Fixed Income

According to BCA Research’s US Bond Strategy service, investment grade corporate bonds are quite expensive. Starting with a simple examination of the average investment grade index OAS, the team observes that the spread has widened somewhat off its pre-…

Executive Summary Spreads Near 2017-19 Average

Spreads Near 2017-19 Average

Spreads Near 2017-19 Average

The main indicators that determine corporate bond performance are valuation, the cyclical/monetary environment and corporate balance sheet health. US corporate bond valuation is quite expensive. Spreads are off their post-COVID lows, but consistent with the 2017-19 average. The flat 2-year/10-year Treasury curve indicates that the cyclical/monetary backdrop is relatively poor. What’s more, the yield curve could easily invert within the next few months as the Fed tightens. This would send an even more negative signal for corporate bond returns. Corporate balance sheets are currently in excellent shape, but their health will deteriorate within the next 12 months as profit growth slows and interest rates rise. Relative valuation favors high-yield over investment grade corporates, and high-yield has a track record of outperformance during periods of restrictive monetary conditions and strong corporate balance sheets. Bottom Line: Investors should cyclically reduce exposure to US corporate bonds while retaining a preference for high-yield over investment grade. We recommend downgrading investment grade corporates from neutral (3 out of 5) to underweight (2 out of 5) and high-yield corporates from overweight (4 out of 5) to neutral (3 out of 5). Feature Chart 1A Rapid Recovery

A Rapid Recovery

A Rapid Recovery

US corporate bonds have had a very good run since the March 2020 peak in spreads. Investment grade corporates outperformed a duration-matched position in US Treasuries by 23% during the first 12 months of the recovery, the best 12-month excess return since 2010 (Chart 1). That same period also saw an extremely rapid re-normalization of credit spreads. It took just 11 months for the investment grade corporate index option-adjusted spread (OAS) to reach 90 bps following its March 2020 peak, and the index delivered an annualized excess return of 26% during that period. In contrast, it took 109 months for the index OAS to reach 90 bps following the 2008 recession and corporates only beat duration-matched Treasuries by an annualized 4% during that time (Table 1). Table 1US Investment Grade Corporate Bond Returns From Spread Peak Until 90 BPs

Turning Defensive On US Corporate Bonds

Turning Defensive On US Corporate Bonds

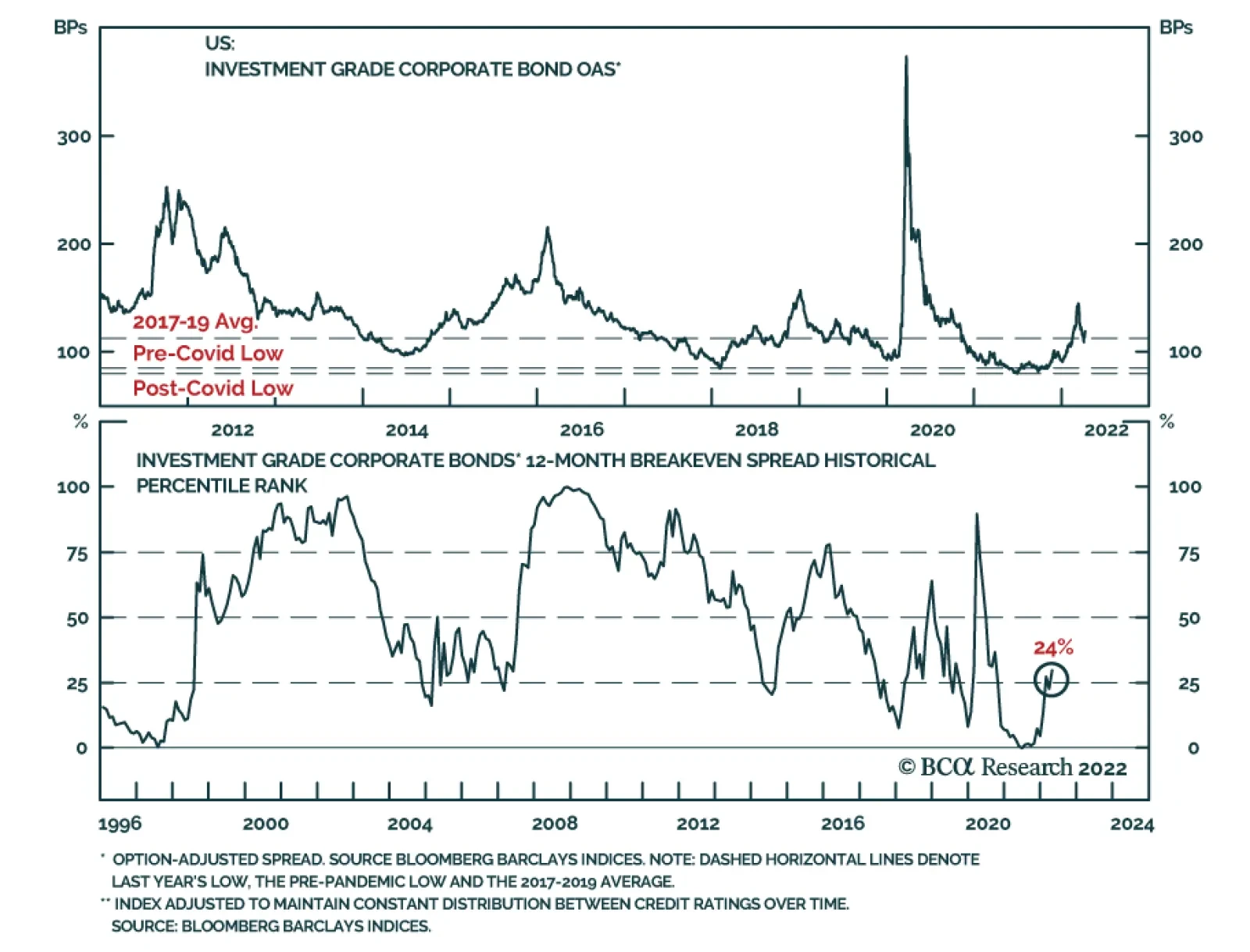

The outlook for US corporate bond returns looks much different today. Spreads are tighter and the Fed is rapidly removing policy accommodation. Against this backdrop, we decided last week to cyclically reduce our corporate bond exposure.1 Specifically, we recommended downgrading investment grade corporates from neutral (3 out of 5) to underweight (2 out of 5) and high-yield corporates from overweight (4 out of 5) to neutral (3 out of 5) within US bond portfolios. This Special Report discusses the rationale for our recent decision. First, we examine trends in the main indicators that determine corporate bond performance. These indicators fall into three categories: (i) valuation, (ii) cyclical/monetary indicators and (iii) balance sheet health. We then discuss the outlook for the relative performance of high-yield versus investment grade corporates. Valuation Starting with a simple examination of the average investment grade index OAS, we see that the spread has widened somewhat off its pre- and post-pandemic lows, but remains close to the average level seen between 2017 and 2019 (Chart 2). The index OAS is a reasonable gauge of value relative to recent history, but for a longer historical perspective we should adjust the index to account for its changing average credit rating and duration. To do this, we first re-weight the index to maintain a constant distribution between the different credit rating buckets. Next, we control for the index’s changing duration by calculating a 12-month breakeven spread. The 12-month breakeven spread is the spread widening that must occur during the next 12 months for the corporate index to perform in line with a duration-matched position in Treasuries. It can be approximated by dividing the index OAS by average index duration. Finally, Chart 3 presents the 12-month breakeven spread as a percentile rank since 1995. It shows that, after controlling for credit rating and duration, the investment grade corporate index has only been more expensive than current levels 24% of the time since 1995. Notice that the spread bounced off the 0% line in late-2021, indicating that it had reached all-time expensive levels. Chart 2Spreads Near 2017-19 Average

Spreads Near 2017-19 Average

Spreads Near 2017-19 Average

Chart 3Investment Grade Valuation

Investment Grade Valuation

Investment Grade Valuation

All in all, we can conclude that investment grade corporate bonds are quite expensive. Spreads aren’t so low that they would justify an underweight allocation in a supportive cyclical/monetary environment. But they are tight enough that it makes sense to proceed cautiously in a neutral or negative cyclical/monetary environment, like the one we are in today. Cyclical/Monetary Indicators The slope of the yield curve is the key variable we use to assess the current state of the cyclical/monetary environment. A very flat or inverted yield curve signals a relatively restrictive monetary policy backdrop, and we have shown that such a backdrop tends to coincide with poor excess corporate bond returns. Conversely, we have found that corporate bonds perform best early in the economic recovery when the yield curve is very steep. This steep yield curve signals that monetary conditions are highly accommodative, and thus supportive of credit spread tightening. Today, the yield curve is sending a somewhat confusing message. The 2-year/10-year Treasury slope briefly inverted last week, and it remains flat at 22 bps. Meanwhile, the 3-month/10-year Treasury slope is very steep, up above 200 bps (Chart 4)! Chart 4Conflicting Signals From The Yield Curve

Conflicting Signals From The Yield Curve

Conflicting Signals From The Yield Curve

We discussed how to interpret the signals from different yield curve segments in a recent Special Report.2 We found that the 2-year/10-year Treasury slope sends the most useful signal for corporate bond excess returns, and we therefore view current cyclical/monetary conditions as negative for corporate bonds. In Table 2 we split each of the past six economic cycles into phases based on the 2-year/10-year Treasury slope. We define Phase 1 of the cycle as the period from the end of the prior recession until the 2-year/10-year slope breaks below 50 bps. Phase 2 of the cycle encompasses the time when the slope is between 0 bps and 50 bps. Phase 3 of the cycle spans from when the yield curve inverts until the start of the next recession. Table 2US Corporate Bond Performance In Different Phases Of The Cycle

Turning Defensive On US Corporate Bonds

Turning Defensive On US Corporate Bonds

The table shows annualized excess returns for both investment grade and high-yield corporate bonds in each of the three phases, and those returns exhibit a clear pattern. Returns are best in Phase 1 when the yield curve is steep. They take a step down in Phase 2 when the slope is between 0 bps and 50 bps, though they usually stay positive. Negative returns are most likely in Phase 3, after the yield curve inverts. Chart 5Limited Room For Curve Steepening

Limited Room For Curve Steepening

Limited Room For Curve Steepening

With the 2-year/10-year Treasury slope at 22 bps, we are firmly in Phase 2 of the cycle. However, we could easily see the 2-year/10-year slope invert within the next few months while a breakout above 50 bps seems less likely. In fact, there are only two ways in which the 2-year/10-year Treasury slope can steepen further from current levels. First, the market could bid up its expectation of the long-run neutral fed funds rate, pushing long-dated bond yields higher. Second, expectations for the pace of near-term Fed tightening could diminish, pulling short-dated yields down. At the long-end, the 5-year/5-year forward Treasury yield is already above survey estimates of the long-run neutral rate (Chart 5). At the front-end, the market is discounting a rapid pace of 272 bps of tightening during the next 12 months (Chart 5, bottom panel), but that pace has limited room to fall given current extremely high inflation readings. Turning back to a comparison of the signals from the 2-year/10-year slope and 3-month/10-year slope, it is worth pointing out that the 3-month/10-year slope is influenced by yield movements at the very front-end of the curve. Meanwhile, the 2-year/10-year slope is purely a function of rate expectations beyond the next two years. As a result, we can view the 3-month/10-year slope as sending a timelier signal about Fed rate hikes and cuts, while the 2-year/10-year slope gives a better reading of how the market views the ultimate economic impact of Fed actions. For example, the 3-month/10-year Treasury slope inverted in 2019 just before the Fed started cutting rates (Chart 6A). The 2-year/10-year slope, however, only briefly dipped below zero. The message from the market was that the Fed would cut rates, but those cuts would be sufficient to sustain the economic recovery. As a result, corporate bonds performed well during this period, consistent with the message from the 2-year/10-year slope. Another interesting example occurred in early 2000 (Chart 6B). This time, the 2-year/10-year Treasury slope inverted while the 3-month/10-year slope remained steep. In this case, the 3-month/10-year slope was telling us that Fed rate hikes would continue, while the 2-year/10-year slope was telling us that those hikes would eventually kill the economic recovery. Once again, corporate bonds took their cues from the 2-year/10-year Treasury slope and performed poorly during this period. Chart 6AStrong Performance In 2019

Strong Performance In 2019

Strong Performance In 2019

Chart 6BPoor Performance In 2000

Poor Performance In 2000

Poor Performance In 2000

Obviously, the current situation looks more like 2000 than 2019, but with the 2-year/10-year slope still positive there remains scope for positive excess corporate bond returns in the near-term. That said, with high odds of 2-year/10-year curve inversion within the next few months and spreads at relatively tight levels, it makes sense to scale back exposure today in advance of the worst phase of the cycle. Balance Sheet Health The final factor we consider is the health of nonfinancial corporate sector balance sheets, and in fact, this is currently the lone bright spot for corporate bond investors. Our Corporate Health Monitor (CHM), a composite indicator of six key balance sheet ratios, is deep in “improving health” territory (Chart 7). This positive signal is driven by exceptionally high Interest Coverage (Chart 7, panel 2) and Free Cash Flow-To-Debt that is just off its highs (Chart 7, panel 3). Return On Capital is up sharply since 2020 but has not recovered its previous peak (Chart 7, bottom panel). Chart 7Balance Sheets Are In Great Shape

Balance Sheets Are In Great Shape

Balance Sheets Are In Great Shape

While corporate balance sheets are in excellent shape right now, their health will certainly deteriorate going forward as profit growth comes down off its highs and interest rates rise. The only question is whether this deterioration will happen slowly or quickly. Turning to history, two relevant periods stand out (Chart 8). First is the mid-1990s when investment grade corporate bond excess returns peaked in July 1997, 16 months before our CHM moved into “deteriorating health” territory. Conversely, the CHM sent a negative signal before the excess return peak in 2007. But even then, investment grade corporates only outperformed Treasuries by an annualized 0.8% between when the 2-year/10-year slope fell below 50 bps in 2005 and when the CHM moved above zero in 2006. In other words, investors didn’t sacrifice much return by heeding the yield curve’s signal even when the CHM was deep in “improving health” territory. Chart 8Cyclical Corporate Bond Performance

Cyclical Corporate Bond Performance

Cyclical Corporate Bond Performance

Investment Conclusions In summary, we view corporate bond valuations as expensive, and the flat 2-year/10-year Treasury slope suggests that the economic recovery is in its mid-to-late stages. Corporate balance sheets are currently in excellent shape, but they will deteriorate going forward as profit growth slows and interest rates rise. The above three factors suggest that corporate bonds could continue to outperform duration-matched Treasuries in the near-term. However, with spreads already at tight levels, we likely aren’t sacrificing much in the way of excess returns by turning cyclically defensive today. This move also ensures that we will not be invested when the credit cycle eventually turns and corporate bond spreads move significantly wider. Retain A Preference For High-Yield Versus Investment Grade While we recommend downgrading allocations for both investment grade (from neutral to underweight) and high-yield (from overweight to neutral), we think investors should still retain a preference for high-yield corporates over investment grade. To see why, let’s return to the 2005-06 period we looked at in the previous section. The yield curve dipped below 50 bps in 2005 when the CHM was still deep in “improving health” territory, and while investment grade corporate bond returns were low during the time between the signal from the yield curve and the signal from the CHM, junk excess returns were very strong (Chart 9). This makes some sense intuitively. Higher-rated investment grade corporates responded negatively to the Federal Reserve’s removal of monetary policy accommodation, but lower-rated junk spreads stayed well bid because actual default risk was benign. It wasn’t until after the CHM rose above zero that junk bonds started to underperform. In terms of present-day valuations, much like for investment grade, junk spreads are up off their 2021 lows. However, they remain close to their pre-pandemic trough (Chart 10). We also note that the differential between high-yield and investment grade spreads was much tighter in 2006-07. Given the similarities between that period and today, we wouldn’t be surprised to see junk spreads compress further relative to investment grade. Chart 9The Bullish Case For Junk

The Bullish Case For Junk

The Bullish Case For Junk

Chart 10High-Yield Valuation

High-Yield Valuation

High-Yield Valuation

Another way to approach high-yield bond valuation is through the lens of our Default-Adjusted Spread. The Default-Adjusted Spread is the difference between the junk index OAS and 12-month default losses, and we have shown that it has a strong correlation with excess returns (Table 3). Specifically, a Default-Adjusted Spread above 100 bps usually coincides with positive excess junk returns versus Treasuries, and higher spreads tend to coincide with higher returns. Table 3The Default-Adjusted Spread & High-Yield Excess Returns

Turning Defensive On US Corporate Bonds

Turning Defensive On US Corporate Bonds

To estimate the Default-Adjusted Spread for the next 12 months we need assumptions for the default and recovery rates (Chart 11). To do this, we model the 12-month speculative grade default rate as a function of gross nonfinancial corporate leverage – total debt over pre-tax profits – and lagged C&I lending standards. We then model the 12-month recovery rate based on the default rate itself. Chart 11Default And Recovery Rate Models

Default And Recovery Rate Models

Default And Recovery Rate Models

Corporate pre-tax profit growth was exceptionally strong during the past 12 months, and we expect it to slow significantly going forward. Profit growth can be modeled as a function of nominal GDP growth and unit labor costs (Chart 12). If we assume that nominal GDP growth comes in at 7.3% this year (the Fed’s median 2.8% real GDP estimate plus 4.5% inflation) and that unit labor cost growth rises to 6%, then profit growth will fall to 0.5% during the next 12 months. If we assume that corporate debt growth remains close to its current level (Chart 12, bottom panel), then we calculate that gross leverage will rise to 6.5 during the next 12 months. Chart 12Profit Growth Will Slow Significantly

Profit Growth Will Slow Significantly

Profit Growth Will Slow Significantly

Table 4 shows the output from our default and recovery rate models under the base case assumption described above. It also shows results for an optimistic case where leverage is 6.0 and a pessimistic case where it is 7.0. The Default-Adjusted Spread is fairly low in the base and pessimistic cases, but it is comfortably above the key 100 bps threshold in all three scenarios. This suggests that junk bonds should deliver positive excess returns versus duration-matched Treasuries during the next 12 months. Table 4Default-Adjusted Spread Scenarios

Turning Defensive On US Corporate Bonds

Turning Defensive On US Corporate Bonds

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Portfolio Allocation Summary, “The Beginning Of The End”, dated April 5, 2022. 2 Please see US Bond Strategy / US Investment Strategy / US Equity Strategy Special Report, “The Yield Curve As An Indicator”, dated March 29, 2022. Treasury Index Returns Spread Product Returns Recommended Portfolio Specification

Turning Defensive On US Corporate Bonds

Turning Defensive On US Corporate Bonds

Other Recommendations

Turning Defensive On US Corporate Bonds

Turning Defensive On US Corporate Bonds

According to BCA Research’s European Investment Strategy service, German yields can rise above 2% without causing a public finance crisis in Italy. How high can yields rise in the Eurozone before Italy experiences meaningful funding stresses? The team…

Executive Summary From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

Yields are rising across Europe. Peripheral spreads are unlikely to experience the same violent widening as last decade. Europe now has a buyer of last resort. Italy and Spain have moved from current account deficit to current account surplus nations. However, Italy and Spain are not conducting the kind of structural reforms necessary to cause public debt-to-GDP ratios to fall back below the Maastricht Treaty criteria. Nonetheless, based on our stress tests, Italian and Spanish yields can rise significantly more before debt-servicing costs become a major problem in these nations. Economic activity, not Spanish or Italian public finances, is the true constraint on European yields. Bottom Line: German yields can rise above 2% without causing a public finance crisis in Italy and Spain. To reach this level, however, nominal growth in Europe must remain robust. As a result, any pullback in yields caused by oversold conditions in the bond market will be temporary. Year-to-date, German 10-year yields have risen more than 80bps, while spreads have widened in the periphery. This has supercharged the interest rate moves: Italian BTP yields and Spanish Bono yields are up nearly 120bps and 110bps, respectively. As a result, Italian government bonds now offer a 2.4% yield, a level not experienced durably since the first half of 2019. Meanwhile, Spanish yields are close to 1.7%—their highest levels since 2017. Investors are increasingly concerned by the damage levied by higher yields in Southern Europe. Since 2018, Italian public debt has risen by 32% of GDP to 170% of GDP, and Spanish public debt has risen by 28% of GDP to 138% of GDP. These higher debt burdens beg the following question: How high can European yields rise before a new sovereign debt crisis engulfs the Eurozone? Private sector financial balances and the balance of payments in the periphery are now very different from what they were between 2008 and 2012. As a result, the odds of a similar crisis are much lower than last decade, which should allow German yields to rise further in the coming years. Italy and Spain have moved on from experiencing an EM-style balance of payment crisis with explosive debt market dynamics. They are now stuck in a Japanese scenario of excess private sector savings and low economic growth. “This Time Is Different” These might be the four most dangerous words in finance, but understanding the differences between the present situation and the sovereign debt crisis is essential to assessing the impact of higher yields on Italian and Spanish public finances. Chart 1From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

The most important transformation in the Southern European economies is the rise in private sector savings. From 1999 to 2013, Italy’s private sector financial balance averaged 2.2% of GDP. Constant government deficits resulted in a significant national dissaving, forcing the country to borrow from abroad as expressed by a current account deficit that lasted from 2000 to 2013 (Chart 1, top panel). At the present moment, Italy’s current account is in a surplus equal to 3.5% of GDP, as private savings stand at 13% of GDP, up from 5% before COVID-19. The change is even more dramatic in Spain. The Spanish private sector financial balance was in a large deficit from 1999 to 2008, which averaged 5.6% of GDP and reached a nadir of 11.3% of GDP in 2007. As a result, Spain relied on foreign lending between 1980 and 2012, with a current account deficit that averaged 3% of GDP over that period (Chart 1, second panel). The switch from the status of foreign borrower to the status of surplus nation is fundamental. A country where excess private savings are so abundant they can finance large public deficits and still generate current account surpluses will experience more limited pressure on borrowing costs than a country that needs to borrow from abroad. Japan is a perfect example. Elevated public borrowing ends up being a vehicle to absorb private sector excess savings and does not constitute profligacy. Despite higher debt loads, Italy’s public finances seem more sustainable than those of Spain. The International Monetary Fund’s (IMF) October 2021 Fiscal Monitor forecast shows the Italian primary budget balance, both on an absolute basis and on a cyclically-adjusted basis, moving from -6% and -2.9% of GDP, respectively, closer to zero by 2026 (Chart 2). In Spain, primary budget balances, both on an absolute basis and on a cyclically-adjusted basis, are anticipated to improve from -8.9% and -3.4% of GDP, respectively, to -2.5% of GDP by 2026. Despite these deficits, the IMF also expects public debt to decrease by 10% of GDP to 146% in Italy and to remain flat at 120% of GDP in Spain (Chart 3). Importantly, in both cases, the upward pressure on public debt will be limited over the next five years because private savings are already high and unlikely to rise further. Chart 2Public Deficits Will Narrow Further

Public Deficits Will Narrow Further

Public Deficits Will Narrow Further

Chart 3Debt Will Stay High, So Will Private Savings

Debt Will Stay High, So Will Private Savings

Debt Will Stay High, So Will Private Savings

The role of the European Central Bank (ECB) as a backstop also contributes to creating a different environment than the one that prevailed prior to the “whatever it takes” era. Before Mario Draghi’s landmark July 2012 speech, there was no explicit buyer of last resort in the European sovereign debt market. Now, there is one, and its presence limits how rapidly private sector buyers might lose confidence in a country’s bond market and how far spreads can widen, even if the central bank buying has its own limit. In fact, Draghi’s forward guidance calmed the markets and caused a 250bps and 280bps collapse in Italian and Spanish 10-year yields before the ECB had even purchased a single BTP or Bono. The role of the ECB as a buyer of last resort remains crucial going forward. Yields in Italy and Spain are still 480bps and 600bps below their 2011-2012 peaks at a time when investors anticipate an end to the PEPP and APP purchases. Importantly, these spreads are narrower, even though the APP and the PEPP have purchased far more German and French sovereign bonds than Italian and Spanish bonds (Chart 4). As long as the ECB continues to emphasize that it maintains its optionality to support Italian and Spanish bond markets, even as its asset purchases end, peripheral spreads will not move back above 300bps, especially since Euroscepticism is not the risk it once was (Chart 5). Chart 4Germany and France, Not Spain and Italy, Dominated PEPP Buying

Stress Testing Italian And Spanish Yields

Stress Testing Italian And Spanish Yields

Chart 5Euroscepticism on the Wane

Euroscepticism on the Wane

Euroscepticism on the Wane

Bottom Line: As illustrated by the evolution of their current account balances, peripheral Eurozone economies have moved from deep savings deficits to a state of surplus savings. This makes them less vulnerable to the funding crises that prompted the European sovereign debt crisis. Moreover, the Eurozone now has a buyer of last resort for sovereign bonds: the post-Draghi ECB. Its presence, not its continued buying, creates the necessary insurance to limit buying strikes by the private sector, which also curtails how far Italian or Spanish spreads can widen. Long-Term Problems Abound In the long term, Italy and Spain will only be able to curtail government debt-to-GDP ratios meaningfully if trend growth recovers. This means more reforms are needed to boost productivity and labor participation rates (Chart 6). Chart 6Reforms, Not Austerity, Will Bring Debt Down Below Maastricht Levels

Stress Testing Italian And Spanish Yields

Stress Testing Italian And Spanish Yields

Chart 7Competitiveness Problems In The Periphery

Competitiveness Problems In The Periphery

Competitiveness Problems In The Periphery

For now, the picture remains bleak. Spain emerged out of the sovereign debt crisis with strong reform zeal. The Mariano Rajoy government reformed pensions and the labor market, which prompted a significant decline in unit labor costs compared to the Euro Area average. The pace of reforms has slowed, however, and the Pedro Sánchez government has eroded some of its predecessor’s efforts. As a result, since 2018, Spanish unit labor costs have increased once again relative to the rest of the Eurozone (Chart 7). Italy never implemented significant reforms, because it has long been beset by political paralysis. Unit labor costs are not outstripping the rest of the Eurozone, but productivity continues to lag. Economic growth in Italy and Spain will remain tepid in the coming years, which will prevent any meaningful decline in debt. The poor trend in relative competitiveness and productivity of the past few years is unlikely to be undone. Work by the OECD shows that prior to the pandemic, Spain and Italy had shifted away from being among the leading reformers in Europe. Instead, this role now falls to France, Greece, Austria, and Germany (Chart 8), which confirms last week’s analysis that France’s reform effort remains serious, even if it is less ambitious than what transpired over the past five years. As a consequence of slow growth, investment in Spain and Italy will trail behind the rest of the Eurozone. Thus, private sector savings will remain elevated and private nonfinancial sector debt loads are unlikely to increase meaningfully (Chart 9). As a result, the public sector will continue to absorb the private sector’s excess savings, which means that the debt-to-GDP ratio could sustain more upside pressure than what either the IMF or the OECD anticipate. Chart 8Italy And Spain As Reform Laggards

Stress Testing Italian And Spanish Yields

Stress Testing Italian And Spanish Yields

Chart 9Private Debt Is Not The Problem

Private Debt Is Not The Problem

Private Debt Is Not The Problem

These dynamics bear a striking resemblance to what happened in Japan. They also imply that Italy and Spain will remain a drag on European growth for years to come, as long as the fundamental reasons behind the private sector’s elevated savings rate are not addressed. Bottom Line: Italian and Spanish public debt-to-GDP ratios will continue to deteriorate as reform efforts are too tepid to lift durably trend GDP growth. Their private sectors will continue to save more than they invest, which, in turn, will push government debt higher. The Italian and Spanish economies will remain a drag on European growth for the foreseeable future. Stress Test Scenarios How high can yields rise in the Eurozone before Italy and Spain experience meaningful funding stresses? We explore two scenarios: one in which 10-year yields rise by an additional 2%, and a very aggressive scenario in which they rise a whopping 5%, bringing Italian and Spanish borrowing costs in the vicinity of the European debt crisis of 2011-2012. To conduct this experiment, we use a simple approach of regressing debt-service payments as a share of GDP on the level of yields. Modeling debt payments in euros was another alternative, but yield levels are also affected by the evolution of nominal GDP. As a result, using this approach considers both the numerator and the denominator of the debt-service payment modeling. Chart 10Private Debt Is Not The Problem

Private Debt Is Not The Problem

Private Debt Is Not The Problem

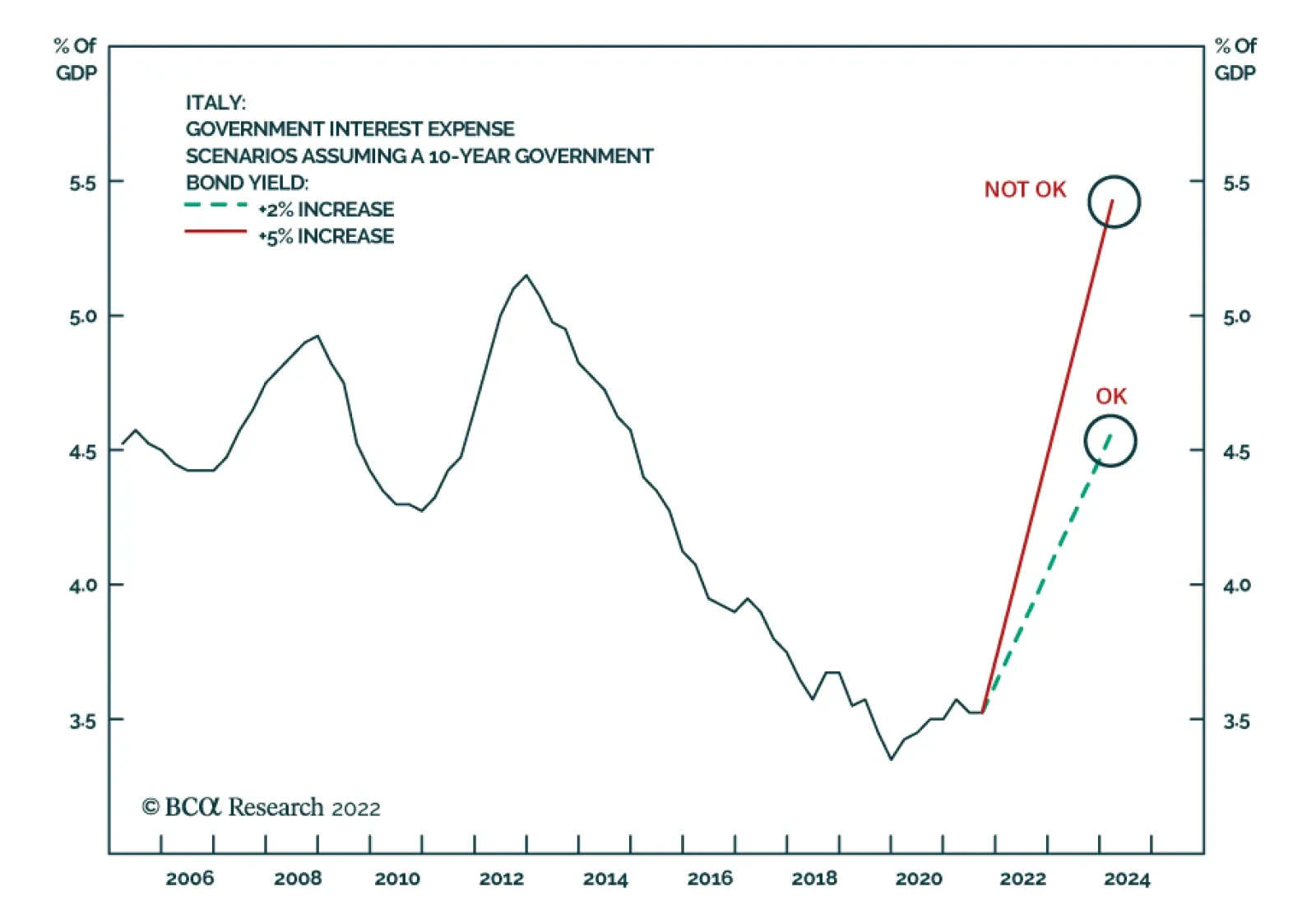

Under the first scenario, Italian 10-year yields would rise to 4.4% from 2.4% today. This is still well below the 7.5% yield recorded in late 2011. In this context, government debt servicing would reach 4.5% of GDP, which is comparable to the average that prevailed prior to the Euro Area crisis (Chart 10). This suggests that Italian yields slightly above 4% are still somewhat manageable, albeit far from ideal. Under the second scenario, 10-year BTP yields would rise to 7.4% from 2.4% today. This is comparable to the level of yields observed at the apex of the European sovereign debt crisis, but it assumes that this yield level would remain in place for a year. As a result of the higher debt load today compared to a decade ago, the resulting debt-servicing costs have reached 5.4% of GDP, which is higher than those between 2012 and 2013 (Chart 10). This scenario is clearly unsustainable and suggests that yields of this magnitude would cripple the Italian government. Moving to Spain, the dynamics are slightly different. Spain’s refinancing schedule is more front-loaded than that of Italy. As a result, using the yields on 10-year Bonos as an independent variable in our regression approach does not explain well the evolution of Spanish debt-servicing costs. Instead, a simple regression model using both 3-year and 10-year yields does a much better job, because it reflects the heavier rollover of Spanish debt. Chart 11Stress Testing Spanish Public Finances

Stress Testing Spanish Public Finances

Stress Testing Spanish Public Finances

In the first scenario, 3-year yields would rise by 1% to 1.7% and 10-year yields would increase from 2% to 3.7%, well below the 7% yields that prevailed in 2012. As a result, the Spanish government’s debt-servicing costs would be expected to rise to 2.8% of GDP, which is well below the levels that prevailed at the apex of the European debt crisis, but still above the level that existed in the first decade following the introduction of the euro (Chart 11). While far from ideal, this level is easily manageable for the Spanish government and is comparable to the Eurozone average prior to 2008. In the second scenario, 3-year yields are assumed to rise 2.5% to 3.2% and 10-year yields to increase an extra 5% to 6.7%, still slightly shy of the 7% yields from 2012. In this scenario, debt servicing costs are expected to jump above 3.5% of GDP (Chart 11) and are unsustainable unless nominal GDP growth remains above 7% and the primary budget balance improves to zero. As a result, an increase in Bono yields toward 7% is far too high for the Spanish government to withstand. We acknowledge that, although it points to an upper bound in yields, the second scenario is highly unlikely for several reasons. First, a 500bps increase in 10-year yields would far exceed the roughly 350bps rise experienced during the sovereign debt crisis of the previous decade. More importantly, many factors have changed since then: Spain and Italy’s shift from borrowing nations to surplus savings nations, the role of the ECB as buyer of last resort, greater support for the euro across all the Eurozone nations, and greater unity among EU countries as exemplified by the NextGenerationEU (NGEU) program. The first scenario would be painful but manageable for both Italy and Spain. It suggests that peripheral yields may rise meaningfully in the coming years, especially if nominal GDP growth remains higher than it was last decade when fiscal austerity was Europe’s mantra. However, fiscal austerity was self-defeating because, the more orthodox countries tried to be, the worse their growth was, making debt arithmetic unmanageable (Chart 12). Chart 12Counterproductive Austerity

Stress Testing Italian And Spanish Yields

Stress Testing Italian And Spanish Yields

We can go one step further. Even if Italian and Spanish spreads widen another 100bps from this point on and settle between 200bps and 300bps above German yields, European public finances can withstand German yields rising to 2%. This seems surprising, but we cannot forget the context. German yields cannot reach those levels in a vacuum. If they increase that much, it is because nominal growth is strong, which makes debt arithmetic more manageable in the European periphery. Statistically, the relationship between Spanish debt servicing costs and German yields is negative, while the link between Italian debt servicing costs and German yields is statistically low, underscoring the role of growth. However, if German yields were to rise as Europe’s nominal GDP growth settled back to last decade’s range, then Italian and Spanish debt would implode. This is a far-fetched scenario; even the recent ECB’s pivot reflects stronger nominal activity. This does not mean that German yields will rise above 2% in the next five years, but rather it highlights that economic activity, not the peripheral nations’ public finances, is the true constraint on European yields. Bottom Line: The ECB’s role as a buyer of last resort, the shift to savings surpluses in Italy and Spain, as well as the greater European unity and lower Euroscepticism prevalent across the continent limit how far spreads can rise in the periphery. In this context, Spain and Italy can withstand higher yields than those of the last decade, since these higher borrowing costs reflect stronger nominal economic activity. Ultimately, the true constraint on German yields is not the finances of Southern Europe, but rather the state of economic growth in the Eurozone. Conclusions Related Report European Investment StrategyThe Lasting Bond Bear Market European yields continue to have significant upside, as we expect European growth to remain stronger than it was last decade even if Italy and Spain will continue to lag behind the rest of Europe. As we observed two weeks ago, Europe is no longer burdened by untimely fiscal austerity. Furthermore, the efforts to decrease the energy dependence on Russia and modernize the European economy will continue to support capex and aggregate demand. The upper band on German yields seems to be around 2%, assuming that Italian and Spanish spreads rise 100bps to 150bps over the coming years. Even the banking sector in the periphery can withstand significant upside in bond yields. BTPs and Bonos represent 11% and 6.8% of the Spanish and Italian financial sectors’ balance sheet, respectively (Chart 13). This is much higher than the role of OATs and Bunds in the French and German financial sectors, but Spanish and Italian banks have much lower NPLs and enjoy much more robust Tier-1 capital ratios than they did a decade ago (Chart 14). As a result, the doom-loop that plagued those economies ten years ago is not as pronounced. In fact, bank lending rates in Italy and Spain are now lower than they are in Germany, which contrasts greatly with the previous decade (Chart 14, bottom panel). Chart 13Exposure To The Home Country

Exposure To The Home Country

Exposure To The Home Country

Chart 14Improved Bank Health In The Periphery

Improved Bank Health In The Periphery

Improved Bank Health In The Periphery

Bottom Line: Bonds around the world and in Europe are massively oversold and are due for a countertrend rally. This pullback in yields, however, will be transitory. Higher trend nominal GDP growth around the world and in Europe indicates that yields have much further to rise over the next five years. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations

Executive Summary To understand the economy and the market we must think of them as non-linear systems which experience sudden phase-shifts. The pandemic introduced phase-shifts in our lives, which led to phase-shifts in our goods demand, which led to phase-shifts in monthly core inflation. As our lives phase-shift back to normality, goods demand will phase-shift back to low growth, and monthly core inflation prints will phase-shift from ‘high phase’ to ‘low phase’. With the 12-month core US inflation rate likely to peak by June at the latest, the long bond yield is likely to peak at some point in April/May, justifying a cyclical overweight position in T-bonds. Go overweight healthcare and biotech versus resources and financials. The leadership of the equity market will once more flip from short-duration sectors to long-duration sectors. Fractal trading watchlist additions: JPY/CHF, non-life insurance versus homebuilders, US homebuilders (XHB), cotton versus platinum, healthcare versus resources, and biotech versus resources.

The Bond Yield Turns About 2-3 Months Before Core Inflation

The Bond Yield Turns About 2-3 Months Before Core Inflation

Bottom Line: With the 12-month core US inflation rate likely to peak by June at the latest, the long bond yield is likely to peak at some point in April/May, and the leadership of the equity market will flip back to long-duration sectors such as healthcare and biotech. Feature Inflation is a non-linear system, meaning that you cannot just dial it up or down gradually like the volume on your music system. Instead of gradual changes, non-linear systems suddenly phase-shift from quiet to loud, from cold to hot, from solid to liquid, or from stability to instability (Box I-1). Box 1: A Classic Non-Linear System – A Brick On An Elastic Band To experience the sudden phase-shift in a non-linear system, attach an elastic band to a brick and try pulling it across a table. As you start to pull, the brick doesn’t move because of the friction with the table. But as you increase your pull there comes a tipping point, at which the brick does move and the friction simultaneously decreases, self-reinforcing the brick’s acceleration. Meanwhile, your pull on the elastic continues to increase as you react with a time-lag. The result is that this non-linear system suddenly phase-shifts from stability – the brick doesn’t move – to instability – the brick hits you in the face! Try as hard as you might, it is impossible to pull the brick across the table smoothly. In this non-linear system, the choice is either stability or instability. Back in 2017, in Mission Impossible: 2% Inflation – An Update, I posed a crucial question: “Given that price stability could phase-shift to instability, when should we worry about it?” I answered that “the risk remains low until the next severe downturn – when policymakers may be forced into desperate measures for a desperate situation.” The words proved prescient. Three years later, the desperate situation was a global pandemic, and the desperate measures were economic shutdowns combined with fiscal stimuluses of unprecedented scope and size. A Phase-Shift In Our Lives Produced A Phase-Shift In Inflation Developed economy inflation has just experienced a stark non-linearity. Since 2007, the US core month-on-month inflation rate remained consistently below 3.5 percent.1 Then came the pandemic’s shutdowns combined with policymakers’ massive response, and month-on-month inflation didn’t just rise to above 3.5 percent, it phase-shifted to well over 6 percent. Developed economy inflation has just experienced a stark non-linearity. The remarkable fact is that since 2007, there have been over a hundred monthly core inflation prints below 4 percent, and nine prints above 6 percent, but just one solitary print between 4 and 6 percent! In other words, monthly core inflation shows the classic hallmark of a non-linear system. It can be cold or hot, but not warm (Chart I-1). Chart I-1Monthly Core Inflation Shows The Classic Hallmark Of A Non-Linear System

Monthly Core Inflation Shows The Classic Hallmark Of A Non-Linear System

Monthly Core Inflation Shows The Classic Hallmark Of A Non-Linear System

So, what caused the phase-shift in core inflation? The simple answer is a phase-shift in durable goods spending, which itself was caused by the pandemic’s shutdown of services combined with massive fiscal stimulus. Again, this is supported by a remarkable fact. Since 2007, the monthly increase in US (real) spending on durables remained consistently below 3.5 percent. Then came the pandemic’s shutdowns and stimulus checks, and the growth in durables demand didn’t just rise to above 3.5 percent, it phase-shifted to well over 8 percent. In other words, the growth in durable goods demand also shows the classic hallmark of a non-linear system. It can be cold or hot, but not warm (Chart I-2). Chart I-2Goods Demand Shows The Classic Hallmark Of A Non-Linear System

Goods Demand Shows The Classic Hallmark Of A Non-Linear System

Goods Demand Shows The Classic Hallmark Of A Non-Linear System

The connection between the phase-shifts in goods demand and the phase-shifts in core inflation is staring us in the face – because the three separate phase-shifts in inflation have each been associated with a preceding or contemporaneous phase-shift in goods demand, which themselves have been associated with the separate waves of the pandemic (Chart I-3). Chart I-3Phase-Shifts In Core Inflation Have Been Associated With Phase-Shifts In Goods Demand

Phase-Shifts In Core Inflation Have Been Associated With Phase-Shifts In Goods Demand

Phase-Shifts In Core Inflation Have Been Associated With Phase-Shifts In Goods Demand

Pulling all of this together, the pandemic introduced phase-shifts in our lives – lockdown or freedom. Which led to phase-shifts in our goods demand – above 8 percent or below 3.5 percent. Which led to phase-shifts in monthly core inflation – above 6 percent or below 4 percent. The key question is, what happens next? Bond Yields Are Close To A Peak As we learn to live with the pandemic, and assuming no imminent ‘super variant’ of the virus, our lives are phase-shifting back to a semblance of normality. Which means that our spending on goods is phase-shifting back to low growth. If anything, the recent overspend on goods implies an imminent corrective underspend. At the same time, it will be difficult to compensate a phase-shift down on goods spending with a phase-shift up on services spending. This is because the consumption of services is constrained by time and biology. There is a limit to how often you can eat out, go to the theatre, or even go on vacation. The upshot is that monthly core inflation prints are likely to phase-shift from ‘high phase’ to ‘low phase’ – even if the monthly headline inflation prints are kept up longer by the commodity price spikes that result from the Ukraine crisis. Monthly core inflation prints are likely to phase-shift from ‘high phase’ to ‘low phase’. Meanwhile central banks and markets focus on the 12-month core inflation rate – which, as an arithmetic identity, is the sum of the last twelve month-on-month inflation rates.2 To establish the 12-month core inflation rate, the crucial question is: how many of the last twelve month-on-month inflation prints will be high phase versus low phase? As just discussed, the new month-on-month core inflation prints are likely to phase-shift to low phase. At the same time, the historic high phase prints will disappear from the last twelve month window. Specifically, by June 2022, the three high phase prints of April, May, and June 2021 – 10 percent, 9 percent, and 10 percent respectively – will no longer be included in the 12-month core inflation rate, with the arithmetic impact of pulling it down sharply (Chart I-4). Chart I-4The High Phase Monthly Inflation Prints Of April, May, And June 2021 Will Disappear From The 12-Month Core US Inflation Rate, Thereby Pulling It Down.

The High Phase Monthly Inflation Prints Of April, May, And June 2021 Will Disappear From The 12-Month Core US Inflation Rate, Thereby Pulling It Down.

The High Phase Monthly Inflation Prints Of April, May, And June 2021 Will Disappear From The 12-Month Core US Inflation Rate, Thereby Pulling It Down.

Clearly, the bond market anticipates some of this ‘base effect’ on 12-month inflation. This explains why turning points in the bond yield have led by 2-3 months the turning points in the 12-month core inflation rate (Chart I-5). With the 12-month core inflation rate likely to peak by June at the latest, this suggests that – absent some new shock – the long bond yield is likely to peak at some point in April/May. Reinforcing our cyclical overweight position in T-bonds. Chart I-5The Bond Yield Turns About 2-3 Months Before Core Inflation

The Bond Yield Turns About 2-3 Months Before Core Inflation

The Bond Yield Turns About 2-3 Months Before Core Inflation

This also carries important implications for equity investors. Rising bond yields favour short-duration equity sectors such as resources and financials versus long-duration equity sectors such as healthcare and biotech. And vice-versa. Indeed, the recent performance of resources versus healthcare and financials versus healthcare is indistinguishable from the bond yield (Chart I-6 and Chart I-7). Chart I-6The Performance of Resources Versus Healthcare Is Indistinguishable From The Bond Yield

The Performance of Resources Versus Healthcare Is Indistinguishable From The Bond Yield

The Performance of Resources Versus Healthcare Is Indistinguishable From The Bond Yield

Chart I-7The Performance of Financials Versus Healthcare Is Indistinguishable From The Bond Yield

The Performance of Financials Versus Healthcare Is Indistinguishable From The Bond Yield

The Performance of Financials Versus Healthcare Is Indistinguishable From The Bond Yield

With bond yields likely to peak soon, the leadership of the equity market will once more flip from short-duration sectors to long-duration sectors. Go overweight healthcare and biotech versus resources and financials. Fractal Trading Watchlist Reinforcing the fundamental analysis in the previous section, the 130-day outperformance of resources versus healthcare and biotech has reached the point of fractal fragility that has marked previous trend exhaustions, suggesting that the recent outperformance of resources is nearing an end. Also new on our watchlist is a commodity pair, cotton versus platinum, whose strong outperformance is vulnerable to reversal. And US homebuilders (XHB), whose recent underperformance is at a potential turning point. There are two new trade recommendations. First, the massive outperformance of world non-life insurance versus homebuilders is at the point of fractal fragility that has consistently marked previous turning points (Chart I-8). Hence, go short non-life insurance versus homebuilders, setting a profit target and symmetrical stop-loss at 14 percent. Second, the strong underperformance of the Japanese yen is also at the point of fractal fragility that has marked several previous turning points (Chart I-9). Accordingly, go long JPY/CHF, setting a profit target and symmetrical stop-loss at 4 percent. Please note that our full watchlist of 19 investments that are experiencing or approaching turning points is now available on our website: cpt.bcaresearch.com Chart I-8The Massive Outperformance Of Non-Life Insurance Is Vulnerable To Reversal

The Massive Outperformance Of Non-Life Insurance Is Vulnerable To Reversal

The Massive Outperformance Of Non-Life Insurance Is Vulnerable To Reversal

Chart I-9Go Long JPY/CHF

Go Long JPY/CHF

Go Long JPY/CHF

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

Cotton’s Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

US Homebuilders’ Underperformance Is At A Potential Turning Point

US Homebuilders' Underperformance Is At A Potential Turning Point

US Homebuilders' Underperformance Is At A Potential Turning Point

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Annualized month-on-month inflation rate. 2 Strictly speaking, the 12-month inflation rate is the geometric product of the last 12 month-on-month inflation rates. Chart I-1The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart I-2The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart I-3AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart I-4Canada Versus Japan Is Vulnerable To Reversal

Canada Versus Japan Is Vulnerable To Reversal

Canada Versus Japan Is Vulnerable To Reversal

Chart I-5Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart I-6US Healthcare Providers Vs. Software Approaching A Reversal

US Healthcare Providers Vs. Software Approaching A Reversal

US Healthcare Providers Vs. Software Approaching A Reversal

Chart I-7The Euro's Underperformance Could Be Approaching a Resistance Level

The Euro's Underperformance Could Be Approaching a Resistance Level

The Euro's Underperformance Could Be Approaching a Resistance Level

Chart I-8A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart I-9Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Chart I-10Biotech Approaching A Major Buy

Biotech Approaching A Major Buy

Biotech Approaching A Major Buy

Chart I-11CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart I-12Financials Versus Industrials Is Reversing

Financials Versus Industrials Is Reversing

Financials Versus Industrials Is Reversing

Chart I-13Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart I-14Greece's Brief Outperformance Has Ended

Greece's Brief Outperformance Has Ended

Greece's Brief Outperformance Has Ended

Chart I-15BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart I-16The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart I-17The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

Chart I-18Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Chart I-19US Homebuilders' Underperformance Is At A Potential Turning Point

US Homebuilders' Underperformance Is At A Potential Turning Point

US Homebuilders' Underperformance Is At A Potential Turning Point

Fractal Trading System Fractal Trades

Fat-Tailed Inflation Signals A Peak In Bond Yields

Fat-Tailed Inflation Signals A Peak In Bond Yields

Fat-Tailed Inflation Signals A Peak In Bond Yields

Fat-Tailed Inflation Signals A Peak In Bond Yields

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

According to BCA Research’s US Bond Strategy service, current spread levels offer a good opportunity to reduce corporate bond exposure. Corporate spreads have rallied to within striking distance of their pre-COVID lows at the same time as the yield curve…

Our Global Fixed Income strategists’ Global Duration Indicator is comprised of three elements: BCA Research’s Global Leading Economic Indicator, the Global Leading Economic Indicator’s diffusion index, and economic expectations indices from the ZEW. The…

Highlights Chart 1Reduce Credit Exposure

Reduce Credit Exposure

Reduce Credit Exposure

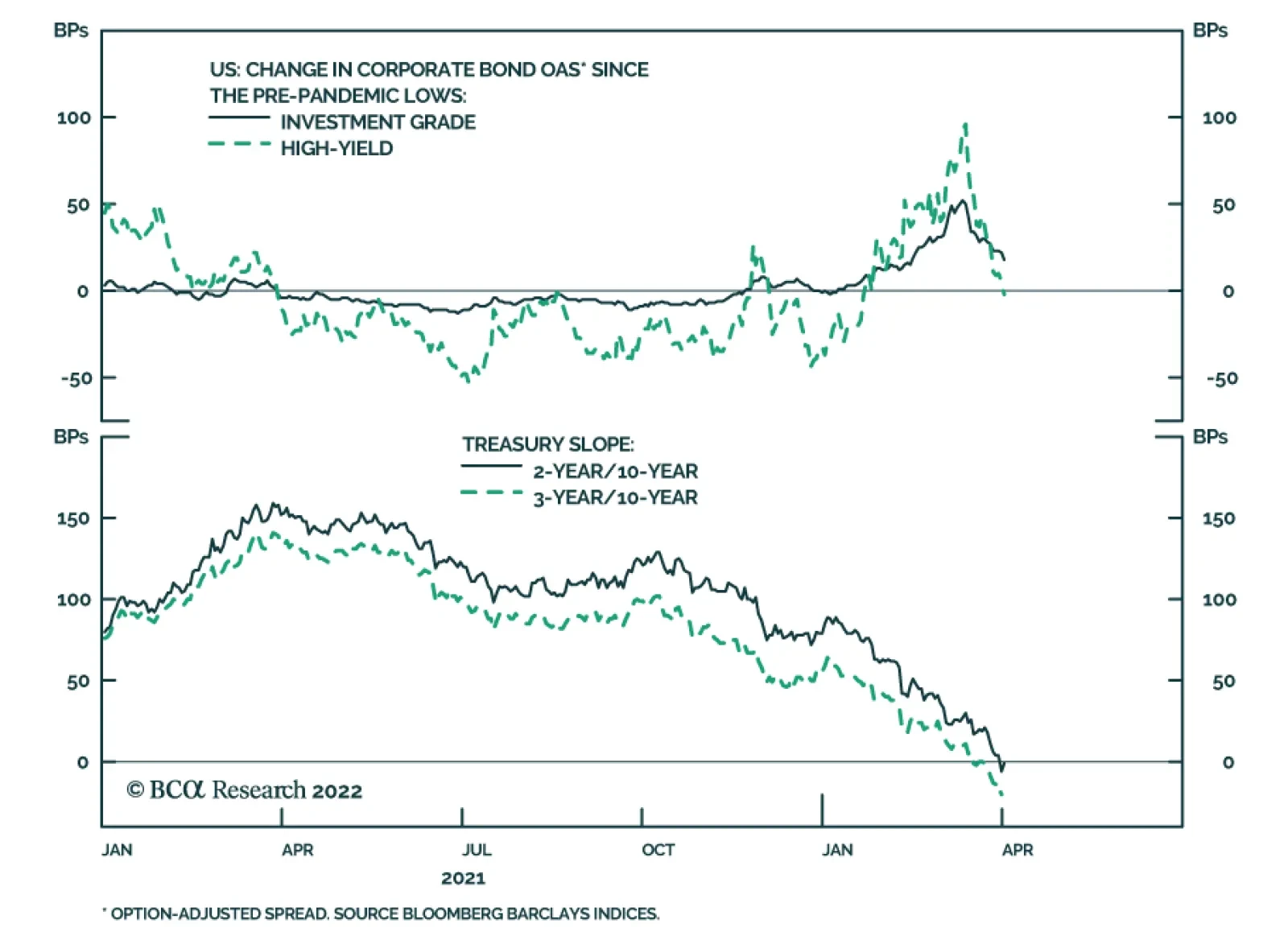

Corporate bond spreads staged a nice rally during the past month. The average index spread for investment grade corporates is only 22 bps above its pre-COVID low and 33 bps above last year’s trough. The average High-Yield index spread is 5 bps above its pre-COVID low and 49 bps above last year’s trough (Chart 1). This rally occurred even as inflation data continued to surprise to the upside and employment data confirmed that the US labor market is extremely tight. With the economic data justifying the Fed’s hawkish pivot, the Treasury curve has flattened dramatically, and both the 2-year/10-year and 3-year/10-year slopes are now inverted (Chart 1, bottom panel). An inverted yield curve is a reliable late-cycle indicator, and we think current spread levels offer a good opportunity to reduce corporate bond exposure. This week, we downgrade investment grade corporates from neutral (3 out of 5) to underweight (2 out of 5) and high-yield corporates from overweight (4 out of 5) to neutral (3 out of 5), placing the proceeds into Treasuries. We also downgrade our recommended allocations EM Sovereigns (see page 8) and TIPS (see page 11), upgrade our recommended allocation to CMBS (see page 13) and adjust our recommended yield curve positioning (see page 10). Feature Table 1Recommended Portfolio Specification

The Beginning Of The End

The Beginning Of The End

Table 2Fixed Income Sector Performance

The Beginning Of The End

The Beginning Of The End

Investment Grade: Underweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 86 basis points in March, bringing year-to-date excess returns up to -154 bps. Our quality-adjusted 12-month breakeven spread shifted down to its 21st percentile since 1995 (Chart 2). As noted on the first page of this report, corporate spreads have rallied to within striking distance of their pre-COVID lows at the same time as the yield curve has become inverted beyond the 2-year maturity. We showed in last week’s report that an inversion of the 2-year/10-year Treasury slope is not necessarily a harbinger of imminent recession, but it does typically coincide with very low (and often negative) excess corporate bond returns.1 The combination of reasonably tight spreads and an inverted yield curve causes us to recommend downgrading investment grade corporate bond allocations from neutral (3 out of 5) to underweight (2 out of 5). It’s important to note that corporate balance sheets remain healthy (bottom panel) and we see no indication that a recession or default cycle will unfold during the next 6-12 months. That said, we must acknowledge that an inverted yield curve signals that the economic recovery is entering its late stages. Economic growth will be slower going forward and corporate spreads are unlikely to tighten much, especially from current depressed levels. Against this backdrop it makes sense to be more cautious on credit, sacrificing small positive excess returns in the near-term to ensure that we aren’t invested when the next downturn hits. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Beginning Of The End

The Beginning Of The End

Table 3BCorporate Sector Risk Vs. Reward*

The Beginning Of The End

The Beginning Of The End

High-Yield: Neutral Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 119 basis points in March, bringing year-to-date excess returns up to -96 bps. The 12-month spread-implied default rate – the default rate that is priced into the junk index assuming a 40% recovery rate on defaulted debt and an excess spread of 100 bps – shifted down to 3.7% (Chart 3). An inverted yield curve sends the same negative signal for high-yield excess returns as it does for investment grade. However, high-yield valuation is currently more attractive. The option-adjusted spread differential between Ba-rated bonds and Baa-rated bonds remains elevated at 86 bps, 41 bps above its pre-COVID low (panel 3). It is also likely that economic growth will remain sufficiently strong for defaults to come in below the spread-implied threshold of 3.7% during the next 12 months (bottom panel). The greater attractiveness of high-yield valuations relative to investment grade causes us to maintain a higher allocation to the sector, even as we downgrade our portfolio’s overall credit risk exposure. We therefore recommend a neutral (3 out of 5) allocation to high-yield corporates. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 14 basis points in March, dragging year-to-date excess returns down to -74 bps. The zero-volatility spread for conventional 30-year agency MBS tightened 3 bps on the month as a 4 bps tightening of the option-adjusted spread (OAS) was partially offset by a 1 bp increase in the compensation for prepayment risk (option cost) (Chart 4). We wrote in a recent report that MBS’ poor performance in 2021 was attributable to an option cost that was too low relative to the pace of mortgage refinancings, noting that the MBA Refinance Index was slow to fall in 2021 despite the back-up in yields.2 This valuation picture is starting to change. The option cost is now up to 40 bps, its highest level since 2016, and refi activity is slowing as the Fed lifts rates. At 28 bps, the index OAS remains unattractive. However, the elevated option cost raises the possibility that the OAS may be over-estimating the pace of mortgage refinancings for the first time in a while. If these trends continue, it may soon make sense to increase exposure to agency MBS. Emerging Market Bonds (USD): Underweight Chart 5Emerging Markets Overview

Emerging Markets Overview

Emerging Markets Overview

Emerging Market bonds underperformed the duration-equivalent Treasury index by 23 basis points in March, dragging year-to-date excess returns down to -505 bps. EM Sovereigns outperformed the Treasury benchmark by 40 bps on the month, bringing year-to-date excess returns up to -609 bps. The EM Corporate & Quasi-Sovereign Index underperformed by 62 bps, dragging year-to-date excess returns down to -439 bps. The EM Sovereign Index underperformed the duration-equivalent US corporate bond index by 7 bps in March. This comes on the heels of a sharp underperformance in February that was driven by Russian bonds which have since been removed from the index. Russian bonds have also been purged from the EM Corporate & Quasi-Sovereign Index, and this index underperformed duration-matched US corporates by 11 bps in March (Chart 5). The yield differential between EM sovereigns and duration-matched US corporates remains negative. As such, we downgrade our recommended allocation to EM sovereigns from underweight (2 out of 5) to maximum underweight (1 out of 5). In sharp contrast, the EM Corporate & Quasi-Sovereign Index continuous to offer a significant yield advantage (panel 4). We retain our neutral (3 out of 5) recommendation for EM Corporates & Quasi-Sovereigns. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds outperformed the duration-equivalent Treasury index by 5 basis points in March, bringing year-to-date excess returns up to -122 bps (before adjusting for the tax advantage). While the war in Ukraine has introduced a great deal of uncertainty into the economic outlook, the municipal bond sector should be better placed than most to deal with the fallout. Trailing 4-quarter net state & local government savings are incredibly high (Chart 6) and 2021’s federal spending splurge will continue to support state & local government coffers for some time. On the valuation front, munis have cheapened up relative to both Treasuries and corporates during the past two months. The 10-year Aaa Muni / Treasury yield ratio is currently at 94%, up significantly from its 2021 trough of 55%. The yield ratios between 12-17 year munis and duration-matched corporate bonds are also up significantly off their lows (panel 2). We reiterate our overweight allocation to municipal bonds within US fixed income portfolios, and we continue to have a strong preference for long-maturity munis. The yield ratio between 17-year+ General Obligation Municipal bonds and duration-matched corporates is 93%. The same measure for 17-year+ Revenue bonds stands at 101%, meaning that Revenue bonds carry a before-tax yield advantage versus duration-matched corporates. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve’s bear-flattening trend continued through March. The 2-year/10-year Treasury slope flattened 35 bps on the month and the 5-year/30-year Treasury slope flattened 44 bps. These slopes are now both inverted, sitting at -6 bps and -12 bps respectively. In last week’s report we noted the unusually wide divergence between very flat slopes at the long end of the yield curve and very steep slopes at the front end.3 For example, the 5-year/10-year Treasury slope is -18 bps but the 3-month/5-year slope is 204 bps. This divergence is happening because the market has moved quickly to price-in a rapid near-term pace of rate hikes that will end in roughly one year. However, so far, the Fed has only delivered 25 bps of those hikes and this is holding down the very front-end of the curve. The oddly shaped curve presents us with an excellent trading opportunity. Specifically, we recommend buying the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. This trade looks attractive on our model (Chart 7) and will profit if the rate hike cycle moves more slowly than what is currently priced in the market but lasts longer, as is our expectation. By entering our new 5-year bullet over 2-year/10-year barbell trade we also close our previous 2-year bullet over cash/10-year barbell trade at a loss. We continue to recommend a position long the 20-year bullet versus a duration-matched 10/30 barbell as an attractive carry trade. TIPS: Underweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 143 basis points in March, bringing year-to-date excess returns up to +271 bps. The 10-year TIPS breakeven inflation rate rose 22 bps on the month and the 5-year/5-year forward TIPS breakeven inflation rate rose 21 bps. Since last May we have been recommending that clients maintain a neutral allocation to TIPS versus nominal Treasuries at the long end of the curve and an underweight allocation to TIPS at the front end. This recommendation was premised on the view that the breakeven curve would steepen as falling inflation put downward pressure on short-maturity TIPS breakevens and long-dated breakevens remained at levels close to the Fed’s target. Recently, the 10-year TIPS breakeven inflation rate has shot up to levels well above the Fed’s 2.3%-2.5% target range (Chart 8) and our TIPS Breakeven Valuation Indictor has shifted into “expensive” territory (panel 2). Further, while inflation has remained high for longer than we expected, it still seems more likely than not that it will roll over between now and the end of the year as pandemic fears fade and consumers shift their spending patterns away from goods and toward services. As such, we think investors should take this opportunity to further reduce exposure to TIPS versus nominal Treasuries at both the short and long ends of the curve. That is, within our overall underweight allocation to TIPS we continue to recommend positioning in breakeven curve steepeners and in real yield curve flatteners. We also continue to recommend an outright short position in 2-year TIPS. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 26 basis points in March, dragging year-to-date excess returns down to -31 bps. Aaa-rated ABS underperformed by 21 bps on the month, dragging year-to-date excess returns down to -27 bps. Non-Aaa ABS underperformed by 49 bps on the month, dragging year-to-date excess returns down to -51 bps. During the past two years, substantial federal government support for household incomes has caused US households to build up an extremely large buffer of excess savings. During this period, many households have used their windfalls to pay down consumer debt and credit card debt levels have fallen to well below pre-COVID levels (Chart 9). Though consumer credit growth has rebounded, debt levels are still low. This indicates that the collateral quality backing consumer ABS remains exceptionally strong. This also indicates that while surging gasoline prices will weigh on consumer activity in the coming months, household balance sheets are starting from such a good place that we don’t expect a meaningful increase in consumer credit delinquencies. Investors should remain overweight consumer ABS and should take advantage of the high quality of household balance sheets by moving down the quality spectrum, favoring non-Aaa rated securities over Aaa-rated ones. Non-Agency CMBS: Overweight Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 20 basis points in March, bringing year-to-date excess returns up to -78 bps. Aaa Non-Agency CMBS outperformed Treasuries by 25 bps on the month, bringing year-to-date excess returns up to -67 bps. Non-Aaa Non-Agency CMBS underperformed by 5 bps on the month, dragging year-to-date excess returns down to -110 bps. CMBS spreads remain wide compared to other similarly risky spread products. Further, commercial real estate (CRE) lending standards have recently shifted into “net easing” territory and demand for CRE loans is strengthening (Chart 10). In light of today’s downgrade of corporate credit, non-agency CMBS look like an attractive alternative to add some spread to a portfolio. Increase exposure from neutral (3 out of 5) to overweight (4 out of 5). Agency CMBS: Overweight Agency CMBS underperformed the duration-equivalent Treasury index by 17 basis points in March, dragging year-to-date excess returns down to -39 bps. The average index option-adjusted spread widened 5 bps on the month. It currently sits at 48 bps, not that far from its average pre-COVID level (bottom panel). Agency CMBS spreads also continue to look attractive compared to other similarly risky spread products. Stay overweight. Appendix A: The Golden Rule Of Bond Investing We follow a two-step process to formulate recommendations for bond portfolio duration. First, we determine the change in the federal funds rate that is priced into the yield curve for the next 12 months. Second, we decide – based on our assessments of the economy and Fed policy – whether the change in the fed funds rate will exceed or fall short of what is priced into the curve. Most of the time, a correct answer to this question leads to the appropriate duration call. We call this framework the Golden Rule Of Bond Investing, and we demonstrated its effectiveness in the US Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018. Chart 11 illustrates the Golden Rule’s track record by showing that the Bloomberg Barclays Treasury Master Index tends to outperform cash when rate hikes fall short of 12-month expectations, and vice-versa. At present, the market is priced for 255 basis points of rate hikes during the next 12 months. Chart 11The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

We can also use our Golden Rule framework to make 12-month total return and excess return forecasts for the Bloomberg Barclays Treasury index under different scenarios for the fed funds rate. Excess returns are relative to the Bloomberg Barclays Cash index. To forecast total returns we first calculate the 12-month fed funds rate surprise in each scenario by comparing the assumed change in the fed funds rate to the current value of our 12-month discounter. This rate hike surprise is then mapped to an expected change in the Treasury index yield using a regression based on the historical relationship between those two variables. Finally, we apply the expected change in index yield to the current characteristics (yield, duration and convexity) of the Treasury index to estimate total returns on a 12-month horizon. The below tables present those results, along with excess returns for a front-loaded and a back-loaded rate hike scenario. Excess returns are calculated by subtracting assumed cash returns in each scenario from our total return projections.

The Beginning Of The End

The Beginning Of The End

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of March 31, 2022)

The Beginning Of The End

The Beginning Of The End

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of March 31, 2022)

The Beginning Of The End

The Beginning Of The End

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of -55 bps in the 5 over 2/10 cell means that we would expect the 5-year to outperform the 2/10 if the 2/10 slope flattens by less than 55 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Beginning Of The End

The Beginning Of The End

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 12Excess Return Bond Map (As Of March 31, 2022)

The Beginning Of The End

The Beginning Of The End

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy / US Investment Strategy / US Equity Strategy Special Report, “The Yield Curve As An Indicator”, dated March 29, 2022. 2 Please see US Bond Strategy Weekly Report, “The Omicron Impact”, dated November 30, 2021. 3 Please see US Bond Strategy / US Investment Strategy / US Equity Strategy Special Report, “The Yield Curve As An Indicator”, dated March 29, 2022. Recommended Portfolio Specification

The Beginning Of The End

The Beginning Of The End

Other Recommendations

The Beginning Of The End

The Beginning Of The End

Treasury Index Returns Spread Product Returns

Executive Summary Our recommended model bond portfolio outperformed its custom index by a robust +48bps in Q1/2022 – an impressive performance given the significant uncertainties stemming from the Ukraine war, surging commodity prices and hawkish central banks. This outperformance came entirely from the rates side of the portfolio (+52bps) as global government bond yields surged, driven by a large underweight to US Treasuries. The credit side of the portfolio was largely unchanged versus the benchmark (-4bps). Looking ahead, we see global bond yields as being more rangebound over the next six months. A lot of rate hikes in 2022 are already discounted (most notably in the US) and global inflation is likely to decelerate in Q2 & Q3. As the global monetary tightening cycle evolves, positioning more defensively in global credit, rather than duration management, will provide the better opportunity to generate alpha in bond portfolios. GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase

GFIS Model Bond Portfolio Q1/2022 Review & Outlook: Trading The Consolidation Phase