Fixed Income

This week’s Special Report updates our US default rate forecast and considers whether corporate bond spreads offer value given the trend in credit fundamentals. We also consider the relative value proposition between investment grade and high-yield credit and between European and US corporate bonds.

Assuming yesterday’s policy rate hike is a sign that Turkey is finally veering towards orthodox economic policies; should investors rush in?

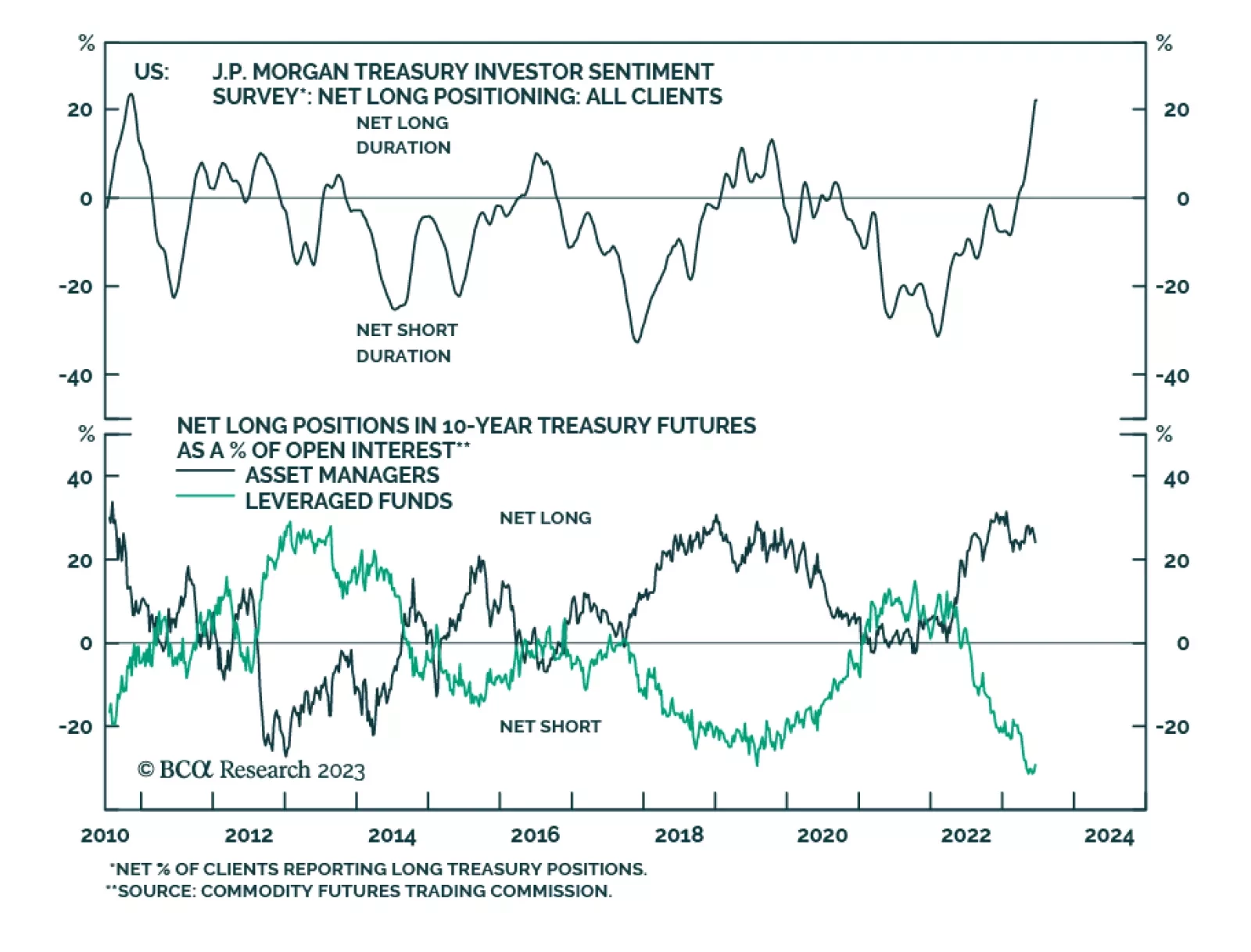

This week’s report examines three potential catalysts that could push Treasury yields meaningfully higher within the next few months. We also consider the rebuild of the Treasury’s cash holdings and its implications for the Fed’s balance sheet policy and financial markets.

China is facing a risk of deflation. Marginal interest rate cuts and targeted stimulus will be insufficient to boost China’s growth given the current deflationary mindset and the danger is that the economy may be entering a liquidity trap. Deflation is bullish for government bonds, but negative for equity prices. Chinese share prices will continue to decline.

In this Insight, we discuss the currency and bond market implications of last week’s ECB and Bank of Japan policy meetings. The conclusion: the ECB is on a path to an overly hawkish policy mistake, while the Bank of Japan’s dovish stance is growing more unsustainable.