Fixed Income

According to BCA Research’s China Investment Strategy service, the Chinese yield curve will likely flatten with long-term government bond yields dropping more than short-term rates in next six to nine months. The long-end of the yield curve will likely…

Dear Client, Owing to BCA’s Annual Investment Conference next week, there will be no report on Wednesday, October 20. We will return to our regular publication schedule on Wednesday, October 27. Please note that there will be a China Outlook panel discussion at 9 AM on Thursday, October 21. We hope you will join us for the event. Best regards, Jing Sima China Strategist Highlights In the next six to nine months, the long-end of the yield curve will likely drop as investors start to price in weaker-than-expected economic growth amid measured stimulus. China’s 10-year government bond yields are set to structurally shift to a lower bound as domestic demand decelerates along with the nation’s total population. Policymakers will favor lower borrowing costs to reduce stress due to high debt levels among companies, central and local governments, and households. National savings are not a constraint for a country to lower domestic bond yields. China will continue to open domestic financial markets to global investors. The country’s large foreign exchange reserves limit the risk to its internal markets from extreme volatility in foreign fund flows. Feature In the past two decades policy rates in advanced economies have been brought close to zero and bond yields have dropped to extremely low levels. The yields on China’s government bonds, however, have remained well above their peers in advanced economies and in neighboring countries (Chart 1). Chart 1China's Government Bond Yields Far Above Other Major Economies

China's Government Bond Yields Far Above Other Major Economies

China's Government Bond Yields Far Above Other Major Economies

Moreover, despite China’s growth slowing from double to mid-single digits, yields on China’s 10-year government bonds have remained at around 2006 levels. China’s working-age population continues to decline and its total population is estimated to start falling in the next five years. China’s demographic headwinds, combined with high leverage in the private sector at around 220% of GDP, will cap the upside in yields. In this report we share our views on China’s short rates and long-term bond yields on a cyclical basis (next six to nine months) and in the next five years. The Cyclical Outlook The yield curve will likely flatten with China’s long-term government bond yields dropping more than short-term rates in next six to nine months. This will occur in the expectation of a further growth slowdown in at least the next two quarters. Meanwhile, the downside is limited on the short-end of the curve, given it is more sensitive to the PBoC’s guidance and monetary authorities will ease policy only gradually. Stimulus in the next two quarters may also disappoint. Credit growth will bottom in Q4 this year, but the rebound will be modest. Stronger issuance in local government bonds in the next two quarters will be offset by sluggish bank loan impulse. Chinese policymakers will refrain from using stimulus for the property market as a counter-cyclical policy tool to revive the economy. Restrictions will be maintained on bank lending to the real estate sector including mortgages and these controls will limit the rebound in credit expansion. Furthermore, infrastructure investment will improve modestly in the next two quarters, but local governments remain under pressure to deleverage, which will limit their incentive and capacity to spend. Chart 2Stimulus In 2018/19 Was Very Measured

Stimulus In 2018/19 Was Very Measured

Stimulus In 2018/19 Was Very Measured

We maintain our view that the current policy backdrop is shaping up to resemble that of H2 2018 and 2019. At that time, even though the central bank maintained an accommodative monetary policy stance and kept liquidity conditions ample, the size of the stimulus was measured and the economy was lackluster (Chart 2). Recent liquidity injections by the PBoC through open market operations should not be viewed as monetary easing because they represent the bank’s efforts to keep policy rates steady, at best (Chart 3). The central bank provided the interbank system with substantial financing to avoid liquidity crunches following the May 2019 Baoshang Bank takeover and the November 2020 Yongcheng Coal company debt default (Chart 4). In both cases, 10-year bond yields did not fall by as much as short rates, reflecting investors’ expectations that the liquidity injections and resulting drop in short rates were not long-lasting. Chart 3Recent PBoC Liquidity Injections Intended To Keep Policy Rates Steady

Recent PBoC Liquidity Injections Intended To Keep Policy Rates Steady

Recent PBoC Liquidity Injections Intended To Keep Policy Rates Steady

Chart 4APBoC Also Injected Liquidity After Previous High-Profile Defaults

PBoC Also Injected Liquidity After Previous High-Profile Defaults

PBoC Also Injected Liquidity After Previous High-Profile Defaults

Chart 4BPBoC Also Injected Liquidity After Previous High-Profile Defaults

PBoC Also Injected Liquidity After Previous High-Profile Defaults

PBoC Also Injected Liquidity After Previous High-Profile Defaults

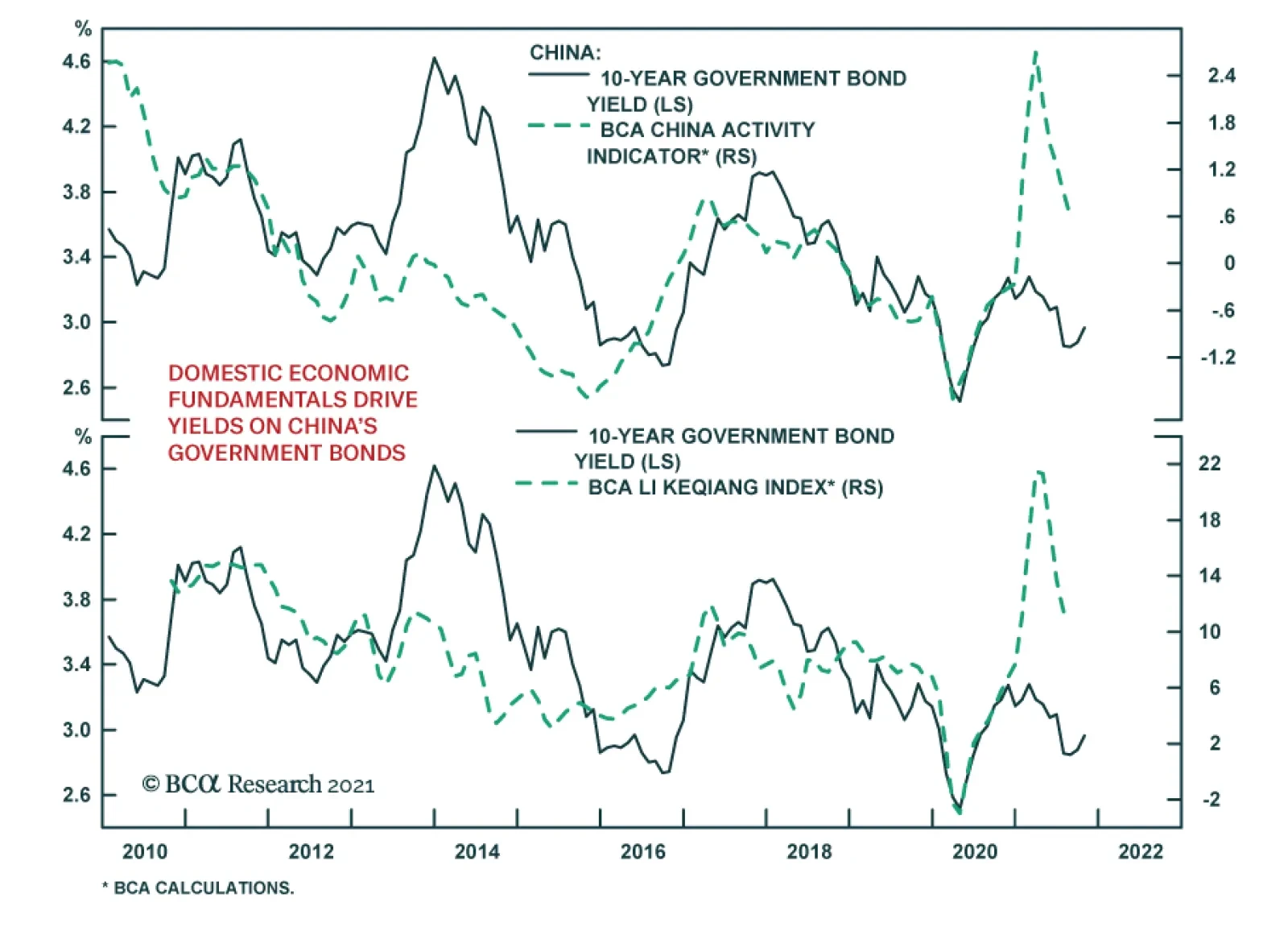

Our view on China’s bond yields will not change with the liftoff of US Fed policy rates, even if the Fed hikes rates earlier and by more than anticipated. The Fed’s policy has little bearing on China’s long-dated yields, which are driven by domestic business cycles and monetary policy (Chart 5). Concerning the exchange rate, we believe that the RMB will modestly depreciate in the next six to nine months, given that the China-US nominal and real interest rate differentials will narrow (Chart 6). While some depreciation in the currency is modestly reflationary for China’s exporters, it will not be enough to offset weaknesses in domestic demand. Chart 5Domestic Economic Fundamentals Drive Yields On China's Government Bonds

Domestic Economic Fundamentals Drive Yields On China's Government Bonds

Domestic Economic Fundamentals Drive Yields On China's Government Bonds

Chart 6China-US Rate Differentials Are Set To Narrow

China-US Rate Differentials Are Set To Narrow

China-US Rate Differentials Are Set To Narrow

Chart 7Pipeline Inflationary Pressures in China Remain Elevated

Pipeline Inflationary Pressures in China Remain Elevated

Pipeline Inflationary Pressures in China Remain Elevated

Inflation remains a risk to our cyclical view on the 10-year bond yield. While the economy is weakening, pipeline inflationary pressures remain elevated (Chart 7). We do not foresee that the PBoC will change its modestly dovish policy stance because of inflationary pressures stemming from supply-side bottlenecks. However, supply constraints will not abate soon and consequently, pipeline inflationary pressures and producer price inflation may not subside in the next six months. Thus, fixed-income investors may start to price in higher inflation, which could prevent long-duration bond yields from declining by much. Bottom Line: In the coming months, the long-end of the yield curve will likely drop as investors start to price in weaker-than-expected economic growth and very measured stimulus. The short-end of the curve will have limited downside potential because there is only a slim chance of aggressive monetary easing. Bond Yields Are On A Structural Downtrend Bond yields in China will likely downshift in the next three to five years. Our secular outlook for government bond yields is based on the country’s demographic trends, inflation, productivity growth and debt levels. While China’s long-term bond yields have persistently averaged below nominal GDP growth, in the past decade the gap has significantly narrowed as economic growth slowed while yields remained within a tight range (Chart 8). This contrasts with other manufacturing and export-oriented Asian economies where interest rates have moved to a lower range in proportion with economic growth rates (Chart 9). Chart 8China's Economic Growth Has Downshifted But Yields Have Not...

China's Economic Growth Has Downshifted But Yields Have Not...

China's Economic Growth Has Downshifted But Yields Have Not...

Chart 9...In Contrast With Other Asian Manufacturing-Based Economies

...In Contrast With Other Asian Manufacturing-Based Economies

...In Contrast With Other Asian Manufacturing-Based Economies

China’s long-dated bond yields will also downshift in the next three to five years given the nation’s declining long-term potential output growth, based on the following: Chart 10Wages Have Risen In China

Wages Have Risen In China

Wages Have Risen In China

A shrinking workforce can be inflationary due to higher labor costs and we expect Chinese workers’ compensation will continue to increase in the next five years (Chart 10). However, wage inflation will likely be offset by labor productivity, which has remained robust. The nation’s unit-labor cost (ULC), measured by the wages paid for each employee to produce one unit of output, has been flat to slightly down in the past decade despite strong wage growth (Chart 11). Similarly, ULC has sagged in Japan and is muted in South Korea (countries with shrinking labor forces) due to fast-growing labor productivity. This contrasts with the US, where ULC has risen even though the labor force has expanded in the past 10 years (Chart 12) China’s labor productivity will not likely undergo a significant decline in the next five years, particularly if China successfully maintains the manufacturing sector’s share in its aggregate economy, because productivity growth in this sector is usually higher than in others. Chart 11ULC Has Been Relatively Flat

ULC Has Been Relatively Flat

ULC Has Been Relatively Flat

Chart 12ULC Muted In Asian Economies Compared With US

ULC Muted In Asian Economies Compared With US

ULC Muted In Asian Economies Compared With US

Meanwhile, China’s total population will shrink within the next five years, which will likely bring powerful disinflationary forces that will more than offset price increases created by labor shortages. Disinflation will cap the upside in interest rates/bond yields. Chart 13Japan's Household Consumption Share Fell Sharply When Total Population Started Shrinking

Japan's Household Consumption Share Fell Sharply When Total Population Started Shrinking

Japan's Household Consumption Share Fell Sharply When Total Population Started Shrinking

A shrinking total population can significantly reduce demand, as evidenced in Japan in the past two decades. Japan’s working-age population started falling in the early 1990s, but the country’s household consumption share in GDP fell sharply after its total population peaked in 2010 and the urban population growth started contracting (Chart 13). In other words, Japan’s rapidly falling demand more than offset a muted increase in wage growth. China’s housing demand may have already peaked and the decline will gather speed in the next five years (Chart 14). Long-term growth in household consumption moves in tandem with housing and, therefore, will also downshift in the coming years (Chart 15). In the next five years or longer, China’s de-carbonization efforts will require shutting down production of many old economy enterprises. Policymakers may keep low interest rates to accommodate such a transformation. Furthermore, amid the geopolitical confrontation with the US, Beijing will need lower interest rates to support the manufacturing sector and to undertake an industrial upgrade. Chart 14China's Demand For Housing Is On A Structural Downshift...

China's Demand For Housing Is On A Structural Downshift...

China's Demand For Housing Is On A Structural Downshift...

Chart 15...Along With Consumption

...Along With Consumption

...Along With Consumption

The main risk to our view is that China’s total factor productivity1 growth could accelerate to more than offset a declining total population. This would boost real per capita income and result in higher potential growth in the economy. In this scenario, long-duration bond yields could climb. However, total factor productivity growth will need to outpace the rate of a shrinking labor pool and capital formation to prop up growth in the aggregate economy (Chart 16A and 16B). This is a daunting mission that Japan and South Korea, where productivity growth has been on par with China, have failed to accomplish. Chart 16AChina's Neighbors Have Not Accelerated Their Productivity Gains To Structurally Boost Economic Growth

China's Neighbors Have Not Accelerated Their Productivity Gains To Structurally Boost Economic Growth

China's Neighbors Have Not Accelerated Their Productivity Gains To Structurally Boost Economic Growth

Chart 16BChina's Neighbors Have Not Accelerated Their Productivity Gains To Structurally Boost Economic Growth

China's Neighbors Have Not Accelerated Their Productivity Gains To Structurally Boost Economic Growth

China's Neighbors Have Not Accelerated Their Productivity Gains To Structurally Boost Economic Growth

Chart 17China Cannot Drastically Improve Its Productivity Growth In The Next Five Years

China’s Interest Rates: Will They Join The Race To Zero?

China’s Interest Rates: Will They Join The Race To Zero?

It is unrealistic to expect that China will drastically improve its productivity growth. Productivity level is much higher now than it was 10-20 years ago when China’s manufacturing sector accounted for more than 40% of GDP (Chart 17). Even though China’s manufacturing share in the economy will stabilize and even increase from the current 27% of the economy, it cannot boost the sector drastically, particularly because its export market share cannot expand much further due to rising geopolitical tensions. In short, sectors of the economy where productivity gains have been most rapid – manufacturing sector including exports that drove China’s productivity in the past 20 years - cannot fully offset the deceleration in other growth drivers going forward. The service sector will grow, but it is much more difficult to achieve fast productivity gains in the service sector. All in all, productivity and economic growth will moderate as China’s growth model shifts from capital-intensive infrastructure and real estate to services. Bottom Line: In the next five years, China’s 10-year government bond yields are more likely to structurally move to a lower bound as final demand falls along with the nation’s total population. Savings, Debt And Interest Rates China’s national savings rate is one of the highest in the world, but it will drop as the population ages. Thus, some economists may argue that a structural decline in the national savings rate will lead to higher interest rates in the long run. Chart 18Lower Savings Rates Do Not Necessarily Herald Higher Interest Rates

Lower Savings Rates Do Not Necessarily Herald Higher Interest Rates

Lower Savings Rates Do Not Necessarily Herald Higher Interest Rates

However, there is no empirical evidence that national savings drive interest rates. There has not been an inverse relationship between national savings rates and government bond yields in either Japan or the US, as illustrated in the middle and bottom panels of Chart 18. There are more periods of positive rather than negative correlation between savings rates and bond yields. Note that China’s national savings rate and its interest rates also are not inversely related; a rising saving rate does not lead to lower interest rates and vice versa (Chart 18, top panel). This empirical evidence is in line with special reports published by BCA’s Emerging Markets Strategy that concluded the following: Banks cannot and do not lend out or intermediate national or households “savings.” In an economy with banks, one does not need to save in the form of a deposit in a bank in order for a bank to lend money to another entity. In any economy, new money originates by commercial banks “out of thin air” when they lend to or buy assets from non-banks. Hence, there is little relationship between national savings (flow concept in economics) and money supply growth (a flow variable too) (Chart 19). The term “savings” in macroeconomics denotes an increase in the economy’s capital stock, not deposits at banks. China’s banking system has an enormous amount of deposits, created by the banks “out of thin air” and not from households’ savings. The above factors explain why Japan’s government bond yields and national savings rate have been falling since 1990 (Chart 18 on Page 12, bottom panel). A lack of demand for borrowing was not why bond yields fell. A reason why China’s bond yields will likely be in a secular decline is that commercial banks will purchase government and corporate bonds en masse as they have done in the past 10 years (Chart 20). To do so, commercial banks will not use existing deposits, but rather they will create new deposits/money “out of thin air.” Chart 19There Is Little Relationship Between National Savings And Money Growth

There Is Little Relationship Between National Savings And Money Growth

There Is Little Relationship Between National Savings And Money Growth

Chart 20China's Commercial Banks Will Continue To Purchase Government And Corporate Bonds

China's Commercial Banks Will Continue To Purchase Government And Corporate Bonds

China's Commercial Banks Will Continue To Purchase Government And Corporate Bonds

The same is true for the banks’ purchases of corporate bonds. In China, commercial banks own about 75% of government (including local government) bonds and 20% of onshore corporate bonds. To avoid a spike in bond yields, Chinese regulators could relax the limitations on commercial banks to purchase government and corporate bonds. The upshot will be a lack of crowding out and no upward pressure on bond yields despite a large bond issuance. Chart 21China's Debt-To-GDP Ratio And Service Costs Have More Than Doubled In The Past 10 Years

China's Debt-To-GDP Ratio And Service Costs Have More Than Doubled In The Past 10 Years

China's Debt-To-GDP Ratio And Service Costs Have More Than Doubled In The Past 10 Years

What are the implications of high indebtedness on interest rates? China’s domestic debt-to-GDP ratio has jumped from 120% of GDP in 2008 to 260% (Chart 21, top panel). This includes local currency borrowing by/debt of government, enterprises and households. Critically, the debt-service ratio2 for enterprises and households has more than doubled from 10% of disposable income in 2008 to over 20% (Chart 21, bottom panel). China cannot afford much higher interest rates because enterprises and households will struggle and will not be able to service their debts. Mortgage rates in China are at around 5.5%, the one-year prime lending rate for companies is 3.85% and onshore corporate bond yields are 3.7%. These are not particularly low borrowing costs given both high indebtedness and the outlook for structurally slower economic growth. Onshore borrowing costs may be brought down further in the years ahead to rule out debt distress among households, enterprises and local governments. Since 2015 and prior to the pandemic, China’s debt-service ratio has been mostly flat despite a rising debt-to-GDP ratio.3 This has been achieved through declining interest rates. In the next five years policymakers will likely maintain a stable debt-to-GDP ratio. Hence, lower bond yields are all but inevitable to decrease the debt-servicing burden. In addition, China’s “common prosperity” policy means larger government spending/deficits. However, to cap the government debt-to-GDP ratio, bond yields should be kept down. This is another reason why China’s will opt for lower interest rates/bond yields. Bottom Line: The high level of debt among local governments, companies and households means that borrowing costs in China will be reduced in the years ahead. National savings are not a constraint in any country for commercial banks to expand credit and/or to buy bonds. China will encourage its banks to buy government and corporate bonds to trim yields amid continuous heavy bond issuance. Will China’s Financial Opening Continue? In the current environment which geopolitical tensions are rising between China and the West, many global investors are concerned whether China will impose tighter capital controls and even seize foreign assets. Despite these challenges, China has continued to make progress opening its domestic markets. The nation seems to be sticking to its key policy goals of attracting foreign capital and internationalizing the RMB; both aspects require open access and repatriation of foreign capital. In addition, the share of foreign holdings in onshore securities is very low and thus, poses limited risk to China’s onshore financial markets during global economic or geopolitical crises. China’s current exposure to foreign capital flows is much smaller than its Asian neighbors during the 1997 Asian Financial Crisis, as well as Russia during the geopolitical standoff in 2014-2016 following the capture of Crimea.4 Despite years of easing access to financial markets, foreign ownership (mostly concentrated in government bonds) remains at only around 3-4% of China’s entire onshore bond market. Furthermore, unlike other Asian economies in 1997-98, China has large foreign exchange reserves to buffer shocks from foreign fund flows. In recent years its capital control mechanism has also been successful in preventing implicit capital outflows and stabilizing the RMB exchange rate. We expect Chinese policymakers to feel confident in continuing their financial opening because they have the capability and sufficient funds to safeguard the economy against retrenchments by global investors. Bottom Line: China will continue to open its domestic financial markets, albeit gradually, to global investors. The country’s domestic financial markets have limited exposure to the extreme volatility of foreign capital flows. Investment Conclusions Chart 22The RMB Still Has Upside Structurally, But Will Modestly Depreciate On A Cyclical Basis

The RMB Still Has Upside Structurally, But Will Modestly Depreciate On A Cyclical Basis

The RMB Still Has Upside Structurally, But Will Modestly Depreciate On A Cyclical Basis

We are constructive on China’s government bonds, both cyclically and structurally. In the next six to nine months, the yield curve will likely flatten, with long-duration bond yields dropping faster than the short-end. China’s 10-year government bond yield will structurally shift to a lower range in the next five years, driven by the impact of falling population on domestic demand, and the country’s rising debt levels and debt-servicing costs. Although the RMB still has upside structural potential, in the next 6 to 12 months the currency will likely modestly depreciate against the US dollar (Chart 22). Jing Sima China Strategist jings@bcaresearch.com Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com Footnotes 1Total Factor Productivity (TFP) is a measure of productive efficiency, determining how much output can be produced from a certain amount of inputs. 2Defined by BIS as the ratio of interest payments plus amortizations to income. 3Despite a rising debt load, debt-servicing costs were contained due to (1) LGFV debt swap as new provincial government bonds had lower yields than LGFV bonds and (2) a large decline in the prime lending rate and mortgage rates. 4Foreign investors held more than 40% of local currency bonds in Indonesia, and over 20% in Malaysia. Foreign ownership accounted for 26% of Russia’s local currency bonds in 2014. Market/Sector Recommendations Cyclical Investment Stance

US corporate bond spreads have been widening recently and have underperformed duration-matched Treasuries so far in October. Notably, these moves are occurring against a backdrop of rising Treasury yields – marking a break in the typically negative…

Highlights Spread Product: Investors should stay overweight spread product versus Treasuries for now (with a preference for high-yield corporates over investment grade). But recent shifts in the yield/spread correlation suggest that the credit cycle is getting a bit long in the tooth. We will be quick to recommend a reduction in spread product exposure once the monetary tightening cycle is more advanced and the 3-year/10-year Treasury slope flattens to below 50 bps. We expect this could occur in the first half of 2022. Labor Market & Fed: September’s employment report likely doesn’t alter the Fed’s timeline. The Fed is still on track to announce a tapering of its asset purchases next month and we expect employment growth will be sufficiently strong for the Fed to start hiking rates in December 2022. The Treasury curve will bear-flatten as that outcome is priced in. Duration: Investors should maintain below-benchmark portfolio duration with an expectation that the 10-year Treasury yield will reach a range of 2%-2.25% by the time of Fed liftoff in December 2022. Feature Chart 1A December Debt Ceiling Debate

A December Debt Ceiling Debate

A December Debt Ceiling Debate

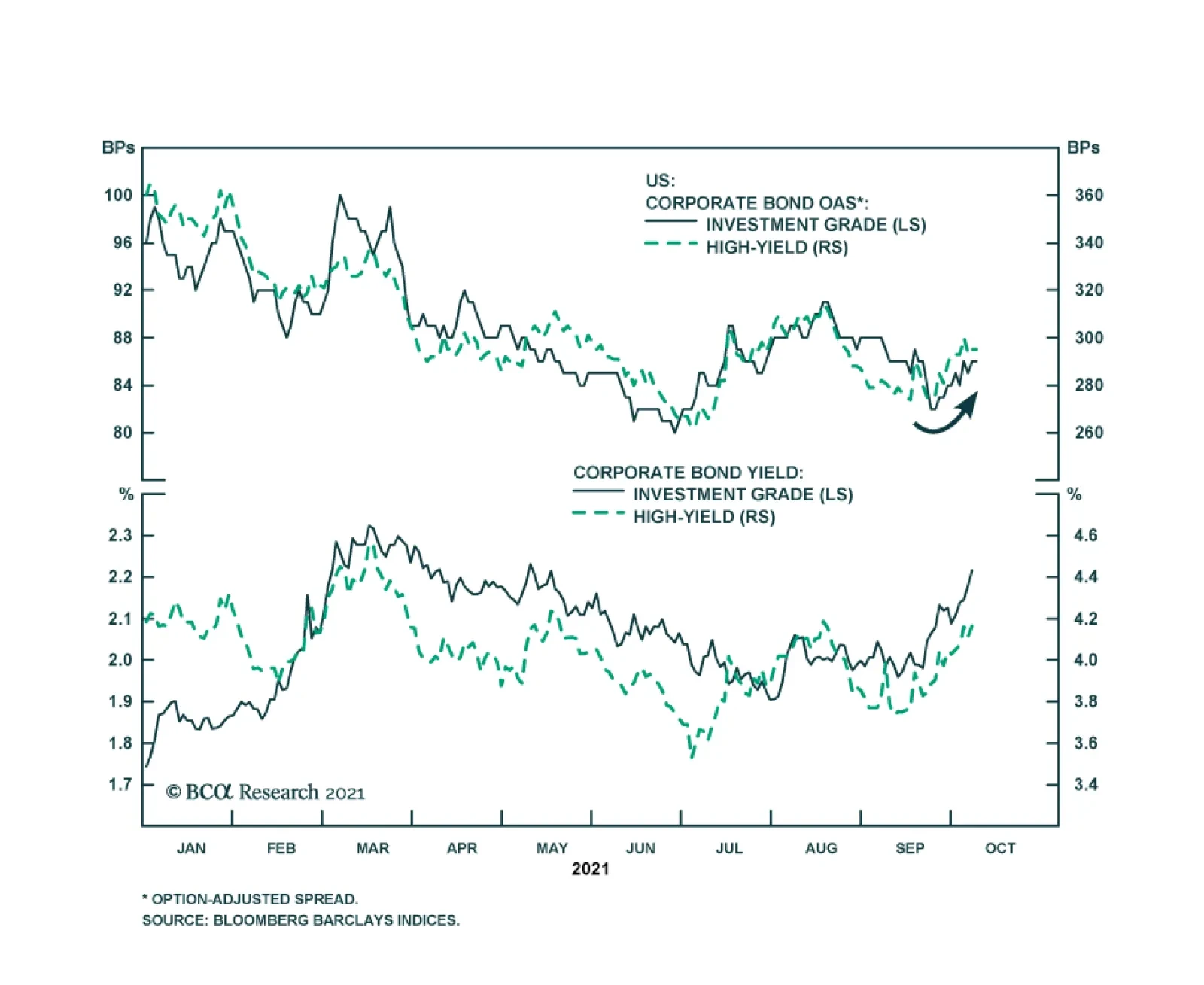

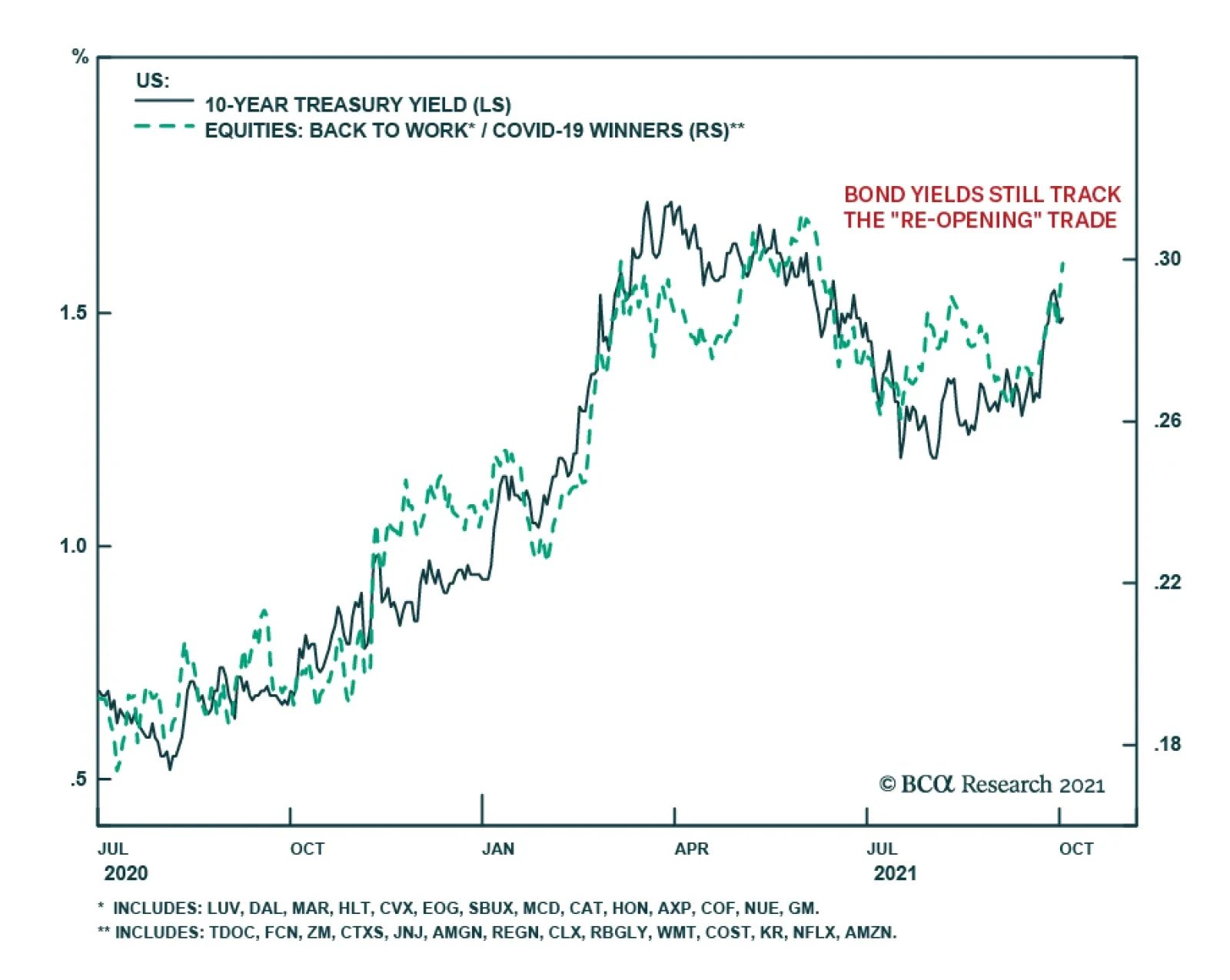

The creditors of the United States government can breathe a little easier, at least for a couple of months, as Congress reached an agreement last week to punt debt ceiling negotiations until December. T-bills maturing this month reacted sharply to price-out the risk of technical default, though December bill yields have already started to push higher in anticipation of more turmoil (Chart 1). Of course, the political incentives to lift the debt ceiling will be the same in December as they are today, and Congress will ultimately act to avert economic disaster.1 Financial markets seem to realize this, and Treasury note and bond yields have been unphased by the drama. Instead, Treasury yields have moved higher in recent weeks alongside other indicators of optimism surrounding economic reflation and re-opening (Chart 2). However, there is one troubling signal from financial markets that warrants further investigation. Corporate bonds (both investment grade and high-yield) have underperformed duration-matched Treasuries so far in October, even as Treasury yields have moved higher (Chart 3). Typically, Treasury yields and corporate bond spreads are negatively correlated – spreads tighten as Treasury yields rise, and vice-versa – so it is notable when the correlation flips. Chart 2The Reflation Trade Is Back

The Reflation Trade Is Back

The Reflation Trade Is Back

Chart 3Bad Times For Bonds

Bad Times For Bonds

Bad Times For Bonds

The next section of this report explores the economic drivers of the yield/spread correlation and considers whether the flip to a positive yield/spread correlation signals anything about future corporate bond performance. An Examination Of The Yield/Spread Correlation The simple economic explanation for the negative yield/spread correlation is that an improved economic outlook leads to both a better environment for credit risk (i.e. tighter corporate bond spreads) and the expectation that higher interest rates will be needed to cool the economy in the future (i.e. higher Treasury yields). With that in mind, when spreads and yields both rise at the same time it usually means that the Fed is “over-tightening”. That is, tightening monetary policy so much that the near-term credit environment is deteriorating. This could be because the Fed is making a policy mistake – tightening into an economic slowdown – or because inflation is high enough that the Fed is deliberately slowing growth in an effort to bring down prices. A Technical Examination Looking at the history of monthly changes in Treasury index yields and High-Yield index spreads since 1994, we see that it is quite unusual for yields and spreads to both rise in the same month (Chart 4). In fact, monthly yield and spread changes are negatively correlated 65% of the time and have only risen together in 15% of the months since 1994. Chart 4Monthly Junk Spread Changes Versus Monthly Treasury Yield Changes Since 1994

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Second, we observe in Chart 4 that almost all months of large spread widening or tightening occur against the back-drop of a negative yield/spread correlation. This shouldn’t be too surprising. The worst months for corporate bond performance occur during economic recessions when the Fed is cutting interest rates. Conversely, the best months for corporate bond performance occur just after the recession-peak in spreads when the Fed has finished cutting rates and the economic recovery is starting up. Tables 1A and 1B delve deeper into the return numbers. Table 1A shows average High-Yield excess returns over different investment horizons following a signal from the yield/spread correlation. For example, the second row shows that after a month when both Treasury yields and junk spreads rise, high-yield bonds deliver average excess returns of 24 bps during the following 3 months, 116 bps during the following 6 months and 75 bps during the following 12 months. Table 1B provides even more detail by showing 90% confidence intervals for each number. Table 1AAverage High-Yield Excess Returns After A Signal From Yield/Spread Correlation

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Table 1BHigh-Yield Excess Returns After A Signal From Yield/Spread Correlation: 90% Confidence Intervals

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

We draw two conclusions from this analysis. First, a month when spreads widen and yields fall sends the worst signal for near-term (3-month) corporate bond performance, though a month where both yields and spreads rise is a close second. Second, and most relevant for the current market, a month when yields and spreads rise together sends the worst signal for junk bond performance over the following 12 months. In fact, it is the only signal where the 90% confidence interval shows the chance of negative excess returns during the following 12 months. This second conclusion aligns with our intuition. A period of both rising Treasury yields and junk spreads likely signals that the market is pricing-in some move toward a tighter monetary policy stance, though not a severe enough move to send long-maturity Treasury yields down. This is most likely to occur in the very early stages of a monetary tightening cycle, when monetary conditions are still accommodative but recent shifts in Fed policy suggest that they will become more restrictive down the road. A Historical Examination A look back through history confirms our analysis of when yields and spreads tend to rise concurrently. The solid line in the third panel of Chart 5 shows the number of months when both junk spreads and Treasury yields rose out of the most recent trailing 12-month period. The dashed line shows the same measure over the trailing 3-month period, multiplied by 4 to put it on the same scale as the solid line. A spike in these lines indicates that Treasury yields and junk spreads were rising at the same time. Chart 5Rising Yields And Spreads Is A Warning Signal For Monetary Tightening

Rising Yields And Spreads Is A Warning Signal For Monetary Tightening

Rising Yields And Spreads Is A Warning Signal For Monetary Tightening

We identify four relevant historical periods. First, yields and spreads rose concurrently during the 1999/2000 Fed tightening cycle. Specifically, yields and spreads rose together in the early stages of the tightening cycle, then spreads continued to widen as yields fell during the 2001 recession. Second, our indicator showed a couple blips higher during the 2004/06 tightening cycle, though corporate bond returns were solid during this period, at least until after the tightening cycle ended and the recession began. Third, the 2013 taper tantrum coincided with a temporary increase in both yields and spreads as investors worried that the Fed was moving too quickly toward rate hikes. Fourth, yields and spreads both moved higher in 2015 as the Fed was heading toward a December 2015 rate hike against a back-drop of slowing economic growth. Turning to today, we view the recent jump in our indicator as similar to the jump seen during the 2013 taper tantrum. Not only is the Fed once again about to taper asset purchases, but the tapering of asset purchases suggests that the Fed’s next move will be a rate hike at some point down the road. We view this as an early warning sign for corporate bond spreads. While the monetary environment remains supportive for positive corporate bond returns for now, this may not be true by this time next year when the Fed is that much closer to liftoff. Bottom Line: Investors should stay overweight spread product versus Treasuries for now (with a preference for high-yield corporates over investment grade). But recent shifts in the yield/spread correlation suggest that the credit cycle is getting a bit long in the tooth. We will be quick to recommend a reduction in spread product exposure once the monetary tightening cycle is more advanced and the 3-year/10-year Treasury slope flattens to below 50 bps. We expect this could occur in the first half of 2022. Labor Market Update: Still On Track For November Taper And December 2022 Liftoff Chart 6Employment Growth Slowed in September

Employment Growth Slowed in September

Employment Growth Slowed in September

September’s employment report delivered a disappointing headline number, with nonfarm payrolls growing only 194 thousand on the month compared to a consensus estimate of 500k (Chart 6). The details of the report were slightly better: August’s nonfarm payroll growth number was revised higher, our measure of the unemployment rate adjusted for distortions in the number of people employed but absent from work fell from 5.5% to 4.9% (Chart A1) and average hourly earnings rose at an annualized monthly rate of 7.7% (Chart 6, bottom panel). Expect A November Taper For bond investors, the most pressing question is whether the report is bad enough to delay the Fed’s tapering announcement past November. We doubt it. The Fed’s test for when to taper asset purchases, that it gave itself last December, is “substantial further progress” back to pre-COVID levels of employment. Since December 2020, total nonfarm payroll employment is 50% of the way back to its February 2020 level (Chart 7) and there are several good reasons to believe that employment growth will be much stronger in October and November. First, the delta wave of COVID cases clearly weighed on employment growth in September, much like it did in August. The Leisure & Hospitality sector only added 74 thousand jobs in September, compared to an average monthly pace of 349 thousand jobs between February and July of this year before the delta wave struck. With a shortfall of almost 1.6 million Leisure & Hospitality jobs compared to pre-COVID levels (Table 2), job growth in this sector will bounce back sharply during the next few months now that new COVID cases are receding (Chart 8). Chart 7"Substantial Further Progress" Has Been Made

"Substantial Further Progress" Has Been Made

"Substantial Further Progress" Has Been Made

Chart 8Delta Wave Has Crested

Delta Wave Has Crested

Delta Wave Has Crested

Second, the last column of Table 2 shows that the government sector accounted for net job loss of 123 thousand in September. This negative number was driven by state & local government education jobs and is almost certainly a statistical artifact. According to the Bureau of Labor Statistics’ release notes: Recent employment changes [in state & local government education] are challenging to interpret, as pandemic-related staffing fluctuations in public and private education have distorted the normal seasonal hiring and layoff patterns. Table 2Employment By Industry

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Expect December 2022 Liftoff As for what this labor market report means for when the Fed will start lifting rates, we believe that we are still on track for liftoff in December 2022. The Appendix to this report updates our scenarios that show the average monthly nonfarm payroll growth that is required to reach different combinations of the unemployment and labor force participation rates by specific future dates. If we use the median assumption from the New York Fed’s Survey of Market Participants that the Fed will lift rates when the unemployment rate is 3.5% and the participation rate is 63%, we calculate that average monthly nonfarm payroll growth of +453k is required to reach those targets by the end of 2022. We see that threshold as eminently achievable.2 Bottom Line: September’s employment report likely doesn’t alter the Fed’s timeline. The Fed is still on track to announce a tapering of its asset purchases next month and we expect employment growth will be sufficiently strong for the Fed to start hiking rates in December 2022. Investors should maintain below-benchmark portfolio duration and hold Treasury curve flatteners in anticipation of that outcome. Ryan Swift US Bond Strategist rswift@bcaresearch.com Appendix: How Far From “Maximum Employment” And Fed Liftoff? Chart A1Defining “Maximum Employment”

Defining "Maximum Employment"

Defining "Maximum Employment"

The Federal Reserve has promised that the funds rate will stay pinned at zero until the labor market returns to “maximum employment”. The Fed has not provided explicit guidance on the definition of “maximum employment”, but we deduce that “maximum employment” means that the Fed wants to see the U3 unemployment rate within a range consistent with its estimates of the natural rate of unemployment, currently 3.5% to 4.5%, and that it wants to see a significant increase in the labor force participation rate (Chart A1). Alternatively, we can infer definitions of “maximum employment” from the New York Fed’s Surveys of Primary Dealers and Market Participants. These surveys ask respondents what they think the unemployment and labor force participation rates will be at the time of Fed liftoff. Currently, the median respondent from the Survey of Market Participants expects an unemployment rate of 3.5% and a participation rate of 63%. The median respondent from the Survey of Primary Dealers expects an unemployment rate of 3.8% and a participation rate of 62.8%. Tables A1-A4 present the average monthly nonfarm payroll growth required to reach different combinations of unemployment rate and participation rate by specific future dates. For example, if we use the definition of “maximum employment” from the Survey of Market Participants, then we need to see average monthly nonfarm payroll growth of +453k in order to hit “maximum employment” by the end of 2022. Table A1Average Monthly Nonfarm Payroll Growth Required For The Unemployment Rate To Reach 4.5% By The Given Date

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Table A2Average Monthly Nonfarm Payroll Growth Required For The Unemployment Rate To Reach 4% By The Given Date

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Table A3Average Monthly Nonfarm Payroll Growth Required For The Unemployment Rate To Reach 3.5% By The Given Date

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Table A4Average Monthly Nonfarm Payroll Growth Required To Reach “Maximum Employment” As Defined By Survey Respondents

An Early Warning Sign For Spreads

An Early Warning Sign For Spreads

Chart A2 presents recent monthly nonfarm payroll growth along with target levels based on the Survey of Market Participants’ definition of “maximum employment”. This chart is to help us track progress toward specific liftoff dates. For example, if monthly nonfarm payroll growth prints +400k per month going forward, we would expect Fed liftoff between December 2022 and June 2023. We will continue to track these charts and tables in the coming months, and will publish updates after the release of each monthly employment report. Chart A2Tracking Toward Fed Liftoff

Tracking Toward Fed Liftoff

Tracking Toward Fed Liftoff

Footnotes 1 For more details on the politics of the debt ceiling please see US Political Strategy Weekly Report, “The House Ways And Means Tax Plan”, dated September 15, 2021. 2 For a discussion about what unemployment and participation rate targets to use in this analysis please see US Bond Strategy Weekly Report, “2022 Will Be All About Inflation”, dated September 14, 2021. Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

Highlights Equity valuations are extremely stretched versus bonds, so there is little wiggle room for bonds to sell off before pulling down large tracts of the stock market. We estimate that bond yields can rise by no more than 30 bps, before the Fed is forced to talk them back down again. Starting from an earnings yield that is extreme versus its history, we should prudently assume that the prospective long-term real return from equities will be far below the current earnings yield of 4.6 percent, and closer to zero, even if not actually negative. In capitalist economies, gluts may or may not lead to shortages; but shortages always lead to gluts. In other words, the current inflation is sowing the seeds of its own destruction. Hence, we reiterate our structural recommendation to overweight US T-bonds versus US TIPS. Fractal analysis: Cotton, and Polish equities. Feature Chart of the WeekTech Stocks Have Been Tracking The 30-Year T-Bond Price One-For-One

Tech Stocks Have Been Tracking The 30-Year T-Bond Price One-For-One

Tech Stocks Have Been Tracking The 30-Year T-Bond Price One-For-One

Equity valuations are extremely stretched versus bonds. The upshot is that there is little wiggle room for bonds to sell off before pulling down large tracts of the stock market. This is not just an abstract hypothesis – it is an empirical fact, as recent market action is making painfully clear. Since February, the global tech sector has tracked the 30-year T-bond price almost one-for-one. The near perfect fit proves that the tech (and broader growth stock) rally has been entirely premised on the bond market rally. Hence, on the three occasions that bonds have sold off sharply – including in the last couple of weeks – tech stocks have sold off sharply too (Chart of the Week). Put simply, the performance of the tech sector is being driven by the change in its valuation, and the change in its valuation is being driven by the change in the bond yield (Chart I-2). Chart I-2Tech Stock Valuations Are Being Driven By The Bond Yield

Tech Stock Valuations Are Being Driven By The Bond Yield

Tech Stock Valuations Are Being Driven By The Bond Yield

Of course, stock prices are also premised on earnings. So, given enough time, rising earnings can make valuations less stretched, adding more wiggle room for bonds to sell off. The trouble is that a change in earnings happens much more gradually than can a change in valuation – a 10 percent rise in earnings can take a year, whereas a 10 percent fall in valuation can happen in a week. Bond Yields Remain The Dominant Driver Of The Stock Market For the next few months at least, the movement in bond yields will remain the dominant driver of the most stretched parts of the stock market and, by extension, the overall market itself. This is especially true for the growth-heavy S&P 500 which, since March, has been tracking the 30-year T-bond price one-for-one (Chart I-3). Chart I-3The S&P 500 Has Also Been Tracking The 30-Year T-Bond Price One-For-One

The S&P 500 Has Also Been Tracking The 30-Year T-Bond Price One-For-One

The S&P 500 Has Also Been Tracking The 30-Year T-Bond Price One-For-One

The key question for investors is, what is the upper limit to bond yields before stock market damage causes the Federal Reserve to talk them down again? To answer this question, our working assumption is that a 15 percent drawdown in growth stocks would damage the growth-heavy S&P 500 enough – and thereby worsen ‘financial conditions’ enough – for the Fed to change its tone. Based on this year’s very tight relationship between tech stocks and the 30-year T-bond yield, a 15 percent drawdown would occur if the 30-year T-bond yield increased to 2.4 percent from 2.1 percent today (Chart I-4). Chart I-4The Fed's 'Pain Point' Is Only 30 Basis Points Away

The Fed's 'Pain Point' Is Only 30 Basis Points Away

The Fed's 'Pain Point' Is Only 30 Basis Points Away

This confirms our view that the resistance level to long-duration bond yields is around 30 bps above current levels, equivalent to around 1.8 percent on the 10-year T-bond yield. More About The ‘Negative Equity Risk Premium’ Our recent report The Equity Risk Premium Turns Negative For The First Time Since 2002 caused quite a stir. So, let’s elaborate and clarify the arguments we made about the equity risk premium (ERP) – the estimated excess return that stocks will deliver over bonds over a long investment horizon, such as 10 years. Many investors estimate the ERP by taking the stock market’s earnings yield – currently 4.6 percent in the US1 – and subtracting the real 10-year bond yield – currently -0.9 percent on US Treasury Inflation Protected Securities (TIPS). At first glance, this presents a very generous ERP of 5.5 percent. So, equities are attractively valued versus bonds, right? Wrong. The glaring error is that the earnings yield estimates the stock market’s prospective return only if the earnings yield starts and ends at the same level. If it does not, then the prospective return could be very different to the earnings yield. For example, imagine that the stock market was trading at a bubble price-to-earnings multiple of 100, meaning an earnings yield of 1 percent. Clearly, from such a bubble valuation, nobody would expect the market to return 1 percent. Instead, as the bubble burst, and valuations normalised, the prospective return would be deeply negative. It follows that when, as now, the earnings yield is extreme versus its history, we must build in some prudent normalisation to estimate the prospective return. The question is, how? One approach is to use history to inform us of the likely normalisation. Chart I-5 does this using the ‘best-fit’ relationship between the earnings yield at each point through 1990-2011 and subsequent 10-year real return from each starting point. Using the best-fit for this specific episode, the current earnings yield of 4.6 percent implies a prospective 10-year real return not of 4.6 percent, but of -1.1 percent. Chart I-5Based On History, The Current Earnings Yield Implies A Prospective 10-Year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 10-year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 10-year Real Return Much Less Than 4.6 Percent

Yet this best-fit approach meets a common reproach – that the best-fit for this specific episode is massively distorted by the dot com bubble peak and the global financial crisis (GFC) trough occurring (by coincidence) almost 10 years apart. We can counter this reproach in two ways. First, the best-fit relationship is much better than the raw earnings yield even for undistorted 10-year periods such as 1995-2005 or 2011-2021. Better still, we can change the prospective return from 10 years to 7 years and thereby remove the dot com bubble peak to GFC trough distortion. Chart I-6 shows that this 7-year best-fit relationship also works much better than the raw earnings yield. Chart I-6Based On History, The Current Earnings Yield Implies A Prospective 7-Year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 7-year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 7-year Real Return Much Less Than 4.6 Percent

Admittedly, the best-fit comes from just one episode in history, and there is no certainty that the 10-year and 7-year relationships that applied during that one episode should apply through 2021-31 and 2021-28 respectively. Nevertheless, starting from an earnings yield that is extreme versus its history, as is the case now, we should prudently assume that the prospective long-term real return from equities will be far below 4.6 percent, and closer to zero, even if not actually negative. Will The ‘Real’ Real Yield Please Stand Up Measuring the ERP also requires an estimate of the prospective real return on bonds. This part should be easy because the yield on the US 10-year TIPS – currently -0.9 percent – is the guaranteed 10-year real return of buying and holding that investment. It is derived by taking the yield on the 10-year T-bond – currently 1.5 percent – and subtracting the market’s expected rate of inflation over the next 10 years – currently 2.4 percent. But the equivalent real return on the much larger conventional bond market could be quite different. In this case, it will be the 10-year T-bond yield minus the actual rate of inflation over the next 10 years. To the extent that the actual rate of inflation turns out less than the expected rate of 2.4 percent, the real return on the T-bond will turn out higher than that on the TIPS. In fact, this has consistently turned out to be the case. The market has consistently overestimated the inflation rate over the subsequent 10 years, meaning that the real return on T-bonds has been around 1 percent higher than that on TIPS (Chart I-7). Chart I-7Will The 'Real' Real Yield Please Stand Up

Will The 'Real' Real Yield Please Stand Up

Will The 'Real' Real Yield Please Stand Up

Yet given the current surge in inflation, and no end in sight for supply chain disruptions and bottlenecks, is it plausible that the next ten years’ rate of inflation will be lower than 2.4 percent? The answer is yes. Because, as my colleague Peter Berezin points out: in capitalist economies, gluts may or may not lead to shortages; but shortages always lead to gluts. And gluts always cause prices to collapse. In other words, the current inflation is sowing the seeds of its own destruction. Hence, we reiterate our structural recommendation to overweight US T-bonds versus US TIPS. The Cotton Is Stretched, And So Are Polish Equities Talking of shortages, cotton now adds to the list of commodities in which supply bottlenecks have raised prices to extremes. Cotton prices have reached a 10-year high due to weather conditions in the US (the world’s biggest cotton producer) combined with shipping disruptions. However, with cotton now exhibiting extreme fragility on its combined 130/260-day fractal structure, there is a high likelihood of a price reversal in the coming months when the shortage turns into a glut (Chart I-8). Chart I-8The Cotton Is Stretched

The Cotton Is Stretched

The Cotton Is Stretched

Meanwhile, the bank-heavy Polish equity market has surged on the back of the spectacular outperformance of its banks sector. This strong uptrend has now reached the point of fragility on its 130-day fractal structure that has indicated several previous reversals (Chart I-9). Chart I-9Poland's Outperformance Is Stretched

Poland's Outperformance Is Stretched

Poland's Outperformance Is Stretched

Accordingly, this week’s recommended trade is to underweight the Warsaw General Index versus the Eurostoxx 600, setting a profit target and symmetrical stop-loss at 6 percent. Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Based on the 12-month forward earnings yield. Fractal Trading System Fractal Trades 6-Month Recommendations Structural And Thematic Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Q3/2021 Performance Breakdown: Our recommended model bond portfolio outperformed the custom benchmark index by +8bps during the third quarter of the year. Winners & Losers: The government bond side of the portfolio outperformed by +4bps, led by the timely downgrade of UK Gilts to underweight in early August. Spread product allocations outperformed by +4bps, coming entirely from the overweights to high-yield in the US and Europe. Portfolio Positioning For The Next Six Months: We are maintaining an overall below-benchmark portfolio duration exposure, concentrated in the US and UK. We expect global growth will rebound from the Delta variant and supply chain disruptions will keep inflation elevated for longer, both of which will push global bond yields higher as central banks – led by Fed – turn less dovish. We are maintaining a moderate overweight to global spread product versus government debt, concentrated on an overweight to US high-yield where valuations still look the least stretched compared to corporate debt in other countries. Feature Global bond markets have had a lot of sources of uncertainty to digest over the past few months. Renewed COVID fears due to the spread of the Delta variant, slowing global growth momentum, supply chain disruptions leading to surging realized inflation, the ongoing US fiscal policy debate in D.C., concerns over Chinese corporate debt and the increasingly hawkish monetary policy signals sent by global central banks, most notably the Fed. The net result of these narratives has been some major swings in government bond market performance during the third quarter of 2021. The benchmark 10-year government bond yield in the US started the quarter at 1.48%, fell to an intraday low of 1.12% on August 4, then soared higher to end the quarter back at 1.50%. Even bigger moves were seen in other countries, with the 10-year UK Gilt yield doubling from its Q3 low of 0.48% on August 4 while the 10-year German bund yield is now 30bps above its low for the quarter. Despite this yield volatility, however, spreads for riskier credit market assets like US high-yield have remained generally well behaved. With that in mind, we present our quarterly review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio during Q3/2021. We also present our recommended positioning for the portfolio for the next six months (Table 1), as well as portfolio return expectations for our base case and alternative investment scenarios. We anticipate that bond investor uncertainty will switch from concerns about global growth to worries that stubbornly elevated inflation will elicit bond-bearish monetary policy responses from central banks. Table 1GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

As a reminder to existing readers (and to new clients), the model portfolio is a part of our service that complements the usual macro analysis of global fixed income markets. The portfolio is how we communicate our opinion on the relative attractiveness between government bond and spread product sectors. We do this by applying actual percentage weightings to each of our recommendations within a fully invested hypothetical bond portfolio. Q3/2021 Model Bond Portfolio Performance: Positive Returns In An Uncertain Environment Chart 1Q3/2021 Performance: Riding The Duration Roller Coaster

Q3/2021 Performance: Riding The Duration Roller Coaster

Q3/2021 Performance: Riding The Duration Roller Coaster

The total return for the GFIS model portfolio (hedged into US dollars) in the third quarter was +0.21%, slightly outperforming the custom benchmark index by +8bps (Chart 1).1 In terms of the specific breakdown between the government bond and spread product allocations in our model portfolio, the former generated +4bps of outperformance versus our custom benchmark index while the latter also outperformed by +4bps. Those small positive excess returns should be considered a victory, given the huge yield swings within the quarter, particularly for government bonds. We maintained a significant underweight position to US Treasuries in the portfolio during Q3, given our view that markets were underestimating the risks that the US economy would weather the summer Delta storm. As Treasury yields declined steadily during July and August, so did the relative performance of our model bond portfolio. The government bond portion of the portfolio was underperforming the benchmark by as much as -30bps before global bond yields bottomed out in early August. In the end, there was only a slight underperformance (-2bps) from the US Treasury portion of the portfolio during the quarter (Table 2). Table 2GFIS Model Bond Portfolio Q3/2021 Overall Return Attribution

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Our biggest government bond overweights have been concentrated in the euro area. There, the sum of active returns during Q3 from our government bond allocations was +3bps, although that came entirely from above-benchmark allocations to inflation-linked bonds in Germany, France and Italy. We did make one major shift in our government bond allocations during the quarter, and it was both timely and successful. We downgraded our recommended UK Gilt exposure to underweight on August 11.2 We observed that the Bank of England (BoE) was starting to prepare the markets for less accommodative monetary policy, with the UK economy holding up well as its Delta variant surge was losing momentum. The BoE rhetoric has proven to be even more hawkish than we anticipated, hinting at a possible rate hike before the end of 2021, leading Gilts to be the worst performing government bond market in our model portfolio universe during the quarter. The result: our UK underweight contributed +4bps to the portfolio performance during the quarter. Turning to the credit side of the portfolio, the most successful positions were our overweight tilts on high-yield in the US (+3bps) and euro area (+1bps). All other exposures contributed little to returns, an unsurprising development given our neutral allocations to investment grade corporates in the US, UK and euro area, as well as for USD-denominated EM corporates. The bar charts showing the total and relative returns for each individual government bond market and spread product sector are presented in Charts 2 & 3. Chart 2GFIS Model Bond Portfolio Q3/2021 Government Bond Performance Attribution

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Chart 3GFIS Model Bond Portfolio Q3/2021 Spread Product Performance Attribution By Sector

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Biggest Outperformers: Overweight UK Gilts with a maturity greater than 10-years (+4bps) Overweight Italian inflation-linked bonds (+2bps) Overweight US high-yield: Ba-rated (+2bps) and B-rated (+1bps) Biggest Underperformers: Underweight US Treasuries with a maturity greater than 10-years (-2bps) Overweight Japanese Government Bonds in longer maturity buckets: 7-10 years (-1bps) and greater than 10-years (-1bps) Overweight UK inflation-linked bonds (-1bps) Chart 4 presents the ranked benchmark index returns of the individual countries and spread product sectors in the GFIS model bond portfolio for Q3/2021. Returns are hedged into US dollars (we do not take active currency risk in this portfolio) and adjusted to reflect duration differences between each country/sector and the overall custom benchmark index for the model portfolio. We have also color coded the bars in each chart to reflect our recommended investment stance for each market during Q3 (red for underweight, dark green for overweight, gray for neutral). Chart 4Ranking The Winners & Losers From The GFIS Model Bond Portfolio Universe In Q3/2021

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Ideally, we would look to see more green bars on the left side of the chart where market returns are highest, and more red bars on the right side of the chart were returns are lowest. As can be seen in the chart, the bars look very close to that ideal for Q3/2021. Among the markets that represent our overweights, the most notably positive returns came from all euro area government bonds (a combined +136bps) and euro area corporates (a combined +20bps from investment grade and high-yield). Returns within our recommended underweight positions were even more notable: UK Gilts (-302bps), New Zealand government bonds (-103bps), EM USD-denominated sovereigns (-85bps), and Canadian government bonds (-45bps). Bottom Line: Our model bond portfolio slightly outperformed its benchmark index in the third quarter of the year by +8bps – a moderately positive result coming equally from underweight positions in government bonds and overweight allocations to spread product. Future Drivers Of Portfolio Returns Chart 5Negative Real Yields: The Biggest Mispricing In Global Bond Markets

Negative Real Yields: The Biggest Mispricing In Global Bond Markets

Negative Real Yields: The Biggest Mispricing In Global Bond Markets

Looking ahead, the performance of the model bond portfolio will continue to be driven primarily by our below-benchmark overall duration tilt – focused on our underweight stance on US Treasuries – and our overweight stance on high-yield corporates. Our most favored cyclical indicators for global bond yields are still, in aggregate, signaling more upside potential over at least the next six months, although the nature of the signal is changing (Chart 5). While our Global Duration Indicator, comprised of leading economic indicators and measures of future economic sentiment, has peaked, the overall level of 10-year bond yields within the major developed markets remains well below levels implied by the Indicator (top panel). That is most clearly evident when looking at the large gap between deeply negative real bond yields and the still-elevated level of the global manufacturing PMI, which typically leads real yields by around six months (second panel). We continue to view this gap between real yields and growth as the biggest mispricing in global bond markets – one that will eventually be rectified by the incremental reduction in monetary accommodation that is signaled by our Global Central Bank Monitor (bottom panel). The combined message from our Central Bank Monitor, Duration Indicator and the manufacturing PMI is that global bond yields are still too low, suggesting a below-benchmark overall portfolio duration stance remains appropriate. With regards to country allocation within the government bond side of our model portfolio, we continue to overweight countries where central banks are less likely to begin normalizing pandemic-era monetary policy quickly (Germany, France, Italy, Spain, Japan, Australia), while underweighting countries where normalization is expected to begin within the next 6-12 months (the US, UK and Canada). We have the highest conviction on the US and UK underweights, with a curve-flattening bias for both markets relative to the rest of the major developed markets (Chart 6). The bond-friendly (and risk asset-friendly) impact of global quantitative easing programs is fading, on the margin, with the annual growth rate of central bank balance sheets having already slowed sharply (Chart 7). The pace of tapering, and any subsequent rate hikes, will differ by country and support our government bond country allocations in the model portfolio. Chart 6Expect More Relative Curve Flattening In The US & UK

Expect More Relative Curve Flattening In The US & UK

Expect More Relative Curve Flattening In The US & UK

Chart 7The 'Great Global Taper' Has Begun

The 'Great Global Taper' Has Begun

The 'Great Global Taper' Has Begun

Chart 8Less Scope For Wider Global Inflation Breakevens

Less Scope For Wider Global Inflation Breakevens

Less Scope For Wider Global Inflation Breakevens

We expect the Fed to taper its pace of bond purchases over the first half of 2022, setting up a first Fed rate hike late next year. The Bank of Canada and the BoE will be the other developed market central banks that will both end QE and lift rates before the Fed does the same. On the other hand, the ECB, Bank of Japan and the Reserve Bank of Australia will maintain a more relatively dovish stance in 2022, with very modest tapering (at worst) and no rate hikes. Turning to inflation-linked bonds, we are maintaining an overall neutral allocation given the competing forces of rising global inflation and rich valuations. Our Comprehensive Breakeven Indicators combine three measures to determine the upside potential for 10-year inflation breakevens: the distance from fair value based on our models, the spread between headline inflation and central bank target inflation, and the gap between market-based and survey-based measures of inflation expectations. Those indicators suggest that the most attractive markets to position for further upside potential for breakevens are Italy, France, Canada and Japan (Chart 8). On the back of this, we are maintaining our overweight allocations to inflation-linked bonds in the euro area and Japan in our model portfolio, while staying neutral on US TIPS. Chart 9Fading Support For Credit Markets From Global QE In 2022

Fading Support For Credit Markets From Global QE In 2022

Fading Support For Credit Markets From Global QE In 2022

Moving our attention to the credit side of our model portfolio, a moderate overweight stance on overall global corporates (focused on high-yield) versus governments remains appropriate. However, the slowing trend in developed market central bank balance sheets is flashing a warning sign for the future performance of global spread product. The annual growth rate of the combined balance sheets of the Fed, ECB, Bank of Japan and Bank of England has been an excellent leading indicator (by about twelve months) of the annual excess returns of both global investment grade and high-yield corporates during the “QE Era” since the 2008 financial crisis (Chart 9). That growth rate peaked back in February of this year, suggesting a peak of global corporate bond outperformance around February 2022, particularly for high-yield versus government bonds and investment grade (top two panels). At the same time, our preferred measure of the attractiveness of credit spreads - the historical percentile ranking of 12-month breakeven spreads – shows that lower-rated high-yield credit tiers in the US and euro area offer spreads that are relatively high versus their own history compared to other credit sectors in our model bond portfolio universe (Chart 10). Using this metric, investment grade corporate spreads look much more fully valued, particularly in the US. Chart 10Lower-Rated High-Yield & EM Sovereigns Offer Relatively Attractive Spreads

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Given sharply reduced default risks in the US and Europe, with strong nominal growth supporting corporate revenues alongside low borrowing rates, the fundamental backdrop for riskier high-yield corporates is still positive. Thus, we are maintaining our overweights to high-yield bonds in both the US and euro area, while sticking with only a neutral stance on investment grade corporates in the US, euro area and the UK. We do anticipate starting to reduce that exposure in the model portfolio sometime in early months of 2022, however, based on the ominous leading signal from the growth of central bank balance sheets – and what that means about the future path for global monetary policy and risk asset performance. Within the euro area, we are maintaining overweights to Italian and Spanish government bonds given the likelihood that the monetary policy backdrop will remain supportive (Chart 11). We expect the ECB to be one of the most accommodative central banks within our model portfolio universe in 2022. At worst, the ECB could deliver a modest reduction of total asset purchases, but with no rate hikes. Chart 11A Relatively Dovish ECB Will Be Positive For European Credit

A Relatively Dovish ECB Will Be Positive For European Credit

A Relatively Dovish ECB Will Be Positive For European Credit

Chart 12EM Headwinds: A Firmer USD, China Tightening & Global QE Tapering

EM Headwinds: A Firmer USD, China Tightening & Global QE Tapering

EM Headwinds: A Firmer USD, China Tightening & Global QE Tapering

Finally, we are sticking with a cautious stance on emerging market (EM) spread product in our model bond portfolio. Slowing Chinese economic growth, a firming US dollar, rate hikes across EM in response to high inflation, and the coming turn in the Fed policy cycle are all headwinds to the relative performance of EM USD-denominated corporates and sovereigns (Chart 12). We are sticking with our overall modestly underweight stance on EM USD-denominated credit. However, rebounding global growth and some potential policy stimulus in China could prompt us to consider an upgrade in the coming months. Summing it all up, our overall allocations and risks in our model portfolio leading into Q4/2021 look like this: An overall below-benchmark stance on global duration, equal to -0.75 years versus the custom index (Chart 13). A moderate overweight stance on global spread product versus government debt, equal to five percentage points of the portfolio (Chart 14). This overweight comes almost entirely from allocations to US and euro area high-yield corporates. The tracking error of the portfolio, or its expected volatility versus that of the benchmark index, is relatively low at 55bps (Chart 15). This fits with our desire to maintain only a moderate level of absolute portfolio risk, while focusing exposures more on relative tilts between countries and credit sectors. Chart 13Overall Portfolio Duration: Stay Below Benchmark

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Chart 14Overall Portfolio Allocation: Small Spread Product Overweight

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

The yield of the portfolio is now slightly higher than that of the benchmark, with a small “positive carry” of 16bps (Chart 16). Chart 15Overall Portfolio Risk: Moderate

Overall Portfolio Risk: Moderate

Overall Portfolio Risk: Moderate

Chart 16Overall Portfolio Yield: Small Positive Carry Vs. Benchmark

Overall Portfolio Yield: Small Positive Carry Vs. Benchmark

Overall Portfolio Yield: Small Positive Carry Vs. Benchmark

Scenario Analysis & Return Forecasts We now turn to scenario analysis to determine the return expectations for the portfolio for the next six months. On the credit side of the portfolio, we use risk-factor-based regression models to forecast future yield changes for global spread product sectors as a function of four major factors - the VIX, oil prices, the US dollar and the fed funds rate (Table 2A). For the government bond side of the portfolio, we avoid using regression models and instead use a yield-beta driven framework, taking forecasts for changes in US Treasury yields and translating those in changes in non-US bond yields by applying a historical yield beta (Table 2B). For our scenario analysis over the next six months, we use a base case scenario plus two alternate “tail risk” scenarios. Table 2AFactor Regressions Used To Estimate Spread Product Yield Changes

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

Table 2BEstimated Government Bond Yield Betas To US Treasuries

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare

GFIS Model Bond Portfolio Q3/2021 Performance Review & Current Allocations: Fading A Growth Scare