Fixed Income

In this Special Report, we consider what some common monetary policy rules are recommending for the major central banks and derive conclusions on duration strategy and country allocation for bond investors. We conclude that rate hike expectations in most countries may appear appropriate given the current global backdrop of high inflation and low unemployment, but look elevated on a forward-looking basis versus slowing global growth and peaking global inflation.

What is the outlook for the European housing market amid rising mortgage rates and the energy crisis? Does housing represent a systemic risk? Can households weather the storm? And what are the opportunities, if any?

The messages from the deteriorating fundamental backdrop (tight monetary policy, slowing global growth) and improved credit valuation (elevated 12-month breakeven spreads) are giving conflicting signals on corporate bond strategy. We are putting more weight on the fundamentals and are staying with an overall underweight stance on global investment grade corporates, with a slight bias towards Europe given more attractive spread valuations. At the same time, we see selective opportunities in sectors where risk-adjusted spreads are wide as signaled by our individual country sector valuation models, like US Energy and euro area Financials.

Stocks will only get temporary relief from gridlock. Inflation will abate but then remain sticky. US and global policy uncertainty and geopolitical risk will remain historically high.

A client concerned about the slump in asset prices, the stubbornness of inflation, and rising bond yields asks what went wrong, and what happens next? This report is the full transcript of our conversation.

Central banker messaging after the latest rate hike announcements in the US, UK and Australia indicates a shift in focus from the pace of hikes to how high rates must rise to slow growth and bring down inflation. This represents the next stage of the global tightening cycle, where rates will go higher in countries where neutral rates are higher, like the US, compared to countries with lower neutral rates like the UK and Australia.

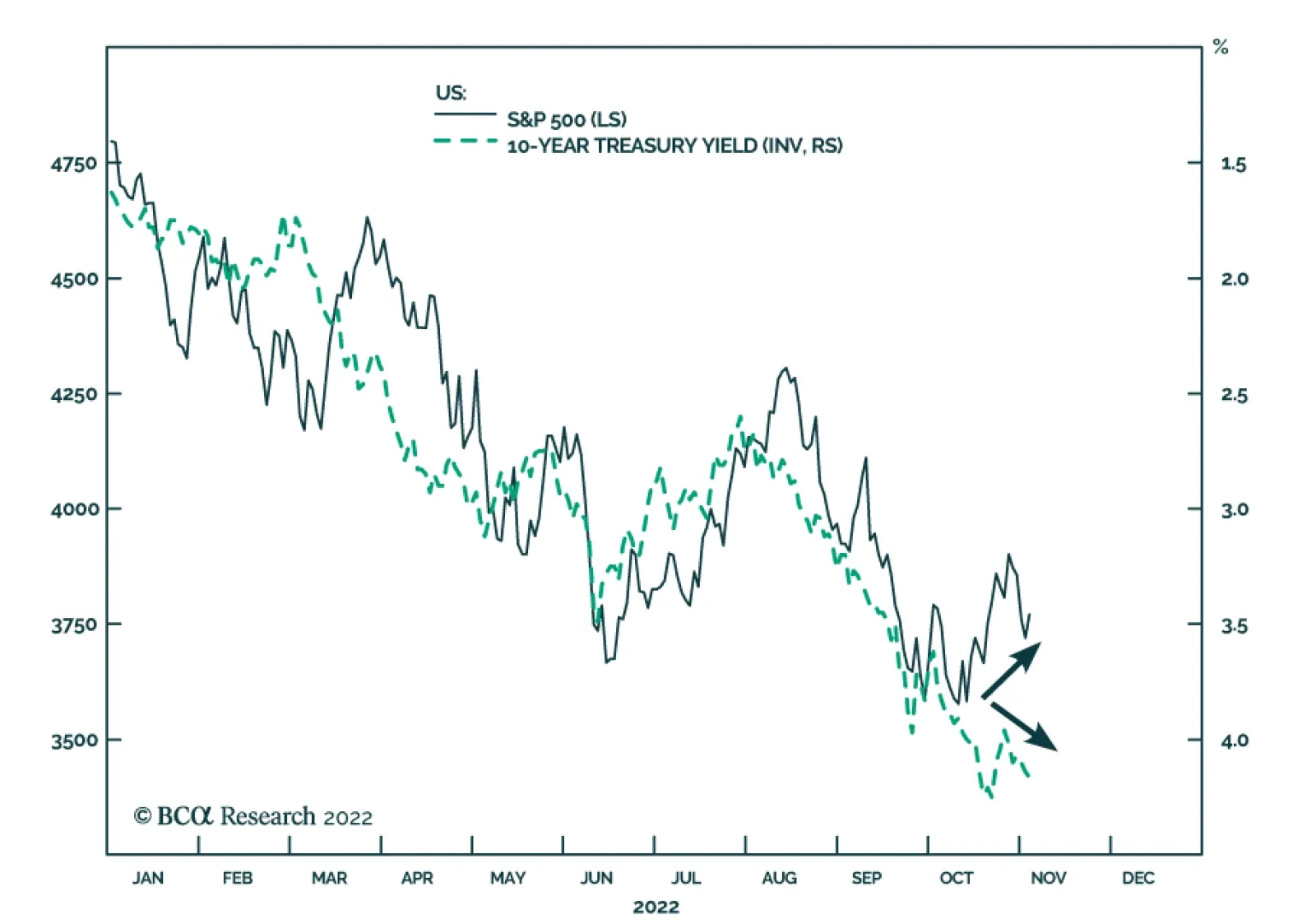

This week we present our Portfolio Allocation Summary for November 2022.

Europe is hampered by a lower trend growth rate, but has room to grow faster than the US over the next two years. How can investors profit from this outlook?

As the FOMC explicitly acknowledged this week, monetary policy operates with substantial lags. We see the risks to stocks as tilted to the upside over the next 6 months but are neutral on global equities over a 12-month horizon.