Fixed Income

Highlights Energy Prices & Bond Yields: Surging energy prices are lifting inflation expectations in the US and Europe, while at the same time dampening consumer confidence amid diminished perceptions of real purchasing power. These conflicting trends are putting central banks in a tricky spot in the near-term, but tightening labor markets will force a more enduring need for dialing back global monetary accommodation in 2022, led by the Fed and the Bank of England. Stay below-benchmark on global duration exposure, favoring euro area government debt over US Treasuries and UK Gilts. High-Yield: Trans-Atlantic junk bond performance has diverged of late, with euro area spreads widening versus the US. This is a temporary distortion created by the pop in oil prices, with the Energy sector that benefits from higher oil prices representing a far greater share of the high-yield universe in the US compared to Europe. Maintain an overweight stance on European high-yield corporates. Feature Chart of the WeekGlobal Bond Yield Breakout?

Global Bond Yield Breakout?

Global Bond Yield Breakout?

It is not easy being an inflation-targeting central bank these days. Soaring energy prices, with the Brent crude benchmark price climbing to a 3-year high of $86/bbl last week and natural gas prices up nearly four-fold year-to-date in Europe. These moves are adding upward pressure to inflation rates already elevated because of disrupted supply chains and rising labor costs. Government bond yields in the developed markets are moving higher in response, driven by rising inflation breakevens and increasing central bank hawkishness that is causing a stir in negative real yields (Chart of the Week). Among the three most important developed economy central banks - the Fed, the ECB and the Bank of England (BoE) – the most forceful signaling of a need for tighter policy is surprisingly coming from Threadneedle Street in London, home to one of the most dovish central banks since the 2008 crisis. Numerous BoE officials, including Governor Andrew Bailey, have strongly hinted that UK rate hikes could begin as soon as next month’s policy meeting. Fed officials have suggested a similar timetable for the start of the QE taper. By contrast, members of the ECB Governing Council have paid lip service to the recent sharp pickup in euro area inflation but, for the most part, have stuck to the view that it will not last long enough to justify a policy response. The relative hawkishness among “The Big Three” central banks fits with our current recommended strategy on global duration exposure, staying below-benchmark, and country allocation, with the largest underweights to US Treasuries and UK Gilts. Should Central Banks Focus More On Inflation Or Growth? Monetary policymakers are in a difficult spot at the moment. Rising energy prices have breathed new life into inflation, and inflation expectations, even as global growth momentum has cooled off somewhat. Given the magnitude and breadth of the global energy price surge – even coal prices in China have shot up 120% since late August - it will be difficult for central bankers to “see through” the inflationary implications and worry more about growth (Chart 2). Rising energy prices are likely to extend the current global inflation upturn that has already gone on for longer than expected because of supply-chain disruptions. This raises the risk that consumers could turn more cautious on spending behavior if they have to devote more of their incomes just to fuel their cars or heat their homes. In the US, this dynamic already appears to be playing out. The acceleration of inflation has broadened out, with the Cleveland Fed’s trimmed mean CPI inflation measure (which removes the most volatile components of the CPI) rising to 3.5% in September (Chart 3, top panel). With US consumers seeing higher prices on a wider range of goods and services, they have raised their inflation expectations. The preliminary October University of Michigan US consumer confidence survey showed that 1-year-ahead inflation expectations rose to a 13-year high of 4.8% (middle panel). Chart 2Pouring Gas On Global Inflation

Pouring Gas On Global Inflation

Pouring Gas On Global Inflation

The New York Fed’s consumer survey showed a similar 1-year-ahead inflation forecast (5.3%), which is well above the forecast for income growth in 2022 (2.9%). Combining those two measures shows that US consumers implicitly see a contraction in their real incomes over the next 12 months. Chart 3US Consumers Expect A Sharp Decline In Real Purchasing Power

US Consumers Expect A Sharp Decline In Real Purchasing Power

US Consumers Expect A Sharp Decline In Real Purchasing Power

This has likely played a big role in the sharp fall in the University of Michigan consumer confidence index since the peak back in June (bottom panel), despite favorable US labor market conditions. US consumer perceptions of inflation appear much greater than the reality of inflation evident in the official price indices. The New York Fed survey also asks US consumers what their 1-year-ahead expectations are for major spending categories, like food or rent (Chart 4). Consumers expect somewhat slower inflation for food (7.0%) and gasoline (5.9%) over the next year, yet they also expect much higher medical care costs (9.4%) and rent (9.7%). For the latter two, those are considerably higher than the latest actual inflation rates seen in the US CPI (2.4% for rent, 0.4% for medical care) or PCE deflator (2.1% for rent, 2.4% for medical care). Taking these survey results at face value, it is likely that US consumers are overestimating how much their real incomes will suffer next year from higher inflation. This is especially true as US household income growth will likely surpass the 2.9% estimate seen in the New York Fed survey. Yet that does not preclude the Fed from starting to turn more hawkish. Central bankers are always on the lookout for signs that higher realized inflation is feeding through into rising inflation expectations, which could require a policy tightening response to prevent an overshoot of inflation targets. The Fed has given itself a bit more leeway in that regard by altering their policy framework to allow temporary deviations of inflation from the central bank targets. The BoE, however, has not given itself the same sort of flexibility, which is why it is now signaling an imminent rate hike in response to survey-based inflation expectations, and breakeven inflation rates on longer-dated index-linked Gilts, climbing to close to 4% (Chart 5). Yet even the Fed, with its Average Inflation Targeting framework, has signaled that a tapering of its bond purchases will likely begin by year-end. Chart 4US Consumer Inflation Expectations Well Above Actual Inflation

US Consumer Inflation Expectations Well Above Actual Inflation

US Consumer Inflation Expectations Well Above Actual Inflation

Markets are looking at the persistence of high inflation and have priced in a more hawkish trajectory for interest rates in the US, UK and even Europe over the next 12-24 months (Chart 6, bottom panel). Chart 5Inflation Weighing On UK & European Consumer Confidence

Inflation Weighing On UK & European Consumer Confidence

Inflation Weighing On UK & European Consumer Confidence

Real bond yields in those regions are also starting to move higher in response to rising rate expectations (third panel) - a bond-bearish dynamic that we have discussed at length in recent reports.1 Between those three, the BoE’s hawkish turn has hammered the Gilt market the hardest. Yet there has definitely been a spillover into rate expectations and bond yields in other countries on the back of the BoE guidance. We have already seen rate hikes from smaller developed market central banks, Norway and New Zealand, over the past month. If a major central bank like the BoE soon follows suit because of overshooting inflation expectations, then markets are justified in thinking that the Fed or even the ECB could be next. Of those “Big 3” central banks, we see the ECB as being the least likely to respond to the current inflation upturn with rate hikes in 2022. There is simply not enough evidence suggesting that the energy/supply-chain driven inflation in the euro area is broadening out into other parts of the economy on a sustainable basis. Furthermore, there is already some degree of monetary tightening “scheduled” in 2022 when the ECB’s pandemic bond purchase program expires in March. The ECB will not want to compound that by moving into rate hiking mode soon after. On the other hand, the Fed will likely see enough further tightening of US labor market conditions to begin hiking rates in the fourth quarter of 2022 (Chart 7). In the UK, After next month’s likely rate hike, the BoE will need to deliver at least another 50-75bps of additional hikes in 2022 and likely more in 2023 with real policy rates already well below neutral before the latest spike in energy prices. Chart 6Expect Higher Real Yields As Central Banks Turn More Hawkish

Expect Higher Real Yields As Central Banks Turn More Hawkish

Expect Higher Real Yields As Central Banks Turn More Hawkish

Chart 7Labor Markets, Not Commodities, Will Dictate Monetary Policy In 2022

Labor Markets, Not Commodities, Will Dictate Monetary Policy In 2022

Labor Markets, Not Commodities, Will Dictate Monetary Policy In 2022

With the Fed and BoE set to be far more hawkish than the ECB next year, we see greater risks of government bond yields rising faster, and higher than current forward rates, in the US and UK compared to the euro area (Chart 8). This justifies an overall cautious strategic stance on duration exposure in global bond portfolios. With regards to inflation-linked bonds, however, we recommend only a neutral overall stance. Elevated inflation breakevens have converged to, or even above, central bank inflation targets in all developed market economies (excluding Japan). 10-year UK breakevens, in particular, look very expensive on our fair value model (Chart 9). Chart 8Our Recommended "Big 3" Country Allocations

Our Recommended 'Big 3' Country Allocations

Our Recommended 'Big 3' Country Allocations

Chart 9Maintain An Overall Neutral Stance On Inflation-Linked Bonds

Maintain An Overall Neutral Stance On Inflation-Linked Bonds

Maintain An Overall Neutral Stance On Inflation-Linked Bonds

Bottom Line: Our view on the policy decisions of the Big 3 central banks in 2022 informs our strategic (6-18 months) investment strategy within those markets. Stay below-benchmark on overall global duration exposure, favoring euro area government debt over US Treasuries and UK Gilts. Fade The Recent Backup In European High Yield Spreads Chart 10A Slight Pickup In European Junk Spreads

A Slight Pickup In European Junk Spreads

A Slight Pickup In European Junk Spreads

Corporate credit markets in the US and Europe have calmed down since the July/August “Delta fueled” selloff with one notable exception – European high-yield (HY). The Bloomberg European HY index spread now sits 39bps above the September low, noticeably diverging from the US HY index spread (Chart 10). We view those wider spreads as a tactical buying opportunity for European junk bonds, both in absolute terms and versus US junk bonds. The recent underperformance appears rooted in soaring European energy prices. The spread widening has been concentrated in European consumer sectors (both cyclicals and non-cyclicals) that would be more exposed to the drain on real incomes from booming natural gas prices. Energy is also a smaller part of the European high-yield index (2%) compared to the US HY index (13%), which helps explain the performance gap with the US – the US index is more exposed to companies that benefit from higher energy prices (Chart 11). Chart 11Sectoral Breakdown Of US & Euro Area High-Yield Indices

Central Banks Backed Into A Corner

Central Banks Backed Into A Corner

Over a more medium-term perspective, there is little reason why there should be a meaningful performance difference between US and European HY. The path of spreads and excess returns (versus duration-matched government debt) for the two markets have been highly correlated in recent years (Chart 12). When adjusting European HY returns to allow a proper apples-to-apples comparison to US HY – by hedging European returns into US dollars and controlling for duration differences between the two markets – there has been little sustained difference in returns dating back to 2018. Chart 12Euro Area HY Has Closed The Gap Vs. The US

Euro Area HY Has Closed The Gap Vs. The US

Euro Area HY Has Closed The Gap Vs. The US

Chart 13Junk Default Rates Will Stay Low In 2022

Central Banks Backed Into A Corner

Central Banks Backed Into A Corner

More fundamentally, there is little difference in default rates that would justify a major divergence of HY spreads on both sides of the Atlantic. Moody’s is forecasting a HY default rate for a rate of 2% in both the US and Europe for 2022 (Chart 13). Such similar default rate expectations make sense with economic growth likely to remain well above trend in 2022 in both the US and Europe. Higher inflation will also boost nominal GDP growth, helping lift corporate revenues and the ability to service debt. From a valuation perspective, there is also little to choose from between European and US HY: The default-adjusted spread, which takes the current HY index spread and subtracts expected default losses over the next twelve months, is 196bps in Europe and 166bps in the US (Chart 14). While those spreads are below the post-2000 mean in both markets, they are still above past valuation extremes. The percentile ranking of 12-month breakeven spreads (the amount of spread widening over one year that would eliminate the yield advantage of HY over duration-matched government bonds) are also similar, 25% for European HY and 26% for US HY (Chart 15). These suggest HY spreads are not particularly “cheap”, from a historical perspective, in either market, but they could move lower to reach previous historical extremes. Chart 14Low Expected Default Losses Supporting HY Valuations

Low Expected Default Losses Supporting HY Valuations

Low Expected Default Losses Supporting HY Valuations

Chart 15Overall HY Spreads Are Tight In The US & Europe

Overall HY Spreads Are Tight In The US & Europe

Overall HY Spreads Are Tight In The US & Europe

Chart 16Euro Area Ba-Rated HY Spreads Look More Attractive

Central Banks Backed Into A Corner

Central Banks Backed Into A Corner

Summing it all up, there is no discernable reason why European HY should trade at a sustainably wider spread to US HY, outside of the compositional issue related to the weight of the Energy sector in both markets. When breaking down the two markets by credit rating buckets, European Ba-rated corporates even look more attractive versus similarly-rated US corporates, based on 12-month breakeven spread percentile rankings (Chart 16). Bottom Line: Maintain a strategic overweight stance on European high-yield corporates, and tactically position for some relatively better performance of European junk bonds versus US equivalents. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Report, "What If Higher Inflation Is Not Transitory?", dated September 23, 2021, available at gfis.bcaresearch.com. Recommendations Duration Regional Allocation Spread Product Tactical Trades GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Central Banks Backed Into A Corner

Central Banks Backed Into A Corner

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

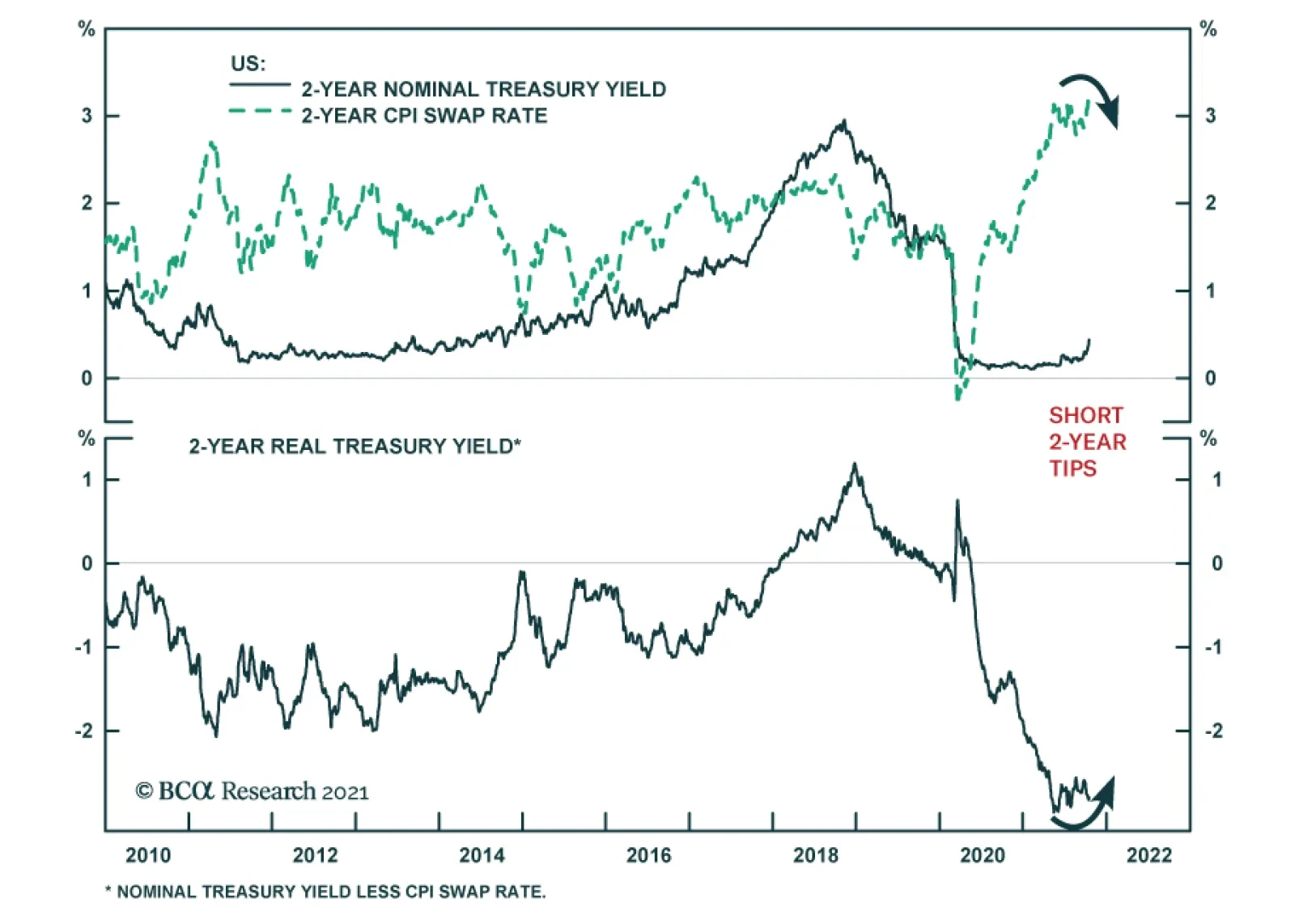

BCA Research’s US Bond Strategy service concludes that investors should position for higher short-maturity real yields. The market’s near-term rate expectations have risen considerably during the past few weeks. While our colleagues think that pricing looks…

Highlights Duration: We recommend that investors run below-benchmark portfolio duration in US bond portfolios on the expectation that the Treasury curve will bear-flatten between now and Fed liftoff in December 2022. Nominal Treasury Curve: We recommend positioning for curve flattening by going short the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. TIPS: Investors should position for higher short-maturity real yields. This can be done through an outright short position in 2-year TIPS, an inflation curve steepener or a real yield curve flattener. The Long And Short Of It Chart 1Short-End Joins The Selloff

Short-End Joins The Selloff

Short-End Joins The Selloff

It’s still a bit early for a 2021 retrospective, but unless something dramatic happens during the next 2 ½ months it’s likely that the year will go into the books as a bad one for US bonds. Looking back, we can identify three phases of bond market performance in 2021. First, a selloff in long-dated bonds early in the year driven by economic re-opening and fiscal stimulus. Second, a partial reversal of this long-end selloff that lasted through the spring and early summer. Finally, a renewed selloff involving both the long and short ends of the yield curve (Chart 1). The Long End Looking first at the long end of the curve, we don’t see any immediate signs that yields have risen too far. Estimates of the 10-year term premium created by taking the difference between the spot 10-year Treasury yield and survey estimates of the future 10-year average fed funds rate show that the term premium is not as elevated as it was when yields peaked last March or when they peaked in 2018 (Chart 2). The 25-delta risk reversal on 30-year Treasury futures – a technical indicator with a strong track record of calling turning points in the 30-year yield – also remains below the 1.5 level that has historically signaled a peak in the 30-year yield (Chart 3). Table 1 shows that while it is rare for the risk reversal to rise above 1.5, such a move usually indicates that yields have risen too far, too fast Chart 210-Year Term Premium Still Low

10-Year Term Premium Still Low

10-Year Term Premium Still Low

Chart 3Technicals Not Stretched

Technicals Not Stretched

Technicals Not Stretched

Table 1Track Record Of Risk Reversal Indicator

Right Price, Wrong Reason

Right Price, Wrong Reason

Finally, we look at the 5-year/5-year forward Treasury yield relative to a range of survey estimates of the long-run neutral fed funds rate (Chart 4). At 2.09%, the 5-year/5-year yield is close to median survey estimates of the long-run neutral fed funds rate.1 We take this to mean that the 5y5y yield has limited upside. Further increases in yields will take the form of the rest of the curve catching up to the 5y5y. Put differently, further increases in yields are more likely to coincide with curve flattening, not steepening.2 Chart 45y5y Is At Its Fair Value

5y5y Is At Its Fair Value

5y5y Is At Its Fair Value

The Short End While long-maturity bond yields have moved up during the past few months, it is the breakout in short-maturity Treasury yields that has been the most notable feature of the recent bond selloff (Chart 1, bottom panel). In particular, near-term interest rate expectations have adjusted sharply higher since the September FOMC meeting (Chart 5). Prior to the September FOMC meeting, the overnight index swap (OIS) market was priced for Fed liftoff in February 2023 and for a total of 80 bps of rate hikes by the end of 2023. Now, the OIS curve is priced for Fed liftoff in September 2022 and for a total of 113 bps of rate hikes by the end of 2023. Chart 5Fed Funds Rate Expectations

Fed Funds Rate Expectations

Fed Funds Rate Expectations

We continue to view the December 2022 FOMC meeting as the most likely date for the first rate hike. We also think it’s reasonable to expect the Fed to lift rates at a pace of 75-100 bps per year once tightening begins. In other words, we view fair pricing at the front-end of the curve as consistent with liftoff in December 2022 and a total of 100-125 bps of rate hikes by the end of 2023. The recent selloff has made front-end pricing more consistent with our assessment of fair value. Therefore, we don’t see any huge opportunities for directional bets on short-dated nominal yields. That said, we also contend that the bond market has arrived at the correct conclusion about the near-term pace of Fed tightening, but for the wrong reason. As is discussed in the next section of this report (see section titled “Massive Upside In Short-Maturity Real Yields”), this presents some attractive opportunities to trade short-maturity real yields and short-maturity inflation breakevens. One other observation from Chart 5 is that the market’s expected pace of Fed tightening flattens off considerably in 2024 and beyond. The market is priced for a mere 34 bps of tightening in 2024 and 2025 and the fed funds rate is still expected to be below 1.6% by the end of 2025. This highlights that, while pricing at the front-end of the yield curve looks reasonable, yields with slightly longer maturities remain too low. Bottom Line: We recommend that investors run below-benchmark portfolio duration in US bond portfolios on the expectation that the Treasury curve will bear-flatten between now and Fed liftoff in December 2022. We recommend positioning for curve flattening by going short the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. Massive Upside In Short-Maturity Real Yields Table 2Yield Changes Since September FOMC (BPs)

Right Price, Wrong Reason

Right Price, Wrong Reason

The prior section noted that the market’s near-term rate expectations have risen considerably during the past few weeks. While we think that pricing looks reasonable compared to our own monetary policy expectations, we alluded to the idea that the market has brought forward its rate hike expectations for the wrong reason. Table 2 illustrates what we mean. Practically all the increase in nominal Treasury yields since the September FOMC meeting has been driven by a rising cost of inflation compensation. Real yields, on the other hand, have either been relatively stable (for long maturities) or have fallen massively (at the short-end of the curve). In fact, the 2-year real yield has declined 34 bps since the September FOMC meeting even as the 2-year nominal yield has increased by 16 bps. What the stark divergence between real yields and the cost of inflation compensation tells us is that the market is concerned that inflation may not fall as much as was previously assumed and the Fed may be forced to tighten more quickly in response. First off, we think concerns about persistently high inflation are a tad overblown. It’s certainly true that 12-month headline and core CPI inflation remain extremely high, at 5.4% and 4.0% respectively, but 3-month rates of change have moderated during the past few months and the 12-month figures will soon follow suit (Chart 6). Second, even if inflation is slow to moderate, the composition of what is driving that high inflation has implications for how the Fed will respond. Specifically, if elevated inflation continues to be driven by extreme readings from a few sectors that have been inordinately impacted by the pandemic, the Fed will be inclined to write-off that inflation as “transitory” while it awaits more broad-based inflationary pressures driven by tight labor markets and accelerating wages. It continues to be worth noting that after stripping out COVID-impacted services and cars, core inflation remains well contained near levels consistent with the Fed’s target (Chart 7). Chart 6Inflation Is Falling

Inflation Is Falling

Inflation Is Falling

Chart 7Inflation Pressures Are Narrow

Inflation Pressures Are Narrow

Inflation Pressures Are Narrow

In a speech last week, Atlanta Fed President Raphael Bostic said that the Fed should use the word “episodic” instead of “transitory” to describe the nature of the current inflationary shock.3 The problem with the word “transitory” is that it is linked to a notion of time. It implies that inflation pressures are expected to fade quickly, but this is not the message that the Fed meant to convey with that word. Rather, in Bostic’s words, the Fed meant to convey that “these price changes are tied specifically to the presence of the pandemic and, once the pandemic is behind us, will eventually unwind, by themselves, without necessarily threatening longer-run price stability.” In other words, the Fed will not tighten policy to lean against narrow inflationary pressures driven by a few sectors that can easily be traced back to the pandemic. Rather, the Fed will only respond if inflationary pressures are sufficiently broad and/or if long-run inflation expectations become un-anchored to the upside. On the first point, there is some evidence that inflation pressures are broadening. As of September, 49% of the CPI index was growing at a 12-month rate above 3%, up from a 2021 low of 22% (Chart 8). However, long-run inflation expectations remain well-anchored near the Fed’s target levels (Chart 9). Chart 8CPI Breadth Indicator

CPI Breadth Indicator

CPI Breadth Indicator

Chart 9Long-Term Inflation Expectations

Long-Term Inflation Expectations

Long-Term Inflation Expectations

Our sense is that inflationary pressures will fade during the next 12 months as pandemic fears abate. Long-dated inflation expectations will remain close to current levels, but short-dated inflation expectations will fall. The Fed will start to lift rates in December 2022 as broad-based inflationary pressures emerge, but inflation will be only slightly above the Fed’s target by then. The best way to position for this outcome is to go short 2-year TIPS. The cost of 2-year inflation compensation will fall as inflation moderates during the next 12 months, but the nominal 2-year yield will rise modestly as we advance toward a Fed tightening cycle. These two factors will combine to drive the 2-year real yield sharply higher (Chart 10). If you prefer not to put on an outright short 2-year TIPS position, there are a few other ways to position for the same trend. First, investors could position for a steeper inflation curve. Chart 11 shows that the cost of short-maturity inflation compensation is much further above the Fed’s target level than the cost of long-maturity inflation compensation. Further, Table 3 shows that monthly changes in the cost of short-maturity inflation compensation are more sensitive to CPI than are changes in the long-maturity cost of inflation compensation. This means that the inflation curve will steepen during the next 12 months as inflation moderates and the short-term cost of inflation compensation falls. Chart 10Short 2-Year TIPS

Short 2-Year TIPS

Short 2-Year TIPS

Chart 11Position For Inflation Curve Steepening...

Position For Inflation Curve Steepening...

Position For Inflation Curve Steepening...

Table 3Regression of Monthly Changes In CPI Swap Rate Versus Monthly Changes In 12-Month Headline CPI Inflation (2010 - Present)

Right Price, Wrong Reason

Right Price, Wrong Reason

Second, you could also position for a flatter TIPS yield curve (Chart 12). The combination of inflation curve steepening and nominal curve flattening will lead to a supercharged flattening of the real yield curve during the next 12 months. Chart 12... And Real Yield Curve Flattening

... And Real Yield Curve Flattening

... And Real Yield Curve Flattening

Bottom Line: Investors should position for higher short-maturity real yields. This can be done through an outright short position in 2-year TIPS, an inflation curve steepener or a real yield curve flattener. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 The median response from the New York Fed’s Survey of Market Participants pegs the long-run neutral fed funds rate at 2.0%. The same measure from the Survey of Primary Dealers sits at 2.25%. 2 For more details on the relationship between the proximity of the 5-year/5-year yield to its fair value range and the slope of the yield curve please see US Bond Strategy Weekly Report, “A Bump On The Road To Recovery”, dated July 27, 2021. 3 https://www.atlantafed.org/news/speeches/2021/10/12/bostic-the-current-inflation-episode.aspx Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

Dear Client, There will be no weekly report next week. Instead, we will host our quarterly webcast on Tuesday, October 26 for the US and EMEA regions and Wednesday, October 27 for the Asia Pacific region. We will resume our regular publishing schedule on Monday, November 1. In the meantime, we look forward to seeing many of you at our BCA Research Investment Conference this week. Best regards, Mathieu Savary Highlights This year’s decline in EUR/USD has rendered this pair sufficiently inexpensive and oversold to account for the near-term risks we highlighted in March. Nonetheless, some risks remain—among them, the continued credit slowdown in China, diverging monetary policy trends, and the energy crisis hurting Europe. However, long-term fundamentals continue to support the euro’s 12- to 18-month outlook. Moreover, Chinese credit growth may soon stabilize and markets already largely factor in the policy divergence between the Fed and the ECB. As a result, we buy the euro today with a preliminary target at 1.25 and a stop loss at 1.1175. The Bank of England will lift rates this December, but the market already prices in a hawkish BoE. GBP/USD has upside, even if the euro should outpace the pound in the coming months. Look to upgrade UK small-cap stocks. Italian equities do not appear particularly appealing on a cyclical horizon, neither in absolute nor relative terms. Investors should favor Spanish stocks over Italian ones for the next 12-to-18 months. Feature EUR/USD recently flirted with 1.15. Did this move create a buying opportunity? Last March, we warned that the euro would correct to the 1.12 to 1.15 zone because short-term models flagged it as expensive, speculators carried a substantial net-long exposure, and Chinese credit growth was set to slow meaningfully. These forces have now mostly played out; thus, the euro’s near-term outlook is becoming more positive. Despite this more constructive view, EUR/USD still carries ample downside risks, especially if Chinese authorities remain reluctant to reflate their economy. Moreover, the energy crisis facing Europe clouds the euro. We are nonetheless buyers of EUR/USD, with a target at 1.25. Investors should set a wide stop in at 1.1175. Cheap And Oversold The internal dynamics of the euro indicate that the bulk of the sell-off is behind us. First, the euro is now cheap on a tactical basis. Back in March, our short-term fair value model for EUR/USD flagged at 7% overvaluation based on real rate differentials, on the slope of the German yield curve relative to that of the US, and on the copper-to-lumber prices ratio. Today, this same measure shows a 5% undervaluation. BCA’s Foreign Exchange Strategy Intermediate Term Timing Model (ITTM) flags an even clearer buy signal. The ITTM framework combines interest rate parity models, with risk aversion and considerations for the currency’s trend. Currently, this model is at -8% or nearly minus one standard error. Historically, such a depressed reading points to generous returns in the subsequent 12 months (Chart 1). Second, the euro is oversold. BCA’s Intermediate Term Technical Indicator has hit 7, which is consistent with past rebounds in EUR/USD (Chart 2). While some of these rallies have been extremely short-lived, the technical indicator’s message is stronger when it is matched by a buy signal from the ITTM. Chart 1Strong Buy Signal From Short-Term Valuations

Strong Buy Signal From Short-Term Valuations

Strong Buy Signal From Short-Term Valuations

Chart 2EUR/USD is Oversold

EUR/USD is Oversold

EUR/USD is Oversold

Chart 3Stale Euro Longs Have Been Purged

Stale Euro Longs Have Been Purged

Stale Euro Longs Have Been Purged

Third, speculators do not carry a large net long position in the euro anymore. This variable suggests that the worst of the selling pressure is behind us, but it has yet to send a strong buy signal on its own (Chart 3). Bottom Line: The euro is sufficiently inexpensive that our Intermediate-term timing model flags a strong buy signal. Moreover, our technical indicators paint an oversold picture consistent with a reversal. Nonetheless, speculators may not be long EUR/USD anymore, but they are not aggressively selling it either. Thus, macro dynamics remain important to the future trend of this currency. Macro Fog Remains The macro environment is not yet conducive to a euro rally, especially when Chinese credit growth remains weak. However, considering the euro’s valuation and technical picture, small changes in the macro environment could be enough to catalyze a jump in EUR/USD. A key problem for the euro is that the dollar remains well bid. The yen and the dollar are the two momentum currencies within the G-10 (Chart 4). This property of the dollar is a large handicap for the euro, because it remains the most liquid vehicle to bet on the USD. Thus, as long as the dollar’s momentum is strong, the euro will find it difficult to rally. Relative economic growth is another headwind for EUR/USD. European activity is weakening versus that of the US. Since 2019, the relative manufacturing PMIs between the Euro Area and the US track EUR/USD, and they currently confirm the euro’s weakness (Chart 5). Moreover, European economic surprises are significantly weaker than US ones, which adds to the euro’s malaise (Chart 5, bottom panel). Chart 4The Dollar Is A Momentum Currency

Time For The Euro To Shine?

Time For The Euro To Shine?

Chart 5Deteriorating European Growth Hurts EUR/USD

Deteriorating European Growth Hurts EUR/USD

Deteriorating European Growth Hurts EUR/USD

The near-term outlook does not signal a resolution of this issue until the first half of 2022. The declines in the expectation and current situation components of both the ZEW and Sentix surveys herald an additional deceleration in manufacturing activity (Chart 6). The Eurozone’s growth problems reflect China’s slowing credit flows. Europe economic activity is still extremely sensitive to the evolution of the global industrial cycle (Chart 7, top panel), much more so than the US GDP is. China’s business cycle is an essential determinant of the robustness of the global manufacturing sector. Consequently, when measures of China’s marginal propensity to consume decelerate, such as the gap between M1 and M2 growth, European PMIs and industrial production underperform those of the US (Chart 7, second and bottom panels). Chart 6A Bit More Time Before Europe's Slowdown Ends

A Bit More Time Before Europe's Slowdown Ends

A Bit More Time Before Europe's Slowdown Ends

Chart 7China's Travails Hurt Europe

China's Travails Hurt Europe

China's Travails Hurt Europe

The fourth quarter of 2021 is likely to represent the tail end of the Chinese headwind on EUR/USD. The Chinese credit impulse remains weak, but signs of a floor are beginning to appear. For example, the decline in Chinese commercial banks excess reserve growth warned us of the coming decline in the credit impulse. Today, excess reserves have begun to stabilize, which points to an upcoming imporvement in credit flows (Chart 8). Additionally, the Evergrande problems continue to weigh on Europe in the near-term because of the deceleration in Chinese construction activity; however, the crisis will also intensify the pressure on Beijing to revive credit growth in order to avoid a systemic collapse. Chart 8Will China's Credit Impulse Bottom Soon?

Will China's Credit Impulse Bottom Soon?

Will China's Credit Impulse Bottom Soon?

Monetary policy differentials also remain euro bearish. The US Federal Reserve will announce the start of its tapering program on November 3. The FOMC is set to hike rates by the end of 2022. Meanwhile, the ECB is unphased by the increase in European inflation, which remains mostly a reflection of energy prices and base effects. Thus, Europe will lag behind the US when it comes to monetary policy tightening. Nonetheless, investors already understand this dichotomy very well. The US OIS curve anticipates four hikes in 2023. Meanwhile, the EONIA curve shows a first 25-bps hike only by September 2023. Thus, the euro will suffer more from policy differentials if the Fed generates hawkish surprises relative to this pricing. The energy crisis shaking Europe is the last major headwind currently affecting the euro. Historically, EUR/USD and the ratio of European to US natural gas prices track each other (Chart 9). This relationship reflects relative growth dynamics. A stronger Eurozone economy relative to the US pushes up the value of the euro and European natural gas, which is a commodity with heavy industrial usage. However, since this summer, the spike in European natural gas prices has coincided with a decline in the euro. This divergence highlights the negative effect on European activity of the current energy shock, which raises fears of stagflation. The cross-Atlantic bond market dynamics confirm the notion that the energy shock increases the perceived stagflation risk in the Eurozone. German yields have risen relative to US ones because of a pick-up in inflation expectations, not real rates (Chart 10). The lack of traction for relative real rates is appropriate because market participants believe that the ECB wants to ignore the spike in energy prices. An environment of rising relative inflation expectations but stable relative real rates is very negative for any currency, including the euro. However, European inflation expectations should decrease relative to those of the US once European natural gas prices normalize, which we expect to take place in the coming months (Chart 10, bottom panel). This process will be very positive for the euro. Chart 9The European Energy Crisis Harms The Euro

The European Energy Crisis Harms The Euro

The European Energy Crisis Harms The Euro

Chart 10Pricing In European Stagflation?

Pricing In European Stagflation?

Pricing In European Stagflation?

Bottom Line: While euro pricing and technicals suggest EUR/USD will bottom soon, the economic environment is murkier. The dollar is a momentum currency, and its current strength feeds the euro’s weakness. China’s credit flows continue to decelerate, which hurts the euro; however, credit flows may stabilize in early 2022. The Fed is a tailwind for the dollar, but markets already price in this reality. Finally, the energy crisis hurts European growth and thus EUR/USD; nonetheless, the spike in natural gas prices will soon give way to a period of decline, which will lessen the pain for the euro. What To Do? When we balance the positives and negative for the euro, we are becoming more comfortable with buying EUR/USD outright, even if it is still a risky bet. To begin with, the big fundamental forces point to a firmer euro on an 18- to 24-month basis: BCA’s Foreign Exchange strategists see greater cyclical downside for the USD and believe the current rebound is a pronounced countertrend move within a multi-year dollar bear market. The euro will naturally benefit over the coming years from a weak greenback. EUR/USD is still inexpensive on long-term valuation metrics. Based on BCA’s purchasing power parity model, this pair trades 17% below its fair value. Moreover, the PPP estimate keeps rising in favor of the euro, a result of the Eurozone’s lower inflation compared to the US (Chart 11). The relative balance of payments favors the euro. The European economy generates a current account surplus of 3% of GDP compared to a current account deficit of 3.1% for the US. The US current account deficit is unlikely to narrow, even if the federal government’s budget hole declines because the private sector’s savings rate is falling even faster. Moreover, US real two-year rates remain well below those of its trading partners. Investors underweight Eurozone assets aggressively. For the past ten years, capital has consistently flowed out of the Euro Area relative to the US (Chart 12). European growth should converge toward the US next year, especially if Chinese credit activity stabilizes. Therefore, 2022 should witness a period of inflows into the Eurozone. Chart 11EUR/USD Significant Long-Term Discount

EUR/USD Significant Long-Term Discount

EUR/USD Significant Long-Term Discount

Chart 12Investors Underweight Eurozone Assets

Investors Underweight Eurozone Assets

Investors Underweight Eurozone Assets

We argued that the valuation and technical backdrop shows the Euro is becoming increasingly supportive and our timing model is clearly arguing against selling EUR/USD. However, the biggest technical risk is the momentum sensitivity of the dollar, which means that the euro’s weakness could last somewhat longer. Nevertheless, BCA’s Dollar Capitulation Index now warns of a pullback in the USD, especially as speculators are very long DXY futures (Chart 13). The biggest downside risk remains China’s credit trend. If it takes more time than we anticipate for Beijing to put an end to the credit impulse slowdown, the euro will experience greater downside pressure. Moreover, the longer it takes Beijing to reflate, the greater the chance of an uncontrolled selloff in the CNY, which would drag down the euro (Chart 14). Chart 13Is The Dollar Technically Vulnerable?

Is The Dollar Technically Vulnerable?

Is The Dollar Technically Vulnerable?

Chart 14China Remains The Euro's Main Risk

China Remains The Euro's Main Risk

China Remains The Euro's Main Risk

Despite this level of near-term uncertainty, we recommend investors buy the euro, with a target at 1.25, and a stop loss at 1.1175. Bottom Line: Conditions are falling in place for the countertrend decline in the euro to end soon. As a result, the euro should converge back toward the upward path driven by fundamentals. The greatest near-term risk remains the path of Chinese credit trends. We recommend investors buy the euro with a preliminary target at EUR1.25 and a stop loss at 1.1175. Country Focus: A Well Discounted BoE Hike The Bank of England will begin to increase interest rates at its December meeting. The BoE’s communication has been clear that it does not see a need to wait between the end of its tapering program in December and the beginning of its hiking campaign. Recent comments by senior MPC members, including new Chief Economist Huw Pill, also suggest a rate hike is looming. Chart 15The BoE's Inflation Problem

The BoE's Inflation Problem

The BoE's Inflation Problem

We see little reason to doubt the willingness of the MPC to start lifting the Bank Rate. UK Core CPI stands at 3.1% or 110 basis points above the BoE’s inflation target. Moreover, both market-based and survey-based long-term inflation expectations are well above 3.5%, which increases the risk of a dangerous dis-anchoring of UK inflation (Chart 15). UK economic activity remains inflationary. Wages are strong, climbing 7.2% in August. This number probably exaggerates the underlying wage growth due to compositional effects, but job creation remains robust and the unemployment rate fell to 5.2%. The BoE was concerned that the end of the furlough scheme last month would cause a jump in unemployment, but their fears have dwindled, because job vacancies stand at a record high and capex intentions are solid (Chart 16). The housing market continues to be a tailwind to growth. House prices are up 10% annually, which lifts household net worth considerably (Chart 17). The pace of transactions in the real estate market will slow this spring because the stamp duty holiday will end; however, low mortgage rates and expectations of further housing gains may fuel greater appreciation. This creates long-term financial stability risks for the UK because household leverage will rise. This worries the BoE. Chart 16The UK's Labor Market Strength Will Continue

The UK's Labor Market Strength Will Continue

The UK's Labor Market Strength Will Continue

Chart 17Rising Household Net Worth

Rising Household Net Worth

Rising Household Net Worth

Market participants already expect a hawkish BoE. A rate hike is priced in for December and the SONIA curve embeds almost two more increases in 2022. The 4.3% underperformance of the UK government bond index over the global benchmark in seven weeks also underscores the rapid adjustment in investors’ perceptions of the UK policy path. BCA’s Global Fixed-Income strategists have underweighted UK government bonds for two months, and they maintain a negative view over the coming quarters. Nonetheless, the risk of a short-lived countertrend rebound in UK bonds’ relative performance is significant. However, it would be a temporary position squaring, while hedge funds and CTAs take profits. BCA’s Foreign Exchange strategists expect GBP/USD to rebound. Cable is oversold and trades at a 12% discount to BCA’s PPP fair-value estimate. GBP/USD is also hurt by fears that the BoE hikes will damage the UK economy. From a contrarian perspective, this creates a positive entry point to buy cable, especially because the pound should benefit from the anticipated dollar weakness and the euro’s upcoming rally. However, BCA’s FX strategists also foresee some decline in the pound versus the euro, because GBP is a low beta play on EUR/USD. Hence, the trade-weighted pound could remain flat to slightly down in the coming months. We stay neutral on UK small-cap stocks relative to large-cap equities, but we are putting them on an upgrade alert. Small-cap stocks benefit from the strength in the domestic economy; however, they are also extremely expensive compared to large-cap ones (Chart 18). The arbiter of performance will be profits. The forward EPS of small-caps have lagged behind those of large-caps by 9% since the COVID recession, after underperforming since 2016 (Chart 19). Small-caps’ relative profits are currently trying to stabilize, but the durability of this trend will be tested if the trade-weighted pound remains flat in the coming months. Thus, the EPS of small-cap shares must regain more ground before moving more aggressively in this market. Chart 18UK Small Cap Are Pricey

UK Small Cap Are Pricey

UK Small Cap Are Pricey

Chart 19Follow The Profits

Follow The Profits

Follow The Profits

Bottom Line: On the back of a strong UK economy and significant inflationary forces, the BoE will start elevating interest rates this December. The market already prices in this outcome. Nonetheless, UK bonds should continue to underperform the global benchmark, and cable has upside, even if the near-term outlook favors the EUR over the GBP. We are putting UK small-cap stocks on a buy alert. They are expensive, but a turnaround in profits would solve this problem. Market Focus: A Quick Take On Italian Equities The Italian equity market remains Europe’s problem child. The Italian MSCI index has underperformed the rest of the Euro Area by 40% since 2010. This underperformance holds even after adjusting for sectoral differences, although it becomes less dramatic (Chart 20, top panel). Despite this underperformance, Italian equities have managed to outperform their Spanish counterparts by 27% since 2010, but this outperformance dissipates once sectoral difference are accounted for (Chart 20, bottom panel). The RoE of Italian non-financial listed equities is equivalent to the rest of the Eurozone, but it only reflects elevated financial leverage, as is the case in Spain (Chart 21). Italy’s RoA is poor, because Italy’s excess capital stocks hurts its return on capital. As a result, Italian equities continue to face a structural handicap. Chart 20A Problem Child

A Problem Child

A Problem Child

Chart 21Italy's Return On Asset Is Poor

Italy's Return On Asset Is Poor

Italy's Return On Asset Is Poor

The good run in Italian equities in absolute terms faces headwinds. Italian stocks are very sensitive to the global business cycle; however, they often respond with a delay and in an exaggerated fashion to decelerations in the global PMI (Chart 22, top panel). Moreover, since 2010, widening European high-yield corporate bond spreads have preceded falling Italian stock prices. Thus, the recent slide in the global PMI and the widening in European high-yield OAS create a period of vulnerability for Italian equities. Finally, Italian share prices have overshot the path implied by US yields (Chart 22, bottom panel). Nonetheless, Italian stocks may be sniffing out further increases in global yields. The cleanest way to play these vulnerabilities in the Italian is via a short bet against Spain. A steeper global yield curve will help both markets due to their heavy exposure to financials. However, we still favor Spanish financials, which benefit from higher RoEs than their Italian counterparts (Chart 23) and lower NPLs. As a result, the forward EPS of Spanish financials should begin to outperform those of Italian financials. Chart 22Some Risks To Italian Stocks

Some Risks To Italian Stocks

Some Risks To Italian Stocks

Chart 23Spanish Banks Are Better Placed To Benefit From Rising Global Yields

Spanish Banks Are Better Placed To Benefit From Rising Global Yields

Spanish Banks Are Better Placed To Benefit From Rising Global Yields

Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Jeremie Peloso, Associate Editor JeremieP@bcaresearch.com Tactical Recommendations

Time For The Euro To Shine?

Time For The Euro To Shine?

Cyclical Recommendations

Time For The Euro To Shine?

Time For The Euro To Shine?

Structural Recommendations

Time For The Euro To Shine?

Time For The Euro To Shine?

Closed Trades

Time For The Euro To Shine?

Time For The Euro To Shine?

Currency Performance Fixed Income Performance Equity Performance

The Japanese yen has been performing poorly recently. It is the only G10 currency that has depreciated vis-à-vis the USD over the past week. Several factors explain the yen’s underperformance. First, after a period of strength in the run up to Prime…

Highlights As US and China’s grand strategies collide, expect major and minor geopolitical earthquakes whose epicenter will now lie in South Asia and the Indian Ocean basin. Another tectonic change will drive South Asia’s emergence as a new geopolitical battle ground - South Asia is now heavily weaponized. All key players operating in this theater are nuclear powers. South Asia’s democratic traditions are well-known but notable institutional and social fault lines exist. These could trigger major geopolitical events in Afghanistan, Pakistan and in pockets of India too. We are bullish on India strategically but bearish tactically. Dangerous transitions are underway to India’s east and west. Within India, key elections are approaching, and it is possible that growth may disappoint. For reasons of geopolitics, we are strategically bullish on Bangladesh but strategically bearish on Pakistan and Sri Lanka. We are booking gains of 9% on our long rare earths basket and 1% on our long GBP-CZK trade. Feature Over the 1900s, East Asia and the Middle East emerged as two key geopolitical focal points on the world map. Global hegemons flexed their muscles and clashed in these two theaters. Meanwhile South Asia was a geopolitical backstage at best. The majority of South Asia was a British colony until the second half of the twentieth century. After WWII it struggled with the difficulties of independence and mostly missed out on the prosperity of East Asia and the Pacific. But will the twenty-first century be any different? Absolutely so. We expect the current century to be marked by major and minor geopolitical earthquakes in which South Asia and the Indian Ocean basin will play a major part. This seismic change is likely to be the result of several tectonic forces: Population: A quarter of the world’s people live in South Asia today and this share will keep growing for the next four decades. India will be the most populous country in the world by 2027 and will account for about a fifth of global population. Supply: China’s growth model has left it heavily dependent on imports of raw materials from abroad. It is clashing with the West over markets and supply chains. Beijing is building supply lines overland while developing a navy to try to secure its maritime interests. These interests increasingly overlap with India’s, creating economic competition and security concerns over vital sea lines of communication. Access: Whilst the Himalayas and Tibetan plateau have historically prevented China from expanding its influence in South Asia, China’s alliance with Pakistan is strengthening. Physical channels like the China Pakistan Economic Corridor (CPEC), and other linkages under the Belt and Road Initiative, now provide China a foot in the South Asian door like never before (Map 1). Weapons: The second half of the twentieth century saw China, India, and Pakistan acquire nuclear arms. Consequently, South Asia today is one of the most weaponized geographies globally (Map 1). Map 1South Asia To Emerge As A Key Geopolitical Theater In The 21st Century

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

With the South Asian economy ever developing, and US-China confrontation here to stay, we expect China to make its presence felt in South Asia over the coming decades. The US’s recent withdrawal from Afghanistan, and the failure of democratization in Myanmar, are but two symptoms of a grand strategic change by which China seeks to prevent US encirclement and Indo-American cooperation develops to counter China. Throw in the abiding interests of all these powers in the Middle East and it becomes clear that South Asia and the Indian Ocean basin writ large will become increasingly important over the coming decades. The Lay Of The Land - India Is The Center Of Gravity Chart 1South Asia Managed Rare Feat Of ‘Steady’ Growth

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

South Asia stands out amongst developing regions of the world for its large and young population. In recent decades, South Asia has also managed to grow its economy steadily, surpassing Sub-Saharan Africa and rivaling the Middle East (Chart 1). While South Asia’s growth rates have not been as miraculous as East Asia post World War II, its growth engine has managed to hum slowly but surely. India and Bangladesh have been the star performers on the economic growth front (Chart 2). Despite decent growth rates, the South Asian region is characterized by very low per capita incomes due to large population. On per capita incomes, Sri Lanka leads whilst Pakistan finds itself at the other end of the spectrum (Chart 3). Chart 2India And Bangladesh Have Been Star Performers

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 3Per Capita Incomes In South Asia Have Grown, But Remain Low

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 4India Accounts For About 80% Of South Asia’s GDP

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

South Asia constitutes eight nations. However only four are material from an investment perspective: India, Pakistan, Sri Lanka, and Bangladesh. India is the center of gravity as it offers the most liquid scrips and accounts for 80% of the region’s GDP (Chart 4). In addition: India accounts for 101 of the 110 companies from South Asia listed on MSCI’s equity indices. MSCI India’s market capitalization is about $1 trillion. In fact, India’s equity market could soon become larger than that of the UK and join the world’s top-five club.1 The combined market cap of MSCI Bangladesh, Sri Lanka, and Pakistan amounts to only about $6 billion. Liquidity is a constraint that investors must contend with whilst investing in these three countries in South Asia. Pakistan is the home of 220 million – set to grow to 300 million by 2040. It lags its neighbors on economic growth and governance but has nuclear weapons and a 650,000-strong military. Bottom Line: India is the center of gravity for the regional economy and financial markets in South Asia. Sri Lanka and Bangladesh are small but are developing. Pakistan is the laggard, but is militarily strong, which raises political and geopolitical risks. South Asia: Major Consumer, Minor Producer Chart 5Manufacturing Capabilities Of South Asian Economies Are Weak

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

South Asia’s defining economic characteristic is that it is a major consumer. This feature contrasts with the region’s East Asian cousins, which worked up economic miracles based on their manufacturing capabilities. South Asia’s appetite to consume is partly driven by population and partly driven by the fact that this region’s economies have an unusually underdeveloped manufacturing base (Chart 5). It’s no surprise that all countries in South Asia (with the sole exception of Afghanistan) are set to have a current account deficit over the next five years (Charts 6A and 6B). Chart 6ASouth Asian Economies Tend To Be Net Importers

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 6BSouth Asian Economies Tend To Be Net Importers

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

India is set to become the third largest global importer of goods and services (after the US and UK) over the next five years. Its rise as a large client state of the world will be both a blessing and a curse, as increased business leverage will coincide with geopolitical insecurity. Structurally, Sino-Indian tensions are rising and growing bilateral trade will not be enough to prevent them. Meanwhile dependency on the volatile Middle East is a geopolitical vulnerability. Either way, India and its region become more important to the rest of the world over time. Whilst the structure of South Asia’s economy is relatively rudimentary, it is worth noting that Bangladesh and Sri Lanka present an exception. Bangladesh has embarked on a path of manufacturing-oriented development via labor-intensive production. Sri Lanka has a well-developed services sector (Chart 7). In particular: Bangladesh: Within South Asia, Bangladesh’s manufacturing sector stands out as being better developed than regional peers. More than 95% of Bangladesh’s exports are manufactured goods –a level that is comparable to China (Chart 8). China’s share in the global apparel and footwear market has been systematically declining and Bangladesh is one of the countries that has benefited most from this shift. Bangladesh’s share in global apparel and footwear exports to the US as well as EU has been rising steadily and today stands at 4.5% and 13% respectively.2 Chart 7Bangladesh’s And Sri Lanka’s Economies Are Relatively Modern

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 8Bangladesh Has The Most Developed Exports Franchise In South Asia

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Sri Lanka: Whilst Sri Lanka social complexities are lower and per capita incomes are higher as compared to peers in South Asia, its transition from a long civil war to a focus on economic development recently suffered a body blow, first owing to terrorist attacks in 2019 and then owing to the pandemic. The economic predicament was then worsened by its government’s hasty transition to organic farming which hit domestic food production. Geopolitically it is worth noting that China is one of the largest lenders to Sri Lanka. Whilst Sri Lanka’s central bank may be able to convince markets of the nation’s ability to meet debt obligations for now, its foreign exchange reserves position remains precarious and public debt levels remain high. Sri Lanka’s vulnerable finances are likely to only increase Sri Lanka’s reliance on capital-rich China. Despite Democracy, South Asia Has Political Tinderboxes Another factor that sets South Asia apart from developing regions like Africa, the Middle East, and Central Asia is the region’s democratic moorings. India and Sri Lanka lead the region on this front, although the last decade may have seen minor setbacks to the quality of democracy in both countries (Chart 9). Pockets of South Asia are socially and politically unstable, characterized by religious or communal strife, terrorist activity, and even the occasional coup d'état. Risk Of Social Conflict Most Elevated In Pakistan And Afghanistan India’s demographic dividend is real, but its benefits should not be overstated. For instance, India’s northern region is a demographic tinderbox. It is younger than the rest of the country, yet per capita incomes are lower, youth underemployment is higher, and society is more heterogeneous. The rise of nationalism in India is an important consequence and could engender potential social unrest. Chart 9India’s Democracy Strongest, But May Have Had Some Setbacks

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 10South Asia Is Young And Will Age Slowly

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 11Social Complexities Are High In Afghanistan & Pakistan

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

A similar problem confronts South Asia as a whole. Pakistan and Afghanistan are younger than India by a wide margin (Chart 10). But both countries are economically backward and have either poor or non-existent democratic traditions. Lots of poor youths and inadequate political valves to release social tensions make for an explosive combination. These countries are highly vulnerable to social conflict that could cause political instability at home or across the region via terrorism (Chart 11). The Gatsby Effect Most Prominent In Pakistan While various regions struggle with inequality, South Asia has less of a problem that way (Chart 12). However South Asia is characterized by very low levels of social mobility as compared to peer regions. This can partially be attributed to two centuries of colonial rule as well as to endemic traditions of social stratification. Chart 12Gatsby Effect: Social Mobility Is Lowest In Pakistan

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Within South Asia it is worth noting that social mobility is the lowest in Pakistan and highest in Sri Lanka. Chart 13Military’s Influence Most Elevated In Pakistan And Nepal Too

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Military Influential In Pakistan (And Nepal) Events that transpired over January 2020 in the US showed that even the oldest constitutional democracy in the world is not immune to a breakdown of civil-military relations. South Asia has seen the occasional coup d'état, one reason for the political tinderboxes highlighted above. Obviously, Myanmar is the worst – it saw its nascent democratization snuffed out just last year. But other countries in the region could also struggle to maintain civilian order in the coming decades. The military’s influence is outsized in Pakistan as well as Nepal (Chart 13). India maintains high levels of defense spending but has a strong tradition of civilian control (Chart 14). Chart 14Pakistan’s Military Budget Is Most Generous, India A Close Second

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

South Asia: A New Global Battle Ground Historically global hegemons have sought to assert their dominance by staking claim over coastal regions in Europe and Asia. Over the past two centuries Asia has emerged as a geopolitical theater second only to Europe. Naval and coastal conflicts have emerged from the rise of Japan (the Russo-Japanese War) and the Cold War (the Korean War & the Vietnam War). Today the rise of China is the destabilizing factor. The “frozen conflicts” of the Cold War are thawing in Taiwan, South Korea, and elsewhere. China is pursuing territorial disputes around its entire periphery, including notably in the East and South China Seas but also South Asia. Meanwhile the US, fearful of China, is struggling to strike a deal with Iran and shift its focus from the Middle East to reviving its Pacific strategic presence. A budding US-China competition is creating conditions for a new cold war or a series of “proxy battles” in Asia. Over the next few decades, we expect disputes to continue. But the focal points are likely to cover South Asia too. In specific, landlocked regions in South Asia are likely to see rising tensions in the twenty-first century (Map 2). Also as mentioned above, China’s naval expansion and the US’s attempt to form a “quadrilateral” alliance with India, Japan, and Australia will generate tensions and potentially conflict. European allies are also becoming more active in Asia as a result of US alliances as well as owing to Europe’s independent need for secure supply lines. Map 2China’s Interest In Landlocked Regions Of South Asia Is Rising

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

While border clashes between India and China will ebb and flow, Indo-Chinese confrontations along India’s eastern border will become a structural theme. Arguably, Sino-Indian rivalries pre-date the twenty-first century. But in a world in which the Asian giants are increasingly economically and technologically developed, Sino-Indian confrontations are likely to persist and result in major geopolitical events. Consider: China is adopting nationalism and an assertive foreign policy to cope with rising socioeconomic pressures on the Communist Party as potential GDP growth slows. China is developing a navy as well as a stronger alliance with Pakistan, which includes greater lines of communication. North India is a key constituency for the political party in power in India today (i.e., the Bhartiya Janata Party or BJP) and this geography harbors especially unfavorable views of Pakistan (Chart 15). Thus, there is a risk that the India of today could respond far more decisively or aggressively to threats or even minor disputes. More broadly, nationalism is rising in India as well as China. India is shedding its historical stance of neutrality and aligning with the US, which fuels China’s distrust (Chart 16). Chart 15Northern India Views Pakistan Even More Unfavorably Than Rest Of India

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 16India Has Aligned With The QUAD To Counter The Sino-Pak Alliance

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Turning attention to India’s western border, clashes between India and Pakistan relating to landlocked areas in Kashmir will also be a recurring theme. Whilst India currently has a ceasefire agreement in place with Pakistan, peace between the two countries cannot possibly be expected to last. This is mainly because: Kashmir: Core problems between the two countries, like India’s control over Kashmir and Pakistan’s use of militant proxies, remain unaddressed. India’s unexpected decision in 2019 to abrogate article 370 of the Indian constitution has reinforced Pakistan’s attention on Kashmir. Sino-Pak Alliance: Pakistan accounted for 38% of China’s arms exports over 2016-20. Pakistan accounts for the lion’s share of Chinese investments made in South Asia (Chart 17). Sino-India rivalries will spill into the Indo-Pak relationship (and vice versa). Revival Of Taliban: The US withdrawal from Afghanistan has revived Taliban rule in that country. Taliban’s rise will resuscitate a range of dormant terrorist movements in Afghanistan as well as in Pakistan. India has a long history of being targeted. South Asia today is very different from what it looked like for most of the post-WWII era: it is heavily weaponized. India, Pakistan, and China became nuclear powers in the second half of the twentieth century and have been steadily building their nuclear stockpiles ever since (Chart 18). North Korea’s growing arsenal is theoretically able to target India, while Iran (more friendly toward India) may also obtain nuclear weapons. Chart 17China And Pakistan: Joined At The Hip?

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Chart 18South Asia: The New Epicenter For Nuclear Activity

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

While nuclear arms create a powerful incentive for nations to avoid total war, they can also create unmitigated fear and uncertainty during incidents of major strategic tension. This is especially true when countries have not yet worked out a mode of living with each other, as with the US and USSR in the early days of the Cold War. Investment Takeaways For investors with an investment horizon exceeding 12 months, we highlight that India presents a long-term buying opportunity for two key reasons: China’s Internal And External Troubles Will Benefit India: As long as US and China do not reengage in a major way, global corporations will fall under pressure to diversify from China and the US will pursue closer relations with India. China faces an array of challenges across its periphery, whereas India need only focus on the South Asian sphere. India Is Rising As A Global Consumer: As long as a major Middle East war and oil shock is avoided (not a negligible risk), India should see more benefits than costs from its growing importance as a client of the world. However, over the next 12 months we worry that India is priced for perfection. India currently trades at a punchy premium relative to emerging markets (Table 1) at a time of when both geopolitical and macroeconomic headwinds are at play. In particular: Table 1We Are Bearish On India Tactically, But Bullish On India & Bangladesh Strategically

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Major Transitions Are Dangerous: Recent developments in South Asia have added to geopolitical risks for India. The assumption of power by Taliban in Afghanistan will activate latent terrorist forces that could target India. Pakistan’s chronic instability combined with the change of power in Afghanistan could set off an escalation in Indo-Pakistani tensions, sooner rather than later. On India’s eastern front, China’s need to distract its population from a souring economy could trigger a clash between China and India. Down south, China’s rising influence over crisis-hit Sri Lanka is notable and could potentially engender security risks for India. Chart 19Politics Can Trump Economics In Run Up To General Elections

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Growth Slowing, Elections Approaching: We worry that India’s growth engine may throw up a downside surprise over the next 12 months owing to poor jobs growth and poor investment growth. History suggests that politics often trumps economics in the run up to general elections (Chart 19). Hence there is a real risk that policy decisions will be voter-friendly but not market-friendly over 2022. As both India and Pakistan are gearing up for elections in the coming years, major military showdown or saber rattling should not be ruled out. Both countries may engineer a rally around the flag effect to bump up their pandemic-battered approval. Tension with China may escalate as Xi Jinping extends his term in power next year and seeks to enforce red lines in China’s eastern and western borders. Globally what are the key geopolitical factors that could lead to India’s underperformance in the short run? We highlight a checklist here: China Stimulates: The near-term clash between markets and policymakers in China should eventually give way to meaningful fiscal stimulus by Chinese authorities. This buoys China as well as emerging markets that depend on China for their growth. However, even if China flounders, India may not continue to outperform. The correlation between MSCI India and China equities has been positive. Fed Tightens Quickly: A faster-than-expected taper and tightening guidance could cause those emerging markets that are richly priced like India to correct. A Crisis Over Iran’s Nuclear Program: If the US is unable to return to diplomacy, tensions in the Middle East will rise and stoke oil prices. This will affect India adversely, given global price pressures and India’s high dependence on oil imports. Conversely, if these developments fail to materialize then that would lower our conviction regarding India’s underperformance in the short run. In summary, we are bullish India strategically but bearish tactically. As regards the three other investable markets in South Asia: We are bearish on Pakistan and Sri Lanka on a strategic time horizon. Whilst both nations’ rising alignment with China could be an advantage ceteris paribus, ironically their deteriorating finances are driving their proximity to capital-rich China (Chart 20). To boot, Sri Lanka’s ability to pay its way out of its economic crisis on its own steam is worsening. This is evident from its rising debt to GDP ratio (Chart 21). Chart 20Pakistan And Sri Lanka Running Low On Reserves

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

Pakistan faces elevated risks of internal social conflict, must deal with a rapidly changing external environment, has a weak democracy and an unusually influential military. Sri Lanka’s social risks are low, but its economic crisis appears likely to persist. The fact that both markets have been characterized by a high degree of volatility in earnings in the recent past implies that even a cyclical “Buy” case for either of these markets is fraught with risks (Table 1). The outlook for Bangladesh is better. Exports account for 15% of GDP and the US and Europe account for around 70% of its exports. Strong fiscal stimulus in these developed markets should augur well for this frontier market. Additionally, Bangladesh is characterized by moderate social risks, reasonably strong democracy scores and low levels of influence from the military. Its healthy public finances (Chart 21) and the fact that it shares no border with China creates the potential to leverage a symbiotic relationship with China. Chart 21Sri Lanka’s Debt Now Exceeds Its GDP

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

But there is a catch. Bangladesh as a market has a low market cap and hence offers low levels of liquidity (Table 1). We thus urge investors to avoid making cyclical investment calls on this South Asian market. However, from a long-term perspective we highlight our strategic bullish view on Bangladesh given supportive geopolitical factors. Watch out for an upcoming report from our Emerging Markets Strategy team, that will delve into the macroeconomic aspects of Bangladesh. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Footnotes 1 Abhishek Vishnoi and Swetha Gopinath, "India's stock market on track to overtake UK in terms of m-cap: Report" Business Standard, October 2021. 2 Arianna Rossi, Christian Viegelahn, and David Williams, "The post-COVID-19 garment industry in Asia" Research Brief, International Labour Organization, July 2021. Open Trades & Positions

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

South Asia: A New Geopolitical Theater

BCA Research’s Global Fixed Income Strategy service initiated a new tactical trade to position for more persistent ECB dovishness and a more hawkish Fed. The team continues to see no reason for the ECB to follow the Fed’s path towards imminent tapering and…

Highlights As US inflation proves to be not-so-transitory, US interest rate expectations will rise. Slowing Chinese domestic demand and rising US interest rate expectations will support the US dollar. The net impact from China’s slowdown and higher US interest rate expectations on mainstream EM will be currency depreciation. Rising mainstream EM nominal and real (inflation-adjusted) interest rates do not often lead to domestic currency appreciation A strengthening dollar vis-à-vis EM currencies is bad news for EM fixed-income markets – both local currency bonds and credit markets. Feature This report discusses EM local currency (domestic) bonds and US dollar bonds (credit markets). To begin with, we reiterate our main macro themes since January this year: (1) a slowdown in China and (2) rising US inflationary pressures and higher US bond yields. These macro themes will create tailwinds for the US dollar, at least for the next several months. A strengthening dollar is bad news for EM fixed-income markets. China’s Slowdown China’s slowdown will continue to unfold. China’s credit (TSF1 excluding equity) growth has slowed further in September (Chart 1, top panel). Similarly, household mortgages are also decelerating sharply (Chart 1, bottom panel). Chart 1China's Money And Credit Are Decelerating

China's Money And Credit Are Decelerating

China's Money And Credit Are Decelerating

Chart 2Curtailed Financing For Property Developers = Less Construction Activity

Curtailed Financing For Property Developers = Less Construction Activity

Curtailed Financing For Property Developers = Less Construction Activity

China's ever-important property market and construction activity will contract in the months ahead. Property sales were down by 20% in September from a year ago. Property developers in recent years have been relying on pre-construction sales as a major source of financing. With pre-sales drying up and borrowing restrained by both government regulations and creditors’ unwillingness to lend, property developers will be unable to sustain the current pace of construction and completion (Chart 2). Chart 3Red Flags For EM ex-TMT Stocks

Red Flags For EM ex-TMT Stocks

Red Flags For EM ex-TMT Stocks