Fiscal

Germany’s economy is regaining momentum after nearly two years of recession. Despite the ongoing cyclical rebound and fiscal stimulus, political gridlock and deep-seated structural challenges threaten to limit the country’s long-term growth potential. Investors should be underweight German Bunds and favor Eurozone equities over German equities.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

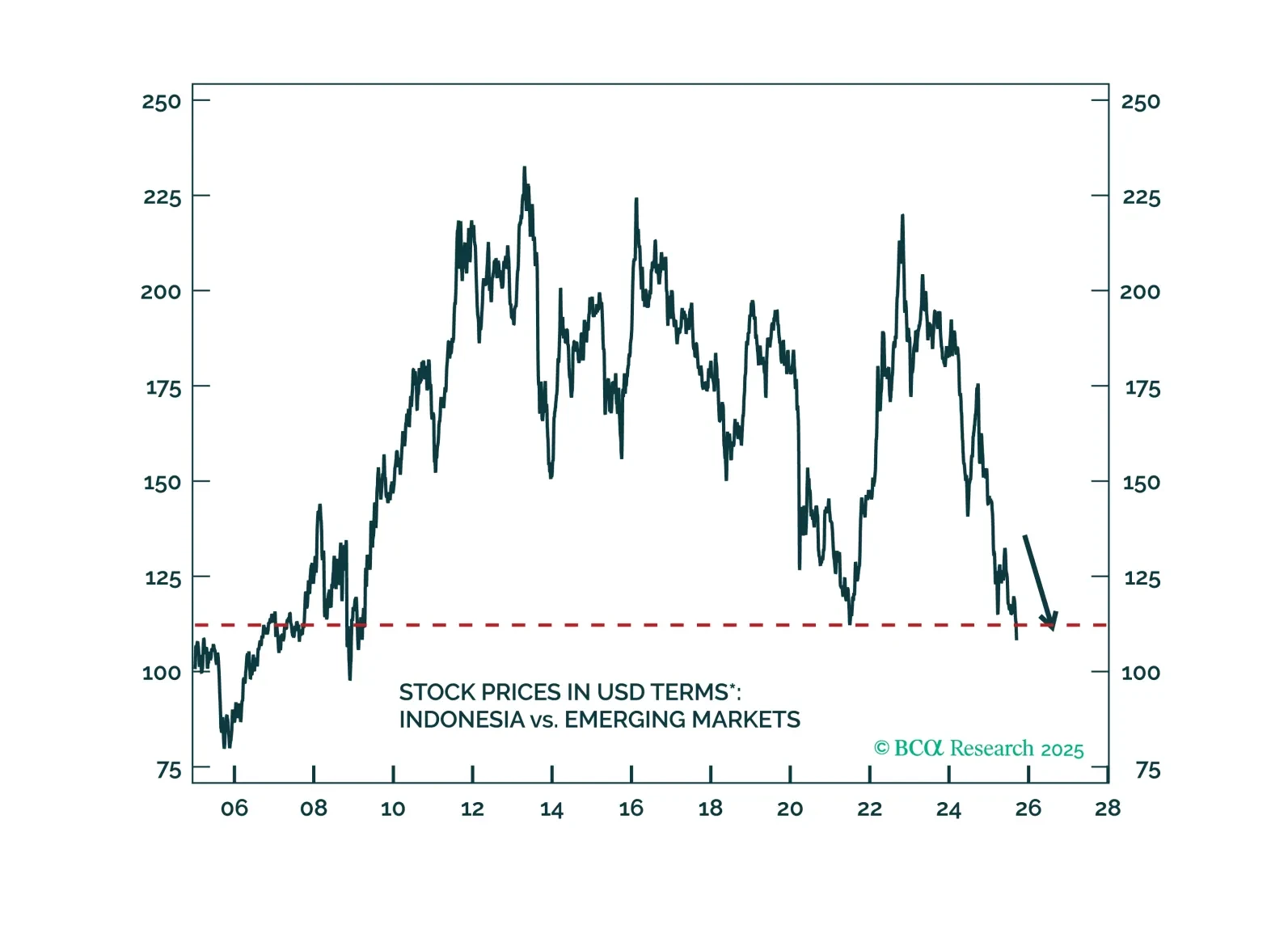

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.