Fixed Income

Some investors have thrown in the towel on investing in Chinese equities, instead deploying capital in EM ex-China – or at least contemplating doing so. This report examines the merits of investing in EM ex-China stocks and concludes that EM – whether including or excluding China - will continue underperforming DM equities.

History suggests that a “soft landing” is highly unlikely after such an aggressive Fed tightening cycle. The rally could continue for a little longer but, on the 12-month horizon, market risks are very skewed to the downside.

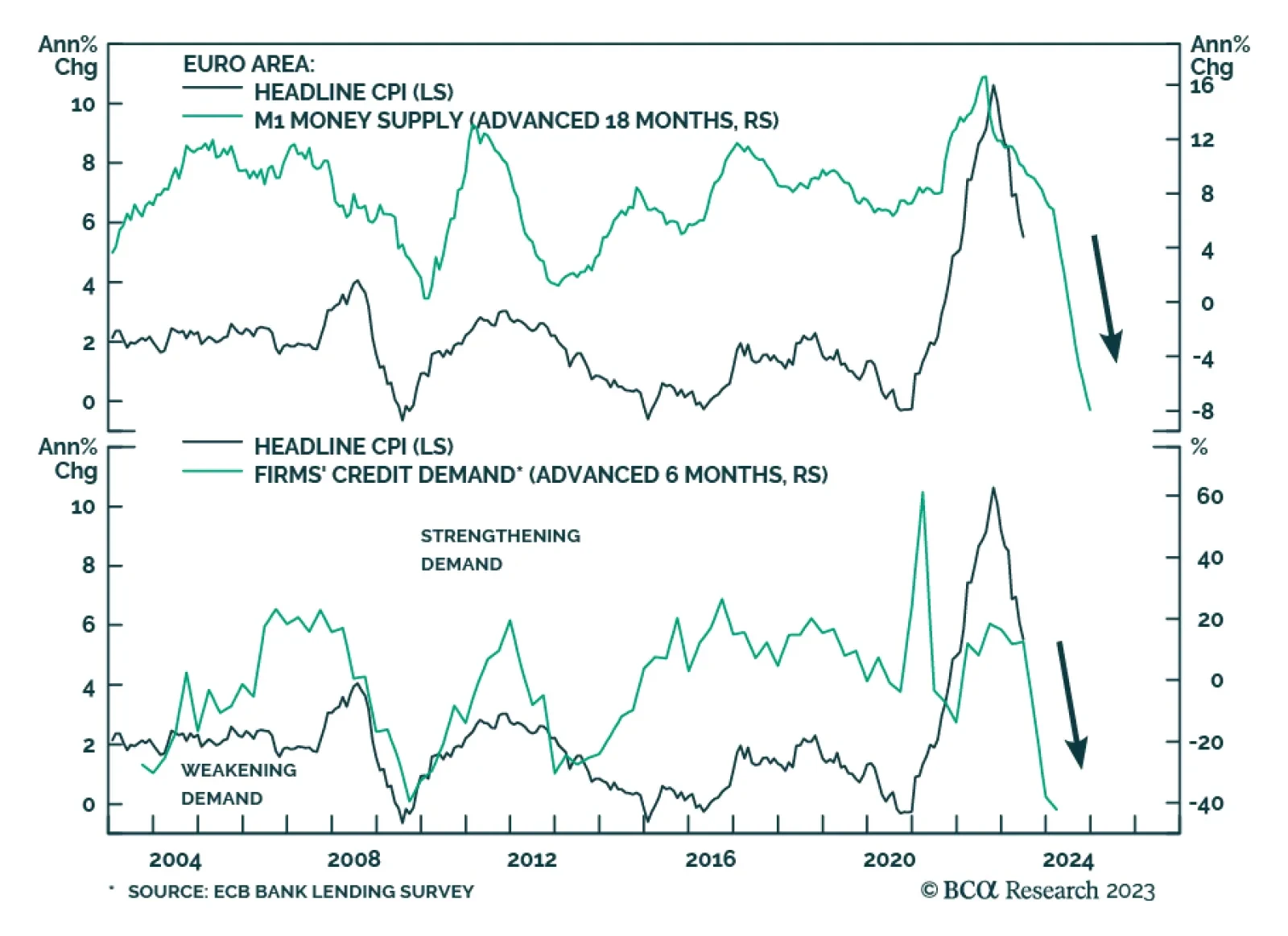

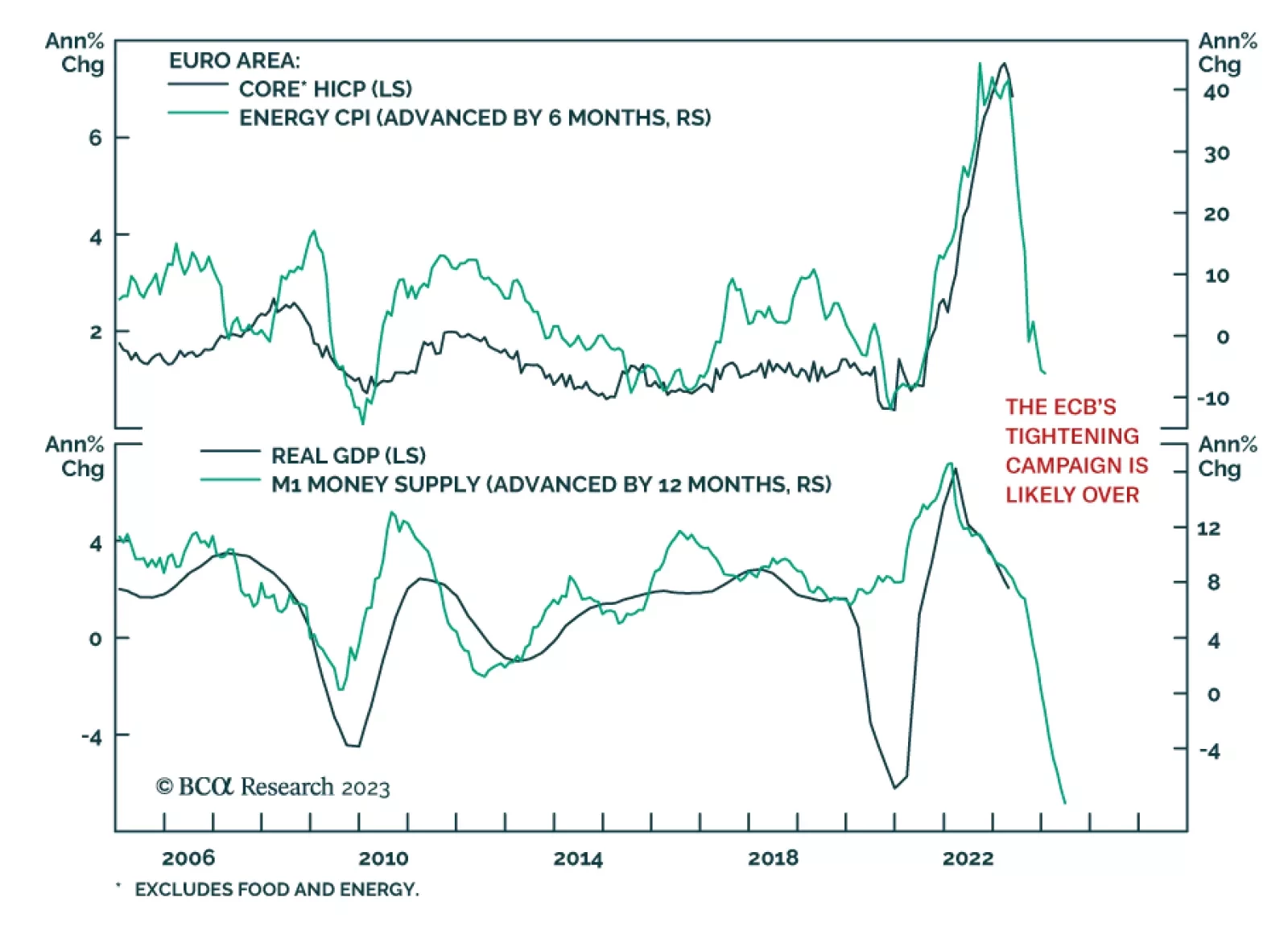

The ECB’s tone has changed decisively. Intransigent forward guidance is gone; data dependency is in. What does this transition mean for the path of European interest rates and the euro?

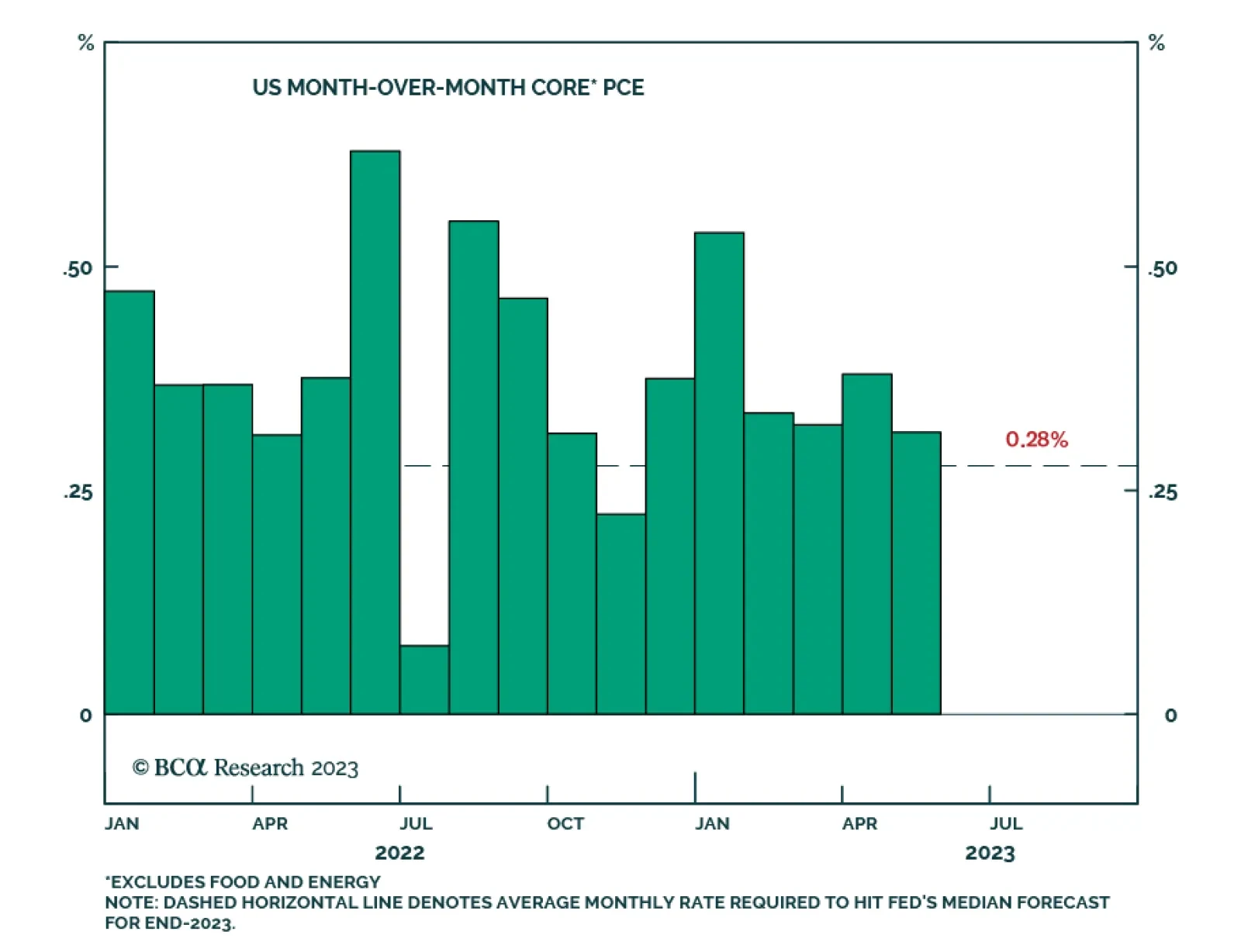

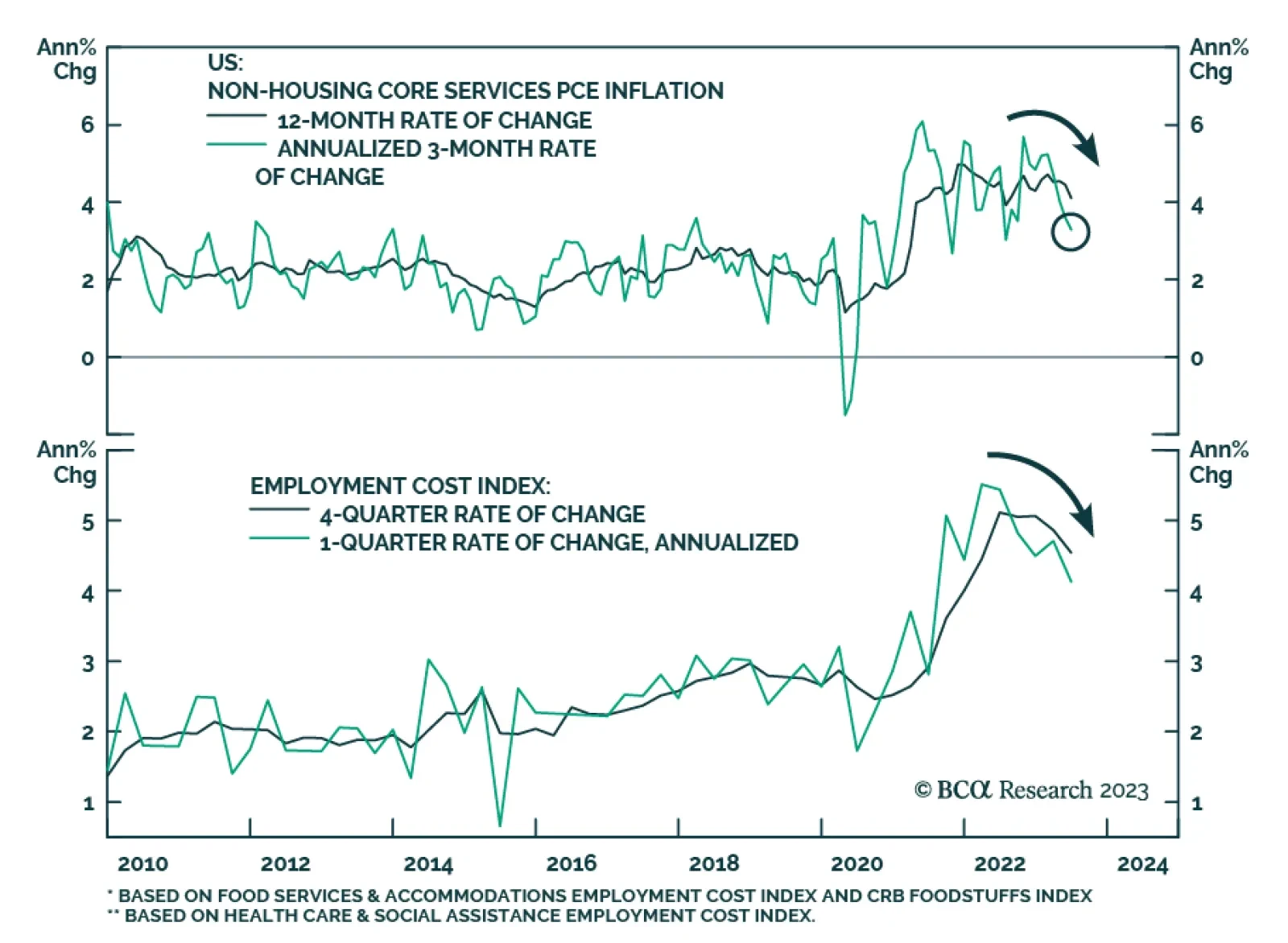

A look at recent US data on economic growth and inflation, with an update on the implications for monetary policy and bond yields.