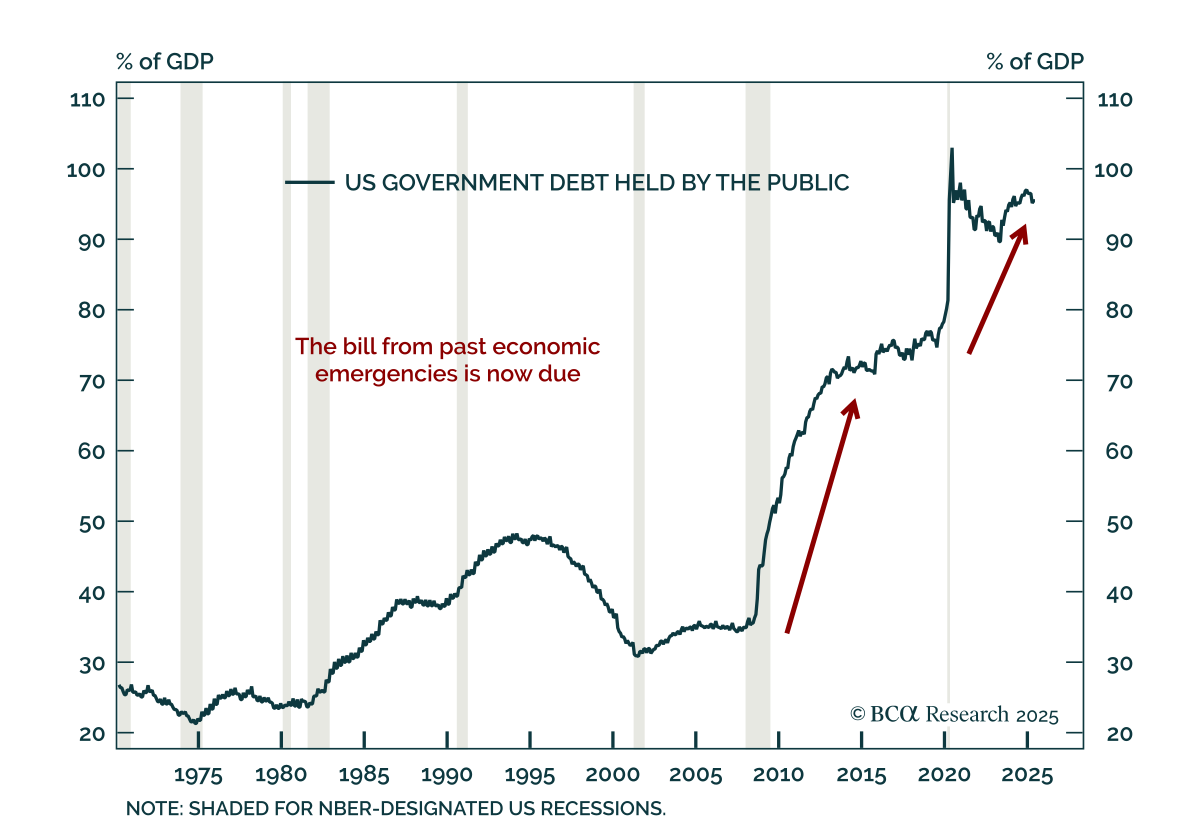

Fiscal

In the Alpha report, we maintain our bullishness on the equity market. We are optimistic that the cash-fueled cycle will evolve into a leverage-driven one, with the AI capex cycle acting as the "bridge" between the two. Our view is easily falsifiable. If the 10-year yield starts moving against us, we will pull the plug on the cycle. One reason to fret is that tariff revenue has now become critical to the equity bull market. Without it, bonds could riot.

Markets have ripped in July, ignoring underwhelming payrolls and retail sales figures. This was our bet, so we don't think this is a mistake. The economy is transitioning from one catalyzed by cash to one led by lower borrowing rates. The combination of a growth slowdown tempered fiscal policy, and an uber-dovish Fed is good for bonds and equities, which has not yet been priced by markets.

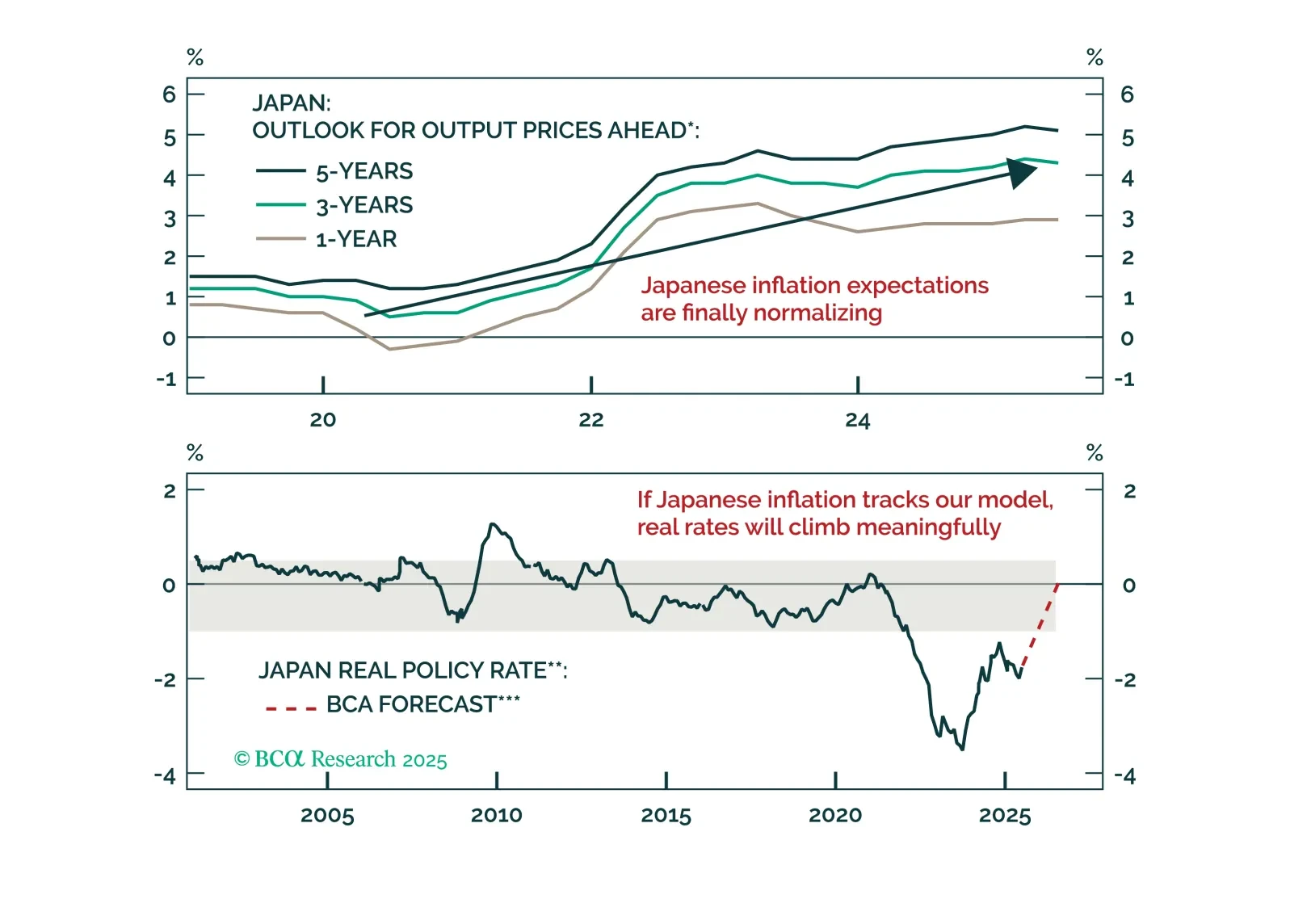

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.