Fixed Income

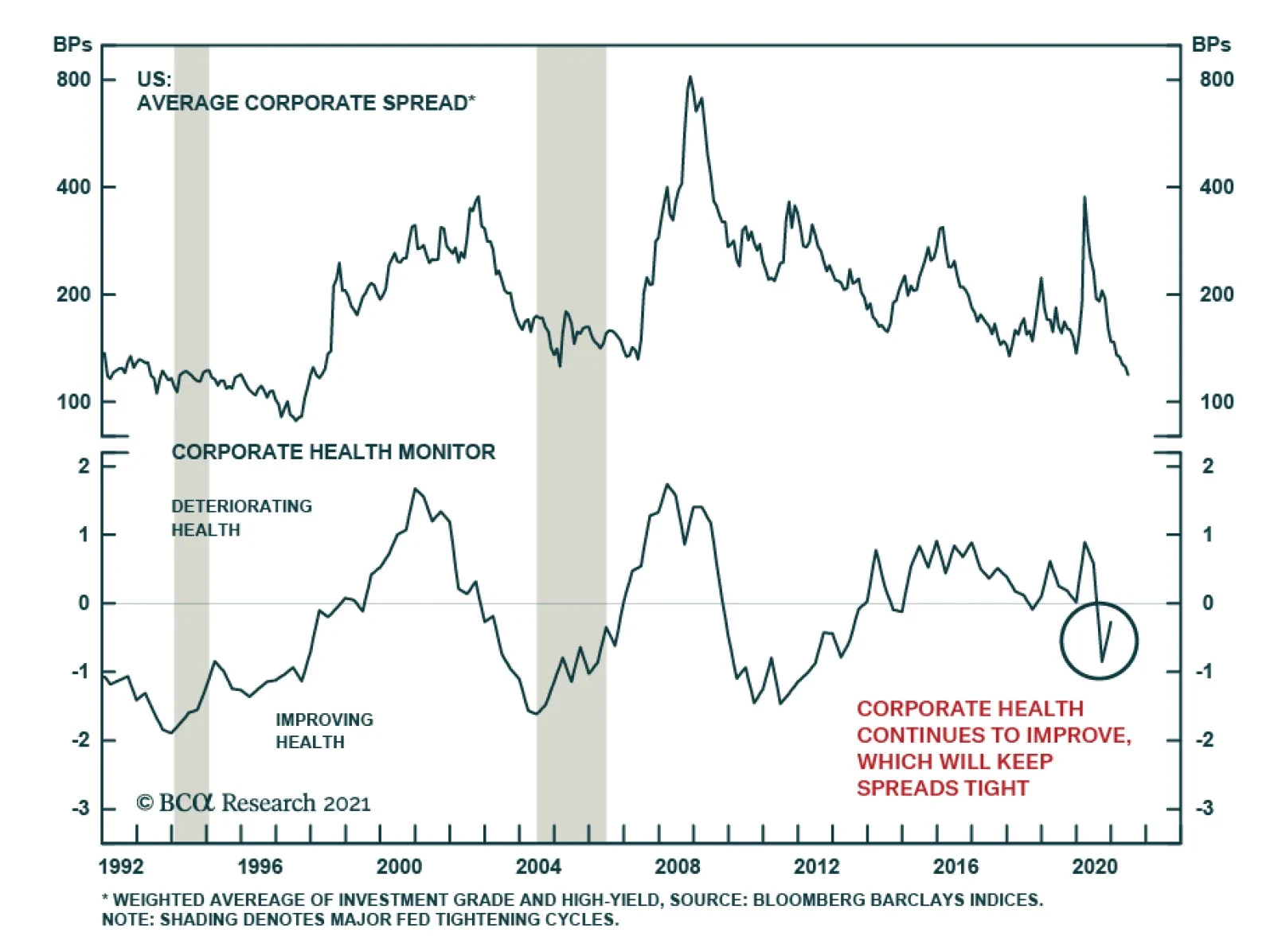

Highlights Spread Product: The macro environment is highly supportive for spread product and it will likely remain supportive for the next 12-18 months, at least until the yield curve flattens to below 50 bps. Remain overweight spread product versus Treasuries in US bond portfolios. High-Yield: High-yield spreads still look fairly valued, or even slightly cheap, compared to our base case outlook for corporate defaults. Investors should continue to favor high-yield over investment grade corporates and maintain an overweight allocation to high-yield in US bond portfolios. EM Corporates: Within the A and Baa credit tiers, US bond investors should favor USD-denominated EM corporates over USD-denominated EM sovereigns and should favor both over US corporate bonds. Within the Aa credit tier, investors should favor USD-denominated EM sovereigns over USD-denominated EM corporates and should favor both over US corporate bonds. Feature Chart 1Fed Meeting Didn't Shock Credit Markets

Fed Meeting Didn't Shock Credit Markets

Fed Meeting Didn't Shock Credit Markets

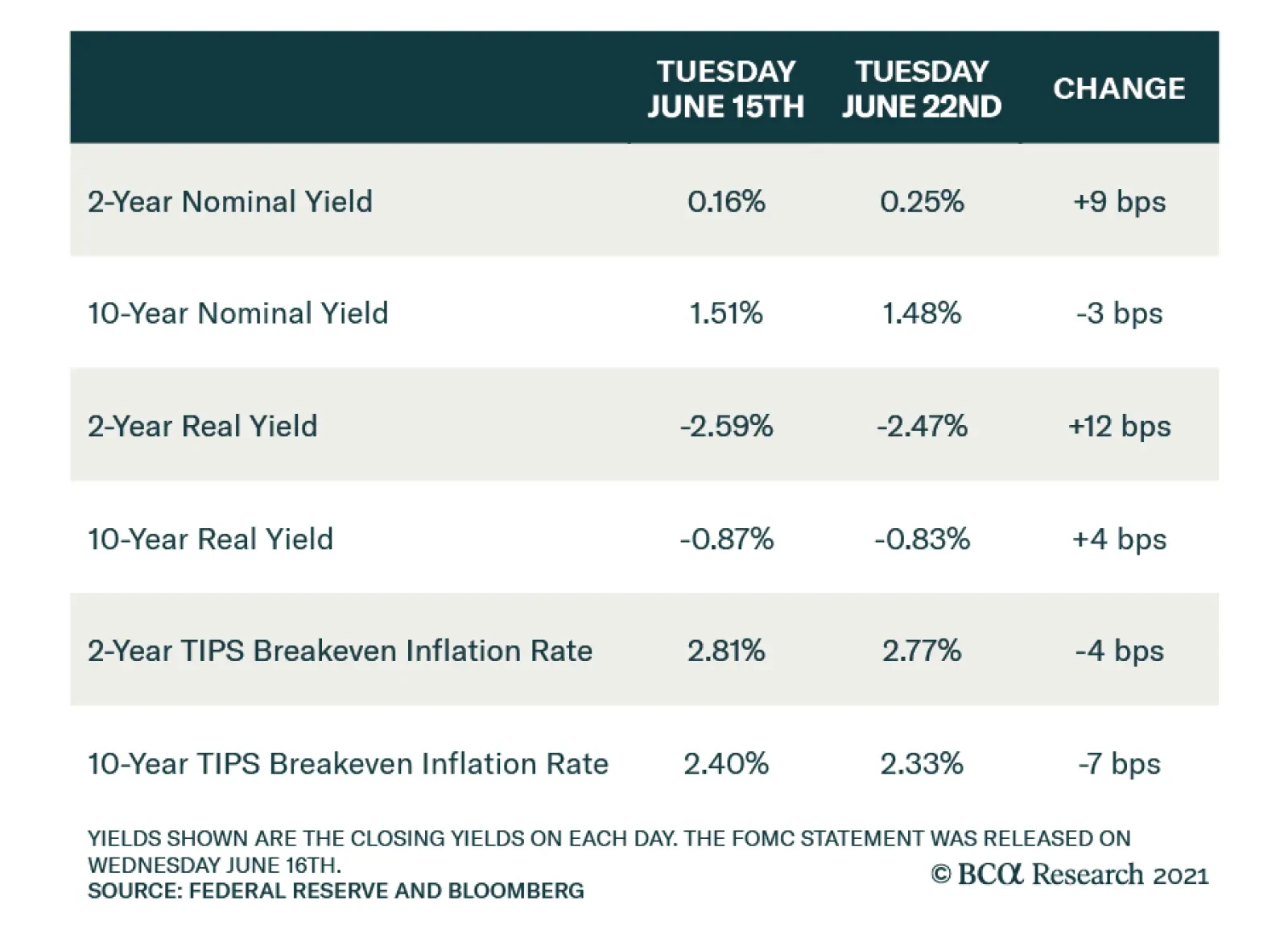

Last week’s report looked at how the June FOMC meeting prompted a massive re-shaping of the Treasury curve.1 It didn’t discuss, however, the impact that June’s meeting had on credit spreads. There’s a simple reason for this. Corporate bond spreads didn’t move very much post-FOMC. In fact, neither investment grade nor high-yield spreads have widened significantly during the past two weeks, despite the Fed’s apparent “hawkish turn” (Chart 1). The VIX jumped briefly above 20 in the days following the Fed meeting but it has since re-discovered its lows (Chart 1, bottom panel). This week’s report considers whether the corporate bond market is too complacent. The first section updates our assessment of where we are in the credit cycle based on two indicators that did see large swings post-Fed. The second section updates our outlook for high-yield defaults and considers whether junk spreads continue to offer adequate compensation. Finally, the third section of this report presents an introductory look at valuation in the USD-denominated Emerging Market (EM) corporate sector. We find that, for the most part, investment grade EM corporates are attractively valued relative to EM sovereigns and US corporates of the same credit rating and duration. Credit Cycle Update Chart 2Credit Cycle Indicators

Credit Cycle Indicators

Credit Cycle Indicators

As we have repeatedly stated in past research, the slope of the yield curve is a very important credit cycle indicator.2 We have documented that spread product tends to outperform duration-matched Treasuries by a wide margin when the yield curve is steep. This outperformance tapers off once the 3-year/10-year Treasury slope falls below 50 bps and it falls off even more when the slope dips below zero.3 With that in mind, it is notable that the Treasury curve flattened dramatically following the June FOMC meeting (Chart 2). At 106 bps, the 3-year/10-year Treasury slope remains well above the 50 bps threshold that would start to get concerning for spread product. However, it’s likely that the yield curve will continue to flatten as we approach a Fed rate hike in 2022. In other words, we expect that monetary conditions will turn sufficiently restrictive for us to reduce our recommended spread product allocation within the next 12-18 months. On the other hand, one positive development for spread product returns is that the 5-year/5-year forward TIPS breakeven inflation rate declined following the June FOMC meeting. In fact, it is now below the 2.3% to 2.5% range that is consistent with the Fed’s inflation target (Chart 2, bottom panel). This is a positive development for spread product because the Fed will strive to ensure that monetary conditions stay accommodative at least until these long-dated inflation expectations are consistent with the 2.3% to 2.5% target. Or put differently, a rebound in long-maturity TIPS breakeven inflation rates back to the target range will slow the near-term pace of curve flattening, giving the credit cycle a small amount of extra running room. In short, the macro environment is highly supportive for spread product and it will likely remain supportive for the next 12-18 months, at least until the yield curve flattens to below 50 bps. Investment Grade Corporates The highly supportive macro environment applies to investment grade corporate bonds, just as it does to all spread sectors. However, investment grade corporates have the problem that valuation is extremely tight. Much like a flat yield curve environment, a tight spread environment tends to coincide with low excess corporate bond returns. However, our research reveals that tight spreads alone are not sufficient for investment grade corporates to underperform duration-matched Treasuries. Table 1 classifies each month since May 1973 based on the investment grade corporate bond spread and the 3/10 Treasury slope. It then shows a 90% confidence interval for corporate bond excess returns during the following 12 months. It shows that, even when the corporate bond spread is below 100 bps (it is 81 bps today), investment grade corporates still tend to outperform duration-matched Treasuries as long as the 3/10 Treasury slope is above 50 bps. Table 1Expected 12-Month Corporate Bond Excess Return* (BPs) Based On OAS And Yield Curve Slope

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Bottom Line: The yield curve has started to flatten but it remains very steep, consistent with spread product outperforming duration-matched Treasuries. We remain overweight spread product versus Treasuries but will re-consider this position once the yield curve flattens to below 50 bps. We expect this could happen within the next 12-18 months. We maintain only a neutral allocation to investment grade corporate bonds because of stretched valuations. We see more attractive opportunities in high-yield corporates (see next section), municipal bonds, USD-denominated EM sovereigns and USD-denominated EM corporates (see final section below). High-Yield Default Update We last updated our default rate outlook in March.4 At that time, we concluded that junk spreads offered adequate compensation for expected default losses. Since then, we have received nonfinancial corporate sector profit and debt growth data for the first quarter of 2021, crucial inputs to our macro-based default rate model. Our macro-based model of the 12-month trailing speculative grade default rate is based on nonfinancial corporate sector gross leverage (i.e. pre-tax profits over total debt) and C&I lending standards (Chart 3). Lending standards enter our model with a lag, but we need a forward-looking estimate of gross leverage for our model to generate predictions. Chart 3Macro-Driven Default Rate Model

Macro-Driven Default Rate Model

Macro-Driven Default Rate Model

To estimate gross leverage we first model corporate profit growth based on real GDP (Chart 4) and assume that real GDP grows by 7% over the next four quarters, consistent with the Fed’s median forecast. This gives us a profit growth expectation of roughly 30%. Chart 4Profit & Debt Growth

Profit & Debt Growth

Profit & Debt Growth

We also need an estimate for corporate debt growth. Corporate debt exploded last year, growing 10% in 2020, but it then slowed to an annualized rate of 4% in Q1 2021. We think corporate debt growth will remain slow going forward. The nonfinancial corporate sector financing gap has been negative in each of the past four quarters (Chart 4, bottom panel), meaning that retained earnings have exceeded capital expenditures. In other words, firms have built up a lot of excess capital that can be deployed in place of debt to finance new investment opportunities. Table 2 shows our model’s predicted 12-month default rate based on different assumptions for profit and debt growth. If we assume corporate profit growth of 30% and corporate debt growth between 0% and 8%, then our model predicts that the 12-month default rate will fall from its current 5.5% to a range of 2.3% - 2.8%. Table 2Default Rate Scenarios

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Next, we need to consider what sort of expected default rate is priced into the High-Yield index. Our analysis of historical junk spreads and returns suggests that we should require a minimum excess spread of 100 bps in the High-Yield index after subtracting default losses to be confident that junk bonds will outperform Treasuries.5 If we also assume a recovery rate of 40% on defaulted debt, then we calculate that the High-Yield index is fairly priced for a 12-month default rate of 2.9% (Chart 5). That is, junk spreads appear slightly cheap compared to the 2.3% - 2.8% range predicted by our macro model. Finally, it’s worth noting that actual corporate default events have been quite rare in recent months. In the first five months of 2021 we’ve seen between 1 and 3 default events per month. If we extrapolate that trend and assume we see 3 defaults per month going forward, then we calculate that the 12-month trailing default rate will fall to 2.0% by December, before leveling off at 2.2% (Chart 6). In other words, the recent trend has been one of significantly fewer defaults than predicted by our macro model Chart 5Spread-Implied Default Rate

Spread-Implied Default Rate

Spread-Implied Default Rate

Chart 6Recent Default Trends

Recent Default Trends

Recent Default Trends

Bottom Line: High-yield spreads still look fairly valued, or even slightly cheap, compared to our base case outlook for corporate defaults. Investors should continue to favor high-yield over investment grade corporates and maintain an overweight allocation to high-yield in US bond portfolios. An Attractive Opportunity In EM Corporates This week we present an introductory look at the risk/reward opportunity in USD-denominated EM corporate bonds. Specifically, we look at the investment grade Bloomberg Barclays USD-denominated EM Corporate & Quasi-Sovereign index. We compare this index to both the investment grade USD-denominated EM Sovereign index and the US Credit index.6 First, we look at recent performance trends and average index statistics (Table 3). Both the EM Corporate and EM Sovereign indexes have average credit ratings between A and Baa, so we compare their performance to the A-rated and Baa-rated US Credit indexes. We observe a significant option-adjusted spread (OAS) advantage in both the EM indexes, though part of the extra spread offered by the Sovereign index is compensation for its longer duration. The EM Corporate index sticks out as offering an extremely attractive OAS per unit of duration. Table 3Performance Trends & Index Statistics

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

As for performance, we see that the EM Corporate index experienced less of a drawdown (in excess return terms) during the COVID recession, though it has also returned less than both the EM Sovereign index and the Baa Credit index during the recent upswing. Chart 7Spreads Versus Credit Rating & Duration-Matched US Credit

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Next, we look at each individual credit tier of both the EM Corporate & Quasi-Sovereign index and the EM Sovereign index, and we calculate the spread relative to a credit rating and duration-matched position in the US Credit index (Chart 7). In general, we see that both EM indexes offer a spread advantage versus duration-matched US Credit across all credit rating tiers. EM sovereigns look better than EM corporates in the Aa credit tier. This is the result of attractive spreads on the sovereign bonds of UAE and Qatar. However, EM corporates clearly dominate sovereigns in both the A and Baa credit tiers. Finally, we consider the risk/reward trade-off in our EM indexes by using our Excess Return Bond Map. Our Excess Return Bond Map shows the relationship between expected return (on the vertical axis) and risk (on the horizontal axis). In Chart 8A our risk measure is the 12-month spread widening required for each index to lose 100 bps versus a position in duration-matched Treasuries divided by that index’s historical spread volatility. It can be thought of as the number of standard deviations of spread widening required for the index to provide an excess return of -100 bps. A higher value corresponds to less risk, and vice-versa. Chart 8B uses the same risk measurement, only we use the spread widening required to lose 500 bps versus Treasuries to assess the risk of a large drawdown. Both Charts 8A and 8B use OAS as the measure of expected return. Chart 8AExcess Return Bond Map (100 BPs Loss Threshold)

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Chart 8BExcess Return Bond Map (500 BPs Loss Threshold)

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

The first thing that sticks out in Charts 8A & 8B is that Baa-rated EM corporates offer greater expected return and less risk than the EM Sovereign index and the Baa US Credit Index. This is true whether our loss threshold is set at 100 bps or 500 bps. Unfortunately, we do not have sufficient data to split the EM Sovereign index by credit tier in these charts. A-rated EM corporates offer slightly less expected return than the EM Sovereign index but with significantly less risk, they also clearly dominate the A-rated US Credit Index. Aa-rated EM corporates appear to offer a similar risk/reward trade-off as the EM Sovereign index, though we know from Chart 7 that sovereigns have a spread advantage in the Aa credit tier. The bottom line is that USD-denominated EM corporates are attractively valued relative to investment grade US corporate bonds with the same duration and credit rating. EM corporates also look preferable to EM sovereigns in the A and Baa credit tiers. EM sovereigns are more attractive than EM corporates in the Aa credit tier. Within the A and Baa credit tiers, US bond investors should favor USD-denominated EM corporates over USD-denominated EM sovereigns and should favor both over US corporate bonds. Within the Aa credit tier, investors should favor USD-denominated EM sovereigns over USD-denominated EM corporates and should favor both over US corporate bonds. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “How To Re-Shape The Yield Curve Without Really Trying”, dated June 22, 2021. 2 Please see US Bond Strategy Weekly Report, “Lower For Longer, Then Faster Than You Think”, dated May 25, 2021. 3 We use the 3-year/10-year Treasury slope in place of the more widely tracked 2-year/10-year slope in our credit cycle research only because using the 3-year/10-year slope allows us to include more historical cycles in our analysis. 4 Please see US Bond Strategy Weekly Report, “That Uneasy Feeling”, dated March 30, 2021. 5 Please see page 33 of the US Bond Strategy Quarterly Chartpack, “Testing The Limits Of Transitory Inflation”, dated May 18, 2021. 6 The US Credit Index consists predominantly of US corporate bonds, but also some non-corporate credit such as: Sovereigns, Foreign Agencies, Domestic Agencies, Local Authority bonds and Supranationals. Fixed Income Sector Performance Recommended Portfolio Specification

Feature Chart 1A Tug-Of-War In The US Treasury Market

A Tug-Of-War In The US Treasury Market

A Tug-Of-War In The US Treasury Market

This week, we are publishing one of our periodic reports, covering global central bank lending standard surveys. Yet given some of the moves seen in US bond markets recently, we felt the need to also provide some additional thoughts, along with that previously scheduled report. The short-term volatility of longer-maturity US Treasury yields since the June 16 FOMC meeting has been a bit extreme, to say the least. The 30-year yield fell from an intraday peak of 2.21% just before the Fed meeting to an intraday low of 1.93% on June 21, a 28bp plunge in a span of just three trading days, but has climbed back to 2.10% as we go to press. Over that same time frame, shorter maturity yields have been relatively more stable. After the 5-year yield rose from 0.78% on 0.93% immediately following the “hawkish” Fed surprise on FOMC Day, the yield has largely held those gains, hitting only a brief intraday low of 0.84% on June 21, and now sits at 0.90%. This price action is consistent with the two opposing forces currently at work in the US Treasury market. Investors are slowly repricing the expected path of Fed policy, pulling forward the liftoff date of the fed funds rate in line with the new “guidance” from the FOMC interest rate forecasts. This is putting upward pressure on the shorter maturity part of the Treasury curve. At the same time, the market continues to work off the deeply oversold condition that had developed in longer-maturity Treasuries, as we discussed in a recent report.1 The sharp volatility of the 30yr yield is consistent with a rapid adjustment of positioning, which had become very short when looking at measures like the CFTC data on 30-year bond futures net positioning (Chart 1). Chart 2Corporate Bond Investors Appear Far Less Worried Than Equity Investors

Corporate Bond Investors Appear Far Less Worried Than Equity Investors

Corporate Bond Investors Appear Far Less Worried Than Equity Investors

Once that overhang of short positioning in longer maturity yields is worked off, the overall Treasury yield curve will begin moving higher again, continuing the cyclical bear market. The next increase in yields, however, will look different than what occurred between August 2020 and March 2021, when rising growth and inflation expectations resulted in a bearish steepening of the Treasury curve. The next move will be led by yields rising more at the front end of the curve, as the Fed begins the long march toward policy normalization. This will result in a bearish flattening of the Treasury curve, which motivated us to introduce a new US yield curve trade last week along with our colleagues at BCA Research US Bond Strategy – going short a 5-year bullet versus going long a duration-matched 2-year/10-year barbell. We have added that trade to our Tactical Overlay portfolio using specific on-the-run Treasury bonds, as can be seen in the table on page 7.2 While yields are jumping around in government bond markets, credit markets remain calm. Corporate bond spreads have been grinding tighter, in line with the steady decline in the VIX index of US equity volatility (Chart 2). Yet investors in other asset classes are exhibiting more cautious optimism. The soaring SKEW index has climbed to an all-time high, suggesting that demand for downside portfolio protection via S&P 500 put options is very robust with the equity index also at an all-time high. However, with the VIX falling, economic growth remaining solid, bank lending standards easing and the Fed not expected to even begin tapering its asset purchases until the start of 2022, the backdrop remains generally positive for US corporate debt versus US Treasuries. Next week, we will be presenting our quarterly review of the Global Fixed Income Strategy model bond portfolio, where we will present our base case and tail risk scenarios for global bond markets over the remaining months of 2021, along with our recommended portfolio positioning. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Report, “A Summer Nap For Global Bond Yields”, dated June 9, 2021, available at gfis.bcaresearch.com. 2 Please see BCA Research US Bond Strategy/Global Fixed Income Strategy Report, “How To Re-Shape The Yield Curve Without Really Trying”, dated June 22, 2021, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Some Brief Comments On Recent US Bond Market Moves

Some Brief Comments On Recent US Bond Market Moves

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Despite the Fed backing away from the point of maximum monetary accommodation, threats to the corporate spreads are low. To begin with, even if QE ends this year and interest rates start rising in 2023, the fed funds rate remains far below the neutral rate…

Highlights Euro Area debt loads have increased significantly during the pandemic. Debt loads are not uniform. While Germany and, to a lesser extent, Spain look best, France has a less attractive total debt profile than Italy. Government debt-service ratios are not a problem for Europe. Private sector debt service ratios do not represent an imminent risk, but the French corporate sector is an important source of long-term vulnerability for the region. As a result of this indebtedness, Euro Area bond yields will not rise much and will be capped below 1.5% over this business cycle. For now, Eurozone corporate bonds remain attractive within a European fixed-income portfolio. High-yield bonds are appealing, but investors should avoid the energy sector. Feature Like the US, the Eurozone economy has witnessed a large increase in debt following the COVID-19 crisis. This debt load will have a long legacy that will impact the ability of the European Central Bank to increase interest rates over the coming years. The French corporate sector will be a particularly vulnerable pressure point. Nonetheless, in the short-term, this uptick in indebtedness will not have a major impact on European debt markets. Disparate Debt Loads… Chart 1The Eurozone's Heavy Debt Load

The Eurozone's Heavy Debt Load

The Eurozone's Heavy Debt Load

After a period of decline in the wake of both the GFC and the European debt crisis, total nonfinancial debt rose by 29% of GDP since the COVID-19 pandemic began (Chart 1). While some of this increase reflects a declining GDP, Euro Area Households and Corporations together added EUR609 billion of debt, while governments accumulated over EUR1 trillion more to their borrowings. The aggregate European picture does not impart the more complex reality. While all countries experienced a marked rise in indebtedness, some major economies are in a much more precarious position than others. The Good Among the largest Eurozone economies, Germany sports the most favorable debt profiles and represents the smallest threat to the Eurozone. Compared with the other major Euro Area countries, Spain shows healthier trends, even if its overall debt load remains important. At 202%, Germany’s nonfinancial-debt-to-GDP ratio is still below its all-time high of 211% (Chart 2, top panel). During the crisis, household debt rose by EUR296 billion or 4% of GDP, but it still stands well below the 72% registered at the turn of the millennium. In absolute terms, nonfinancial corporate debt has increased to a record, but it remains 5% below its 2003 high (Chart 2, third panel). Despite a 9% rebound to 70% of GDP, government debt still lies nearly 12% below its 2010 summit (Chart 2, bottom panel). In Spain, total nonfinancial debt rose by 45% of GDP since the pandemic started, but remains 12% below its 2013 all-time high of 301%. However, the private sector’s borrowing is well behaved, and it has only risen to 170% of GDP, well below the 227% level recorded in 2010 (Chart 3, top panel). Both the household and corporate sectors have gone a long way toward improving their debt situation, with borrowing 23% and 33%, respectively, below their crisis peaks (Chart 3, second and third panel). Spain’s problem is government debt. The pandemic forced the public sector to borrow EUR316 billion, which pushed its debt load to 120% of GDP (Chart 3, bottom panel). Chart 2Germany Is The Best Student

Germany Is The Best Student

Germany Is The Best Student

Chart 3Spain's Previous Efforts Have Paid Off

Spain's Previous Efforts Have Paid Off

Spain's Previous Efforts Have Paid Off

The Bad Chart 4Italy Remains Problematic

Italy Remains Problematic

Italy Remains Problematic

Italian debt remains a troublesome spot for the Eurozone, which sheds some light on the higher interest rate commanded by BTPs. Burdened by tepid GDP growth, Italy’s total nonfinancial debt did not decline much in the years between the European debt crisis and the onset of the pandemic. As a result, overall nonfinancial debt jumped to an all-time high of 276% of GDP in response to COVID-19 (Chart 4, top panel). Private sector nonfinancial credit is high by Italian standards, but at 120% of GDP, it is low compared with other major European or G-10 nations. Italian household debt has hit a record high of 45% of GDP, which also compares well to other countries, while corporate debt rose to 76% of GDP, which is also well below historical highs and other nations (Chart 4, second and third panels). Italy’s perennial problem remains the public sector’s debt, which stands at 156% of GDP, the highest reading among major Eurozone nations. The Ugly The major Eurozone country with the worst debt situation is France, and we expect this country to become an increasingly large hurdle on the ability of the ECB to lift rates in the future. Next week, we will devote a Special Report to the French situation. Chart 5France's Debt Binge

France's Debt Binge

France's Debt Binge

France’s nonfinancial debt towers above 350% of GDP, and the private sector nonfinancial debt has also hit an all-time high of 240% of GDP (Chart 5, top panel). No sector is spared. French households have accumulated EUR239 billion of liabilities during the pandemic, which pushed their leverage ratio to an all-time high of nearly 70% of GDP (Chart 5, second panel). Meanwhile, after rising by 21%, nonfinancial corporate credit stands above 170% of GDP (Chart 5, third panel). Finally, at 116% of GDP, public debt may not be as high as in Italy, but it is comparable to that of Spain (Chart 5, bottom panel). Bottom Line: The Eurozone indebtedness has hit a record high, but considering this factor in isolation oversimplifies a complicated picture. Among the major economies, Germany has the cleanest balance sheet, especially in terms of its private sector. Spain continues to sport high leverage, but the private sector remains in much better shape than last decade. Italy has made little progress, but it still looks good compared with France, where both the public and private sector borrowings stand at record highs. … And Debt Servicing Costs With the exception of the French corporate sector, debt-servicing costs do not represent a great risk for Europe. Chart 6Interest Payments Are Not The Government's Problem

Interest Payments Are Not The Government's Problem

Interest Payments Are Not The Government's Problem

When it comes to governments, the picture is particularly benign. As Chart 6 illustrates, debt-servicing costs as a percentage of GDP or tax revenues are extremely low in both France and Germany. While these two variables are higher in Italy and Spain, they remain distant from the levels recorded during the European debt crisis. Beyond their low levels, a very accommodative policy environment limits the risk created by Europe’s public debt servicing costs. The ECB has purchased EUR1.3 trillion of government bonds since April 2020, which added to its already large ownership. Moreover, BCA’s Global Fixed Income Strategy service, as well as this publication, anticipates that the ECB will roll the stock of government paper purchased under the PEPP into the PSPP. Beyond the ECB’s actions, the NGEU funds also create the embryo of fiscal risk sharing in the EU, which limits how far yields (and thus debt servicing costs) will rise in the Italy or Spain. For the private sector, the picture is more nuanced. In Germany, household debt-servicing costs are low, both historically and compared with other nations. Meanwhile, BIS data highlights that the nonfinancial corporate debt services consume a larger share of operating cash flows than at any point over the past 20 years, but they remain low by international standards (Chart 7, top panel). Meanwhile, in Spain and Italy, both the household and nonfinancial corporate sectors sport historically low debt servicing costs (Chart 7, second and third panels), which also compare well to other OECD nations. Once again, France stands out. Its household debt servicing costs are historically elevated, even if they are not particularly demanding at a global level. However, the corporate sector spends a substantial share of its cash flow on debt, both compared with its own history and internationally (Chart 7, bottom panel). Chart 7Debt Servicing Costs Across Europe

Debt Servicing Costs Across Europe

Debt Servicing Costs Across Europe

Bottom Line: Generally, the debt-service picture in Europe does not represent a major threat for now. While risks are particularly well contained on the government front, the French corporate sector creates danger for the private sector. Investment Implications The elevated debt load in the Euro Area, especially in the corporate sector, constitutes a crucial limiting factor for interest rates in Europe over the coming business cycle. Compared with global economies, the Eurozone corporate sector sports elevated debt ratios. As Chart 8 illustrates, the Eurozone’s net debt-to-equity ratio is higher than that of the US across most sectors, and even surpasses that of Canada, another country with a heavily indebted corporate sector, for telecommunication firms and financials. The picture is even worse when looking at the net debt-to-EBITDA ratio. Except for energy and utilities, the Eurozone carries poorer numbers than both the US and Canada (Chart 9). Chart 8Debt-To-Equity Ratio Comparison

A Lot Of Debt

A Lot Of Debt

Chart 9Net Debt-To-EBITDA Comparison

A Lot Of Debt

A Lot Of Debt

The picture for debt service payments is even more damning. Despite the very low European corporate bond rates, Eurozone corporations generally have poorer interest rate coverage ratios than both the US and Canada (Chart 10). This indicates that, unless the subpar European profitability is resolved, significantly higher interest rates will cause significant damage to the European corporate sector. Chart 10Interest Coverage Lags In Europe

A Lot Of Debt

A Lot Of Debt

Chart 11The French Corporate Sector And Dutch Households Will Limit The ECB

A Lot Of Debt

A Lot Of Debt

On this front, the French corporate sector once again stands out as the most likely place for an accident. As the top panel of Chart 11 shows, French firms are positioned especially poorly, with both their debt-to-GDP and debt-servicing costs among the highest in advanced economies. Meanwhile, in the household sectors, only the Netherlands represents a potential risk (Chart 11, bottom panel). The level of corporate debt in the Eurozone and in France in particular suggests that the current level of yields in Canada may represent a cap on European long-term rates. Thus, it will be difficult for German yields to move beyond the 1% to 1.5% zone this cycle. For now, despite the elevated debt loads of the European corporate sector, we continue to overweight corporate bonds within European fixed-income portfolios. The ECB will maintain very accommodative monetary conditions for the next 24 months, at least. Moreover, the European recovery, especially in the service sector, will improve the operating cash flows of the corporate sector, and thus, increase the tolerance of the private sector for higher yields in the near terms. Finally, the strength in the Euro anticipated by BCA’s Foreign Exchange strategists will limit the upside to Eurozone inflation, and thus, to yields in the region. Nonetheless, investors should avoid certain sectors (see next section). Market Focus: How To Play Euro Area High Yield Bonds? Chart 12Valuations Are Getting Expensive

Valuations Are Getting Expensive

Valuations Are Getting Expensive

We have argued that investors should continue to favor investment grade corporate bonds within European fixed-income portfolios over high-yield corporate bonds. Eurozone investment grade credit still offered enough value to delay a move down in quality (Chart 12). However, this value cushion is thinning and spreads are only 10 bps from their 2018 lows. BCA Research’s Global Fixed-Income strategists have recently increased their allocation to Euro Area high-yield to overweight, with a focus on the Ba-rated credit tier, while maintaining a neutral weighting in IG credit. However, European high-yield is also becoming expensive. The yield on the overall index is a meagre 44 bps away from its lows of 2018. Moreover, the breakeven spreads of European junk bonds have only been more expensive 11% of the time since 2000 (Chart 12, bottom panel). Despite these observations, high-yield credit is not a uniform block. Caa-rated debt still offers decent value, with a breakeven spread historical percentile standing at 27%. The stretched level of valuation suggests that investors should become more selective in the high-yield space, in order to avoid the industries with the worst risk profiles. To assess the sectors most at risk of experiencing significant spread widening or default occurrences in the coming quarters, we evaluate how the 10 main high-yield industry groups, as defined by Bloomberg Barclays, perform on the following credit metrics: Risk profile The share of firms rated Caa Growth in value of debt outstanding over the past 10 years Change in net debt-to-EBITDA ratio over the past 10 years Risk Profile Chart 13Risk Profile Of HY Sectors

A Lot Of Debt

A Lot Of Debt

We look at the duration-times-spread (DTS) ratio to determine the risk profile of each sector (Chart 13). The DTS is a simple measure that correlates closely with excess return volatility for corporate bonds. The ratio of an issue’s, or sector’s DTS, to that of the benchmark index is loosely equivalent to the beta of a stock or industry to the equity benchmark. A DTS ratio above 1.0 signals that the sector is cyclical (or “high beta”); a DTS ratio below 1.0 indicates that the sector is defensive (or “low beta”). Cyclical sectors are expected to outperform (underperform) the benchmark when spreads are narrowing (widening), while the opposite is expected of defensive sectors. In Europe, only three sectors sport a high DTS. Within these cyclical sectors, energy clearly stands out as essentially being the one most at risk of underperforming during the next episode of spread widening. Meanwhile, materials, healthcare, and utilities display the lowest DTS ratios and should trade defensively relative to the high-yield benchmark index. Share of Caa-rated debt Chart 14High Share Of Caa-Rated Debt Implies Higher Risk Of Default

A Lot Of Debt

A Lot Of Debt

The bulk of defaults happens in the Caa-rated space and below. Hence, evaluating sector risk starts by assessing the share of Caa-rated (and below) debt sported by each industry (Chart 14). Sectors bearing a larger share of low-rated debt should display higher spreads. Consumer non-cyclicals and healthcare have the highest instance of low-rated debt, 16% and 13% respectively, and yet their spreads do not adequately compensate investors for this threat. The energy sector also stands out: spreads are wide because, despite the low percentage of Caa-rated debt, this sector has amassed considerable debt and has seen a meaningful deterioration in net debt-to-EBITDA (see below). Meanwhile, utilities shine under this metric, as they have not issued debt rated Caa or lower. Debt Growth Chart 15Debt Growth Justify Spread Levels

A Lot Of Debt

A Lot Of Debt

The speed and amount of debt accumulated during economic recoveries are other important determinants of future spread volatility, because the sectors that have rapidly levered-up are more likely to experience defaults. Chart 15 shows that, if we ignore the outlying utilities, then there is a robust positive linear relationship between this metric and spreads. Utilities, energy, and the tech sectors have added the most debt, while debt accumulation in the basic materials and health care sectors has lagged over the past 10 years. Crucially, tech and communications spreads trade below what their debt growth implies. Net Debt-To-EBITDA Chart 16Only Financials Have Improved Their Net Debt-To-EBITDA

A Lot Of Debt

A Lot Of Debt

A rapid debt accumulation is not a concern, as long as earnings are rising more rapidly or at least at the same pace. From this case, we infer that companies are using the new debt issued efficiently, for CAPEX or to pursue projects exceeding their IRR. In this light, wide spreads are justified for the energy, consumer cyclical, and consumer non-cyclical sectors (Chart 16). Conversely, financials have seen improvement. Bottom Line: After surveying Euro area high-yield corporate sectors based on four credit metrics, it appears that the sectors most at risk are energy and consumer non-cyclical. By contrast, basic materials seem to be a good sector in which to hide. Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com Jeremie Peloso, Associate Editor JeremieP@bcaresearch.com Currency Performance

A Lot Of Debt

A Lot Of Debt

Fixed Income Performance Government Bonds

A Lot Of Debt

A Lot Of Debt

Corporate Bonds

A Lot Of Debt

A Lot Of Debt

Equity Performance Major Stock Indices

A Lot Of Debt

A Lot Of Debt

Geographic Performance

A Lot Of Debt

A Lot Of Debt

Sector Performance

A Lot Of Debt

A Lot Of Debt

Highlights The ongoing transition to a post-pandemic state and fiscal policy are either positive or net-neutral for risky asset prices. Fiscal thrust will turn to fiscal drag over the coming year, but the negative impact this will have on goods spending will likely be offset by a significant improvement in services spending, and thus is not likely to cause a concerning slowdown in overall economic activity. A modestly hawkish shift in the outlook for monetary policy is likely over the coming year, potentially occurring over the late summer or early fall in response to outsized jobs growth. However, such a shift is not likely to become a negative driver for risky asset prices over the coming 6-12 months, barring a major rise in market expectations for the neutral rate of interest. This may very well occur once the Fed begins to raise interest rates, but not likely before. Investors should overweight risky assets within a multi-asset portfolio, and fixed-income investors should maintain a below-benchmark duration position. We continue to favor value over growth on a 6-12 month time horizon, although growth may outperform in the near term. A bias toward value over the coming year supports an overweight stance toward global ex-US equities, and an overall pro-risk stance favors bearish US dollar bets. Feature Three factors continue to drive our global macroeconomic outlook and our cyclical investment recommendations. The first factor is our assessment of the global progress that is being made on the path to a post-pandemic state, and the return to pre-COVID economic conditions; the second is the likely contribution to growth from fiscal policy over the coming year; and the third is the outlook for monetary policy and whether or not monetary conditions will remain stimulative for both economic activity and financial markets. If the world continues to progress meaningfully on the path to a post-pandemic state, and if the impact of fiscal and monetary policy remains in line with market expectations, then we see no reason to alter our recommended investment stance. Equity market returns will be modest over the coming 6 to 12 months in this scenario given how significantly stocks have rebounded from their low last year, but we would still expect stocks to outperform bonds and would generally be pro-cyclically positioned. We present below our assessment of these three factors and their potential to deviate from consensus expectations over the coming year, to determine their likely impact on economic activity and financial markets. The Ongoing Transition To A Post-Pandemic World Chart I-1Enormous Progress Has Been Made In The Fight Against COVID-19

Enormous Progress Has Been Made In The Fight Against COVID-19

Enormous Progress Has Been Made In The Fight Against COVID-19

Chart I-1 highlights that meaningful progress continues to be made in vaccinating the world's population against COVID-19. North America and Europe continue to lead the rest of the world based on the share of people who have received at least one dose, but South America continues to make significant gains, and recent data updates highlight that Asia and Oceania are also making meaningful progress. Africa is the clear laggard in the war against SARS-COV-2 and its variants, but progress there has been delayed, at least in part, by India’s export restrictions of the Oxford-AstraZeneca/COVISHIELD vaccine. This suggests that, while Africa will continue to lag, the share of Africans provided with a first dose of vaccine will begin to rise once India resumes its exports and deliveries to African countries under the COVAX program continue. If variants of the disease were not a source of concern, Chart I-1 would highlight that the full transition to a post-pandemic economy over the next several months would be near certain. However, as evidenced by the recent decision in the UK to postpone the lifting of COVID-19 restrictions by 4 weeks due to the spreading of the Delta variant, the global economy is not entirely out of the woods yet. Encouragingly, the delay in the UK genuinely appears to be temporary. Chart I-2 highlights that while the number of confirmed UK COVID-19 cases has been rising over the past month, the uptick in hospitalizations and fatalities has so far been quite muted. Importantly, the rise in hospitalizations appears to be occurring among those who have not yet been fully vaccinated, underscoring that variants of the disease are only truly concerning if they are vaccine-resistant. The evidence so far is that the Delta variant is more transmissible and may increase the risk of hospitalization, but that two doses of COVID-19 vaccine offer high protection. Of course, vaccines only offer protection if you get them, and evidence of vaccination hesitancy in the US is thus a somewhat worrying sign. Chart I-3 shows that the daily pace of vaccinations in the US has slowed significantly from mid-April levels, resulting in a slower rise in the share of the population that has received at least one dose (second panel). On this metric, the US has recently been outpaced by Canada, and the gap between the UK and the US is now widening. Germany and France are close behind the US and may surpass it soon. Chart I-2The UK Delay In Removing Restrictions Seems Genuinely Temporary

The UK Delay In Removing Restrictions Seems Genuinely Temporary

The UK Delay In Removing Restrictions Seems Genuinely Temporary

Chart I-3Recent Vaccination Progress In The US Has Been Underwhelming

Recent Vaccination Progress In The US Has Been Underwhelming

Recent Vaccination Progress In The US Has Been Underwhelming

Sadly, Chart I-4 highlights that there is a political dimension to vaccine hesitancy in the US. The chart shows that state by state vaccination rates as a share of the population are strongly predicted by the share of the popular vote for Donald Trump in the 2020 US presidential election. Admittedly, part of this relationship may also be capturing an urban/rural divide, with residents in less-dense rural areas (which typically support Republican presidential candidates) perhaps feeling a lower sense of urgency to become vaccinated against the disease. Chart I-4The US Politicization Of Vaccines Raises The Risk From COVID-19 Variants

July 2021

July 2021

But given the clear politicization that has already occurred over some pandemic control measures, such as the wearing of masks, Chart I-4 makes it difficult to avoid the conclusion that the same thing has occurred for vaccines. This is unfortunate, and seemingly raises the risk that the Delta variant may spread widely in red states over the coming several months, potentially delaying economic reopening, or risking the reintroduction of pandemic control measures. However, there are two counterarguments to this concern. First, non-vaccine immunity is probably higher in red than blue states, and CDC data suggest that this effect could be large. While this figure is still preliminary and subject to change (and likely will), the CDC estimates that only 1 out of 4.3 cases of COVID-19 were reported from February 2020 to March 2021. Taken at face value, this implies that there were approximately 115 million infections during that period, compared with under 30 million reported cases. That gap accounts for 25% of the US population, and given that red states were slower to implement pandemic control measures last year and their residents often more resistant to the measures, it stands to reason that a disproportionate share of unreported cases occurred in these states. Second, as noted above, the evidence thus far suggests that the Delta variant is not vaccine resistant, at least for those who are fully vaccinated. This is significant because if Delta were to spread widely in red states over the coming several months, the resulting increase in hospitalizations would likely convince many vaccine hesitant Americans to become vaccinated out of fear and self-interest – two powerfully motivating factors. Thus, the Delta variant may become a problem for the US in the fall, but if that occurs a solution is not far from sight. And, in other developed countries where vaccine hesitancy rates appear to be lower, it would seem that a new, vaccine-resistant variant of the disease would likely be required in order to cause a major disruption in the transition to a post-pandemic state. Such a variant could emerge, but we have seen no evidence thus far that one will before vaccination rates reach levels that would slash the odds of further widespread mutation. Fiscal Policy: Passing The Baton To Services Spending Chart I-5 highlights that US fiscal policy is set to detract from growth over the coming 6-12 months, reflecting the one-off nature of some of the fiscal response to the pandemic. This is true outside of the US as well, as Chart I-6 highlights that the IMF is forecasting a two percentage point increase in the Euro Area’s cyclically-adjusted primary budget balance, representing a significant amount of fiscal drag relative to the past two decades. Chart I-5Fiscal Thrust Will Eventually Turn To Fiscal Drag In The US…

July 2021

July 2021

Should investors be concerned about the impact of fiscal drag on advanced economies over the coming year? In our view, the answer is no. The reason is that much of the fiscal response in the US and Europe has been aimed at supporting income that has been lost due to a drastic reduction in services spending, which will continue to recover over the coming months as the effect of the pandemic continues to ebb. Chart I-7 underscores this point by highlighting the “gap” in US consumer goods and services spending relative to its pre-pandemic trend. The chart highlights that US goods spending is running well above what would be expected, whereas there is a sizeable gap in services spending (which accounts for approximately 70% of US personal consumption expenditures). Goods spending will likely slow as fiscal thrust turns to fiscal drag, but services spending will improve meaningfully – aided not just by a post-pandemic normalization in economic activity, but also by the sizeable amount of excess savings that US households have accumulated over the past year (Chart I-7, panel 2). Chart I-6... And In Europe

... And In Europe

... And In Europe

Chart I-7But Reduced Transfers Will Only Impact Spending On Goods, Not Services

But Reduced Transfers Will Only Impact Spending On Goods, Not Services

But Reduced Transfers Will Only Impact Spending On Goods, Not Services

While some of these savings have already been deployed to pay down debt and some may be permanently saved in anticipation of higher future taxes, the key point for investors is that the negative impact on goods spending from reduced fiscal thrust will be offset by a significant improvement in services spending, and thus is not likely to cause a concerning slowdown in overall economic activity. Monetary Policy: A Modestly Hawkish Shift Is Likely This leaves us with the question of whether or not monetary policy will become a negative driver for risky asset prices over the coming 6-12 months, which is especially relevant following last week’s FOMC meeting. The updated “dot plot” following the meeting shows that 7 of the 18 FOMC participants anticipate a rate hike in 2022, and the majority (13 members) expect at least one rate hike before the end of 2023, raising the median forecast for the Fed funds rate to 0.6% by the end of that year. Chart I-8 highlights that while 10-year Treasury yields remains mostly unchanged following the meeting, yields moved higher at the short-end and middle of the curve. Chart I-8The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

Investor fears that the Fed may shift in a significantly hawkish direction at some point over the next year have been far too focused on inflation, and far too little focused on employment. It is not a coincidence that the Fed’s guidance was updated following the May jobs report, which saw a stronger pace of jobs growth relative to April. Table I-1 updates our US Bond Strategy service’s calculations showing the average monthly nonfarm payroll growth that will be required for the unemployment rate to reach 3.5-4.5% assuming a full recovery in the participation rate, which is the range of the Fed’s NAIRU estimates. May’s payroll growth number of 560k implies that the Fed’s maximum employment criterion will be met sometime between June and September next year, if monthly payroll growth continues at that pace. Table I-1Calculating The Distance To Maximum Employment

July 2021

July 2021

Chart I-9Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

It is currently difficult to assess with great confidence what average payroll growth will prevail over the coming year, but we noted in last month’s report that there were compelling arguments in favor of outsized jobs growth this fall.1 In addition to those points, we note the following: Blue states have generally been slower to reopen their economies, and Chart I-9 highlights that these states have consequently been slower to return to their pre-pandemic unemployment rate. Among blue states, California and New York are the largest by population, and it is notable that both states only lifted most COVID-19 restrictions on June 15 – including the wearing of masks in most settings. This implies that services jobs are likely to grow significantly in these states over the coming few months. Both consensus private forecasts as well as the Fed’s expectation for real GDP growth imply that the output gap will be closed by Q4 of this year (Chart I-10). These expectations appear to be reasonable, given the substantial amount of excess savings that have been accumulated by US households and the fact that monetary policy remains extremely stimulative. When the output gap turned positive during the last economic cycle, the unemployment rate was approximately 4% – well within the Fed’s NAIRU range. Chart I-10 also shows that the Fed’s 7% real GDP growth forecast for this year would put the output gap above its pre-pandemic level, when the unemployment rate stood at 3.5%. In fact, it is possible that annualized Q2 real GDP growth will disappoint current consensus expectations of 10%, due to the scarcity of labor supply (scarcity that will be eased by labor day when supplemental unemployment insurance benefit programs end). Were Q2 GDP to disappoint due to supply-side limitations, it would strengthen the view that job gains will be very strong this fall ceteris paribus, as it would highlight that real output per worker cannot rise meaningfully further in the short-term and that stronger growth later in the year will necessitate very large job gains. Chart I-11 highlights that US air travel and New York City subway ridership have already returned close to 75% and 50% of their pre-pandemic levels, respectively. Based on the trend over the past three months, the chart implies that air travel will return to its pre-pandemic levels by mid-October of this year, and New York City subway ridership by June 2022. This underscores that travel-related services employment will recover significantly in the fall, and that jobs in downtown cores will rebound as office workers progressively return to work. Chart I-10Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Chart I-11Services Employment Will Recover In The Fall

Services Employment Will Recover In The Fall

Services Employment Will Recover In The Fall

On the latter point, one major outstanding question affecting the outlook for monetary policy is the magnitude of the likely permanent impact of work from home policies on employment in central business districts. Fewer office workers commuting to downtown office locations suggests that some jobs in the leisure & hospitality, retail trade, professional & business services, and other services industries will never return or will be very slow to do so, arguing for a longer return to maximum employment (and the Fed’s liftoff date). We examine this question in depth in Section 2 of this month’s report, and find that the “stickiness” of work from home policies will likely cause permanent central business job losses on the order of 575k (or 0.35% of the February 2020 labor force). While this would be non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. Outsized jobs growth this fall, at a pace that quickly reduces the unemployment rate, argues for a first Fed rate hike that is even earlier than the market expects. Chart I-12 presents The Bank Credit Analyst service’s current assessment of the cumulative odds of the Fed’s liftoff date by quarter; we believe that it is likely that the Fed will have raised rates by Q3 of next year, and that a rate hike in the first half of 2022 is a possibility. These odds are slightly more aggressive than those presented by our fixed-income strategists in a recent Special Report,2 but are consistent with their view that the Fed will raise interest rates by the end of next year. Chart I-12The Bank Credit Analyst’s Assessment Of The Odds Of The First Rate Hike

July 2021

July 2021

The odds presented in Chart I-12 are also more hawkish than the Fed funds rate path currently implied by the OIS curve, meaning that we expect investors to be somewhat surprised by a shifting monetary policy outlook at some point over the coming year, potentially over the next 3-6 months. Payroll growth during the late summer and early fall will be a major test for the employment outlook, and is the most likely point for a hawkish shift in the market’s view of monetary policy. Is this likely to become a negative driver for risky asset prices over the coming 6-12 months? In our view, the answer is “probably not.” While investors tend to focus heavily on the timing of the first rate hike as monetary policy begins to tighten, the reality is that it is the least relevant factor driving the fair value of 10-year Treasury yields. Investor expectations for the pace of tightening and especially for the terminal Fed funds rate are far more important, and, while it is quite possible that expectations for the neutral rate of interest will eventually rise, it seems unlikely that this will occur before the Fed actually begins to raise interest rates given that most investors accept the secular stagnation narrative and the view that “R-star” is well below trend rates of growth (we disagree).3 Chart I-13 highlights the fair value path of 10-year Treasury yields until the end of next year, assuming a 2.5% terminal Fed funds rate, no term premium, and a rate hike pace of 1% per year. The chart highlights that while government bond yields are set to move higher over the coming 6-12 months, they are likely to remain between 2-2.5%. This would drop the equity risk premium to a post-2008 low (Chart I-14), which would further reduce the attractiveness of stocks relative to bonds. But we doubt that this would be enough of a decline to cause a selloff, and it would still imply a stimulative level of interest rates for households and firms. Chart I-1310-Year Yields Will Rise Over The Coming Year, But Not Sharply

10-Year Yields Will Rise Over The Coming Year, But Not Sharply

10-Year Yields Will Rise Over The Coming Year, But Not Sharply

Chart I-14Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Investment Conclusions Among the three factors driving our global macroeconomic outlook and our cyclical investment recommendations, continued progress on the path toward a post-pandemic state and fiscal policy remain either positive or mostly neutral for risky assets. A potentially hawkish shift in the outlook for monetary policy this fall remains the chief risk, but we expect the rise in bond yields over the coming year to remain well-contained barring a sea change in investor expectations for the terminal Fed funds rate – which we believe is unlikely to occur before the Fed begins to raise interest rates. Consequently, we continue to recommend that investors should overweight risky assets within a multi-asset portfolio, and that fixed-income investors should maintain a below-benchmark duration position. We expect modest absolute returns from global equities, but even mid-single digit returns are likely to beat those from long-dated government bonds and cash positions. While value stocks may underperform growth stocks over the coming 3-4 months,4 rising bond yields over the coming year will ultimately favor value stocks and will likely weigh on elevated tech sector (and therefore growth stock) valuations (Chart I-15). Chart I-16 highlights that the attractiveness of US value versus growth is meaningfully less compelling for the S&P 500 Citigroup indexes, suggesting that investors should continue to favor MSCI-benchmarked value over growth positions over a 6-12 month time horizon.5 Chart I-15Value Is Extremely Cheap

Value Is Extremely Cheap

Value Is Extremely Cheap

Chart I-16Value Vs. Growth: The Benchmark Matters

Value Vs. Growth: The Benchmark Matters

Value Vs. Growth: The Benchmark Matters

The likely outperformance of value versus growth also has implications for regional allocation within a global equity portfolio. The US is significantly overweight broadly-defined technology relative to global ex-US stocks, and financials – which are overrepresented in value indexes – have already meaningfully outperformed in the US this year compared with their global peers and are now rolling over (Chart I-17). This underscores that investors should favor ex-US stocks over the coming year, skewed in favor of DM ex-US given that China’s credit impulse continues to slow (Chart I-18). Chart I-17Favor Global Ex-US Stocks Over The Coming Year

Favor Global Ex-US Stocks Over The Coming Year

Favor Global Ex-US Stocks Over The Coming Year

Chart I-18Concentrate Global Ex-US Exposure In Developed Markets

Concentrate Global Ex-US Exposure In Developed Markets

Concentrate Global Ex-US Exposure In Developed Markets

Finally, global ex-US stocks also tend to outperform when the US dollar is falling, and we would recommend that investors maintain a short dollar position on a 6-12 month time horizon despite the recent bounce in the greenback. Chart I-19 highlights that the dollar remains strongly negatively correlated with global equity returns, and that the dollar’s performance over the past year has been almost exactly in line with what one would have expected given this relationship. Thus, a bullish view toward global stocks implies both US dollar weakness and global ex-US outperformance over the coming year. Chart I-19A Bullish View Towards Global Stocks Implies A Dollar Bear Market

A Bullish View Towards Global Stocks Implies A Dollar Bear Market

A Bullish View Towards Global Stocks Implies A Dollar Bear Market

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst June 24, 2021 Next Report: July 29, 2021 II. Work From Home “Stickiness” And The Outlook For Monetary Policy Work from home policies, originally designed as emergency measures in the early phase of the COVID-19 pandemic, are likely to be “sticky” in a post-pandemic world. This will negatively impact the labor market in central business districts, via reduced spending on services by office workers. The potential impact of working from home is often cited as an example of what is likely to be a lasting and negative effect on jobs growth, but we find that it is not likely to be a barrier to the labor market returning to the Fed’s assessment of “maximum employment.” The size of the impact depends importantly on whether employee preferences or employer plans for WFH prevail, but our sense is that the latter is more likely. A weaker pace of structures investment in response to elevated office vacancy rates will likely have an even smaller impact on growth than the effect of reduced central business district services employment. The contribution to growth from structures investment has been small over the past few decades, office building construction is a small portion of overall nonresidential structures, and there are compelling arguments that the net stock of office structures will stay flat, rather than decline. Our analysis suggests that job growth over the coming year could be even stronger than the Fed and investors expect, possibly resulting in a first rate hike by the middle of next year. This would be earlier than we currently anticipate, but it underscores that fixed-income investors should remain short duration on a 6-12 month time horizon, and that equity investors should favor value over growth positions beyond the coming 3-4 months. The outlook for US monetary policy over the next 12 to 18 months depends almost entirely on the outlook for employment. Many investors are focused on the potential for elevated inflation to force the Fed to raise interest rates earlier than it currently anticipates, but it is the progress in returning to “maximum employment” that will determine the timing of the first Fed rate hike – and potentially the speed at which interest rates rise once policy begins to tighten. In this report, we estimate the extent to which the “stickiness” of working from home (WFH) policies and practices could leave a lasting negative impact on the US labor market. We noted in last month's report that a large portion of the employment gap relative to pre-pandemic levels can be traced to the leisure & hospitality and professional and business services industries, both of which – along with retail employment – stand to be permanently impaired if the office worker footprint is much lower in a post-COVID world.6 Using employee surveys and a Monte Carlo approach, we present a range of estimates for the permanent impact of WFH policies on the unemployment rate, and separately examine the potential for lower construction of office properties to weigh on growth. We find that the impact of reduced office building construction is likely to be minimal, and that WFH policies may structurally raise the unemployment rate by 0.3 to 0.4%. While non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. Relative to the Fed’s expectations of a strong, lasting impact on the labor market from the pandemic, this suggests that job growth over the coming year could be even stronger than the Fed and investors expect, possibly resulting in a first rate hike by the middle of next year. This would be earlier than we currently anticipate, but it underscores that fixed-income investors should remain short duration on a 6-12 month time horizon, and that equity investors should favor value over growth positions beyond the coming 3-4 months (a period that may see outperformance of the latter). Quantifying The Labor Market Impact Of The New Normal For Work In a January paper, Barrero, Bloom, and Davis (“BBD”) presented evidence arguing why working from home will “stick.” The authors surveyed 22,500 working-age Americans across several survey “waves” between May and December 2020, and asked about both their preferences and their employer’s plans about working from home after the pandemic. Chart II-1 highlights that the desired amount of paid work from home days (among workers who can work from home) reported by the survey respondents is to approximately 55% of a work week, suggesting that a dramatic reduction in office presence would likely occur if post-pandemic WFH policies were set fully in accordance with worker preferences. Chart II-1Employee Preferences Imply A Dramatic Reduction In Post-COVID Office Presence

July 2021

July 2021

However, Table II-1 highlights that employer plans for work from home policies are meaningfully different than those of employees. The table highlights that employers plan for employees to work from home for roughly 22% of paid days post-pandemic, which essentially translates to one day per week on average.7 BBD noted that CEOs and managers have cited the need to support innovation, employee motivation, and company culture as reasons for employees’ physical presence. Managers believe physical interactions are important for these reasons, but employees need only be on premises for about three to four days a week to achieve this. Table II-1 also shows that employers plan to allow higher-income employees more flexibility in terms of working from home, and less flexibility to employees whose earnings are between $20-50k per year. Table II-1Employer Plans, However, Imply Less Working From Home Than Employees Prefer

July 2021

July 2021

Based on the survey results, BBD forecast that expenditure in major cities such as Manhattan and San Francisco will fall on the order of 5 to 10%. In order to understand the national labor market impact of work from home policies and what implications this may have on monetary policy, we scale up BBD’s calculations using a Monte Carlo approach that incorporates estimate ranges for several factors: The percent of paid days now working from home for office workers The amount of money spent per week by office workers in central business districts (“CBDs”) The number of total jobs in CBDs The percent of CBD jobs in industries likely to be negatively impacted by reduced office worker expenditure The average weekly earnings of affected CBD workers The average share of business revenue not attributable to strictly variable expenses The percent of affected jobs likely to be recovered outside of CBDs Our approach is as follows. First, we calculate the likely reduction in nationwide CBD spending from reduced office worker presence by multiplying the likely percent of paid days now permanently working from home by the number of total jobs in CBDs and the average weekly spending of office workers. This figure is then increased due to the estimated acceleration in net move outs from principal urban centers in 2020 (Chart II-2); we assume a 5% savings rate and an average annual salary of $50k for these resident workers, and assume that all of their spending occurred within CBDs. We also assume that roughly 50% of jobs connected to this spending are recovered. Chart II-2Fewer Residents Will Also Lower Spending In Central Business Districts

July 2021

July 2021

Then, we calculate the gross number of jobs lost in leisure & hospitality, retail trade, and other services by multiplying this estimate of lost spending by an estimate of non-variable costs as a share of revenue for affected industries, and dividing the result by average weekly earnings of affected employees. For affected CBD employees in the administrative and waste services industry, we simply assume that the share of jobs lost matches the percent of paid days now permanently working from home. Finally, we adjust the number of jobs lost by multiplying by 1 minus an assumed “recovery” rate, given that some of the reduction in spending in CBDs will simply be shifted to areas near remote workers’ residences. We assume a slightly lower recovery rate for lost jobs in the administrative and waste services industry. Table II-2 highlights the range of outcomes for each variable used in our simulation, and Charts II-3 and II-4 present the results. The charts highlight that the distribution of outcomes based on employer WFH intensions suggest high odds that nationwide job losses in CBDs due to reduced office worker presence will not exceed 400k. Based on average employee preferences, that number rises to roughly 800-900k. Table II-2The Factors Affecting Permanent Central Business District Job Losses

July 2021

July 2021

Chart II-3The Probability Distribution Of CBD Jobs Lost…

July 2021

July 2021

Chart II-4…Based On Our Monte Carlo Approach

July 2021

July 2021

This raises the question of whether employer plans or employee preferences for WFH arrangements will prevail. Our sense is that it will be closer to the former, given that we noted above that employer WFH plans are the least flexible for employees whose earnings are between $20-50k per year (who are presumably employees who have less ability to influence the policy of firms). Chart II-5 re-presents the projected job losses shown in Chart II-4 as a share of the February 2020 labor force, along with a probability-weighted path that assumes a 75% chance that employer WFH plans will prevail. The chart highlights that WFH arrangements would have the effect of raising the unemployment rate by approximately 0.35%. However, relative to a pre-pandemic starting point of 3.5%, this would raise the unemployment rate to a level that would still be within the Fed’s NAIRU estimates (Chart II-6). Therefore, the “stickiness” of WFH arrangements alone do not seem to be a barrier to the labor market returning to the Fed’s assessment of “maximum employment,” suggesting that the conditions for liftoff may be met earlier than currently anticipated by investors. Chart II-5CBD Job Losses Will Not Be Trivial, But They Will Not Be Enormous

July 2021

July 2021

Chart II-6Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

The Impact Of Lower Office Building Construction A permanently reduced office footprint could also conceivably impact the US economy through reduced nonresidential structures investment, as builders of commercial real estate cease to construct new office towers in response to expectations of a long-lasting glut. However, several points highlight that the negative impact on growth from US office tower construction will be even smaller than the CBD employment impact of reduced office worker presence that we noted above. First, Chart II-7 highlights the overall muted impact that nonresidential building investment has had on real GDP growth by removing the contribution to growth from nonresidential structures and for overall nonresidential investment. The chart clearly highlights that the historically positive contribution to real US output from capital expenditures over the past four decades has come from investment in equipment and intellectual property products, not from structures. Chart II-8 echoes this point, by highlighting that US real investment in nonresidential structures has in fact been flat since the early-1980s, contributing positively and negatively to growth only on a cyclical basis (not on a structural basis). Chart II-7Structures Have Not Contributed Significantly To US Growth For Some Time

Structures Have Not Contributed Significantly To US Growth For Some Time

Structures Have Not Contributed Significantly To US Growth For Some Time

Chart II-8Nonresidential Structures Investment Has Been Flat For Four Decades

Nonresidential Structures Investment Has Been Flat For Four Decades

Nonresidential Structures Investment Has Been Flat For Four Decades

Second, Table II-3 highlights that office properties make up a small portion of investment in private nonresidential structures. In 2019, nominal investment in office structures amounted to $85 billion, compared with $630 billion in overall structures investment, meaning that office properties amounted to just 13% of structures investment. Table II-3Office Structures Investment Is A Small Share Of Total Structures Investment

July 2021

July 2021

Table II-4Conceivably, Vacant Office Properties Could Be Converted To Luxury Residential Units

July 2021

July 2021