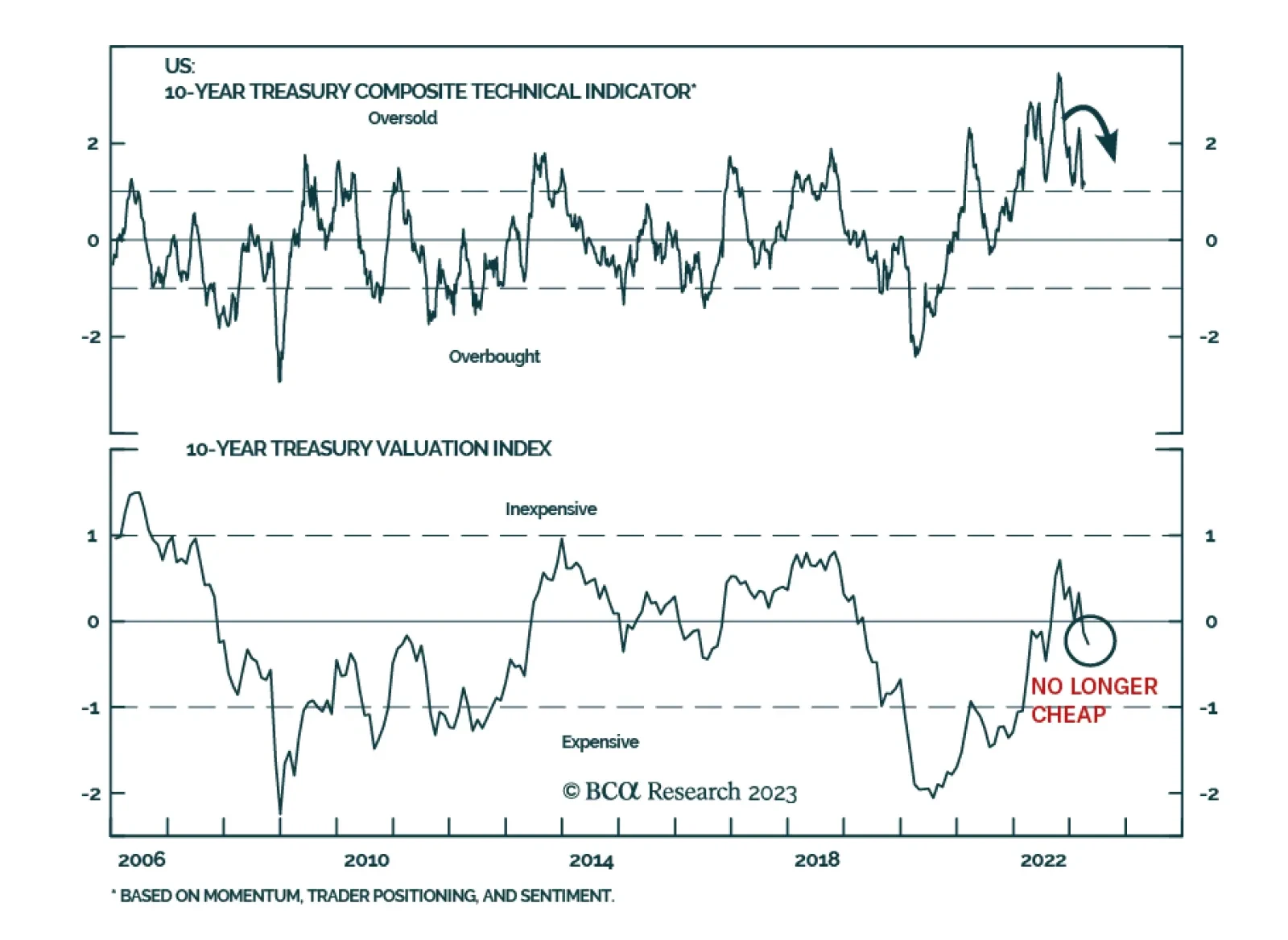

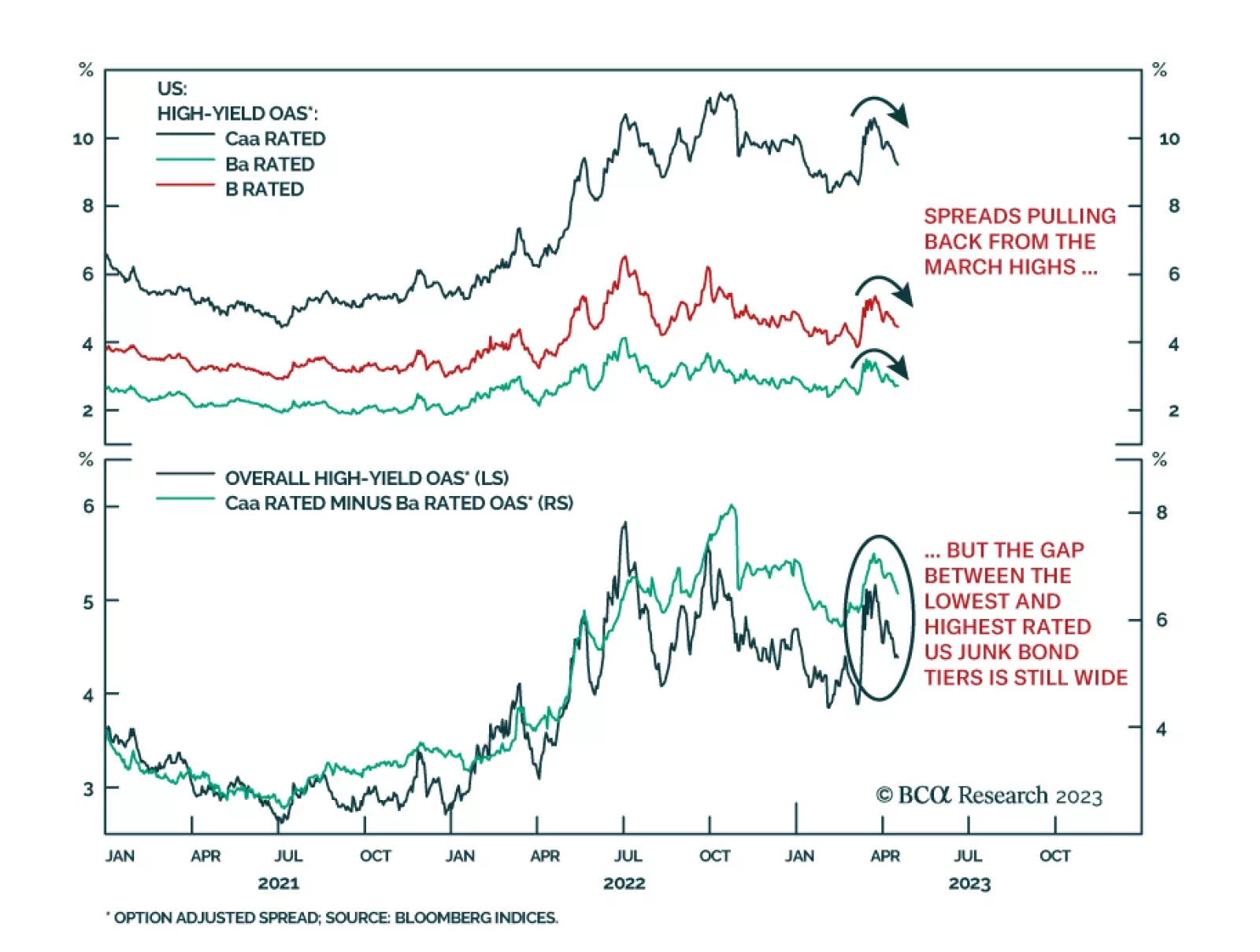

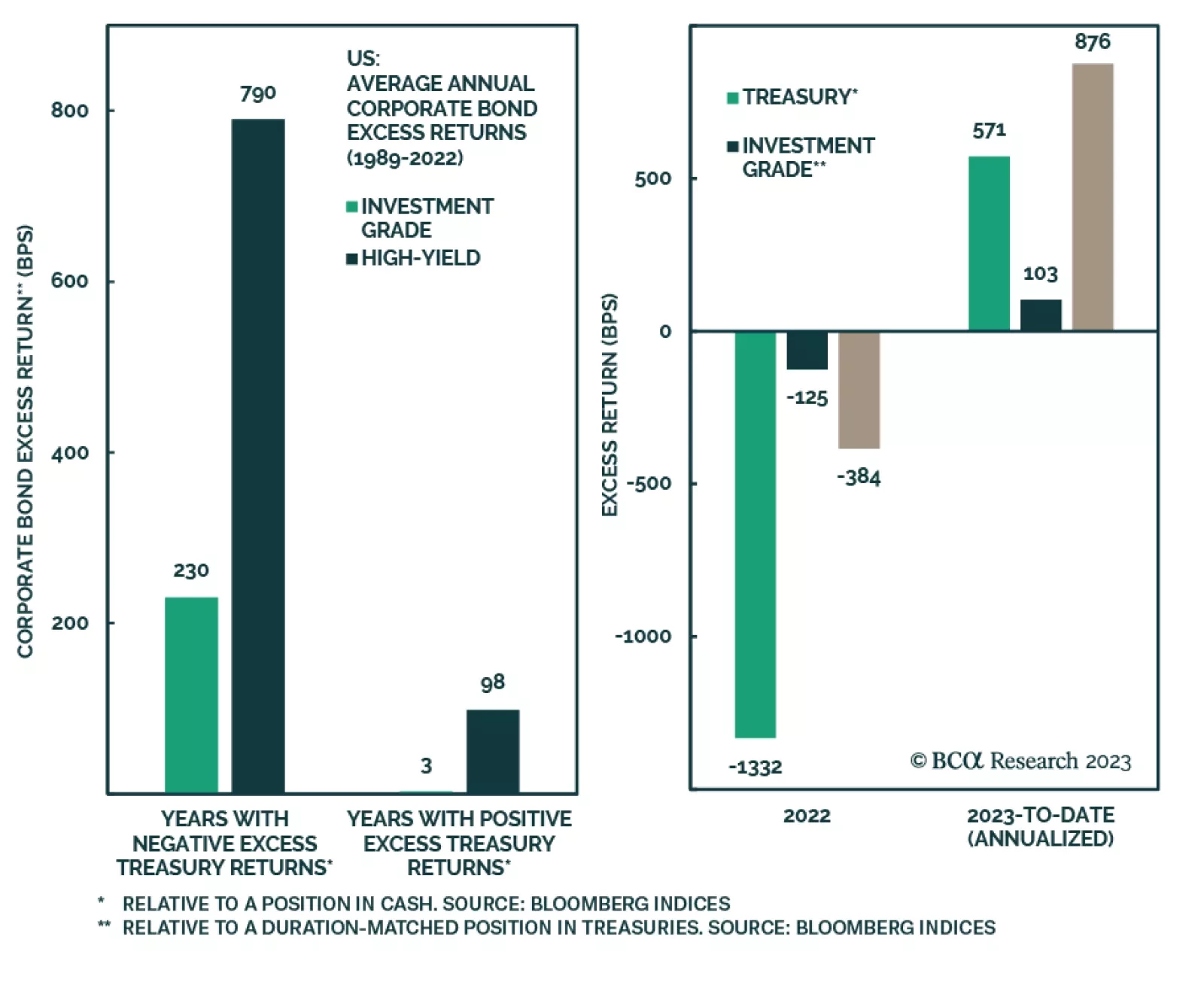

Fixed Income

This report looks at the relationship between rate risk and credit risk and how it has changed over time. It also makes the case for favoring agency MBS within an underweight allocation to US spread product.

In this Special Report, we evaluate future prospects for the Australian dollar and Australian government bonds. The currency remains fundamentally cheap, and positioning is very short, but the AUD will continue to underperform in the near-term due to sluggish global growth. Australian government bonds have had a nice run of outperformance over the past year, but it is now time to take profits with given the uncertainty that the RBA will deliver the rate cuts currently discounted.

There are several widespread market narratives regarding US inflation, the Fed’s policy, global manufacturing/trade and China’s recovery that we disagree with. In this report, we explain our reasoning and where it puts us in terms of investment strategies.

Today’s releases of the March CPI and March FOMC minutes do not change our view that the Fed will deliver one more 25 basis point rate increase before going on hold.

Through February and March, the number of US ‘job losers’ surged by almost half a million. Constituting the largest two-month increase in Americans who have lost their job since the depth of the pandemic. Unless we see a big drop in the number of job losers in the coming months, the correct investment strategy is still to position for a US recession that starts in 2023.

In this report, we present our performance review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for the Q1/2023, and the outlook and scenario analysis for the next six months. The portfolio slightly underperformed its benchmark during the quarter as global growth showed surprising resilience to begin the year. Looking ahead, the portfolio is positioned to capitalize on an expected slowing of global growth over the rest of the year through an overweight stance on government bonds versus spread product.