Fixed Income

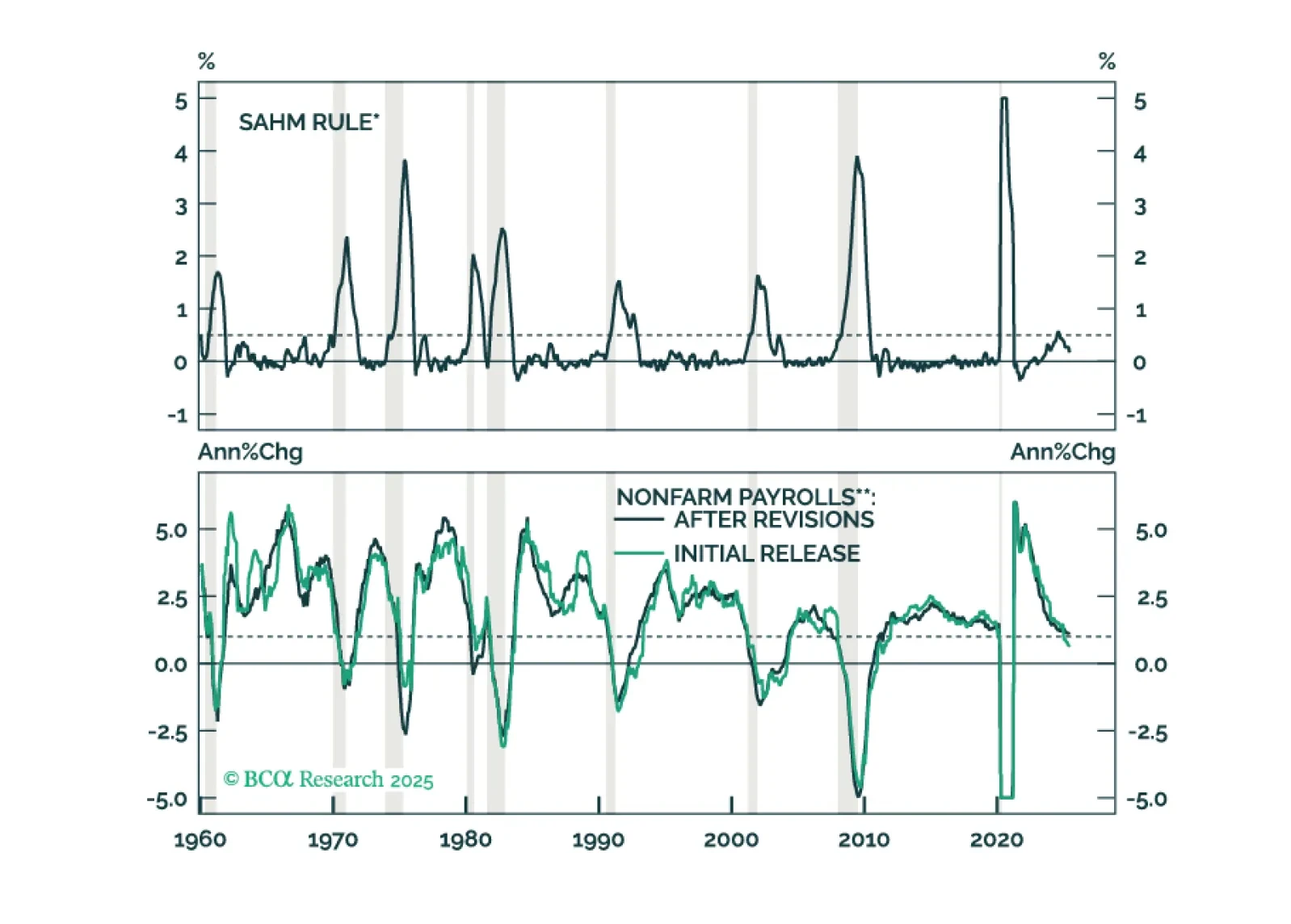

June’s employment report showed a tick down in the unemployment rate, an improvement that rules out a Fed rate cut later this month.

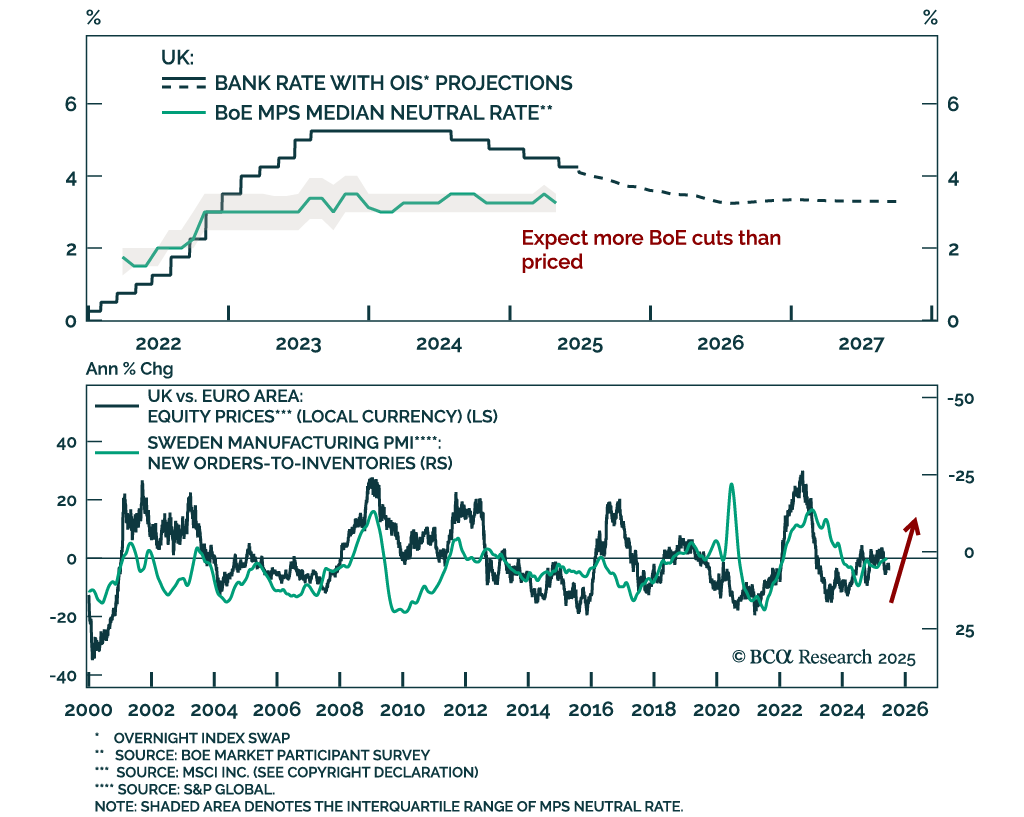

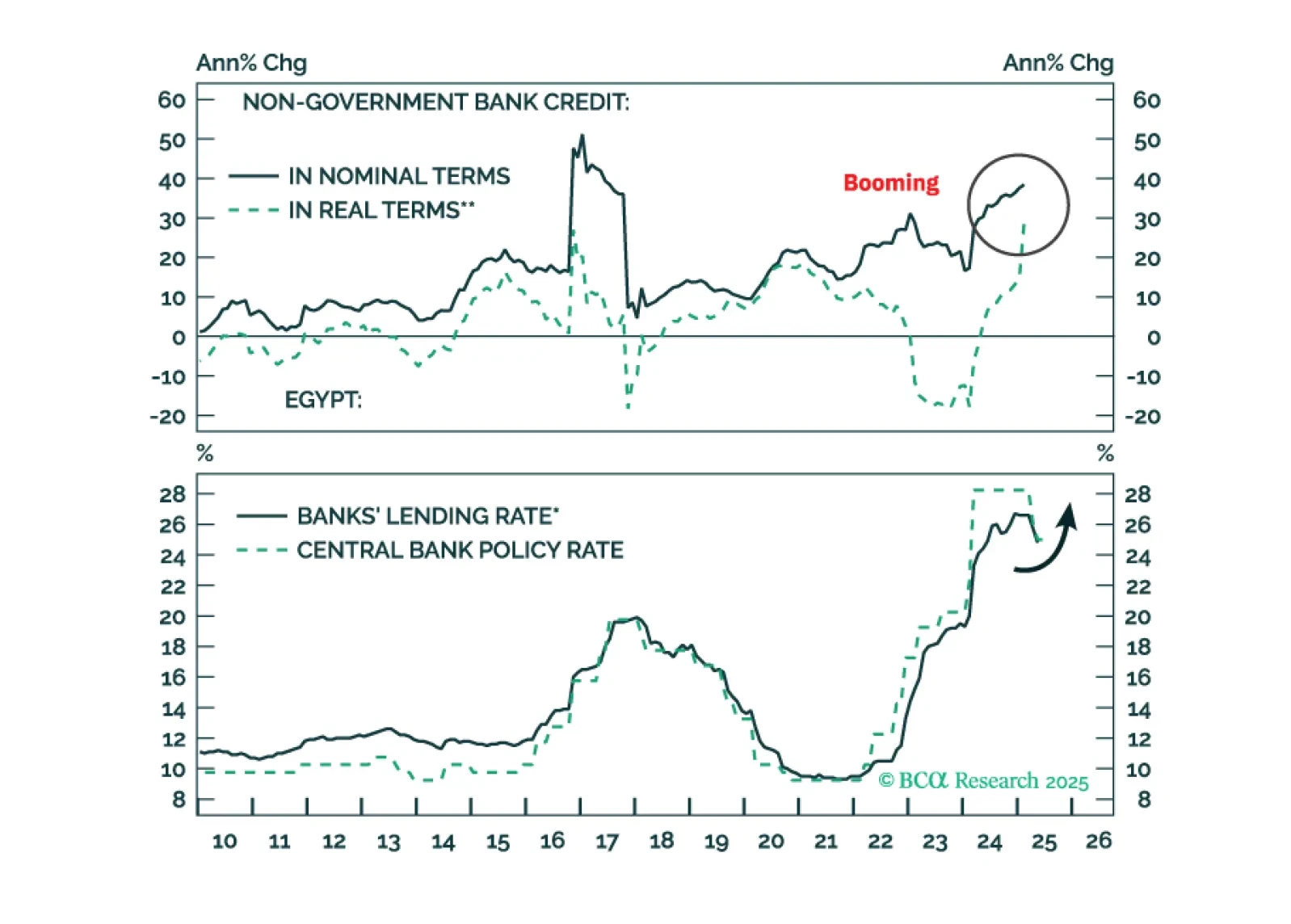

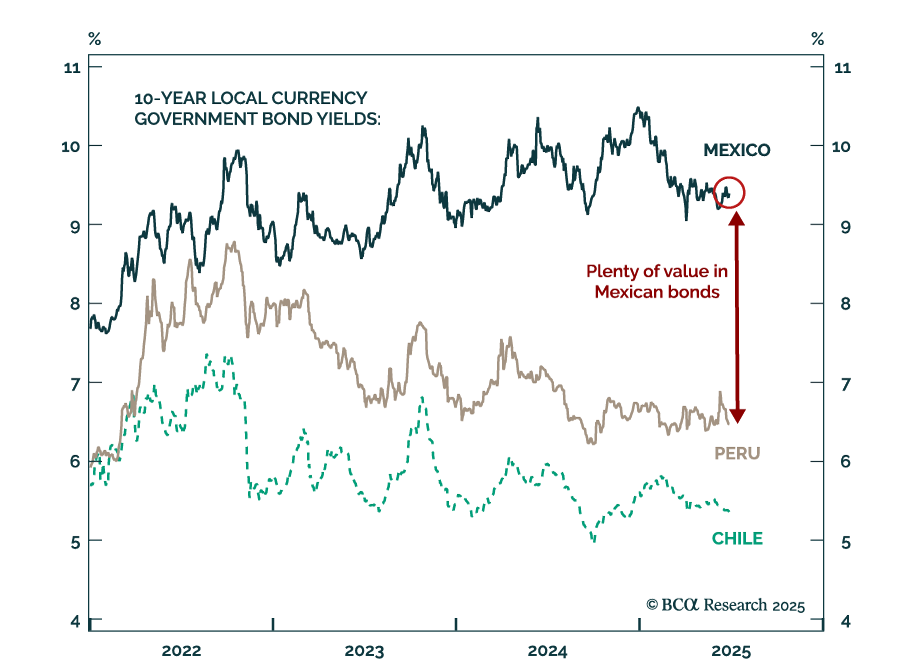

Downward pressure on the pound will rise in the coming months. Inflation will go up, so will bond yields. It’s time to book profits on Egyptian domestic bonds.

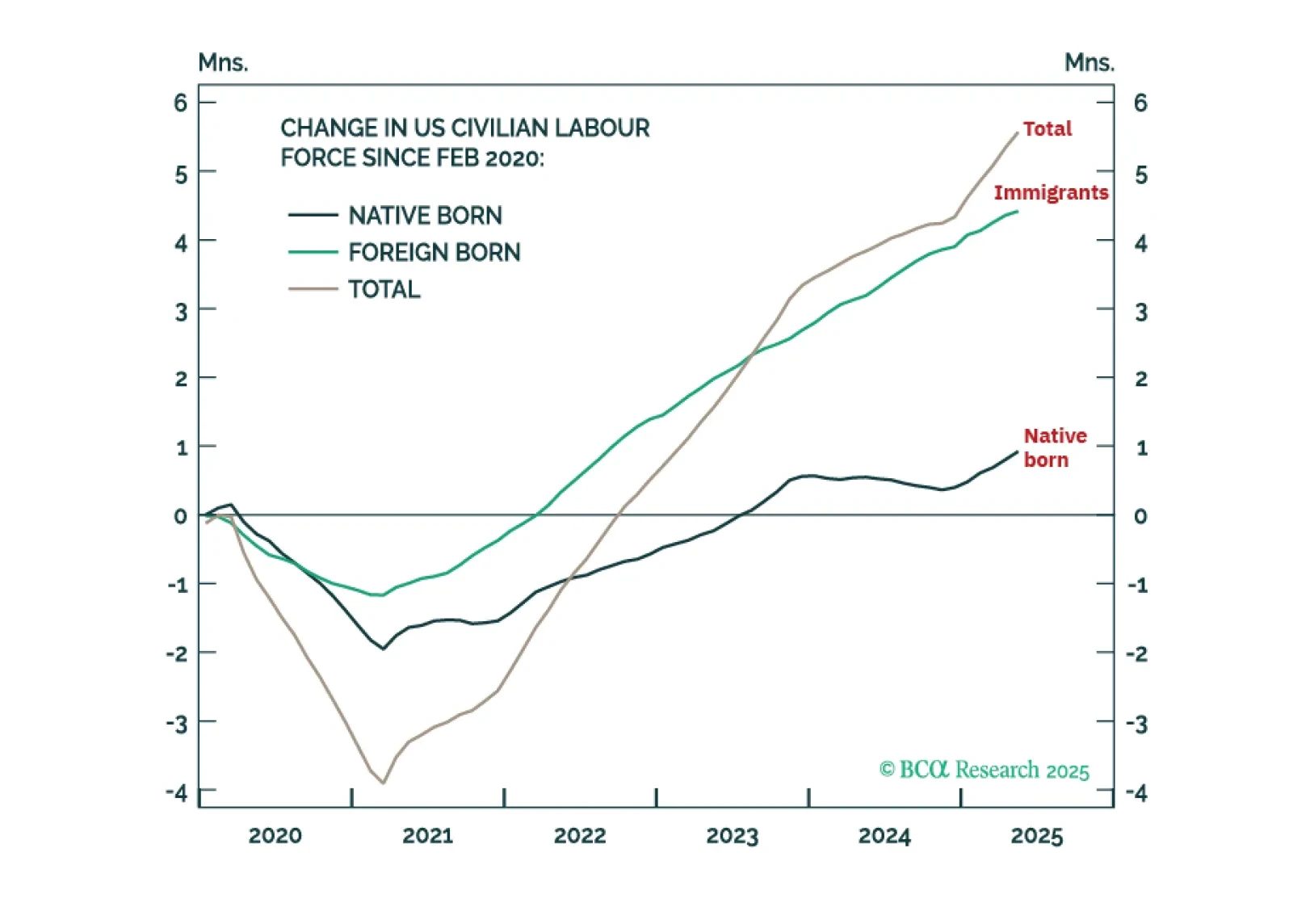

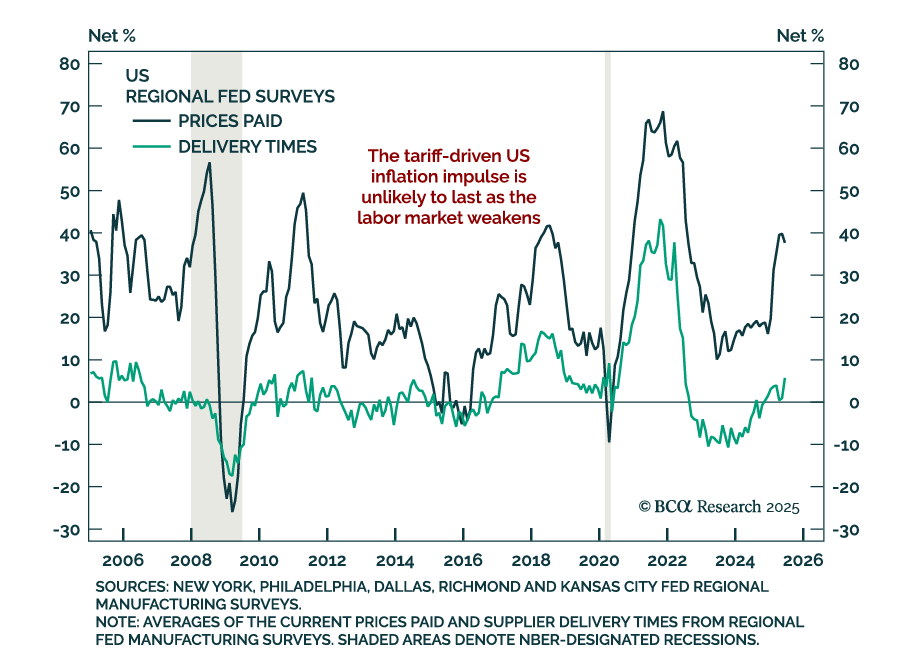

Trump’s immigration policies are protecting the US economy from a sharp rise in unemployment but steering it into a ‘mini stagflation’. Plus: a new tactical trade is to underweight global technology (IXN).

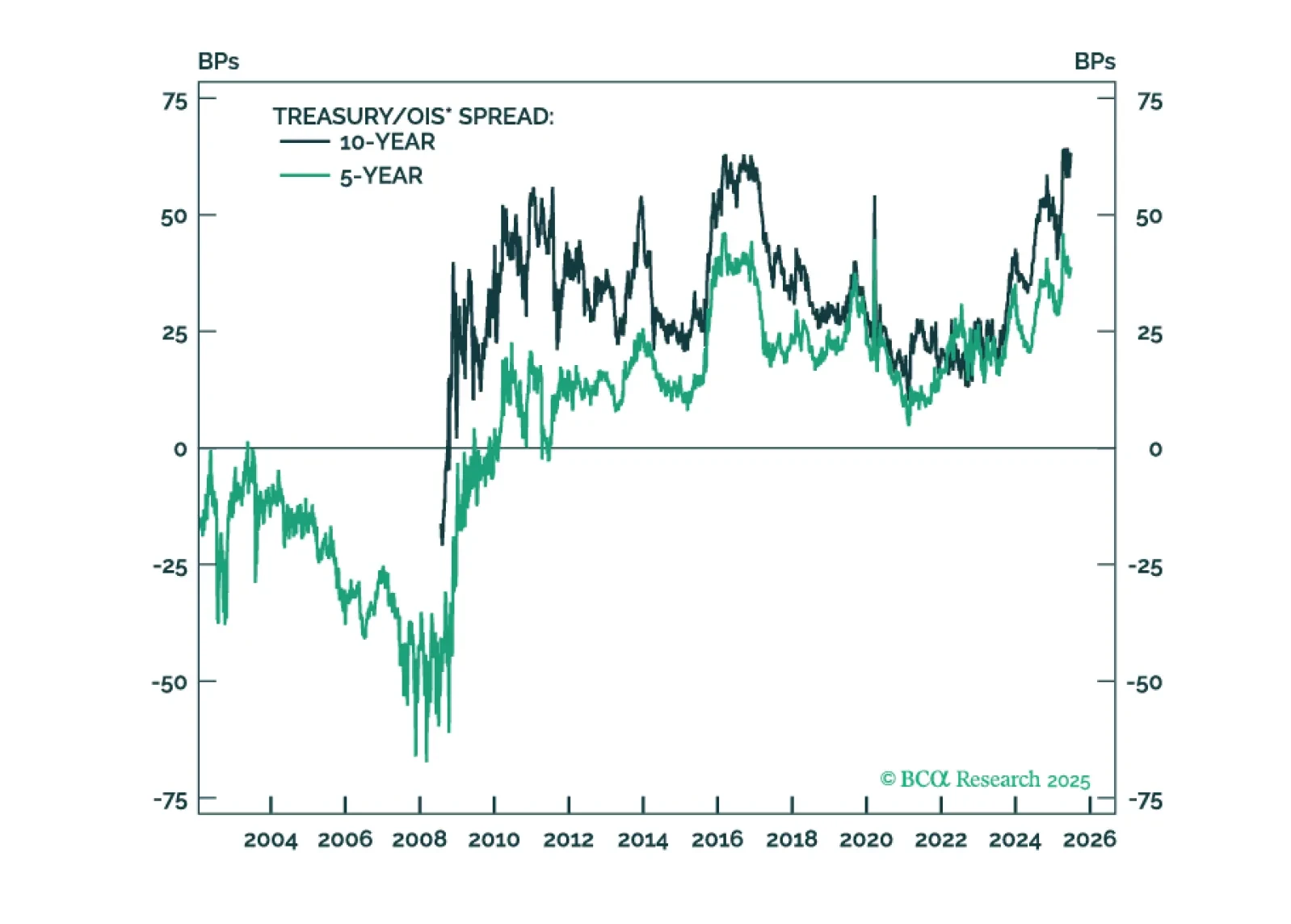

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.

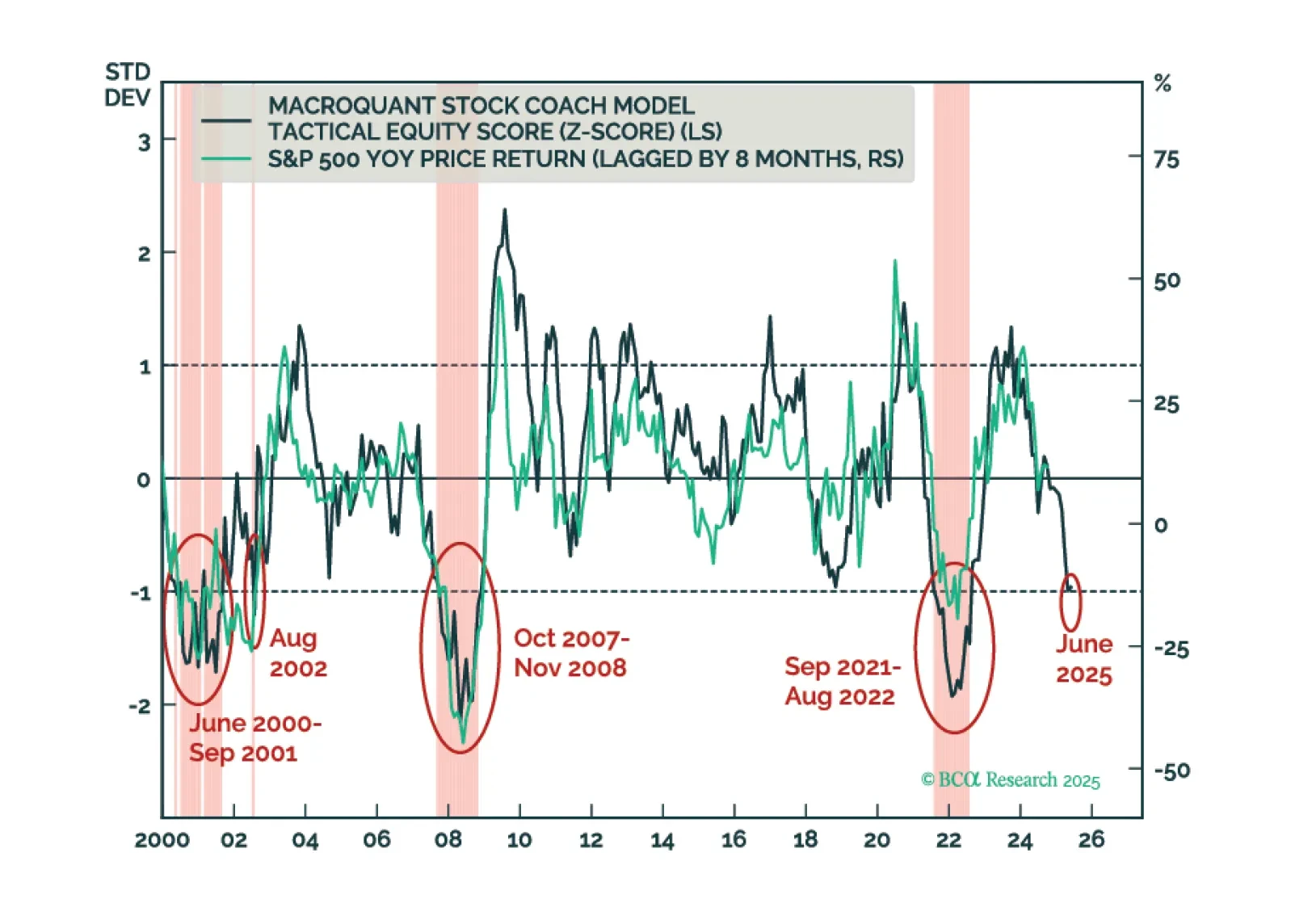

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.