Fixed Income

Our Portfolio Allocation Summary for June 2025.

Bitcoin has become one of investors’ favorite assets to safeguard against fading US exceptionalism, but physical bullion has some macro advantages over its digital counterpart. First, bitcoin has benefited greatly from the selloff in Treasurys. While US…

Global currency markets have entered a new era. This implies that the framework for analyzing exchange rates must also change. We introduce a new framework for analyzing EM currencies and classify them into resilient and vulnerable categories. Finally, we are adding more EM domestic bonds to our portfolio and making many changes to our currency trades.

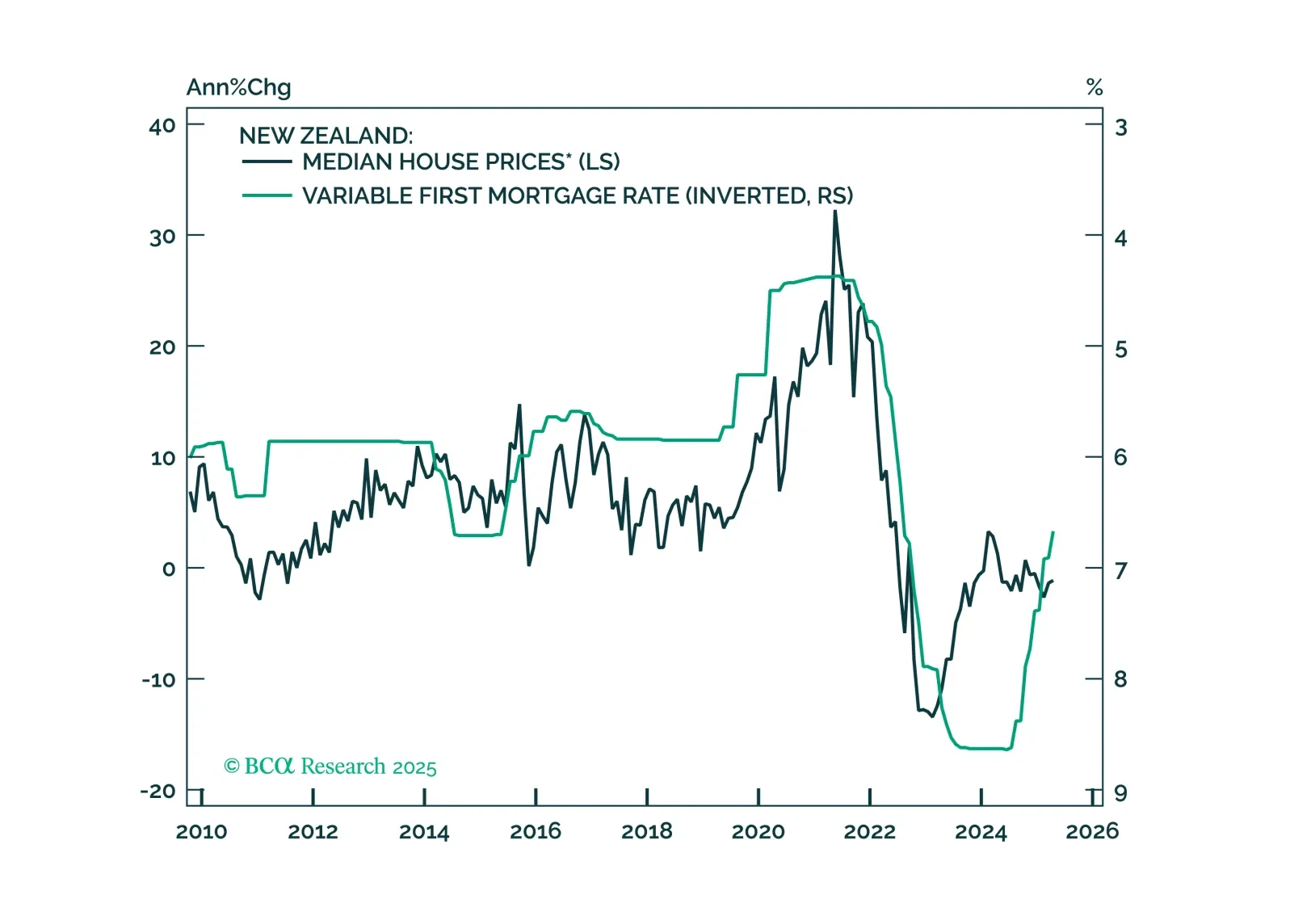

This Insight looks at the implications of the RBNZ’s rate cut on New Zealand assets.

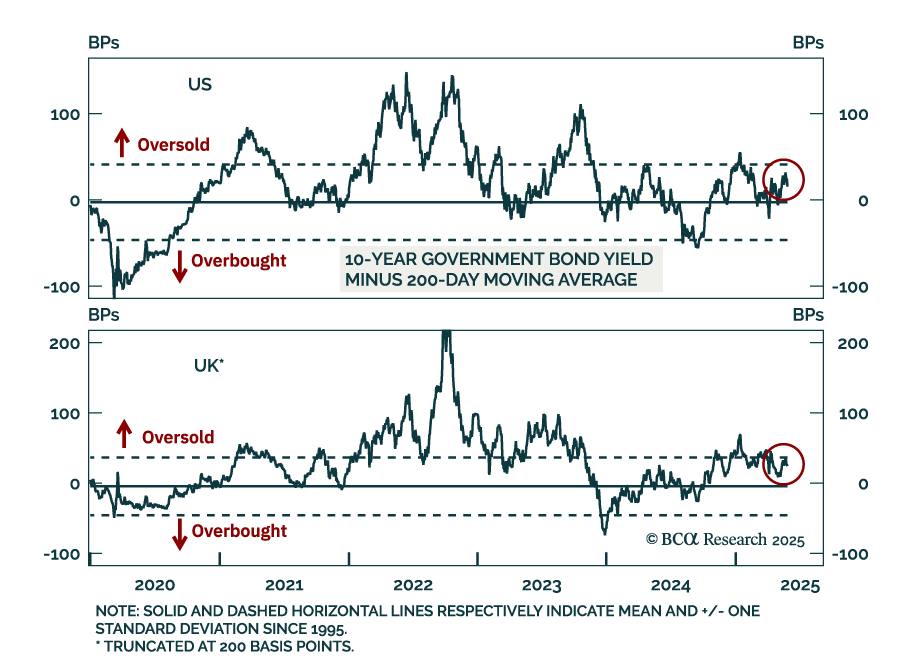

BCA’s latest technical analysis suggests that global bond markets are oversold, offering an attractive entry point to add long-duration bets in fixed-income portfolios. Our Global Fixed Income strategists analyzed a timing tool to assess when to adjust…

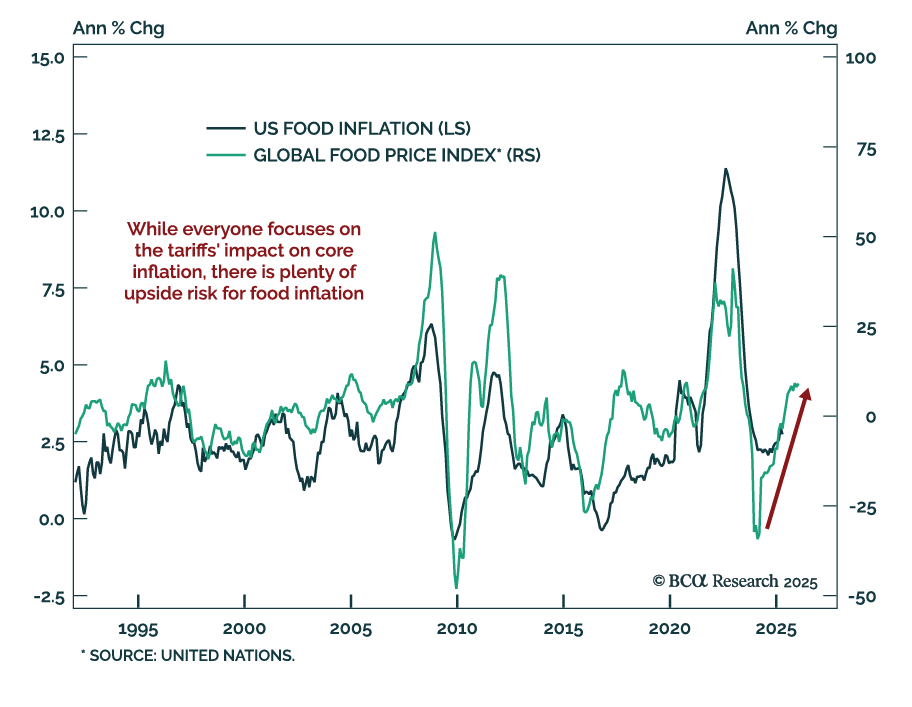

The upward trend in global food prices suggests that food inflation risks re-accelerating in the US. Historically, US food inflation lags the United Nations’ global food price index by about nine months. The annual growth in global food prices has been…

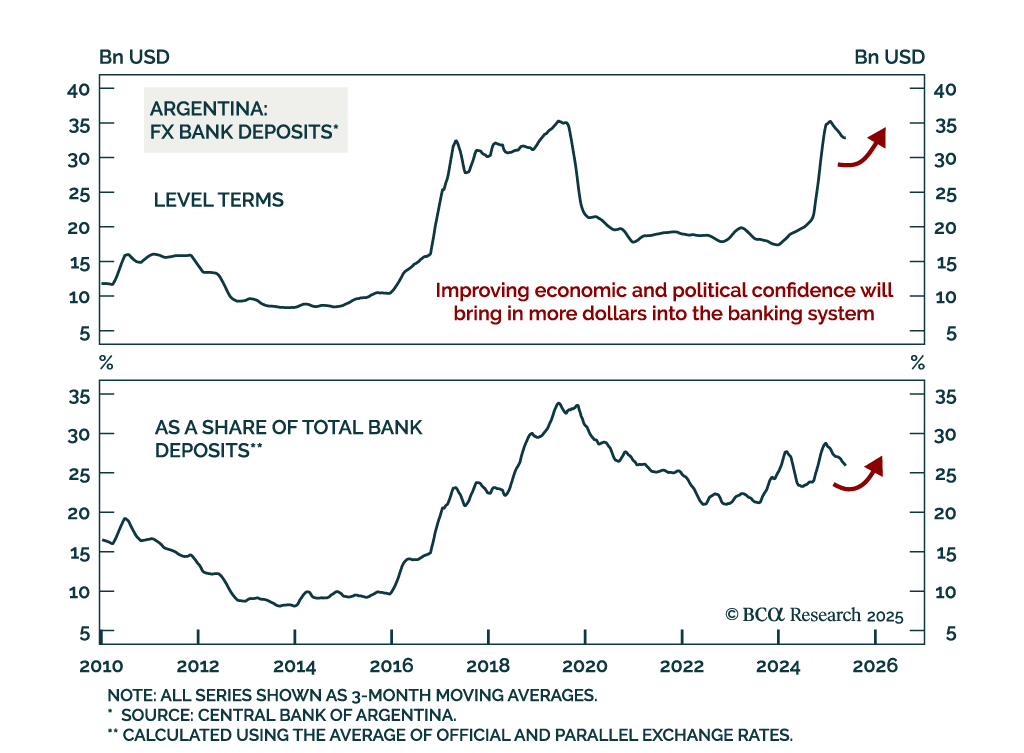

The latest political developments in Argentina increase the odds of further liberalizing reforms and solidify the economy’s structural upside. First, the libertarian governing party came out on top in Buenos Aires’ legislative elections. While municipal…

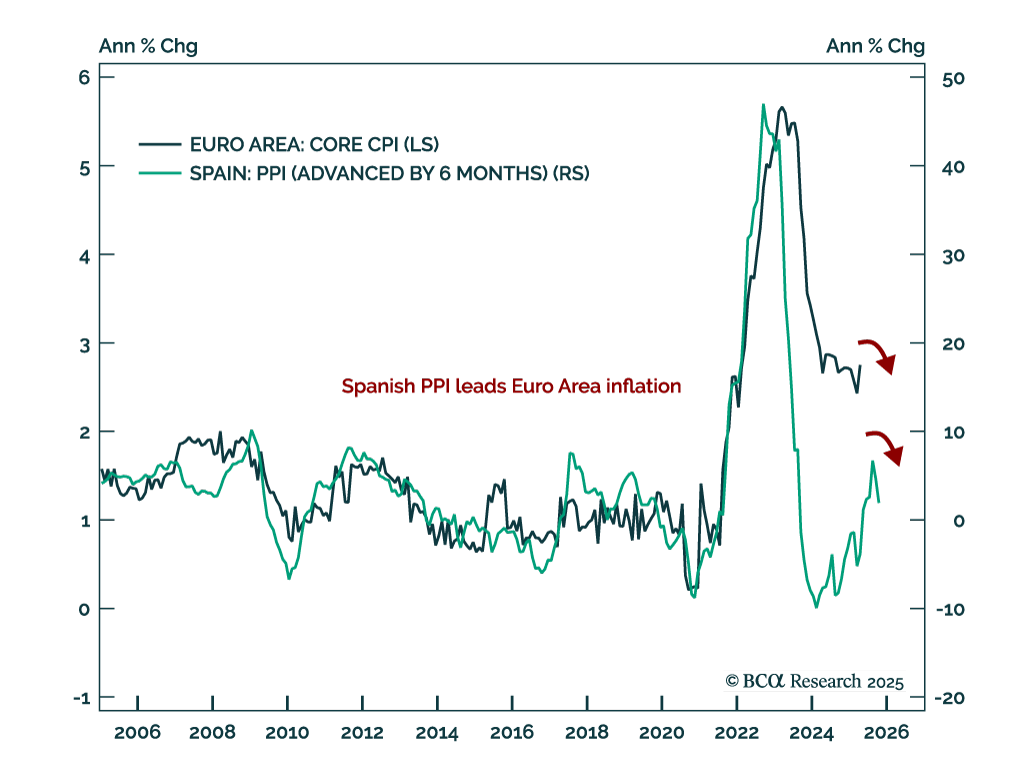

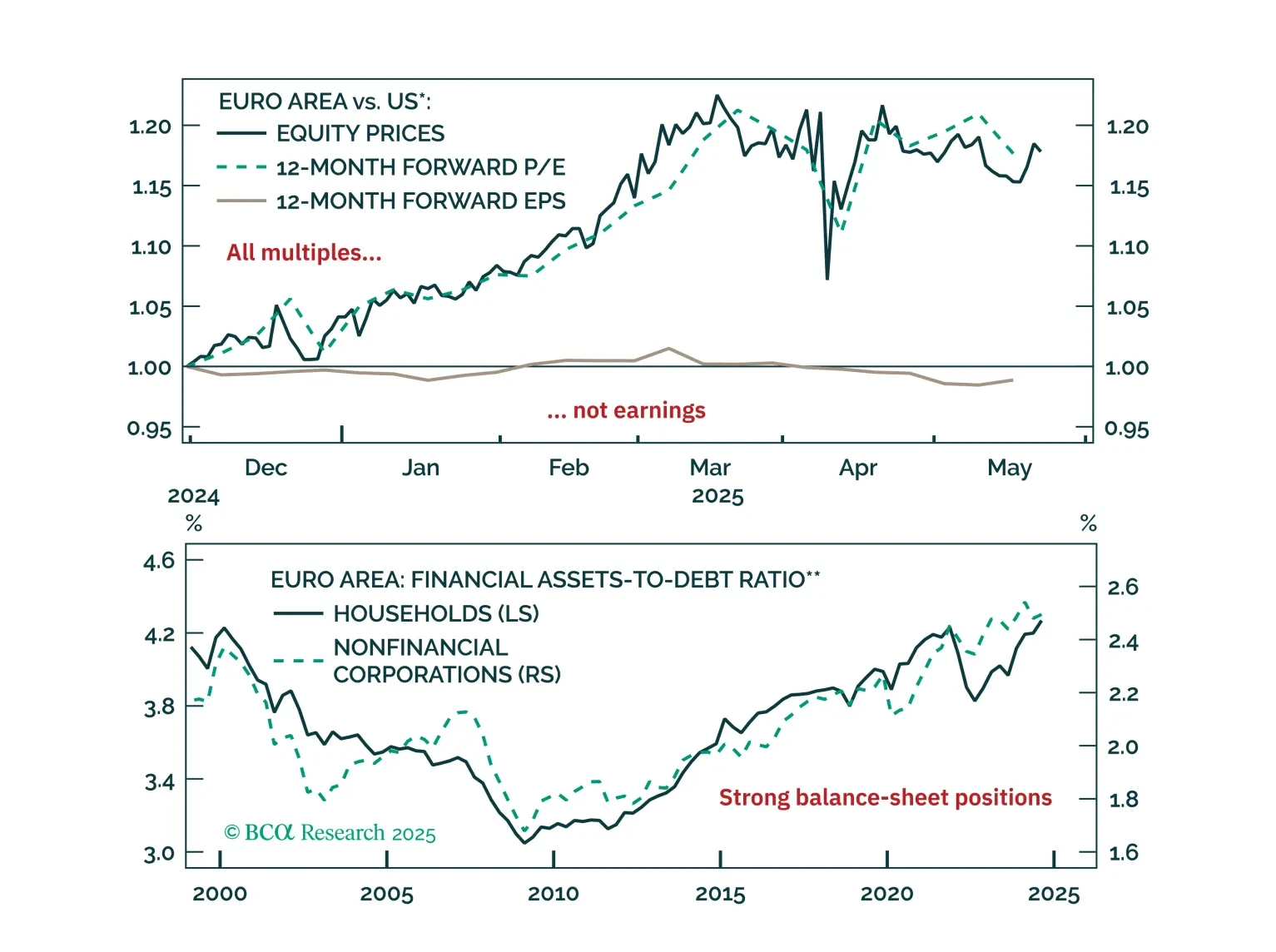

Producer prices in Spain surprised to the downside, foreshadowing a relapse in Euro Area inflation and cementing the ECB’s dovish stance. The Spanish PPI index fell to 1.9% in April, continuing the disinflation trend from the last period while recording the…

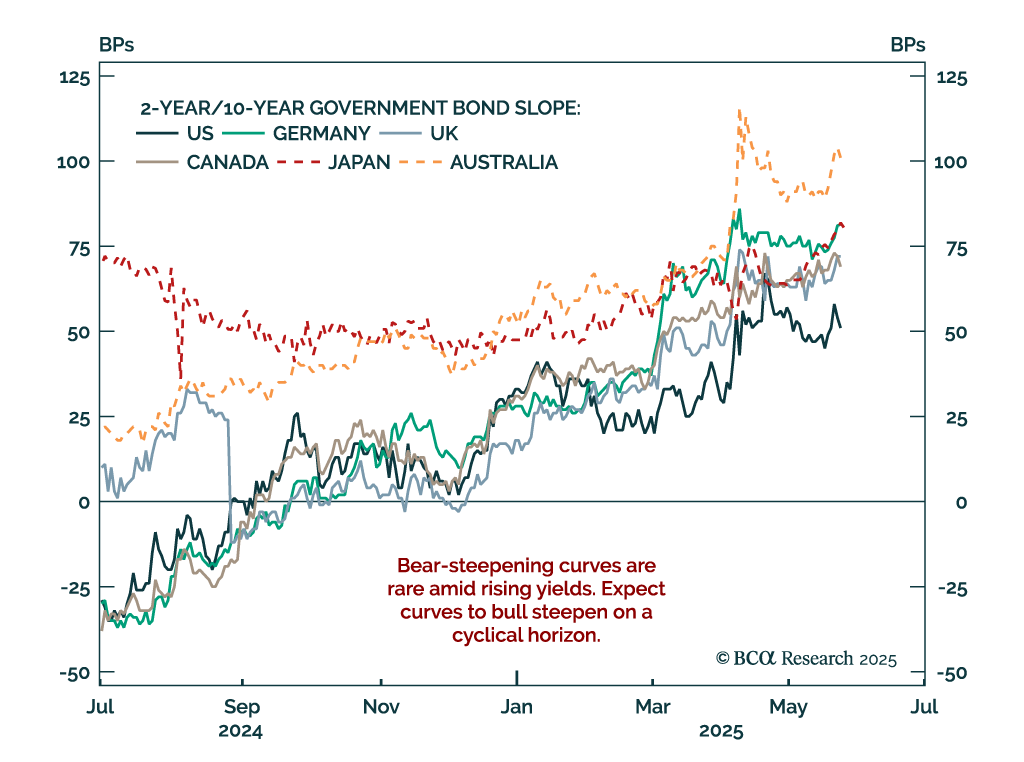

According to our fixed income strategists, the main drivers of rising global yields have been widening bond/OIS spreads and term premiums. Wider government bond/OIS spreads reflect increasing government bond supply (net of central bank purchases) among…

Five questions, five answers from the road. We unpack what Europe’s biggest investors are worried about right now, from trade‑war whiplash to bund‑versus‑Treasury positioning; and where the real opportunities still lie.