Fixed Income

Ironically, increased confidence that the economy can withstand higher bond yields may be necessary to lift yields to a level that is actually detrimental to growth. Thus, until more investors are convinced that a recession will be averted, a recession will be averted. Remain tactically bullish on stocks for now. A more defensive posture will likely be necessary later this year.

Biden’s State of the Union address will mostly be blocked by a gridlocked Congress. The one point of agreement, big spending, spells trouble over the long run, even if a technical default is avoided this fall.

The Fed is betting that the usual non-linearity of unemployment is different this time, but so far, there is nothing to suggest that it is different. We discuss the key signposts to watch out for, plus the implications for interest rates and asset allocation.

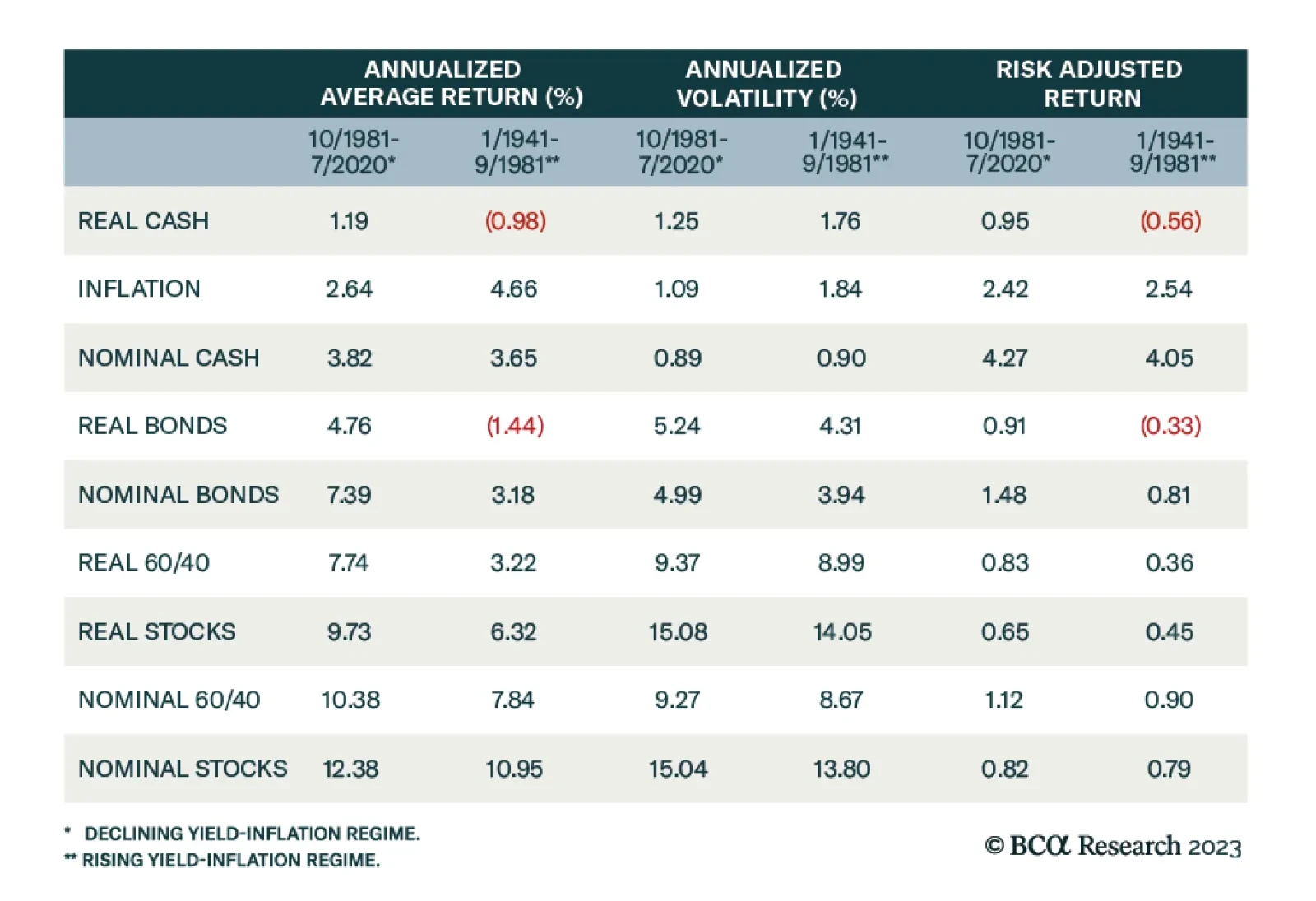

This is the first of two Special Reports aiming to answer client questions in response to the recent dramatic changes in stock-bond correlations. In this report we focus on what role US Treasurys have played since 1872, how the current regime shift in stock-bond correlation compares to 150-years of history, and how it will impact asset allocation going forward.

The Fed’s actions at its meeting last Wednesday were no surprise – downshifting to 25 basis points while guiding for more hikes was widely expected – but Chair Powell’s newly conciliatory tone at the press conference helped to spark a two-day equity rally. We remain overweight equities, expecting the S&P 500 to rally into the mid-4,000s at some point in the first half.

This week we present our Portfolio Allocation Summary for February 2023.

Financial markets were taken on a wild ride between Wednesday and Friday of this week, with hugely important monetary policy meetings in the US, euro area and UK along with a rash of economic data. Despite all the news, noise and market volatility, the underlying message for monetary policy and bond yields in the US, euro area and UK is unchanged.

The US economy will experience a period of benign disinflation over the next few quarters. Beyond this goldilocks period, either the economy will slip into a mild recession in 2024, or more ominously, a second wave of inflation will prompt the Fed to slam on the brakes, leading to a deep recession.