Fixed Income

Provided that US inflation is due to excess demand rather than supply constraints, demand destruction will likely be needed to bring core inflation below 3.5%. Such growth contraction is positive for counter-cyclical currencies like the US dollar. In China, the Party's focus is to alleviate structural inequality and a long-term confrontation with the US; and authorities are not yet panicking about the cyclical state of the economy. Hence, an economic recovery is unlikely in the coming months.

Older workers have deserted the labour force in the US and the UK, but not so in the Euro area and Japan. The result is that wage inflation is red hot in the US and the UK, but not so in the Euro area and Japan. Hence, the Bank of Japan is right to remain a lone dove, the ECB must pivot from its uber-hawkish stance quite soon, but the Fed and the BoE must not pivot from their uber-hawkish stance too soon. We go through the major investment implications.

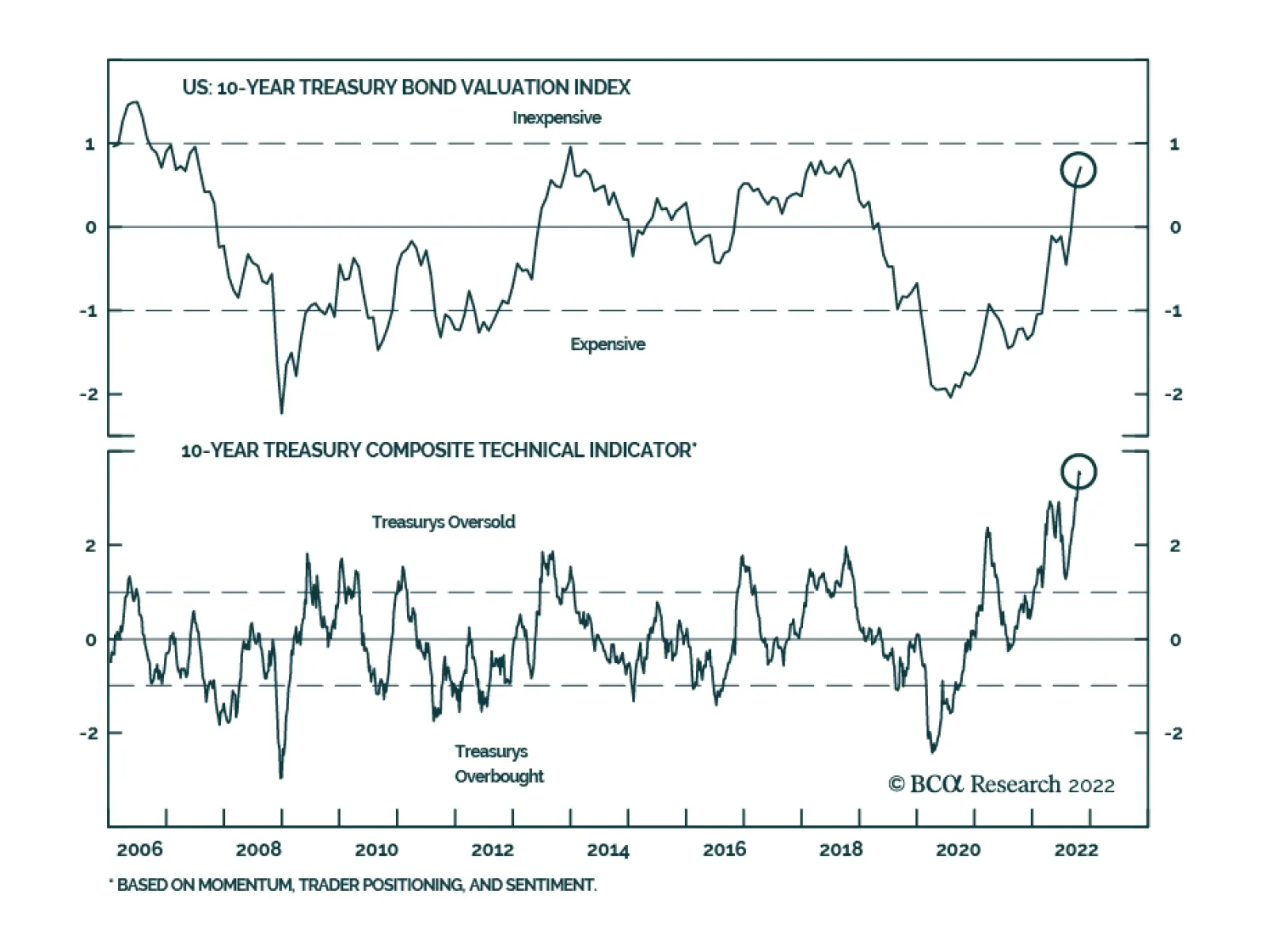

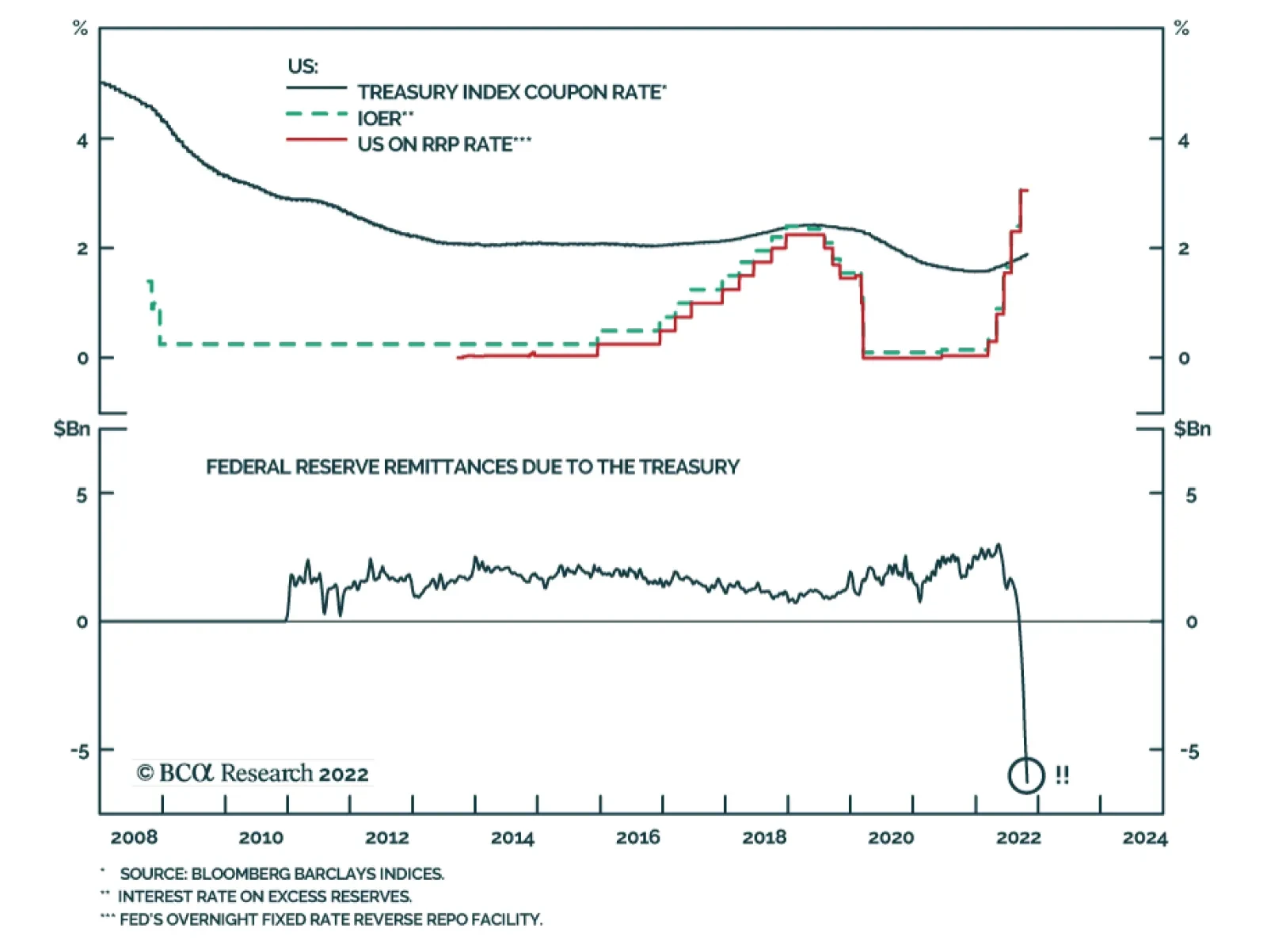

This week’s report examines the state of the global monetary tightening cycle and addresses some frequently asked questions about the Fed’s QT program. New yield curve trades are recommended for the US and German yield curves.

The ECB increased interest rates and announced the start of its balance sheet wind down; yet, markets took the news as a dovish outcome. Are we really getting close to the end of the ECB’s tightening campaign? How asset prices will react?

Falling inflation will allow bond yields to decline in the major economies over the next few quarters. As such, we recommend that investors shift their duration stance from underweight to neutral over a 12 month-and-longer horizon and to overweight over a 6-month horizon. Structurally, however, a depletion of the global savings glut could put upward pressure on yields.

In Section I, we note that while recent inflation developments point to some supply-side and pandemic-related disinflation, they also point to potentially stickier inflation over the coming several months. The inflation, monetary policy, and geopolitical outlook remains sufficiently risky that an overweight stance towards equities within a global multi-asset portfolio is not justified, and we continue to recommend a neutral stance for now. This month’s Section II is a guest piece written by Martin Barnes. Martin, who retired from BCA Research as Chief Economist last year after a long and illustrious career, discusses the outlook for government debt and the possibility of an eventual crisis.

We recommend that investors use the following framework to think about whether potential disinflation would be bullish or bearish for share prices: disinflation will prove to be bullish for global share prices if it is due to an improvement in supply-side dynamics, but bearish if it is demand driven. We believe it is the latter.

It takes time for wage inflation to die. So, if 2022 was the year that central banks’ monster tightening killed bond and stock market valuations, then 2023 will be the year that it finally reaches the economy and kills profits, jobs, and the wage inflation that has so far refused to die. This means that commodity prices have substantial further downside, while healthcare relative performance has substantial further upside.