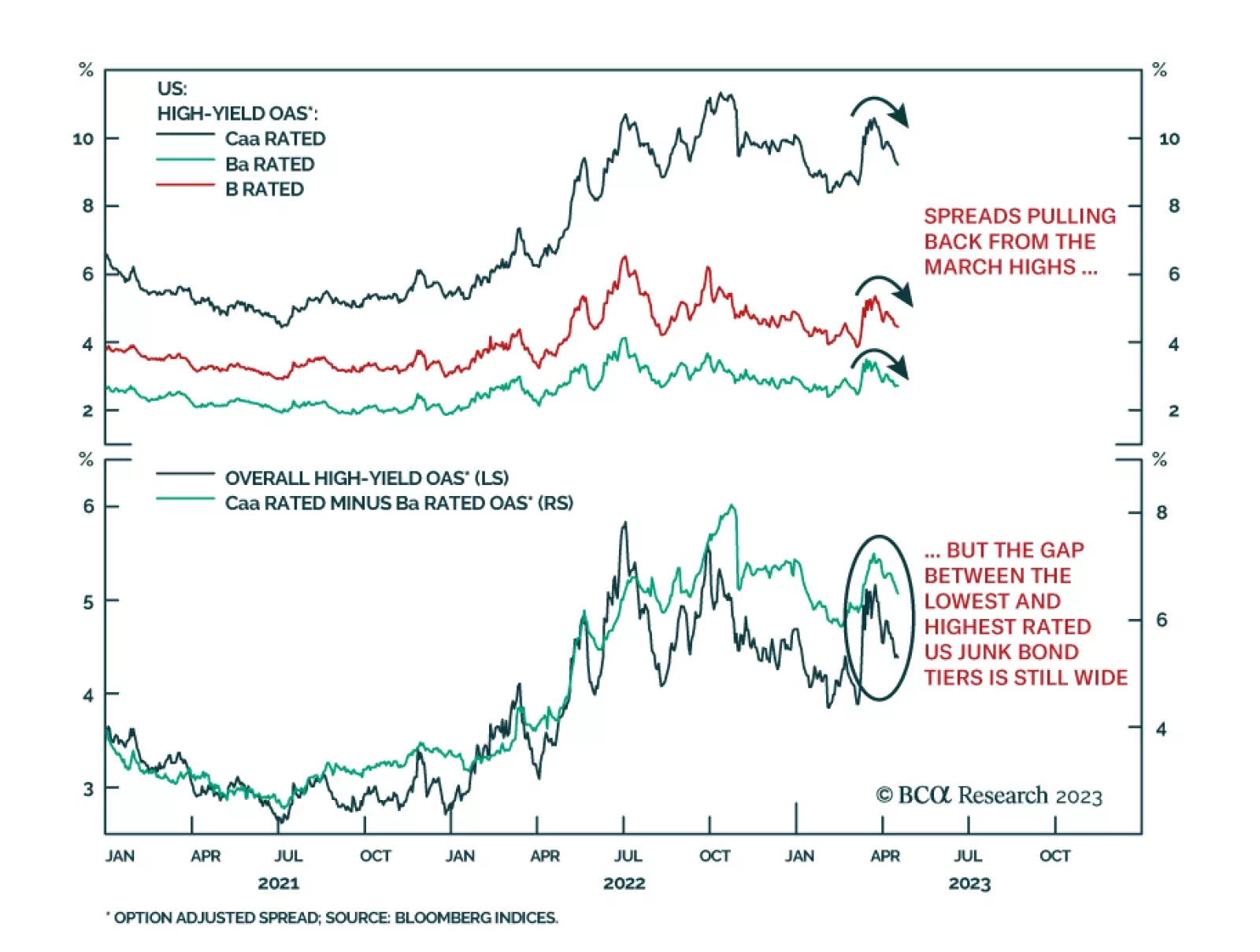

Fixed Income

Pent-up demand for services is keeping the global economy going, but we still expect recession over the next 12 months. Investors should keep a cautious portfolio stance.

This week we present our Portfolio Allocation Summary for May 2023.

In Section I, we discuss why the rally in stock prices over the past month reflects the soft-landing view, and why that is not a likely economic outcome. US inflation is slowing, but target inflation remains elusive. Meanwhile, cracks in the US labor market are already apparent, and there is strong evidence against the view that US stocks are appropriately priced for an eventual US recession. This underscores that conservative investment positioning is still warranted. In Section II, we check in on the indebtedness risk of several major economies, and examine whether these risks exist primarily in the household, nonfinancial corporate, or government sectors. While there are limited cyclical implications of recent trends in global indebtedness, there are several problems that will eventually “come home to roost” – particularly in the US and China.

First Republic Bank’s earnings report showed how its struggles have exaggerated the perception of other banks’ distress. Ex-FRC, the banking system appears to be coping with the post-Silicon Valley Bank turmoil pretty well.

Inflation is hot, but inflation expectations are not. We explain the answer to this apparent puzzle and discuss the investment implications. Plus we identify two commodities that are at imminent risk of reversal.

Government financing vehicles (LGFVs) are a key component of China’s credit system. LGFV bonds make up a 40% share of the onshore corporate bond market, and loans to LGFVs make up 20% of total loans. LGFV debt-servicing capacity is very weak. What are the ramifications of all of these for Chinese economic growth and financial markets?

This Special Report discusses why there is a non-negligible risk that the US Congress will not reach a timely agreement to lift the debt ceiling this summer. It also discusses what will happen in bond markets in the lead up to the debt limit and in the case where a deal is not reached in time.

The latest round of earnings calls from the systemically important banks was encouraging on balance. Households are still flush and still spending and consumer and business delinquencies remain remarkably low. Though a recession is surely coming, it doesn’t seem to be lurking just around the corner.

The dollar has entered a structural bear market. Although the greenback could get a temporary reprieve during the next recession, investors should position for a weaker dollar over the long haul.