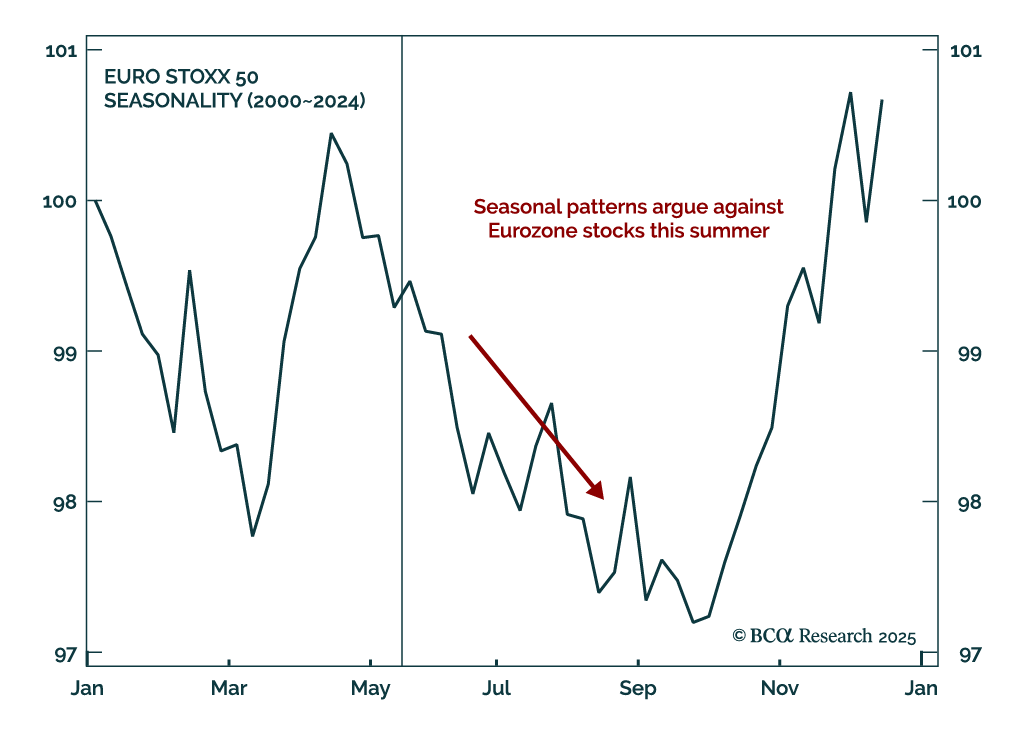

Our European strategists expect the EURO STOXX 50 to remain rangebound between 4750 and 5500 this summer, creating a punishing environment for buy-and-hold investors. With the index near the top of its range, they recommend trimming outright exposure and…

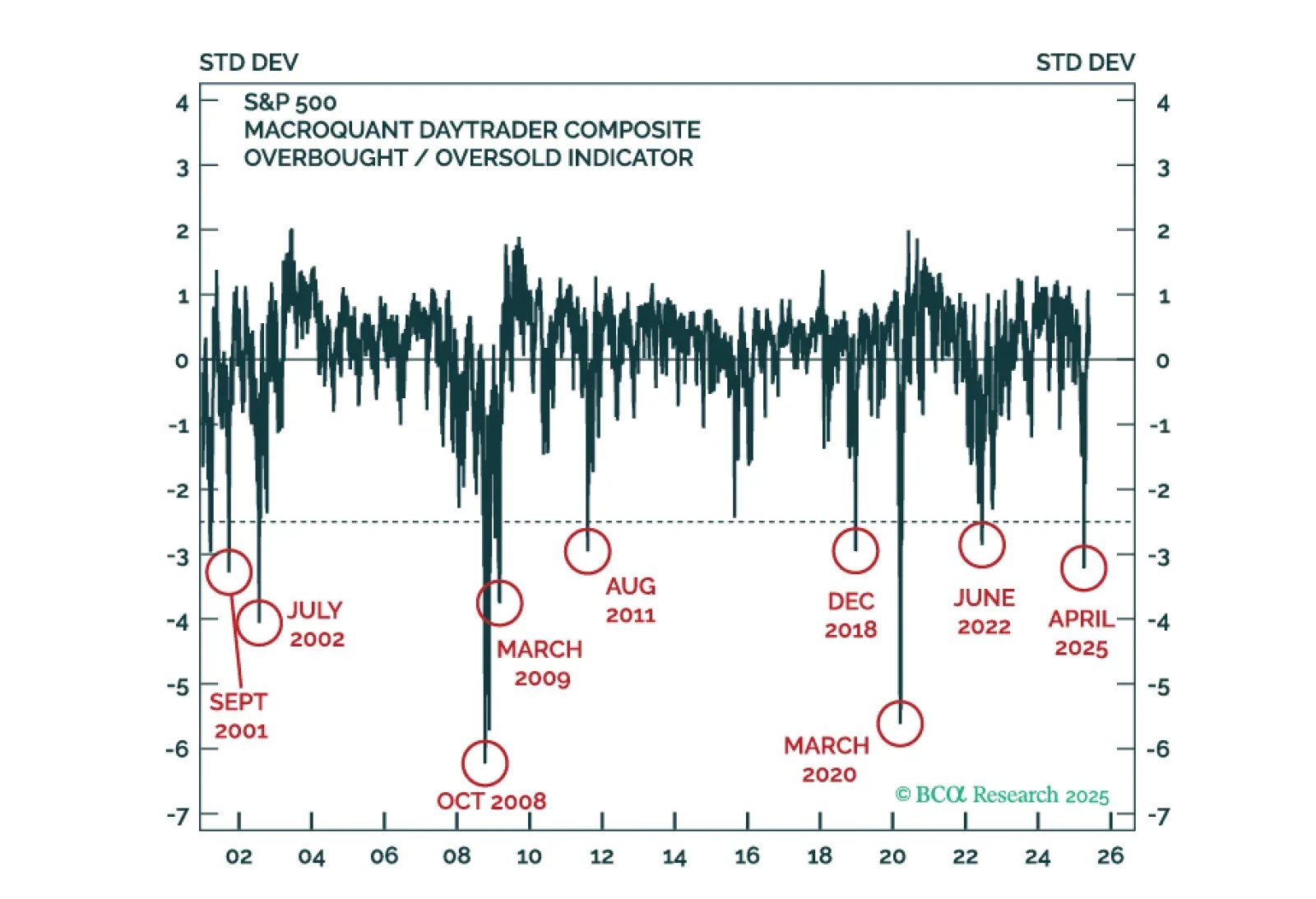

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.