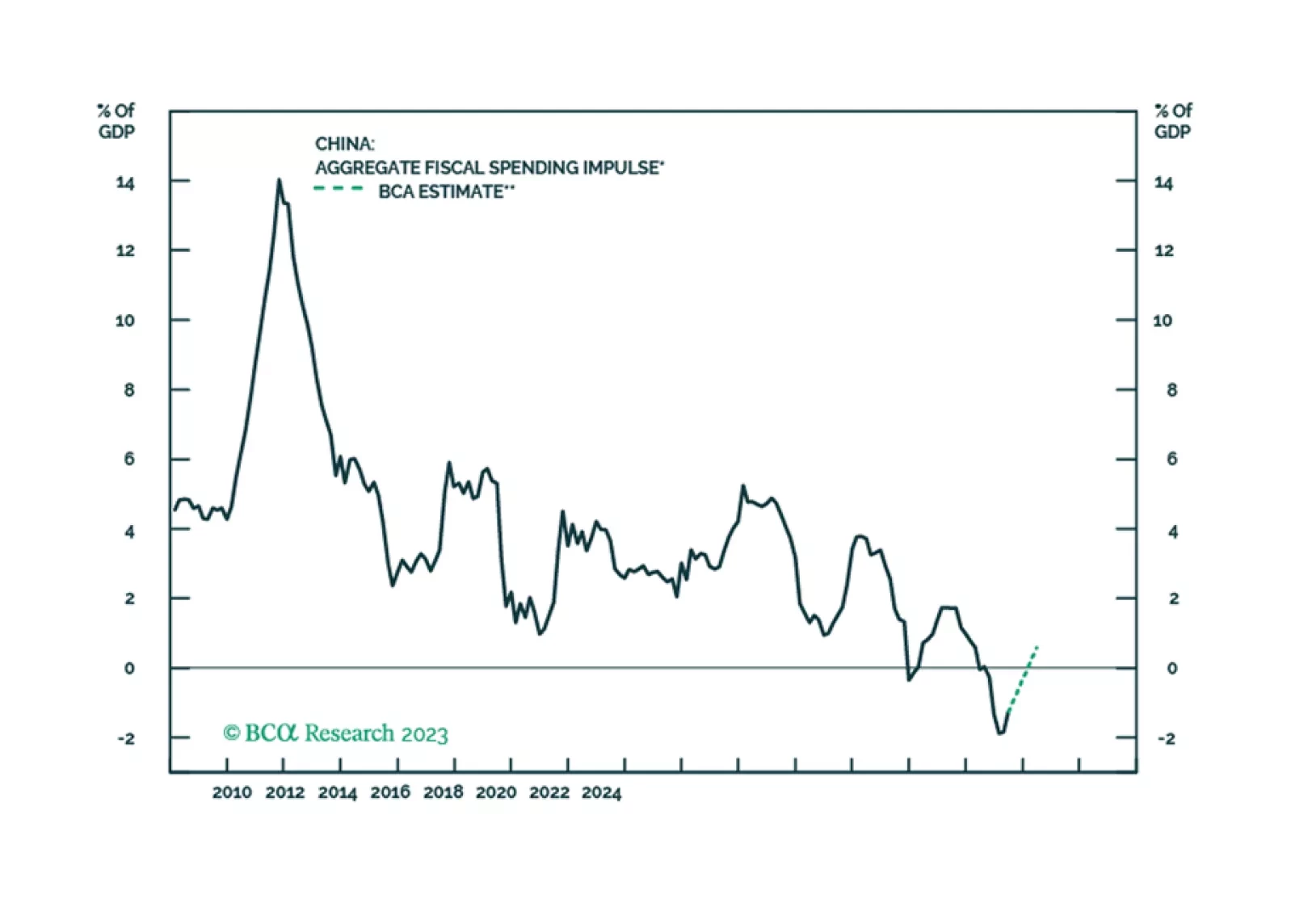

Fiscal

We maintain our view that China’s economic growth in the coming months will remain lackluster. Beijing's recent measures to provide additional financing may help to bridge the gap in government spending in the rest of 2023 and into 2024, but the impact on growth will be very limited.

Stronger US growth elicits a response from the House Republicans. But a government shutdown is not devastating to the economy. What is more devastating would be a crisis in the Middle East, Europe, and Asia. Stay long US defense, energy, and large caps stocks.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

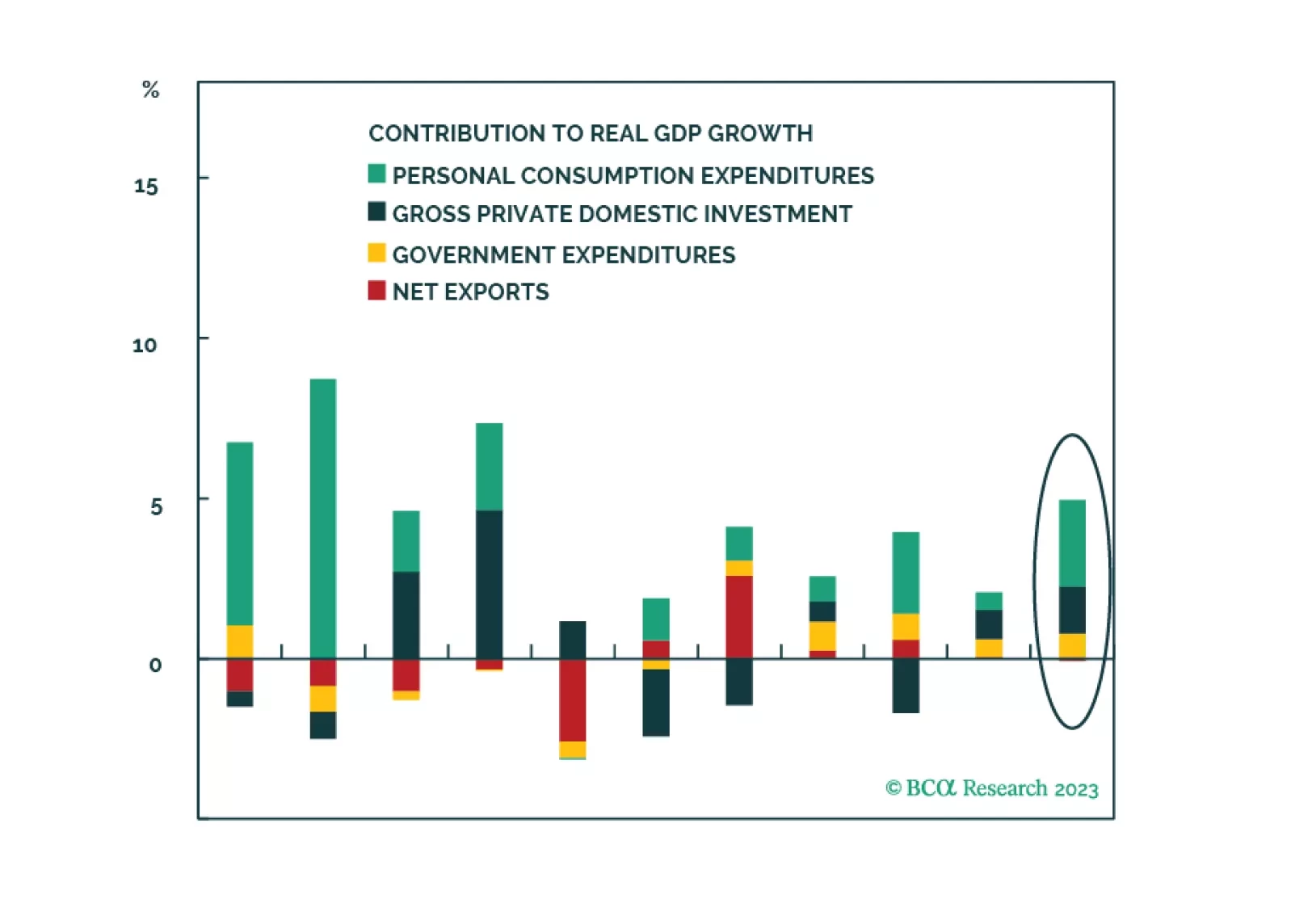

Bulls and bears have capitulated, and the majority of the clients surveyed expect a rangebound market in the near term. Our fair value PE NTM indicates that the S&P 500 is only modestly overvalued. The continued outperformance of the Magnificent Seven faces multiple hurdles. Meanwhile, fiscal spending is unlikely to create an impetus for another leg up in equity performance.

US fiscal, monetary, and foreign policies are unlikely to deliver any dovish surprises for investors in Q4, due to the impending government shutdown, persistent inflation, and instability among OPEC+ and China.

China removed checks and balances in its political system to deal with a very dangerous economic transition. The transition is going badly, yet investors cannot rely on checks and balances to correct or prevent policy mistakes. The Taiwanese election is a looming bellwether.

Investors should prepare for an equity market pullback this fall, prefer Treasuries over stocks, and US defensives over cyclicals. A pullback could also morph into another bear market given that monetary policy is tight, policy uncertainty will spike, global growth is slowing, and geopolitical risks are still high.

The next six-to-nine months hold a crucial test of whether the equity market will ratify the soft landing and the Biden administration or not. If so, then markets will rally on policy continuity and likely gridlock. If not, then markets will struggle until the election is over and again in 2025-26.