Fixed Income

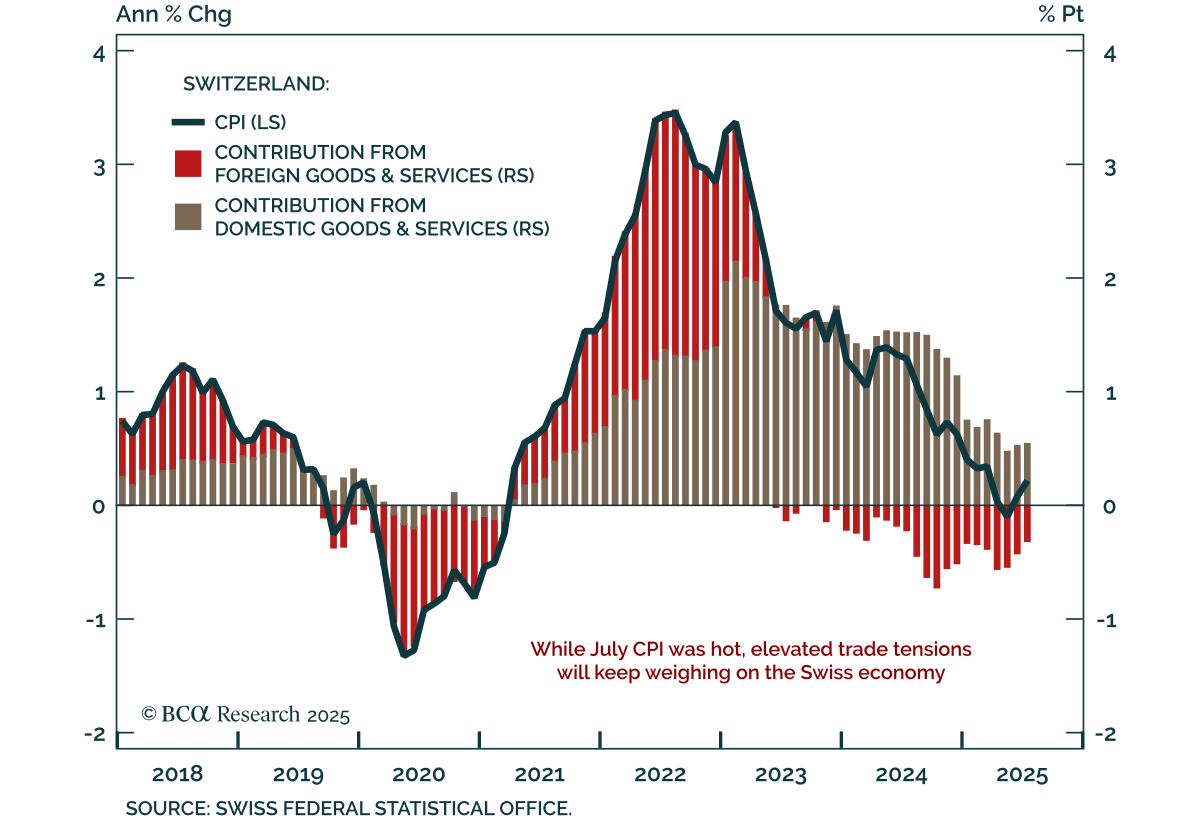

Hot July inflation does little to alter Switzerland’s near-term deflationary outlook, as soft data and trade risks support a defensive stance and preference for bonds over equities. CPI ticked up to 0.2% y/y from 0.1%, with core rising to 0.8%, both…

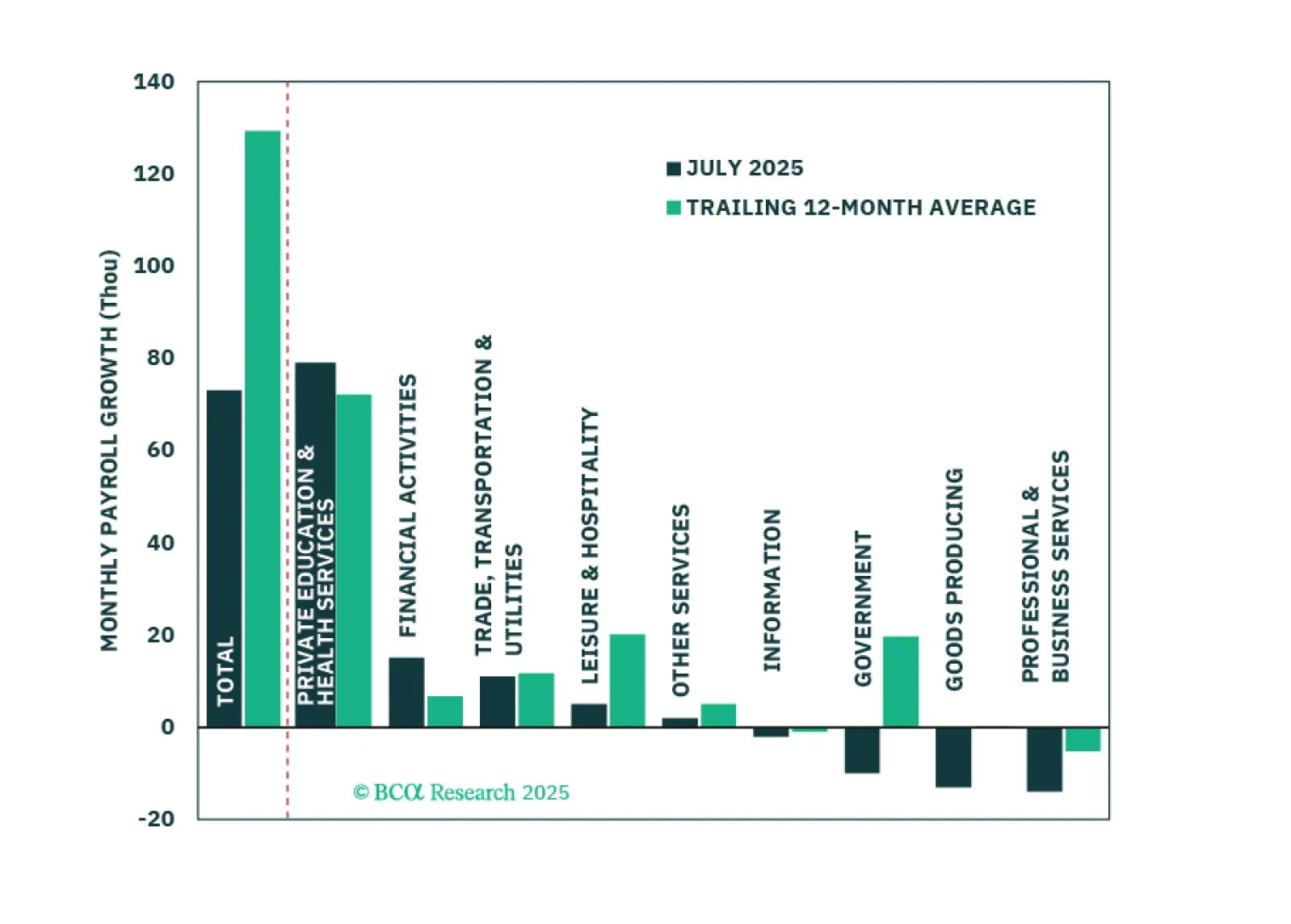

Economic activity and hiring cooled significantly in the first half of the year. The most important question for investors is whether this signals an imminent increase in labor market slack.

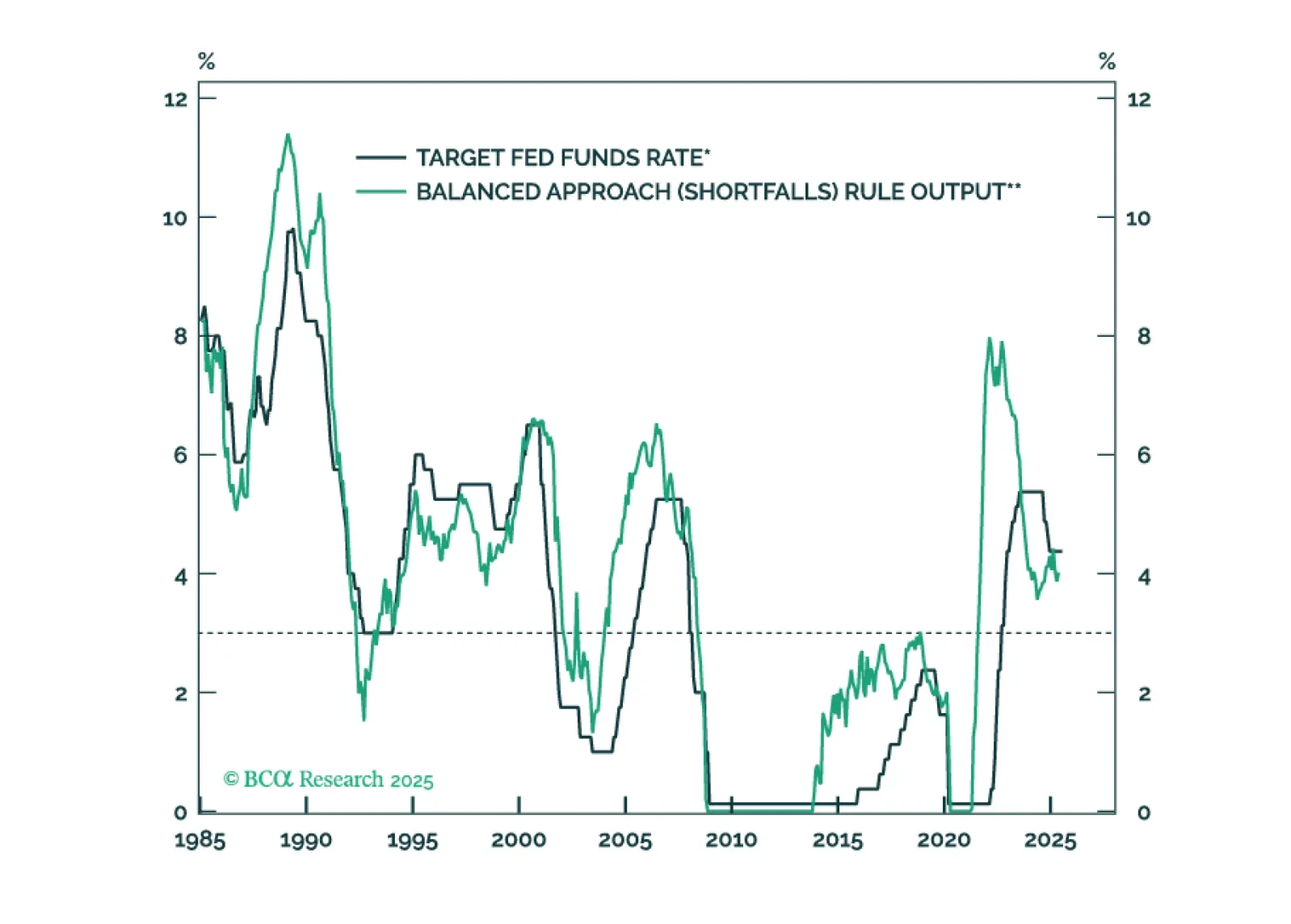

The Fed will keep rates on hold until the unemployment rate forces its hand.

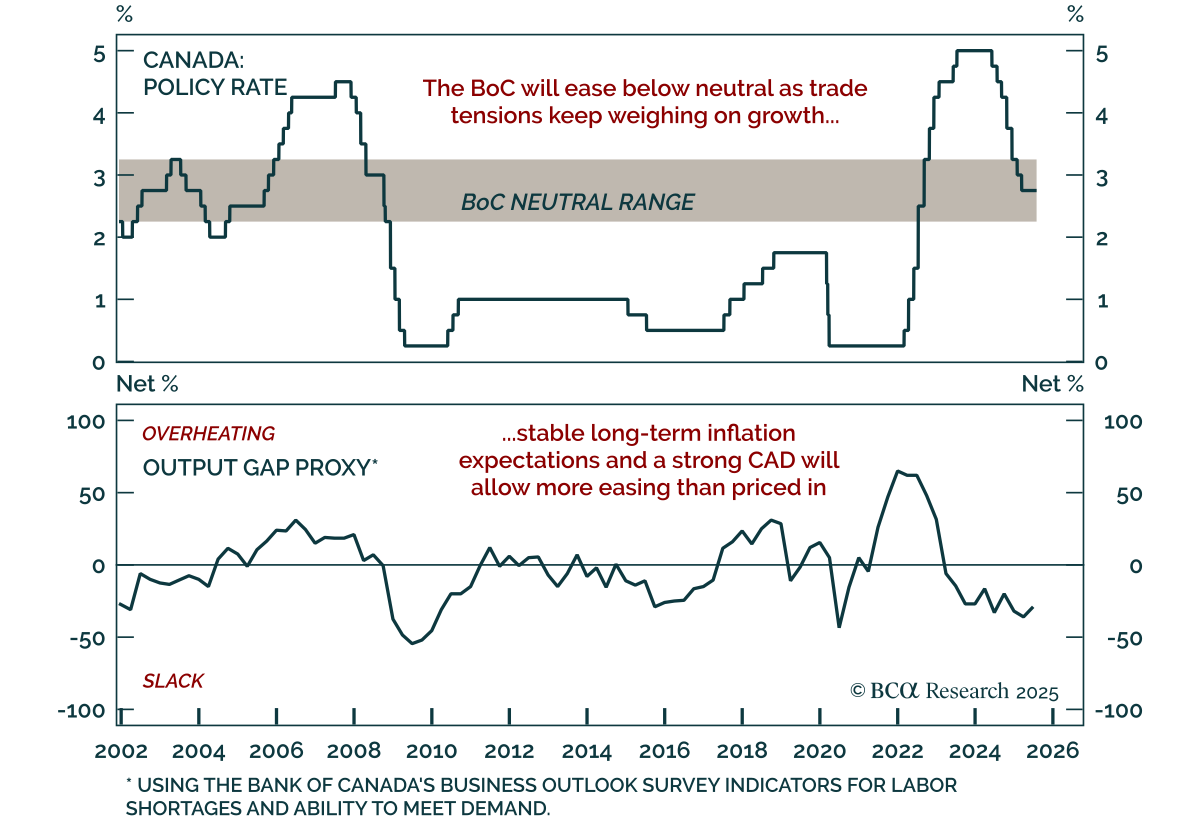

The BoC held rates at 2.75% for a third consecutive meeting, but a weak growth outlook and contained inflation reinforce our overweight in Canadian bonds. With policy within the 2.25%–3.25% neutral range, the BoC remains comfortable waiting for clarity…

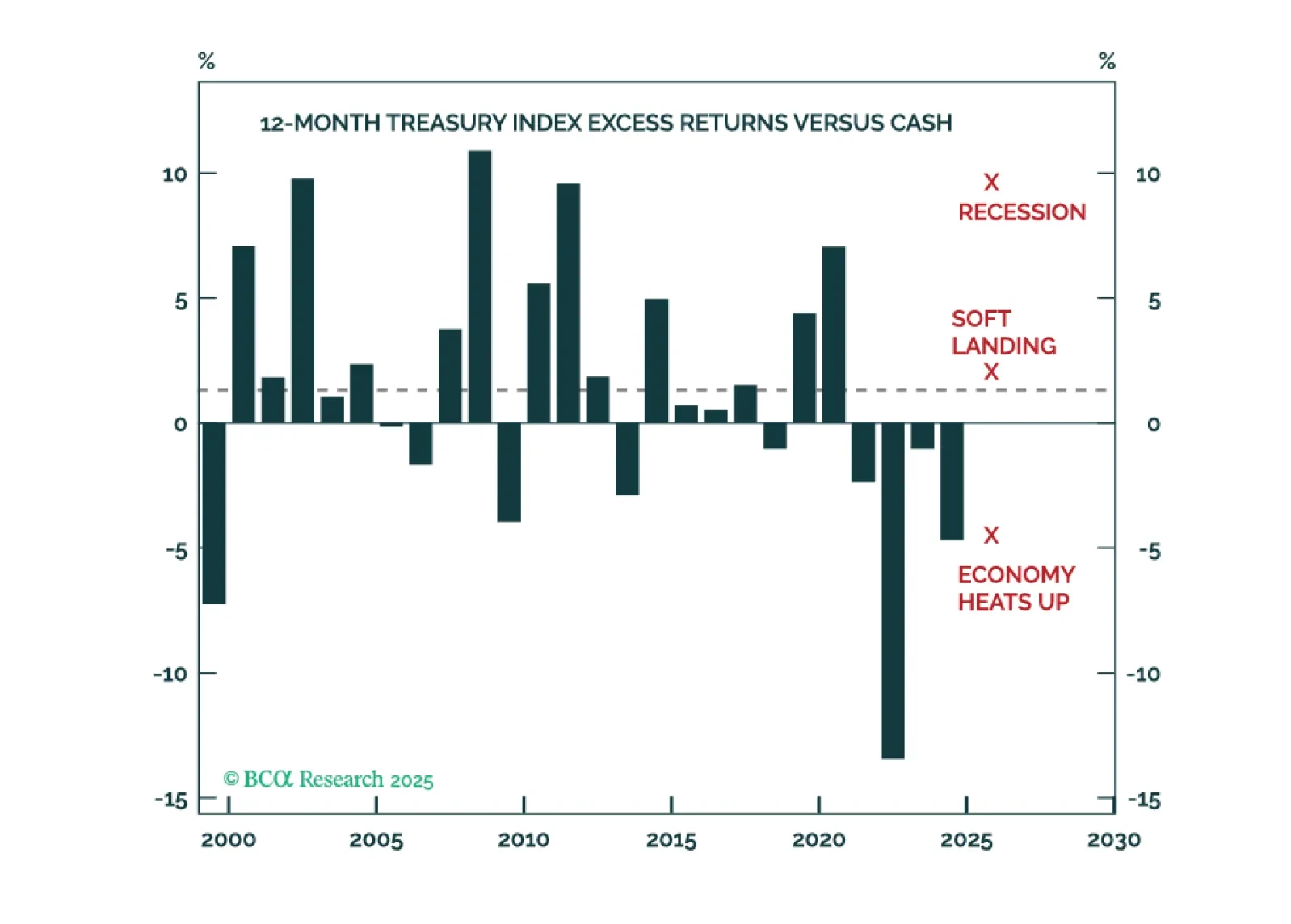

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

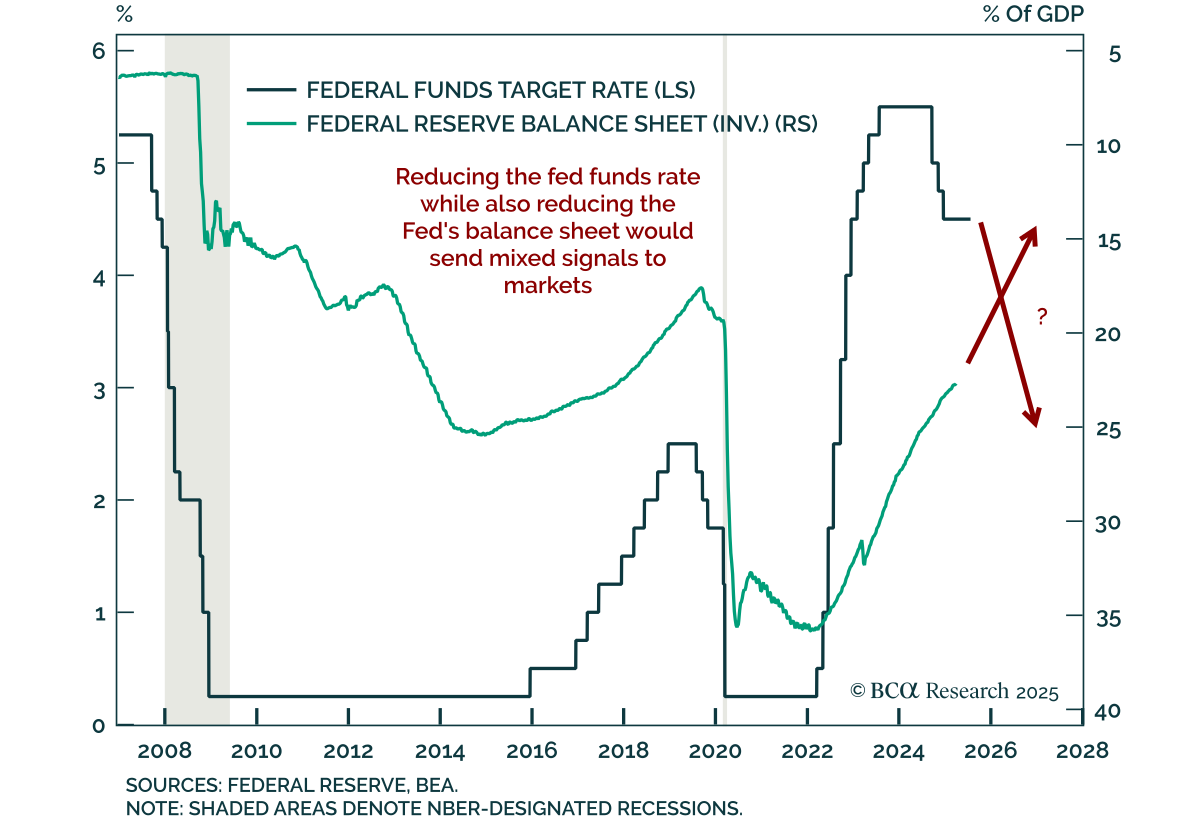

Recent criticism of the Fed centers on post-GFC policy, but proposed solutions would risk policy incoherence and higher long-end yields. Criticism covers the Fed’s reliance on balance sheet policies aimed at easing financial conditions after hitting the…

The Japan-US trade deal removes short-term uncertainty but leaves in place high tariffs. The deal imposes a 15% tariff on most Japanese exports, lower than the previously threatened 25% on autos, and includes Japanese commitments to purchase Boeing aircraft…

Jay Powell won’t be removed as Fed Chair before the expiry of his term next May, but we will learn the identity of his replacement this year, setting up a potentially awkward “shadow Fed Chair” situation.

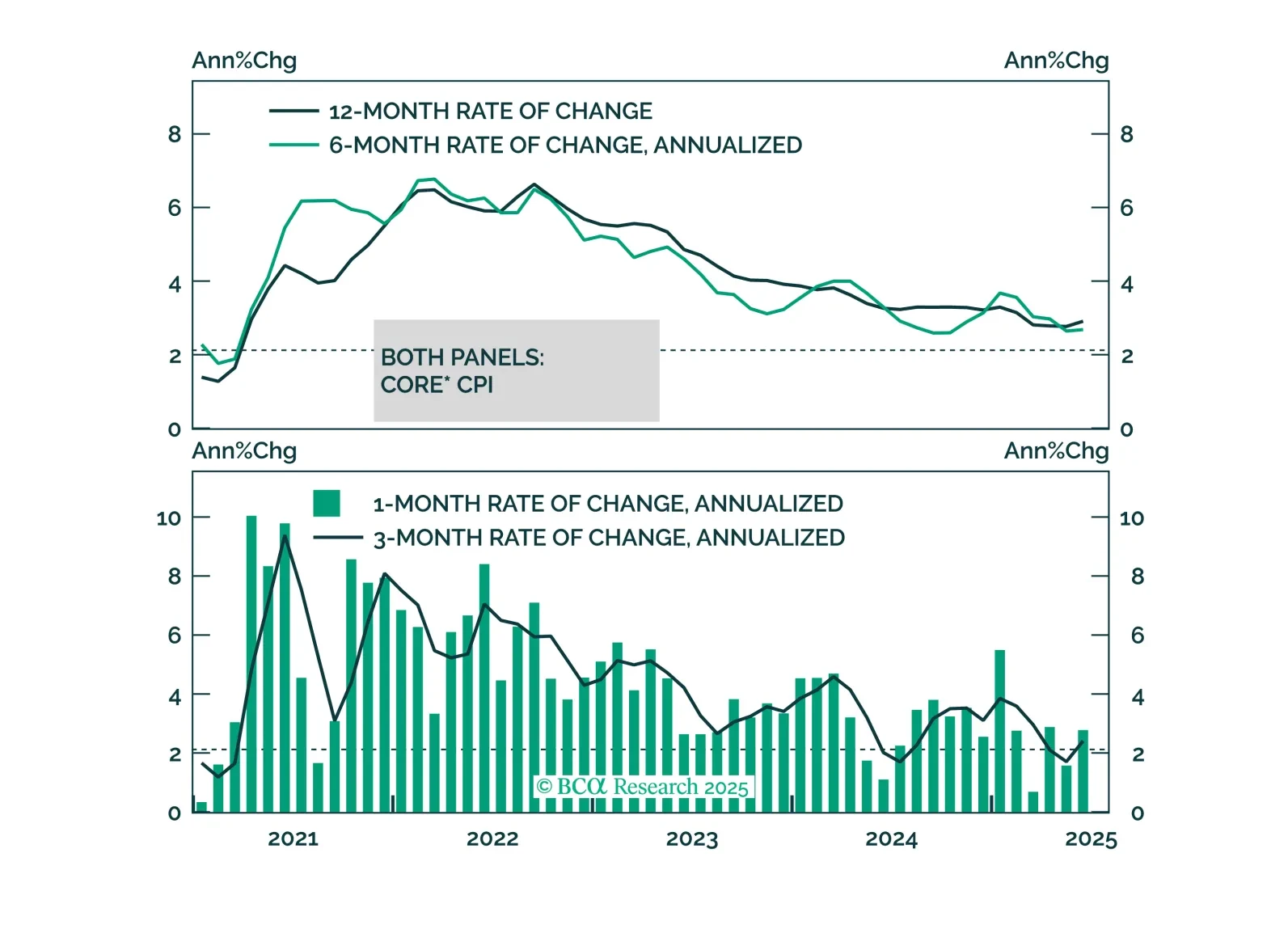

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.

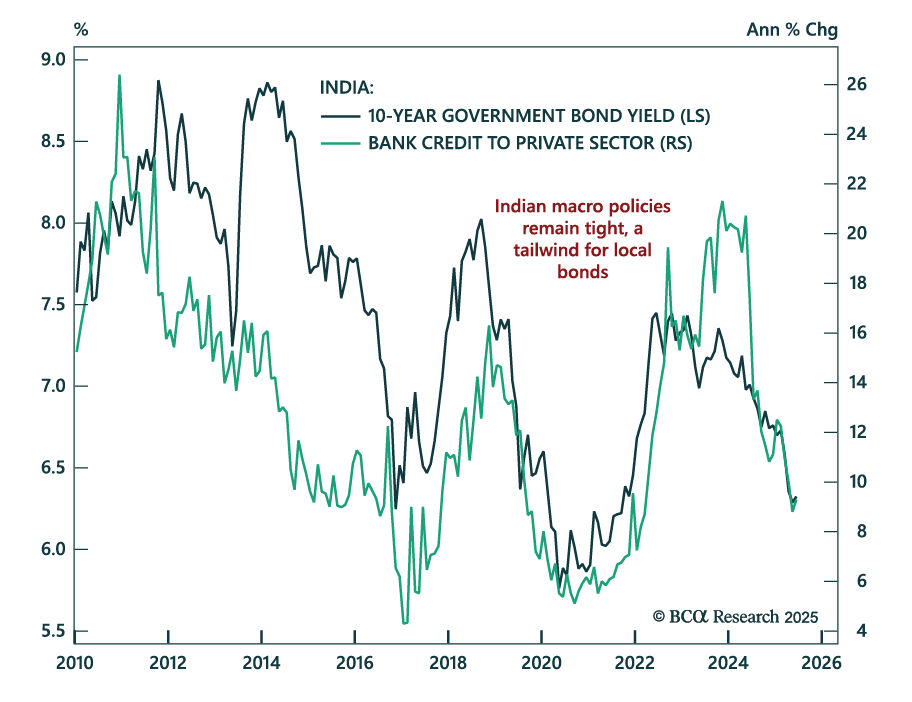

With inflation at a six-year low and restrictive policy weighing on growth, our EM strategists remain long Indian bonds and underweight equities. Headline CPI fell to 2.1% y/y, largely driven by lower food prices, bringing inflation to the lower bound of the…