Fixed Income

Is the BoE’s emergency intervention in its bond market a British idiosyncrasy that global investors can ignore? No, the UK’s near death experience sends three salutary warnings, with implications for all investors.

Our preferred tactical global fixed income trades for the rest of 2022 into early 2023 are all expressions of our views on relative monetary policy shifts within the main developed market economies. These involve bets on a relatively more hawkish Fed and Bank of England versus a relatively more dovish ECB and Bank of Canada, while also betting on additional selling pressure on Italian government bonds.

We continue to anticipate that the Fed won’t pause its tightening cycle until Q1 or Q2 of 2023, and current labor market trends certainly give no indication that a Fed pause (or “pivot”) is imminent.

In this report, we elaborate on why the Chinese central government has been reluctant to open stimulus taps as much as in the past, especially when it comes to the ailing property market. In recent years, there has been a major shift in Beijing’s assessment of the trade-offs between short-term economic growth, sociopolitical stability and the nation's long-term goals. We explain this difficult balancing act, little-known in the global investment community.

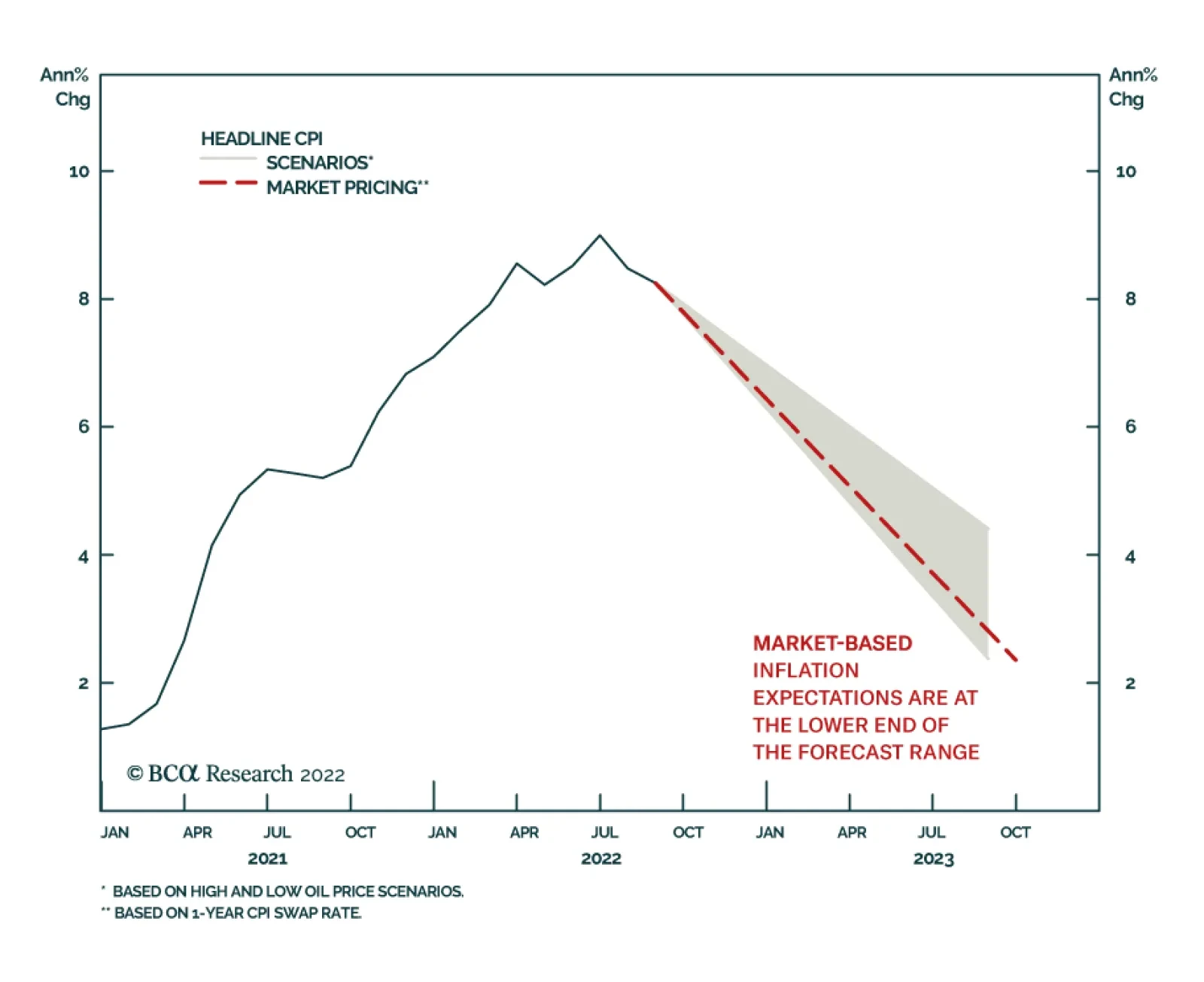

The Fed says that to get back to 2 percent inflation, the US unemployment rate must increase by ‘just’ 0.6 percent through 2023-24. All well and good you might think, except that the Fed is forecasting something that has been unachievable for at least 75 years! Is the Fed gaslighting us? And what does it mean for investment strategy?

This week, we present our quarterly review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for Q3/2022. We also discuss the model portfolio’s expected performance over next 3-6 months after our recent moves to reduce overall duration exposure and increase the underweight to US Treasuries.

This week we present our Portfolio Allocation Summary for October 2022.

The BoE is the key to arrest the meltdown in UK assets, but will the malaise engulfing London only end up traveling to Rome?