Fixed Income

Please note that there will no US Bond Strategy publication next week. Our regular publishing schedule will resume on September 6th with our Portfolio Allocation Summary for September. Executive Summary This report describes a framework for implementing long/short positions in the TIPS market relative to duration-matched nominal Treasuries. The framework is modeled after the Golden Rule of Bond Investing that we use to implement portfolio duration trades. The TIPS Golden Rule states that investors should buy TIPS versus nominal Treasuries when their 12-month headline inflation expectations are above those priced into the market, and vice-versa. We demonstrate a method for forecasting headline CPI inflation and conclude that it will fall into a range of 2.4% to 4.8% during the next 12 months, with risks to the upside. This suggests a high likelihood that headline inflation will exceed current market expectations. The TIPS Golden Rule’s Track Record

The TIPS Golden Rule's Track Record

The TIPS Golden Rule's Track Record

Bottom Line: We see value in TIPS on a 12-month investment horizon but anticipate that an even better entry point to get long TIPS versus nominal Treasuries will emerge during the next couple of months as headline CPI weakens. We recommend a neutral allocation to TIPS for now, though we are looking for a good opportunity to increase exposure. Feature Regular readers will no doubt be familiar with our Golden Rule Of Bond Investing, the framework we use to think about our portfolio duration recommendations. In brief, the Golden Rule states that investors should set their overall bond portfolio duration based on how their own 12-month fed funds rate expectations differ from the expectations that are priced into the market. Our research shows that this investment strategy has a strong historical track record.1 The thing we like most about the Golden Rule framework is that it provides us with a good method for filtering incoming information. Does this new piece of news or economic data change our 12-month rate expectations? If not, then we probably don’t want to assign much weight to it when setting our portfolio duration. In this Special Report we demonstrate that the same Golden Rule logic that we apply to duration trading can also be applied to the TIPS market. Specifically, it can be applied to long/short positions in TIPS versus duration-matched nominal Treasuries. Developing The TIPS Golden Rule Before diving into the TIPS Golden Rule, it’s worth running through the logic that underpins this investment strategy. The logic starts with the Fisher Equation – the well-known formula that relates nominal bond yields to real bond yields. Simply, the Fisher Equation can be stated as follows: Nominal Yield = Real Yield + The Cost Of Inflation Protection In financial market terms, we can re-write the equation as: Nominal Treasury Yield = TIPS Yield + TIPS Breakeven Inflation Rate Two of the three variables in this equation have what we call valuation anchors. The nominal Treasury yield’s valuation is anchored by expectations about the future path for the federal funds rate. Put differently, if you buy a 5-year Treasury note and hold it until maturity, your excess returns versus a position in cash are purely determined by the path of the federal funds rate over that 5-year investment horizon. Similarly, the TIPS breakeven inflation rate’s valuation is anchored by expectations about CPI inflation. If held to maturity, the profits from an inflation protection position (long TIPS/short nominals or short TIPS/long nominals) are purely determined by the path of CPI inflation during the investment horizon. It’s worth noting that, unlike the nominal Treasury yield and the TIPS breakeven inflation rate, the TIPS yield has no independent valuation anchor. Within our framework, the best way to forecast the TIPS yield is to follow a 3-step process: Forecast the nominal yield based on a view about the fed funds rate. Forecast the TIPS breakeven inflation rate based on a view about inflation. Use the Fisher Equation to combine the results from steps 1 and 2 into a forecast for the TIPS yield. As an aside, while our framework relies on viewing the nominal Treasury yield and the TIPS breakeven inflation rate as reflective of expectations for the fed funds rate and CPI inflation respectively, we do not argue that those bond yields can be used to accurately forecast the fed funds rate or CPI inflation. In fact, history tells us that bond markets are usually poor predictors of future outcomes for the fed funds rate and for CPI inflation. Chart 1 shows that there is only a loose correlation (R2 = 22%) between 12-month bond-market implied expectations for the change in the fed funds rate and the actual change in the fed funds rate. Similarly, Chart 2 shows that there is hardly any correlation (R2 = 3%) between market-implied inflation expectations and the 12-month rate of change in headline CPI. Chart 1Market Prices Are A Poor Predictor Of The Fed Funds Rate

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Chart 2Market Prices Are A Poor Predictor Of Inflation

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

In other words, it’s more advisable to view the expectations priced into bond markets as a breakeven threshold for trading, not as a tool for forecasting. Stating The TIPS Golden Rule To apply the TIPS Golden Rule, investors should follow these three steps: Calculate market-implied expectations for what headline CPI inflation will be over the next 12 months. This can be done by looking at the 1-year CPI swap rate or the 1-year TIPS breakeven inflation rate.2 Develop an independent forecast for 12-month headline CPI inflation. We demonstrate one method for doing this later in the report.3 Compare your own headline CPI forecast with the forecast that is priced in the market. If your own forecast is higher, then you should go long TIPS/short nominal Treasuries. If your own forecast is lower, then you should go short TIPS/long nominal Treasuries. Testing The TIPS Golden Rule Chart 3 shows the historical track record of the TIPS Golden Rule going back to 2005.4 The top panel shows 12-month excess returns from the Bloomberg Barclays TIPS index relative to a duration-matched position in nominal Treasuries. The bottom panel shows whether inflation surprised market expectations to the upside or to the downside during the investment horizon. We can see that, visually, it looks as though TIPS tend to outperform nominal Treasuries when there is an inflationary surprise and underperform when there is a deflationary surprise. Chart 3The TIPS Golden Rule's Track Record

The TIPS Golden Rule's Track Record

The TIPS Golden Rule's Track Record

Chart 4 shows the same relationship in a little more detail. The 12-month inflation surprise is placed on the x-axis and 12-month TIPS excess returns are on the y-axis. For the TIPS Golden Rule to be useful, we would need to see most of the datapoints in the top-right and bottom-left quadrants of the chart, and indeed this is the case. Chart 412-Month TIPS Excess Returns Vs. Inflation Surprises

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Finally, Table 1 shows the relationship in even more detail. It shows that inflationary surprises coincide with positive TIPS excess returns 73% of the time for an average excess return of 2.6%. It also shows that deflationary surprises coincide with negative TIPS excess returns 80% of the time, for an average excess return of -3.2%. Table 112-Month TIPS Excess Returns* And Inflation Surprises (2005 – Present)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Please note that all the above return calculations are performed on the overall Bloomberg Barclays TIPS Index relative to a duration-matched position in nominal Treasuries. However, the TIPS Golden Rule also performs well when applied to TIPS of any maturity. The Appendix of this report replicates the above analysis for every point along the TIPS curve and shows that the results are consistently excellent. Applying The TIPS Golden Rule Now that we have stated the TIPS Golden Rule and demonstrated its effectiveness as an investment strategy, it is time to apply it to the current market. To do that, we first determine 1-year market-implied inflation expectations by looking at the 1-year CPI swap rate. As of last Friday’s close, the 1-year CPI swap rate is 3.16%. This means that if we think headline CPI inflation will be above 3.16% during the next 12 months, then we should go long TIPS versus duration-matched nominal Treasuries. If we think headline CPI inflation will come in below 3.16% during the next 12 months, then we should go short TIPS versus duration-matched nominal Treasuries. Next, we must build up our own forecast of headline CPI inflation for the next 12 months. To do this, we follow a bottom-up approach where we split the CPI basket into five components (energy, food, shelter, core goods, and core services ex. shelter) and model each one individually. Energy Inflation (9% Of Headline CPI) Chart 5Modeling Energy Inflation

Modeling Energy Inflation

Modeling Energy Inflation

Energy accounts for roughly 9% of headline CPI, though its often violent price swings mean that this component usually accounts for a much larger percentage of the volatility in headline CPI. In practice, we can accurately model Energy CPI using the prices of retail gasoline, natural gas, and heating oil (Chart 5). To get a 12-month forecast for Energy CPI we therefore need forecasts for the prices of retail gasoline, natural gas, and heating oil. In this analysis, we will consider two possible scenarios for energy prices. First, a benign ‘low oil price’ scenario where we assume that the prices of retail gasoline, natural gas and heating oil follow the paths discounted in their respective futures curves. Second, we consider a ‘high oil price’ scenario that incorporates the view of our Commodity & Energy Strategy service that a drop in Russian oil supply, among other factors, will cause the Brent crude oil price to reach $119 per barrel by the end of this year and average $117 per barrel in 2023.5 To incorporate this outlook into our model, we regress the prices of retail gasoline, natural gas and heating oil on the Brent crude oil price and extrapolate forward using our commodity strategists’ forecasts. The ‘low oil price’ scenario has Energy CPI inflation falling from its current 32.9% level all the way down to -9.9% during the next 12 months. In contrast, our ‘high oil price’ scenario has it falling to just 15.8%. Food Inflation (13% Of Headline CPI) Chart 6Modeling Food Inflation

Modeling Food Inflation

Modeling Food Inflation

Our Food CPI model is based on the cost of fertilizer, agricultural commodity prices and diesel prices. This model has done a reasonably good job explaining trends in Food CPI inflation over time, but the last few months have seen food inflation jump well above the levels suggested by our model (Chart 6). Given that the inputs to our Food CPI model are highly correlated with the oil price, we also apply the ‘low oil price’ and ‘high oil price’ scenarios discussed above to our Food CPI forecast. Using this method, the ‘low oil price’ scenario has Food CPI inflation falling to 3.8% during the next 12 months and the ‘high oil price’ scenario has it coming down to 4.2%. One key risk to these forecasts is that they both assume that the current gap between food inflation and our model’s fair value will close. It’s possible that other factors not included in our model could prevent the gap from closing. We therefore consider our Food CPI forecast to be quite optimistic. Core Goods Inflation (21% Of Headline CPI) Chart 7Modeling Goods Inflation

Modeling Goods Inflation

Modeling Goods Inflation

Core goods inflation, currently running at 6.9%, appears to have already peaked following its post-pandemic surge. We model Core Goods CPI using the New York Fed’s Global Supply Chain Pressure Index, as it is the supply chain constraints that arose during the pandemic that explain the bulk of the movement in core goods prices since that time (Chart 7).6 To forecast Core Goods CPI, we assume that global supply chain constraints continue to ease and that the New York Fed’s index reverts to its pre-pandemic level during the next 12 months. This gives us a forecast for 12-month Core Goods CPI inflation of 0%. Shelter Inflation (32% Of Headline CPI) Chart 8Modeling Shelter Inflation

Modeling Shelter Inflation

Modeling Shelter Inflation

We model shelter inflation, currently running at 5.6%, using the unemployment rate, rental vacancy rate and home prices (Chart 8). Except for the unemployment rate, all our model’s independent variables enter with a lag of at least 12 months. In other words, we wouldn’t expect any near-term change in home prices to impact Shelter CPI for at least a year. To forecast Shelter CPI, we assume that the unemployment rate rises to 4% during the next 12 months. This results in a shelter inflation forecast of 4.7% for the next 12 months. Much like with food inflation, we tend to view this forecast as relatively optimistic as it assumes a large reversion from the current rate of shelter inflation back to our model’s fair value. It’s conceivable that other factors not included in our model, such as rapid wage growth, could prevent this reversion from occurring. Services ex. Shelter Inflation (24% Of Headline CPI) Chart 9Modeling Services Inflation

Modeling Services Inflation

Modeling Services Inflation

This final component of CPI is a bit of a hodgepodge of different service industries that may not have much in common. However, we find that wage growth does a good job of tracking its trends (Chart 9). We therefore model Services ex. Shelter CPI using the Employment Cost Index, which enters our model with a 10 month lag. To forecast Services ex. Shelter CPI, we assume that the Employment Cost Index holds steady at its current growth rate. This gives us a Services ex. Shelter CPI inflation forecast of 5.5% for the next 12 months. Combining Our Bottom-Up Inflation Forecasts & Investment Conclusions Combining our bottom-up forecasts, we calculate a 12-month headline CPI inflation rate of 2.4% for the ‘low oil price’ scenario and a rate of 4.8% for the ‘high oil price’ scenario. For core CPI inflation, we calculate a 12-month forecast of 3.6%. Given the optimistic assumptions that we incorporated into our forecasts, particularly the large reversions of food and shelter inflation back to our estimated fair value levels, we view the risks to our forecasts as heavily tilted to the upside. We also acknowledge that the re-normalization of global supply chains may not proceed as smoothly as the scenario that is baked into our forecasts. Any hiccup in that process would cause our goods inflation forecast to be too low. Chart 10Inflation Forecasts

Inflation Forecasts

Inflation Forecasts

Chart 10 shows our 12-month headline and core CPI forecasts alongside the market-implied forecast from the CPI swap curve, currently 3.16%. Notice that the market-implied inflation forecast is much closer to the bottom-end of our range of headline CPI estimates, and we have already acknowledged that a lot of things will have to go right for our estimates to pan out. In other words, we see a high likelihood that 12-month headline CPI will be above 3.16% for the next 12 months which, according to our TIPS Golden Rule, tells us that we should go long TIPS versus duration-matched nominal Treasuries. While we acknowledge that there is likely some value in going long TIPS versus nominal Treasuries today, we are inclined to maintain our recommended neutral allocation to TIPS versus nominals for now. Given the recent drop in oil prices, we anticipate further weakness in headline inflation during the next couple of months. This could push TIPS breakeven inflation rates even lower in the near term, creating even more value. The bottom line is that we see attractive value in TIPS versus nominal Treasuries on a 12-month investment horizon. While we maintain a neutral allocation to TIPS for now, we anticipate turning more bullish in the near future, hopefully from a better entry point after one or two more weak CPI prints. Appendix Chart A112-Month TIPS Excess Returns Vs. Inflation Surprises (1-3 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Table A112-Month TIPS Excess Returns* And Inflation Surprises (1-3 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Chart A212-Month TIPS Excess Returns Vs. Inflation Surprises (3-5 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Table A212-Month TIPS Excess Returns* And Inflation Surprises (3-5 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Chart A312-Month TIPS Excess Returns Vs. Inflation Surprises (5-7 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Table A312-Month TIPS Excess Returns* And Inflation Surprises (5-7 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Chart A412-Month TIPS Excess Returns Vs. Inflation Surprises (7-10 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Table A412-Month TIPS Excess Returns* And Inflation Surprises (7-10 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Chart A512-Month TIPS Excess Returns Vs. Inflation Surprises (10-15 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Table A512-Month TIPS Excess Returns* And Inflation Surprises (10-15 Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Chart A612-Month TIPS Excess Returns Vs. Inflation Surprises (15+ Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Table A612-Month TIPS Excess Returns* And Inflation Surprises (15+ Year Maturities)

The Golden Rule Of TIPS Investing

The Golden Rule Of TIPS Investing

Ryan Swift US Bond Strategist rswift@bcaresearch.com Robert Timper Research Analyst robert.timper@bcaresearch.com Footnotes 1 Please see US Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018. 2 In this report we use the 1-year CPI swap rate because it is easier to access. 3 To make the TIPS Golden Rule easy to implement, we use seasonally adjusted headline CPI for all our calculations even though TIPS are technically linked to the non-seasonally adjusted index. We also ignore the fact that TIPS coupons adjust to CPI releases with a lag. Our analysis shows that the rule works very well even without incorporating these complications. 4 CPI swap rates are only available from 2004 onwards, so this is the largest historical sample we can use. 5 Please see Commodity & Energy Strategy Weekly Report, “EU Russian Oil Embargoes, Higher Prices”, dated August 18, 2022. 6 For more details on the Global Supply Chain Pressure Index: https://www.newyorkfed.org/research/policy/gscpi#/overview Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

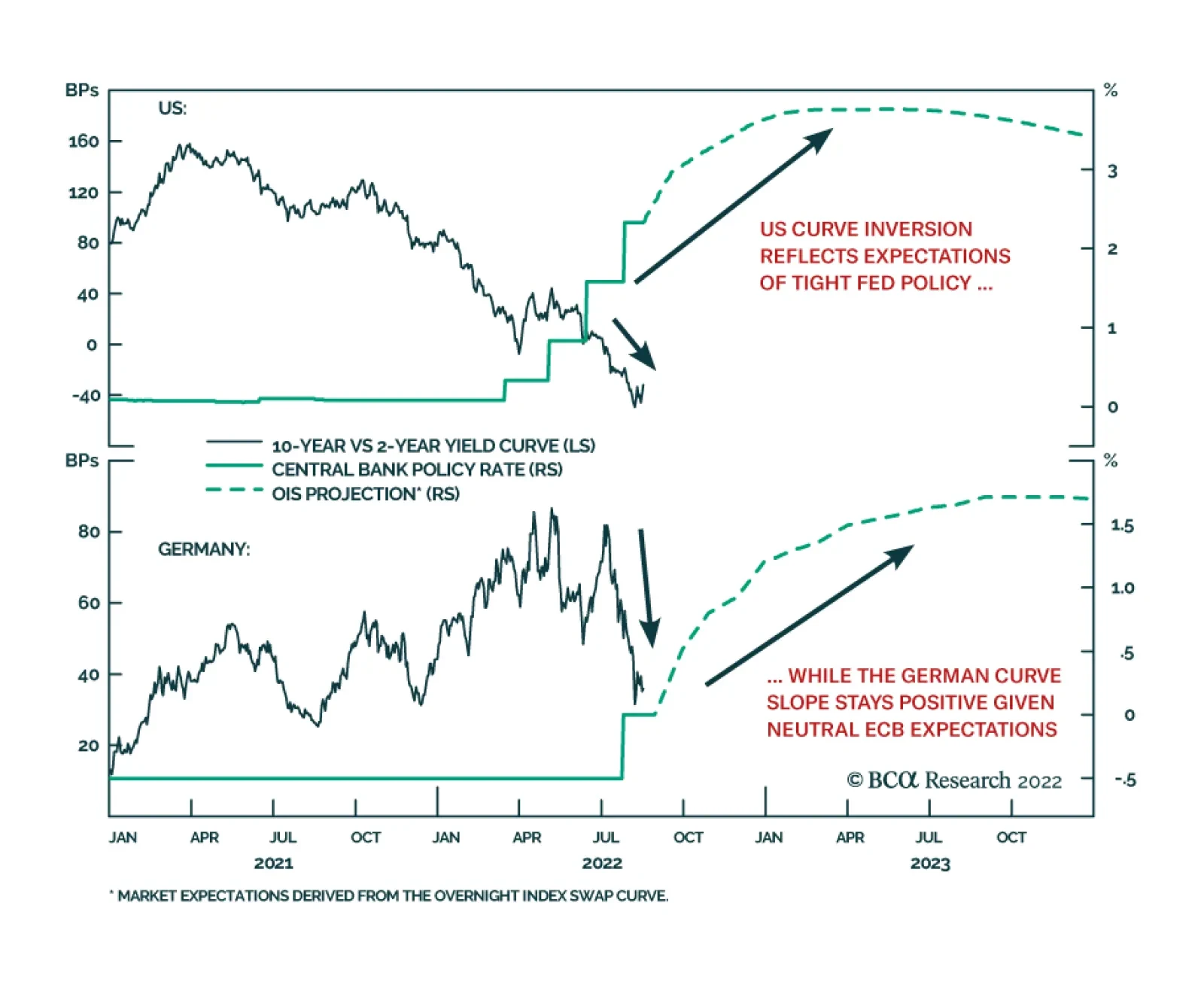

As of Thursday’s close, the 2-year/10-year US Treasury curve is inverted, with the 10-year yield trading -35bps below the 2-year yield. In Europe, there is no inversion, with the 10-year German yield trading 37bps above the 2-year yield. Why the…

Dispatches From The Future: From Goldilocks To President DeSantis

Listen to a short summary of this report. Executive Summary Back From The Future: An Investor’s Almanac

Dispatches From The Future: From Goldilocks To President DeSantis

Dispatches From The Future: From Goldilocks To President DeSantis

Stocks will rally over the next six months as recession risks abate but then begin to swoon as it becomes clear the Fed will not cut rates in 2023. A second wave of inflation will begin in mid-2023, forcing the Fed to raise rates to 5%. The 10-year US Treasury yield will rise above 4%. While financial conditions are currently not tight enough to induce a recession, they will be by the end of next year. In the past, the US unemployment rate has gone through a 20-to-22 month bottoming phase. This suggests that a recession will start in early 2024. The US dollar will soften over the next six months but then get a second wind as the Fed is forced to turn hawkish again. Over the long haul, the dollar will weaken, reflecting today’s extremely stretched valuations. Bottom Line: Investors should remain tactically overweight global equities but look to turn defensive early next year. Somewhere in Hilbert Space I have long believed that anything that can possibly happen in financial markets (as well as in life) will happen. Sometimes, however, it is useful to focus on a “base case” or “modal” outcome of what the world will look like. In this week’s report, we do just that, describing the evolution of the global economy from the perspective of someone who has already seen the future unfold. September 2022 – Goldilocks! US headline inflation continues to decline thanks to lower food and gasoline prices (Chart 1). Supply-chain bottlenecks ease, as evidenced by falling transportation costs and faster delivery times (Chart 2). Most measures of economic activity bottom out and then begin to rebound. The surge in bond yields earlier in 2022 pushed down aggregate demand, but with yields having temporarily stabilized, demand growth returns to trend. The S&P 500 moves up to 4,400. Chart 1ALower Food And Gasoline Prices Will Drag Down Headline Inflation (I)

Lower Food And Gasoline Prices Will Drag Down Headline Inflation (I)

Lower Food And Gasoline Prices Will Drag Down Headline Inflation (I)

Chart 1BLower Food And Gasoline Prices Will Drag Down Headline Inflation (II)

Lower Food And Gasoline Prices Will Drag Down Headline Inflation (II)

Lower Food And Gasoline Prices Will Drag Down Headline Inflation (II)

October 2022 – Europe’s Prospects of Avoiding a Deep Freeze Improve: Economic shocks are most damaging when they come out of the blue. With about half a year to prepare for a cut-off of Russian gas, the EU responds with uncharacteristic haste: Coal-fired electricity production ramps up; the planned closure of Germany’s nuclear power plants is postponed; the French government boosts nuclear capacity, which had been running at less than 50% earlier in 2022; and, for its part, the Dutch government agrees to raise output from the massive Groningen natural gas field after the EU commits to establishing a fund to compensate the surrounding community for any damage from increased seismic activity. EUR/USD rallies to 1.06. November 2022 – Divided Congress and Trump 2.0: In line with pre-election polling, the Democrats retain the Senate but lose the House (Chart 3). Markets largely ignore the outcome. To no one’s surprise, Donald Trump announces his candidacy for the 2024 election. Over the following months, however, the former president has trouble rekindling the magic of his 2016 bid. His attacks on his main rival, Florida governor Ron DeSantis, fall flat. At one rally in early 2023, Trump’s claim that “Ron is no better than Jeb” is greeted with boos. Chart 2Supply-Chain Pressures Are Easing

Supply-Chain Pressures Are Easing

Supply-Chain Pressures Are Easing

Chart 3Democrats Will Lose The House But Retain The Senate

Dispatches From The Future: From Goldilocks To President DeSantis

Dispatches From The Future: From Goldilocks To President DeSantis

December 2022 – China’s “At Least One Child Policy”: The 20th Party Congress takes place against the backdrop of strict Covid restrictions and a flailing housing market. In addition to reaffirming his Common Prosperity Initiative, President Xi stresses the need for actions that promote “family formation.” The number of births declined by nearly 30% between 2019 and 2021 and all indications suggest that the birth rate fell further in 2022 (Chart 4). Importantly for investors, Xi says that housing policy should focus not on boosting demand but increasing supply, even if this comes at the expense of lower property prices down the road. Base metal prices rally on the news. Chart 4China's Baby Bust

China's Baby Bust

China's Baby Bust

January 2023 – Putin Declares Victory: Faced with continued resistance by Ukrainian forces – which now have wider access to advanced western military technology – Putin declares that Russia’s objectives in Ukraine have been met. Following the playbook in Crimea and the Donbass, he orders referenda to be held in Zaporizhia, Kherson, and parts of Kharkiv, asking the local populations if they wish to join Russia. The legitimacy of the referenda is immediately rejected by the Ukrainian government and the EU. Nevertheless, the Russian military advance halts. While the West pledges to maintain sanctions against Russia, the geopolitical risk premium in oil prices decreases. February 2023 – Credit Spreads Narrow Further: At the worst point for credit in early July 2022, US high-yield spreads were pricing in a default rate of 8.1% over the following 12 months (Chart 5). By late August, the expected default rate has fallen to 5.2%, and by January 2023, it has dropped to 4.5%. Perceived default risks decline even more in Europe, where the economy is on the cusp of a V-shaped recovery following the prior year’s energy crunch. Chart 5The Spread-Implied Default Rate Has Room To Fall If Recession Fears Abate

The Spread-Implied Default Rate Has Room To Fall If Recession Fears Abate

The Spread-Implied Default Rate Has Room To Fall If Recession Fears Abate

March 2023 – Wages: The New Core CPI? US inflation continues to drop, but a heated debate erupts over whether this merely reflects the unwinding of various pandemic-related dislocations or whether it marks true progress in cooling down the economy. Those who argue that higher interest rates are cooling demand point to the decline in job openings. Skeptics retort that the drop in job openings has been matched by rising employment (Chart 6). To the extent that firms have been converting openings into new jobs, the skeptics conclude that labor demand has not declined. In a series of comments, Jay Powell stresses the need to focus on wage growth as a key barometer of underlying inflationary pressures. Given that wage growth remains elevated, market participants regard this as a hawkish signal (Chart 7). The 10-year Treasury yield rises to 3.2%. The DXY index, having swooned from over 108 in July 2022 to just under 100 in February 2023, moves back to 102. After hitting a 52-week high of 4,689 the prior month, the S&P 500 drops back below 4,500. Chart 6Drop In Job Openings Is Matched By Rise In Employment

Drop In Job Openings Is Matched By Rise In Employment

Drop In Job Openings Is Matched By Rise In Employment

Chart 7Wage Growth Remains Strong

Wage Growth Remains Strong

Wage Growth Remains Strong

April 2023 – Covid Erupts Across China: After successfully holding back Covid for over three years, the dam breaks. When lockdowns fail to suppress the outbreak, the government shifts to a mitigation strategy, requiring all elderly and unvaccinated people to isolate at home. It helps that China’s new mRNA vaccines, launched in late 2022, prove to be successful. By early 2023, China also has sufficient supplies of Pfizer’s Paxlovid anti-viral drug. Nevertheless, the outbreak in China temporarily leads to renewed supply-chain bottlenecks. May 2023 – Biden Confirms He Will Stand for Re-Election: Saying he is “fit as a fiddle,” President Biden confirms that he will seek a second term in office. Little does he know that the US will be in a recession during most of his re-election campaign. Chart 8Consumer Confidence And Real Wages Tend To Move Together

Consumer Confidence And Real Wages Tend To Move Together

Consumer Confidence And Real Wages Tend To Move Together

June 2023 – Inflation: The Second Wave Begins: The decline in inflation between mid-2022 and mid-2023 sows the seeds of its own demise. As prices at the pump and in the grocery store decline, real wage growth turns positive. Consumer confidence recovers (Chart 8). Household spending, which never weakened that much to begin with, surges. The economy starts to overheat again, leading to higher inflation. After having paused raising rates at 3.5% in early 2023, the Fed indicates that further hikes may be necessary. The DXY index strengthens to 104. The S&P 500 dips to 4,300. July 2023 – Tech Stock Malaise: Higher bond yields weigh on tech stocks. Making matters worse, investors start to worry that many of the most popular US tech names have gone “ex-growth.” The evolution of tech companies often follows three stages. In the first stage, when the founders are in charge, the company grows fast thanks to the introduction of new, highly innovative products or services. In the second stage, as the tech company matures, the founders often cede control to professional managers. Company profits continue to grow quickly, but less because of innovation and more because the professional managers are able to squeeze money from the firm’s customers. In the third stage, with all the low-lying fruits already picked, the company succumbs to bureaucratic inertia. As 2023 wears on, it becomes apparent that many US tech titans are entering this third stage. August 2023 – Long-term Inflation Expectations Move Up: Unlike in 2021-22, when long-term inflation expectations remained well anchored in the face of rising realized inflation, the second inflation wave in 2023 is accompanied by a clear rise in long-term inflation expectations. Consumer expectations of inflation 5-to-10 years out in the University of Michigan survey jump to 3.5%. Whereas back in August 2022, the OIS curve was discounting 100 basis points of Fed easing starting in early 2023, it now discounts rate hikes over the remainder of 2023 (Chart 9). The 10-year yield rises to 3.8%. The 10-year TIPS yield spikes to 1.2%, as investors price in a higher real terminal rate. The S&P 500 drops to 4,200. The financial press is awash with comparisons to the early 1980s (Chart 10). Chart 9The Markets Expect The Fed To Cut Rates By Over 100 Basis Points Starting In 2023

The Markets Expect The Fed To Cut Rates By Over 100 Basis Points Starting In 2023

The Markets Expect The Fed To Cut Rates By Over 100 Basis Points Starting In 2023

Chart 10The Early-1980s Playbook

The Early-1980s Playbook

The Early-1980s Playbook

October 2023 – Hawks in Charge: After a second round of tightening, featuring three successive 50 basis-point hikes, the Fed funds rate reaches a cycle peak of 5%. The 10-year Treasury yield gets up to as high as 4.28%. The 10-year TIPS yield hits 1.62%. The DXY index rises to 106. The S&P 500 falls to 4,050. November 2023 – Housing Stumbles: With mortgage yields back above 6%, the US housing market weakens anew. The fallout from rising global bond yields is far worse in some smaller developed economies such as Canada, Australia, and New Zealand, where home price valuations are more stretched (Chart 11). Chart 11Rising Rates Will Weigh On Developed Economies With Pricey Housing Markets

Rising Rates Will Weigh On Developed Economies With Pricey Housing Markets

Rising Rates Will Weigh On Developed Economies With Pricey Housing Markets

January 2024 – Unemployment Starts to Rise: After moving sideways since March 2022, the US unemployment rate suddenly jumps 0.2 percentage points to 3.6%, with payrolls contracting for the first time since the start of the pandemic. The 22-month stretch of a flat unemployment rate is broadly in line with the historic average (Table 1). Table 1In Past Cycles, The Unemployment Rate Has Moved Sideways For Nearly Two Years Before A Recession Began

Dispatches From The Future: From Goldilocks To President DeSantis

Dispatches From The Future: From Goldilocks To President DeSantis

February 2024 – The US Recession Begins: Although there was considerable debate about whether the US was entering a recession at the time, in early 2025, the NBER would end up declaring that February 2024 marked the start of the recession. The 10-year yield falls back below 4% while the S&P 500 drops to 3,700. Lower bond yields are no longer protecting stocks. March 2024 – The Fed Remains in Neutral: Jay Powell says further rate hikes are unwarranted in light of the weakening economy, but with core inflation still running at 3.5%, the Fed is in no position to ease. April 2024 – The Global Recession Intensifies: The US unemployment rate rises to 4.7%. The economic downdraft is especially sharp in America’s neighbor to the north, where the Canadian housing market is in shambles. Back in June 2022, the Canadian 10-year yield was 21 basis points above the US yield. By April 2024, it is 45 basis points below. Europe and Japan also fall into recession. Commodity prices continue to drop, with Brent oil hitting $60/bbl. May 2024 – The Fed Cuts Rates: Reversing its position from just two months earlier, the Federal Reserve cuts rates for the first time since March 2020, lowering the Fed funds rate from 5% to 4.5%. The Fed funds rate will ultimately bottom at 2.5%, below the range of 3.5%-to-4% that most economists will eventually recognize as neutral. August 2024 – Republican National Convention: Unwilling to spend much of his own money on the campaign, and with most donations flowing to DeSantis, Trump’s bid to reclaim the White House fizzles. While the former president never formally bows out of the race, the last few months of his primary campaign end up being a nostalgia tour of his past accomplishments, interspersed with complaints about all the ways that he has been wronged. In the end, though, Trump makes a lasting imprint on the Republican party. During his acceptance speech, in typical Trumpian style, Ron DeSantis attacks Joe Biden for “eating ice cream while the economy burns” and declares, to thunderous applause, that “Americans are sick and tired of having woke nonsense hurled in their faces and then being dared to deny it at the risk of losing their jobs.” Chart 12The Dollar Is Very Overvalued

The Dollar Is Very Overvalued

The Dollar Is Very Overvalued

October 2024 – The Stock Market Hits Bottom: While the unemployment rate continues to rise for another 12 months, ultimately reaching 6.4%, the S&P troughs at 3,200. The 10-year Treasury yield settles at 3.1% before starting to drift higher. The US dollar, which began to weaken anew after the Fed starts cutting rates, enters a prolonged bear market. As in past cycles, the dollar is unable to defy the gravitational force from extremely stretched valuations (Chart 12). November 2024 – President DeSantis: Against the backdrop of rising unemployment, uncomfortably high inflation, and a sinking stock market, Ron DeSantis cruises to victory in the 2024 presidential election. Unlike Trump, DeSantis deemphasizes corporate tax cuts and deregulation during his presidency, focusing instead on cultural issues. With the Democrats still committed to progressive causes, big US corporations discover that for the first time in modern history, neither of the two major political parties are willing to champion their interests. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn & Twitter Global Investment Strategy View Matrix

Dispatches From The Future: From Goldilocks To President DeSantis

Dispatches From The Future: From Goldilocks To President DeSantis

Special Trade Recommendations Current MacroQuant Model Scores

Dispatches From The Future: From Goldilocks To President DeSantis

Dispatches From The Future: From Goldilocks To President DeSantis

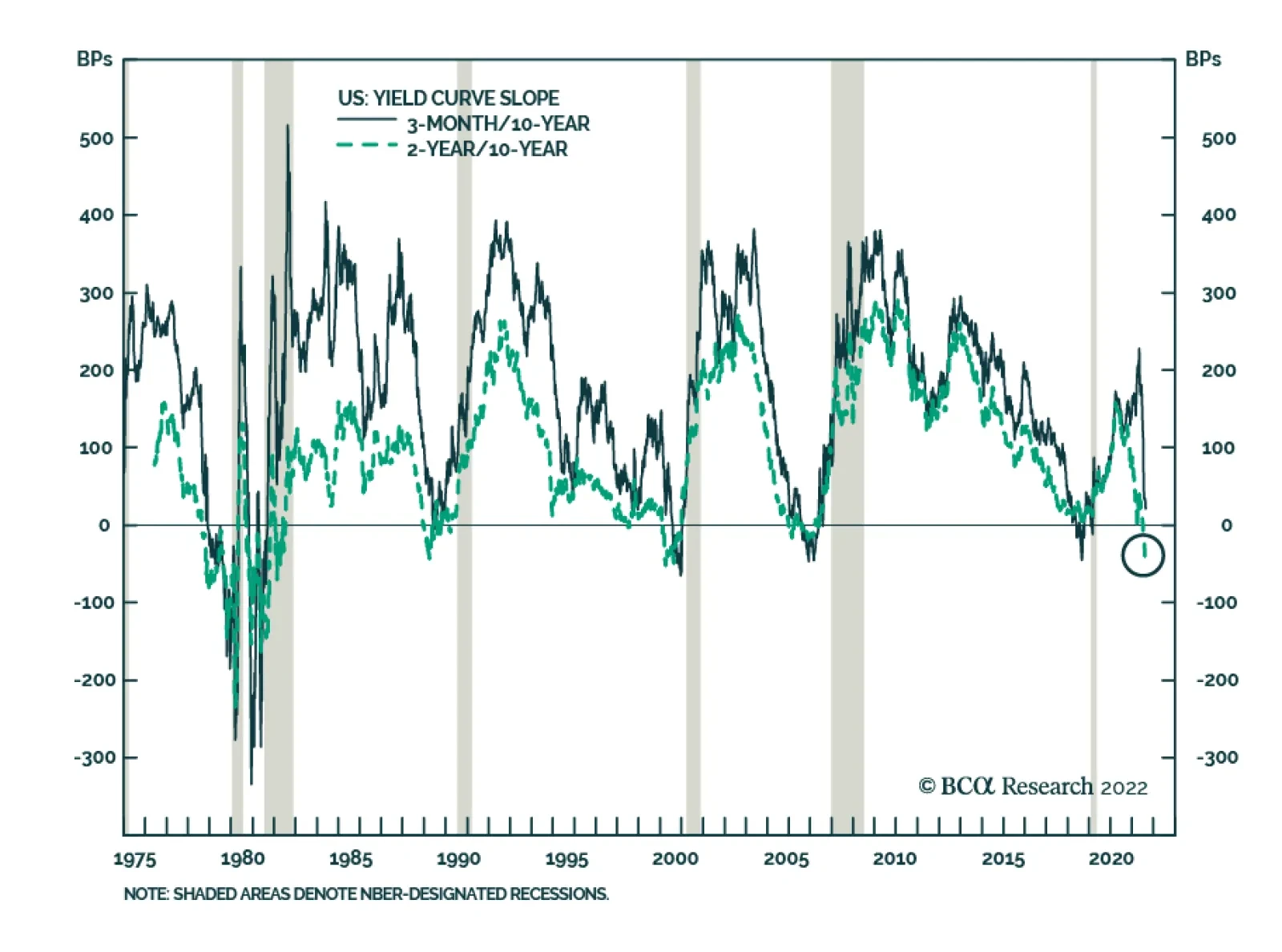

Despite all the worries, the most reliable yield curve slope measure, the 3-month/10-year segment, is not yet sending a recessionary signal. At 14bps, it is very flat, but recessions only follow an actual inversion, not a mere flattening episode. However, the…

Executive Summary More Regional Divergences Within Our Global LEI

More Regional Divergences Within Our Global LEI

More Regional Divergences Within Our Global LEI

The BCA global leading economic indicator (LEI) is still in a downtrend, but its diffusion index – which tends to lead the overall global LEI at major cyclical turning points – has crept higher since bottoming in January. The diffusion index is rising in part because of very marginal increases in the LEIs of a few countries, but there have been more decisive increases in the LEIs of two major countries outside the developed world – China and Brazil. There is not yet enough evidence pointing to a true bottoming of the BCA global LEI anytime soon, but an improvement in the LEI diffusion index above 50 (i.e. a majority of countries with a rising LEI) would be a more convincing signal that global growth momentum is set to rebound. Bottom Line: Given the uncertain message on growth from our global LEI, and with inflation rates still too high for central banks to pivot dovishly, we recommend staying close to neutral on overall global fixed income duration and modestly defensive on overall spread product exposure. Feature Investors can be forgiven for being a bit confused by some conflicting messages in recent global economic data. For example, US real GDP contracted in both the first and second quarter of this year – a so-called “technical recession” – and consumer confidence is at multi-decade lows, yet the US unemployment rate fell to 3.5%, the lowest level since 1969, in July. A similar story is playing out across the Atlantic, where a historic surge in energy prices was supposed to have already tipped the euro area into recession, yet real GDP expanded in both Q1 and Q2 at an above-trend pace and unemployment continues to decline. At times like the present, when market narratives do not always line up with hard data, we always believe it important to look within our vast suite of indicators to help clear the fog. One of our most trusted growth indicators, the BCA Global Leading Economic Indicator (LEI), is still falling and, thus, signaling a continued deceleration of global growth over at least the next 6-9 months. However, there are some signs of more optimistic news embedded within our global LEI stemming from outside the developed economies, which could be a potential early sign of a bottoming in global growth momentum. In this report, we dig deeper into the guts of our global LEI to assess the odds of an imminent turning point in the LEI and, eventually, global growth. This has important implications for global bond yields, which are likely to remain rangebound until there is greater clarity on global growth momentum (and inflation downside momentum). What Leads The Leading Indicator? The BCA global LEI is a composite index that combines the LEIs of 23 individual countries using GDP weights. The underlying list of countries differs from that of the widely followed OECD LEI, which is comprised of data from 33 countries but with a heavy weighting on developed market economies. The overall OECD LEI excludes important exporting countries such as Taiwan and Singapore, which are highly sensitive to changes in global growth. Most importantly, the OECD LEI omits the world’s largest economy, China. For our global LEI, we prefer to use a smaller set of countries but one that includes China and a bigger weighting on emerging market (EM) economies. For most of the nations in our global LEI, we do use the country-level LEIs produced by the OECD.1 That also includes several large and important non-OECD EM countries for which the OECD calculates LEIs - a list that includes China, Brazil, India, Russia, Indonesia and South Africa. For a few selected countries, however, we use the following data: US, Korea, Taiwan and Singapore: LEIs produced by national government data sources or, in the case of the US, the Conference Board. Argentina, Malaysia and Thailand: LEIs are produced in-house at BCA, a necessary step given the lack of domestically-produced LEIs in those countries at the time our global LEI was first constructed. We find that our global LEI leads global real GDP growth by around six months, and leads global industrial production growth by around twelve months (Chart 1). Chart 1A Gloomy Message From Our Global LEI

A Gloomy Message From Our Global LEI

A Gloomy Message From Our Global LEI

The latest reading on the global LEI from July is pointing to a further deceleration of global GDP into a “growth recession” where GDP is expanding slower than the pace of potential global GDP growth (less than 2%). The global LEI is also pointing to an outright contraction of global industrial production, a path also signaled by the JPMorgan global manufacturing PMI index which hit a two-year low of 51.1 – closing in on the 50 level that signifies expanding industrial activity – in July. Chart 2A Ray Of Hope On Global Growth?

A Ray Of Hope On Global Growth?

A Ray Of Hope On Global Growth?

The momentum of our global LEI is largely influenced by its breadth. Specifically, we have found that when a growing share of countries within the global LEI have individual LEIs that are rising, the overall LEI will eventually follow suit. Thus, the diffusion index of our global LEI, which measures the percentage share of countries with rising individual LEIs, is itself a fairly good leading indicator of the global LEI at major cyclical turning points. We may be approaching such a turning point, as our global LEI diffusion index has increased from a low of 9 back in January of this year to the level of 30 in July (Chart 2). In past business cycles, the diffusion index has tended to lead the global LEI by around 6-9 months, which suggests that a bottom in the actual global LEI could occur sometime in the next few months – although that outcome is conditional on the magnitude of the rise in the diffusion index. In the top half of Table 1, we list previous episodes since 1980 where the global PMI diffusion index followed a similar path to that seen in 2022 – bottoming out below 10 and then rising to at least 30. We identified nine such episodes. In the table, we also show the subsequent change in the level of the global LEI after the increase in the diffusion index. Table 1Global LEI Diffusion Index Greater Than 50 Typically Signals LEI Uptrend

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

The historical experience shows that an increase in the diffusion index to 30 was only enough to trigger a decisive rebound in the global LEI over a 6-12 month horizon in the 2000-01 and 2008 episodes. In several episodes, the global LEI actually contracted despite the pickup in the diffusion index. Related Report Global Fixed Income StrategyDovish Central Bank Pivots Will Come Later Than You Think In the bottom half of Table 1, we run the same analysis but define the episodes as when the diffusion index rose from a low below 10 to at least 50. Unsurprisingly, periods when at least half of the countries have a rising LEI tend to result more frequently in the overall global LEI entering an uptrend within one year – although the two most recent episodes in 2010 and 2018-19 were notable exceptions. Bottom Line: After looking at past experience, the latest pickup in the global LEI diffusion index has not been by enough to confidently forecast a rebound in the LEI – and, eventually, faster global growth. No Broad-Based Improvement In Our Global LEI When grouping the countries within our global LEI by geographical region, it is clear that there is still no sign of improvement in North America or Europe, but some signs of bottoming in Asia and Latin America (Chart 3). Typically, the regional LEIs tend to be very positively correlated during major cyclical moves in the overall LEI, with no one region being particularly better than the others at consistently leading the global business cycle. Chart 3More Regional Divergences Within Our Global LEI

More Regional Divergences Within Our Global LEI

More Regional Divergences Within Our Global LEI

Table 2Country Weightings In Our Global LEI

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

Of course, the global LEI is a GDP-weighted index that is dominated by the US and China (Table 2). When looking at individual country LEIs, the recent improvement in the LEI diffusion index looks less impressive. Some countries, like the UK and Korea, have only seen a tiny fractional uptick in the most recent LEI reading – moves small enough to qualify as statistical noise, even though the tiniest of positive moves still register as an “increase” when calculating the diffusion index. When looking at all the individual country LEIs within our global LEI, only two countries stand out as having meaningful increases over the past few months – China and Brazil (Chart 4). In the case of China, the idea that there could be signs of improving growth runs counter to the broad swath of recent data that highlight slowing momentum of Chinese consumer spending, business investment and residential construction. However, the production-focused components of the OECD’s China LEI, which we use in our global LEI, have shown some improvement of late (Chart 5). For example, motor vehicle production grew at a 32% year-over-year rate in July according to the OECD’s data, while total construction activity (based on OECD aggregates of production by industry) rose 9% year-over-year. Chart 4LEI Improvement In China & Brazil, Sluggish Elsewhere

LEI Improvement In China & Brazil, Sluggish Elsewhere

LEI Improvement In China & Brazil, Sluggish Elsewhere

Chart 5Improvement In Some Components Of The OECD's China LEI

Improvement In Some Components Of The OECD's China LEI

Improvement In Some Components Of The OECD's China LEI

The OECD’s LEI methodology is designed to include the minimum number of data series to optimize the fit of the LEI to the growth rate of each country’s industrial production index, which does lead to some peculiar series being included in the LEIs. However, there are signs of a potential rebound in Chinese economic growth evident in indicators preferred by our emerging market strategists, like the change in overall credit and fiscal spending as a share of GDP, a.k.a. the credit and fiscal impulse (Chart 6). The latter has shown a modest improvement that is hinting at faster Chinese growth in 2023, similar to the OECD’s China LEI. Turning to Brazil, the improvement in the OECD’s LEI there is focused on more survey-based data, like confidence among manufacturers and expectations on the demand for services. However, some hard data that the OECD includes in its Brazil LEI, namely net exports to Europe, have also shown clear improvement (Chart 7). Chart 6China Credit/Fiscal Impulse Signaling A Growth Rebound

China Credit/Fiscal Impulse Signaling A Growth Rebound

China Credit/Fiscal Impulse Signaling A Growth Rebound

Bottom Line: The modest improvement in our global LEI diffusion index is even less than meets the eye, as only China and Brazil have seen LEI increases that are meaningfully greater than zero. Chart 7Improvement In Many Components Of The OECD's Brazil LEI

Improvement In Many Components Of The OECD's Brazil LEI

Improvement In Many Components Of The OECD's Brazil LEI

Investing Around The Global LEI Chart 8Global Financial Conditions Not Signaling An LEI Rebound

Global Financial Conditions Not Signaling An LEI Rebound

Global Financial Conditions Not Signaling An LEI Rebound

Investors spend a sizeable chunk of their time focused on the future growth outlook to make investment decisions. This would, presumably, give leading economic indicators a useful role in any investment process. However, when looking at the relationship between our global LEI and the returns on risk assets like equities and corporate credit, the correlation is highly coincident (Chart 8). In other words, risk assets are themselves leading indicators of future economic growth – so much so that equity indices are often included as a component of the leading indicators of individual countries. On that front, the recent rebound in global equity markets, and the pullback in global credit spreads from the mid-June peak, could be signaling a more stable growth outlook that would be reflected in a bottoming of our global LEI. However, the monetary policy cycle matters, as evidenced by the correlation between the shape of government bond yield curves and our global LEI (bottom panel). That relationship is less strong than that of the LEI and equity/credit returns, but there are very few examples where yield curves are flat, or even inverted as is now the case in the US, and leading indicators are rising. Chart 9Stay Neutral On Overall Duration Exposure

Stay Neutral On Overall Duration Exposure

Stay Neutral On Overall Duration Exposure

In the current environment where more central banks are worrying more about overshooting inflation than slowing growth, a turnaround in our global LEI will be difficult to achieve until inflation is much closer to central bank target levels, allowing policymakers to loosen policy and steepen yield curves. We do not expect such a scenario to unfold over at least the next 12-18 months, given broad-based entrenched inflation pressures in global services and labor markets. While leading indicators may not be of much value in forecasting risk assets, we do find value in using them to forecast moves in government bond yields. Regular readers of BCA Research Global Fixed Income Strategy will be familiar with our Global Duration Indicator, comprised of growth-focused measures that have historically had a leading relationship to the momentum (annual change) in developed market bond yields (Chart 9). The Duration Indicator contains both the global LEI and its diffusion index, as well as the ZEW expectations indices for the US and Europe. Three of those four indicators remain at depressed levels suggesting waning bond yield momentum. Overshooting global inflation has weakened the correlation between bond yield momentum and our Duration Indicator over the past year. However, with global commodity and goods inflation now clearly decelerating, we expect bond momentum to begin tracking growth dynamics more closely again. This leads us to expect bond yields to remain trapped in ranges over at least the balance of 2022, defined most prominently by the 10-year US Treasury yield trading between 2.5% and 3%. Bottom Line: Given the uncertain message on growth from our global LEI, and with inflation rates still too high for central banks to pivot dovishly, we recommend staying close to neutral on overall global fixed income duration and modestly defensive on overall spread product exposure. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Details on how the OECD calculates the individual country leading economic indicators can be found here: http://www.oecd.org/sdd/leading-indicators/compositeleadingindicatorsclifrequentlyaskedquestionsfaqs.htm\ GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Cyclical Recommendations (6-18 Months)

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

A Hint Of Recovery In The BCA Global Leading Economic Indicator?

Dear Client, This week, the US Bond Strategy service is hosting its Quarterly Webcast (August 16 at 10:00 AM EDT, 15:00 PM BST, 16:00 PM CEST). In addition, we are sending this Quarterly Chartpack that provides a recap of our key recommendations and some charts related to those recommendations and other areas of interest for US bond investors. Please tune in to the Webcast and browse the Chartpack at your leisure, and do let us know if you have any questions or other feedback. To view the Quarterly Chartpack PDF please click here. Best regards, Ryan Swift, US Bond Strategist Treasury Index Returns Spread Product Returns

Executive Summary Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Inflation is not about oil, food or used car prices. Looking at prices of individual components of a consumer basket is akin to missing the forest for the trees. Despite the latest drop in US headline inflation, various core CPI measures continue trending up and registered considerable month-on-month rises in July. Wages and, more specifically, unit labor costs are the true measure of genuine and persistent inflation. US wage growth is very elevated, and the pace of unit labor cost gains has surged to a 40-year high. The conditions for sustainable and persistent disinflation in the US are not yet present. US inflation will prove to be much stickier and more entrenched than many market participants presently believe. The recovery in China will be U- rather than V-shaped, with risks tilted to the downside. The mainland’s property market breakdown is structural, not cyclical. Excesses are very large, and problems are snowballing, rendering the enacted policy stimulus insufficient. Bottom Line: US core inflation lingering above 4% and easing financial conditions will compel the Fed to continue hiking rates. This will cap global risk asset prices and put a floor under the US dollar. We continue to recommend an underweight allocation to EM in global equity and credit portfolios. Consistently, we are also reluctant to chase EM currencies higher. Feature The bullish macro narrative circulating in the investment community is that conditions for a cyclical rally in global risk assets have fallen into place. Specifically: US inflation will drop sharply as US growth has crested and commodity prices have plunged; The Fed is nearing the end of a tightening cycle; China has stimulated sufficiently, and its economy is about to recover, which will boost economic conditions among its trading partners in general and EM in particular. These assumptions along with the fact that the S&P 500 index has found support at a 3-year moving average – a proven line of defense – suggest that US share prices have likely bottomed (Chart 1). Are we witnessing déjà vu of the 2011, 2016, 2018 and 2020 market bottoms? Chart 1Déjà Vu? Is 2022 Like The 2011, 2016 And 2018 Bottoms In The S&P 500?

Déjà Vu? Is 2022 Like The 2011, 2016 And 2018 Bottoms In The S&P 500?

Déjà Vu? Is 2022 Like The 2011, 2016 And 2018 Bottoms In The S&P 500?

We have reservations about all of the above fundamental conjectures. We elaborate on these reservations in this report. On the whole, we contend that the current environment is different, and the roadmaps of all post-2009 equity market bottoms are not necessarily currently applicable. BCA’s Emerging Markets Strategy team believes that (1) US consumer price inflation is much more entrenched and will prove stickier than is commonly believed; and (2) the Chinese property market’s breakdown is structural, not cyclical; hence, the recovery will not gain traction easily. Is This The End Of The US Inflation Problem? Not Quite This week’s US inflation data confirmed that headline CPI inflation has probably peaked: prices in several categories plunged. However, inflation is not about oil, food or used car prices. Chart 2 reveals that historically there have been several episodes whereby core inflation remains elevated despite plunging oil prices. Chart 2US Core Inflation Does Not Always Follow Oil Prices

US Core Inflation Does Not Always Follow Oil Prices

US Core Inflation Does Not Always Follow Oil Prices

Looking at price dynamics among the individual components of the CPI basket is akin to missing the forest for the trees. Inflation is a very inert and persistent phenomenon. Underlying inflation does not change its direction often and/or quickly. That is why we believe that it is premature to celebrate the end of the US inflation problem. A few observations on this matter: Despite the drop in US headline inflation, various core CPI measures − like trimmed-mean CPI, median CPI and core sticky CPI − all continue trending up and registered substantial month-on-month rises in July (Chart 3). The range of core inflation based on these annual and month-month annualized rates is between 4-7%. In brief, the rate of genuine/sticky inflation is well above the Fed’s 2% target. Given its unconditional commitment to bringing inflation down to 2%, the Fed will continue hiking interest rates ceteris paribus. Chart 3US Core CPI Measures Are Still Very High

US Core CPI Measures Are Still Very High

US Core CPI Measures Are Still Very High

Chart 4US Wages Growth Has Been Surging

US Wages Growth Has Been Surging

US Wages Growth Has Been Surging

We continue to emphasize that wages and, more specifically, unit labor costs are the true measures of persistent and genuine inflation. We have written at length about why wages and unit labor costs are more important to inflation than oil or food prices. US wage growth is very elevated and is accelerating (Chart 4). Unit labor costs, calculated as hourly wages divided by productivity, have also been surging to a 40-year high (Chart 5, top panel). Chart 5Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

Unit Labor Costs, Not Oil Prices, Are The Key To US Core Inflation

The reason for this very strong wage growth and swelling unit labor costs is the very tight labor market. The bottom panel of Chart 5 demonstrates that labor demand is still outpacing labor supply by a wide margin. Hence, wage inflation will not subside until the unemployment rate rises meaningfully. Bottom Line: Conditions for sustainable and persistent disinflation in the US are not yet present. Inflation will prove to be much stickier and more entrenched than many market participants presently believe. Core inflation lingering above 4% and easing financial conditions will compel the Fed to continue hiking rates. This will cap risk asset prices and put a floor under the US dollar. China: Is This Time Different? If one believes that China’s current business cycle is similar to all previous ones seen since 2009, odds are that a buying opportunity in China-related financial markets is at hand. Chart 6 illustrates that the credit and fiscal spending impulse leads the business cycle by about nine months. Given that this impulse bottomed late last year, a trough in the Chinese business cycle is due. Chart 6Is A Recovery In China's Business Cycle Imminent?

Is A Recovery In China's Business Cycle Imminent?

Is A Recovery In China's Business Cycle Imminent?

It is always risky to suggest that this time is different. Nevertheless, at the risk of being wrong, we contend that a combination of (1) property markets woes, (2) an impending export contraction, and (3) the dynamic zero-COVID policy will reduce the multiplier effect of current stimulus measures. Hence, a meaningful recovery in economic activity will likely fail to materialize in the coming months. The challenges facing the mainland property market are now well known. Yet, excesses are very large, and problems are snowballing, making policy stimulus insufficient. In particular: Authorities are contemplating bailout funds for property developers in the range of RMB 300-400 billion to enable them to complete housing that has been pre-sold. This is not sufficient financing for overall property construction. Table 1How Large Are Property Developers Bailout Funds?

Déjà Vu?

Déjà Vu?

Table 1 illustrates that these amounts are equal to just 3-4% of annual fixed-asset investment in real estate excluding land purchases, 1.5-2% of total financing of developers, and 3-4% of the advance payments that property developers received for pre-sold housing in 2021. Property developers will not be receiving any cash upon the completion and delivery of presold housing units because they were paid in advance. Hence, without liquidating their other assets, homebuilders cannot repay the bailout financing. Consequently, only state financing can work here because, from the viewpoint of providers of this financing, this scheme de-facto means throwing good money after bad. The property industry in China is extremely fragmented. This makes bailouts difficult to organize and execute. There are officially about 100,000 property developers in China. The overwhelming majority of them are not state-owned companies. Plus, the two largest property developers, Evergrande (before defaulting) and Country Garden, had only 3.8% and 3.3% of market share respectively in 2020. The failure of homebuilders to complete and deliver pre-sold housing units could unleash a death spiral for them. In recent years, 90% of housing units have been pre-sold, i.e., buyers made advance payments/prepayments, often taking out mortgages (Chart 7, top panel). Witnessing the inability of developers to deliver on presold units, a rising number of people may decide to wait to buy. The largest source of developers’ financing – advance payments for pre-sold housing units – might very well dry up. This source has accounted for 50% of real estate developers’ total financing in recent years (Chart 7, bottom panel). In brief, a vicious cycle is possible. The lack of financing for homebuilders bodes ill for construction activity (Chart 8). Chart 7China: Housing Presales And Pre-Payments Are Critical To Developers

China: Housing Presales And Pre-Payments Are Critical To Developers

China: Housing Presales And Pre-Payments Are Critical To Developers

Chart 8Lack Of Homebuilder Financing = Shrinking Construction Activity

Lack Of Homebuilder Financing = Shrinking Construction Activity

Lack Of Homebuilder Financing = Shrinking Construction Activity

Chart 9Chinese Property Developers Are Extremely Leveraged

Chinese Property Developers Are Extremely Leveraged

Chinese Property Developers Are Extremely Leveraged

Besides, property developers are very leveraged with an assets-to-equity ratio close to nine (Chart 9). They have grown accustomed to borrowing heavily to accumulate real estate assets. They have been starting but not completing construction (Chart 10, top panel). We have been referring to this phenomenon as the biggest carry trade in the world. The bottom panel of Chart 10 shows two different measures of residential floor space inventories held by property developers. One measure subtracts completed floor space from started floor space, and another one deducts sold floor space from started floor space. On both measures, residential inventories are enormous. In theory, they could raise funds by selling their real estate assets. However, if they all try to sell simultaneously, there will not be enough buyers, and asset prices will plunge, which could lead to a full-blown debt deflation spiral. The last time the real estate market was similarly distressed in 2014-15, the central bank launched the Pledged Supplementary Lending (PSL) facility. This was effectively a QE program to monetize housing. This was the reason why housing recovered strongly in 2016-2017. There is currently no such program up for discussion. On the whole, odds are that the current property market breakdown is structural, not cyclical. Financial markets – the prices of stocks and USD bonds of property developers – convey a similar message and continue to plunge (Chart 11). Chart 10Excessive Property Inventories

Excessive Property Inventories

Excessive Property Inventories

Chart 11No Green Light From Property Stocks And Corporate Bond Prices

No Green Light From Property Stocks And Corporate Bond Prices

No Green Light From Property Stocks And Corporate Bond Prices

Chart 12There Has Been No Recovery In China Without A Revival in Real Estate

There Has Been No Recovery In China Without A Revival in Real Estate

There Has Been No Recovery In China Without A Revival in Real Estate

Without an improvement in the housing market, a meaningful business cycle recovery is unlikely in China. Chart 12 illustrates that all recoveries in the Chinese broader economy since 2009 occurred alongside a revival in property sales. The importance of the property market goes beyond its size. Rising property prices lift household and business confidence, boosting aggregate spending and investment. The sluggish housing market and falling house prices will impair consumer and business confidence. This, along with uncertainty related to the dynamic zero-COVID policy, will dent consumer spending and private investments. Finally, the upcoming contraction in Chinese exports will dampen national income growth. Taken together, the multiplier effect of stimulus in the upcoming months will be lower than it has been in previous periods of stimulus. There are two areas that will see meaningful improvement in the coming months: infrastructure spending and autos. BCA’s China Investment Strategy service discussed the outlook for auto sales in a recent report. Chart 13Green Shoots In China's Infrastructure Investment

Green Shoots In China's Infrastructure Investment

Green Shoots In China's Infrastructure Investment

On the infrastructure front, there has been mixed evidence of an improvement in activity. The top and middle panels of Chart 13 demonstrate that Komatsu machinery’s operational hours and the number of approved infrastructure projects might be bottoming. However, the installation of high-power electricity lines has fallen to a 15-year low (Chart 13, bottom panel). As we elaborated in last month’s report, the new financing/stimulus for infrastructure development will not result in new investments. Rather, it will by and large offset the drop in local government (LG) revenues from land sales this year. In short, there is little new stimulus for infrastructure beyond what was approved in the budget plan earlier this year. Bottom Line: The recovery in China will be U- rather than V-shaped, with risks tilted to the downside. Investment Recommendations Our bias is that the rebound in global risk assets could last for a few more weeks. The basis is that investor positioning in risk assets was very light when this rebound began. Plus, falling oil prices could reinforce the idea among investors that US inflation is no longer a problem. Looking beyond the next several weeks, the outlook for global and EM risk assets is dismal. Markets will realize that the Fed cannot halt its tightening with core inflation well above 4-5%. Hawkish Fed policy and contracting global trade will boost the US dollar and weigh on cyclical assets. We continue to recommend an underweight allocation to EM in global equity and credit portfolios. Consistently, we are also reluctant to chase EM currencies higher. EM local bonds offer value, as we have argued over the past couple of months, but for now we prefer to focus on yield curve flattening trades. We continue betting on yield curve flattening/inversion in Mexico and Colombia and are long Brazilian 10-year domestic bonds while hedging the currency risk. In addition, we recommend investors continue receiving 10-year swap rates in China and Malaysia. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

Executive Summary Realized Real Interest Rates Must Rise

Realized Real Interest Rates Must Rise

Realized Real Interest Rates Must Rise

Policymakers must continue engineering higher real interest rates, and tighter financial conditions, to help cool off growth and bring down overshooting inflation. This will inevitably lead to inverted yield curves across most of the developed world, following the recent trend of US Treasuries. US growth expectations remain overly pessimistic, which opens up the potential for more near-term bond-bearish upside data surprises like the July employment and ISM Services reports. The Bank of England – under increasing political pressure for its relatively timid response to the massive UK inflation overshoot – is now forecasting a long policy-induced recession as the only way to tame UK inflation expected to reach 13% by year-end. Expect UK Gilts to be a relative outperformer within developed bond markets over the next 12-18 months. Bottom Line: Stay overweight UK Gilts versus US Treasuries in global bond portfolios, but increase exposure to yield curve flattening in both countries. The Fed and Bank of England are both on course to push monetary policy into restrictive, growth-damaging territory. Don’t Get TOO Comfortable Taking Risk In a bit of a summer surprise, global financial markets have been staging a mild recovery from the stagflationary doom that prevailed during the first half of 2022. In the US, the S&P 500 index is up 14% from the year-to-date intraday low reached on June 16, with the VIX index back down to low-20s zone last seen in April (Chart 1). High-yield corporate bond spreads in the US and euro area are down 97bps and 36bps, respectively, since that mid-June trough in US equities. Even emerging market equities and credit – the most unloved of asset classes in 2022 – have stabilized. Related Report Global Fixed Income StrategyIt’s Time To Flip The Script - Upgrade UK Gilts Some of this risk rally is surely short-covering, but there are some valid reasons to be less pessimistic on growth-sensitive risk assets. In the US, where the back-to-back contractions in GDP in the first two quarters of the year have stoked recession fears, the latest data releases have seen upside surprises suggesting an expanding, not contracting, economy (Chart 2). The July ISM non-manufacturing (services) index rose +1.4 points in July to 56.7, a broad-based move that included increases in Production, New Orders and New Export Orders. Core durable goods orders rose +0.5% in June for the second straight month. The biggest surprise was the July Payrolls report, which showed a whopping +528,000 increase in employment – over twice the expected gain of +250,000 – with a downtick in the unemployment rate to 3.5%. Chart 1Stepping Back From The Recessionary Abyss

Stepping Back From The Recessionary Abyss

Stepping Back From The Recessionary Abyss

Chart 2The US Recession Talk May Have Been Premature

The US Recession Talk May Have Been Premature

The US Recession Talk May Have Been Premature

Chart 3Goods Inflation Pressures Easing

Goods Inflation Pressures Easing

Goods Inflation Pressures Easing

There was also some good news on the inflation front in the latest US data. The Prices Paid components of both the ISM manufacturing and non-manufacturing indices showed big declines, 18.5pts and 7.8pts respectively, in July, continuing the downtrends that began in the latter half of 2021 (Chart 3). This is not just a US story. The Prices Paid components of the S&P Global manufacturing PMIs in the euro area, the UK, Japan and China have also been falling. Lower global commodity prices, particularly for oil, are playing a large role in the pullback in reported business input costs. The Supplier Deliveries components of both ISM reports also fell on the month, continuing a trend seen throughout 2022 as global supply chain pressures have eased. Combined with the drop in the Prices Paid data, global PMIs are sending a strong message - inflationary pressures on the traded goods side of the global economy are finally easing. Slower goods inflation, however, does not provide an all-clear for risk assets on a cyclical basis. Non-goods price pressures are showing little sign of peaking across most of the developed world. Labor markets remain tight, and both wage inflation and services inflation rates continue to accelerate in the major economies of the US, UK and euro area at a pace well above central bank inflation targets (Chart 4). Until these domestic sources of inflation show signs of peaking, central banks will continue to push up policy rates to slow growth, generate higher unemployment and, eventually, bring domestically driven inflation back down to central bank targets. Expect the so-called Misery Index, summing headline inflation and the unemployment rate, to remain elevated across the major developed economies until negative real interest rates begin to rise through a combination of more nominal rate hikes and, eventually, slower inflation (Chart 5). Chart 4Domestic Inflation Pressures Accelerating

Domestic Inflation Pressures Accelerating

Domestic Inflation Pressures Accelerating

Chart 5Realized Real Interest Rates Must Rise

Realized Real Interest Rates Must Rise

Realized Real Interest Rates Must Rise

As we discussed in last week’s report, bond markets were getting way ahead of themselves in pricing in aggressive rate cuts in 2023, especially in the US. This was setting up for a potential move higher in yields on any positive data news. Within the “Big 3” developed economies, US Treasuries look most vulnerable to a rebound in bond yield momentum, judging by what looks like a true bottom in the mean-reverting Citigroup US Data Surprise Index (Chart 6). The flow of data surprises is more mixed in the euro area and UK and is not yet at the stretched extremes that would signal a sustainable increase in bond yields. Taken at face value, this fits with our current recommendation to underweight the US, and overweight core Europe and the UK, within global government bond portfolios. With central banks now on track to push policy rates into restrictive territory, there is the potential for additional flattening of already very flat yield curves across the Big 3. Forward rates are not priced for additional curve flattening in those markets, looking at both the 2-year/10-year and 5-year/30-year government bond curves (Chart 7). This makes positioning for more curve flattening in the US, UK and euro area a positive carry trade by leaning against the pricing of forward rates. Chart 6Greater Potential For Bond-Bearish Data Surprises In The US

Greater Potential For Bond-Bearish Data Surprises In The US

Greater Potential For Bond-Bearish Data Surprises In The US

Chart 7Increase Exposure To Curve Flattening In The 'Big 3'

Increase Exposure To Curve Flattening In The 'Big 3'

Increase Exposure To Curve Flattening In The 'Big 3'

We are adjusting the positioning within the BCA Research Global Fixed Income Strategy Model Bond Portfolio this week to benefit from the trend towards additional curve flattening in the US, the UK and core Europe (Germany and France). With the 2-year/10-year curve already inverted by -45bps in the US, we see better value by adding flattening exposure between the 5-year and 30-year points – a curve segment that is not yet in inversion. In the UK and euro area, we see a case for positioning for flattening across the entire yield curve. Bottom Line: Stay overweight both UK Gilts and core European government bonds versus US Treasuries in global bond portfolios, but increase exposure to yield curve flattening in all countries. The Fed and Bank of England are both clearly on course to push monetary policy into restrictive, growth-damaging territory, and the ECB may be forced to do the same. Painful Honesty From The Bank Of England The Bank of England (BoE) delivered its largest rate hike since 1995 last week, raising Bank Rate by 50bps to 1.75%. Planned sales of UK Gilts accumulated by the BoE during the quantitative easing phase of pandemic stimulus, at a pace of £10bn per quarter starting in September, were also announced. While those moves were largely expected by markets, the BoE’s new set of economic forecasts contained quite a shocker – an expectation of recession starting in Q4 of this year, running through the end of 2023 (Chart 8). The UK unemployment rate is expected to rise substantially from the current 3.8% to 6.3% by Q3/2025. Chart 8Brutal Honesty In The Latest BoE Forecasts

Brutal Honesty In The Latest BoE Forecasts

Brutal Honesty In The Latest BoE Forecasts

Chart 9Energy Prices Driving BoE Inflation Forecasts

Energy Prices Driving BoE Inflation Forecasts

Energy Prices Driving BoE Inflation Forecasts