Fixed Income

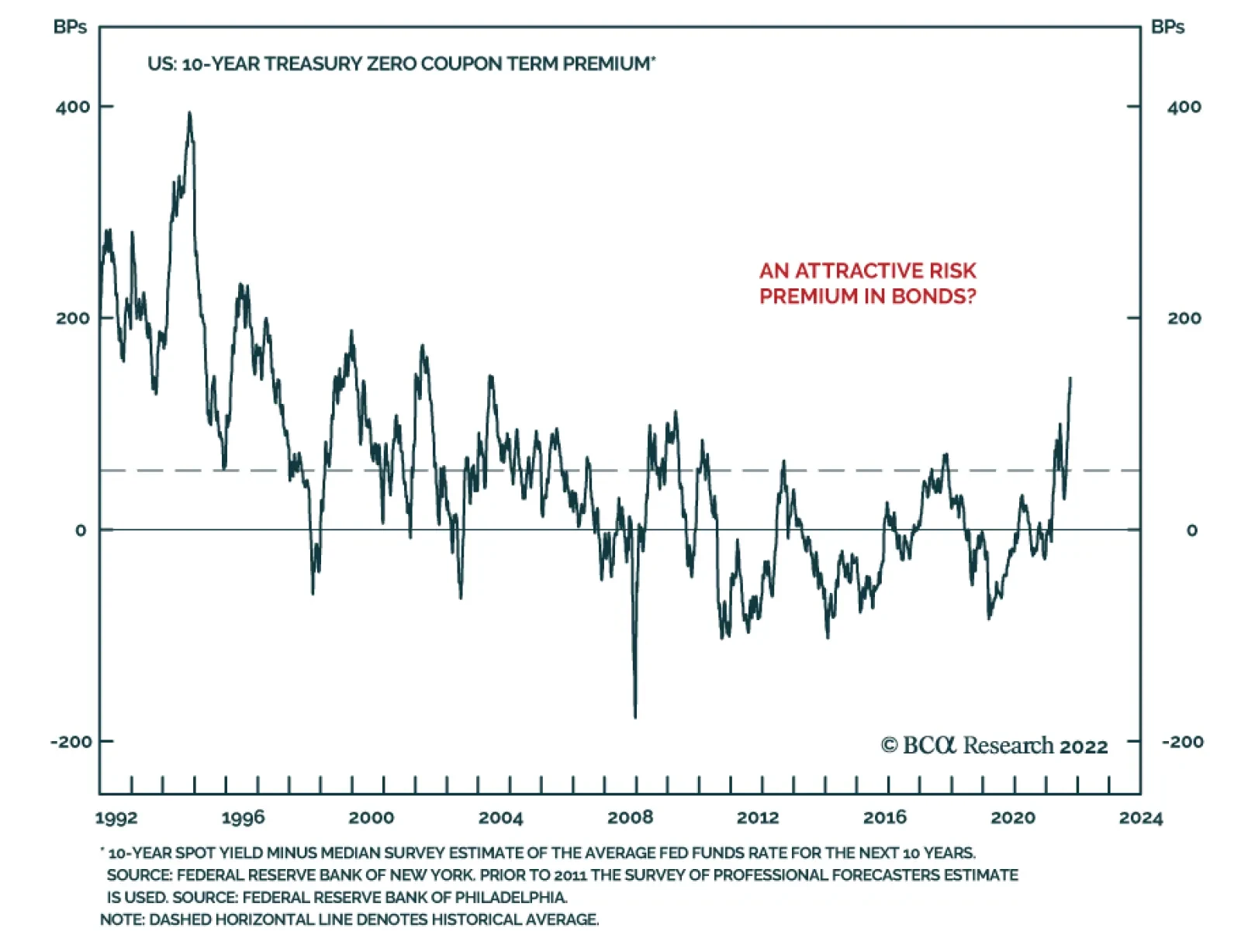

This week’s report takes a look at risk-adjusted return opportunities in US spread product.

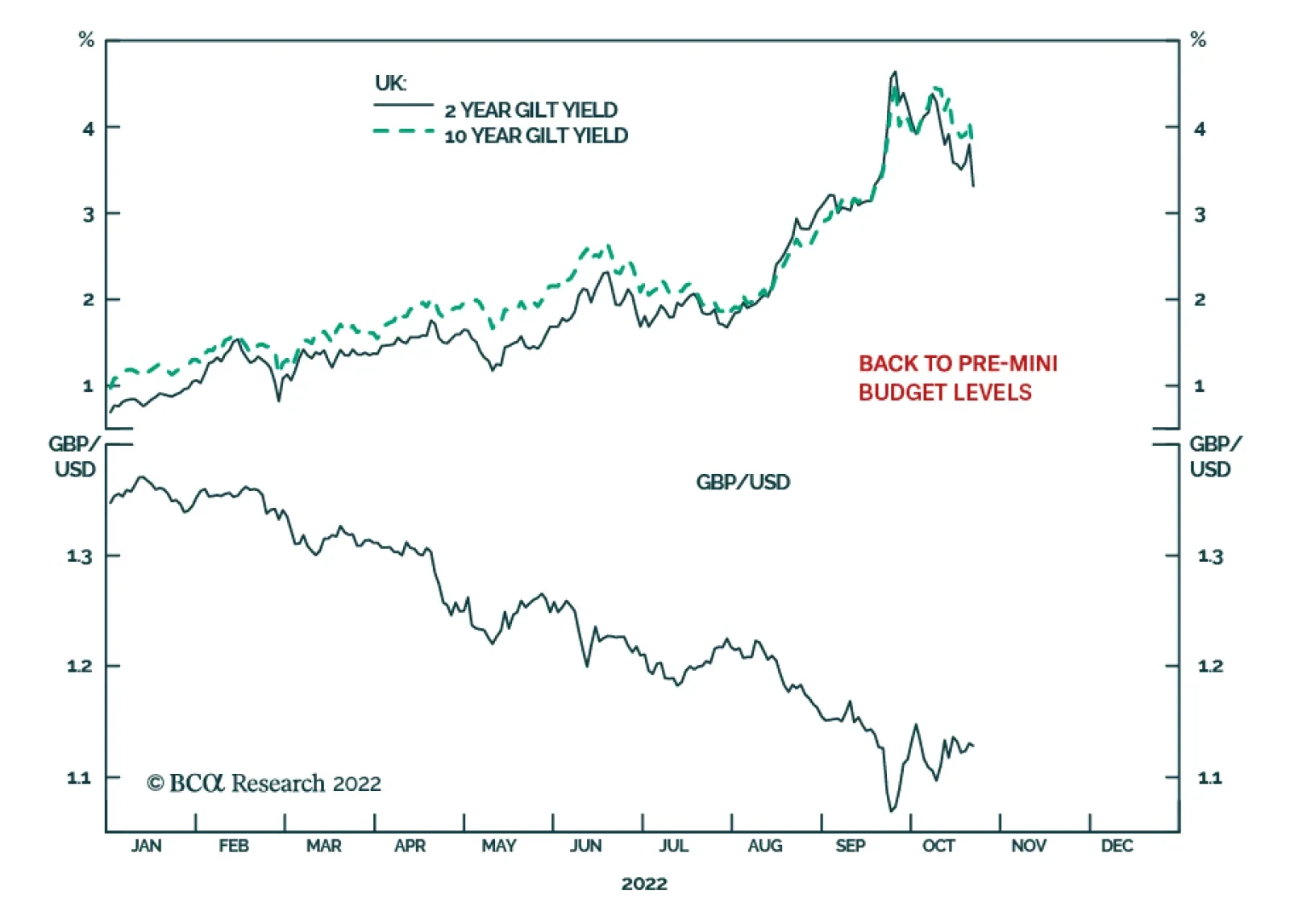

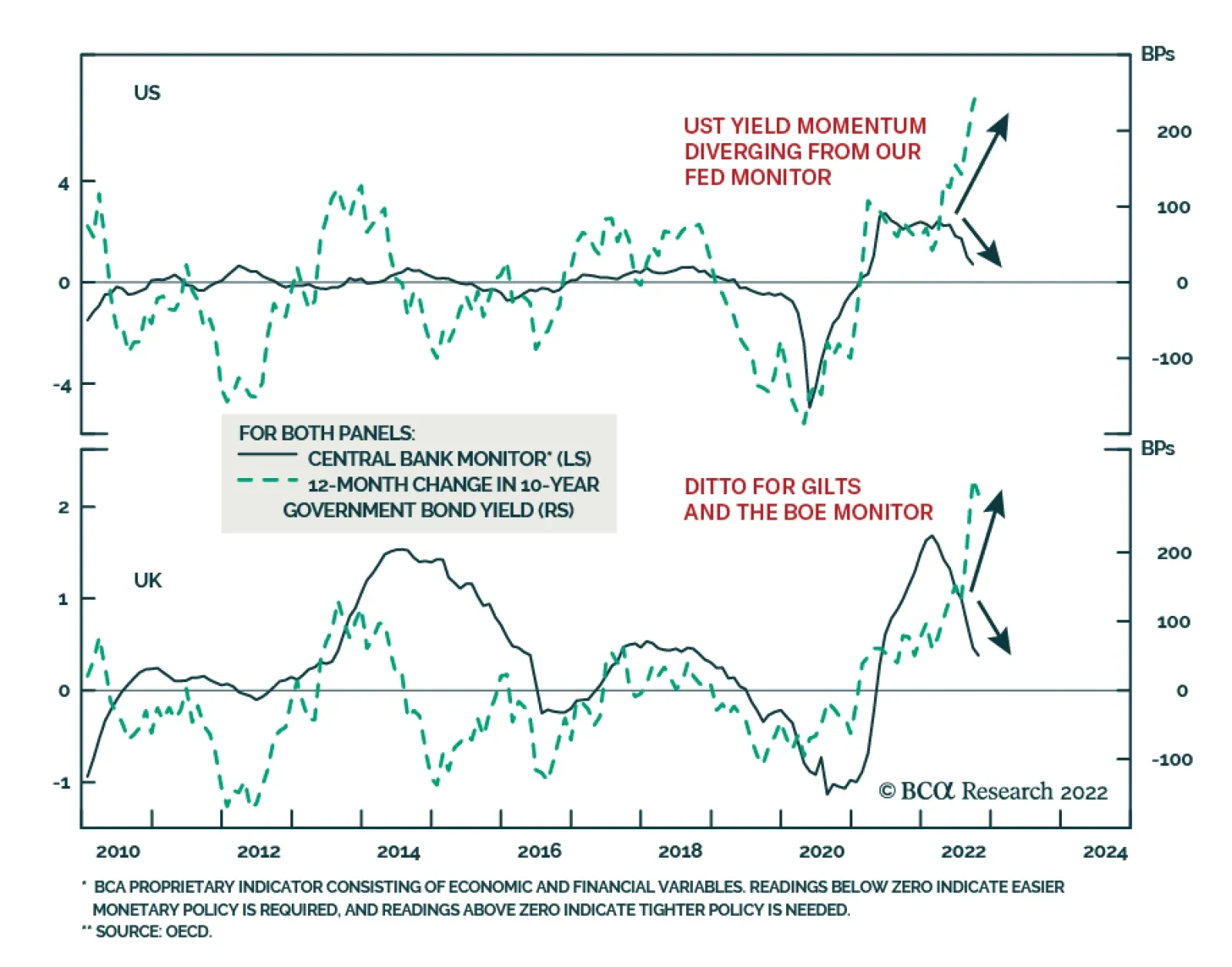

Is the US in a wage-price inflation spiral that could lead to more aggressive Fed rate hikes? Is it time to buy UK Gilts after a wild month of volatility? We answer "no" to both questions, as we discuss in this week’s report.

The Fed’s tone has taken a decidedly dovish turn during the past week and, despite September’s hot CPI print, there is mounting evidence that a period of disinflation is coming. This makes the case for a pause in the Fed’s tightening cycle in Q1 or Q2 of next year.

The ECB will continue to lift rates due to sticky inflation and a tight labor market. Will it be enough to push long-term German yields higher?

The kinked Phillips curve not only explains why inflation surged last year but makes a number of surprising predictions, chief of which is that inflation could fall significantly over the coming months without a major increase in the unemployment rate. In the near term, that is bullish for stocks.

BCA’s Emerging Markets Strategy team’s view remains that US inflation will prove to be sticky. That said, in this report, we examine under what conditions a considerable drop in US core inflation, whenever it transpires, would be bullish for stocks. Potentially significant US disinflation would be bullish for stocks if it is due to an improvement in supply-side dynamics, but bearish if it is demand driven.