Fixed Income

Listen to a short summary of this report. Executive Summary Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

It is still possible that equities can outperform bonds over the next 12 months, but the risks to this are rising. Inflation may surprise further to the upside, amid rising commodity prices, pushing the Fed to tighten aggressively. Tighter financial conditions augur badly for growth (see Chart). We cut our recommendation for global equities to neutral and increase our allocation to cash. We continue to prefer the lower-beta US stock market over the euro zone and Emerging Markets. We are overweight defensive and structural growth sectors: Healthcare, Consumer Staples, IT and Industrials. Government bond yields have limited upside from here to year-end. We are neutral duration. US high-yield bonds are attractive: They are pricing in a big rise in defaults this year, which we see as unlikely. Recommendation Changes

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Bottom Line: Rising uncertainty warrants a more defensive stance. Prudent investors should have only a benchmark weight in equities, and look for other hedges against downside risk. Overview Recommended Allocation

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Rather like Arnold Toynbee’s definition of history, markets in the past few months have been hit by “just one damned thing after another”. But, despite war in Ukraine, big upward surprises to inflation, and a swift aggressive turn by the Fed, global equities are only 6% off their all-time high. It is still possible that equities may outperform bonds over the next 12 months and that the global economy will avoid recession (Chart 1). But the risks to this are rising. We recommend, therefore, that prudent investors reduce their equity holdings to benchmark weight and generally have somewhat defensive portfolio positioning. We put the money raised from going neutral on equities into cash, not bonds. What are the risks? Inflation could surprise further to the upside. Inflation has spread beyond a few pandemic-related items to goods where prices are usually sticky (Chart 2). There are now clear signs that price rises are feeding through to wage increases in the US, UK and Canada – though not yet in the euro area, Japan or Australia (Chart 3). The supply response that we expected to see emerge later this year may be delayed because of Covid lockdowns in China and disruptions in supply from Russia and Ukraine (Chart 4). Consensus forecasts for US core PCE inflation see it coming down to 2.5% by next year. The risk is that it could exceed that. The Fed has got way behind the curve. In retrospect, it should have raised rates last summer – and it now understands its error. Its first hike this cycle came only when the economy had already overheated (Chart 5). The Fed may, therefore, be tempted to get rates up very quickly – something the futures market is now pricing in, since it implies that the year-end Fed Funds Rate will be 2.5%. An aggressive Fed cycle – propelled by inflation fears – is not a good environment for risk assets. Chart 1Can Stocks Keep On Outperforming Bonds?

Can Stocks Keep On Outperforming Bonds?

Can Stocks Keep On Outperforming Bonds?

Chart 2Even Sticky Prices Are Now Rising

Even Sticky Prices Are Now Rising

Even Sticky Prices Are Now Rising

Chart 3Price Rises Feeding Through To Wages In Some Regions

Price Rises Feeding Through To Wages In Some Regions

Price Rises Feeding Through To Wages In Some Regions

Chart 4Supply Chains Remain Disrupted

Supply Chains Remain Disrupted

Supply Chains Remain Disrupted

Financial conditions had already tightened before the Fed hiked because of higher long-term rates, widening credit spreads, and a strengthening dollar. The Goldman Sachs Financial Conditions Index points to the ISM Manufacturing Index falling below 50 later this year (Chart 6). That is the level that historically has been the dividing line between stocks outperforming bonds year-over-year (Chart 7). In particular, the sharp rise in long-term rates (the US 10-year Treasury yield has risen by 110 BPs, and the German yield by 93 BPs over the past seven months) could start to put some pressure on housing markets (Chart 8). Chart 5The Fed Hiked Too Late

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Chart 6Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Tighter Financial Conditions May Affect Growth

Chart 7Will PMIs Fall Below 50?

Will PMIs Fall Below 50?

Will PMIs Fall Below 50?

Chart 8Rising Rates Might Dampen The Housing Market

Rising Rates Might Dampen The Housing Market

Rising Rates Might Dampen The Housing Market

The war in Ukraine is unlikely to be a risk in itself. BCA Research’s geopolitical strategists think it very improbable that the conflict will spill beyond the borders of Ukraine – though there remains tail risk of a mistake. But the war is having a big impact on energy prices, especially electricity prices in Europe (Chart 9). The oil price could remain high while Russian oil, which used to be consumed in Europe, is diverted elsewhere. Our Commodity & Energy Strategy service expects that increased supply from OPEC members will bring Brent crude down to around $90 a barrel by year-end. But, as our Client Question on page 14 details, that calculation relies on many assumptions, and the risk is that the oil price stays high. A doubling of the oil price year-on-year (which currently equates to $120/barrel) has historically often been followed by recession (Chart 10). Chart 9Europe's Electricity Prices Have Soared

Europe's Electricity Prices Have Soared

Europe's Electricity Prices Have Soared

Chart 10Oil Price Is Close To The Risk Level

Oil Price Is Close To The Risk Level

Oil Price Is Close To The Risk Level

China has been easing fiscal and monetary policy. But it is questionable how effective its stimulus will be this time. Confidence in the real estate market remains damaged. And the pick-up in credit growth has been limited to local government bond issuance; there is little sign that the private sector has appetite to borrow (Chart 11). Already some of these risks are affecting economic data. Consumer confidence has collapsed, presumably because of the rising cost of living (Chart 12). Although US activity indicators such as the manufacturing ISM remain elevated (see Chart 6 above), data in Europe is showing notable weakness (Chart 13). Chart 11China's Stimulus Not Helping The Private Sector

China's Stimulus Not Helping The Private Sector

China's Stimulus Not Helping The Private Sector

Chart 12Consumer Confidence Has Been Hit

Consumer Confidence Has Been Hit

Consumer Confidence Has Been Hit

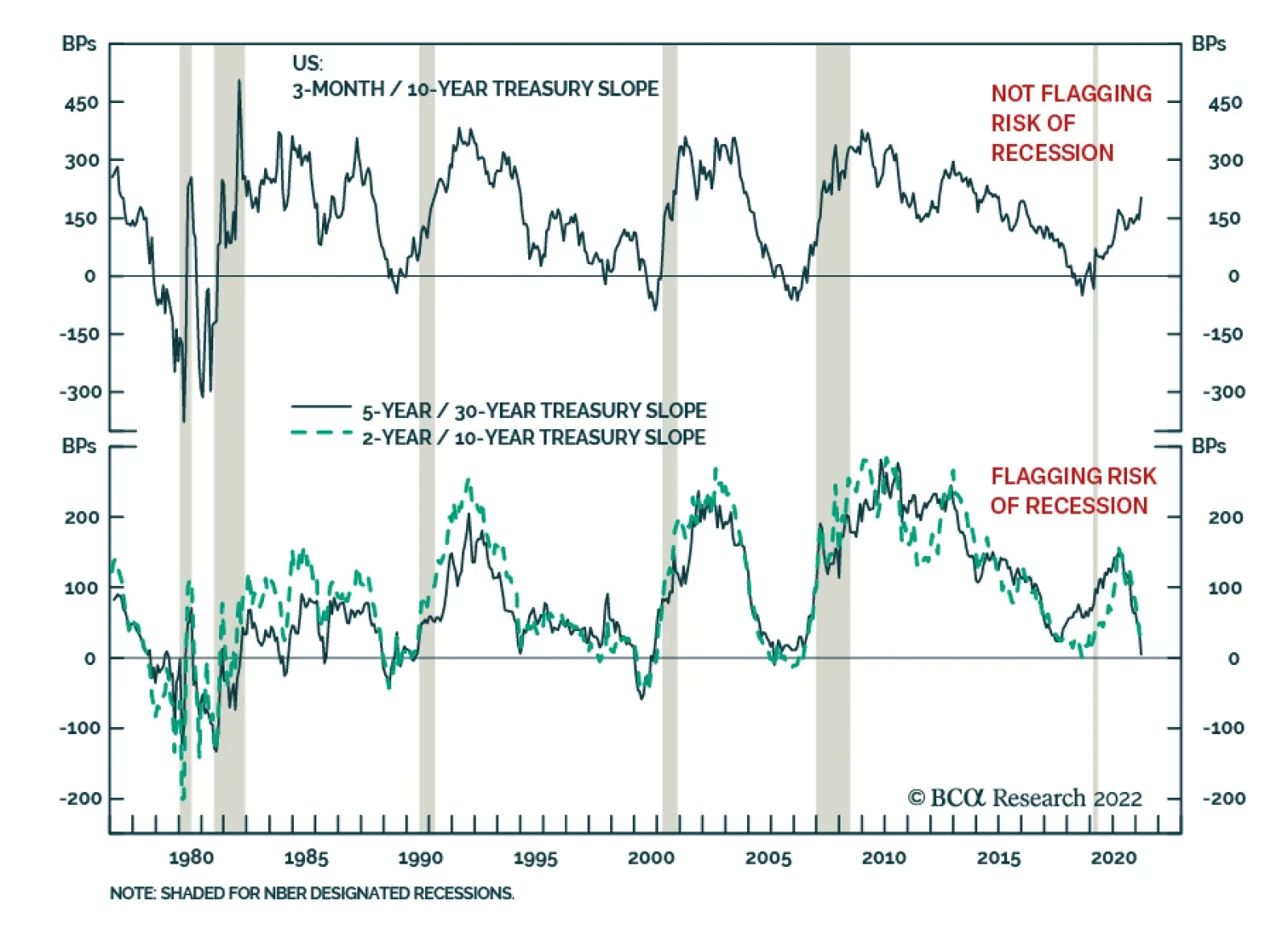

The yield curve is also getting close to signaling recession. There has been much debate of late about which yield curve to use, with Fed Chair Jerome Powell arguing for the 3-month/3-month 18-month forward curve, rather than the more usual 2/10 year or 3 month/10 year curves (Chart 14). The 2/10 is close to inverting, while the others are still a long way away. All measures of the yield curve have historically given reliable recession signals; the difference is simply a matter of timing, with the 2/10 giving the longest lead time.1 If the Fed ends up tightening as much as it intends, all the yield curves will likely invert within the next year or so. Chart 13European Data Starting To Weaken

European Data Starting To Weaken

European Data Starting To Weaken

Chart 14It Depends On Which Yield Curve You Look At

It Depends On Which Yield Curve You Look At

It Depends On Which Yield Curve You Look At

And, despite all these warning signals, forecasts for economic and earnings growth have not been revised down much. Economists still expect 3.4-3.5% real GDP growth in the US and euro zone this year, well above trend (Chart 15). And, despite the drop in GDP forecasts, earnings forecasts have actually been revised up since the start of the year, with analysts now expecting 9.6% EPS growth in the US and 8.2% in the euro zone (Chart 16). Chart 15GDP Growth Is Still Expected To Be Above Trend...

GDP Growth Is Still Expected To Be Above Trend...

GDP Growth Is Still Expected To Be Above Trend...

Chart 16...And Earnings Have Not Been Revised Down At All

...And Earnings Have Not Been Revised Down At All

...And Earnings Have Not Been Revised Down At All

This all seems too much uncertainty for most asset allocators to want to stay fully risk-on. There are valid arguments that equities and other risk assets can continue to perform (which we outline in the following section, Risks To Our View). But the risks have shifted enough since the start of the year that a more defensive stance is now warranted. Garry Evans, Senior Vice President Global Asset Allocation garry@bcaresearch.com Risks To Our View Chart 17Fed Feedback Loop Back In Action?

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Since our main scenario is somewhat cautious – and sentiment towards risk assets pretty pessimistic – we need to consider what could cause upside surprises to the economy and market. The most likely would be if the Fed were to turn more dovish. But the main trigger for this would be if the stock market fell sharply or growth showed clear signs of slowing – which would obviously be negative for stocks first. This scenario could produce the sort of Fed feedback loop we saw in 2015-17, when tightening financial conditions caused the Fed to ease back on rate hikes (Chart 17). More benign would be a gradual easing of inflation over the summer which would mean that the Fed could eventually hike a little less than the market currently expects. The economy may also not be as vulnerable to higher energy prices and higher rates as we fear. Food and energy are now a much smaller part of the consumption basket than they were in the 1970s (Chart 18). Rates may have a limited impact on the housing market, given the low inventory of new houses, strong household formation, and the fact that, in the US at least, some 90% of mortgages are 30-year fixed rate. Consumers continue to hold large amounts of excess savings – more than $2 trillion in the US alone. This should keep retail sales growth strong, though there might be some shift from spending on goods to spending on services as Covid fears recede (Chart 19). Chart 18Consumers Are Less Sensitive To Food And Energy Prices...

Consumers Are Less Sensitive To Food And Energy Prices...

Consumers Are Less Sensitive To Food And Energy Prices...

Chart 19...And So May Keep On Spending

...And So May Keep On Spending

...And So May Keep On Spending

Other upside risks include: A ceasefire and settlement in Ukraine (unlikely soon, since Russia will not withdraw without taking over Crimea and the Donbass, something Ukraine could not accept); more aggressive stimulus in China (possible, but only if Chinese growth weakened much further); and a sharp fall in the oil price caused by new supply coming onto the market from Saudi Arabia and North American shale fields, and possibly also Iran and Venezuela. What Our Clients Are Asking What Is The Risk Of Stagflation? Chart 20The Combination Of High Inflation And High Unemployment Was The Key Problem In The 1970s

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Several clients have asked about the risk of stagflation, and how the current episode compares to the 1970s. We can begin by dispelling some myths about the 1970s. There is a notion that this was a decade of poor growth for the US. That is simply not true. Real GDP grew by a solid 3.3% annual rate during the 1970s, higher than in any post-WW2 decade other than the 1990s and the 1960s (Chart 20, panel 1). The underlying problem during the 1970s was the combination of high inflation and a poor labor market. Despite solid growth, the unemployment rate kept grinding higher as inflation was increasing, never dropping below 4.5% even at the peaks of the expansions (Chart 20, panel 2). This situation went against the commonly held belief that it was not possible for both these variables to remain high at the same time for an extended period. With the economy plagued by both high inflation and high unemployment, the Fed faced a difficult dilemma: Keep interest rates too high and the already weak labor market would worsen; keep interest rates too low and inflation would spiral out of control. Throughout the decade, the Fed chose the latter option, causing inflation expectations to become unmoored. Chart 21Demographic Shocks And The Structure Of The Labor Force Led To A Weak Labor Market

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Why was there so much slack in the labor market? Demographics were one of the main culprits. The entrance of baby boomers into the workforce dramatically increased the pool of workers. At the same time, prime-age female participation rose at the fastest pace on record, adding additional supply to the labor force (Chart 21, panel 1). The structure of the labor market also played a key role. Almost a third of employees belonged to a union and most of their salaries were indexed to inflation (Chart 21, panels 2 & 3). This made for a rigid labor market where neither employment nor wages could adjust properly to the economic cycle. True, the oil shocks of 1974 and 1979 exacerbated inflationary pressures. But what made inflation truly pernicious during the 1970s was the inability of the Fed to fight it without compromising its employment mandate. Today the economic picture is very different. Union membership stands at only 10% and cost of living adjustments have essentially disappeared. There is also no labor supply shock on the horizon comparable to the baby boomers or women entering the labor force. This makes the calculus for the Fed easy. With its employment mandate already met, it will simply keep raising rates until inflation is back under control. As a result, the risk that it keeps policy too easy and unleashes further inflationary pressures is relatively low over the next 12 months. How Will The War In Ukraine Affect The World Economy? Chart 22The Ukrainian War Has Impacted The Global Economy

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Global growth, monetary policy, and employment were projected to return to pre-pandemic trends in 2023. In January, the IMF projected global growth of 4.4% in 2022, but now it is poised to cut its forecast due to the war in Ukraine. According to OECD estimates, global economic growth could be 1% lower than what was previously predicted (Chart 22, panel 1). The conflict is putting fresh strain on overstretched global supply chains, causing the price of many commodities to surge. Russia and Ukraine are relatively small in terms of economic output (together they comprise only 1.9% of global GDP in US dollar terms). But they are very big producers and exporters of energy, metals, and key food items. Russia, for example, produces 12% of global oil, one-third of palladium, and (with Belarus) 40% of potash (used in fertilizers). Ukraine is also a major producer of auto parts, such as wire harnesses. Some European car manufacturers have had to idle factories due to a lack of components. Global central banks have been increasing interest rates to battle inflation. But higher energy and food prices will require additional rate hikes to ensure price stability. The war in Ukraine could push up world inflation by around 2.5% this year, according to the OECD. Developing economies are in a particularly tight spot, being hit with high inflation in food and basic commodities. Their consumer price indices are very sensitive to these items. Russia and Ukraine are the main global exporters of several agricultural items (for example, they together account for a quarter of global wheat exports) which could cause global food insecurity to increase (Chart 22, panel 2). International sanctions on Russia create a risk for foreign companies with operations there. Withdrawal could have a meaningful effect on earnings. Most multinationals have only limited exposure to Russia, but a small number of prominent names make more than 5% of global revenues from the country (Chart 22, panel 3). Chart 23AOPEC Is Able To Cover Supply Shortages...

OPEC Is Able To Cover Supply Shortages...

OPEC Is Able To Cover Supply Shortages...

Chart 23B...Unlike Other Countries...

...Unlike Other Countries...

...Unlike Other Countries...

Chart 23CTo Restore A Balanced But Tight Market

To Restore A Balanced But Tight Market

To Restore A Balanced But Tight Market

What Is The Risk That The Oil Price Stays High? Our Commodity & Energy strategists see 1.3mm b/d of supply from OPEC coming onto the market beginning in May. Because of this, they expect the price of Brent crude to fall back, to average $93 per barrel this year and next. OPEC core producers fear that low inventories and an oil price above $100 per barrel will lead to demand destruction. They will therefore aim to bring prices down. They have enough spare capacity (approximately 3.2mm b/d) to cover physical deficits in global markets (Chart 23A). However, the risk to this view is tilted to the upside. The key question is whether OPEC producers will in fact ramp up production. The OPEC meeting held on March 2, 2022 noted that current market volaility is a function of geopolitical developments and does not reflect changes in market fundamentals: This could imply a reluctance to increase production as quickly as we expect. Saudi Arabia’s interest in exploiting yuan-settled oil trades with China adds an element of uncertainty. With OPEC’s intention to increase production in question, and Russian oil sanctioned and unlikely to be rerouted easily and quickly, there remains little alternative supply: Countries such as Iraq and Venezuela are unlikely to make up for supply deficits (Chart 23B). The US-Iran talks also add downside uncertainty to our price outlook. Our commodity strategists have recently ended their forecast of a return of 1-1.3mm b/d of Iranian oil (Chart 23C). A no-deal scenario is likely to lead to an escalation in tensions and volatility, warranting higher oil prices in the short term. Nevertheless, there remains the possibility that the US administration will be keen on striking a deal with Iran to reduce the risk of a global oil supply shock. This would, in turn, reduce the risk of military conflict, at least in the short-term, and remove some risk premium from oil prices. It might also lead to further increases in production from the Gulf states to prevent Iran from stealing market share, putting further downward pressure on the oil price. Chart 24Is It Time To Favor EMU Equities?

Is It Time To Favor EMU Equities?

Is It Time To Favor EMU Equities?

When Will Euro Area Stocks Rebound? Chinese policy makers have sounded more aggressive of late in terms of supporting the Chinese economy and stock market, especially property and tech shares. This is a positive development for euro area equities given the region’s strong reliance on the Chinese economy (Chart 24, panel 1). Euro area equities have been in a structural downtrend relative to US equities, but have historically staged occasional counter-trend rallies (Chart 24, panel 2). It’s possible that stocks in this region may stage another short-term rebound at some point because they are technically oversold, and valuation is extremely cheap (Chart 24, panel 3). Investors with a longer-term investment horizon, however, should remain underweight euro area stocks until there are more signs that the region is out of its stagflation state. As we argue in the Global Equities section on page 18, the key factor to watch over the next 9-12 months is profitability. Global earnings growth will slow significantly this year in response to higher input costs and lower revenue growth. As a net importer of energy and industrial metals, euro area earnings growth will continue to slow more than in the US (Chart 24, panel 4). In addition, in times of high uncertainty, we prefer to shelter in less volatile markets. The euro area has a much higher beta than the US (Chart 24, panel 5). Bottom Line: While there could be an opportunity to overweight euro area stocks versus the US tactically, long-term investors should continue to favor the US. Global Economy Chart 25Global Growth Remains Robust...

Global Growth Remains Robust...

Global Growth Remains Robust...

Overview: Global growth has been strong. But this has triggered a surge in inflation, which is pushing central banks to tighten policy more quickly than was expected even three months ago. At the same time, higher prices – and falling real wages – have started to hurt consumer confidence. This raises the risk of stagflation, particularly if disruptions caused by the war in Ukraine push commodity prices up further. A recession is still unlikely over the next 12-18 months, but the risk of one has clearly risen. US economic growth has remained robust, led by consumption and capex. GDP growth in Q4 was 5.6% QoQ annualized. The ISMs remain strong, with manufacturing at 58.5 and services 58.9 (Chart 25, panel 2). However, there are some early signs of slowdown. The Atlanta Fed Nowcast points to only 0.9% annualized growth in Q1. The effect of higher inflation (with headline CPI at 7.9% YoY) might hurt consumer confidence, since average hourly earnings growth lags behind inflation at only 5.1%. Higher rates could also dampen the housing market. With the average mortgage rate rising to 4.5%, from 3.3% at the end of last year, there are signs of a slowdown in house sales (which fell 9.5% YoY in January). Euro Area: Growth remains decent, with Q4 GDP 4.6% QoQ annualized, and robust PMIs (manufacturing at 57.0 and services at 54.8). However, wage growth lags that in the US (negotiated wages rose only 1.5% YoY in Q4), and the impact of a sharp jump in energy prices (exacerbated by the war in Ukraine) could dent consumption. Recent data have deteriorated noticeably: Consumer confidence collapsed to -18.7 in March, and the March ZEW survey (Chart 26, panel 1) fell to -38.7 (from +48.6 in February). With weak underlying growth, and core CPI inflation a relatively modest 2.7%, the ECB will not need to rush to raise rates. Chart 26...But Higher Inflation Is Starting To Damage Confidence

...But Higher Inflation Is Starting To Damage Confidence

...But Higher Inflation Is Starting To Damage Confidence

Japan: Economic growth remains rather anemic. Manufacturing is supported by exports (which rose by 19.1% YoY in January), helping the manufacturing PMI to stay in positive territory at 53.2. But wage growth remains stagnant (0.9% YoY) and the rise in oil prices has pushed up headline inflation to 0.9%, leading to a weakening of consumer sentiment. The services PMI is a weak 48.7. There are hopes that this year’s shunto wage round will lead to strong wage rises (the government is lobbying businesses to raise wages by 3%) but this seems unlikely. With inflation ex food and energy languishing at -1.9% (even if that is distorted by cuts in mobile phone charges), there seems little need for the Bank of Japan to tighten policy. Emerging Markets: Chinese economic indicators remain depressed (Chart 26, panel 3), even though global demand for manufactured goods means exports are rising 16.4% YoY. The authorities have been easing policy, which has led to a mild uptick in credit growth. But there are questions on how effective stimulus will be, since the housing market has been damaged by the problems at Evergrande and other developers, and because China seems to be sticking to its zero-Covid policy. Some other EMs will be helped by the rise in commodity prices: South Africa, for example, saw 4.9% annualized GDP growth in Q4. But many developed countries were forced to raise rates sharply last year because of inflation and this may slow growth in 2022. Brazil’s policy rate, for example, has risen to 11.75% from 2% last April, and that has dampened activity: Brazilian industrial production is falling 7.2% YoY, and retail sales are -1.9% YoY. Interest Rates: Recorded inflation and inflation expectations (Chart 26, panel 4) have risen sharply everywhere. Slowing demand for manufactured goods and a supply-side response should allow monthly inflation to peak over the next few months – although the risks remain to the upside if commodity prices continue to rise. The surge in inflation has pushed up long-term rates, with the US 10-year Treasury yield rising by 82 BPs year-to-date and that in Germany by 73 BPs. However, the market is now pricing in very aggressive tightening by central banks through year-end: 214 BPs of further hikes by the Fed, and even 75 BPs by the ECB. The probability is that neither will do quite that much, and therefore the upside for long-term government bond yields is probably capped around its current level for the next 6-9 months. Global Equities Chart 27Watch Earnings Revisions Closely

Watch Earnings Revisions Closely

Watch Earnings Revisions Closely

Watch Earnings Closely: Global equities suffered a loss of 4% in Q1/2022 despite strong earnings growth. Except for the Utilities sector, all other sectors have positive 12-month trailing and forward earnings growth. Consequently, overall equity valuation, based on forward PE, is no longer stretched (Chart 27). Going forward, however, the macro backdrop of rising inflation and a slowing economy does not bode well for earnings growth, with the profit margin in developed markets already at a historical high. Rising input costs from both materials and wages will put downward pressure on profit margins while revenue growth slows. BCA Research’s global earnings model suggests that earnings growth will slow significantly this year. As such, we downgrade equities to neutral from overweight at the asset class level (see Overview section on page 2). Within equities, we maintain our already cautious country allocation, which served us well in both 2021 and Q1/22. The out-of-consensus overweight on the US and underweight on the euro area panned out well in Q1 2022, as the US outperformed the euro area by 5.9%. After the more defensive adjustment between the UK and Canada in the March Monthly Update, our country allocation portfolio has been well positioned, with overweights in the US and UK, underweights in the euro area, Canada and emerging markets excluding China, while neutral Australia, Japan, and China. In line with the shift of our structural view on industrial commodities, we upgrade the Materials sector to neutral from underweight at the expense of Real Estate and Communication Services. After these adjustments and the added defensive tilt that we took in the February Monthly Update, our global sector portfolio has a tilt towards defensive and structural growth by being overweight Tech, Industrials, Healthcare and Consumer Staples, underweight Consumer Discretionary, Utilities, and Communication Services, while neutral Materials, Financials, Energy and Real Estate. Chart 28Sector Adjustments

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Sector Allocation: Upgrade Materials To Neutral, Downgrade Real Estate to Neutral, Downgrade Communication Services to Underweight. Russia’s war on Ukraine is a watershed moment for industrial metals. It has altered the dynamics of the metals market which used to be dominated by Chinese demand. We had a structural underweight in the Materials sector because China was undergoing a deleveraging process. Now the Russian-Ukrainian war has demonstrated how dangerous it is for Europe to rely on Russia for energy supply and how important it is for Europe to have a strong military defense system. Rebuilding Europe’s defense will compete with energy diversification initiatives to boost demand for metals. Such a structural shift no longer warrants an underweight in Materials (Chart 28, panel 1). In addition, relative valuation in the Materials sector is as low as it was in the early 2000s, right before the multi-year upcycle in Materials’ relative performance (Chart 28, panel 2). Why not go overweight then? The concern is that the sector is technically overbought due to the sharp rises in metal price. Covid lockdowns in China have disrupted the supply chain in metals, and the Russian-Ukrainian war has further intensified the rise in metals prices due to extremely low inventories. We will watch closely for a better entry point to upgrade this sector to overweight. To finance this upgrade, we downgrade Real Estate to neutral from overweight, and Communication Services to underweight from neutral. Both downgrades are driven by a deteriorating relative earnings growth outlook as shown in Chart 28, panels 4 and 5. Rising mortgage rates do not bode well for the Real Estate sector. “Reopening from Covid lockdowns” reduces the “work from home” tailwind for the Communication Services sector, where relative valuation is also stretched. Government Bonds Chart 29WILL INFLATION COME DOWN IN 2022?

WILL INFLATION COME DOWN IN 2022?

WILL INFLATION COME DOWN IN 2022?

Maintain At-Benchmark Duration. The first quarter of 2022 had seen a steady rise in global bond yields even before the Russian-Ukrainian war, in response to a higher inflation outlook. The negative shock to bond yields from the war was quickly reversed and bond yields continued to march higher as the supply shortage in the commodity complex further pushed up commodity prices and inflation expectations. The US 10-year TIPS breakeven inflation rate has risen above the 2.3-2.5% range that is consistent with the Fed’s 2% PCE target. However, the 5-year/5-year forward breakeven inflation rate, the measure that the Fed pays more attention to, is only slightly above 2.3% (Chart 29, panel 2). The base case of BCA Research’s Fixed Income Strategists is that inflation will moderate in the coming months so that there should be limited upside for bond yields. We already upgraded duration to at-benchmark from below-benchmark, and government bonds to neutral from underweight within the bond asset class in the March Portfolio Update. These are still appropriate going forward with the US 10-year Treasury yield currently standing at 2.33%. Inflation-linked bonds are not cheap anymore. We maintain a neutral stance to hedge against the tail risk of a further rise in inflation. Corporate Bonds Chart 30Continue To Favor High-Yield Credit

Continue To Favor High-Yield Credit

Continue To Favor High-Yield Credit

Since the beginning of the year, investment-grade bonds have underperformed duration-matched Treasurys by 191 basis points, while high-yield bonds have underperformed duration-marched Treasurys by 173 basis points. Even with spreads widening, we continue to underweight investment-grade credits within the fixed-income category. Spreads currently do not offer enough value to warrant a neutral shift. Moreover, investment-grade corporate bonds have been performing poorly compared to high-yield corporate bonds (Chart 30, panel 1). But shouldn’t one expect lower-rated bonds to perform worse in bear markets, and better in bull markets? Our US Bond Service believes that one explanation for the poor performance of investment-grade compared to high-yield bonds is that the industry composition of the two categories is quite different. High-yield has a large concentration in the Energy sector while investment-grade bonds have a larger weighting in Financials. And with the recent surge in oil prices, it’s possible that the strong performance of Energy credits is the reason behind that return divergence. We continue to overweight high-yield bonds, as there is likely to be no material increase in corporate default risk. The market currently implies that defaults will rise to 3.7% during the next 12 months, from 1.2% over the past 12 months (Chart 30, panel 2). That seems too high. What about European credit? The ECB’S hawkish turn and then the Ukranian crisis made yields almost double this year. The spreads for both investment-grade and high-yield corporate bonds have been widening since the beginning of the year (Chart 30, panel 3). Their valuations seem to offer an attractive entry point but investors should be cautious as spreads could continue to widen in response to the negative news from the Ukranian crisis. Commodities Chart 31Risks To Oil Price Are To The Upside

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Quarterly Portfolio Outlook: Too Much Uncertainty To Ignore – Turn More Cautious

Energy (Overweight): Oil prices surged to $120 – the highest level since 2013 – in the aftermath of Russia’s invasion of Ukraine, pricing in sanctions against the nation’s oil producers and an estimated 3-5 mm b/d of supply disruptions (Chart 31, panel 1). While the actual hit to Russian production might end up being lower, Russia accounts for over 10% of global production, almost half of which is exported (Chart 31, panel 2). The price shock was slightly offset by a marginal demand weakness from China amid another outbreak of Covid-19. However, uncertainty regarding how quickly core OPEC producers will ramp up production to fill supply shortages – as well as the breakdown in the US-Iranian talks – continue to keep oil prices jittery. Our Commodity & Energy strategists see 1.3mm b/d of increased supply from OPEC coming onto the market beginning in May. This should bring the price of Brent crude down to average $93 per barrel this year and next. The risks to this view however remain tilted to the upside. For more details, see What Our Clients Are Asking on page 14. Industrial Metals (Neutral): Russia is a major player in the metals market, providing more than a third of the world’s palladium output; it is also the third biggest producer of nickel (Chart 31, panel 3). The prices of those metals, as well as the broad industrial metals complex, have shot up following the invasion: Industrial metals had the largest weekly price change since 1990 in the week following the invasion. The outlook for industrial metals prices is tilted to the upside. Inventories for some of the industrial metals required for the energy transition are low. Moreover, if China implements significant stimulus – and supply remains tight – prices are likely to stay elevated. Precious Metals (Neutral): Gold prices reacted in line with the moves in US real rates over the first quarter of this year, initially relatively flat, before rising in the past few weeks as real rates came down. The upward move in gold prices was further amplified by Russia’s invasion of Ukraine, which pushed the bullion’s price close to $2040, just shy of its all-time high in late 2020. This comes as no surprise: The metal is known (despite its volatility) for its safe-haven and inflation-hedging characteristics. We maintain our neutral exposure to gold. Real rates should start to rise as inflation pressures abate in the second half of the year. Gold is also somewhat expensively valued, with the price in inflation-adjusted terms close to its record high (Chart 31, panel 4). Currencies Chart 32Don't Turn Bearish On The Dollar Yet

Don't Turn Bearish On The Dollar Yet

Don't Turn Bearish On The Dollar Yet

US Dollar: The DXY index has risen by 2.3% this quarter. We are maintaining our neutral stance on the US dollar. While the dollar is expensive by more than 20% according to purchasing power parity (PPP), positive momentum continues to be too strong to take an outright bearish position (Chart 32, panels 1 and 2). We will look to downgrade the dollar to underweight when momentum starts to weaken and when there is clear evidence that the Fed will have to back off from its tightening path. Japanese Yen: With stock markets rebounding and expectations of interest-rate hikes rising in the US, the yen has fallen by more than 18% since the beginning of the year. Still, we reiterate the overweight that we placed at the beginning of March. The yen should act as a hedge if global stock markets sell off anew. Moreover, we believe there is now limited upside for US yields, given that there are now more than 250 basis points of Fed hikes priced over the next 12 months. This should put a cap on USDJPY, as this cross is closely tied to the relative expectations of tightening between the US and Japan (Chart 32, panel 3). Canadian Dollar: We are currently underweight the Canadian dollar. Our Commodity and Energy Strategists believe that oil should come down to around $90/barrel by the end of the year. Additionally, the BoC won’t be able to follow along with the Fed in its tightening cycle, given that household debt is much higher in Canada than in the US. Both developments should put downward pressure on the CAD over the next 12 months. Alternatives Chart 33Prepare To Turn To Defensive Alternatives

Prepare To Turn To Defensive Alternatives

Prepare To Turn To Defensive Alternatives

Return Enhancers: We previously suggested that private equity tends to outperform other alternative assets in the early years of expansions as it benefits from cheaper financing opportunities and attractive entry valuations. This view has been correct: Following the large drawdown in Q1 2020 due to Covid, PE returns have significantly outperformed those of hedge funds (Chart 33, panel 1). However, financing conditions are tightening and could weigh down on economic activity and PE returns going forward (Chart 33, panel 2). Preliminary results for Q3 2021 show PE funds returning only around 6% compared to an average quarterly return of 10% since the beginning of the pandemic. Given the time it takes to move allocations in the illiquid space, investors should prepare to pare back exposure from PE, and look for more defensive alternative assets, such as macro hedge funds. Inflation Hedges: We have been of the view that inflation will follow a “two steps up, one step down” trajectory: More likely than not, we are near the top of those two steps. Accordingly, we were positioned to favor real estate over commodities; real estate tends to outperform when inflation is more subdued (close to 2%-3%). Inflation, globally, however has turned out to be stickier than expected and recent economic and political developments have propelled another surge in commodity prices. Scarce inventories, lingering inflation, and a potential significant Chinese stimulus imply, at least in the short-term, that commodity prices have room to run (Chart 33, panel 3). Volatility Dampeners: Timberland and Farmland remain our long-time favorite assets within this bucket. We have previously shown that both assets outperform other traditional and alternative assets during recessions and equity bear markets. Farmland particularly continues to offer an attractive yield of approximately 2.8% (Chart 33, panel 4). Footnotes 1 Please see BCA Research Special Report, "The Yield Curve As An Indicator," for a detailed analysis of this. Recommended Asset Allocation Model Portfolio (USD Terms)

Highlights There is no evidence of a decline in US corporate credit or bank lending spreads over the past few decades, meaning that any excess savings effect structurally depressing interest rates is occurring in the Treasury market. We note the possible mechanisms of action for excess savings to lower government bond yields, by lowering the current policy rate, expectations for the policy rate in the future, or the term premium on long-maturity bonds. To investigate the impact that excess savings may be having on bond yields, we define historical periods of abnormal yields based on the gap between long-maturity Treasury yields and the potential rate of economic growth. This reflects our view that potential growth is the equilibrium interest rate under normal economic conditions. Since 1960, there have been three major episodes when the difference between bond yields and economic growth was large and persistent, but the first two seem to be easily explained by the stance of US monetary policy rather than by a savings/investment imbalance. The excess savings story better fits the facts after 2000. We do find evidence that a global savings glut lowered bond yields during the early-2000s, and it may have even modestly contributed to the excessive household credit demand that ultimately caused the global financial crisis. But as a deviation from equilibrium, the effect of the global savings glut was relatively insignificant compared to what has prevailed over the past decade. Excess savings did certainly play a role in lowering long-term investor expectations for the Federal funds rate during the last economic cycle, but it did so for cyclical reasons that spanned several years rather than as a result of demographic effects or other structural factors unrelated to the business cycle. That is an important distinction, as long-term investor expectations for the Fed funds rate remained low in the second half of the last economic expansion despite a reduction in savings and significantly stronger growth. The historical impact of FOMC meetings on the structural decline in long-maturity US Treasury yields strongly implies that fixed-income investors have been guided by the Fed to expect a lower average Fed funds rate. It is our view that the Fed has a backward-looking neutral rate outlook, informed by an incomplete understanding of the economic circumstances of the latter half of the last expansion. A low neutral rate narrative has become entrenched in the minds of investors and the Fed itself, and we regard this as the primary factor anchoring yields at the long-end of the maturity spectrum. This phenomenon is only likely to dissipate once short-term interest rates rise and a recession does not materialize. While the nearer-term outlook more likely favors a neutral or at best modestly short duration stance within a fixed-income portfolio, investors should remain structurally short duration in response to a potentially rapid shift in long-term interest rate expectations from the Fed and fixed-income investors over the coming few years. Feature Chart II-110-Year US Treasury Yields Are The Lowest Relative To Headline Inflation In Over 60 Years

10-Year US Treasury Yields Are The Lowest Relative To Headline Inflation In Over 60 Years

10-Year US Treasury Yields Are The Lowest Relative To Headline Inflation In Over 60 Years

For many investors, one of the most striking features of the pandemic, especially over the past year, is how low US long-maturity government bond yields have remained in the face of the highest headline consumer price inflation in four decades (Chart II-1). To many investors, this has provided even further evidence of a structural “excess savings” effect that has kept interest rates well below the prevailing rate of economic activity. The theory of secular stagnation, revived by Larry Summers in late 2013, is a related concept, but many investors believe that interest rates will remain low even in a world in which the US economy is growing at or even above its trend. The fundamental basis for this view is the idea that over the longer term, the real rate of interest is determined by the balance (or imbalance) between desired savings and investment, and that advanced economies have and will continue to experience excess savings – defined as a chronically high level of desired savings relative to the investment opportunities available. According to this view, in order for the actual level of savings to equal investment, interest rates must fall. Chart II-2Do Excess Savings Explain This Gap? (Spoiler: No)

Do Excess Savings Explain This Gap? (Spoiler: No)

Do Excess Savings Explain This Gap? (Spoiler: No)

This report challenges the view that excess savings are mostly responsible for the current level of long-term bond yields in the US. We agree that excess savings have played a role in explaining changes in long-term bond yields at different points over the past 20 years; we also agree that it is normal for interest rates in advanced economies to trend down over time in response to a demographically-driven decline in potential growth. But our goal is not to explain the downtrend in interest rates over time. Instead, we aim to explain the gap between the level of long-term bond yields today and the prevailing rate of economic activity, or consensus forecasts of the trend rate of growth (Chart II-2). We do not believe that this gap is economically justified, nor do we believe that it is driven by excess savings. We conclude that the Fed’s backward-looking neutral rate outlook is the primary factor anchoring US Treasury yields at the long-end of the maturity spectrum. This is only likely to change once short-term interest rates rise and a recession does not materialize; it suggests that investors should remain structurally short duration in response to a potentially rapid shift in long-term interest rate expectations from the Fed and fixed-income investors over the coming few years. Excess Savings And Interest Rates: Defining A “Mechanism Of Action” Households, businesses, and governments can directly purchase debt securities in capital markets, but they do not typically provide loans directly to borrowers. Direct lending usually occurs through the banking system, which means that excess savings would only lower interest rates in the economy through one of the following ways: By lowering the Fed funds rate By lowering long-maturity government bond yields relative to the Fed funds rate, by reducing either the term premium or investors’ expectations for the average Fed funds rate in the future By lowering corporate bond yields relative to duration-matched government bond yields By lowering lending rates on bank loans relative to banks’ cost of borrowing Charts II-3-II-5 highlight that there is no evidence of a structural decline in corporate credit spreads or bank lending rates relative to the Fed funds rate, so we can rule out this effect as a mechanism of action for excess savings to have structurally lowered interest rates. Chart II-6 highlights that interest paid on bank deposits lags the Fed funds rate, so we can also rule out the idea that excess deposits force the Fed to keep the effective Fed funds rate low. Chart II-3No Evidence Of A Structural Decline In Corporate Credit Spreads…

No Evidence Of A Structural Decline In Corporate Credit Spreads...

No Evidence Of A Structural Decline In Corporate Credit Spreads...

Chart II-4…Or Auto Loan Rate Spreads…

...Or Auto Loan Rates Spreads...

...Or Auto Loan Rates Spreads...

Chart II-5…Or Personal Loan Rate Spreads…

...Or Personal Loan Rate Spreads...

...Or Personal Loan Rate Spreads...

Chart II-6...Or Bank Deposit Rate Spreads

...Or Bank Deposit Rate Spreads

...Or Bank Deposit Rate Spreads

This means that if excess savings are depressing interest rates in the US, that the effect is truly occurring in the Treasury market. As noted, this could occur by lowering the current policy rate, expectations for the policy rate in the future, or the term premium on long-maturity bonds. Related Report The Bank Credit AnalystR-star, And The Structural Risk To Stocks All of these effects are certainly possible. Keynes’ paradox of thrift highlights that excess savings can manifest itself as a chronic shortfall in aggregate demand, which would persistently lower the Fed funds rate as the Fed responds to a long period of high unemployment. This could also lower the term premium on long-maturity bond yields in a scenario in which the Fed repeatedly engages in asset purchases to help stabilize aggregate demand. As well, domestic excess savings could lower the term premium on long-maturity bond yields, as aging savers directly purchase government securities as part of their retirement portfolios. Finally, foreign capital inflows could also cause this effect, especially if they originate from countries with chronic current account surpluses that use an increase in US dollar reserves to purchase long-maturity US government securities. Table II-1 summarizes these possible mechanisms of action for excess savings to lower US government bond yields. With these mechanisms in mind, we review the past 60 years to identify periods of “abnormal” bond yields, with the goal of understanding whether excess savings appear to explain major gaps. Table II-1Possible Mechanisms Of Action For Excess Savings To Lower Long-Term Government Bond Yields

April 2022

April 2022

Identifying Periods Of “Abnormal” Long-Maturity Bond Yields Chart II-7There Have Been Three Distinct Periods Of Abnormal Long-Maturity Bond Yields

There Have Been Three Distinct Periods Of Abnormal Long-Maturity Bond Yields

There Have Been Three Distinct Periods Of Abnormal Long-Maturity Bond Yields

Chart II-7 shows the difference between nominal 10-year US Treasury yields and nominal potential GDP growth. Panel 2 shows an alternative version of this series using the ten-year median annualized quarterly growth rate of nominal GDP in lieu of estimates of potential growth, which highlights a generally similar relationship. This approach to defining “abnormal” long-maturity bond yields reflects our view that the potential rate of economic growth is the equilibrium interest rate under normal economic conditions. To see why, given that GDP also effectively represents gross domestic income, an interest rate that is persistently below the potential growth rate of the economy would create a strong incentive to borrow on the part of households and especially firms. Chart II-7 makes it clear that the relationship has been mean-reverting over time, but that there have been three major episodes when the difference between bond yields and economic growth was large and persistent. The first episode occurred from 1960 to the late 1970s, and saw government bond yields average well below the prevailing rate of economic growth. We do not see this period as having been caused by an excess of desired savings relative to investment. As we discussed in our November Special Report,1 this gap represented a period of persistently easy monetary policy which contributed to excessive aggregate demand and a structural rise in inflation. The second major episode is also easily explained, as it occurred in response to the first. Following a decade of high inflation, Fed chair Paul Volcker raised interest rates aggressively beginning in 1979 to combat inflationary expectations, which led to a two-decade period of generally tight monetary policy. Like the first period, this was not caused by an imbalance between desired savings and investment. The third episode has prevailed since the late-1990s, and has seen a negative yield/growth gap on average – albeit one that has been smaller than what occurred in the 1960s and 1970s. From 2000 to 2007, the gap was generally negative, although it turned positive by the end of the economic cycle. It was modestly negative on average from 2008 to 2010, and only became persistently negative starting in 2011. The gap fell to a new low during the COVID-19 pandemic, and remains wider today than at any point during the last economic recovery. It is these post-2000 periods of a persistently negative yield/growth gap that should be closely investigated for evidence of an excess savings effect. The Global Savings Glut As noted, prior to 2000, the yield/growth gap in the US seems clearly explained by the Fed’s monetary policy stance, not by an excess savings effect. So the question is whether there is any evidence of excess savings having caused this negative gap since 2000. In our view, the answer is yes, but the effect was relatively small compared to what prevails today. We do find evidence of a global savings glut during the early-2000s. Chart II-8 highlights that the private and external sector savings/investment balances in China and emerging markets more generally were persistently positive during the 2000s. Chart II-9 highlights that multiple estimates of the term premium declined around that time – especially during Greenspan’s “conundrum” period of between 2004 and 2005. Chart II-8There Was A Global Savings Glut Prior To The Global Financial Crisis

There Was A Global Savings Glut Prior To The Global Financial Crisis

There Was A Global Savings Glut Prior To The Global Financial Crisis

Chart II-9The Global Savings Glut Does Seem To Have Lowered The Term Premium On US 10-Year Treasurys

The Global Savings Glut Does Seem To Have Lowered The Term Premium On US 10-Year Treasurys

The Global Savings Glut Does Seem To Have Lowered The Term Premium On US 10-Year Treasurys

Chart II-10 breaks down the components of the 10-year yield into the 5-year yield and the 5-year/5-year forward yield, and highlights that the negative correlation between the two components lasted for only one year. Overall, the 10-year Treasury yield was lower than potential growth for roughly two years as a result of the global savings glut effect. Chart II-10Still, The Global Savings Glut Effect Did Not Last Long And Was Not Especially Large In Magnitude

Still, The Global Savings Glut Effect Did Not Last Long And Was Not Especially Large In Magnitude

Still, The Global Savings Glut Effect Did Not Last Long And Was Not Especially Large In Magnitude

This was a significant event, and it may even have modestly contributed to the excessive household credit demand that ultimately caused the global financial crisis. But as a deviation from equilibrium, it was relatively insignificant compared to what has prevailed over the past decade. Excess Savings And US Household Deleveraging Chart II-11Most Of The Post-2007 Decline In 10-Year Yields Is Attributable To Lower Long-Term Fed Funds Rate Expectations

Most Of The Post-2007 Decline In 10-Year Yields Is Attributable To Lower Long-Term Fed Funds Rate Expectations

Most Of The Post-2007 Decline In 10-Year Yields Is Attributable To Lower Long-Term Fed Funds Rate Expectations

Chart II-11 highlights that, relative to June 2007 levels, the vast majority of the cumulative decline in the 10-year Treasury yield has occurred because of a decline in implied long-term expectations for the Fed funds rate, rather than a major decline in the term premium. The chart also shows that almost all the decline in implied long-term interest rate expectations since 2007 occurred during the 2008/2009 recession. This normally occurs during a recession as investors price in a low average Fed funds rate at the short end of the curve; the anomaly is that these expectations remained permanently low even as the economy recovered and as the Fed raised interest rates from 2015 to 2018. To us, Chart II-11 also underscores that the Fed’s asset purchases are not the main culprit behind low long-maturity bond yields today, given that the decline in long-term expectations for the Fed funds rate persisted even as the Fed stopped purchasing assets in 2014. It is not difficult to see why investors lowered their long-term Fed funds rate expectations in the immediate aftermath of the global financial crisis, even as economic recovery took hold. Chart II-12 highlights that the “balance sheet” nature of the 2008/2009 recession unleashed the longest period of US household deleveraging in the post-WWII period, and Chart II-13 highlights that this occurred despite extremely low interest rates – and in contrast to other countries like Canada that did not experience the same loss in household net worth. Chart II-12Household Deleveraging Did Lower The Neutral Rate For Several Years Following The Global Financial Crisis

Household Deleveraging Did Lower The Neutral Rate For Several Years Following The Global Financial Crisis

Household Deleveraging Did Lower The Neutral Rate For Several Years Following The Global Financial Crisis

Chart II-13The US Balance Sheet Recession Structurally Impaired Credit Demand For Several Years After 2008

The US Balance Sheet Recession Structurally Impaired Credit Demand For Several Years After 2008

The US Balance Sheet Recession Structurally Impaired Credit Demand For Several Years After 2008

Given that interest rates represent the price of borrowing, it is entirely unsurprising that a US balance sheet recession led to a persistent period in which credit growth was essentially unresponsive to interest rates, as households struggled to rebuild wealth lost during the recession and were unable to, or uninterested in, releveraging. This is another way of saying that the neutral rate of interest fell during that period, which we agree did occur. It is also accurate to characterize the US as having experienced a sharp increase in desired savings over that period, as highlighted by the explosion in the US private sector financial balance in the initial years of the last economic recovery (Chart II-14). Chart II-14Excess Savings Surged After 2008, But Eventually Normalized. Long-Term Rate Expectations Ignored The Normalization.

Excess Savings Surged After 2008, But Eventually Normalized. Long-Term Rate Expectations Ignored The Normalization.

Excess Savings Surged After 2008, But Eventually Normalized. Long-Term Rate Expectations Ignored The Normalization.

So excess savings did certainly play a role in lowering long-term investor expectations for the Federal funds rate during the last economic cycle, but it did so because of cyclical reasons that spanned several years rather than because of demographic effects or other structural factors unrelated to the business cycle. That is an important distinction, because while Chart II-14 shows that this excess savings effect eventually waned in importance, long-term investor expectations for the Fed funds rate remained low in the second half of the last economic expansion. Chart II-15Growth Was Historically Weak Last Cycle, But Only Because Of The First Few Years Of The Expansion

April 2022

April 2022

Chart II-15 highlights that the cumulative annualized growth in real per capita GDP during the last economic cycle was significantly below that of the average of previous expansions, but this was only the case because of the very slow growth period between 2008 and 2014. Per capita growth during the latter half of the expansion was comparable to that of previous expansions, and this occurred while the Fed was raising interest rates. And yet, investors only modestly raised their long-term interest rate expectations during that period. In our view, it is this fact that holds the key to understanding why investors’ long-term rate expectations are still low today. An Alternative Explanation For Today’s Extremely Low Long-Maturity Bond Yields Chart II-16Fixed-Income Investors Have Been Guided By The Fed To Expect A Low Average Fed Funds Rate

Fixed-Income Investors Have Been Guided By The Fed To Expect A Low Average Fed Funds Rate

Fixed-Income Investors Have Been Guided By The Fed To Expect A Low Average Fed Funds Rate

Chart II-16 highlights that, since 1990, all of the structural decline in US 10-year Treasury yields has occurred within a three-day window on either side of FOMC meetings. This strongly suggests that fixed-income investors have been guided by the Fed to expect a low average Fed funds rate, which is consistent with how similar 5-year/5-year forward US Treasury yields are in relation to published FOMC and market participant estimates of the average longer-run Fed funds rate (as shown in Chart II-2). This raises the important question of why the Fed did not revise up its expectation for the neutral rate during or following the second half of the last economic expansion, when growth was much stronger than during the first half. In our view, one of the clearest articulations of the Federal Reserve’s understanding of the neutral rate of interest was presented in a 2015 speech by Lael Brainard at the Stanford Institute for Economic Policy Research. Brainard noted the following: “The neutral rate of interest is not directly observable, but we can back out an estimate of the neutral rate by relying on the observation that output should grow faster relative to potential growth the lower the federal funds rate is relative to the nominal neutral rate. In today’s circumstances, the fact that the US economy is growing at a pace only modestly above potential while core inflation remains restrained suggests that the nominal neutral rate may not be far above the nominal federal funds rate, even now. In fact, various econometric estimates of the level of the neutral rate, or similar concepts, are consistent with the low levels suggested by this simple heuristic approach.”2 Chart II-17The Fed, Wrongly, Sees The 2019 Experience As Having Confirmed A Low Neutral Rate...

The Fed, Wrongly, Sees The 2019 Experience As Having Confirmed A Low Neutral Rate...

The Fed, Wrongly, Sees The 2019 Experience As Having Confirmed A Low Neutral Rate...

Given how the Fed determines the neutral rate is, two factors explain why the Fed’s estimates of the neutral rate have not increased (and, in fact, fell modestly in March). First, core inflation remained below 2% from 2015-2019, despite the fact that the economy was clearly growing at an above-trend pace during this period in the face of Fed rate hikes. We have noted in previous reports the role that the 2014 collapse in oil prices had on household inflation expectations. The latter were already vulnerable to a disinflationary shock, given how negative the output gap had been in the first half of the expansion.3 We do not think that the decline in inflation expectations that occurred following the 2014 collapse in oil prices reflects a low neutral rate, but rather we believe that the Fed saw this as a conundrum that supported the expectation of a low average Fed funds rate. The second event explaining the Fed’s persistently low long-term rate expectations is the fact that the Fed was forced to cut interest rates in 2019, which we believe it saw as confirmation that the stance of monetary policy had become either meaningfully less easy or openly tight. From the Fed’s point of view, this perspective was also supported by recessionary indicators, such as the inversion of the 2-10 yield curve (Chart II-17), and popular (but now discontinued) econometric estimates of the real neutral rate of interest, such as those calculated by the Laubach-Williams model (panel 3). Chart II-18...Without Appreciating The Damaging Impact The China-US Trade War Had On Global Activity

...Without Appreciating The Damaging Impact The China-US Trade War Had On Global Activity

...Without Appreciating The Damaging Impact The China-US Trade War Had On Global Activity

However, this view entirely ignores the fact that the US and global economies were negatively impacted in 2018 and 2019 by a politically-motivated nonmonetary shock to aggregate demand: the China-US trade war, which also impacted or targeted several major advanced economies. Chart II-18 highlights that global trade uncertainty exploded during this period, which severely damaged business confidence around the world and caused a slowdown in global industrial production. Tighter Chinese policy also likely contributed to the slowdown in global activity, but the bottom line is that factors other than US monetary policy contributed to economic weakness during this period, and that it is incorrect to infer from the 2018/2019 experience that interest rates rose to or exceeded the neutral rate of interest. In short, it is our view that the Fed has simply become backward-looking in how it perceives the neutral rate of interest; it has not yet observed a period when the Fed funds rate has risen to its estimate of neutral but is unambiguously still easy. Fixed-income investors, having demonstrably anchored their own assessments to those of the Fed over the past 30 years, have had no basis to come to a meaningfully different conclusion. We believe that the Fed’s backward-looking low neutral rate outlook has now become entrenched in the minds of investors and the Fed itself, and is the primary factor anchoring yields at the long-end of the maturity spectrum. This will probably only change once short-term interest rates rise and a recession does not materialize. As a final point, we clearly acknowledge that private savings increased massively during the pandemic. Investors who are inclined to see excess savings as the primary driver of low bond yields will point to this fact. But this was a forced increase in savings, rather than a desired one. The rise in household sector savings occurred mostly because of a substantial reduction in services spending, as pandemic restrictions and forced changes in behavior prevented the consumption of many services. The household savings rate has already returned to its pre-pandemic level in the US, and 5-year/5-year forward Treasury yields have risen to a higher point than they were prior to the onset of the COVID-19 pandemic. US households are likely to deploy a portion of their enormous stock of excess savings, as the pandemic continues to recede in importance, which is one of the main reasons to expect that the US economy will not succumb to a recession over the coming 12-18 months – and why investors and the Fed may soon be presented with evidence that warrants an increase in their long-term interest rate expectations. Investment Conclusions There are two important investment implications of the view that the Fed’s backward-looking neutral rate projection is the primary factor anchoring yields at the long end of the maturity spectrum. As we noted in Section 1 of our report, the first implication is that investors will likely be faced with a recession scare as the 2-10 yield curve durably inverts and as rate sensitive sectors of the economy, such as housing, inevitably slow in response to the extremely sharp rise in mortgage rates that has occurred over the past three months. We believe that it is ultimately the level of interest rates that matters for economic activity, rather than the change in interest rates. Large changes over short periods of time, however, create a degree of uncertainty about the trajectory of rates that temporarily impacts economic activity. This underscores that investors should not maintain an aggressively overweight stance toward global equities in a multi-asset portfolio, as it is likely that concerns about corporate profits will increase significantly at some point this year. The second investment implication is that US long-maturity bond yields could increase to much higher levels over the coming 12-24 months than many investors expect, in a scenario in which pandemic-driven price pressure dissipates, real wages recover, and no major politically-driven nonmonetary policy shocks emerge. We acknowledge that long-term interest rate expectations are unlikely to change until hard evidence of the economy’s capacity to tolerate interest rates above the Fed’s implied current estimate of the neutral rate emerges. This is a case, however, when we believe that investors should heed the now-famous words of Rüdiger Dornbusch: “In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.” As such, while the nearer-term outlook more likely favors a neutral or at best modestly short duration stance within a fixed-income portfolio, investors should remain structurally short duration in response to a potentially rapid shift in long-term interest rate expectations from the Fed and fixed-income investors over the coming few years. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Please see The Bank Credit Analyst "Gauging The Risk Of Stagflation," dated October 29, 2021, available at bca.bcaresearch.com 2 Lael Brainard, Normalizing Monetary Policy When The Neutral Rate Is Low, December 2015 3 Please see The Bank Credit Analyst "The Modern-Day Phillips Curve, Future Inflation, And What To Do About It," dated December 18, 2020, available at bca.bcaresearch.com

The Yield Curve & Equity Returns

…

Executive Summary Refreshing Our Tactical Trade List

A Post-Invasion Reassessment Of Our Tactical Trade Recommendations

A Post-Invasion Reassessment Of Our Tactical Trade Recommendations

Our current list of tactical trade recommendations centers around two broad themes that predate the Ukraine conflict – rising global inflation expectations and relatively stronger upward pressure on US interest rates. Both themes have been strengthened by the spillovers from the war in Eastern Europe, most notably the link between soaring commodity prices and rising inflation. We still see value in holding our recommended cross-country spread trades that will benefit from continued US bond underperformance (short US Treasuries versus government bonds in Germany, Canada and New Zealand, all at the 10-year maturity). We also maintain our bias to lean against the yield curve flattening trend in the US, but we now prefer to do it solely via our existing SOFR futures calendar spread position. Finding attractively valued inflation breakeven spread trades is more difficult after the latest oil-fueled run-up in developed market inflation expectations. Canadian breakevens, however, stand out as having the greatest upside potential according to our Comprehensive Breakeven Indicators. Bottom Line: Remain in US-Germany, US-Canada an US-New Zealand 10-year government bond yield spread widening trades. Maintain our recommended position in the US SOFR futures curve (long Dec/22 futures, short Dec/24 futures). Add a new inflation-linked bond trade, going long 10-year Canadian breakevens. Feature One month has passed since Russia invaded Ukraine, and investors are still struggling to sort out the financial market implications. Equity markets in the US and Europe have recovered the losses incurred immediately after the conflict began. Equity market volatility has also fallen back to pre-invasion levels according to the VIX index (and its European counterpart, the VStoxx index). That decline in equity volatility has also coincided with a narrowing of corporate credit spreads in both the US and Europe, with the former now fully back to pre-invasion levels. Yet while credit spread volatility has calmed down, government bond yield volatility remains elevated thanks to rising commodity prices putting upward pressure on expectations for inflation and monetary policy (Chart 1). Chart 1Global Bond Yields Are Above Pre-Invasion Levels

Global Bond Yields Are Above Pre-Invasion Levels

Global Bond Yields Are Above Pre-Invasion Levels

Table 1Refreshing Our Tactical Trade List

A Post-Invasion Reassessment Of Our Tactical Trade Recommendations

A Post-Invasion Reassessment Of Our Tactical Trade Recommendations

We have already made some “wartime” adjustments to our global bond market cyclical recommendations, with those changes reflected in our model bond portfolio. This week, we review our shorter-term tactical trade recommendations. Our current list of tactical trades revolves around two broad themes that predate the Ukraine conflict – rising global inflation expectations and relatively stronger cyclical upward pressure on US interest rates. Both themes have been strengthened by the spillovers from the war in Eastern Europe, most notably the link between soaring commodity prices and rising inflation. We continue to see the value in holding on to most of our existing tactical trades, with only a couple of adjustments to be made to our US yield curve and global inflation-linked bond positions (Table 1). US Yield Curve Tactical Trades: Shift Focus To SOFR Steepeners We have recommended trades that lean against the aggressive flattening of the US Treasury curve discounted in forward rates since late 2021. Our view has been that markets were discounting too rapid a pace of Fed rate increases in 2022. With the Fed likely delivering fewer hikes than expected, Treasury curve steepening trades would benefit as the spot Treasury curve would flatten by less than implied by the forwards. Related Report Global Fixed Income StrategyFive Reasons To Tactically Increase US Duration Exposure Now Needless to say, that view has not panned out as we anticipated. The spread between 10-year and 2-year US Treasury yields now sits at a mere +13bps, down from +104bps when we initiated our 2-year/10-year steepener trade last November. The forwards now discount an inversion of that curve starting in June of this year, which would be an extraordinary outcome by historical standards. Typically, the US Treasury curve inverts only after the Fed has delivered an extended monetary tightening cycle that delivers multiple rate hikes over at least a 1-2 year period (Chart 2). Today, the curve has nearly inverted with the Fed having only delivered only a single 25bp rate increase earlier this month. Chart 2The UST Curve Is Unusually Flat Right Now

The UST Curve Is Unusually Flat Right Now

The UST Curve Is Unusually Flat Right Now

Of course, the Fed’s reaction function in the current cycle is different compared to the past. The Fed now follows an average inflation targeting framework that tolerates temporary inflation overshoots after periods when US inflation ran below the Fed’s 2% target. Now, however, the Fed has no choice but to respond to surging US inflation, which has been accelerating since September and is now at levels last seen in 1982. Chart 3Our SOFR Trade Is Similar To Our UST Curve Trade

Our SOFR Trade Is Similar To Our UST Curve Trade

Our SOFR Trade Is Similar To Our UST Curve Trade

We still see the market pricing in too much Fed tightening this year and too few rate hikes in 2023/24. The US overnight index swap (OIS) curve now discounts 218bps of rate hikes in 2022, but 44bps of rate cuts between June 2023 and December 2024. We think a more likely scenario is the Fed doing less than discounted this year, as US inflation should show some deceleration in the latter half of 2022, but then continuing to raise rates in 2023 into 2024. We have expressed this view more specifically through an additional tactical trade that was initiated last month, going long the December 2022 3-month SOFR futures contract versus shorting the December 2024 3-month SOFR futures contract. This new trade is essentially a calendar spread trade between two futures contracts, but with a return profile that has looked quite similar to our 2-year/10-year US Treasury curve flattening trade (Chart 3). Having two tactical trades that are highly correlated, and which both are driven by the same theme of the Fed doing less this year and more over the next two years, is inefficient. We see the SOFR calendar spread trade as a more precise expression of our Fed policy view compared to the 2-year/10-year Treasury curve steepener. In addition, the SOFR trade now offers slightly better value after it has lagged the performance of the Treasury curve trade over the past couple of weeks. Thus, we are keeping this trade in our Tactical Overlay portfolio (see the table on page 15), while closing out our 2-year/10-year steepener at a loss of -92bps.1 Cross-Country Spread Trades: Keeping Betting On Relatively Higher US Yields In our Tactical Overlay portfolio, we currently have three recommended cross-country government bond spread trades that all have one thing in common – a sale of 10-year US Treasuries. The long side of the three trades are different (Germany, New Zealand and Canada), but the logic underlying all three trades is the same. The Fed will deliver more rate hikes than the central banks in the other countries. 10-year US Treasury-German Bund spread Chart 4UST-Bund Spread Is Too Low

UST-Bund Spread Is Too Low

UST-Bund Spread Is Too Low