Fixed Income

Highlights The equity risk premium has turned negative for the first time since 2002. It follows that any significant rise in bond yields will cause risk-asset prices to collapse, quickly flipping any incipient inflationary shock into a deflationary shock. Shorting bonds yielding 2 percent is a ‘widow maker’ trade, as anybody who has tried this with a long list of government bonds has learned to their cost, the most recent being UK gilts. Hence, the next on the list for the ‘widow maker’ is shorting the US 30-year T-bond which is now yielding 2 percent. In fact, the US 30-year T-bond is a must-own structural investment. Fractal analysis: Medical equipment versus healthcare services. Feature Chart of the WeekThe Equity Risk Premium Turns Negative For The First Time Since 2002

The Equity Risk Premium Turns Negative For The First Time Since 2002

The Equity Risk Premium Turns Negative For The First Time Since 2002

Mainstream investments are now priced to deliver negative, zero, or at best, feeble long-term investment returns. Mainstream investments are now priced to deliver negative, zero, or at best, feeble long-term investment returns. For example, the US 10-year Treasury Inflation Protected Security (TIPS) and the UK 10-year index linked gilt are yielding -1.3 percent and -2.8 percent respectively. Meaning that anybody who buys and holds these bonds to redemption is guaranteed a deeply negative 10-year real return. Meanwhile, in nominal yield space, 10-year government bonds yield -0.35 percent in Germany and Switzerland, 0.7 percent in the UK, and 1.3 percent in the US. What about equities? Unlike a bond’s redemption yield, equities do not offer a guaranteed long-term return for buy-and-hold investors. So, some analysts assume that the equity market’s earnings yield is the proxy for this long-term return. According to these analysts, the US equity market’s earnings yield of 4.4 percent means that it will deliver a prospective long-term real return of 4.4 percent per annum. Compared to the 10-year TIPS real yield of -1.3 percent, they argue that this offers an excess return or ‘equity risk premium’ of a comfortable +5.7 percent. Therefore, claim these analysts, equities are reasonably valued, relative to bonds, and in absolute terms. But as we will now demonstrate, this analysis is deeply flawed. The Equity Risk Premium Has Turned Negative The equity market’s earnings yield is a valuation metric, so clearly there is some connection between it and the prospective return delivered by the equity market. Nevertheless, the crucial point to grasp is that: The equity market’s earnings yield does not equal its prospective return. Charts I-2 - I-3 should make this point crystal clear. As you can see, the earnings yield rarely equals the delivered prospective 10-year return, either real or nominal. When the earnings yield is elevated, the prospective return turns out higher. Conversely, when the earnings yield is depressed, as now, the prospective return turns out to be much lower. Chart I-2The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

Chart I-3...Or In Nominal ##br##Terms

...Or In Nominal Terms

...Or In Nominal Terms

Therefore, to take the current earnings yield of 4.4 percent and subtract the real bond yield of -1.3 percent to derive an equity risk premium of +5.7 percent is analytically flawed, just as it is analytically flawed to subtract apples from oranges. To derive the equity risk premium, the correct approach is first to translate the earnings yield into a prospective 10-year return based on the established mathematical relationship between these variables. Chart I-4 does this and shows that, based on a very tight mathematical relationship through the past thirty five years, an earnings yield of 4.4 percent translates into a prospective 10-year nominal return of just 1 percent. Chart I-4We Must Mathematically Map The Earnings Yield Into A Prospective Return...

We Must Mathematically Map The Earnings Yield Into A Prospective Return...

We Must Mathematically Map The Earnings Yield Into A Prospective Return...

Having translated the earnings yield into a prospective 10-year nominal return of 1 percent, we can now make an apples-for-apples comparison with the 10-year T-bond yield of 1.3 percent (Chart I-5). Chart I-5...And Only Then Subtract The Bond Yield

...And Only Then Subtract The Bond Yield

...And Only Then Subtract The Bond Yield

Derived correctly therefore, the equity risk premium has turned negative for the first time since 2002 (Chart of the Week). We deduce that the equity market is very richly valued both in absolute terms and relative to bonds. And crucially, that this rich valuation is contingent on bond yields remaining ultra-low, or going even lower. Shorting Bonds Yielding 2 Percent Is A ‘Widow Maker’ All of which brings us to one of the most pressing questions we get from clients. When a bond is offering a feeble yield, what is the point in owning it? Maybe the best people to answer are the casualties of the now infamous ‘widow maker’ trades. The original widow maker trade was the idea that the yield on the Japanese Government Bond (JGB), at 2 percent, was so feeble that there was no point in owning it. Furthermore, with massive Japanese fiscal stimulus coming down the pike, the ‘no-brainer’ investment strategy was not just to disown the JGBs, but to take an outright short position, as it seemed that the only direction that JGB yields could go was up. In fact, JGB yields did not go up, they continued to trend down. As feeble yields became even feebler, the owners of the short positions got carried out of their careers, feet first. Meanwhile, those investors who owned 30-year JGBs yielding a ‘feeble’ 2 percent in 2013 reaped returns of 75 percent, and even now, are sitting on handsome profits of 55 percent. Some people protest that Japan is an exceptional and isolated case, rather than a template for economies which will not repeat their putative policy-errors. Such protests have always struck us as factually wrong, blinkered, and even prejudiced. Nevertheless, let’s indulge these prejudices with a simple rejoinder – forget Japan, what about Switzerland, or the UK? (Chart I-6) Chart I-6Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Just like the JGB widow maker, anybody who shorted UK gilts yielding 2 percent is nursing heavy losses. Meanwhile, those investors who owned 30-year UK gilts yielding a ‘feeble’ 2 percent in 2018 reaped returns of 40 percent, and even now are sitting on tidy profits of 30 percent. Just like the JGB widow maker, anybody who shorted UK gilts yielding 2 percent is nursing heavy losses. Bear in mind that a 30-year bond yielding a feeble 2 percent will deliver a cumulative return of more than 80 percent to redemption. And that if the feeble yield becomes even feebler, this return will get front-end loaded, creating widow makers for the short positions and spectacular gains for the long positions, as witnessed in JGBs and UK gilts. The 30-Year T-Bond Is A Must-Own Structural Investment The next candidate for the widow maker is shorting the US 30-year T-bond, which is yielding, you guessed it, 2 percent. Remember that while Japan may not be a great template for the US, the UK certainly is – because the US and UK have very similar economic, financial, political, social, and cultural structures. Until recently therefore, bond yields in the US and UK were moving in near-perfect lockstep (Chart I-7). Chart I-7The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

So, what happened? The one word answer is: Brexit. The recent difference between US and UK bond yields is simply that the UK has had one more deflationary shock than the US. Put the other way around, the US is just one deflationary shock away from a UK level of bond yields – meaning the 30-year yield not at 2 percent, but at 1 percent. But why can’t the next shock be an inflationary shock resulting in much higher yields? The simple answer is that the equity risk premium has turned negative for the first time since 2002. Moreover, as we pointed out in The Road To Inflation Ends At Deflation the extremely rich valuation of $300 trillion of global real estate is also highly contingent on ultra-low bond yields. It follows that any significant rise in bond yields will collapse the value of $500 trillion of risk-assets. In a $90 trillion global economy, this will quickly flip any incipient inflationary shock into a deflationary shock. Any significant rise in bond yields will collapse the value of $500 trillion of risk-assets. We conclude that the US 30-year T-bond is a must-own structural investment. Fractal Analysis Update As hospitals have rushed to clear their backlog of non-pandemic treatments and procedures, medical equipment stock prices have surged. This is particularly true for US medical equipment (ticker IHI) which, since June, is up by 25 percent versus US healthcare services (Iqvia, Veeva, or loosely proxied by ticker XHS). Given that the backlog of treatments will eventually clear, and that the intense rally is now extremely fragile on its 65-day fractal structure (Chart I-8), a recommended countertrend trade is to short US medical equipment versus healthcare services. Set the profit target and symmetrical stop-loss at 8.5 percent. Chart I-8The Intense Rally In Medical Equipment Stocks Has Become Fragile

The Intense Rally In Medical Equipment Stocks Has Become Fragile

The Intense Rally In Medical Equipment Stocks Has Become Fragile

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System Fractal Trades 6-Month Recommendations Structural Recommendations Closed Fractal Trades Closed Trades Asset Performance Equity Market Performance Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Chart 1Employment Growth Will Rebound

Employment Growth Will Rebound

Employment Growth Will Rebound

August’s weak employment growth reflects the surge of Delta variant COVID cases in the United States. This is evidenced by the fact that Leisure & Hospitality sector payrolls held flat in August after having grown by 415k in July and 397k in June (Chart 1). While Delta could still be a drag on employment growth for another month or two, there is mounting evidence that the daily new case count is close to its peak. Leisure & Hospitality employment growth will regain its prior pace as new Delta cases trend down. This will lead to a resumption of strong monthly payroll reports (500k – 1000k) as we head into the new year. For monetary policy, we calculate that average monthly nonfarm payroll growth of 414k will be sufficient for the Fed to start rate hikes before the end of 2022 (bottom panel). We anticipate that this threshold will easily be met. The Treasury curve will bear-flatten as employment growth improves and the market prices-in an earlier start and quicker pace of Fed rate hikes. Investors should maintain below-benchmark portfolio duration and stay short the 5-year Treasury note versus a duration-matched 2/10 barbell. Feature Table 1Recommended Portfolio Specification

The Delta Drag

The Delta Drag

Table 2Fixed Income Sector Performance

The Delta Drag

The Delta Drag

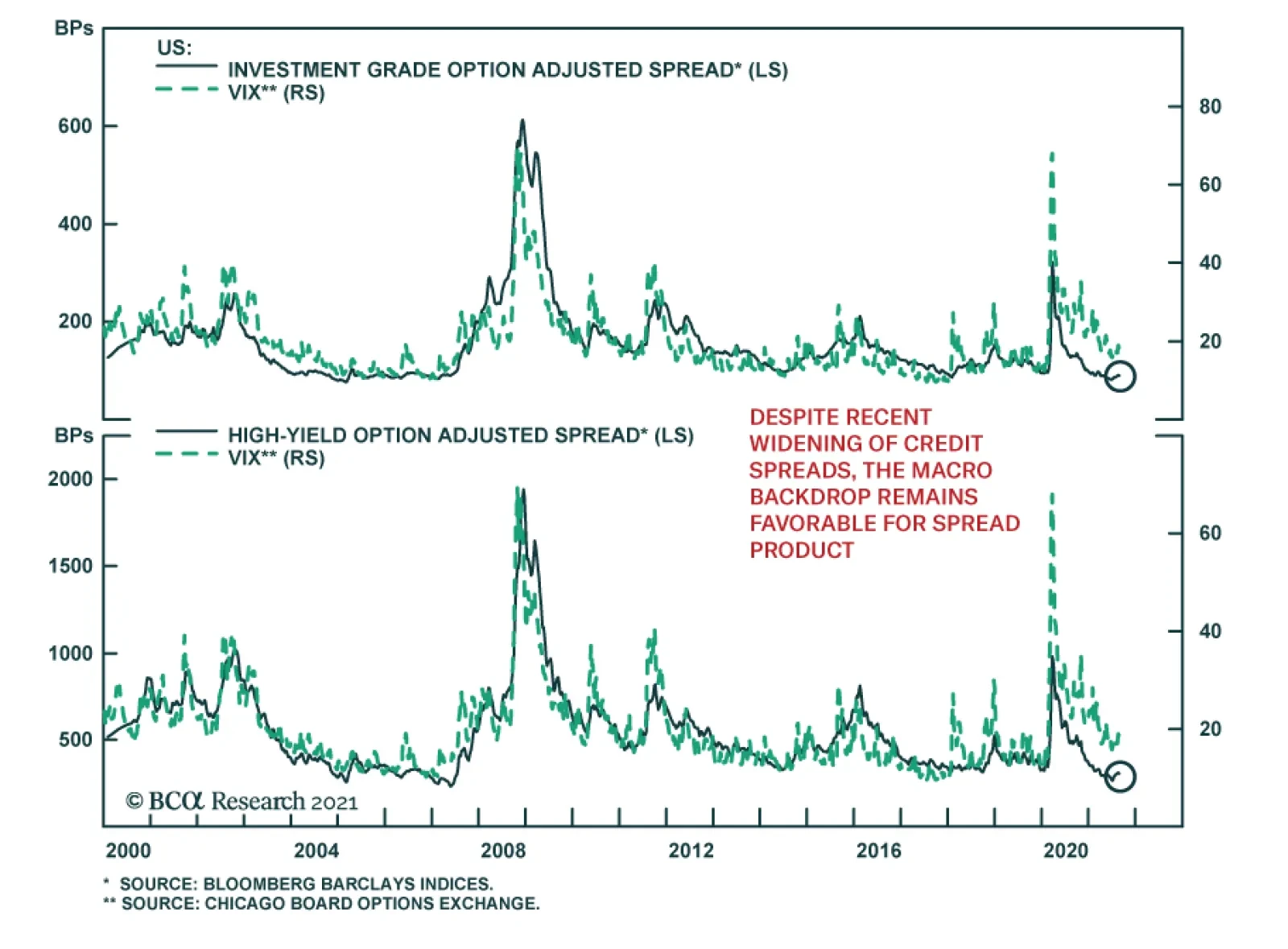

Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds underperformed the duration-equivalent Treasury index by 5 basis points in August, dragging year-to-date excess returns down to +166 bps. The combination of above-trend economic growth and accommodative monetary policy supports continued positive excess returns for spread product versus Treasuries. At 91 bps, the 3-year/10-year Treasury slope remains steep. This is a strong signal that monetary conditions are accommodative. But despite the positive macro back-drop, investment grade valuations are extremely tight (Chart 2). A recent report looked at what different combinations of Treasury slope and corporate spreads have historically signaled for corporate bond excess returns.1 It shows that tight corporate spreads only correlate with negative excess returns once the 3-year/10-year Treasury slope is below 50 bps. Though we retain a positive view of spread product as a whole, better value can be found outside of the investment grade corporate sector. Specifically, we recommend that investors shift into high-yield corporates, municipal bonds and USD-denominated Emerging Market sovereigns and corporates. We also advise investors to favor long-maturity corporate bonds and those corporate sectors with elevated Duration-Times-Spread.2 Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Delta Drag

The Delta Drag

Table 3BCorporate Sector Risk Vs. Reward*

The Delta Drag

The Delta Drag

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 66 basis points in August, bringing year-to-date excess returns up to +502 bps. A recent report looked at the default expectations that are currently priced into the junk index and considered whether they are likely to be met.3 If we demand an excess spread of 100 bps and assume a 40% recovery rate on defaulted debt, then the High-Yield index embeds an expected default rate of 3.0% (Chart 3). Using a model of the 12-month trailing speculative grade default rate that is based on gross corporate leverage (pre-tax profits over total debt) and C&I lending standards, we estimate that the 12-month default rate will fall to between 2.3% and 2.8%, below what the market currently discounts. Notably, the corporate default rate is tracking at an annualized rate of roughly 1.7% through the first seven months of the year, well below the estimate generated by our macro model. Another recent report looked at the incremental spread pick-up investors can earn by moving out of investment grade corporates and into junk.4 It concluded that the extra spread available in high-yield is worth grabbing and that B-rated bonds look particularly attractive in risk-adjusted terms. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 3 basis points in August, dragging year-to-date excess returns down to -67 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries tightened 4 bps in August. The spread is wide compared to recent history, but it remains tight compared to the pace of mortgage refinancings (Chart 4). The conventional 30-year MBS option-adjusted spread (OAS) widened 2 bps in August (panel 2), and it is now starting to look attractive compared to other similarly risky spread sectors. The conventional 30-year MBS OAS sits at 38 bps, below the 56 bps offered by Aa-rated corporate bonds but above the 20 bps offered by Aaa-rated consumer ABS and the 35 bps offered by Agency CMBS. In a recent report we looked at MBS performance and valuation across the coupon stack.5 We noted that the higher convexity of high-coupon MBS makes them likely to outperform lower-coupon MBS in a rising yield environment. Higher coupon MBS also have greater OAS than lower coupons. This makes the high-coupon MBS more likely to outperform in a flat bond yield environment as well. Given our view that bond yields will be higher in 6-12 months, we recommend favoring high coupons (4%, 4.5%) over low coupons (2%, 2.5%, 3%) within an overall underweight allocation to Agency MBS. Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 27 basis points in August, bringing year-to-date excess returns up to +84 bps (Chart 5). Sovereign debt outperformed duration-equivalent Treasuries by 122 bps in August, bringing year-to-date excess returns up to +7 bps. Foreign Agencies outperformed the Treasury benchmark by 8 bps on the month, bringing year-to-date excess returns up to +44 bps. Local Authority bonds outperformed by 9 bps in August, bringing year-to-date excess returns up to +382 bps. Domestic Agency bonds outperformed by 3 bps, bringing year-to-date excess returns up to +30 bps. Supranationals outperformed by 5 bps, bringing year-to-date excess returns up to +31 bps. USD-denominated Emerging Market (EM) Sovereign bonds outperformed US corporates in August and relative valuation between the two sectors is starting to equalize (panel 4). That said, we retain a preference for EM sovereigns over US corporates, particularly the bonds of Russia, Mexico, Saudi Arabia, UAE and Qatar where value remains attractive. A recent report looked at valuation within the investment grade USD-denominated EM corporate space.6 It found that EM corporates are attractively priced relative to US corporate bonds across the entire investment grade credit spectrum. It also found that EM corporates are attractive relative to EM sovereigns within the A and Baa credit tiers. EM sovereigns have the edge in the Aa credit tier. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 9 basis points in August, dragging year-to-date excess returns down to +262 bps (before adjusting for the tax advantage). The economic and policy back-drop remains favorable for municipal bond performance. Trailing 4-quarter net state & local government savings were already positive through the end of Q1 2021 and they received another significant boost in Q2 as funds from the American Rescue Plan were doled out (Chart 6). With state & local government balance sheets in such good shape, we are comfortable moving down in quality within municipal bonds. A move down in quality is especially compelling because of tight Aaa muni valuations relative to Treasuries (top panel). Valuation is more compelling in the lower investment grade credit tiers, especially at the long-end of the curve.7 GO munis in the 12-17 year maturity bucket offer a 5% breakeven tax rate versus corporates with the same credit rating and duration. 12-17 year Revenue munis actually offer a before-tax yield pick-up (panel 2). Finally, high-yield muni spreads are reasonably attractive relative to high-yield corporates, offering a breakeven tax rate of 23% (panel 4). But despite the attractive spread, we recommend only a neutral allocation to high-yield munis versus high-yield corporates as the deep negative convexity of high-yield munis makes them susceptible to extension risk if bond yields rise. Treasury Curve: Buy 2/10 Barbell Versus 5-Year Bullet Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury yields moved higher in August, with the 5-year and 7-year maturities bearing the brunt of the sell-off. The 2-year/10-year Treasury slope steepened 5 bps to end the month at 110 bps. The 5-year/30-year slope flattened 5 bps to end the month at 115 bps. We expect bond yields to be higher in 6-12 months, but we also anticipate that the next significant move higher in bond yields will coincide with curve flattening, not steepening. At 1.93%, the 5-year/5-year forward Treasury yield is not that far below our target fair value range of 2% - 2.25%. In a recent report, we demonstrated that yield curve steepening only occurs when either the Fed is cutting rates or the 5-year/5-year forward yield rises.8 This means that the 2/10 Treasury curve is more likely to flatten than steepen during the next 6-12 months, even as bond yields move higher. Similarly, we observe that the overnight index swap (OIS) curve is priced for the fed funds rate to be 0.21% in one year’s time and 1.47% in five years (Chart 7). The latter rate has 146 bps of upside if it converges all the way back to its 2018 high, but this pales in comparison to the 265 bps of upside in the 12-month forward rate. The yield curve will flatten as the 12-month forward OIS rate converges with the 5-year forward rate (panel 3). Investors should position in yield curve flatteners on a 6-12 month horizon. Specifically, we recommend shorting the 5-year bullet versus a duration-matched 2/10 barbell. TIPS: Neutral Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS performed in line with the duration-equivalent nominal Treasury index in August, leaving year-to-date excess returns unchanged at +578 bps. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates both fell by 7 bps in August. At 2.37%, the 10-year TIPS breakeven inflation rate is near the middle of the 2.3% to 2.5% range that is consistent with inflation expectations being well anchored around the Fed’s target (Chart 8). Meanwhile, at 2.21%, the 5-year/5-year forward TIPS breakeven inflation rate is only just below target (panel 3). With long-dated inflation expectations close to the Fed’s target levels, we see limited upside on a 6-12 month investment horizon. We also see the cost of short-maturity inflation protection falling during the next few months as realized inflation continues to moderate from its current extremely high level. This will lead to some modest steepening of the inflation curve (bottom panel). While the inflation curve has some room to steepen, we don’t see it returning to positive territory. An inverted inflation curve is simply more consistent with the Fed’s Average Inflation Target than a positively sloped one. This is because the Fed’s new framework calls for it to attack its inflation target from above rather than from below. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 3 basis points in August, bringing year-to-date excess returns up to +40 bps. Aaa-rated ABS outperformed by 2 bps on the month, bringing year-to-date excess returns up to +30 bps. Non-Aaa ABS outperformed by 4 bps, bringing year-to-date excess returns up to +92 bps. The stimulus from last year’s CARES Act led to a significant increase in household savings when individual checks were mailed in April 2020. That excess savings has still not been spent and the most recent round of stimulus checks has only added to the stockpile (Chart 9). The extraordinarily large stock of household savings means that the collateral quality of consumer ABS is also extraordinarily high. Indeed, many households have been using their windfalls to pay down consumer debt (bottom panel). Investors should remain overweight consumer ABS and should also take advantage of the high quality of household balance sheets by moving down the quality spectrum. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 6 basis points in August, bringing year-to-date excess returns up to +193 bps. Aaa Non-Agency CMBS outperformed Treasuries by 10 bps in August, bringing year-to-date excess returns up to +92 bps. Non-Aaa Non-Agency CMBS underperformed Treasuries by 9 bps on the month, dragging year-to-date excess returns down to +529 bps (Chart 10). Though returns have been strong and spreads remain attractive, particularly for lower-rated CMBS, we continue to recommend only a neutral allocation to the sector because of the structurally challenging environment for commercial real estate. Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 4 basis points in August, bringing year-to-date excess returns up to +91 bps. The average index option-adjusted spread held flat on the month. It currently sits at 35 bps (bottom panel). Though Agency CMBS spreads have recovered to well below pre-COVID levels, they still look attractive compared to other similarly risky spread products. Stay overweight. Ryan Swift US Bond Strategist rswift@bcaresearch.com Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 12 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 12 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Delta Drag

The Delta Drag

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Footnotes 1 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 2 For ideas on how to increase the average spread of a US bond portfolio please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 3 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 4 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 5 Please see US Bond Strategy Weekly Report, “A New Conundrum”, dated April 20, 2021. 6 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 7 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 8 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “A Bump On The Road To Recovery”, dated July 27, 2021.

Highlights A trio of ECB hawks raised the prospect of an ECB taper. In the past, the current set of economic conditions in the Euro Area would have prompted the ECB to tighten policy. A potential economic deceleration this fall, the transitory nature of the Eurozone’s inflation spike, and the level of inflation expectation in the region limit the ECB’s ability to taper this week. We expect a one-off return to the pre-Q2 2021 level of asset purchases couched in a very dovish forward guidance. Peripheral bonds and European corporate bonds will outperform German and other core European paper. Stay long European curve steepeners, while buying US curve flatteners. Overweight German Bunds versus US Treasury Notes, on a USD-hedged basis. European productivity will remain structurally hampered compared to that of the US. US real bond yields will rise relative to Europe. Feature Last week, a chorus of ECB Governing Council members raised the idea among investors that the central bank may soon begin to taper its asset purchases, which prompted Bund yields to hit -0.35% on Wednesday. Robert Holzmann of Austria, Klaas Knot of the Netherlands, and Jens Weidmann of Germany all suggested that monetary conditions were too accommodative for the Eurozone and that the ECB needed to remedy this problem. The complaints of this hawkish trio reflect the current environment. In August, the Eurozone HICP reached a 3% annual rate while the preliminary estimate for core CPI clicked in at 1.6%. Meanwhile, July PPI rose to 12.1%. Such robust inflation readings are at odds with the low level of interest rates in the Eurozone, where the yields on European IG credit and 10-year Italian BTPs average a paltry 0.45% (Chart 1). Beyond the level of inflation, its broad geographic nature is an additional source of concern. Headline CPI is accelerating across all the bloc’s nations, and it stands above 2% in 82% of the members’ states. Historically, this kind of inflationary backdrop resulted in either higher interest rates or some tapering of asset purchases, especially when economic activity was also improving in the Eurozone (Chart 2). Chart 1A Gap For The Hawks

A Gap For The Hawks

A Gap For The Hawks

Chart 2In The Past, The ECB Would Have Tightened

In The Past, The ECB Would Have Tightened

In The Past, The ECB Would Have Tightened

Will the ECB listen to its most hawkish members and follow its past script? We do not believe that the Governing Council is about to start a sustained period of decreased bond buying, even if a return to the pre-Q2 2021 pace of buying is likely this fall. Thus, a dovish taper is the most likely outcome of this week’s meeting. The ECB’s Three Constraints The outlook for growth, the temporary nature of the current spike in European inflation, and the low-level of Euro Area inflation expectations limit the ECB’s ability to remove monetary accommodation. First, European economic growth is at its apex and will decelerate over the next six months. Currently, domestic activity as approximated by the Services PMI stands at near a 15-year high of almost 60. Moreover, despite the spike in COVD-19 cases linked to the Delta variant, mobility remains very robust. If anything, the decline in cases in Spain and France should lead to further improvement in mobility (Chart 3). Nonetheless, the recent fall in consumer confidence and the recent US experience, which the European economy usually follows, point to a deceleration in the Services PMI. The case for a decline in manufacturing activity is more pronounced. The European manufacturing sector responds strongly to the fluctuation of the global industrial sector. US consumer spending on durable goods is 21% above its pre-pandemic trend and is beginning to weaken as pent-up demand for such products has been satiated and households shift their spending back toward services. Moreover, the Chinese credit cycle, which leads the Eurozone Manufacturing PMI by nine months, indicates a greater deceleration in the coming quarters, because European exports to China will slow (Chart 4, top and middle panels). In response to these two forces, Europe will not diverge from the deterioration in our Global Activity Nowcast (Chart 4, bottom panel). Chart 3So Far, No Delta Impact

So Far, No Delta Impact

So Far, No Delta Impact

Chart 4The Coming Manufacturing Slowdown

The Coming Manufacturing Slowdown

The Coming Manufacturing Slowdown

Chart 5Abnormal Goods Inflation

Abnormal Goods Inflation

Abnormal Goods Inflation

Second, most evidence still suggests that the current inflation increase will be temporary, despite its violence. To begin with, the spike in inflation remains consigned to the goods sectors, while services inflation stands at 1.1%, in line with the experience of the past 10 years (Chart 5). Even within goods prices, the spike in CPI is limited to sectors facing bottlenecks or linked closely to commodity and shipping prices. As Chart 6 illustrates, the categories experiencing abnormal inflation are directly related to higher energy prices, cars, complex machinery, hotels, and fresh food. Meanwhile, underlying inflation as estimated by our trimmed-mean CPI measure is bottoming, but remains at a very low 0.2% annual rate (Chart 7). Chart 6Inflation Remains A Commodity and Bottleneck Story

The ECB Taper Dilemma

The ECB Taper Dilemma

In the same vein, the surge in Selling Price Expectations of the European Commission Business Survey is a function of commodity inflation (Chart 8). In other words, companies feel they can increase their selling prices, because natural resource prices have spiked. However, inflation across many commodities is currently peaking, which suggests that Selling Price Expectations will soon do so as well. Moreover, this process indicates that headline inflation should hit its summit by year end, because Selling Price Expectations are a coincident indicator of inflation (Chart 8, bottom panel). Chart 7Narrow Inflation

Narrow Inflation

Narrow Inflation

Chart 8Rising Selling Prices And Commodities

Rising Selling Prices And Commodities

Rising Selling Prices And Commodities

A wage-inflation spiral also remains far away. Historically, rapidly accelerating wage growth marked periods of elevated inflation. Despite current fears, such a development is not taking place in the Eurozone. For the whole bloc, negotiated wages are growing at a modest 1.7% annual rate (Chart 9). Even in Germany, negotiated wages are only increasing at the same rate. While some labor shortages have been reported, total hours worked remain below the equilibrium level based on the Euro Area demographic profile (Chart 9, bottom panel). Furthermore, the past ten years reveal that labor shortages only caused stronger salary growth with a multi-year delay. Third, the market doubts the credibility of the ECB when it comes to achieving a 2% inflation target. So far, survey-based inflation expectations remain below 2% at all tenors (Chart 10, top panel). The same is true of market-based measures, which are still lower than the levels that prevailed before the sovereign debt crisis of the past decade (Chart 10, bottom panel). Chart 9No Wages/Inflation Spiral

No Wages/Inflation Spiral

No Wages/Inflation Spiral

Chart 10The ECB's Inflation Mandate Is Not Yet Credible

The ECB's Inflation Mandate Is Not Yet Credible

The ECB's Inflation Mandate Is Not Yet Credible

Bottom Line: Risks to growth over the winter, the transitory nature of the recent inflation shock, and inflation expectations that remain significantly below target are constraints limitating the ability of the ECB to announce a true tapering of its asset purchases this Thursday. A Dovish Taper? Considering the current set of conditions prevailing in the Eurozone, we expect the ECB to announce a return to the pace of asset purchases that existed prior to Q2 2021. However, the Governing Council (GC) will go out of its way to issue clear forward guidance that strongly indicates this is not the beginning of a taper campaign. Instead, the GC will hint at the transmutation of a large proportion of the PEPP monthly buying into the PSPP after March 2022. The inflation target change enacted at the conclusion of the ECB’s strategy review in July limits the central bank’s ability to go back to its old rule book and tighten policy at the first hint of inflation. First, the ECB must believe that inflation will overshoot 2% on a durable basis, which will necessitate an upgrade to its long-term inflation forecast above the target. Too many members of the GC do not share this view, which makes it unlikely that inflation forecasts will rise this much this week. Moreover, inflation expectations are also too low to warn of a meaningful change in the behavior of European economic agents, especially if the current spike in inflation proves to be transitory. Another problem for the ECB is the Fed. If the ECB were to announce a durable tapering of its asset purchase this week, it would be doing so ahead of the Fed. The GC fears that this action would put considerable upward pressure on EUR/USD, which would create a grave deflationary tendency in the Eurozone (Chart 11). Despite these shackles, the ECB will also acknowledge that the current emergency pace of asset purchases is no longer warranted. Starting Q2 2021, the ECB increased its average monthly purchase from EUR80 billion in the August 2020 to March 2021 period, to EUR95 billion since April 2021 (Chart 12). However, these increased purchases followed a 0.1% GDP contraction in Q1 in the wake of a spike in COVID-19 cases and deaths, which prompted a large reduction in mobility. Moreover, the larger bond buying also followed large increases in bond yields across the main economies of the continent, a rise which, if it had been left unchecked, would have exacerbated the economic malaise. Chart 11The ECB Fears A Strong Euro

The ECB Fears A Strong Euro

The ECB Fears A Strong Euro

Chart 12Normalizing Purchases

The ECB Taper Dilemma

The ECB Taper Dilemma

None of these factors are still present. The increasing level of vaccination has dulled the economic impact of the third wave of infection. The economy is expanding robustly and, even if it slows in the months ahead, growth will remain well above trend. Crucially, financial conditions are much more generous than in the first half of the year, with a euro that trades 4% below its January peak and with yields in the bloc’s four largest economies 25 to 45 basis points below their spring peaks. Bottom Line: In response to the aforementioned crosscurrents, we anticipate the ECB to announce a return of its monthly asset purchases to the level that prevailed in the August 2020 to March 2021 period. However, the GC will also clearly indicate, as it did last March, that this policy shift is a one-off, and that investors must not anticipate any further curtailment of asset purchases over the next six months. To reinforce this guidance, we expect the ECB’s inflation forecast to show a return of HICP below 2% by the end of 2023. The GC might also hint at the roll-over of the PEPP program into the PSPP after March 2022. Investment Implications An ECB that conducts a dovish taper on Thursday will support our main fixed-income themes in Europe. First, it will remain a tailwind behind an overweight position in peripheral government bonds versus German bonds. The combination of continued purchases of EUR80 billion a month of bonds over the foreseeable future, above-trend growth, and the fiscal risk mutualization from the NGEU and REACT EU programs means that investors can continue to safely pocket the yield premium offered by BTPs and BONOs. Moreover, our geopolitical strategists expect a left-wing coalition to govern Germany after the September 26 election, which will limit the pressures to tighten budgets in the periphery over the coming years. Chart 13European Corporates Remain Attractive

European Corporates Remain Attractive

European Corporates Remain Attractive

Second, continued liquidity injections by the ECB are also consistent with a preference for European corporate credit over government securities, especially in Germany, France, and the Netherlands. European breakeven spreads for IG and high-yield debts are in the 18th and 13th percentile rank, respectively (Chart 13). Easy monetary conditions and above-trend growth will facilitate further yield-seeking behavior in the Eurozone. This process will allow these securities to offer continued excess returns over at least the next six months. Third, we hold on to our box trade of being long Eurozone curve steepeners and long US curve flatteners. In our base case scenario, the Fed will soon indicate the beginning of its tapering campaign and will be on track to raise rates by early 2023, while the ECB will still conduct a very easy monetary policy. In this context, the US yield curve will flatten relative to the European one, driven by a more rapid increase at the short end of the curve. Chart 14Still Favor Bunds Over T-Notes

The ECB Taper Dilemma

The ECB Taper Dilemma

Finally, in a global bond portfolio, it still makes sense to overweight German Bunds (hedged into USD) relative to US Treasury Notes. Bunds display a significantly lower yield beta than their US counterparts, which creates an attractive defensive feature in an environment in which global yields are likely to rise. Moreover, as the model in Chart 14 highlights, the US/German 10-year yield spread is roughly 50bps below an equilibrium estimate based on relative inflation, unemployment and policy rates, and the size of the Fed and ECB balance sheets. US inflation is likely to remain perkier than that of Europe over the coming quarters, and the US unemployment rate will decline faster as well. Additionally, in the unlikely scenario that the Fed declines to taper its purchases this year, but the ECB does, inflation expectations will rise in the US relative to the Euro Area, which will put upward pressure on yield spreads. Bottom Line: A dovish ECB taper, whereby the GC executes a one-off adjustment in asset purchases with an easy forward guidance, will support our overweight in peripheral government bonds relative to bunds, our preference for European corporate credit relative to government paper, our Europe / US box trade, and BCA’s underweight in Treasurys relative to Bunds. Europe’s Productivity Deficit Is Not Over Compared to the US, GDP growth in the Eurozone has been trending lower since the introduction of the euro in 1999. While a weaker demographic profile has hurt Europe, so has slower productivity growth. Going forward, the gap between European and US productivity growth will somewhat narrow compared to last decade, but it will still favor the US. The cross-Atlantic gap in output per hour growth between has a cyclical and a structural component. The cyclical element is set to ebb. Last decade, the Eurozone suffered a double-dip recession, as the European sovereign debt crisis raged. As a result, capex and debt accumulation in Europe lagged that of the US, which hurt demand and, thus, output-per-hour worked (Chart 15, top panel). Going forward, the European debt crisis has been addressed, the ECB has demonstrated its willingness to do “whatever it takes” to support the monetary union and both the European Commission and the German government have thrown their full weight behind the integrity of Europe, even if it means bailing out their profligate southern neighbors. Despite this positive, some structural headwinds will continue to handicap European productivity. Since 2000, total factor productivity in the major Euro Area economies has lagged that of the US (Chart 15, bottom panel). Many factors suggest this will not change: Chart 15Europe’s Productivity Deficit

The ECB Taper Dilemma

The ECB Taper Dilemma

The Eurozone’s big four economies continue to linger well behind the US in terms of ICT investment, which in recent decades has been a crucial driver of productivity. R&D represents a significantly lower share of GDP in the Eurozone than it does in the US (Chart 16). More investment in intangible assets has been linked to higher productivity growth. Additionally, Ortega-Argilés et al. have shown that EU companies do not convert R&D into productivity gains as well as US businesses do, because they generate lower return on investments.1 Confirming this insight, an empirical study using microdata on R&D spending for EU and US firms highlights that both R&D intensity and productivity are lower for EU firms than for their US counterparts.2 For a 10% increase in R&D intensity, US businesses generated a 2.7% increase in productivity, while EU firms enjoyed a much smaller 1% gain. The gap is larger for high-tech companies, where the same rise in R&D intensity produced a 3.3% productivity gain in the US, but only a 1.2% one in the EU. The European economy remains much more fragmented than that of the US, and the greater prevalence of small firms in the Euro Area results in a less efficient use of the human and capital stocks. Finally, the low rate of investments in recent years has caused the European capital stock to age faster than that of the US. An older pool of assets is further away from the technological frontier and thus weighs on TFP and overall labor productivity (Chart 17). Chart 16Lagging European R&D

The ECB Taper Dilemma

The ECB Taper Dilemma

Chart 17The Ageing European Capital Stock

The Ageing European Capital Stock

The Ageing European Capital Stock

Notwithstanding cyclical fluctuations related to the global debt cycle, the Eurozone profit margins and RoEs will not converge meaningfully toward US levels on a structural basis because of this productivity problem. Europe’s lower industry concentration ratios, lower markups, and greater share of output absorbed by wages will only accentuate this problem. Chart 18TIPS Yields Vs Real Bunds

TIPS Yields Vs Real Bunds

TIPS Yields Vs Real Bunds

As a result of the lower trend growth rate caused by lower productivity and its inferior return on invested capital, Europe’s R-Star is unlikely to catch up meaningfully to US levels. Consequently, the gap between US and Germany real rates will remain wide and will drive the increase in US yields relative to those of Germany, as the Fed begins to tighten policy while the ECB stands pat (Chart 18). Bottom Line: Europe’s productivity deficit is not the only consequence of last decade’s sovereign debt crisis. Thus, the Euro Area’s potential GDP growth and return on invested capital will lingers behind those of the US. As a corollary, the Eurozone’s R-star is well below that of the US. Hence, we expect higher real rates to drive the increase in US yields over Germany as the Fed tightens policy ahead of the ECB. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Footnotes 1R. Ortega-Argilés, M. Piva, and M. Vivarelli, “The Transatlantic Productivity Gap: Is R&D the Main Culprit?,” Canadian Journal of Economics 47.4 (2014), pp. 1342-71. 2D. Castellani, M. Piva, T. Schubert, and M. Vivarelli, “The Productivity Impact of R&D Investment: A Comparison between the EU and the US,” IZA Discussion Papers 9937 (2016). Tactical Recommendations

The ECB Taper Dilemma

The ECB Taper Dilemma

Cyclical Recommendations

The ECB Taper Dilemma

The ECB Taper Dilemma

Structural Recommendations

The ECB Taper Dilemma

The ECB Taper Dilemma

Closed Trades

The ECB Taper Dilemma

The ECB Taper Dilemma

Currency Performance Fixed Income Performance Equity Performance

Highlights Jackson Hole: The message from Jackson Hole is that the majority of the FOMC – including Fed Chair Powell - is ready to begin tapering asset purchases before year-end. There is less unanimity within the FOMC over the timing of interest rate increases following the taper. Fed Policy: The Fed is trying to communicate a separation of the balance sheet and interest rate components of its monetary policy, hoping to limit bond volatility stemming from markets pulling forward the timing of rate hikes during the taper. A tightening US labor market will make that separation difficult given the shallow path for interest rates currently discounted in the US yield curve - particularly if the current surge in US inflation proves not to be as transitory as the Fed is expecting. US Treasury Yields: Expect higher Treasury yields over the next 12-18 months as the Fed transitions from talking about tapering to actual tapering and, eventually, to rate hikes starting in H2/2022. A September To Remember? Chart 1The Fed Faces Some Tough Decisions

The Fed Faces Some Tough Decisions

The Fed Faces Some Tough Decisions

The much anticipated Jackson Hole speech from Fed Chair Jerome Powell offered a balanced tone.1 Powell did say that the Fed could begin tapering asset purchases by the end of this year, given the “substantial further progress” on the Fed’s 2% average inflation goal, if the US economy evolved in line with the Fed’s forecasts. However, Powell also noted that rate hikes would not occur without greater improvements in the US labor market, particularly given the Fed’s view that the current surge in US inflation will not prove lasting. Several other Fed officials speaking to the media before Powell’s speech hinted at a much more accelerated timetable, with tapering to begin in September and rate hikes potentially starting as soon as mid-2022. The Fed’s messaging is part of an extended conversation with financial markets to prepare for a withdrawal of pandemic-era policy stimulus from quantitative easing (QE). The FOMC is well aware that valuations on asset prices of all stripes have been boosted by loose monetary settings. Powell’s Jackson Hole comments were more nuanced than those of his FOMC colleagues, but this is no surprise as the words of the Fed Chair carry the greatest weight among investors. The Fed Chair does not want to risk a repeat of the 2013 Taper Tantrum in Treasury yields, or the December 2018 plunge in US equity prices, by sounding unexpectedly hawkish and triggering a market rout that tightens US financial conditions (Chart 1). Our baseline assumption has been that the Fed would signal a tapering at the December FOMC meeting and begin to slow asset purchases in January 2022, leading to an eventual liftoff of the fed funds rate by the end of next year. The comments from Powell and others have raised the risk that the Fed moves a bit faster than our expectations on tapering, and perhaps even for liftoff (Chart 2). This would also be faster than the expectations among bond investors. Chart 2The Fed May Be Set To Move Faster Than Our Expected Timeline

The Fed’s Separation Anxiety

The Fed’s Separation Anxiety

The New York Fed’s Survey of Primary Dealers in July showed that tapering is expected by Q1 of next year but a rate hike was not projected until the latter half of 2023 (Table 1). Current pricing in the US overnight index swap (OIS) forward curve is a bit more hawkish than that, with a full 25bp rate hike discounted by January 2023. Table 1Primary Dealers Expect A Taper, Not Rate Hikes

The Fed’s Separation Anxiety

The Fed’s Separation Anxiety

The Fed’s next move will depend on how the questions regarding the Delta variant, the true state of the US labor market and underlying US inflation momentum are resolved. Dismissing The Delta Threat? There has been a clear hit to US economic confidence from the spread of the variant. The August readings from the University of Michigan consumer sentiment survey, the Philadelphia Fed business outlook survey and the ZEW survey of US growth expectations all showed sharp declines (Chart 3). The August flash estimate of the Markit PMIs fell to 8-month and 4-month lows, respectively, indicating that the pace of US economic activity slowed. Higher frequency data like restaurant reservations and hotel bookings have also dipped in recent weeks, potentially a sign of US consumers turning more cautious on leaving home during the Delta surge. Yet there is some tentative positive news on the spread of the variant. The 7-day moving average of new COVID-19 cases in the US appears to be rolling over (Chart 4). In the more stricken states in the US south like Florida, Texas and Louisiana, the effective reproduction number has fallen below one and cases are clearly peaking, suggesting that the transmission of Delta is slowing. If these trends continue, the full hit to US growth from the variant could prove to be minimal and potentially contained to only August data Chart 3A Hit To US Confidence From The Delta Variant

A Hit To US Confidence From The Delta Variant

A Hit To US Confidence From The Delta Variant

Chart 4Has The US Delta Wave ##br##Peaked?

Has The US Delta Wave Peaked?

Has The US Delta Wave Peaked?

Fed officials have been highlighting Delta as a potential near-term risk to the economy, but some comments made last week suggested only a modest level of concern that would not derail tapering plans. For example: Dallas Fed President Robert Kaplan: “[…] what I'm seeing is, in certain sectors, as you would expect, travel-related, you're seeing weakness in some other sectors but by and large, predominantly, what we're seeing is resilience across the indicators that we look at.”2 Kansas City Fed President Esther George: “[…] by and large, I think, unlike what we experienced last year, people have mechanisms to continue to interact with the economy in a way that we didn't before. And so that gives me some confidence in the outlook that we see, that we could continue to push through this.”3 Atlanta Fed President Raphael Bostic: “What I have seen is some suggestion that things are slowing down, but they are still just slowing from extremely high levels. I have not seen big changes in the underlying dynamic.”4 Even Powell himself noted in his speech that “while the Delta variant presents a near-term risk, the prospects are good for continued progress toward maximum employment.” If the hit to the domestic US economy from Delta proves to be modest and short-lived, the Fed will want to see confirmation of this in the US employment data. Labor market slack overestimated? It is clear from other comments made last week that FOMC officials will be watching the August payrolls report very closely, especially given the perception that the US job market may be a lot tighter than the headline unemployment rate suggests. For example, Fed Governor Christopher Waller noted that “when you adjust the labor force for early retirements, if we get another million [jobs in August] we will recover about 85% of the jobs that were lost and that took almost seven years after the last recession.”5 Kaplan noted that “we do think that the labor market is much tighter than the headline statistics indicate. We've had 3 million retirements since February 2020.” Our colleagues at BCA Research’s The Bank Credit Analyst came to a similar conclusion on labor market tightness in a report published last week.6 They determined that the single largest factor driving the US labor force participation rate lower since the onset of the pandemic has been individuals choosing to retire (Chart 5). Only some of that decline has been related to early retirement decisions made in response to COVID. There has been a structural trend of a falling participation rate, by an average of 0.3 percentage points per year, since 2008 due to demographic factors. The labor force participation rate does not need to fully return to pre-pandemic levels for the Fed to conclude that its maximum employment goal has been reached, after accounting for retirements and other demographic shifts (Chart 6). This fits with the comments from Waller and Kaplan indicating that there has likely been enough labor market improvement to begin tapering asset purchases. Chart 5Most Of The Pandemic Decline In Labor Force Participation Has Occurred Due To Retirement

The Fed’s Separation Anxiety

The Fed’s Separation Anxiety

Chart 6Full Employment Without A Pre-COVID Participation Rate

Full Employment Without A Pre-COVID Participation Rate

Full Employment Without A Pre-COVID Participation Rate

Transitory or persistent inflation? In his Jackson Hole speech, Fed Chair Powell downplayed many of the factors that have driven US headline inflation higher in 2021 as “[…] the product of a relatively narrow group of goods and services that have been directly affected by the pandemic and the reopening of the economy.” He also noted that the current surge in durable goods inflation, which has contributed “about one percentage point to the 12-month measures of headline and core inflation”, was likely to end once current supply chain disruptions fade. Durables would then return to the deflationary trend of the past 25 years and help cool off current overheated US inflation. Chart 7US Inflation Is Not Slowing Down

US Inflation Is Not Slowing Down

US Inflation Is Not Slowing Down

Powell also noted the absence of significant US wage growth as reason not to be overly worried about a sustained period of high inflation. He also highlighted that “there is little reason to think” that ongoing structural disinflationary forces like technology and globalization “have suddenly reversed or abated” and that “it seems more likely that they will continue to weigh on inflation as the pandemic passes into history.” This is the message that the Fed has consistently communicated over the past several months, that high inflation was merely “transitory” and the inevitable result of year-over-year base effect comparisons and temporary supply squeezes. The problem with this interpretation is that we are now well into the summer months of 2021, past the period where base effects would be expected to boost US year-over-year inflation rates (the level of both the CPI and PCE deflator indices fell between January and May 2020 before starting to climb again in June). The July 2021 readings on annual headline and core PCE inflation were 4.2% and 3.6%, respectively, the highest rates seen since 1991 (Chart 7, top panel). The year-over-year increase appears to have been concentrated in a few components, with the Dallas Fed’s trimmed mean PCE 12-month inflation for July only climbing to 2.0%. However, the 6-month annualized measure was a more rapid 2.6% - the fastest such pace in 13 years - suggesting that the momentum of US inflation is both broadening and accelerating on the margin (second panel). Chart 8A Sustainable, Not Transitory, Rise In Global Inflation

A Sustainable, Not Transitory, Rise In Global Inflation

A Sustainable, Not Transitory, Rise In Global Inflation

Powell, like many other developed market central bankers, is making a big bet that the “transitory” inflation narrative will prove to be correct and the current surge in inflation will soon subside. Yet already, global supply chain disruptions have lingered longer than the Fed has been expecting. There are also deeper underlying trends in inflation that are challenging the “transitory” narrative. The NFIB small business survey showed that a net 52% of respondents reported raising selling prices in July, while a net 44% planned future price hikes (third panel), both readings last seen during the days of double-digit US inflation in the late 1970s. US firms are successfully passing on rising input costs to US consumers, which is influencing US consumer inflation expectations. The University of Michigan consumer survey for August showed that US households expect inflation over the next year of 4.6% and over the next 5-10 years of 2.9%, with both series well above pre-pandemic lows (bottom panel). The trends in higher inflation seen in the US, and elsewhere, are not just limited to commodity prices where supply squeezes were most prevalent earlier this year and where price momentum is peaking (Chart 8). A GDP-weighted average of core inflation rates for 14 developed market economies reached 2.50% in June and 2.4% in July, levels last seen in the mid-1990s. Higher core inflation readings are consistent with intensifying price pressures stemming from diminished economic slack. The broad swings in our global core inflation measure correlate strongly with the IMF’s estimate of the output gap for the advanced economies (bottom panel). The current acceleration in global core inflation is entirely consistent with the rapid narrowing of the global output gap projected by the IMF for 2021 and, more importantly, 2022. This suggests that underlying inflation pressures, both within and outside the US, will linger into next year, providing an offset the expected drag on “non-core” inflation from slowing commodity price momentum. Already, lingering supply squeezes and stubbornly high US inflation are causing concern among some FOMC members, as noted in these comments last week: Robert Kaplan: “[…] headline PCE inflation next year, we think is going to be in the neighborhood of 2.5%, and there's risk that could be higher. And so we think some of these supply-demand imbalances for materials, some of them will not moderate, but some of them are going to persist longer than people think.” Esther George: “[…] if you continue to have supply constraints and strong demand, you might expect that those will persist more through this year or longer than we originally anticipated.” Chris Waller: “I do think it’s going to be more persistent than I may have thought back in May.” Chart 9Fed Tapering To Deal With Financial Stability Risks?

Fed Tapering To Deal With Financial Stability Risks?

Fed Tapering To Deal With Financial Stability Risks?

Importantly, the senior FOMC leadership - Powell, Lael Brainard, Richard Clarida – has been sticking with the “transitory” narrative. However, even Clarida noted in a speech in early August that he would consider core PCE inflation at or above 3% at year-end to be “much more than a “moderate” overshoot” of the Fed’s 2% inflation objective.7 In his role as Fed Chair, Powell must speak on behalf of the entire FOMC, even if those views are not necessarily his own. Given the growing chorus of Fed voices expressing concern that US inflation could remain higher for longer, it will be increasingly difficult for Powell to do what he did at Jackson Hole – sound more dovish than the individual FOMC members with regards to inflation risks. What about financial stability risks from QE? Fed officials have been understandably cautious in their comments about how QE (and a 0% funds rate) could be influencing asset prices (Chart 9). However, with equity markets at record highs, corporate bond yields near record lows despite high levels of corporate leverage, and US house prices soaring – the S&P CoreLogic Case-Shiller national index rose 18.6% on a year-over-year basis in June, the fastest pace in its 35-year history - it is difficult not to see the role of the Fed’s easy money policies in boosting risk seeking, yield chasing activities. Stimulative financial conditions are also creating future upside growth risks, with the Conference Board leading economic indicator now reaccelerating (bottom panel). Robert Kaplan, Boston Fed President Eric Rosengren and St. Louis Fed President James Bullard have voiced concerns that QE, particularly the Fed’s buying of agency mortgage-backed securities (MBS), have played a significant role in the current US housing boom. The senior FOMC leadership has avoided any such comments for obvious reasons – imagine the market reaction if Powell expressed concerns about high house prices or equity market valuations. However, for those at the Fed already looking to begin tapering sooner, booming asset prices are an additional reason to vote that way as soon as the September FOMC meeting. Separating Tapering From Rate Hikes It seems clear that the majority of the FOMC is now leaning towards starting to taper before year-end, if US growth and employment maintain recent strength. The common message of Fed officials, from Powell on down, is that enough progress has been made on the Fed’s 2% average inflation target objective to justify tapering. Market-based inflation expectations from the TIPS and CPI swap markets are consistent with that interpretation, with breakevens and forward inflation rates within the 2.3-2.5% range consistent with the Fed’s 2% inflation mandate (Chart 10). Yet while our Fed Monitor continues to flag the need for tighter US monetary policy, only 100bps of rate hikes are discounted in the US OIS curve by the end of 2024 – and only after a first rate hike not expected to occur until January 2023. Despite the common messaging on the start of the taper, the Fed voices were singing a bit less in harmony about the potential timing of the first interest rate hike post-taper. Powell went out of his way to note in his Jackson Hole speech that “the timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test.” That test, of course, is when the Fed deems that its maximum employment objective has been reached. Can the Fed continue to successfully separate guidance on balance sheet decisions from guidance on future interest rate moves? Current pricing from US OIS and CPI swap forward curves indicates that the market is discounting negative real policy rates, with the Fed never raising rates above inflation, for the next decade (Chart 11). This goes a long way to explain the persistence of negative real US Treasury yields at a time of elevated inflation readings. Although a decade of negative real interest rates is also consistent with the market believing the equilibrium real interest rate (i.e. r-star) is negative – a view currently expressed by no one on the FOMC. Chart 10Too Few Rate Hikes Discounted In The US OIS Curve

Too Few Rate Hikes Discounted In The US OIS Curve

Too Few Rate Hikes Discounted In The US OIS Curve

Chart 11Markets Believe The Fed Will Never Raise Rates Above Inflation

Markets Believe The Fed Will Never Raise Rates Above Inflation

Markets Believe The Fed Will Never Raise Rates Above Inflation

That persistent pricing of negative real rates make sense when there is modest headline inflation and ample spare capacity in the US economy and labor markets. However, that complacency on future rate hikes will be shaken if the US economy approaches full employment and inflation remains above the Fed’s 2% target – outcomes that we expect to occur by the second half of next year. That will lead to the first fed rate hike of the next cycle in Q4 2022, but only after the taper that we expect to start in either December 2021 or January 2022 is completed in Q3 2022. Bottom Line: A tightening US labor market will make the Fed’s current guidance on the separation of tapering from rate hikes increasingly unconvincing, given the shallow path for interest rates currently discounted in the US yield curve - particularly if the current surge in US inflation proves not to be as transitory as the Fed is expecting. Jackson Hole Investment Conclusion – Expect Higher US Treasury Yields Chart 12Stay Below-Benchmark On US Duration

Stay Below-Benchmark On US Duration

Stay Below-Benchmark On US Duration

With such a modest path for future rate hikes, and bond yields, discounted in US forward interest rate curves, we continue to advocate positioning for higher US Treasury yields on a strategic (6-18 months) basis (Chart 12). We see the benchmark 10-year Treasury yield eventually reaching a peak in the 2-2.25% range by the end of 2022. We recommend maintaining a below-benchmark duration stance in the US, while staying underweight US Treasuries in US and global bond portfolios. There is even a case to be made for a more tactical (i.e. shorter-term) bearish stance on US Treasuries with the US data surprise cycle set to turn towards upside surprises, especially if the negative impact of the Delta variant on confidence and spending begins to wane as case numbers start to decline in the coming weeks. Bottom Line: Expect higher Treasury yields over the next 12-18 months as the Fed transitions from talking about tapering to actual tapering and, eventually, to rate hikes starting in H2/2022. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 A transcript of Powell’s speech can be found here: https://www.federalreserve.gov/newsevents/speech/powell20210827a.htm 2 https://finance.yahoo.com/news/dallas-fed-president-robert-kaplan-yahoo-finance-transcript-august-2021-215700082.html 3 https://finance.yahoo.com/news/kansas-city-fed-president-esther-george-yahoo-finance-transcript-august-2021-113024734.html 4 https://www.reuters.com/business/exclusive-feds-bostic-says-reasonable-begin-bond-buying-taper-october-2021-08-27/ 5 https://finance.yahoo.com/news/fed-gov-waller-strong-august-jobs-report-will-be-green-light-for-taper-202340105.html 6 Please see BCA Research The Bank Credit Analyst September 2021 Section II, “The Return To Maximum Employment: It May Be Faster Than You Think”, available at bca.bcaresearch.com 7 https://www.federalreserve.gov/newsevents/speech/clarida20210804a.htm Recommendations Duration Regional Allocation Spread Product Yields & Returns Global Bond Yields Historical Returns

Highlights We are reviewing our recommendations. We are also introducing recommendation tables to monitor these positions. Overall, our main recommendations have generated alpha and have a positive batting average. Feature The end of the month of August offers an opportunity to review the positions recommended in this publication. We introduce three tables corresponding to three investment horizons—tactical, cyclical, and structural—which summarize our main views. Each table is subdivided by asset class, namely equities, fixed income, and currencies. The tables can be found on page 12 and 13 and will be available at the end of future strategy reports. Tactical Recommendations Short Equity Leaders / Long Laggards This position is down 1.4% since inception. The idea behind this bet was that the easy money in the market had been made, and investors needed to become more discerning, although the big-picture economic backdrop continued to favor a pro-cyclical, pro-risk bias in a portfolio. To achieve this goal, we opted to buy cyclicals sectors that had lagged the broad market and to sell the ones that had already overtaken their pre-COVID highs, in the hope of creating a portfolio hedge. Practically, this meant buying sectors such as Industrials, Banks and Energy, while selling sectors such as Capital goods, Autos and Consumer services (Chart 1). This position has not worked out well as yields fell. Chart 1Leaders vs Laggards

The Road So Far

The Road So Far

UK Mid-Cap And Small-Cap To Outperform This position is up 3.4% since inception. We initially favored the more domestically-oriented mid- and small-cap indices in the UK as a bet on the re-opening trade, following the lead taken by the UK in the global vaccination campaign. A faster re-opening would not only boost the ability of smaller domestic firms to generate cash flows, it would also elevate the pound, which would hurt the profit translation of the multinational dominating the UK large-cap indices. By mid-May, we opted to move small cap back to neutral, as the positive story was well discounted and we expected the GBP to correct, which would help large-cap stocks. Favor European Banks Relative To US Ones This position is up 4.1% since inception. It is mainly a value trade. The European economy has lagged behind that of the US, and European yields remain well below US ones. As a result, European financials have greatly underperformed their US counterparts. However, this performance differential has left European banks trading at an enormous discount relative to their US peers. Hence, as continental European economies were catching up to the US on the vaccination front, we expected European banks to regain some ground. This trade has further to go, as valuation differentials remain excessive, especially since European banks are not as risky as they once were. Underweight / Short Norway As Hedge To Swedish Stocks This position is down 1% since inception. We have a cyclical overweight on the Swedish equity market (see page 9), which is extremely sensitive to the global industrial cycle. Thus, we were concerned by the potential near-term impact of the Chinese credit slowdown on this position. Selling Norway remains an appropriate hedge, because this market massively overweight materials stocks, which are even more exposed to the Chinese credit cycle than industrials are. Positive European Small-Cap Stocks This position is up 0.2% since inception. This was a bet on the economic re-opening taking place in the wake of the accelerating pace of vaccination in Europe. However, the weakness in the Euro since May has caused the large-cap European stocks to perform almost as well as their more-domestically focused counterparts. Neutral Stance On Cyclicals Relative To Defensives Chart 2The Cause Of Our Cautious Tactical Stance

The Cause Of Our Cautious Tactical Stance

The Cause Of Our Cautious Tactical Stance

This trade is up 2.3% since inception. While we like cyclical plays on an eighteen to twenty-four months basis, we became concerned this spring about a tactical pullback. Globally, cyclical stocks had become extremely expensive and overbought relative to defensive sectors (Chart 2). Moreover, the rapid deceleration of the Chinese credit impulse pointed toward a period of negative economic surprises and was historically consistent with a period of underperformance of cyclical names. Now that China is stepping off the brake pedal, this trade is becoming long in the tooth. Neutral Stance On Europe Relative To The Rest of The World This trade is down 0.3% since its inception. This position is a corollary to the neutral view on cyclicals, as European equities possess a high beta. This bet did not pan out; European equities did underperform US stocks, but weaknesses in China and EM undid this benefit. Favoring Industrials Over Materials This trade is up 0.6% since inception. Industrial equities are less exposed to the Chinese credit slowdown than materials, but are more direct beneficiaries of the large infrastructure spending packages being rolled out across advanced economies. Industrials are also a direct bet on a capex recovery, which we expect to intensify over the next two years as companies address supply side issues. The tactical element of this trade may soon dissipate as China’s policy tightening ends, which would warrant booking profits. However, the industrials versus materials theme remains attractive as a cyclical bets on capex. Financials Over Other Cyclicals This trade is down 1.6% since inception. This was another trade aiming to keep some cyclical exposure on the book (long financials), while diminishing the exposure to the Chinese credit slowdown. The fall in yields and the weakness in the euro prevented this trade from working out. We now close this position. Long / Short Basket Based On Combined Mechanical Valuation Indicator This trade is flat since inception. This market-neutral trade uses the methodology developed in our May 31st Special Report in which we introduced our Combined Mechanical Valuation Indicator (CMVI). We bought the most undervalued sectors and sold the most overvalued. We will look to rebalance this portfolio in the coming months. Short Euro Area Energy Stocks / Long UK Energy Stocks Chart 3UK Energy Stocks As A Bargain

UK Energy Stocks As A Bargain

UK Energy Stocks As A Bargain

This trade is up 7.5% since inception. This market neutral trade was fully based on the results from our CMVI (Chart 3). We are taking profits today. Short Consumer Discretionary / Long Telecommunication In Europe This trade is up 10.6% since inception. It is our favored way to express our tactical worries toward cyclical equities and the resulting preference for defensive stocks. Moreover, this trade is attractive from a valuation perspective, as the CMVI gap between discretionary and telecommunication equities is at a record high despite the higher RoE offered by telecom equities (Chart 4). Short Tech / Long Healthcare In Europe This trade is up 9.3% since inception. It is a low-octane version of the short discretionary / long telecommunications position. While it is a short cyclicals / long defensive trade, it does not have the long value / short growth overlay as its higher-octane cousin. However, it is also supported by attractive valuation differentials (Chart 5). Chart 4An Extreme Version Of Short Cyclicals / Long Defensives...

An Extreme Version Of Short Cyclicals / Long Defensives...