Fixed Income

Highlights The decline in US Treasury yields has once again reduced the appeal of US paper, relative to foreign developed and emerging market bonds. Historically, lower US bond yields relative to other markets has been dollar bearish. The caveat is that if declining yields are due to a flight to safety, the dollar initially benefits due to US bond inflows. The academic research on which yields matter for currencies is mixed. Historically, short rates have mattered more. But with short-term interest rates anchored at zero, there is evidence investors are moving out the curve. Our bias is that looking across the yield curve will provide a more accurate picture of the countries that will benefit from bond inflows. More importantly, it is the sum of portfolio flows that drive a currency. This means equity flows will be important as well. Feature Global bond yields have rolled over, driven by the long end of the curve. The US 10-year yield has fallen from a high of 1.74% at the end of March to 1.29% today. While other bond yields have rolled over, the move has been more pronounced in the US. For example, the spread between the US 10-year Treasury and the 10-year German bund has narrowed from 200bps to 175bps. Given the correlation between relative interest rates – especially in real terms – and the dollar, a rare divergence has opened up in favor of short dollar positions (Chart I-1). A fall in yields can be driven by prospects of either slowing growth, lower inflation expectations, or a combination of the two. In the case of the US and to a certain extent the eurozone, the culprit behind lower yields has been a drop in both the real and the nominal component. This suggests that the markets are worried about central banks becoming too hawkish at the exact moment global growth is set to slow. Across maturities, the US yield curve has thus flattened (Chart I-2). Chart I-1Real Yields And Currencies Have Diverged

Real Yields And Currencies Have Diverged

Real Yields And Currencies Have Diverged

Chart I-2Flattening Yield Curves

Flattening Yield Curves

Flattening Yield Curves

A few questions arise from the setup above. How do you trade the dollar in the current environment? What is the future path for yields, especially relative yields? Should investors focus on a specific maturity as a signal for future currency moves? Finally, are yields the key driver of currencies in the current environment or should investors focus on other factors as well? Explaining Recent Dollar Strength Chart I-3Rising Demand For Hedges

Rising Demand For Hedges

Rising Demand For Hedges

If the decline in rates globally has been led by the US, then why has the dollar remained strong? The first reason is rising safe-haven demand, especially as global growth peaks. Usually, as a counter-cyclical currency, the dollar benefits in a risk-off environment. The latest Treasury International Capital (TIC) data show that foreign inflows into US bonds have been part of the reason for the decline in Treasury yields since March. A reset in equity markets has also been a driver. The DXY index has been very closely correlated with the put-call ratio in the US, and increased demand for hedges, including long dollar positions, have benefited the greenback (Chart I-3). This has been consistent with the outperformance of the more defensive US equity market. The third reason has been a slowdown in relative economic momentum between the G10 and the US. Chart I-4 shows that the Citigroup economic surprise index for the euro area relative to the US remains strong but has rolled over. The story is similar using relative PMIs between the US and the rest of the G10. Relative economic performance has usually tended to dictate currency movements in the near term. Chart I-4Relative Economic Momentum Is Slowing

Relative Economic Momentum Is Slowing

Relative Economic Momentum Is Slowing

Finally, as we highlighted a fortnight ago, the dollar was oversold and due for a tactical bounce. Leveraged funds have been covering their short positions in recent weeks, while speculators are now long the dollar (Chart I-5). Chart I-5Speculators Are Now Long The Dollar

Speculators Are Now Long The Dollar

Speculators Are Now Long The Dollar

Going forward, most of these trends should reverse. While the Delta variant of COVID-19 is raging across countries, hospitalizations are low, and thus the case for renewed lockdowns is weak. Meanwhile, non-US growth should regain the upper hand, especially in countries like Japan where vaccinations are ramping up quite fast. Global yields should also rise, as output gaps close and inflation remains well anchored. The Dollar And Interest Rates: Real Versus Nominal? As Chart 1 highlights, it is important to think about relative rates when looking for the next move in the dollar. The historical evidence is that there is little correlation between the dollar and the absolute level or direction of bond yields. Over the last few decades, global bond yields have collapsed while the dollar has undergone rolling bull and bear markets. Currencies react more to the path of relative real rates than nominal rates. By definition, a currency is the mechanism by which prices are equalized across borders. Rising inflation lowers the purchasing power of a currency, which in turn forces the currency to adjust lower in a globally competitive pricing system. Across the G10, there has been a longstanding relationship between real interest rate differentials and the path of the currency (Chart I-6). Chart I-6Negative Real Rates In The US Across The Curve

Negative Real Rates In The US Across The Curve

Negative Real Rates In The US Across The Curve

Chart I-7The US Sports A Very Negative ##br##Real Yield

Which Rates Matter For Currencies?

Which Rates Matter For Currencies?

Importantly, US real rates, especially at the short end of the curve, are very depressed. In fact, compared to other G10 countries, the US sports one of the worst 2-year real yields (Chart I-7). Based on the historical precedent illustrated in Chart I-6, a significant increase in US real rates is required to allow the dollar to rise on a structural basis. What About Hedged Yields? It is true that hedged yields in the US are positive for foreign investors. For example, hedged 10-year US yields for German bond investors provide 97 bps of pickup. For a Japanese investor, the yield pickup in the US is 96 bps, and for a British investor, it is 73 bps (Chart I-8A, Chart I-8B, Chart I-8C). Chart I-8BUS Hedged Yields For Japanese Investors

US Hedged Yields For Japanese Investors

US Hedged Yields For Japanese Investors

Chart I-8AUS Hedged Yields For Euro Investors

US Hedged Yields For Euro Investors

US Hedged Yields For Euro Investors

Chart I-8CUS Hedged Yields For British Investors

US Hedged Yields For British Investors

US Hedged Yields For British Investors

However, there is little correlation between the hedged yields and currency performance, and for good reason: Under covered interest rate parity, a hedged yield will be an arbitrage opportunity, which should be duly uncovered by efficient markets. This arbitrage window for hedged yields disappears if you extend the maturity of your hedging, as economic theory suggests. For example, hedging a 10-year bond with a 3-month currency forward can lead to massive losses as you roll over these contracts. This is because the cost of hedging in the short term tends to have wild fluctuations. For example, hedging in euros for a German investor buying Treasurys was over 300bps at the end of 2018. This wiped out the positive spread between the two bonds. Many investors do not hedge currency exposure. In fact, the “least regrets” approach of hedging 50% of currency exposure has been quite popular.1 Therefore, focusing on the real yield, rather than the hedged or nominal yield (Chart I-9), has been a far more robust solution in gauging the direction of currencies. By definition, a hedged yield means buying a currency at spot and selling it forward. This should be currency neutral, and especially, arbitrage away the yield differential. Chart I-9Hedged Yields And Currencies: No Correlation

Hedged Yields And Currencies: No Correlation

Hedged Yields And Currencies: No Correlation

Which Bond Yields Matter? The academic evidence suggests that short-term interest rates matter more for currencies, especially when policy is close to the zero bound. According to a BIS paper,2 not only has the FX impact of monetary policy grown significantly in the last few years, but short maturity bonds have had the strongest impact. Moreover, at a lower level of interest rates, the foreign-exchange impact is greater as the adjustment burden falls onto the exchange rate. Looking purely through the lens of the US dollar, our view is more nuanced. Foreign inflows into US long-term Treasurys have been improving tremendously, while flows into T-bills are relapsing (Chart I-10). This suggests longer-term rates have been a bigger driver of inflows into the US, and, more recently, the dollar rally. It is similar to what occurred at beginning of the dollar bull market last decade. Admittedly, the picture shifted over time, with shorter term flows becoming increasingly important as the Fed began to hike interest rates. Taking a step back, bond investors tend to span the duration spectrum, with pension funds investing in bonds many years out. As 1-year and 2-year yield differentials are not meaningfully different across countries (Chart I-11), this curtails the appeal of short-term paper. If inflation differentials are considered, it reduces the appeal of US paper even further. Chart I-10Long-Term Versus Short-Term Flows

Long-Term Versus Short-Term Flows

Long-Term Versus Short-Term Flows

Chart I-11Narrow Gap In Short Term Yields

Narrow Gap In Short Term Yields

Narrow Gap In Short Term Yields

Let’s not forget quantitative easing. If a central bank explicitly targets a bond yield near zero, like in Japan or Australia, that makes it difficult for that same yield tenor to generate positive inflows or send a reliable signal about the economy. This suggests a better method is looking at a spectrum of indicators, including yields at various maturities. Charts I-12 plots the yield differentials across maturities and countries. It shows that currencies have been correlated across the relative yield maturity spectrum. As such, we recommend investors monitor both short- and long-term yields in evaluating currency decisions. Chart I-12AYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12BYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12CYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12DYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12EYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12FYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12GYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12HYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Chart I-12IYield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Yield Differentials Across Different Maturities

Other Asset Classes There are multiple drivers of exchange rates. Bond yields are just one of them. Equity and other flows also matter. It is the sum of portfolio flows that drive a currency. In fact, inflows into US equities and agency bonds have been the bigger drivers of the US dollar this year (Chart I-13). Outside the US, the correlation between interest rates and the currency can be very weak. The Canadian dollar is much more correlated with terms of trade than with real interest rate differentials. Rising oil prices attract inflows into Canadian corporate bonds and equities, which are positive for the currency. The key point is that flows tend to gravitate to capital markets with the highest expected returns. As such, monitoring flows other than government bond purchases is important. We expect that yields will be higher on a cyclical horizon. This will be beneficial for cyclical stocks, especially banks. This will also be beneficial for flows into non-US bourses, that have a higher weighting of cyclical stocks.. In short, the US equity market has become very tech heavy. Rising interest rates will hurt higher duration sectors such as technology and health care. At the margin, this hurts the relative performance of US equities (Chart I-14). Given that equity inflows have been a key driver of the US dollar, this will also hurt at the margin Chart I-13Agency Bonds And Equity Purchases Have Driven US Inflows

Agency Bonds And Equity Purchases Have Driven US Inflows

Agency Bonds And Equity Purchases Have Driven US Inflows

Chart I-14US Valuations Benefit From ##br##Lower Rates

US Valuations Benefit From Lower Rates

US Valuations Benefit From Lower Rates

Concluding Thoughts US real interest rates have deteriorated relative to the rest of the world. As such, it will require a significant rise in US real rates to seriously question a dollar bearish view. Meanwhile, a modest rise in global rates will also be bearish for US stocks compared to non-US bourses. US rates are usually high beta, and so could rise more in an improving growth environment. But relative rates are correlated to relative growth. As such, if non-US growth picks up relative to the US, like the IMF expects, this will provide a modest fillip to non-US yields (Chart I-15). US real rates are also very negative, so the bar to create a genuine dollar rally is very high. Finally, the market still expects the Federal Reserve to lead the hiking cycle. This means that there is still potential for an upside surprise in interest rates outside the US, compared to within (Chart I-16). Chart I-15Relative Bond Yields And Relative Economic Momentum

Relative Bond Yields And Relative Economic Momentum

Relative Bond Yields And Relative Economic Momentum

Chart I-16The Market Is Still Relatively Hawkish On The Fed

The Market Is Still Relatively Hawkish On The Fed

The Market Is Still Relatively Hawkish On The Fed

Housekeeping Our long Scandinavian basket was triggered at our buy point of a -2% pullback from July 9th levels. As such, we are now short EUR/NOK, USD/NOK, EUR/SEK, and USD/SEK. We were also stopped out of our long silver/short gold position for a small loss. We will be looking to reopen this trade in the coming weeks. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Michenaud, S., and Solnik, B., , “Applying regret theory to investment choices: Currency hedging decisions,” Journal of International Money and Finance 27, 2008, 677-694. 2 Ferrari, Massimo, Kearns, Jonathan and Schrimpf, Andreas, “Monetary policy’s rising FX impact in the era of ultra-low rates,” Bank of International Settlements, April 2017. Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Data out of the US this week was mixed: June retail sales came in better than expected. The control group rose 1.1% month on month, versus a -1.4% decline in May. For July, the University of Michigan survey showed inflation expectations continue to edge higher, but the sentiment of current conditions and expectations was well below consensus. Inflows into US assets reversed in May, with net outflows of $30.2bn. Existing home sales rose by 1.4% month on month in June to 5.9 million units. The US dollar DXY index rose modestly this week. Technically, the dollar is now approaching overbought territory. Our intermediate-term indicator has broken above 60, speculators are now long the dollar and sentiment on the greenback has turned up at a time when real rates remain negative in the US. This suggests much optimism is in the price. Report Links: Arbitrating Between Dollar Bulls And Bears - March 19, 2021 The Dollar Bull Case Will Soon Fade - March 5, 2021 Are Rising Bond Yields Bullish For The Dollar? - February 19, 2021 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Data out of the eurozone this week was robust: The trade balance came it at €9.4bn for May. Final June CPI was in line with expectations – 1.9% for headline and 0.9% for core. The ECB kept rates unchanged in their July 22 meeting, but added to their framework of forward guidance. The euro fell by 40bps this week. Following Christine Lagarde’s Bloomberg interview last week, the ECB made some policy changes. First, they will allow for an inflation overshoot should this be consistent with longer-term inflation at 2%. They will also likely extend the PEPP beyond the March deadline, so no tapering before then. Finally, interest rates are expected to remain negative as far as the eye can see. This is nudging the euro towards becoming a low-beta currency. Report Links: Relative Growth, The Euro, And The Loonie - April 16, 2021 The Euro Dance: One Step Back, Two Steps Forward - April 2, 2021 On Japanese Inflation And The Yen - January 29, 2021 The Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

There was some positive news out of Japan this week: Exports rose 48.6% year on year in June. Imports also expanded at a 32.7% year-on-year pace, signaling rising domestic demand momentum. National CPI for June was in line with expectations. The core measure was at 0.2%. Supermarket sales continued to improve in June. The yen was down 0.3% against the dollar this week. The yen is the most shorted developed-market currency, and our intermediate-term indicator is at bombed-out levels. This is occurring at a time when domestic data is on the mend. This is bullish from a contrarian perspective. Report Links: The Case For Japan - June 11, 2021 The Dollar Bull Case Will Soon Fade - March 5, 2021 On Japanese Inflation And The Yen - January 29, 2021 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

There was some mixed data out of the UK this week: Rightmove house prices rose 5.7% year on year in July. The CBI survey was softer than expected in July. Total orders fell from 19 to 17, while the component of selling prices and business optimism fell 4 and 5 points respectively. The pound fell by 0.5% against the US dollar this week. Momentum on the pound continues to suggest near-term downside. Our intermediate term indicator is still blasting downward, and speculators are cutting their long positions from very aggressive levels. This suggests continued near-term downside in cable. Report Links: Why Are UK Interest Rates Still So Low? - March 10, 2021 Portfolio And Model Review - February 5, 2021 Thoughts On The British Pound - December 18, 2020 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

There was scant data out of Australia this week: NAB business confidence for Q2 fell from 19 to 17. The RBA minutes confirmed that the central bank will stay dovish in the near term. The AUD fell by 0.7% this week against the USD, the worst performing G10 currency. COVID-19 will continue to dictate near-term developments in Australia, with the latest lockdowns having slowed economic activity. Speculators have started shorting the AUD on this basis (in addition to the risk of a decline in metal prices). In the end, if the COVID-19 crisis proves transient, it will create a coiled spring response for the AUD. Report Links: The Dollar Bull Case Will Soon Fade - March 5, 2021 Portfolio And Model Review - February 5, 2021 Australia: Regime Change For Bond Yields & The Currency? - January 20, 2021 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

The was scant data out of New Zealand this week: Credit card spending rose 6.3% year on year in June. The performance services index rose from 56.1 to 58.6 in June. The NZD was down 23bps versus the US dollar this week. Last week’s rally in the NZD, following the signal that the RBNZ will end QE this week, is fizzling. From a technical standpoint, speculators are neutral the NZD, but our intermediate-term indicator has not yet bottomed out. We are long CHF/NZD, as a reset in global asset prices could increase currency volatility and benefit the pair. Report Links: How High Can The Kiwi Rise? - April 30, 2021 Portfolio And Model Review - February 5, 2021 Currencies And The Value-Versus-Growth Debate - July 10, 2020 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Data out of Canada this week has been robust: June housing starts came in at 282.1K versus expectations of 270K. Foreigners continued to accumulate Canadian securities in June, to the tune of C$20bn. House prices remain on fire. The Teranet/National Bank index rose 16% year on year in June. The Bloomberg Nanos Confidence index held steady at 66.3. The CAD rose by 0.2% this week, performing better than other G10 currencies. The longer-term outlook for the loonie is clearly positive as the BoC will hike interest rates ahead of the Federal Reserve. Near term, USD/CAD could retest the 1.28 level as our intermediate-term indicator continues to work off overbought conditions. Ultimately, we will be selling this pair between 1.28 and 1.30. Report Links: Relative Growth, The Euro, And The Loonie - April 16, 2021 Will The Canadian Recovery Lead Or Lag The Global Cycle? - February 12, 2021 The Outlook For The Canadian Dollar - October 9, 2020 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

There was scant data out of Switzerland this week: Exports fell 3% month on month in June. However, watches continued to sell well, with exports rising 71% year on year. Total sight deposits were unchanged at CHF 712 bn for the week of July 16. The Swiss franc was down 0.2% this week. A rebound in global bond yields is a threat to franc long positions. However, we believe the period of volatility in both economic data and equity markets is not over. As such, the franc will benefit from safe-haven inflows. We are long the CHF/NZD cross on this basis. Report Links: An Update On The Swiss Franc - April 9, 2021 Portfolio And Model Review - February 5, 2021 The Dollar Conundrum And Protection - November 6, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Data out of Norway is improving: Industrial confidence came in at 11.3 for Q2, from 8.6 the previous quarter. The NOK was down by 0.5% this week against the dollar. This triggered our limit-buy on Scandinavian currencies at the -2% trigger level we had originally been targeting. As such, we are now short EUR/NOK and USD/NOK. With real yields in Norway much higher than in the US or Europe, portfolio flows should benefit the NOK. Report Links: The Norwegian Method - June 4, 2021 Portfolio And Model Review - February 5, 2021 Revisiting Our High-Conviction Trades - September 11, 2020 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data from Sweden have been somewhat mixed: There is a slight upward revision to the Bloomberg economic forecasts. GDP growth is now expected to be 4% year on year in 2021, from a previous estimate of 3.5%. However, CPI was revised down 10bps to 1.7% this year, and 1.4% next year, considering the disappointing CPI print last week. The SEK was down 20bps this week. The SEK remains one of our most potent plays on a global growth recovery. Historically, the SEK has correlated very well with global growth variables and relative economic growth between Sweden and the rest of the world. This week, our limit-buy on Scandinavian currencies was triggered. As such, we are now short EUR/SEK and USD/SEK. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 More On Competitive Devaluations, The CAD And The SEK - May 1, 2020 Sweden Beyond The Pandemic: Poised To Re-leverage - March 19, 2020 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights US Treasuries: Peaking global growth expectations and the growing spread of the Delta variant are challenging the “reflation and reopening” narrative that drove bond yields higher in Q1 of this year. Underlying growth, however, is likely to stay above-trend in most developed economies over the next 1-2 years, leading to tighter labor markets, increased domestic inflation pressures, and less dovish central banks - especially in the US. We continue to recommend an overall below-benchmark duration position in global bond portfolios, with an underweight stance on US Treasuries, on a strategic (6-24 month) basis. New Zealand: House prices, inflation, and the overall economic backdrop justify the RBNZ’s recent hawkish shift. However, government bond and interest rate swap markets have not fully priced in how quickly, and how far, the RBNZ can hike during the upcoming tightening cycle. As a play on further RBNZ hawkishness, we are entering a new recommended tactical trade: a 2-year/5-year yield curve flattener in New Zealand government bonds. Feature Dear Client, We will be taking a summer break over the next two weeks to recharge our batteries for what is shaping up to be an eventful time for global financial markets over the remaining months of 2021. Next week, you will be receiving a report written by our Chief US Bond Strategist, Ryan Swift. The following week, there will be no Global Fixed Income Strategy report published. We will return to our normal publishing schedule on Tuesday, August 10. Best Regards, -Rob Robis The World’s Most Important Asset Price We spent much of last week talking with clients (still virtually, sadly) in the US and Europe. In all the meetings, the first - and in some cases, only - topic of discussion was how to interpret the fall in longer-maturity US Treasury yields over the past few months. With the benchmark 10-year US yield hitting the lowest level since February earlier this week, breaching the 1.20% level, the message from the Treasury market will remain very much top of mind for investors - and for us, too - especially with bond yields in other countries also following US yields lower. Chart 1

bca.gfis_wr_2021_07_21_c1

bca.gfis_wr_2021_07_21_c1

The falling trend in US yields can be attributed to a number of factors, some of which are more legitimately bond bullish than others. Investors are increasingly convinced that global growth momentum has peaked, including in the US. While the global manufacturing PMI is still at the highest levels seen over the past decade, our global leading economic indicator (LEI) is rolling over from a very high level (Chart 1). The plunge in the global LEI diffusion index suggests that the dip in the global LEI is broad based across all the countries in the LEI (Chart 1, middle panel). This is not a sign that growth is slowing now, though, given the long lags between the swings in the diffusion index and the LEI, and between the LEI and actual economic growth. Importantly, US leading indicators like the Conference Board LEI are not rolling over and continue to signal that US growth will remain solid over the next 6-12 months. US consumer and business confidence are still upbeat, labor demand remains robust and corporate profits are growing smartly in the Q2 earnings data available so far. US growth will inevitably decelerate from the overheated pace of Q2 that was boosted by the rapid reopening from pandemic restrictions. Yet the US economy will continue to expand at an above-trend pace into 2022 – especially with an extra boost from fiscal stimulus - that is likely to tighten US labor markets and keep the Fed on the path towards bond-bearish tapering and, eventually, rate hikes by the end of next year. The renewed pickup in COVID-19 cases in the US could damage that positive narrative on US economic confidence. The uptick in the Delta variant raises the risk of a new wave of economic restrictions, even with nearly half the US population now fully vaccinated (Chart 2). To date, the latest surge in cases has not resulted in significant surges in hospitalizations and deaths in the US and, more importantly, the UK where the Delta variant has spread far more rapidly. If the hospitalization figures were to accelerate, investors would likely interpret that as a sign that a) vaccine efficacy against the variants is not as robust as for the original strain of the virus; and/or b) the next wave of COVID has arrived before the US could achieve herd immunity. At the moment, there is little political will to impose a new wave of growth-crushing - and bond bullish – economic restrictions in the US, especially with case numbers still low compared to previous waves of the virus amid ample vaccine supplies. Even in New York City, the epicenter of the first wave of the pandemic in the US in 2020 and one of the last major cities to reopen, the mayor said this week that a return to a mask-wearing mandate was not on the table (the city’s preference is to push for more of the unvaccinated to get their jabs to fight the variant). Lower US bond yields also reflect a growing belief that the rise in US inflation will prove to be transitory, as the Fed expects. Headline CPI inflation in the US reached 5.4% in June on a year-over-year basis, but was an even faster 8.8% on a 6-month annualized basis (Chart 3). Soaring US inflation rates have been dismissed by many as simply a function of temporary supply squeezes and favorable base effect comparisons versus the pandemic-fueled price collapses in Q2/2020. Yet the longer the inflation acceleration continues, the more the narrative will shift from “transitory” to “persistent” inflation, especially if inflation also keeps moving higher outside the US as well. Chart 2Delta Variant: Highly Contagious, But Not Lethal

Delta Variant: Highly Contagious, But Not Lethal

Delta Variant: Highly Contagious, But Not Lethal

Investors, and the Fed, will not be able to assess if the US inflation surge is truly a short-lived phenomenon until at least 2-3 more inflation data prints are available. Chart 3Is This 'Transitory' Inflation?

Is This 'Transitory' Inflation?

Is This 'Transitory' Inflation?

This means the “transitory or not” question will linger until the September inflation data is available in mid-October. What will be critical is the mix of US inflation. If more domestically generated inflation rates – rents, wages, etc. – accelerate, that would result in overall US inflation being driven more by stickier core inflation rather than surging non-core inflation fueled by rising commodity prices. That implies a higher floor for headline inflation, and a more bond-bearish challenge to the “transitory” narrative as the Fed would be even more emboldened to begin dialing back monetary accommodation sooner, or faster, than the current forward guidance. Beyond the fundamentals, the Treasury market continues to work off the technically oversold condition that developed in the first quarter of 2021, leading to short-covering that is pushing yields lower. The 10-year Treasury yield became extremely stretched versus the underlying trend in yields, defined by the 200-day moving average, with survey and positioning data showing large short positioning and below-benchmark duration exposures among bond investors (Chart 4). As the factors underpinning the US “reflation trade” in Q1 have come into question in Q2, speculators have covered much of the huge short positioning that built up in the 30-year Treasury, according to the CFTC (bottom panel). However, the JP Morgan survey of client duration positioning still shows a large number of clients are running duration exposures below that of their benchmark, suggesting that real money investors have not yet capitulated even as Treasury yields have moved lower. In a report published back in June, we looked at previous episodes where the 10-year US yield became stretched versus its underlying trend over the past two decades.1 We concluded that it could take until at least August before the 10-year Treasury worked off its oversold condition, defined as the yield returning to its 200-day moving average using daily closing prices, based on the average length of those past episodes. The US 10-year yield is now below its 200-day moving average of 1.28%, but it is still too soon to declare this oversold episode over given the still large underweight duration position visible in the JP Morgan survey. Some reduction in that tilt will be necessary before longer-term Treasury yields can begin to climb again. Summing it all up, the uncertainty over global growth momentum, the Delta variant, and the underlying pace of US inflation will likely keep Treasury yields under some downward pressure, especially with short positioning not yet completely cleaned out. We suspect that it will take a reacceleration of US employment growth before US Treasury yields can begin to move higher once again. That would not begin to be visible until at least the September payrolls data – a month when extended US federal unemployment benefits expire and children return to in-person learning at school, freeing up some of the supply bottlenecks in US labor markets. Our base case scenario is that the current pickup in COVID-19 cases will not derail the US economic recovery from the pandemic. A tightening US labor market and stickier-than-expected US realized inflation will lead the Fed to announce in December a tapering of its asset purchases starting in January 2022. A shift to a less dovish Fed, and eventual rate hikes beginning at the end of 2022 after tapering is complete, will be the driver of the next upleg in US Treasury yields. Looking outside the US, our Central Bank Monitors continue to highlight that developed economy central banks are all under cyclical pressure to begin dialing back the massive monetary accommodation put in place to fight the temporary economic shock of COVID-19 (Chart 5). Yet pricing in Overnight Index Swap (OIS) markets highlight the diverging messages from policymakers. Chart 4USTs Still Working Off Oversold Condition

USTs Still Working Off Oversold Condition

USTs Still Working Off Oversold Condition

Chart 5A Clear Message From Our Central Bank Monitors

The Message From Falling US Bond Yields

The Message From Falling US Bond Yields

A rate hike is now expected before year-end in New Zealand and by July 2022 in Canada (Table 1) “Liftoff” is now expected in January 2023 in the US, Australia and the UK; while rates are expected to remain unchanged until November 2023 in the euro area and February 2024 in Sweden. The bigger future issue for markets, however, is the pace of rate hikes given how little tightening is expected after liftoff. Table 1Bond Markets Are Vulnerable To Hawkish Monetary Policy Shifts

The Message From Falling US Bond Yields

The Message From Falling US Bond Yields

OIS curves are only discounting a handful of rate hikes to occur by the end of 2024 in most countries. Beyond that, 5-year/5-year forward OIS rates – a good proxy for the so-called “terminal rate”, or how high rates will end up in the next tightening cycle – show that markets have downgraded their assessment of how high global interest rates can possibly go. With global growth likely to remain above trend over the next 1-2 years, the current surge in global inflation will likely not be as transitory as the Fed and other central banks expect, leading to a faster pace of monetary tightening than markets are discounting (outside of Europe and Japan) and a renewed move higher, on average, for global bond yields led by US Treasuries. Bottom Line: Peaking global growth expectations and the growing spread of the Delta variant are challenging the “reflation and reopening” narrative that drove bond yields higher in Q1 of this year. Underlying growth, however, is likely to stay above-trend in most developed economies over the next 1-2 years, leading to tighter labor markets, increased domestic inflation pressures, and less dovish central banks - especially in the US. We continue to recommend an overall below-benchmark duration position in global bond portfolios, with an underweight stance on US Treasuries, on a strategic (6-24 month) basis. New Zealand: Primed For Liftoff Recent news from New Zealand has confirmed the market pricing of the Reserve Bank of New Zealand (RBNZ) as one of the most hawkish central banks within the developed economies. We have been of the view that the RBNZ would be among the first to withdraw the monetary accommodation put in place because of the pandemic, and recommended that investors avoid New Zealand sovereign debt in our Special Report on global house prices earlier this year.2 Increasingly, that view is being borne out, with the RBNZ delivering a hawkish surprise last week by announcing an end to the Large-Scale Asset Purchase (LSAP) program by July 23. On the surface, New Zealand’s situation does not appear that different from other higher-yielding bond markets in the developed world such as the US, UK, Australia, and Canada. However, there are a number of factors that make higher interest rates more appropriate for this economy: An unsustainable housing market If nothing else, the RBNZ’s hawkish turn can be attributed to the country’s wildly unsustainable housing market (Chart 6). Nominal house prices have been in an unimpeded accelerating trend since mid-2019, and are now growing at a whopping 28% year-over-year as of June. The anecdotal stories of housing market frothiness in New Zealand are at times unbelievable, like the recent sale of a run-down house in an Auckland suburb, with no bathroom or toilet, for a whopping two million dollars.3 The housing boom has undoubtedly been caused by accommodative monetary policy, with mortgage rates reaching all-time lows during the pandemic. While the RBNZ has implemented macroprudential measures such as increased loan-to-value restrictions on mortgages, it will take a significant pickup in mortgage rates to truly curb the acceleration in house prices. Housing affordability – or, more accurately, unaffordability - has reached a point where a 20% down payment on the median national house price is equal to 223% of the median disposable income, according to the RBNZ (Chart 6, middle panel). A similar measure, the OECD’s house price-to-income ratio, is most elevated in New Zealand among the developed economies. The overheating housing market also poses a major financial stability risk. New Zealand also leads the pack when it comes to the housing exposure of commercial bank balance sheets (Chart 6, bottom panel). With nearly half of commercial bank balance sheets composed of housing loans, New Zealand’s financial system is especially susceptible to a housing downturn. The takeaway is clear - even in the absence of other factors, the housing situation alone would be enough to force the RBNZ to act. Inflation accelerating above target The RBNZ tapering decision came a mere two days before the release of a very strong CPI print for Q2/2021, with consumer prices rising 1.3% during the quarter and 3.3% on a year-over-year basis – the fastest pace since 2011 (Chart 7). The central bank had been expecting some near-term spikes in headline inflation owing to temporary supply shortfalls and high oil prices. However, the RBNZ does not see all inflation as “transitory” and acknowledges that rising capacity pressures and labor shortages could continue to push up inflation going forward Chart 6The RBNZ's Housing Headache

The RBNZ's Housing Headache

The RBNZ's Housing Headache

Chart 7A Broad-Based Spike In NZ Inflation

A Broad-Based Spike In NZ Inflation

A Broad-Based Spike In NZ Inflation

Inflation has also been broad-based, with both tradables and non-tradables inflation running above the upper band of the RBNZ’s 1-3% inflation target. Although the bank does, on net, favor a lower New Zealand dollar (NZD) for the export-driven New Zealand economy, the depreciation in the NZD could push up tradeables inflation further, making urgent action from the RBNZ all the more necessary. Also important are the sources of inflation. The housing basket was responsible for more than a third of the rise in prices in Q2 (Chart 8). With housing affordability now a politically fraught issue creating major headaches for the RBNZ, expect the bank to be extra-sensitive to this sort of inflation. Accelerating food prices also create the risk that the “sticker shock” of rapidly rising costs for everyday spending items pushes up consumer inflation expectations past the RBNZ target range. Chart 8Prices Are Rising For 11 Out Of The 12 Groups In The NZ CPI Basket

The Message From Falling US Bond Yields

The Message From Falling US Bond Yields

Chart 9The RBNZ Is Running Out Of Bonds To Buy

The RBNZ Is Running Out Of Bonds To Buy

The RBNZ Is Running Out Of Bonds To Buy

An asymmetric monetary policy backdrop The monetary policy backdrop in New Zealand also favors a withdrawal of stimulus, on the margin. After only sixteen months of quantitative easing, the RBNZ now owns nearly half of all the sovereign debt outstanding in the country. That is a level of ownership on par with the ECB, which has had a long-running asset purchase program, and far exceeds the shares held by peers such as the Fed and Bank of Canada (Chart 9). Had they not terminated purchases, the RBNZ would have been limited by the simple fact that there is not enough government bond issuance for it to buy up without starting to impair the liquidity of the bond market Looking beyond the end of the LSAP, the central bank may have to push policy rates considerably higher to contain inflation. At only 0.25%, the official cash rate is 165bps below the mean estimate of the neutral rate —the rate at which monetary policy would be neither restrictive or stimulative – derived from the RBNZ’s suite of quantitative models (Chart 10). There is also some uncertainty around this number, with the upper end of the range of estimates as high as 4.5%. This signals that the RBNZ could hike rates quite a bit without choking off the economy. Chart 10The Market Is Pricing In An Extremely Slow RBNZ Hiking Cycle

The Market Is Pricing In An Extremely Slow RBNZ Hiking Cycle

The Market Is Pricing In An Extremely Slow RBNZ Hiking Cycle

In this context, market pricing in the New Zealand OIS curve, which discounts a very slow hiking cycle with the policy rate not expected to reach the median RBNZ neutral rate estimate until 2028, appears overly dovish. A buoyant economic backdrop Lastly, the RBNZ has arguably already satisfied its mandate to support the economic recovery coming out of the pandemic (Chart 11). Real GDP and aggregate employment are both above pre-COVID levels, while business and consumer confidence are continuing the recovery started last year. Yields have picked up across the New Zealand government bond curve, reflecting this improvement in growth and sentiment. Even though some pandemic restrictions remain in place, the vaccination program has shown steady progress and is likely to ramp up further as the government has just acquired a large shipment of the Pfizer vaccine. Looking at the broader picture, there appears to be little remaining justification for the RBNZ to remain as accommodative as it is right now. The economic recovery from the pandemic is largely complete and the upside inflation and financial stability risks are too important to ignore. After such an abrupt end to the RBNZ’s LSAP program, rate hikes are likely just around the corner. Yet with the OIS curve now discounting a full rate hike by October of this year, markets have adjusted to a sooner than expected RBNZ liftoff date. However, we believe that the New Zealand sovereign yield curve has not fully priced in how much the RBNZ - historically one of more active central banks that is not afraid to raise or lower interest rates aggressively - will need to tighten, and how flat the curve will get, once the rate hikes begin. Although the entire New Zealand government bond curve has already flattened somewhat, experience from previous hiking cycles shows that the curve usually continues to flatten well after rate hikes begin, usually reaching zero or inverting slightly by the time the RBNZ is done hiking rates. This is especially true for the yield curve between two and five years, which is the maturity range that is most sensitive to rate hike expectations (Chart 12). Chart 11The NZ Economy Has Recovered For The Most Part

The NZ Economy Has Recovered For The Most Part

The NZ Economy Has Recovered For The Most Part

Chart 12Monetary Policy And The NZ Yield Curve

Monetary Policy And The NZ Yield Curve

Monetary Policy And The NZ Yield Curve

Currently, the 2-year/5-year New Zealand yield curve is 22bps, leaving ample room for the curve the flatten further once the RBNZ begins to hike rates. Meanwhile, implied forward rates are currently priced for a re-steepening of the curve in the short term, making a 2-year/5-year flattener an especially attractive trade in New Zealand with the RBNZ set to tighten. This is also a “cleaner” play on monetary policy expectations over a cyclical horizon than, for example, a 2s/10s flattener where the longer-maturity yield could be boosted by higher inflation expectations (and where some flattening is already discounted in the forwards). Today, we are initiating a new recommended 2-year/5-year curve flattener trade in New Zealand using cash government bonds. This trade involves selling a 2-year bond, and using the proceeds to buy a combination of a 5-year bond and a 3-month treasury bill that has the same duration as the 2-year bond. This makes the trade both duration-neutral and “proceeds-neutral” by fully investing the cash from the sale of the 2-year bond. Details of the trade, including the duration weightings and specific bonds used, can be found in our Tactical Trade Overlay table on page 17. Bottom Line: House prices, inflation, and the overall economic backdrop justify the RBNZ’s hawkish shift. However, government bond and interest rate swap markets have not fully priced in how quickly, and how far, the RBNZ can hike during the upcoming tightening cycle. As a play on further RBNZ hawkishness, we are entering a new recommended tactical trade – a 2-year/5-year yield curve flattener in New Zealand government bonds. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Shakti Sharma Senior Analyst ShaktiS@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Report, "A Summer Nap For Global Bond Yields", dated June 9, 2021, available at gfis.bcaresearch.com. 2 Please see BCA Research Global Fixed Income Strategy Special Report, "Global House Prices: A New Threat For Policymakers", dated May 28, 2021, available at gfis.bcaresearch.com. 3https://www.theguardian.com/world/2021/jul/15/house-with-no-toilet-sells-for-2m-as-new-zealand-property-market-soars Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The Message From Falling US Bond Yields

The Message From Falling US Bond Yields

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

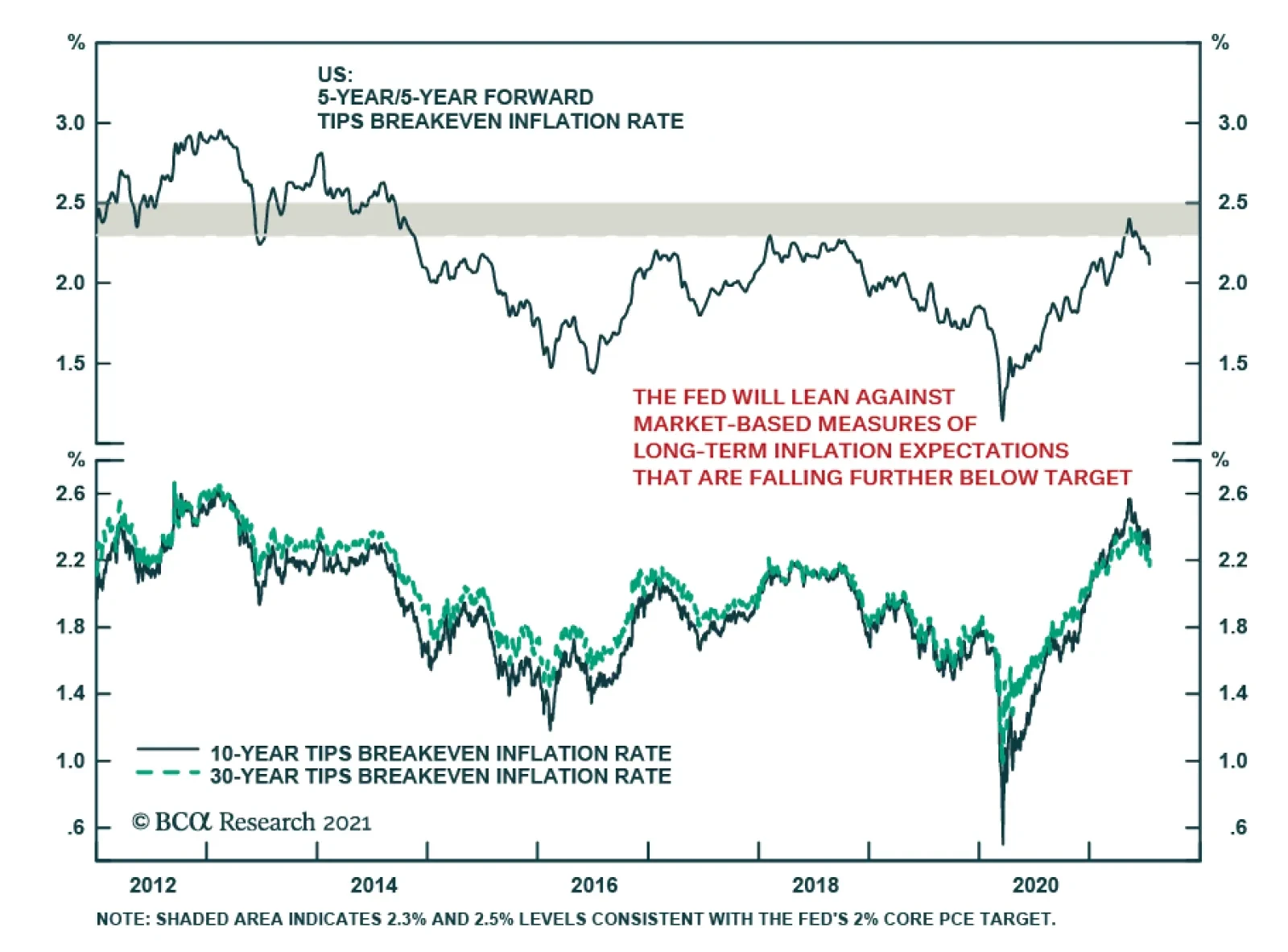

After rising to levels consistent with the Fed’s 2% core PCE target in May and June, the 5-year/5-year forward TIPS breakeven inflation rate has continued to decline, falling further below the Fed’s target zone. On Monday, this market-based measure of…

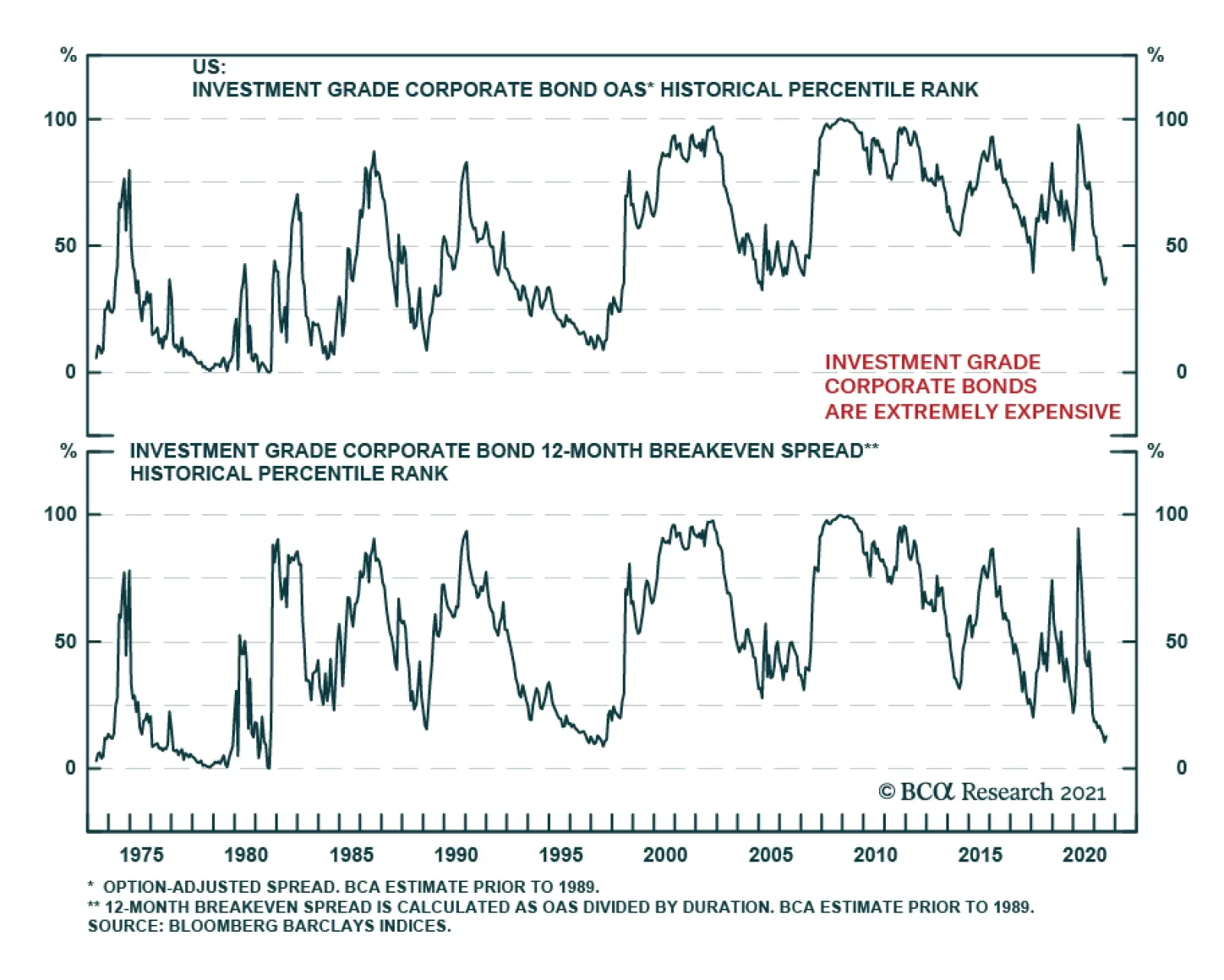

The credit risk premium in US bonds has shrunk considerably during the past 16 months. While BCA Research’s US Bond Strategy service doesn’t foresee a period of significant spread widening any time soon, lower spreads mean lower excess corporate bond returns.…

Highlights Metals prices are likely to suffer in the short term on the back of weakening Chinese demand and fading inflationary pressures. Accordingly, in our most recent Global Asset Allocation (GAA) Quarterly Outlook, we downgraded the AUD to underweight against the greenback. Bond yields, globally, are bound to rise moderately over the course of the coming 12 months. Australian yields, however, are likely to rise slower than those in the US. The RBA has been explicit in communicating what it would take to adjust its policy stance and is likely to lag behind other central banks in DM. We therefore recommend investors favor Australian government bonds in a global bond portfolio. Australian equities, now dominated by Financials rather than the Materials sector, would benefit from a rise in bond yields. However, a weaker AUD and declining metal prices warrant no more than a benchmark exposure to Australian equities within a global equity portfolio. Introduction Recently, clients have often been asking about Australia. The reasons seem clear. With a potential commodities “super-cycle” driven by a shift to renewable energy and electric vehicles (EVs), both the Australian economy and equities should be in a position to benefit. The reality, however, has been much less positive. Particularly the divergence between the core driver of the Australian market, industrial metals, and the performance of both equities and the currency over the past few years has been a concern (Chart 1). Over the past year and a half, Australian equities have underperformed the MSCI ACWI by 12.4% (Chart 2, panel 1). This underperformance was mainly due to the outperformance of the US. However, even against global markets excluding the US, Australian equities did not match the rise in commodity prices – particularly industrial metals (Chart 2, panel 2). Chart 1Despite The Rise In Metals Prices...

Despite The Rise In Metals Prices...

Despite The Rise In Metals Prices...

Chart 2...Australian Equities Have Not Outperformed

...Australian Equities Have Not Outperformed

...Australian Equities Have Not Outperformed

Chart 3Financials Dominate Australian Equities

Financials Dominate Australian Equities

Financials Dominate Australian Equities

The structure of the Australian market has changed over the past few years. The commodities boom and subsequent global liquidity boom over the past two decades have fueled a housing bubble in Australia and an unsustainable rise in household debt. As a result, Australian equities are no longer dominated by metals and mining stocks, but rather by banks (Chart 3). We structured this Special Report in a Q&A format, answering questions we think are most relevant for investors to assess both the short- and long-term outlook for Australia. We aim to provide an overview of the economy and draw some conclusions on how investors should be positioned. Our conclusions are as follows: Over the past year and a half, the Australian economy has shown how complementary actions between fiscal and monetary policy, as well as social restriction measures, can mitigate both economic and human damage. The Reserve Bank of Australia (RBA) will be in no rush to adjust its policy stance until wage growth is back to its 3% target. However, RBA officials risk running the economy hot in the meantime given that measures of employment are back to their pre-pandemic levels. The RBA is not likely to change its policy stance before reaching its wage growth and inflation targets and will probably lag behind other global central banks in tightening. In that case, investors should favor Australian government bonds in a global bond portfolio. Australian banks remain well-funded and in good health. But their excessive exposure to the housing sector puts them at grave risk if home prices collapse. Despite this, there seems to be a feedback loop where a decline in mortgage rates fuels further demand for loans, pushing up home prices. A slowdown in Chinese credit growth and economic activity will hamper commodity demand, weighing down on Australian equities. The longer-term outlook remains compelling for Australian equities and metals as we enter into a new commodities “supercycle” fueled by a transition to renewable and alternative energy. The Australian economy stands to benefit given that the country has high levels of both production and reserves of the minerals needed for this transition. Q: How Does The Economy Look In The Short-Term? A: Australia can be regarded as one of the few countries that successfully navigated the pandemic with a minimal amount of damage, both to its population and economy. With swift measures to limit travel and implement social restrictions, the spread of the outbreak was curtailed to slightly over 30,000 total cases, representing only 0.12% of its population (Chart 4). On the other hand, its vaccination campaign has been much slower (at 38 doses administered per 100 people) than in other DM economies such as the US, UK, France, or Germany with 100, 120, 90, and 102 doses per 100 people, respectively. In the short term, this might not seem particularly damaging to the economy. However, if vaccination rates do not pick up rapidly, Australia’s international travel restrictions (which cannot sustainably be kept in place) will hamper economic growth and become a major drag on the tourism and education sectors (Chart 5, panels 1 & 2). Chart 4Government Policies Contained The Pandemic Outbreak...

Government Policies Contained The Pandemic Outbreak...

Government Policies Contained The Pandemic Outbreak...

Chart 5...At The Expense Of Tourism

...At The Expense Of Tourism

...At The Expense Of Tourism

Ample fiscal support – in the form of wage subsidies and business support through the JobKeeper program – mitigated the shortfall in household incomes (Chart 6). This provided a boost to both consumers and businesses with Q1 GDP growth coming in at 1.8% quarter-on-quarter (7.4% annualized). GDP expectations for the remainder of this year and next show a resilient strong momentum for Australian growth and domestic demand (Chart 7). Chart 6Fiscal Stimulus Supported Employment...

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

Chart 7...And Overall Growth

...And Overall Growth

...And Overall Growth

Chart 8Labor Market Back To Pre-Pandemic Levels...

Labor Market Back To Pre-Pandemic Levels...

Labor Market Back To Pre-Pandemic Levels...

The labor market recovery has been an excellent example of how fiscal support and lockdown measures complement each other. Most employment indicators have almost recovered or surpassed their pre-pandemic levels: The unemployment rate stands at 4.90%, compared to 5.13%, the underemployment rate is at 7.44%, compared to 8.60%. The total number of those employed is now above its pre-pandemic level, albeit still below the 2018-2019 growth trend (Chart 8). Q: When Will The RBA Shift Its Policy Stance? A: The RBA has been explicit in communicating that changes in its policy stance hinge on Australian wage growth rising sustainably towards 3% – a level last reached in Q1 2013. Even with economic activity mostly restored, wage growth remains low at 1.49% (Chart 9). Our belief is that until that occurs, the RBA will probably maintain its accommodative stance. Our global fixed-income strategists, in a recent report, highlighted their belief that the RBA is likely to be less hawkish than markets currently expect – on both tapering and hiking rates. We agree with that assessment. Comments by RBA Governor Lowe earlier last month back our dovish belief: He stated that “The Board is committed to maintaining highly supportive monetary conditions to support a return to full employment in Australia and inflation consistent with the target…This is unlikely to be until 2024 at the earliest”. Market expectations nevertheless remain much more hawkish – pointing to a first rate hike by mid 2022 and almost 70 basis points of hikes by 2024 (Chart 10). Chart 9...However Wage Growth Remains Muted

...However Wage Growth Remains Muted

...However Wage Growth Remains Muted

Chart 10Market Expects A Hawkish RBA...

Market Expects A Hawkish RBA

Market Expects A Hawkish RBA

Chart 11...And Is Already Pricing That Down The Curve

...And Is Already Pricing That Down The Curve

...And Is Already Pricing That Down The Curve

Chart 12Inflation Remains Well-Below The RBA's Target

Inflation Remains Well-Below The RBA's Target

Inflation Remains Well-Below The RBA's Target

This means that the RBA will probably risk running the economy hot for a while. With total employment back to its pre-pandemic level and other employment indicators closely behind, inflationary pressures, sooner or later, will begin to mount. Higher growth prospects and inflation risks are being discounted further down the curve (Chart 11). The June CPI print is likely to reflect a transitory short-term base effect and the RBA is mostly going to see through that. In the meantime, we would watch other broad inflation indicators to gauge for price pressures. Broader measures such as the trimmed-mean inflation index or median inflation remain subdued at 1.1% and 1.3%, respectively. The 10-year breakeven rate currently stands at 2.1%, within the RBA’s range of 2%-3%, highlighting the market’s belief that long-term inflation remains well under control (Chart 12). Bottom Line: The RBA is likely to maintain its dovish stance for longer than the market expects. A return to sustainable levels of wage growth and inflation will remain the top objectives and it is unlikely that policy will be reversed before they are achieved. Our global fixed-income strategists laid out a checklist of what would make the RBA turn less dovish. So far, only 1 out of 5 items on their list (the recovery in private-sector demand) signals the need for a more hawkish stance. The remaining items signal no imminent pressure on the RBA to adjust policy (Table 1). The RBA is also wary of the currency appreciating if it took a more hawkish stance ahead of other central banks (e.g., the Fed) and is therefore likely to switch policy only after other central banks do so (Chart 13). Accordingly, investors should favor Australian government bonds within a global bond portfolio. Table 1RBA Checklist

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

Chart 13The RBA Will Be Wary Of A Rising AUD

The RBA Will Be Wary Of A Rising AUD

The RBA Will Be Wary Of A Rising AUD

Q: Are There Signs Of Improvement In The Banking Sector? A: Headline indicators of the health of the Australian banking sector paint a picture of a well-capitalized, highly funded, and profitable industry. Return on equity (ROE) has averaged 12.1% over the past decade. Capital adequacy and Tier 1 capital ratios stand at 14.5% and 18.2%, respectively – much higher than at the start of the Global Financial Crisis (GFC). The ratio of non-performing loans remains low and Australian banks’ reliance on leverage has also decreased (Chart 14). Chart 14Banks Look Healthy...

Banks Look Healthy...

Banks Look Healthy...

Chart 15...But Remain Exposed To The Housing Sector...

...But Remain Exposed To The Housing Sector

...But Remain Exposed To The Housing Sector

However, these indicators mask a major underlying risk. Banks remain heavily exposed to the housing market, with housing loans as high as 62% of banks’ gross outstanding loans and 40% of total assets (Chart 15, panel 1). Over the past decade and a half, banks have lent an average of A$56 of housing-related loans for every A$100 in total loans (Chart 15, panel 2). Chart 16...Which Is Showing No Signs Of Slowing Down

...Which Is Showing No Signs Of Slowing Down

...Which Is Showing No Signs Of Slowing Down

Chart 17Households Remain Heavily Indebted

Households Remain Heavily Indebted

Households Remain Heavily Indebted

With interest rates falling over the past few decades, construction activity has boomed. Consequently, the demand for loans for new homes has been rising, leading home prices higher (Chart 16). This also meant that household debt levels have climbed and currently standing at a staggering 130% of GDP and 180% of disposable income (Chart 17). So what does this mean for banks’ stock prices? The short answer is that absent a bursting of the bubble in house prices, banks should continue to fare well. Interestingly, the long-standing relationship between bond yields and banks’ relative stock price returns – one that works in other financial-heavy markets such as the euro area – did not hold in Australia, at least until recently. In fact, we find that, historically, Australian banks outperformed the broad market when bond yields were falling. This relationship changed post-GFC, most likely when inflation expectations became unanchored and trended lower – reflecting lower commodity prices (Chart 18). Bottom Line: Rising rates, reflecting better growth prospects and higher long-term inflation, should be a tailwind for bank stocks in the short term. Accommodative monetary policy will spur activity in the property market, propping up bank profits. This, however, puts banks at even greater risk when profitability starts to decline, NPLs rise and regulations tighten further. The latter risk is one we would highlight following RBA deputy governor Guy Debelle’s statement that monetary policy will not be used as a tool to curtail housing prices and that there are other tools to address that issue. Chart 18Rising Yields Will Be A Tailwind For Australian Equities

Rising Yields Will Be A Tailwind For Australian Equities

Rising Yields Will Be A Tailwind For Australian Equities

Q: How Does Chinese Policy Impact Australian Growth? A: China's role in global supply chains, as both a producer and consumer, has increased dramatically since the early 2000s. China’s demand for commodities generally and industrial metals in particular has grown over the past two decades from an average of 10% of total global demand to 50% for most metals (Chart 19). Australia stood to benefit, redirecting more and more of its metals’ production away from the rest of the world and towards China. For example, during the same period, the share of Australian iron ore exports to China increased fourfold (Chart 20). Chart 19China Is A Major Consumer Of Metals...

China Is A Major Consumer Of Metals...

China Is A Major Consumer Of Metals...

Chart 20...And This Has Benefited Australia Over The Past Two Decades

...And This Has Benefited Australia Over The Past Two Decades

...And This Has Benefited Australia Over The Past Two Decades

However, this dynamic leaves the Australian economy very exposed to the Chinese business cycle – one that is heavily reliant on policymakers’ decisions on how much liquidity to inject into the economy. After strong credit and fiscal support throughout 2020, the Chinese authorities – wary of excessive leverage in the economy – have begun paring back stimulus which is likely to lead to weaker growth in the second half of the year and put downward pressure on metal demand (Chart 21). Chart 21Weakening Chinese Demand Will Hurt Metals In The Short-Term

Weakening Chinese Demand Will Hurt Metals In The Short-Term

Weakening Chinese Demand Will Hurt Metals In The Short-Term

Heightened political tensions between Australia and China have also played a role. China recently imposed restrictions, including additional tariffs and bans, on Australian imports such as beef, wine, coal, and other goods. Consequently, Australian exports to China slowed. However, the goods not imported by China were absorbed by other economies – Australian export growth did not fall that much. It is unlikely that a new commodity-heavy marginal buyer will emerge in the short-term to replace Chinese demand. The recent rise in commodity prices reflected a return to economic activity, as well as inflationary fears, and supply, shipping, and logistical backlogs. These will ease in the short term, weighing on both the AUD and Australian equities. Q: Can The Shift To Renewable Energy Spur Future Australian Growth? A: The shift to renewable energy and electrification – particularly in the transport sector – will occur sooner rather than later. Some commodity-exporting countries stand to benefit, and Australia is likely to be one. We previously highlighted that modeling longer-term demand is tricky since it relies on assumptions for the emergence of new technologies, metals’ efficiency and recycling rates, and the rate of conversion to renewables. Chart 22The Shift To Renewables Will Require More Resources...

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

The mechanics of the future demand/supply relationship hinge on the following: Demand will rise during this energy transition period – simply due to the fact that the new clean energy systems require more minerals (such as copper and zinc) than the current traditional hydrocarbon-fueled energy system (Chart 22, panel 1). Electric vehicles (EVs) require about four and a half times more of certain commodities – particularly copper, nickel, and graphite – than conventional vehicles do (Chart 22, panel 2). Supply limitations, on the other hand, are what might propel metal prices even higher and lead the world economy into a new commodities “supercycle”. A study by the Institute for Sustainable Futures has shown that, in the most positive energy transition scenarios, demand for some metals will exceed supply, in terms of both available resources and reserves (Table 2). Table 2...Which Are Likely To Be In Short Supply

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

For some of those metals, Australia is either among the top producers, or has the largest reserves. For example, Australia produces almost 45% and 12% of the world’s lithium and zinc, and has 22% and 27% of the world’s reserves. Looking at other metals, supply disruptions – particularly in economies where political, social, and environmental influences are an issue – might be the driver of further price rises. For example, Chile has the largest shares of global lithium reserves (~44%), and copper reserves (~23%), while South Africa has the largest share of global manganese reserves (~40%). Bottom Line: The transition to renewable energy is already underway and is likely to intensify. Forecast demand should outstrip supply and Australia stands to benefit given its large share of current production and/or reserves. How much will depend on the pace of renewable energy integration but miners are likely to be long-term winners. Q: What Is The Outlook For The AUD? A: The Global Asset Allocation (GAA) service, in its latest Quarterly Outlook, turned negative on the AUD. The currency has historically had a high positive correlation with commodity prices and industrial metals prices, which in turn are very sensitive to Chinese demand (Chart 23). Given our outlook for metals in the short term (falling demand driven by slowing Chinese activity), we expect some weakening in the AUD over the coming 9-to-12 months (Chart 24). Chart 23The AUD Is Highly Correlated To Metal Prices...

The AUD Is Highly Correlated To Metal Prices...

The AUD Is Highly Correlated To Metal Prices...

Chart 24...Which In Turn Are Highly Correlated To Chinese Activity

...Which In Turn Are Highly Correlated To Chinese Activity

...Which In Turn Are Highly Correlated To Chinese Activity

Additionally, short-term weakness in the economy, caused by further lockdowns as Delta-variant COVID cases rise, is a risk since it might reduce domestic demand. From a valuation perspective, the AUD is slightly below its fair value (Chart 25). However, this on its own does not compel us to remain positive on the currency. We also consider other indicators such as investor positioning – which has reached a decade high, according to Citibank’s FX Positioning Alert Indicator (PAIN) (Chart 26). This indicator suggests that active FX traders hold substantial long positions in the AUD against the USD. Historically, this indicator has provided contrarian signals, with extreme optimism (pessimism) providing useful short (long) signals. Chart 25The AUD Is Close To Fair Value

The AUD Is Close To Fair Value

The AUD Is Close To Fair Value

Chart 26Investors Are Long The AUD

Investors Are Long The AUD

Investors Are Long The AUD

Bottom Line: Short-term weakness in the economy and a reversal in metal prices warrant caution on the currency. While valuations do not signal overbought conditions, investor positioning (a contrarian indicator) does. Q: How Should Equity Investors Be Positioned? A: Our recent Special Report on whether country or sector effects drive equity performance showed that sector composition was relatively important in Australia, given the large difference in sector weightings relative to the global benchmark. Our analysis showed that cumulative Australian sector performance over the past two decades detracted from overall returns (Chart 27). Given that framework, and the relationship between the Australian economy and industrial metals, we find that Australian equity performance relative to the US mirrors the performance of global metal and mining relative to global tech stocks (Chart 28). This underperformance makes sense: Commodity prices have been in a structural downtrend throughout the past decade. Chart 27Country Vs Sector Effect

Country Vs Sector Effect

Country Vs Sector Effect

Chart 28Australia / US = Metals / Tech

Australia / US = Metals / Tech

Australia / US = Metals / Tech

Therefore, given our view of the outlook for metals, we would not want to shun Australian equities. The Global Asset Allocation (GAA) service is currently neutral the Australian market within a global equity portfolio, and underweight the Materials sector over the next 12 months. We believe this positioning makes sense given the slowdown in the Chinese economy and the improbability that another country will emerge as the alternative marginal buyer of commodities. The longer-term outlook is more compelling however, as the shift to decarbonization, renewables, and alternative energy gets underway. Conclusions In the short term metals prices are likely to suffer on the back of weakening Chinese demand (with no immediate substitute as a marginal buyer) as well as fading inflationary fears and an easing of supply/logistical issues. Our analysis shows that sector composition is a larger driver of Australian equity relative performance than country composition. While Australian equities – dominated by Financials – would benefit from a moderate rise in global bond yields, yields will rise more slowly in Australia than in the US and the AUD is likely to weaken. Over the next 12 months, investors should remain neutral on Australian equities within a global equity portfolio. The RBA is likely to lag other central banks in tightening policy. Investors should therefore favor Australian government bonds over other developed economies such as the US and Canada. Amr Hanafy, Senior Analyst Global Asset Allocation amrh@bcaresearch.com

Highlights Spread Product: The credit risk premium has shrunk considerably during the past 16 months. While we don’t foresee a period of significant spread widening any time soon, lower spreads mean lower excess corporate bond returns. We recommend three ways for investors to grab extra spread and increase their excess corporate bond returns: (i) move down in quality, (ii) extend maturity, (iii) favor high-DTS industry groups. Corporate Bond Sectors: High-DTS industry groups like Energy, Communications, Utilities and Basic Industry offer the best risk-adjusted spread pick-up within both investment grade and junk bonds. Consumer Noncyclicals and Transportation also look attractive within high-yield. Municipal Bonds: Investors can increase the average after-tax yield of their bond portfolios without taking greater credit or duration risk by favoring long-maturity tax-exempt municipal bonds (both GO and Revenue). EM Bonds: Investors can increase the average yield of their US bond portfolios by shifting out of investment grade US corporates and into USD-denominated EM Sovereign and Corporate bonds. Feature US bond yields have been on a wild ride since the pandemic struck in March 2020. The 10-year Treasury yield collapsed to 0.52% last year. It then rebounded to a high of 1.74% in March 2021 before falling back to its current 1.21%. But throughout all this volatility in rates markets, the steady outperformance of credit risk has been a constant. For the past 16 months, accommodative monetary policy has spurred a steady flow of investment into spread product, a trade that was amplified by the Fed’s extraordinary intervention in the corporate bond market. On March 23rd 2020, the Fed essentially announced a back-stop of the corporate bond market that gave investors the green light to pile into the sector. Since then, the investment grade corporate bond index has outperformed a duration-matched position in Treasury securities by 24% and the high-yield index has outperformed by 39%. Of course, the result of this consistent flow of funds into spread product has been a collapse in credit spreads. The average spread on the investment grade corporate bond index is only slightly below its post-1973 median, but it is at its tightest level since the mid-1990s (Chart 1). When we adjust for the fact that the index’s average duration has increased significantly since the 1970s, we find that the spread has only been tighter 13% of the time since 1973 (Chart 1, bottom panel). What’s more, this analysis doesn’t control for the fact that the average credit rating of the index has fallen significantly during the past few decades. In short, investment grade corporate bonds are extremely expensive and are quite possibly the most expensive they have ever been in risk-adjusted terms. Chart 1Investment Grade Corporate Bond Valuation

Investment Grade Corporate Bond Valuation

Investment Grade Corporate Bond Valuation

How should bond investors proceed in this environment? Of course, tight credit spreads will cause us to exit our recommended spread product overweight earlier in the cycle than would otherwise be the case. But for the time being, we still see quite a bit of life left in credit markets. We showed in a recent report that corporate bond excess returns tend not to turn negative until the 3/10 Treasury slope is below 50 bps, even during periods when credit spreads are tight.1 At 88 bps, the slope still has a ways to go before breaching that threshold. In the meantime, we advise investors to run high levels of credit risk in their bond portfolios, grabbing attractive risk premiums where they can be found. As for what investors can do to find attractive risk premiums, we have a few suggestions. Move Down In Quality The most obvious way to add spread to a bond portfolio is to move down in quality. Charts 2A-2E show the extra spread that can be picked up by moving down one credit tier at a time. We show both the raw spread pick-up since 1995 and the spread pick-up after adjusting for duration risk (i.e. the 12-month breakeven spread). The additional spread on offer for moving out of Aa-rated bonds and into A-rated bonds is currently 17 bps, very low compared to history (Chart 2A). The extra compensation looks a little better after adjusting for duration risk (Chart 2A, bottom panel), but it is still well below its historical mean. Similarly, investors only earn an additional 38 bps by moving out of A-rated bonds and into Baa-rated bonds (Chart 2B). This is very low compared to history and it looks even worse in duration-adjusted terms (Chart 2B, bottom panel). A move down in quality within the investment grade space may still be worth it, even though the reward for doing so is meager in historical terms. However, investors can get much more bang for their buck by moving out of investment grade entirely and into junk bonds. The additional spread earned in Ba-rated bonds compared to Baa-rated bonds (130 bps) is below its historical average, but it has been much lower in the recent past (Chart 2C). This is also true in duration-adjusted terms (Chart 2C, bottom panel). A move out of Ba-rated bonds and into B-rated bonds looks even better (Chart 2D). Yes, the raw 116 bps spread pick-up in the B-rated index compared to the Ba-rated index is well below its historical mean, but after adjusting for the lower duration of the B-rated index we see that the duration-adjusted spread pick-up in B-rated bonds is above its average historical level (Chart 2D, bottom panel). Finally, we observe that investors earn an extra 159 bps by moving out of the B-rated sector and into the Caa-rated sector (Chart 2E). This is extremely low compared to history, but it looks considerably more appealing in duration-adjusted terms (Chart 2E, bottom panel). All in all, we think it makes sense for investors to grab extra spread by moving down the quality ladder. In particular, investors should favor high-yield bonds over investment grade and focus on the B-rated credit tier where the duration-adjusted spread is most attractive. Chart 2AA Versus Aa

A Versus Aa

A Versus Aa

Chart 2BBaa Versus A

Baa Versus A

Baa Versus A

Chart 2CBa Versus Baa

Ba Versus Baa

Ba Versus Baa