Fixed Income

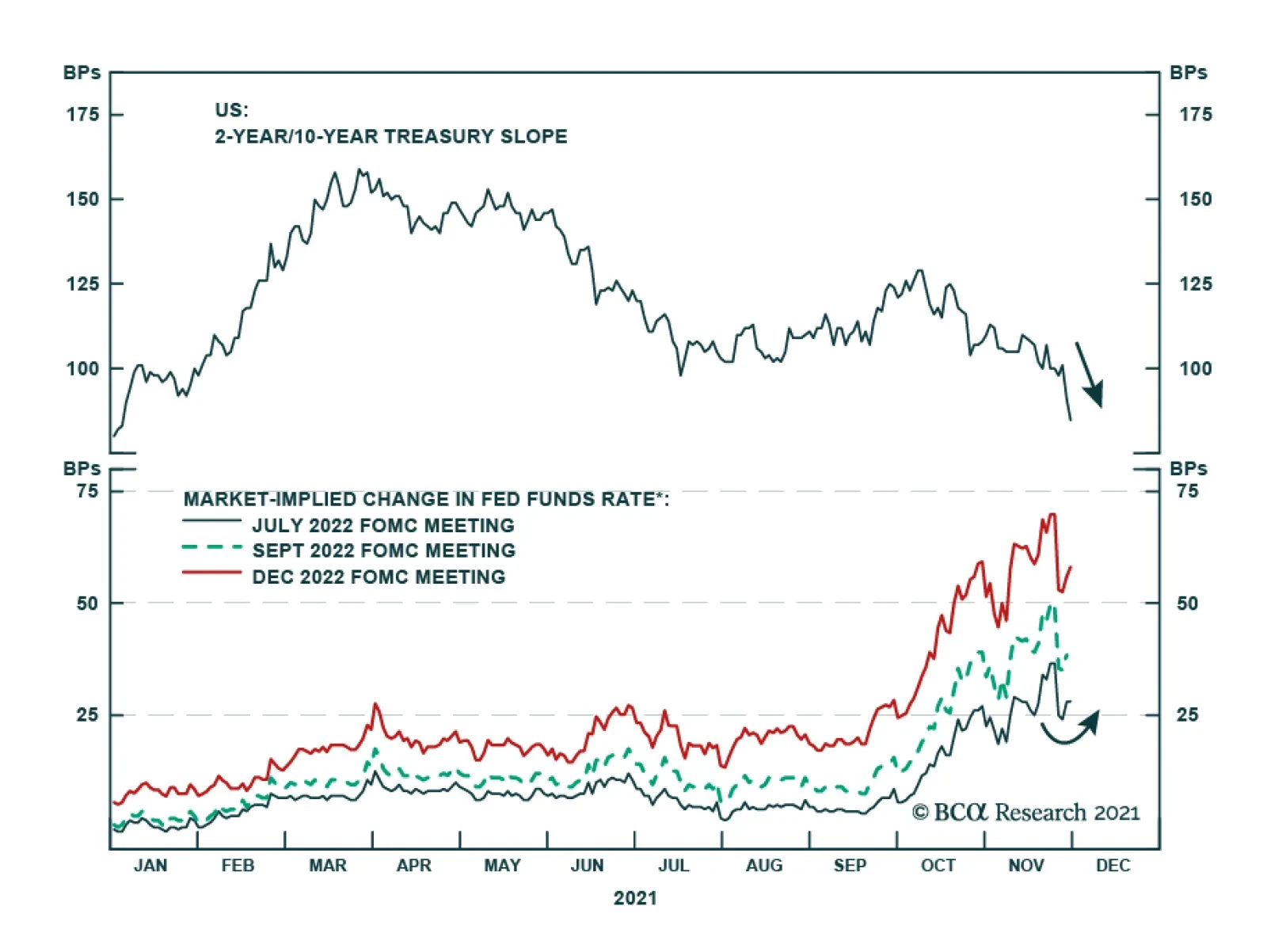

Highlights Below-Benchmark Portfolio Duration: Bond investors should keep portfolio duration low in 2022. While the market’s pricing of the expected Fed liftoff date and initial pace of rate hikes is reasonable, terminal fed funds rate expectations are far too low. Own Treasury Curve Steepeners: The 2/10 Treasury slope will flatten by less than what is currently discounted in the forward curve in 2022. Investors should position for this by going long the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. Sell Short-Maturity TIPS: Investors should maintain a neutral allocation to long-maturity TIPS versus nominal Treasuries and an underweight allocation to short-maturity TIPS versus nominal Treasuries. We also recommend an outright short position in 2-year TIPS, as short-maturity real yields have a lot of upside in 2022. Overweight Corporate Bonds Versus Treasuries … For Now: We are overweight corporate bonds versus duration-matched Treasuries, for now, but expect to turn more defensive in the first half of 2022 once the yield curve sustainably moves into a flatter regime. Relative valuations suggest that investors should favor high-yield corporates over investment grade. Overweight Emerging Market Bonds Versus US Corporates: EM bonds offer an attractive spread advantage versus US corporates, and a weakening US dollar will help boost returns in 2022. A Maximum Overweight Allocation To Municipal Bonds: Municipal bonds offer exceptional value, especially at the long-end of the curve, and state & local government balance sheets are in excellent shape. Underweight Agency MBS: Agency Mortgage-Backed Securities don’t adequately compensate investors for the likely pace of refi activity in 2021. An up-in-coupon stance is also advisable to take advantage of rising bond yields. Feature BCA published its 2022 Outlook on December 1st. That report lays out the main macroeconomic themes that our strategists see driving markets next year. This Special Report explains how investors can profit from those themes in US fixed income markets. Specifically, we offer seven key US fixed income views for 2022. This report is limited to the seven key investment views, and only discusses Fed policy in the context of how it influences those views. Next week we will publish a more comprehensive “Fed In 2022” report that will delve into our outlook for the Fed next year. Outlook Summary First, a summary of the main economic views presented in BCA’s 2022 Outlook.1 On Economic Growth: The COVID-19 pandemic will recede in importance in 2022 allowing US economic growth to remain above trend. Sizeable household savings and wealth will support consumer spending, the composition of which will shift away from goods and towards services. Corporate capital expenditures also look set to surge. On Inflation: A transition in consumer spending from goods to services and an increase in labor supply will cause US inflation to fall in 2022, though it will remain above the Fed’s target. On Fed Policy: The first Fed rate hike will occur between June and December 2022, depending on the paths of inflation and inflation expectations during the next few months. Fed tightening will continue into 2023. On China and Emerging Markets: Further policy easing in H1 2022 will lead to a reacceleration in Chinese economic activity in the back half of the year. The BCA house view is negative on EM equities for now but will turn more bullish when clearer signs of Chinese policy easing emerge. Risks To The Outlook: The greatest risk to the outlook is that the spread of the Omicron variant leads to the re-imposition of public health measures that will weigh on economic activity. The effect of the Omicron variant remains uncertain, but increasingly widespread vaccination and the advent of anti-viral treatments should help mitigate any negative economic impacts. Key View #1: Below-Benchmark Portfolio Duration Bond investors should keep portfolio duration low in 2022, favoring the 2-year maturity over the 10-year. While the market’s pricing of the expected Fed liftoff date and initial pace of rate hikes is reasonable, terminal fed funds rate expectations are far too low. Our recommendation to keep portfolio duration low in 2022 stems directly from our assessment of Federal Reserve policy. Without going into too much detail – we will do that in next week’s “Fed In 2022” report – the Fed appears to have adopted a more hawkish reaction function during the past month. The Fed’s official forward guidance says that it will not lift rates until the labor market reaches “maximum employment”. However, Fed Chair Jay Powell weakened that commitment in recent Senate testimony. Powell said that persistently high inflation threatens the economic recovery and implied that to reach its maximum employment goal the Fed may need to act pre-emptively to tame inflation. To us, this means that the Fed’s “maximum employment” condition for lifting rates is no longer binding. The Fed will accelerate the pace of tapering when it meets this week and will start lifting rates between June and December of next year, depending on the interim trends in inflation and inflation expectations. After liftoff, Fed rate hikes will proceed at a predictable pace of 75-100 bps per year until economic growth slows significantly. We expect the fed funds rate to reach at least 2% before that occurs, consistent with survey estimates of the long-run neutral fed funds rate. Let’s compare our estimate of the future fed funds rate path with what is currently priced in the bond market (Chart 1). Chart 1The Market's Rate Expectations

The Market's Rate Expectations

The Market's Rate Expectations

Liftoff The overnight index swap (OIS) curve is priced for Fed liftoff in May 2022. This is a tad early compared to our projections, but not by much. Pace After liftoff, the OIS curve is priced for the fed funds rate to rise 79 bps during the subsequent 12 months. Again, this is roughly consistent with our own expectations that the Fed will deliver three or four 25 basis point rate hikes per year. Terminal Rate It is the market’s pricing of the endpoint of the next tightening cycle – the terminal fed funds rate – that disagrees significantly with our forecast. The OIS curve is priced for the funds rate to reach 1.5% in 2024 and then stabilize. This is too low. It is too low compared to the last tightening cycle when the fed funds rate reached 2.45% in 2019. It is also too low compared to survey estimates from market participants and primary dealers. The median respondent to the New York Fed’s Survey of Market Participants estimates that the long-run neutral fed funds rate is 2%. The median response to the same question from the Survey of Primary Dealers is 2.25% and the median FOMC participant pegs the long-run neutral rate at 2.5%. Meanwhile, the 5-year/5-year forward Treasury yield – a rough proxy for the long-run neutral interest rate that’s priced in the Treasury market – sits at only 1.73%. Historically, the 5-year/5-year forward yield converges with survey estimates of the long-run neutral rate as the Fed moves toward tightening (Chart 2). This means the 5-year/5-year forward Treasury yield has at least 27-52 bps of upside in 2022. Chart 25y5y Has Room To Rise

5y5y Has Room To Rise

5y5y Has Room To Rise

Treasury Yield Forecasts Chart 3Treasury Yield Forecasts

Treasury Yield Forecasts

Treasury Yield Forecasts

Chart 3 shows the 2-year, 5-year and 10-year Treasury yields along with the expected paths that are discounted in the forward curve for the next 12 months. The shaded regions in each panel represent our fair value estimates of where those yields will trade if the market moves to price-in our expected future path for the fed funds rate. The upper bound of the fair value range represents the most hawkish fed funds rate scenario that we think is feasible. It assumes that Fed liftoff occurs in June, that rate hikes proceed at a pace of 100 bps per year and that the fed funds rate levels-off at a terminal rate of 2.08% (8 bps above the lower-end of a 2%-2.25% target range). The lower bound of the fair value range represents the most dovish fed funds rate scenario that we think is feasible. It assumes that Fed liftoff occurs in December 2022, that rate hikes proceed at a pace of 75 bps per year and that the fed funds rate levels-of at a terminal rate of 2.08%. Chart 3 shows that the 10-year Treasury yield is well below even the lower-end of our fair value range. The 5-year Treasury yield is a bit too low compared to our target range and the 2-year yield is consistent with our fair value range, though at the very upper-end. The investment conclusions are obvious. Bond investors should keep portfolio duration low in 2022. They should avoid the 10-year maturity and allocate most funds to shorter maturities like the 2-year. It should be noted that we used a conservative 2.08% terminal rate estimate in the scenarios presented in Chart 3. This is at the low-end of most survey estimates. What’s more, the BCA Outlook makes a strong case that those survey estimates will be revised higher once it becomes apparent that interest rates will have to rise to well above 2% to contain inflation. We agree that survey estimates of the long-run fed funds rate are probably too low, but we don’t expect them to be revised higher in 2022. Upward terminal rate revisions are probably a story for 2023 or 2024, sometime after the Fed has delivered a few rate hikes and it becomes apparent that more will be needed to slow an overheating economy. Appendix A at the end of this report translates different fed funds rate scenarios into 12-month expected returns for every Treasury maturity. We show scenarios where the liftoff date varies between June 2022 and December 2022, where the pace of rate hikes varies between 75 bps and 100 bps per year and where the terminal fed funds rate varies between 2.08% and 2.58%. The 10-year Treasury note is projected to deliver negative returns in every scenario we tested. Meanwhile, the 2-year Treasury note is projected to deliver a small positive return in every single scenario. These results support our conclusion from Chart 3. Investors should maintain below-benchmark portfolio duration and favor short maturities over long maturities. Risks To The View The first risk to our bearish view on US Treasuries is a resurgence of the pandemic. The 10-year Treasury yield continues to track the “pandemic trade” in the stock market. That is, the 10-year yield rises when a basket of equities that benefit from economic re-opening outperforms a basket of equities that benefit from lockdowns, and vice-versa (Chart 4). So far, the news about the virulence of the Omicron COVID variant has been encouraging, and our base case scenario assumes a further easing of pandemic concerns over the course of 2022. The second risk to our view is that the Fed moves too aggressively toward rate hikes causing an abrupt tightening of financial conditions that weighs on economic growth and sends long-dated bond yields lower. The shaded region in Chart 5 shows that this exact dynamic played out in 2018. Fed rate hikes started to pressure the dollar higher and weigh on equities. This led to tighter financial conditions and slower economic growth. The impact of tighter financial conditions was not immediately evident in the bond market, but slower growth eventually caused the Fed to back away from rate hikes leading to a late-2018 peak in the 10-year yield. Chart 410yr Tracks The "Pandemic Trade"

10yr Tracks The "Pandemic Trade"

10yr Tracks The "Pandemic Trade"

Chart 5Watch Financial Conditions In 2022

Watch Financial Conditions In 2022

Watch Financial Conditions In 2022

Compared to the 2018 scenario, we see less risk of Fed over-tightening in 2022 mainly because the fed funds rate is starting out at a much lower level. However, it will be important to track financial conditions as the Fed moves toward liftoff. Undue tightening would cause us to reverse our positioning. Key View #2: Own Treasury Curve Steepeners The 2/10 Treasury slope will flatten by less than what is currently discounted in the forward curve in 2022. Investors should position for this by going long the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. We also recommend buying the 20-year bond versus a duration-matched barbell consisting of the 10-year note and 30-year bond as an attractive duration-neutral carry trade. The scenarios presented in the prior section show that the 2-year Treasury yield is priced within the bounds of our estimated fair value range while the 10-year Treasury yield looks too low. Logically, it makes sense to position for a steepening of the 2/10 Treasury curve to profit from this divergence. Chart 6 illustrates the implications of the prior section’s fair value estimates for different Treasury slopes. Our fair value range projects that the 2/10 Treasury slope will be between 38 bps and 89 bps in 12 months, above the 37 bps that is currently priced into the forward curve. The forward curve is also priced for too much flattening in the 2/5 Treasury slope, while the 5/10 slope is consistent with the lower end of our fair value range. The conclusion is that investors should implement 2/10 Treasury curve steepeners in 2022 on the expectation that the 2/10 slope will flatten by less than what is currently discounted in the forward curve. A comparison of the 5-year/5-year forward Treasury yield with a target range based on survey estimates of the long-run neutral fed funds rate also supports the case for 2/10 steepeners. Historically, an increase in the 5-year/5-year forward yield towards its target range corresponds with a steepening of the 2/10 slope (Chart 7). Bear-flattening moves in the 2/10 slope only occur when the 5-year/5-year forward is within its target band, as was the case in 2017/18. Given that the 5-year/5-year forward yield is currently well below its survey-derived target range, there is room for some 2/10 steepening as yields rise. Chart 6Treasury Slope Forecasts

Treasury Slope Forecasts

Treasury Slope Forecasts

Chart 7A Rising 5y5y Will Steepen The Curve

A Rising 5y5y Will Steepen The Curve

A Rising 5y5y Will Steepen The Curve

One way to position for a steeper 2/10 curve is to go long the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. Presently, this trade looks very attractive. The 2/5/10 butterfly spread shows a significant yield advantage in the 5-year bullet over the 2/10 barbell, both in absolute terms and relative to our fair value model (Chart 8). While we view this as a good trade, we don’t think it’s the best way to position for 2/10 steepening. We prefer a position long the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. This trade gives you long exposure at the 2-year maturity instead of the 5-year maturity which will boost returns if the 2/5 slope steepens, as we anticipate it will (Chart 6, panel 2). Chart 8Curve Steepeners Are Cheap

Curve Steepeners Are Cheap

Curve Steepeners Are Cheap

In addition to our recommended 2/10 steepener, we advise clients to favor the 20-year bond versus a duration-matched barbell consisting of the 10-year note and 30-year bond. While we’d expect some flattening of the 10/30 slope in 2022, this trade should still perform well because of its huge carry advantage. The tables in Appendix A show that the 20-year bond earns a massive 12-month carry (income plus rolldown return) of 3.05% compared to 1.85% for the 10-year note and 1.80% for the 30-year bond. Key View #3: Sell Short-Maturity TIPS Chart 9TIPS Breakevens

TIPS Breakevens

TIPS Breakevens

Investors should maintain a neutral allocation to long-maturity TIPS versus nominal Treasuries and an underweight allocation to short-maturity TIPS versus nominal Treasuries. Other attractive positions include: an outright short position in 2-year TIPS, an inflation curve steepener (short 2yr TIPS/long 2yr nominal/long 10yr TIPS/short 10yr nominal), and a TIPS curve flattener (short 2yr TIPS/long 10yr TIPS). As noted at the beginning of this report, we see inflation trending down in 2022. Inflation will remain high enough for the Fed to feel comfortable lifting rates, but it won’t match the elevated readings that are currently discounted in TIPS. Interestingly, long-maturity TIPS breakeven inflation rates are roughly consistent with the Fed’s 2.3%-2.5% target range (Chart 9). The 5-year/5-year forward TIPS breakeven inflation rate is a bit too low, at 2.13%, and the 10-year TIPS breakeven inflation rate is currently 2.47%. With long-dated TIPS breakevens so close to the Fed’s target, we recommend a neutral allocation to long-maturity TIPS versus long-maturity nominal Treasuries heading into 2022. In our view, the mispricing in TIPS lies at the front-end of the curve. The 2-year TIPS breakeven inflation rate has risen to 3.23%, well above the Fed’s 2.3%-2.5% target range. This year’s surge in short-maturity TIPS breakevens has also resulted in a deeply inverted inflation slope (Chart 9, bottom panel). Table 1Regression of Monthly Changes In CPI Swap Rate Versus Monthly Changes In 12-Month Headline CPI Inflation (2010 - Present)

2022 Key Views: US Fixed Income

2022 Key Views: US Fixed Income

Short-maturity inflation expectations are highly sensitive to changes in CPI inflation, much more so than long-maturity expectations. In fact, monthly changes in the 2-year CPI swap rate are more than twice as sensitive to headline inflation than are monthly changes in the 10-year CPI swap rate (Table 1). This means that the cost of short-maturity inflation compensation will decline as inflation moderates in 2022. We recommend an underweight allocation to short-maturity TIPS versus short-maturity nominal Treasuries. We also think an outright short position in 2-year TIPS will be highly profitable in 2022. If we assume that the 2-year TIPS breakeven inflation rate falls to the middle of the Fed’s target range during the next 12 months, and additionally that the 2-year nominal Treasury yield converges with our fair value estimate using the scenario of a September Fed liftoff, 100 bps per year hike pace and 2.08% terminal rate, then we calculate that the 2-year TIPS yield will rise from its current -2.56% to -0.98% during the next 12 months (Chart 10). Chart 10A Lot Of Upside In Short-Maturity Real Yields Short 2-Year TIPS

A Lot Of Upside In Short-Maturity Real Yields Short 2-Year TIPS

A Lot Of Upside In Short-Maturity Real Yields Short 2-Year TIPS

Chart 10 also shows that the anticipated rise in the 2-year TIPS yield greatly outpaces the modest expected increase in the 10-year TIPS yield. This means that a position in 2/10 TIPS curve flatteners will turn a profit in 2022 (Chart 10, bottom panel). Key View #4: Overweight Corporate Bonds Versus Treasuries … For Now We are overweight corporate bonds versus duration-matched Treasuries, for now, but expect to turn more defensive in the first half of 2022 once the yield curve sustainably moves into a flatter regime. Relative valuations suggest that investors should favor high-yield corporates over investment grade. A key pillar of our corporate bond investment process is to split the economic cycle into three phases based on the slope of the yield curve (Chart 11). Phase 1 of the cycle is defined as the period from the end of the last recession until the 3-year/10-year Treasury slope breaks below 50 bps. Phase 2 of the cycle spans the period when the slope is between 0 bps and 50 bps. Phase 3 lasts from when the yield curve inverts until the start of the next recession. Chart 11The Three Phases Of The Economic Cycle

The Three Phases Of The Economic Cycle

The Three Phases Of The Economic Cycle

Our historical analysis shows that excess corporate bond returns versus duration-matched Treasuries tend to be strongest in Phase 1. They are usually positive, but much lower, in Phase 2 and are often negative in Phase 3 (Table 2). Table 2Corporate Bond Returns Across The Three Phases Of The Cycle

2022 Key Views: US Fixed Income

2022 Key Views: US Fixed Income

We have been firmly in Phase 1 since April 2020 and, as we would expect, excess corporate bond returns have been strong. However, we will not remain in Phase 1 much longer. The 3-year/10-year Treasury slope is currently 50 bps, right on the precipice between Phase 1 and Phase 2. We recommend an overweight allocation to corporate bonds versus Treasuries for now, but we will adopt a more defensive posture toward corporates once we transition into Phase 2. We expect this will happen sometime in the first half of 2022. Why Are We Not In Phase 2 Already? Chart 12Curve Flattening Is Overdone

Curve Flattening Is Overdone

Curve Flattening Is Overdone

The 3-year/10-year Treasury slope is hovering right around 50 bps. However, as is noted earlier in this report, we think that recent yield curve flattening is overdone and expect it to reverse somewhat in the coming months. Chart 12 shows the 3-year/10-year slope along with an expected fair value range. This range is based on a 100 bps Fed rate hike pace, a 2.08% terminal rate and varying the liftoff date between June 2022 and December 2022. This fair value range only breaks below 50 bps between March and September of next year. Given our yield curve view, we are positioned for one last period of strong corporate bond outperformance during the next few months. But we will turn more defensive once we judge that we have sustainably transitioned into a Phase 2 environment. Why Turn More Defensive In Phase 2? Chart 13IG Corporate Valuations

IG Corporate Valuations

IG Corporate Valuations

It’s correct to point out that excess corporate bond returns are still generally positive in Phase 2 environments, so ideally, we would remain overweight corporate bonds versus Treasuries throughout Phase 2. This makes sense theoretically, but strategically we think it will be wise to adopt a different approach this cycle. The main reason to err on the side of caution is that corporate bond valuations are extremely stretched. The 12-month breakeven spread for the investment grade corporate bond index is at its 6th percentile since 1995. This means that the investment grade corporate bond index has only been more expensive than today 6% of the time since 1995 (Chart 13). Tight spreads mean that expected returns will be modest, even in a favorable cyclical environment. In other words, we are not sacrificing much expected return by reducing exposure early in the cycle. Given that we can’t predict the start of the next Phase 3 period with exact precision, we think it makes sense to be more defensive this cycle. We will sacrifice some modest expected returns to ensure that we are well positioned for the next period of significant spread widening. Our corporate bond strategy is supported by an empirical study of historical returns. Table 3A shows average 12-month excess returns for the investment grade corporate bond index after certain combinations of the 3/10 Treasury slope and average index option-adjusted spread (OAS) are observed. Table 3B shows 90% confidence intervals for the averages presented in Table 3A.

Chart

Chart

The tables show that a strategy of remaining overweight corporate bonds versus Treasuries after the yield curve transitions into Phase 2 only works when the corporate index OAS is above 100 bps. A transition into Phase 2 portends negative excess corporate bond returns when the OAS is below 100 bps, as it is today. Favor High-Yield Over Investment Grade Chart 14HY Corporate Valuations

HY Corporate Valuations

HY Corporate Valuations

While investment grade corporate bonds look extremely expensive compared to history, high-yield corporate bonds look somewhat expensive, but much less so. The average High-Yield index OAS is 1 bp below its pre-COVID low, but investors still get a nice spread pickup for moving out of the Baa-rated credit tier and into the Ba-rated tier (Chart 14). Our prior research has shown that high-yield corporates tend to outperform duration-matched Treasuries when the excess index spread after accounting for default losses is above 100 bps.2 If we assume a minimum required excess spread of 100 bps and a 40% recovery rate on defaulted debt, we can calculate that the junk index is priced for a default rate of 3.4% during the next 12 months (Chart 14, bottom panel). All available evidence suggests that the default rate will come in below 3.4% during the next 12 months, leading to positive excess returns for high-yield corporate bonds. The default rate came in at 1.8% for the 12-month period ending in November and it has been dropping like a stone, consistent with the reading from our Default Rate Model (Chart 15). We also recently wrote about the exceptionally good health of corporate balance sheets.3 We expect the default rate will be in the mid-2% range in 2022, below what is priced into the junk index. Chart 15Corporate Defaults Will Stay Low In 2022

Corporate Defaults Will Stay Low In 2022

Corporate Defaults Will Stay Low In 2022

Junk’s valuation advantage leads us to recommend that investors maintain a preference for high-yield corporates over investment grade. We will turn more defensive on both investment grade and high-yield corporates once we transition into a Phase 2 environment, but we may still retain our preference for high-yield over investment grade at that time, as long as junk stays relatively cheap. Key View #5: Overweight Emerging Market Bonds Versus US Corporates Investment grade USD-denominated Emerging Market bonds (both sovereigns and corporates) will outperform US corporate bonds with the same credit rating and duration in 2022. EM bonds offer an attractive spread advantage versus US corporates, and 2022 returns will be boosted by a weakening US dollar. We see an opportunity in Emerging Market (EM) bonds for US investors in 2022. Note that we are only referring to investment grade EM bonds denominated in US dollars. We consider both investment grade USD-denominated EM sovereign bonds and investment grade USD-denominated EM corporate & quasi-sovereign bonds. EM Sovereigns Chart 16EM Sovereigns

EM Sovereigns

EM Sovereigns

EM sovereigns have modestly outperformed Treasuries so far this year (see Appendix B for a complete breakdown of year-to-date performance for different corporate bond sectors), and yet the sector remains attractively valued in the sense that the average index OAS has still not recovered its pre-COVID low (Chart 16). A look at recent performance trends shows that EM sovereigns outperformed credit rating and duration-matched US corporates in H2 2020 when the sector benefited from a huge yield advantage and a rapidly depreciating US dollar.4 This year, EM sovereigns lagged US corporates as the dollar strengthened. Looking ahead to 2022, we think that the recent bout of dollar strength is close to its end as the bond market has already moved to price-in an extremely hawkish Fed outlook at the front-end of the curve. A flat or depreciating dollar will benefit EM bonds in 2022, as will the yield advantage in EM sovereigns versus credit rating and duration-matched US corporates (Chart 16, panel 4). This yield advantage will only look more attractive as the Treasury curve flattens and the outlook for US corporate spreads deteriorates. At the country level, we see the best EM sovereign opportunities in Mexico, Russia, Chile, UAE, Qatar and Saudi Arabia. The bonds of all these countries outperformed credit rating and duration-matched US corporate bonds during the past 12 months, and they continue to offer a sizeable spread advantage (Chart 17).

Chart 17

EM Corporates & Quasi-Sovereigns The investment grade USD-denominated EM Corporate & Quasi-Sovereign index shows a similar relative return pattern to the EM Sovereign index, though overall performance has been better (Chart 18). We see that the index outperformed credit rating and duration-matched US corporates dramatically in H2 2020 when the dollar was under pressure. Relative returns have been more stable this year as the dollar has strengthened. Chart 18EM Corporates & Quasi-Sovereigns

EM Corporates & Quasi-Sovereigns

EM Corporates & Quasi-Sovereigns

EM corporates & quasi-sovereigns should continue to outperform credit rating and duration-matched US corporates in 2022. A weaker dollar will certainly help, but the main driver of outperformance will be the very attractive yield advantage (Chart 18, panel 4). Key View #6: A Maximum Overweight Allocation To Municipal Bonds Municipal bonds offer exceptional value, especially at the long-end of the curve, and state & local government balance sheets are in excellent shape. US bond investors should favor tax-exempt municipal bonds relative to both Treasuries and equivalently-rated corporate bonds. Long-maturity tax-exempt municipal bonds continue to be one the most attractively priced assets in the US fixed income space. As we discussed in a recent report, one big reason for the attractive valuation is that municipal bonds tend to pay premium coupon rates.5 This significantly reduces the duration risk in long-dated munis. The first two columns of Table 4 show the yield ratios and breakeven tax rates between different municipal bond sectors and duration-matched Treasury securities. We see that the breakeven tax rate – the tax rate that equalizes after-tax yields between the two sectors – is a mere 11% for 12-17 year general obligation munis. The breakeven tax rate between 12-17 year revenue munis and duration-matched Treasuries is only 3%, and the longest-maturity munis actually offer a before-tax yield advantage versus Treasuries! Table 4Muni/Treasury And Muni/Credit Yield Ratios

2022 Key Views: US Fixed Income

2022 Key Views: US Fixed Income

Table 4 shows that munis also offer excellent value compared to corporate bonds with the same credit rating and duration, especially at the long-end of the curve. Breakeven tax rates between munis and corporate credit range from 3% to 21% for maturities longer than 12 years. What’s even more impressive about municipal bonds is that their attractive valuations are buttressed by extremely high credit quality. State & local government balance sheets have received a huge boost from federal stimulus during the past two years, and this has sent net state & local government savings (revenues minus expenditures) surging into positive territory (Chart 19). But it’s not just federal stimulus that has aided state & local governments. Even if we exclude transfer payments altogether, we find that the difference between tax receipts and consumption expenditures is rising sharply relative to interest expense (Chart 19, panel 2). Ratings agencies have noticed the improvement in state & local government budgets and ratings upgrades have far outpaced downgrades during the past year (Chart 19, bottom panel). Chart 19State & Local Balance Sheets In Good Shape

State & Local Balance Sheets In Good Shape

State & Local Balance Sheets In Good Shape

Key View #7: Underweight Agency MBS Chart 20Poor MBS Performance Will Continue

Poor MBS Performance Will Continue

Poor MBS Performance Will Continue

Agency Mortgage-Backed Securities don’t adequately compensate investors for the likely pace of refi activity in 2021. An up-in-coupon stance is also advisable to take advantage of rising bond yields. We noted in a recent report that Agency Mortgage-Backed Securities have performed poorly in 2021.6 The main reason for the poor performance is that the compensation for prepayment risk embedded in MBS spreads (aka option cost) started the year at a very low level, but mortgage refinancing activity has been much higher than expected (Chart 20). The conventional 30-year MBS option cost has been rising, but it is still only back to where it was in 2019 (Chart 20, panel 2). This is not sufficiently attractive for us to advocate buying MBS. While rising bond yields will be a tailwind for refi activity in 2022, we still expect the pace of refinancings to be relatively strong because the rapid run-up in home prices has made it extremely enticing for households to tap the equity in their homes through cash-out refis. Within a recommended underweight allocation to MBS, we recommend that investors favor higher coupon securities over lower coupon ones. Higher-coupon MBS carry less duration than lower-coupon MBS and also wider OAS and greater convexity. This means that high-coupon MBS will outperform low-coupon MBS if bond yields rise in 2022, as we expect they will. Appendix A: Treasury Return Forecasts

Image

Image

Image

Image

Image

Image

Image

Image

Image

Image

Image

Image

Appendix B: US Bond Sector Year-To-Date Performance

Image

Image

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see The Bank Credit Analyst, “Outlook 2022: Peak Inflation – Or Just Getting Started?”, dated December 1, 2021. 2 Please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020. 3 Please see US Bond Strategy Weekly Report, “The Fed’s Inflation Problem”, dated November 23, 2021. 4 A weaker dollar tends to benefit USD-denominated EM bonds because it makes it easier for foreign issuers to service their dollar denominated debts. 5 Please see US Bond Strategy Weekly Report, “The Best & Worst Spots On The Yield Curve”, dated October 26, 2021. 6 Please see US Bond Strategy Weekly Report, “The Omicron Impact”, dated November 30, 2021. Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

Highlights The risk to European stocks from higher yields is overstated for 2022. Not only do equities possess a valuation cushion compared to bonds, but also the stock returns/bond yields correlation remains positive. This positive correlation is only two decades old, and it is a consequence of the stabilization of inflation and inflation expectations, which caused bond yield changes to mostly reflect adjustment in anticipated economic activity. As long as the recent inflation upsurge peters off next year, the equity/yield correlation will remain positive in 2022. Despite this sanguine short-term view, the long-term outlook is fraught with risks because next year’s inflation decline will be temporary; inflation is on a secular uptrend. The equity returns/bond yield correlation will become negative toward the middle of the decade, which will create a major headwind for the secular returns of both stocks and bonds. Feature Extremely low yields and elevated valuations constitute a potentially toxic mix for the equity outlook next year. The logic is straightforward: if yields rise enough, nosebleed multiples will become unjustifiable and the stock market will crash. Chart 1Protection Against Higher Yields

Protection Against Higher Yields

Protection Against Higher Yields

The picture is more complex and instead, European equities are likely to withstand higher yields. To begin with, BCA Research’s US Bond strategists anticipate a modest rise in Treasury yields to 2.25% in 2022, and our Global Fixed-Income strategists foresee an even more limited increase in German rates. Moreover, as we showed in our 2022 Key Views piece published last week, European equities embed a large valuation cushion in the form of a significant premium in their dividend yield relative to Bund yields (Chart 1). The correlation between yields and equities is another facet that will impact the effect of higher yields on the equity bull market. For now, it is premature to conclude that the positive correlation between yields and the absolute performance of European equities is poised to turn negative again in 2022. However, over the next couple of years, such a correlation reversal will take place, because inflation expectations are increasingly likely to become unmoored to the upside. Stocks Like Higher Yields Over the past two decades, one of the major financial market paradoxes has been the relationship between equity prices and bonds yields. Since 1998, the weekly returns of the MSCI Euro Area equity benchmark have correlated positively with the change in 10-year German yields (Chart 2). However, prior to the late 1990s, changes in bond yields and stocks prices were negatively correlated. Chart 2For Two Decades, Bond Yields And Stocks Prices Have Moved Together

For Two Decades, Bond Yields And Stocks Prices Have Moved Together

For Two Decades, Bond Yields And Stocks Prices Have Moved Together

The key to the shifting relationship between stocks and bonds is the link between yields and economic activity. Stock returns have always been procyclical because earnings are the most important driver of equity returns (Chart 3). However, bond yields have become increasingly pro-cyclical over time. Today, Bund yields and the German LEI move in tandem, but, prior to 1986, their five-year rolling correlation was negative (Chart 4). Chart 3Stocks Follow Earnings Who Follow Growth

Stocks Follow Earnings Who Follow Growth

Stocks Follow Earnings Who Follow Growth

Chart 4Shifting Link Between Bunds And German Growth

Shifting Link Between Bunds And German Growth

Shifting Link Between Bunds And German Growth

The positive correlation between German growth and German yields sheds light on why the correlation between yields and stocks is now positive, but it does not explain why this positive link emerged in the late 1990s and not earlier. Financial asset prices reflect global phenomena. Stock indices in advanced economies overrepresent multinationals which are affected by global economic fluctuations. Meanwhile, capital is fungible and flows freely across borders. As a result, German bond yields are not the unique factor that matters to the correlation between equities and stock. Instead, the behavior of global yields and equities is critical. Chart 5Living In The Shadow Of The Asian Crisis

Living In The Shadow Of The Asian Crisis

Living In The Shadow Of The Asian Crisis

According to this logic, the correlation between global yields and global growth becomes important. As Chart 5 illustrates, the relationship between global bond returns and global economic activity became much closer around 1998 than it was prior to this date. The key turning point was the Asian crisis of 1997/98. Why was the Asian crisis so fundamental? It was the end state of the disinflationary trend started under Federal Reserve Chairman Paul Volker. After the Asian crisis, the region’s newly industrialized economies switched from chronic current account deficits to chronic surpluses, which added to the global supply of savings. Moreover, Asian economies became hypercompetitive because of severely devalued exchange rates, which limited pricing power around the world. Finally, the Chinese economy became a force to be reckoned with and its share of global trade expanded massively. Together, these forces amplified competitive pressure around the world and made every inflation uptick self-limiting. The impact of the shock is visible in the inflation data. As Chart 6 shows, core inflation in the US and in the G7 has been stable since 1998, capped near 2.5%, except for 2021. Additionally, after the Asian crisis, the volatility of core inflation collapsed among both the G7 and Eurozone economies (Chart 7). Chart 62.5%, A 20-Year Old Ceiling

2.5%, A 20-Year Old Ceiling

2.5%, A 20-Year Old Ceiling

Chart 71998: RIP CPI Volatility

1998: RIP CPI Volatility

1998: RIP CPI Volatility

The effect of this steady inflation was to stabilize inflation expectations. Thus, after 1998, the most important driver of bond price annual changes has been fluctuations in anticipated real economic activity, which explains why the relationship between global bond returns and the global LEI became much tighter afterward (Chart 5, on page 4). This result is crucial to understand the impact of higher yields for equities. It suggests that, if rising yields reflect improving economic growth, then the correlation between yields and stocks will remain positive and equities may climb higher along with mounting long-term interest rates. Bottom Line: Higher yields do not necessarily portend the end of the equity bull market. Stock prices and bond yields have been positively correlated since the Asian crisis of 1997/98 because fluctuating growth expectations drive most of the change in yields. As long as this remains the case, equities can handle higher yields. Can The Correlation Shift Sign Again? The correlation between equities and bonds is not static. There are threats that could restore both temporarily or permanently the negative correlation between changes in bond yields and stock returns that prevailed prior to 1998. A Temporary Correlation Shift? Since their March 2020 lows, 10-year yields have increased 94bps and 51bps in the US and Germany, respectively. Meanwhile, the MSCI Eurozone equity benchmark is up 78%. We are clearly not yet in an environment in which rising long-term interest rates hurt stocks. In the short term, the correlation between yield changes and equity returns may turn negative if yield moves into constraining territory—this is to say, if they rise enough to risk a recession. In more academic terms, this equates to rates moving above the neutral rate of interest, or r-star. Chart 8A Long Way To Go Before Policy Becomes Tight

A Long Way To Go Before Policy Becomes Tight

A Long Way To Go Before Policy Becomes Tight

There is little indication that interest rates are moving above this level in the short term. US and European policy rates remain well below Taylor rule estimates of equilibrium (Chart 8), which suggests that policies are still highly accommodative. The most worrisome signal comes from the slope of the yield curve. Since March 2021, the US 2-/10-year yield curve has flattened by 76bps to 81bps and, since October 2021, the same yield curve has flattened by 23bps to 35bps in Germany. Moreover, the 20-/30-year US yield curve became inverted in October 2021. These dynamics may indicate that policy is already on the verge of becoming too tight, even if only five interest rate hikes are expected in the US over the next two years. Chart 9Term Premia Are Still Negative

Term Premia Are Still Negative

Term Premia Are Still Negative

A curve flattening episode is the normal course of events when central banks become less accommodative; it is not a sign of impending doom. Instead, an inverted yield curve is the indication that the policy rate is above r-star. After all, if interest rates genuinely constrain growth, they will slow economic activity in the future, which will necessitate lower rates and generate a negative curve slope. We are not there yet. Moreover, the term-premium remains negative across major advanced economies, which suggests that a recessionary signal will come from a deeper yield-curve inversion than in the past (Chart 9). Chart 10Upside To The Terminal Rate

Upside To The Terminal Rate

Upside To The Terminal Rate

Another factor likely to allow yields to rise without killing the equity market is that the expected terminal rate of interest remains too low, as we wrote in our 2022 Key Views piece last week. Historically, it is common for the expected terminal rate to rise as central banks begin to lift interest rates, especially if the economy handles the first hikes well. Today, the expected terminal rate is below the levels that prevailed after the GFC, despite a much firmer economy unburdened by private sector deleveraging and excessive fiscal tightening (Chart 10). As such, we anticipate the expected terminal rate to increase, which will limit how quickly the yield curve will flatten next year even if the Fed elevates interest rates and the ECB aggressively downshifts its pace of asset purchases once the PEPP ends. Chart 11Long-Term Inflation Expectations Are Not A Concern, Yet

Long-Term Inflation Expectations Are Not A Concern, Yet

Long-Term Inflation Expectations Are Not A Concern, Yet

Under this aperture, the biggest risk for stocks remains inflation. Further acceleration in inflation, especially if it pushes the 5-year/5-year forward inflation breakeven rate above the Fed’s comfort zone (Chart 11), could hurt stocks. Essentially, investors would price in a shift in the monetary policy environment whereby risks of a severe tightening would increase. However, as we recently wrote, the odds are mounting that short-term inflation will soon peak. Oil inflation is ebbing, while transportation costs are declining and supply bottlenecks are beginning to ease. Moreover, money growth in the US and the Eurozone, which proved relevant variables to explain inflation this year, is also waning (Chart 12). Finally, a mounting number of global central banks are tightening policy, which implies that maximum accommodation is behind us (Chart 13) In this context, we expect the positive correlation between stock returns and yield changes to remain broadly positive. A short-term rise in yields could easily contribute to equity market volatility and may even cause a deeper stock market correction than any experienced since April 2020. However, this will prove to be a temporary phenomenon, and thus we remain buyers of the dip. Chart 12Slowing Money Supply Growth, At Last

Slowing Money Supply Growth, At Last

Slowing Money Supply Growth, At Last

Chart 13Global Policy Is Becoming Less Easy

Global Policy Is Becoming Less Easy

Global Policy Is Becoming Less Easy

A Longer-Term Correlation Shift? A shift in the long-term correlation between equity returns and bond yield changes is a much more meaningful risk to stocks than short-term changes. BCA expects inflation to peak in the short term, but this will only be part of a stop-and-go process. Inflation is on a structural uptrend and so, any decline in 2022 and early 2023 will morph into renewed pressure, after the global output gap becomes positive again by the end of next year. Chart 14A Deflationary Tailwind Is Gone

A Deflationary Tailwind Is Gone

A Deflationary Tailwind Is Gone

Many structural forces are moving away from deflationary to inflationary. True, technological progress remains a deflationary anchor. However, this downward pressure on inflation is no longer buttressed by a deepening of globalization (Chart 14). Moreover, because of the rise of populism around the world over the past five years, fiscal policy is unlikely to move back to the austere Washington Consensus that dictated governance from President Reagan up to the moment President Trump took power. Additionally, ageing across advanced economies and China, as well as the so-called “Great Resignation,” will constrain the expansion of the global supply side. This background suggests that the period of flat inflation that prevailed from 1998 to 2020 is ending. As a corollary, inflation expectations will embark on a multi-year upward drift. This process is likely to loosen the correlation between economic activity and yields. As a result, the period of positive correlation between yield changes and equity returns is in its last innings. This will represent a major difficulty for asset allocators over the next ten to twenty years, as it points to poor long-term real returns for both bonds and stocks. Bottom Line: The correlation between stock returns and bond yield changes is likely to remain positive in 2022, which implies that European stocks will eke out another year of positive returns, despite BCA’s house view that yields will rise. However, the long-term outlook is more problematic. The growing likelihood that inflation is making a secular upturn means that the two-decades old positive correlation between equity returns and bond yield change will become negative again around the middle of the decade. This shift will have a profound and deleterious impact on both stocks’ and bonds’ secular returns. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations

The Correlation Convolution

The Correlation Convolution

Cyclical Recommendations

The Correlation Convolution

The Correlation Convolution

Structural Recommendations

The Correlation Convolution

The Correlation Convolution

Closed Trades Currency Performance Fixed Income Performance Equity Performance

Highlights The helicopter drops are over, … : The economic impact payments and supplemental unemployment insurance benefits may have stopped, but their full impact has yet to be felt. … but fiscal and monetary policy will continue to support demand, … : US households are sitting on more than $2 trillion of excess pandemic savings. If they were to spend just half of their stash over the next two or three years, the economy would gain a steady tailwind. … and the macro backdrop will remain equity-friendly, … : Monetary policy will be less accommodative going forward but it will remain solidly supportive of markets and the economy across all of 2022. … so investors should stick around for one last round: Equities and spread product outperform when monetary policy is easy. As long as COVID-19 doesn’t spring a nasty surprise, the expansion will continue and risk assets will once again generate positive excess returns over Treasuries and cash. Feature BCA editors’ annual sit-down with Mr. and Ms. X provides a welcome opportunity to gather our thoughts for the coming year and review how this year’s calls panned out. Looking back to this time last year,1 our risk-friendly recommendations performed well as the rationale behind them proved to be sound. Financial markets thrived in the wake of monetary and fiscal policy measures intended to err on the side of providing too much accommodation. The policy efforts were massive, and their support for markets and the economy has yet to be fully exhausted; indeed, their lengthy half-life is a key pillar of our sanguine 2022 outlook. Unlike last December, investors cannot look forward to peak accommodation in the year ahead; the peak is behind us and monetary and fiscal stimulus will be throttled back. The Fed is currently deliberating how much to accelerate its taper timetable, with an eye toward gaining the flexibility to hike rates sooner than previously planned. The hawkish turn foreshadowed by Chair Powell two weeks ago in Congressional testimony unsettled markets somewhat, but it is important to note that monetary policy settings are merely on track to become less accommodative – they are nowhere near crossing the line to restrictive and will not approach it anytime soon. Investors can be certain that markets will enjoy ample policy support across all of 2022 and we expect that equities will still be in a bull market when Mr. and Ms. X return to discuss the outlook for 2023. We are on board with the BCA consensus as detailed in the Bank Credit Analyst’s 2022 outlook.2 Early indications suggest that the Omicron variant will not be enough of a threat to provoke a negative growth surprise and we expect that the pandemic will recede in importance as the year unfolds. As it fades, supply chains should become less snarled, easing the near-term pressures that have been pushing prices higher. We expect that markets are overestimating inflation in the near term and that growth will be robust in the US and other developed economies. Despite the dialing back of some accommodation, monetary policy will remain easy, supporting economic activity and market valuations. We foresee another year of solidly positive excess returns for risk assets. The Economy Is Firing On All Cylinders You wouldn’t necessarily know it to talk with investors, much less consumer confidence survey respondents, but aggregate demand is surging and ought to remain robust going forward. Households are in fantastic shape. Although their net worth growth slowed in the third quarter, its 13% annualized seven-quarter (1Q20 through 3Q21) pace is within a whisker of all-time highs (Chart 1). They have accumulated $2.3 trillion of excess savings since the pandemic began and have plenty of capacity to borrow to augment their spending power. Just about anyone who wants a job can have one: the ratio of job openings to unemployed workers is making new highs (Chart 2) and the share of people in the labor force filing initial jobless claims is approaching the all-time lows set before the pandemic (Chart 3). Chart 1The Wealth Effect Will Support Consumption

The Wealth Effect Will Support Consumption

The Wealth Effect Will Support Consumption

Chart 2More Jobs Than People Without Them ...

More Jobs Than People Without Them ...

More Jobs Than People Without Them ...

Businesses are on a solid financial footing, as well. Debt as a share of net worth is near the lower end of its typical range since the high yield bond market got going in the late ‘80s (Chart 4). Borrowing costs are scraping all-time lows (Chart 5) and profit margins are wide (Chart 6). Banks and fixed income asset managers are falling all over themselves to lend to businesses and will continue to do so while default rates remain low. Chart 3... And Almost No Layoffs

... And Almost No Layoffs

... And Almost No Layoffs

Chart 4Corporations Have Less Debt And More Equity, ...

Corporations Have Less Debt And More Equity, ...

Corporations Have Less Debt And More Equity, ...

Chart 5... But Debt Has Never Cost Less ...

... But Debt Has Never Cost Less ...

... But Debt Has Never Cost Less ...

Chart 6... And Profit Margins Are Wide

... And Profit Margins Are Wide

... And Profit Margins Are Wide

Financial conditions will remain highly accommodative despite the Fed’s and other major developed world central banks’ moves to make them less easy at the margin. Below-equilibrium policy rates will continue to encourage financed purchases of homes, autos and other durable goods and entice investment via low hurdle rates. If sovereign bond yields rise modestly in 2022 in line with our high-conviction base case, governments won’t feel any pressure to tighten the fiscal screws. That may nourish modern monetary theory fantasies to the ultimate detriment of public finances, but it should ensure that all three engines of domestic demand – households, businesses and government – will hum in 2022. Omicron has reminded everyone that the pandemic is not over, but the shadow it casts on public health and economic activity is set to shrink. Booster shots of the Pfizer vaccine apparently provide effective protection, and Omicron’s mutations will not allow it to evade Merck’s and Pfizer’s soon-to-be-approved antiviral pills. The availability of pills to treat those who contract COVID could possibly be a game-changer in terms of neutralizing its global threat. Distributing shelf-stable pills is vastly simpler than delivering vaccines that need to be transported at temperatures below -70 degrees Fahrenheit. The Earnings Bar Has Been Set Very Low Our constructive view would not translate into risk friendly investment strategy if asset prices already discounted it or were expecting something even better. Just as the economy is on a better path than consumers seem to perceive and investors believe can persist, S&P 500 earnings per share are poised to grow over the next four quarters by more than the bottom-up analyst consensus expects. As compared to the simple annualized run rate of last quarter’s earnings ($215.76, or $53.89 times 4), the analyst consensus is calling for effectively no growth ($215.87) over the four quarters through 3Q22. That is a surprising prediction based on two sets of empirical evidence. First, earnings typically rise outside of recessions (Chart 7). Second, analysts have consistently forecast that forward four-quarter earnings would top the run rate of the last reported quarter’s earnings for four decades (Chart 8). This year, though, analysts have repeatedly called for quarter-over-quarter declines in earnings (Table 1), only to have reported numbers shred their estimates by jaw-dropping margins, just as they have in all six full quarters since COVID-19 arrived (Chart 9). We interpret the phase shift in the magnitude of earnings beats as evidence that companies have surprised themselves by how much they’ve been able to increase efficiency and/or cut costs during the pandemic. Our interactions with the investment community suggest that it has also been surprised but views the gains as one-off events that are unlikely to continue. Chart 7Earnings Declines Outside Of Recessions Are Rare

Earnings Declines Outside Of Recessions Are Rare

Earnings Declines Outside Of Recessions Are Rare

Chart 8This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

Table 1Grim Expectations

2022 Key Views: Stay For One More Round

2022 Key Views: Stay For One More Round

Expectations of sequentially declining earnings would fit if the economy were flirting with falling below stall speed, as it regularly did during the sluggish post-GFC expansion. But they are completely at odds with the Bloomberg economist consensus that GDP will grow at a 5% real annualized rate this quarter and 3.9% in calendar 2022 (Table 2). Over time, S&P 500 revenue growth should converge with nominal GDP growth, so the current expectations for around 10% and 7% annualized nominal GDP growth in 4Q21 and 2022, respectively, are a decent starting point for estimating S&P 500 revenue growth over those periods. While we expect that S&P 500 profit margins have peaked, we do not foresee a sharp decline in 2022, and operating leverage should ensure that high single-digit revenue growth will translate into healthy earnings gains.

Chart 9

Table 2Above-Trend Growth Ahead

2022 Key Views: Stay For One More Round

2022 Key Views: Stay For One More Round

Bottom Line: The S&P 500 should have no trouble topping consensus estimates that foresee next to no growth in earnings over the next four quarters. There is ample room for corporate earnings to surprise to the upside. Our Major Disagreement With Markets Differences of opinion make markets and our biggest one pertains to the future direction of interest rates. We think the widespread conviction that the Fed will be unwilling or unable to raise the fed funds above 2%, if that, lest it crush financial markets and the real economy is way off base. The majority of investors seem to have taken the decade between the crisis and the pandemic as evidence that rates will remain very low for very long. Many of them must be buying the longer end of the Treasury curve in anticipation that an expedited liftoff date is the first step on the path to the next recession (Chart 10). Chart 10The Bond Market Sees Ice, Not Fire

The Bond Market Sees Ice, Not Fire

The Bond Market Sees Ice, Not Fire

The risk asset selloff that ensued in December 2018 after the FOMC marched the fed funds rate up to 2.5% looms large in the markets’ minds and feeds the widespread view that an ambitious program of rate hikes will pull the rug out from under financial assets and the economy. Many investors have also been conditioned by the post-crisis decade to assume that inflation cannot exceed 2% for a sustained period. The market view is rooted in honest-to-goodness evidence, but we think it is of little relevance now, given the way the massive pandemic fiscal stimulus programs have altered the backdrop. In the space of thirteen months from March 2020 through March 2021, Congress passed bills injecting over $5 trillion of aid – 25% of a year’s GDP – into the economy. The Herculean effort contrasted sharply with the skittish disbursement of less than 5% of GDP on the Bush and Obama administrations’ watch from 2008 through 2010. The aftermath of the crisis demonstrated that even multiple rounds of QE do not by themselves trigger inflation, especially if demoralized households and businesses are disinclined to borrow money to consume or invest, and chastened banks are subjected to regulatory strictures forcing them to maintain sizable new capital buffers and discouraging them from making any but plain-vanilla loans to highly rated borrowers. The Bernanke Fed’s three rounds of QE presumably tamped down interest rates, but the cash that bought the Treasury and agency securities barely tiptoed into the wider world before the primary dealer banks sent it right back to the Fed as excess reserves. With banks hiding their QE money under the mattress, the money supply didn’t expand in any notable way after the crisis. Thanks to Congress’ series of 2020-21 helicopter drops, the money supply has been growing at rates that would make the late Paul Volcker’s head spin (Chart 11). Inflation is fiendishly more complicated than Milton Friedman’s always-and-everywhere dictum suggests, but there’s now a whole lot of money chasing a limited amount of goods, services and assets. We expect that a receding pandemic will allow greater quantities of goods and services to be produced, and that securities underwriters and their clients are hard at work ramping up asset supply, but inflation has far more of a chance to gain traction now than it did in the decade before the pandemic. Chart 11Bringing "Always And Everywhere" Back Into Vogue?

Bringing "Always And Everywhere" Back Into Vogue?

Bringing "Always And Everywhere" Back Into Vogue?

We therefore think the lower-for-longer and lower-for-ever crowd will find itself offsides at some point in the next few years. We do not think it will get its comeuppance in 2022, however, as we see long yields rising only modestly, with the 10-year Treasury yield ending next year at 2-2.25%. Though we expect the fed funds rate will end the upcoming hiking cycle well north of 2%, bringing about the end of the bull markets in equities and credit, and quite possibly inducing the next recession, we do not think markets will abandon their new-normal rates view by the end of next year. This story will be continued, likely with a greater sense of urgency, in our 2023 outlook. Investment Recommendations Consistent with the foregoing, we make the following recommendations for 2022: Overweight equities in multi-asset portfolios. Although they are not cheap, and may experience a turbulent ride in 2022 as inflation concerns wax and wane, COVID-19 infections periodically surge and the Fed tries to adjust its messaging and actions on the fly, stocks should continue to generate sizable positive excess returns over Treasuries and cash. Overweight cyclical sectors and underweight defensive sectors within equity portfolios. If we’re right to be constructive on the global economy, Energy, Industrials, Materials and Financials are better positioned to benefit than Health Care, Staples and Utilities. Overweight small-cap equities versus large-cap equities. The S&P 600 SmallCap Index has greater exposure to our cyclicals-over-defensives call and our US Equity Strategy colleagues highlight that its constituents are cheaper than the S&P 500’s and are projected to have better earnings growth. Adding small-cap exposure to equity portfolios aligns with our constructive view on the economy and markets. Underweight fixed income in multi-asset portfolios. Underweight Treasuries within bond portfolios. Maintain below-benchmark duration within bond portfolios. Though we do not expect the bond market to see things entirely our way next year, we think the long end of the yield curve will shift out somewhat. We therefore have little appetite for duration and Treasuries and expect spread product will outperform Treasuries and high-yield corporate bonds will outperform investment-grade corporates. Consider hybrid alternatives to traditional fixed income securities. When we roll out our multi-asset ETF portfolio next month, it will include a hybrid bucket of income-generating assets to help multi-asset investors seeking income find low-beta destinations with a fighting chance of generating positive real total returns. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the December 14, 2020 US Investment Strategy Report, "2021 Key Views: It’s The Policy, Stupid." 2 Please see the December 2021 Bank Credit Analyst, "OUTLOOK 2022: Peak Inflation – Or Just Getting Started?"

Highlights 1. How will the pandemic resolve? 2. Will services spending recover to its pre-pandemic trend? 3. Will we spend our excess savings? 4. How will central banks react to inflation? 5. Will cryptocurrencies continue to eat gold’s lunch? 6. How fragile is Chinese real estate? 7. Will there be another shock? Fractal analysis: Personal goods versus consumer services. Feature Chart of the WeekWill Services Spending Recover To Its Pre-Pandemic Trend?

Will Services Spending Recover To Its Pre-Pandemic Trend?

Will Services Spending Recover To Its Pre-Pandemic Trend?

“Judge a man by his questions, not by his answers” The quotation above is often misattributed to Voltaire instead of its true author, Pierre-Marc-Gaston de Lévis. Irrespective of the misattribution, we agree with the maxim. Asking the right questions is more important than finding answers to the wrong questions. In this vein, this report takes the form of the seven crucial questions for 2022 (and our answers). 1. How Will The Pandemic Resolve? As new variants of SARS-CoV-2 have arrived like clockwork, the number of new global cases of infection and the virus reproduction rate have formed a near-perfect mathematical ‘sine wave’. This near-perfect sine wave will propagate into 2022 (Chart I-2). Chart I-2The Pandemic's Sine-Wave Will Propagate Into 2022

The Pandemic's Sine-Wave Will Propagate Into 2022

The Pandemic's Sine-Wave Will Propagate Into 2022

But how will this sine wave of infections translate into mortality, morbidity, and stress on our healthcare systems? As we explained in RNA Viruses: Time To Tell The Truth, the answer depends on the specific combination of contagiousness, immuno-evasion, and pathogenicity of each variant. Yet none of this should come as any surprise. Flus and colds also come in waves, which is why we call them flu and cold seasons. And the morbidity of a given flu and cold season depends on the aggressiveness of that season’s flu and cold variant. So, just like the flu and the cold, Covid will become an endemic respiratory disease which comes in waves. The trouble is that our under-resourced health care systems can barely cope with a bad flu season, let alone with an additional novel disease that can be worse than the flu. Hence, until we add enough capacity to our healthcare systems, expect more disruptions to economic activity from periodic non-pharmaceutical interventions such as travel bans, vaccine passports, and face-mask mandates. 2. Will Services Spending Recover To Its Pre-Pandemic Trend? The pandemic has given us a crash course in virology and epidemiology. We now understand antigens, antibodies, and ‘reproduction rates.’ We understand that a virus transmits as an aerosol in enclosed unventilated spaces, and that singing, and yelling eject this viral aerosol. We understand that vaccinations for RNA viruses have limited longevity, do not prevent reinfections, and that certain environments create ‘super-spreader’ events. Armed with this new-found awareness, a significant minority of people have changed their behaviour. Services which require close contact with strangers – going to the dentist or in-person doctors’ appointments, going to the cinema or to amusement parks, or using public transport – are suffering severe shortfalls in demand. Given that this change in behaviour is likely long-lasting, demand for these services is unlikely to regain its pre-pandemic trend in 2022 (Charts I-3 - I-6). Chart I-3Dental Services Are Far Below The Pre-Pandemic Trend

Dental Services Are Far Below The Pre-Pandemic Trend

Dental Services Are Far Below The Pre-Pandemic Trend

Chart I-4Physician Services Are Far Below The Pre-Pandemic Trend

Physician Services Are Far Below The Pre-Pandemic Trend

Physician Services Are Far Below The Pre-Pandemic Trend

Chart I-5Recreation Services Are Far Below The Pre-Pandemic Trend

Recreation Services Are Far Below The Pre-Pandemic Trend

Recreation Services Are Far Below The Pre-Pandemic Trend

Chart I-6Public Transportation Is Far Below The Pre-Pandemic Trend

Public Transportation Is Far Below The Pre-Pandemic Trend

Public Transportation Is Far Below The Pre-Pandemic Trend

Therefore, to keep overall demand on trend, spending on goods will have to stay above its pre-pandemic trend. This will be a tough ask. Durables, by their very definition, last a long time. Even clothes and shoes, though classified as nondurables, are in fact quite durable. Meaning that are only so many cars, iPhone 13s, gadgets, clothes and shoes that any person can own before reaching saturation. If, as we expect, spending on goods falls back to its pre-pandemic trend, but spending on services does not recover to its pre-pandemic trend, then there will be a demand shortfall in 2022 (Chart of the Week). 3. Will We Spend Our Excess Savings? If spending falls short of income – as it did through the pandemic – then, by definition, our savings have gone up. Many people claimed that this war chest of savings would unleash a tsunami of spending. Well, it didn’t. And, it won’t. Previous episodes of excess savings in 2004, 2008, and 2012 had no impact on the trend in spending (Chart I-7).

Image

The explanation comes from a theory known as Mental Accounting Bias. The theory states that we segment our money into different accounts, which are sometimes physical, sometimes only mental, and that our willingness to spend money depends on which mental account it occupies. This contrasts with standard economic theory which assumes that money is perfectly fungible, meaning that a dollar in a current (checking) account is no different to a dollar in a savings or investment account. In practice, money is not fungible, because we attach different emotions to our different mental accounts. A dollar in our current account we will gladly spend, but a dollar in our savings account we will not spend. Hence, the moment we move the dollar from our current account into our savings account, our willingness to spend it collapses. This explains why consumption trends have no connection with windfall income receipts once those income receipts end up in our savings mental or physical account. Pulling all of this together, the war chest of savings accumulated during the pandemic is unlikely to change the overall trend in spending. 4. How Will Central Banks React To Inflation? The real story of the current ‘inflation crisis’ is that while goods and commodity prices have surged exactly as expected in a positive demand shock, services prices have not declined as would be expected in the mirror-image negative demand shock. The result is that aggregate inflation has surged even though aggregate demand has not (Chart I-8 and Chart I-9). Chart I-8Goods Prices Have Reacted To A Positive Demand Shock...

Goods Prices Have Reacted To A Positive Demand Shock...

Goods Prices Have Reacted To A Positive Demand Shock...

Chart I-9...But Service Prices Have Not Reacted To A Negative Demand Shock

...But Service Prices Have Not Reacted To A Negative Demand Shock

...But Service Prices Have Not Reacted To A Negative Demand Shock

Why have services prices remained resilient despite a massive negative demand shock? One answer, as explained in question 2, is that much of the shortfall in services demand is due to behavioural changes, which cannot be alleviated by lower prices. If somebody doesn’t go to the dentist or use public transport because he is worried about catching Covid, then lowering the price will not lure that person back. In fact, the person might interpret the lower price as a signal of greater risk, and might become more averse. In technical terms, the price elasticity of demand for certain services has flipped from its usual negative to positive. This creates a major problem for central banks, because if the price elasticity of services demand has changed, then surging aggregate inflation is no longer a reliable indicator of surging aggregate demand. To repeat, inflation is surging even though aggregate demand is barely on its pre-pandemic trend. Hence in 2022, central banks face a Hobson’s choice. Choke demand that does not need to be choked, or turn a blind eye to inflation and risk losing credibility. 5. Will Cryptocurrencies Continue To Eat Gold’s Lunch? Most of the value of gold comes not from its economic utility as a beautiful, wearable, and electrically conductive metal, but from its investment value as a hedge against the debasement of fiat money. The multi-year investment case for cryptocurrencies is that they are set to displace much of gold’s investment value. Still, to displace gold’s investment value, cryptocurrencies need to match its other qualities: an economic utility, and limited supply. A cryptocurrency’s economic utility comes from its means of exchange for the intermediation services that its blockchain provides. For example, if you issue a bond or smart-contract using the Ethereum blockchain, then you must pay in its cryptocurrency ETH. Which gives ETH an economic utility. Furthermore, the number of blockchains that will succeed as go-to places for intermediation services will be limited, and each cryptocurrency has a limited supply. Thereby, the supply of cryptocurrencies that have a utility is also limited. With an economic utility, a limited supply, and drawdowns that are becoming smaller, cryptocurrencies can continue to displace gold’s dominance of the $12 trillion anti-fiat investment market. Therefore, the cryptocurrency asset-class can continue its strong structural uptrend, albeit punctuated by short sharp corrections (Chart I-10). Chart I-10Cryptocurrencies Will Continue To Displace Gold's Investment Value

Cryptocurrencies Will Continue To Displace Gold's Investment Value

Cryptocurrencies Will Continue To Displace Gold's Investment Value

The corollary is that the structural outlook for gold is poor. 6. How Fragile Is Chinese Real Estate? A decade-long surge in Chinese property prices has lifted Chinese valuations to nosebleed levels. According to global real estate specialist Savills, prime real estate yields in China’s major cities are now barely above 1 percent, and the world’s five most expensive cities are all in China: Hangzhou, Shenzhen, Guangzhou, Beijing, and Shanghai (Chart I-11).

Chart I-11

Without a social safety net and with limited places to park their money, Chinese savers have for years been encouraged to buy homes, in the widespread belief that property is the safest investment, whose price only goes up. With the bulk of people’s wealth in property acting as a perceived economic safety net, even a modest decline in house prices would constitute a major shock to the household sector’s hopes and expectations of what property is. Therefore, in contrast to the US housing debacle in 2008, the Chinese government will ensure that its property market adjustment does not come from a collapse in home prices. Rather, it will come from a collapse in property development and construction activity. This will have negative implications for commodities, emerging Asia, developing countries that produce raw materials, and machinery stocks worldwide. 7. Will There Be Another Shock? Most strategists claim that shocks, such as the pandemic, are unpredictable. We disagree. Yes, the timing and source of an individual shock is unpredictable, but the statistical distribution of shocks is highly predictable. We define a shock as any event that causes the long-duration bond price in a major economy to rally or slump by at least 20 percent.1 Using this definition through the last 60 years, the statistical distribution of the number of shocks in any ten-year period is Poisson (3.33) and the time between shocks is Exponential (3.33). This means that in any ten-year period, the likelihood of suffering a shock is a near-certain 95 percent; in any five-year period, it is an extremely high 80 percent; in a two-year period it is a coin toss at 50 percent; and even in one year it is a significant 30 percent (Chart I-12).

Chart I-12

Therefore, on a multi-year horizon, another shock is a near-certainty even if we do not know its source or precise timing. The question is, will it be net deflationary, or net inflationary? Our high-conviction view is that it will be net deflationary. Meaning that even if it starts as inflationary, it will quickly morph into deflationary. The simple reason is that it is not just Chinese real estate that is fragile. Through the past ten years, world prime residential prices are up by 70 percent while rents are up by just 25 percent2 (Chart I-13). Meaning that the bulk of the increase in global real estate prices is due to skyrocketing valuations. The culprit is the structural collapse in global bond yields – which, in turn, is due to persistently ultra-low policy interest rates combined with trillions of dollars of quantitative easing. Chart I-13Property Price Inflation Has Far Exceeded Rent Inflation

Property Price Inflation Has Far Exceeded Rent Inflation

Property Price Inflation Has Far Exceeded Rent Inflation