Fixed Income

Highlights Rising Global Yields: The increased turbulence in global bond markets is part of the adjustment process to a more positive outlook for global economic growth. Rising real yields are now the main driver of nominal yield movements, with stable inflation expectations indicating that investors are not overly concerned about a sustained inflation overshoot. Duration: Central bankers will eventually be forced to shift to less dovish interest rate guidance to reflect the new reality of faster growth and increased inflation pressures, but this is likely to not occur until much later in 2021, starting with the Fed. Maintain a below-benchmark cyclical duration stance in global bond portfolios. UST Yields & Spreads: The selloff in US Treasuries has pushed US yields to levels that are starting to look a bit stretched relative to yields from other major developed economies like Germany and Japan. This is especially true on a volatility-adjusted basis. As a result, we are closing our tactical US-Germany spread widening trade in bond futures at a profit of 1.8%. Feature Chart of the WeekBond Yields Are Rising Because Of Growth

Bond Yields Are Rising Because Of Growth

Bond Yields Are Rising Because Of Growth

The rapid surge in global bond yields seen so far in 2021 has led some commentators to declare that the dreaded “bond vigilantes” have returned to dole out punishment for overly stimulative fiscal and monetary policies (most notably in the US). The rapid pace of the bond selloff, with the 10-year US Treasury yield reaching 1.6% on an intraday basis last week, has raised fears that spiking yields could damage a fragile global economic recovery. This logic is backwards – it is surging growth expectations that are driving bond yields sustainably higher from deeply depressed levels. Global growth is projected to accelerate at a very rapid pace over the rest of this year and 2022. The combination of the Bloomberg consensus real GDP growth and inflation forecasts for the major developed economies suggest that nominal year-over-year GDP growth is expected to climb to 7.2% in the US, 8.4% in the UK and 6.4% in the euro area by year-end (Chart of the Week). Nominal growth in 2022 is expected to grow by another 5-7% across the same regions, suggesting a return to a slightly faster pace than prevailed during the pre-pandemic years of 2017-19 - even after a boom in 2021. Nominal longer-term global government bond yields, which had been priced for a pandemic-stricken economic backdrop, are now playing catch-up to the new reality of a post-pandemic, vaccinated world. Bond investors understand that the need for extreme monetary accommodation is ebbing, especially in the US where there will be an enormous fiscal impulse to growth in 2021 (and beyond). As a result, interest rate expectations are moving higher, fueling a repricing towards higher bond yields around the world. This process has more room to run. A Global Move Higher In Yields, For The Right Reasons Chart 2Reflationary Bear-Steepening Of Global Yield Curves

Reflationary Bear-Steepening Of Global Yield Curves

Reflationary Bear-Steepening Of Global Yield Curves

The cyclical rise in developed market bond yields that began last summer was initially focused on longer-maturity yields boosted by rising inflation expectations (Chart 2). The very front-ends of bond yield curves – which are more sensitive to expectations of changes in central bank policy rates – have remained subdued. The upward pressure on global bond yields is starting to infect some shorter maturities, however. 5-year government bonds yields in the UK, Canada and Australia rose 44bps, 42bps and 35bps, respectively, during the month of February. The latter two represented a near doubling of the level of the 5-year yield. In the case of the UK, the surge in 5-year Gilt yields came from a starting point of negative yields at the end of January. Last week, the 5-year US Treasury yield jumped a massive 22bps on a single day due to a poorly received US Treasury auction. Year-to-date, longer-term global bond yields have been rising more through the real yield component than higher inflation expectations (Charts 3A & 3B). This is a change in the dynamics from the latter half of 2020 when inflation expectations were the dominant force pushing global yields higher. Chart 3AReal Yields Are Driving The Recent Bond Selloff …

Real Yields Are Driving The Recent Bond Selloff...

Real Yields Are Driving The Recent Bond Selloff...

Chart 3B… Even In The Lower-Yielding Markets

...Even In The Lower-Yielding Markets

...Even In The Lower-Yielding Markets

This shift in “leadership” of the global bond market selloff has been broad-based. 10-year real yields from inflation-linked bonds have surged higher in the US (+35bps year-to-date), UK (+40bps), Australia (+44bps) and Canada (+25bps). Real 10-year yields have even inched up in France (+9bps), despite euro area growth suffering because of COVID-19 lockdowns. This coordinated rise in real bond yields comes on the heels of a sharp improvement in overall global economic momentum and improving expectations for future growth. Manufacturing PMIs, a reliable leading indicator of real yields in the developed markets, began a cyclical improvement in the middle of last year and, right on cue, global bond yields bottomed out toward the end of 2020 (Chart 4). The link between that strong growth momentum and real bond yields comes from expected changes in central bank policies. Our Central Bank Monitors for the US, euro area, UK, Japan, Canada and Australia – designed to measure cyclical pressures on monetary policy - have all moved significantly higher since mid-2020 (Chart 5). This suggests a diminished need for additional monetary stimulus because of rebounding economic growth and intensifying inflation pressures. The Monitors have climbed to above pre-pandemic levels in the US and Australia. Chart 4Real Yields Starting To Catch Up To Solid Growth

Real Yields Starting To Catch Up To Solid Growth

Real Yields Starting To Catch Up To Solid Growth

Chart 5Markets Starting To Discount Rate Hikes In 2023

Markets Starting To Discount Rate Hikes In 2023

Markets Starting To Discount Rate Hikes In 2023

Interest rate markets are responding to this cyclical pressure to tighten monetary policies by repricing the expected timing and pace of the next rate hiking cycle. Our 24-month discounters, which derive the amount of interest rate changes priced into overnight index swap (OIS) curves up to two years in the future, are now pricing in higher policy rates in the US (+40bps), the UK (+32bps), Australia (+36bps) and Canada (a whopping +82bps) by the first quarter of 2023. This repricing of interest rate expectations does conflict with current central bank forward guidance, to varying degrees. For example, the Fed continues to signal that there will not be any rate hikes until at least the end of 2023. Policymakers will not be overly concerned about higher government bond yields and shifting interest rate expectations, however, if there is limited spillover into broader financial market performance. In the US, the latest increase in real Treasury yields to date has had minimal impact on US equity market valuations or corporate bond yields (Chart 6A), suggesting no tightening of financial conditions that could impact future US economic growth. A similar situation is playing out in Europe, where higher longer-term real yields have had little impact on equity market valuations or the borrowing rates that the ECB is most concerned about, like Italian BTP yields (Chart 6B). Chart 6ANo Tightening Of Financial Conditions In The US...

No Tightening Of Financial Conditions In The US...

No Tightening Of Financial Conditions In The US...

Chart 6B...Or Europe

...Or Europe

...Or Europe

Currency valuations are a more important indicator of financial conditions for other central banks. For example, the Reserve Bank of Australia (RBA) has been explicit that its current policies – near-zero policy rates, yield curve control to anchor the level of 3-year bond yields and quantitative easing (QE) to moderate the level of longer-term yields – are intended to not only keep borrowing costs low but also dampen the value of the Australian dollar. At the moment, the US dollar is being pulled in different directions by the typical fundamental drivers. Real rate differentials between the US and other major developed economies remain unattractive for the greenback, even with the latest rise in US real yields (Chart 7). At the same time, growth differentials between the US and the other major economies are turning more USD-positive. For now, rate differentials are the more dominant factor for the US dollar and will remain so until the Fed begins to shift to a less dovish policy stance – an outcome that we do not expect until much later this year when the Fed will begin to prepare the market for a tapering of asset purchases in 2022. A sustainable bottoming of the US dollar, fueled by a shift to a less accommodative Fed, will also likely mark the end of the rising trend for global inflation expectations, given the links between the dollar, commodity prices and inflation breakevens (bottom panel). Central banks outside the US will continue to resist any unwelcome appreciation of their own currencies versus the US dollar. That means doing more QE when bond yields rise too quickly, as the RBA did this week and the ECB has threatened to do in recent comments from senior policymakers (Chart 8). Increasing the size of asset purchases is unlikely to sustainably drive non-US bond yields lower, however, in an environment of improving global growth that is causing investors to reassess the future path of interest rates. All more QE can hope to do at this point in the global business cycle is limit how fast bond yields can increase. Chart 7The USD Remains The Critical Reflationary Variable

The USD Remains The Critical Reflationary Variable

The USD Remains The Critical Reflationary Variable

Chart 8More QE Is Less Effective At Capping Bond Yields

More QE Is Less Effective At Capping Bond Yields

More QE Is Less Effective At Capping Bond Yields

Chart 9Markets With A Lower Yield Beta To USTs Are Outperforming

Markets With A Lower Yield Beta To USTs Are Outperforming

Markets With A Lower Yield Beta To USTs Are Outperforming

From an investment strategy perspective, the current growth-fueled move higher in global real bond yields does not change any of our suggested tilts. We continue to recommend a below-benchmark overall duration stance within global bond portfolios. Within our recommended country allocation among developed market government bonds, we continue to prefer a large underweight to US Treasuries and overweights to markets that are less susceptible to changes in US Treasury yields like Germany, France, Japan and the UK (Chart 9). We also continue to recommend only neutral allocations to Canadian and Australian government bonds (with below-benchmark duration exposure within those allocations), although we are on “downgrade alert” for both given their status as higher-beta bond markets with central banks more likely follow the Fed down a less dovish path later this year. Bottom Line: Rising real yields are now the main driver of nominal yield movements, with stable inflation expectations indicating that investors are not overly concerned about a sustained inflation overshoot. Central bankers will eventually be forced to shift to less dovish interest rate guidance to reflect the new reality of faster growth and increased inflation pressures, but this is likely to not occur until much later in 2021, starting with the Fed. Maintain a below-benchmark cyclical duration stance in global bond portfolios, with a large underweight allocation to US Treasuries. The UST-Bund Spread Widening Looks Stretched Chart 10Yield Chasing Has Been A Losing Strategy In 2021

Yield Chasing Has Been A Losing Strategy In 2021

Yield Chasing Has Been A Losing Strategy In 2021

Last August, we published a report discussing how “yield chasing” – a strategy of consistently favoring the highest yielding government bond markets – had become the default strategy for bond investors during the early months of the pandemic.1 We concluded that yield chasing would be a successful strategy for only as long as central banks stuck to their promises to maintain very loose monetary policy for the next few years. Investors would be forced to chase scarce yields in that environment, while worrying less about cyclical economic and inflation factors that could push up bond yields. Yield chasing has performed quite poorly so far in 2021. A basket of higher-yielding markets like the US, Canada and Australia has underperformed a basket of low-yielders like Germany, France and Japan by -1.4 percentage points (Chart 10). Obviously, such a carry-driven strategy would be expected to perform poorly during an environment of rising bond volatility as is currently the case. Markets that have been offering relatively enticing yields, like the US or Australia (Table 1), are actually generating the largest total return losses. Those higher-yielders have suffered more aggressive repricing of interest rate expectations, as discussed in the previous section of this report, leading to losses from duration that are dwarfing the higher yields. This is especially true in the US, where there remains the greater scope for an upward repricing of interest rate and inflation expectations. Table 1Government Bond Yields: Unhedged & Hedged Into USD

Are Central Banks Losing Control Of Bond Yields? No.

Are Central Banks Losing Control Of Bond Yields? No.

This suggests that investors must be cautious on determining when to consider increasing exposure to higher yielders like the US, even after Treasury yields have increased substantially. One way to evaluate that is to look at the spreads between US Treasuries and low yielders like Germany and Japan, relative to US bond volatility. In Chart 11, we show the spread of 10-year US Treasuries to 10-year German Bunds. To facilitate a fair comparison between the two, we hedge the Treasury yield into euros while adjusting the spread for duration difference between the two bonds. The currency-hedged and duration-matched Treasury-Bund spread is shown in the middle panel of the chart. In the bottom panel, we adjust that spread for US interest rate volatility by dividing the spread by the level of the MOVE index of US Treasury option volatility. On an unadjusted basis, the 10-year yield gap now sits at 175bps, +70bps higher than the lows seen in August 2020. That spread is narrower on a currency hedged basis, with the 10-year US Treasury yield hedged into euros +73ps higher than the 10-year German bund yield. Two conclusions stand out from the chart: The currency-hedged and duration-matched spread is still well below the prior peaks dating back to 2000; The volatility-adjusted spread is already one standard deviation above the mean value since 2000. In other words, there is scope for US Treasuries yields to continue rising relative to German Bund yields based on levels reached in past cycles. Yet at the same time, the spread provides a reasonable level of compensation compared to the riskiness (volatility) of Treasuries, also based on past cycles. We show the same chart for the spread between 10-year US Treasuries and 10-year Japanese government bonds (JGBs) in Chart 12. In this case, there is also scope for additional spread widening although the volatility-adjusted spread is still not as attractive as at previous peaks since 2000. Chart 11UST-Bund Spread Looking Stretched Vs UST Vol

UST-Bund Spread Looking Stretched Vs UST Vol

UST-Bund Spread Looking Stretched Vs UST Vol

Chart 12UST-JGB Spread Getting Stretched Vs UST Vol

UST-JGB Spread Getting Stretched Vs UST Vol

UST-JGB Spread Getting Stretched Vs UST Vol

The message from the volatility-adjusted Treasury-Bund spread lines up with that of the momentum measures of the unadjusted spread. The latter is historically stretched relative to its 200-day moving average, while the change in the spread over the past six months has been as rapid as any of the moves seen since the 2008 financial crisis (Chart 13). Adding it all up, positioning for additional widening of the Treasury-Bund spread is a much poorer bet from a risk versus reward perspective than it was even a few months ago. On a fundamental medium-term basis, however, there is still room for the Treasury-Bund spread to widen further. Relative inflation and unemployment (spare capacity) trends both argue for relatively higher US bond yields (Chart 14). In addition, the Fed is almost certainly going to start tightening monetary policy well before the ECB, thus policy rate differentials will underpin a wider bond spread – although that is already largely discounted in the spread on a forward basis (top panel). Chart 13UST-Bund Spread Momentum Looks Stretched

UST-Bund Spread Momentum Looks Stretched

UST-Bund Spread Momentum Looks Stretched

Chart 14Fundamentals Still Support A Wider UST-Bund Spread

Fundamentals Still Support A Wider UST-Bund Spread

Fundamentals Still Support A Wider UST-Bund Spread

Chart 15Stay Underweight US Vs. Germany On A Strategic Basis

Stay Underweight US Vs. Germany On A Strategic Basis

Stay Underweight US Vs. Germany On A Strategic Basis

Our fundamental fair value model of the 10-year Treasury-Bund spread shows that the spread is still cheap relative to fair value, which is rising (Chart 15). This suggests more medium-term upside in the spread, perhaps even by more than currently priced into the forwards over the next year. Based on this analysis, we see a case for maintaining a core strategic (6-12 month holding period) underweight position for the US versus Germany in our recommended country allocation within our model bond portfolio. At the same time, with the spread looking a bit stretched on some of the momentum and volatility-adjusted measures, we are taking profits on our tactical (0-6 month holding period) 10-year Treasury-Bund spread widening trade using bond futures, realizing a 1.8% return (see the Tactical Overlay table on page 18). Bottom Line: The selloff in US Treasuries has pushed US yields to levels that are starting to look a bit stretched relative to yields from other major developed economies like Germany and Japan. This is especially true on a volatility-adjusted basis. As a result, we are taking profits on our tactical US-Germany spread widening trade. However, we are maintaining our strategic overweight for Germany versus the US in our model bond portfolio, as fundamentals argue for a wider Treasury-Bund spread on a cyclical and strategic basis. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Report, "We’re All Yield Chasers Now", dated August 11, 2020, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Are Central Banks Losing Control Of Bond Yields? No.

Are Central Banks Losing Control Of Bond Yields? No.

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Chart 1Back To Fair Value

Back To Fair Value

Back To Fair Value

February was a terrible month for the bond market. In fact, the Bloomberg Barclays Treasury Master Index returned -1.8%, its worst month since November 2016. The 5-year/5-year forward Treasury yield rose 37 bps. At 2.19%, it is now fairly valued for the first time since 2019, at least according to survey estimates of the long-run neutral fed funds rates (Chart 1). We outlined a checklist for increasing portfolio duration in our Webcast two weeks ago. So far, only two of the five items on our list have been checked. In particular, dollar sentiment and cyclical economic indicators continue to point toward higher yields, even though the market is now priced for a rate hike cycle that is slightly more hawkish than the Fed’s median forecast from December. We anxiously await this month’s revisions to the Fed’s interest rate forecasts. If the Fed’s forecasts remain unchanged from December, then we may get an opportunity to add some duration back into our recommended portfolio. Stay tuned. Feature Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 65 basis points in February, bringing year-to-date excess returns up to +68 bps. The combination of above-trend economic growth and accommodative monetary policy supports positive excess returns for spread product versus Treasuries. Though Treasury yields have risen in recent weeks, this does not yet pose a risk for credit spreads. The 5-year/ 5-year forward TIPS breakeven inflation rate remains below 2%. We won’t be concerned about restrictive monetary policy pushing credit spreads wider until it reaches a range of 2.3% to 2.5%. Despite the positive macro backdrop, investment grade corporate valuations are extremely tight. The investment grade corporate index’s 12-month breakeven spread is down to its 2nd percentile (Chart 2). This means that the breakeven spread has only been tighter 2% of the time since 1995. The same measure shows that Baa-rated bonds have only been more expensive 3% of the time (panel 3). We don’t anticipate material underperformance versus Treasuries, but we see better value outside of the investment grade corporate space.1 Specifically, we advise investors to favor tax-exempt municipal bonds over investment grade corporates with the same credit rating and duration. We also prefer USD-denominated Emerging Market Sovereign bonds over investment grade corporates with the same credit rating and duration. Finally, the supportive macro environment means we are comfortable adding credit risk to a portfolio. With that in mind, we encourage investors to pick up the additional spread offered by high-yield corporates. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

Stay Bearish On Bonds

Stay Bearish On Bonds

Table 3BCorporate Sector Risk Vs. Reward*

Stay Bearish On Bonds

Stay Bearish On Bonds

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 115 basis points in February, bringing year-to-date excess returns up to +178 bps. Ba-rated credits outperformed duration-matched Treasuries by 111 bps on the month, besting B-rated bonds which outperformed by only 104 bps. The Caa-rated credit tier delivered 138 bps of outperformance versus duration-matched Treasuries. We view Ba-rated junk bonds as the sweet spot within the corporate credit space. The sector is relatively insulated from default risk and yet still offers a sizeable spread pick-up over investment grade corporates (Chart 3). We noted in our 2021 Key Views Special Report that the additional spread earned from moving down in quality below Ba is merely in line with historical averages.2 Assuming a 25% recovery rate on defaulted debt and a minimum required risk premium of 150 bps, we calculate that the junk index is priced for a default rate of 2.3% for the next 12 months (panel 3). This represents a steep drop from the 8.3% default rate observed during the most recent 12-month period. However, only 2 defaults occurred in January, down from a peak of 22 in July. Job cut announcements, an excellent indicator of the default rate, have also fallen dramatically (bottom panel). Overall, we see room for spread compression across all junk credit tiers in 2021 but believe that Ba-rated bonds offer the best opportunity in risk-adjusted terms. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 26 basis points in February, dragging year-to-date excess returns down to -2 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries widened 6 bps in February, but it remains low relative to the recent pace of mortgage refinancings (Chart 4). The MBS option-adjusted spread (OAS) tightened 1 bp on the month to 24 bps. This is considerably below the 57 bps offered by Aa-rated corporate bonds and the 42 bps offered by Agency CMBS. It is only slightly above the 22 bps offered by Aaa-rated consumer ABS. The plummeting primary mortgage spread was a key reason for the elevated refi activity seen during the past year. However, the spread has now recovered back to more typical levels (bottom panel). The implication is that further increases in Treasury yields will likely be matched by higher mortgage rates. This means that mortgage refinancings are likely close to a peak. A drop in refi activity would be a positive development for MBS returns, but we aren’t yet ready to turn bullish on the sector. First, relative OAS valuation favors Aa-rated corporates and Agency CMBS over MBS. Second, the gap between the nominal MBS spread and the MBA Refinance Index remains wide (panel 2) meaning that we could still see spreads adjust higher. Last year’s spike in the mortgage delinquency rate is alarming (panel 4), but it will have little impact on MBS returns. The increase was driven by household take-up of forbearance granted by the federal government. Our US Investment Strategy service has shown that a considerable majority of households will remain current on their loans once the forbearance period ends, causing the delinquency rate to fall back down.3 Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index underperformed the duration-equivalent Treasury index by 3 basis points in February, dragging year-to-date excess returns down to +21 bps (Chart 5). Sovereign debt underperformed duration-equivalent Treasuries by 95 bps in February, dragging year-to-date excess returns down to -116 bps. Foreign Agencies outperformed the Treasury benchmark by 31 bps on the month, bringing year-to-date excess returns up to +25 bps. Local Authority bonds outperformed by 63 bps in February, bringing year-to-date excess returns up to +203 bps. Domestic Agency bonds outperformed by 1 bp, bringing year-to-date excess returns up to +16 bps. Supranationals underperformed by 2 bps, dragging year-to-date excess returns down to +5 bps. We recently took a detailed look at valuation for USD-denominated Emerging Market (EM) Sovereigns.4 We found that, on an equivalent-duration basis, EM Sovereigns offer a spread advantage versus US corporates for all credit tiers except Ba. We recommend that investors take advantage of this spread pick-up by favoring investment grade EM Sovereigns over investment grade US corporates. Attractive countries include: Qatar, UAE, Saudi Arabia, Mexico, Russia and Colombia. We prefer US corporates over EM Sovereigns in the high-yield space. Ba-rated high-yield US corporates offer a spread advantage over EM Sovereigns and the extra spread available in B-rated and lower EMs comes from distressed credits in Turkey and Argentina. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 6 basis points in February, dragging year-to-date excess returns down to +102 bps (before adjusting for the tax advantage). Municipal bond spreads have tightened dramatically during the past few months and Aaa-rated Munis now look expensive compared to Treasuries, with the exception of the short-end of the curve (Chart 6). That said, if we match the duration and credit rating between the Bloomberg Barclays Municipal bond indexes and the US Credit index, we find that both General Obligation (GO) and Revenue Munis appear attractive compared to US investment grade Credit. Both GO and Revenue Munis offer a before-tax spread pick-up relative to US Credit for maturities above 12 years (bottom panel), the same goes for Revenue bonds in the 8-12 year maturity bucket (panel 3). Revenue bonds in the 6-8 year maturity bucket offer an after-tax yield pick-up versus Credit for investors with an effective tax rate above 0.3%. GO bonds in the 8-12 year and 6-8 year maturity buckets offer breakeven effective tax rates of 1% and 10%, respectively. All in all, municipal bond value has deteriorated markedly in recent months and we downgraded our recommended allocation from “maximum overweight” to “overweight” in January. However, investors should still prefer municipal bonds over investment grade corporate bonds with the same credit rating and duration. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury yields moved up dramatically in February, with the curve steepening out to the 7-year maturity point and flattening thereafter. The 2/10 Treasury slope steepened 30 bps on the month to reach 130 bps. The 5/30 slope, meanwhile, held steady at 142 bps. Slopes across the entire yield curve traded directionally with yields for the bulk of February. That is, until last Thursday when a surge in bond yields occurred alongside flattening beyond the 5-year maturity point. As a result, the 2/5/10 butterfly spread spiked (Chart 7), moving into positive territory for the first time in a while (panel 4). This curve behavior raises an interesting question. Was last week’s sharp underperformance in the belly a one-off move driven by convexity selling and other technical factors, as many have suggested?5 Or, are we now close enough to a potential Fed liftoff date that we should expect some segments of the yield curve to flatten on days when yields rise? We will be watching the correlations between different yield curve segments and the overall level of yields closely during the next few weeks, but as of today, we think it’s premature to declare that the 5/10 slope has transitioned into a regime where it flattens on days when yields move higher. That being the case, we expect further increases in bond yields to coincide with a falling 2/5/10 butterfly spread, and we retain our recommended position long the 5-year bullet and short a duration-matched 2/10 barbell. TIPS: Overweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 39 basis points in February, bringing year-to-date excess returns up to +183 bps. The 10-year TIPS breakeven inflation rate rose 2 bps on the month to hit 2.17%. The 5-year/5-year forward TIPS breakeven inflation rate fell 15 bps in February to reach 1.91%. February’s TIPS outperformance was concentrated at the front-end of the curve, as investors started to price-in the possibility of higher inflation during the next year or two that eventually subsides. It’s interesting to note that, despite last month’s surge in bond yields, the 5-year/5-year forward TIPS breakeven inflation rate fell, moving further away from the Fed’s 2.3% to 2.5% target range in the process (Chart 8). The Fed will continue to strive for an accommodative policy stance at least until this target is met. Last month’s price action caused our recommended positions in inflation curve flatteners and real yield curve steepeners to perform very well, but we think further gains are possible in the coming months. The 2/10 CPI swap slope has only just dipped into negative territory (panel 4). With the Fed officially targeting a temporary overshoot of its 2% inflation target, this slope should remain inverted for some time yet. With the Fed also continuing to exert more control over short-dated nominal yields than over long-term ones, short-maturity real yields will continue to come under downward pressure relative to the long end (bottom panel). ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 3 basis points in February, bringing year-to-date excess returns up to +20 bps. Aaa-rated ABS outperformed by 2 bps on the month, bringing year-to-date excess returns up to +13 bps. Non-Aaa ABS outperformed by 9 bps on the month, bringing year-to-date excess returns up to +58 bps. The stimulus from last year’s CARES act led to a significant increase in household savings when individual checks were mailed last April. This excess savings has still not been spent, and now another round of checks is pushing the savings rate higher again (Chart 9). The large stock of household savings means that the collateral quality of consumer ABS is very high, with many households using their windfall to pay down debt (bottom panel). Investors should remain overweight consumer ABS and take advantage of strong collateral performance by moving down in credit quality. The Treasury department’s decision to let the Term Asset-Backed Loan Facility (TALF) expire at the end of 2020 does not alter our recommendation. Spreads are already well below the borrowing cost that was offered by TALF, and these tight spread levels are justified by strong household balance sheets. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 12 basis points in February, bringing year-to-date excess returns up to +87 bps. Aaa Non-Agency CMBS underperformed Treasuries by 5 bps in February, dragging year-to-date excess returns down to +37 bps. Meanwhile, non-Aaa CMBS outperformed by 75 bps, bringing year-to-date excess returns up to +262 bps (Chart 10). We continue to recommend an overweight allocation to Aaa-rated Non-Agency CMBS and an underweight allocation to non-Aaa CMBS. Even with the expiry of TALF, Aaa CMBS spreads are already well below the cost of borrowing through TALF and thus won’t be negatively impacted. Meanwhile, the structurally challenging environment for commercial real estate could lead to problems for lower-rated CMBS (panels 3 & 4). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 11 basis points in February, bringing year-to-date excess returns up to +39 bps. The average index option-adjusted spread tightened 3 bps on the month to reach 42 bps (bottom panel). Though Agency CMBS spreads have completely recovered back to their pre-COVID lows, they still look attractive compared to other similarly risky spread products. This is especially true when you consider the Fed’s continued pledge to purchase as much Agency CMBS as “needed to sustain smooth market functioning”. Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of February 26TH, 2021)

Stay Bearish On Bonds

Stay Bearish On Bonds

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of February 26TH, 2021)

Stay Bearish On Bonds

Stay Bearish On Bonds

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 39 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 39 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

Stay Bearish On Bonds

Stay Bearish On Bonds

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of February 26th, 2021)

Stay Bearish On Bonds

Stay Bearish On Bonds

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 For a look at alternatives to investment grade corporates please see US Bond Strategy Weekly Report, “Searching For Value In Spread Product”, dated January 26, 2021, available at usbs.bcaresearch.com 2 Please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 3 Please see US Investment Strategy Weekly Report, “The Big Bank Beige Book, January 2021”, dated January 25, 2021, available at usis.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “Searching For Value In Spread Product”, dated January 26, 2021, available at usbs.bcaresearch.com 5 https://www.bloomberg.com/news/articles/2021-02-25/convexity-hedging-haunts-markets-already-reeling-from-bond-rout?sref=Ij5V3tFi Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

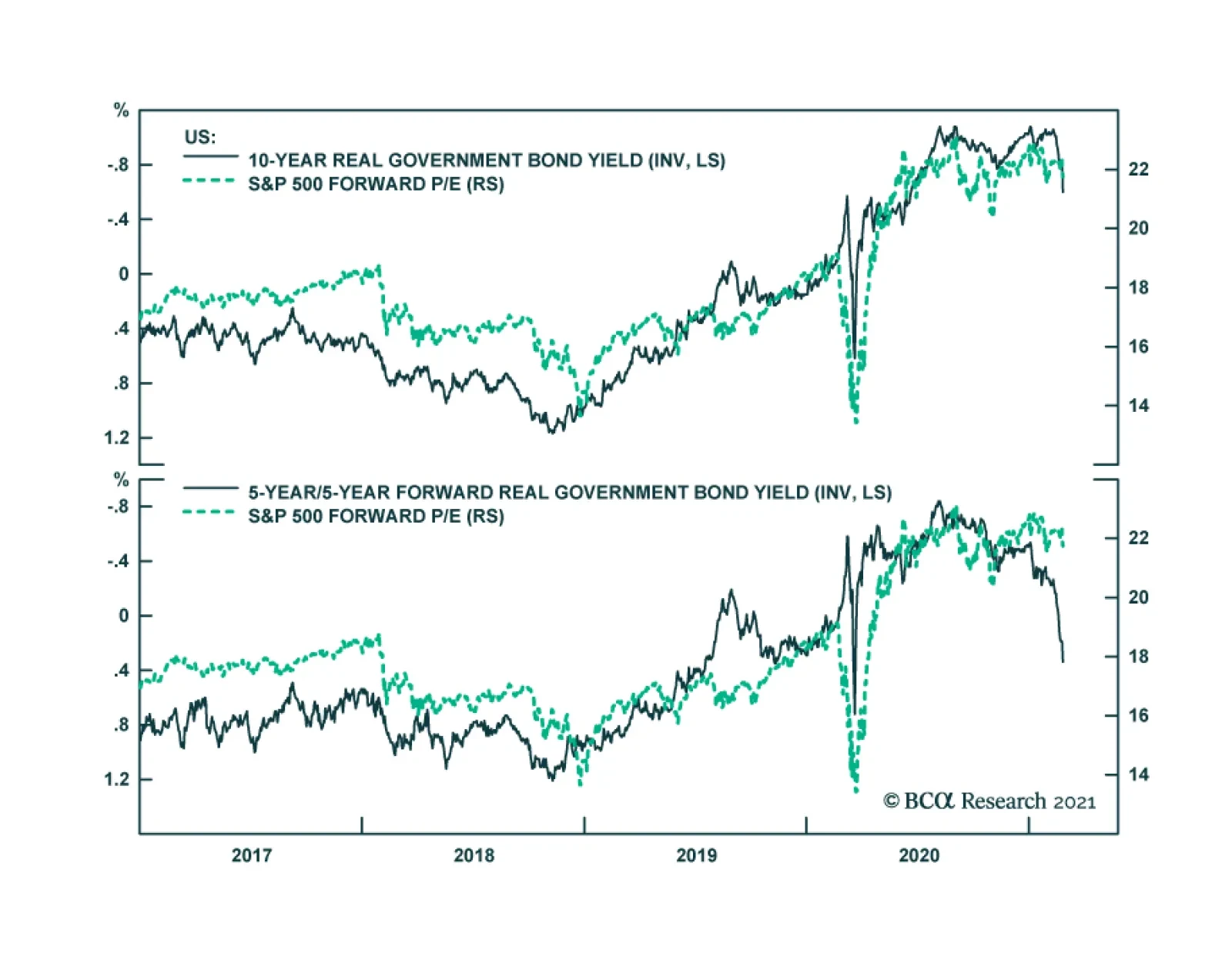

BCA Research’s Global Investment Strategy service concludes that the recent increase in real yields could put further downward pressure on equity prices in the near term. Bond yields have jumped in recent weeks. After bottoming at 0.52% in August, the US…

Dear Client, In addition to this week’s abbreviated report, we are sending you a Special Report on Bitcoin. I don’t recommend you buy it. Best regards, Peter Berezin Highlights Real government bond yields have increased in recent weeks, which could put further downward pressure on equity prices in the near term. Nevertheless, we continue to advocate overweighting equities over a 12-month horizon. Historically, rising real yields have been most toxic for stocks when yields have increased in response to hawkish central bank rhetoric. This is manifestly not the case today. The Fed’s accommodative stance should limit any near-term upward pressure on the US dollar. Investors should favor cyclical and value-oriented stocks over defensive and growth-geared plays. Higher Real Yields: A Near-Term Risk For Stocks Chart 1Government Bond Yields Have Increased Since Bottoming Last Year

Government Bond Yields Have Increased Since Bottoming Last Year

Government Bond Yields Have Increased Since Bottoming Last Year

Bond yields have jumped in recent weeks. After bottoming at 0.52% in August, the US 10-year Treasury yield has climbed to 1.54%, up from 0.93% at the beginning of the year. Government bond yields in the other major economies have also risen (Chart 1). While inflation expectations have bounced, the most recent increase in yields has been concentrated in the real component of bond yields (Chart 2). Optimism about a vaccine-led global growth recovery, reinforced by continued fiscal stimulus – especially in the US – has prompted investors to move forward their expectations of how soon and how high policy rates will rise (Chart 3). Chart 2AThe Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

Chart 2BThe Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

How menacing is the increase in bond yields to stock market investors? Chart 4 shows that there has been a close correlation between real yields and the forward P/E ratio at which the S&P 500 trades. The 5-year/5-year forward real yield, in particular, has moved up sharply, which could put further downward pressure on stocks in the near term. Chart 3Path Of Expected Policy Rates Being Revised Upwards

Path Of Expected Policy Rates Being Revised Upwards

Path Of Expected Policy Rates Being Revised Upwards

Chart 4Rise In Real Rates Is A Headwind For Equity Valuations

Rise In Real Rates Is A Headwind For Equity Valuations

Rise In Real Rates Is A Headwind For Equity Valuations

Nevertheless, we continue to advocate overweighting equities over a 12-month horizon. As we pointed out two weeks ago, rising real yields have historically been most toxic for stocks when yields have increased in response to hawkish central bank rhetoric. This is manifestly not the case today. In his testimony to Congress this week, Jay Powell downplayed inflation risks, stressing that the US economy was “a long way” from the Fed’s goals. He pledged to tread “carefully and patiently” and give “a lot of advance warning” before beginning the process of normalizing monetary policy. We expect the 10-year Treasury yield to stabilize in the 1.6%-to-1.7% range, still well below the level that would threaten the health of the economy. Favor Cyclical And Value-Oriented Stocks In A Weaker Dollar Environment The Fed’s accommodative stance should limit any near-term upward pressure on the US dollar. Whereas stocks are most sensitive to absolute changes in long-term real bond yields, the dollar is more sensitive to changes in short-term real rate differentials with US trading partners (Chart 5). Since the Fed is unlikely to tighten monetary policy anytime soon, US short-term real rates could fall further as inflation rises. Chart 5The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

Chart 6Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical stocks, which are overrepresented outside the US, tend to benefit the most from strengthening global growth and a weakening dollar (Chart 6). Value stocks also generally do well in a weak dollar-strong growth environment (Chart 7). Moreover, bank shares – which are concentrated in value indices – typically outperform when long-term bond yields are rising (Chart 8). Chart 7AA Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

Chart 7BA Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

Chart 8Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

In contrast, as relatively long-duration assets, growth stocks often struggle when bond yields go up. The same is true for more speculative plays such as cryptocurrencies. In this week’s Special Report, we discuss the fate of Bitcoin, arguing that investors should resist buying it. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

When Good News Is Bad News

When Good News Is Bad News

Special Trade Recommendations

When Good News Is Bad News

When Good News Is Bad News

Current MacroQuant Model Scores

When Good News Is Bad News

When Good News Is Bad News

Highlights Higher yields in China should continue to encourage inflows into the RMB. However, the gap between Chinese and US/global interest rates will narrow. This will temper the pace of RMB appreciation. The RMB remains modestly undervalued. Higher productivity gains in China will raise the fair value of the currency. The US dollar could have entered a structural bear market. This will also buffet the CNY-USD exchange rate. A big driver for the RMB in the coming years will also be widespread diversification away from USD assets. This will dovetail nicely with the ascension of the RMB in global FX reserves. Feature Chart 1The RMB Often Moves With Relative Rates

The RMB Often Moves With Relative Rates

The RMB Often Moves With Relative Rates

The appreciation in the Chinese yuan has been a boon for global bond, equity and currency investors. With extremely low volatility, the yuan has appreciated by approximately 10% since its May 2020 lows. This places the rise in the RMB on par with what we saw in the 2017/2018 period. It also makes the yuan one of the best performing emerging market currencies this year. One of the key drivers of the yuan’s stellar performance has been the interest rate gap between China and the US (Chart 1). The Chinese economy was one of the first to emerge from the pandemic-driven lockdown. As economic activity recovered, so did local bond yields. With global bond yields now on the rise, this raises the specter that Sino-global bond yield spreads will narrow. The implications for the path of the Chinese yuan are worth monitoring. On the other hand, structural factors also argue that the path of least resistance for the US dollar over the next few years is down. This is positive for the Chinese yuan. Which force will dominate the path of the RMB going forward? In this Special Report, we discuss the intersection between the People’s Bank of China (PBoC) monetary policy and the global environment, and what that means for the Chinese yuan on a 12-month horizon. China And The Global Cycle The evolution of the global economic cycle has important implications for the yuan exchange rate in particular, because the RMB is a pro-cyclical currency. The USD/CNY has been moving tick for tick with emerging market equities, Asian currencies and commodity prices (Chart 2). Meanwhile, China has also been a major engine for global growth. Ever since the global financial crisis, the money and credit cycle in China has led the global recovery (Chart 3). With the authorities set to modestly decelerate the pace of credit creation, it will be important to gauge if this is a risk to global growth and, by extension, the path of the RMB. Chart 2The RMB Has Traded Like A Pro-cyclical Currency

The RMB Has Traded Like A Pro-cyclical Currency

The RMB Has Traded Like A Pro-cyclical Currency

Chart 3The Chinese Impulse Leads ##br##The Global Cycle

The Chinese Impulse Leads The Global Cycle

The Chinese Impulse Leads The Global Cycle

In our view, while the credit impulse in China will roll over, the impact will be to slow the pace of RMB appreciation rather than reverse it, because: The interest rate gap between China and the rest of the world will remain very wide. The current level of 10-year yields in China is 3.3% versus 1.4% in the US. In a world of very low nominal interest rates, a differential of almost 200 basis points makes all the difference. Our base case is that the Chinese credit impulse could slow to 30% of GDP. If past is prologue, this could compress the yield spread to 1.5% but will still provide a meaningful yield pickup for foreign investors (Chart 4). Meanwhile, the real rate differential between China and the US might not narrow much if China continues to reign in credit growth, while the US pursues inflationary policies. Already, inflation in China is collapsing relative to the US, which supports relative real rates in China. The credit impulse tends to lead the economy by six to nine months, thus, for much of 2021, Chinese growth will remain robust. Overall industrial production is picking up meaningfully, with the production of electricity and steel, and all inputs into the overall manufacturing value chain inflecting higher. This will continue to support bond yields in China (Chart 5). In recent weeks, both steel and iron ore prices have been soaring. While supply bottlenecks are playing a role, it is evident from both the manufacturing data and the trend in prices that demand is also a key driver (Chart 6). Chart 4The China-US Spread Will Stay Positive

The China-US Spread Will Stay Positive

The China-US Spread Will Stay Positive

Chart 5Underlying Economic Activity Is Resilient

Underlying Economic Activity Is Resilient

Underlying Economic Activity Is Resilient

Chart 6Strong Chinese Demand For Commodities

Strong Chinese Demand For Commodities

Strong Chinese Demand For Commodities

China has had a structurally higher productivity growth rate compared to the US or Europe for many years, which will continue. It is also the reason why the fair value of the currency has been rising over the last two decades (Chart 7). Higher productivity growth suggests the neutral rate of interest in China will remain high for many years and will attract further fixed income inflows. China is running a basic balance surplus, which indicates that the RMB does not need to cheapen to entice capital inflows (Chart 8). Chart 7The RMB Is Not Overvalued

The RMB Is Not Overvalued

The RMB Is Not Overvalued

Chart 8A Basic Balance Surplus

A Basic Balance Surplus

A Basic Balance Surplus

Chinese bonds are gaining wider investor appeal. Following their inclusion in the Bloomberg Barclays Global Aggregate Index (BBGA) since April 2019, and in the JP Morgan Government Bond - Emerging Market Index (GBI-EM) since February 2020, FTSE Russell announced the inclusion of Chinese government bonds in the FTSE World Government Bond Index (WGBI) as of October 2021. The inclusion of Chinese government bonds in all of the world’s three major bond indices is a seminal milestone in the process of liberalizing the Chinese fixed-income market. Based on both the US$2-4 trillion in AUM, tracking the WGBI index and a 5-6% weight of Chinese bonds, an additional US$150 billion in foreign investments will flow into China’s bond market following the WGBI inclusion. Moreover, the JPMorgan Global Index team predicts that the inclusion of Chinese bonds in the world’s three major bond indices will bring RMB inflows of up to US$250-300 billion. This will be particularly true if Chinese bonds are perceived as a better hedge against equity volatility (Chart 9). Finally, currencies respond to relative rates of return, which include equity returns in addition to fixed income ones. The relative performance of the Chinese equity market in common currency terms has also moved neck and neck with the performance of the RMB (Chart 10). Chart 9Chinese Bonds Could Become The Perfect Hedge

Chinese Bonds Could Become The Perfect Hedge

Chinese Bonds Could Become The Perfect Hedge

Chart 10The RMB Follows Domestic Equity Relative Performance

The RMB Follows Domestic Equity Relative Performance

The RMB Follows Domestic Equity Relative Performance

Bottom Line: Even though the Chinese credit impulse will continue to roll over, bond investors will still benefit from enticing real interest rates in China as its neutral rate of interest is higher. Equity investors will also benefit from a cheaper market, as well as exposure to sectors that are primed to benefit as the global economy reopens. This combination will sustain the pace of foreign capital inflows (Chart 11). Chart 11Inflows Into China Remain Strong

Inflows Into China Remain Strong

Inflows Into China Remain Strong

The Dollar Versus The RMB The path of the RMB in the short-term will follow relative growth dynamics between China and the rest of the world, but structural factors such as the dollar’s reserve status will also dictate its longer-term trend. What China (and other countries for that matter) decide to do with their war chest of US Treasuries is of critical importance. In recent years, foreign investors have been fleeing the US Treasury market at an exceptional pace. On a rolling 12-month total basis, the US saw an exodus of about US$500 billion in bond flows from foreigners, the largest on record (Chart 12). Vis-à-vis official flows, China has become the number one contributor to the US trade deficit. Concurrently, Beijing has been destocking its holdings of Treasuries, if only as retaliation against past US policies, or perhaps to make room for the internationalization of the RMB (Chart 13). Chart 12An Exodus From US Treasurys

An Exodus From US Treasurys

An Exodus From US Treasurys

Chart 13China Destocking Of Treasurys

China Destocking Of Treasurys

China Destocking Of Treasurys

Data from the International Monetary Fund (IMF) shows that the allocation of global foreign exchange reserves towards the US dollar peaked at about 72% in the early 2000s and has been in a downtrend since. Meanwhile, allocation to other currencies, including the RMB, is surging. Moreover, foreign central banks have been amassing tremendous gold reserves, notably Russia and China, almost to the tune of the total annual output of the yellow metal. A diversification away from dollars and into other currencies such as the RMB and gold will be a key factor in dictating currency trends in the next few years (Chart 14). Chart 14The RMB Rises In Global Currency Reserves

The RMB Rises In Global Currency Reserves

The RMB Rises In Global Currency Reserves

The US dollar will remain the reserve currency of the world for years to come, but that exorbitant privilege is clearly fraying at the edges. This is especially the case as balance-of-payments dynamics are deteriorating. Rising US twin deficits have usually been synonymous with a cheapening dollar. Bottom line: For one reason or another, foreign central banks are diversifying out of dollars. This could be a long-term trend, which will dictate the path of the dollar (and by extension the RMB) in the years to come. Other Considerations Chart 15A Forward Discount On The RMB

A Forward Discount On The RMB

A Forward Discount On The RMB

The RMB has historically suffered from capital outflows, especially illicit flows. This is less risky today than in 2015-2016.1 Nonetheless, investors must monitor this possibility. Typically, offshore markets have anticipated the yuan’s depreciation. Back in 2014, offshore markets started pricing in a rising USD/CNY rate, and maintained that view all the way through to 2018, when the yuan eventually bottomed. Right now, 12-month non-deliverable forwards expect a modest depreciation in the yuan (Chart 15). Offshore markets in Hong Kong and elsewhere can be prescient because more often than not, they are the destination for illicit flows out of China. However, this time might be different. First, higher relative interest rates in China have lowered the forward RMB rate investors will receive to hedge currency exposure. Second, junkets (key operators in Macau casinos) have been one of the often-rumored vehicles used for Chinese money to leave the country.2 These junkets bankroll their Chinese clients in Macau while collecting any debts in China, allowing for illicit capital outflows. This was particularly rampant before the Chinese 2015-2016 corruption clampdown, when Macau casino equities were surging while equity prices in China were subdued. This time around, with tourism taking a backseat, the Chinese MSCI index is heavily outpacing the performance of Macau casino stocks, suggesting little evidence of hot money outflows (Chart 16). Chart 16China Versus Macau Stocks: Little Hot Money Outflows Like In 2013/2014

China Versus Macau Stocks: Little Hot Money Outflows Like In 2013/2014

China Versus Macau Stocks: Little Hot Money Outflows Like In 2013/2014

Sino-US trade relations will also affect the exchange rate. China remains the biggest contributor to the US trade deficit, even though the gap has narrowed (Chart 17). There is little evidence that the Biden administration will engage in an all-out trade war with China, but the case for subtle skirmishes exists. Chart 17The US Trade Deficit With China Remains Wide

The US Trade Deficit With China Remains Wide

The US Trade Deficit With China Remains Wide

In a broader sense, the pandemic might have supercharged the de-globalization trend witnessed since 2011. The stability and self-sufficiency in the production capacity of any country's core supply chain have become paramount. From the perspective of the US, this means introducing more policies that attract investment into domestic manufacturing, such as clean energy. US multinational companies may also continue to diversify production risk away from China to other emerging countries, among them Vietnam, Myanmar, and India. This will curtail FDI flows into China at the margin (previously mentioned Chart 8). Concluding Thoughts Chart 18The RMB And The Trade-Weighted Dollar

The RMB And The Trade-Weighted Dollar

The RMB And The Trade-Weighted Dollar

While USD/CNY could bounce in the near term, it is likely to reach 6.2 in the next 12 months. Interest rate spreads at the long end already overtook their 2017 highs and are near cyclically elevated levels. The bond market tends to lead the currency market by a few months, since China does not yet have a fully flexible and open capital account. Meanwhile, the path of the US dollar will also be critical for the USD/CNY exchange rate. We expect the USD to keep depreciating, which will boost the RMB (Chart 18).3 A slower pace of RMB appreciation will fend off interventionist policies by the PBoC. While the exchange rate has appreciated sharply since mid-2020, the CFETS rate has not deviated much from the onshore USD/CNY rate. This will remain the case if the pace of RMB appreciation moderates. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Chinese Investment Special Report, titled “Monitoring Chinese Capital Outflows,” dated March 20, 2019, available at fes.bcaresearch.com. 2 Please see Reuters article “Factbox: How Macau’s casino junket system works,” available at reuters.com. 3 Please see Foreign Exchange Strategy Special Report, titled “2021 Key Views: Tradeable Themes,” dated December 4, 2020, available at bcaresearch.com. Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

BCA Research’s Emerging Markets Strategy service concludes that there are many similarities between the current US macro picture and the late 1960s. In the late 1960s, US inflation was subdued, and interest rates were very low in the preceding two-three…

For this month’s Special Report, we are sending you a collaboration between our US Investment Strategy and US Political Strategy teams. US Political Strategy is our newest strategy service and it extends the proprietary framework of our Geopolitical Strategy service to provide analysis of political developments that is relevant for US-focused investors. Please contact your relationship manager if you would like more information or to begin trialing the service. Highlights Ronald Reagan cast a long shadow over the elected officials who followed him … :The influence of the economic policies associated with Ronald Reagan held such persistent sway that even the Clinton and Obama administrations had to follow their broad outlines. … just as Paul Volcker did over central bankers at home and abroad … : The Volcker Fed’s uncompromising resistance to the 1970s’ runaway inflation established the Fed’s credibility and enshrined a new global central banking orthodoxy. … but it appears their enduring influence may have finally run its course … : The pandemic overrode everything else in real time, but investors may ultimately view 2020 as the year in which Democrats broke away from post-Reagan orthodoxy and the Fed decided Volcker’s vigilance was no longer relevant. … to investors’ potential chagrin: If inflation, big government and organized labor come back from the dead, globalization loses ground, regulation expands, anti-trust enforcement regains some bite and tax rates rise and become more progressive, then the four-decade investment golden age that Reagan and Volcker helped launch may be on its last legs. Feature The pandemic dominated everything in real time in 2020, as investors scrambled to keep up with its disruptions and the countermeasures policymakers deployed to shelter the economy from them. With some distance, however, investors may come to view it as a year of two critical policy inflection points: the end of the Reagan fiscal era and the end of the Volcker monetary era. The shifts could mark a watershed because Reagan’s and Volcker’s enduring influence helped power an investment golden age that has lasted for nearly 40 years. What comes next may not be so supportive for financial markets. Political history often unfolds in cycles even if their starting and ending dates are never as clear cut in real life as they are in dissertations. Broadly, the FDR administration kicked off the New Deal era, a 48-year period of increased government involvement in daily life via the introduction and steady expansion of the social safety net, broadened regulatory powers and sweeping worker protections. It was followed by the 40-year Reagan era, with a continuous soundtrack of limited government rhetoric made manifest in policies that sought to curtail the spread of social welfare programs, deregulate commercial activity, devolve power to state and local government units and the private sector and push back against unions. The Obama and Trump administrations challenged different aspects of Reaganism, but the 2020 election cycle finally toppled it. Ordinarily, that might only matter to historians and political scientists, but the Reagan era coincided with a fantastic run in financial markets. So, too, did the inflation vigilance that lasted long after Paul Volcker’s 1979-1987 tenure at the helm of the Federal Reserve, which drove an extended period of disinflation, falling interest rates and rising central bank credibility. Our focus here is on fiscal policy, and we touch on monetary policy only to note that last summer’s revision of the Fed’s statement of long-run monetary policy goals shut the door on the Volcker era. The end of both eras could mark an inflection point in the trajectory of asset returns. The Happy Warrior The nine most terrifying words in the English language are, “I’m from the government, and I’m here to help.”1 Chart II-1After The Recession, Reagan Was A Hit

After The Recession, Reagan Was A Hit

After The Recession, Reagan Was A Hit

Ronald Reagan held his conservative views with the zeal of the convert that he was.2 Those views were probably to the right of much of the electorate, but his personal appeal was strong enough to make them palatable to a sizable majority (Chart II-1). Substitute “left” for “right” and the sentiment just as easily sums up FDR’s ability to get the New Deal off the ground. Personal magnetism played a big role in each era’s rise, with both men radiating relatability and optimism that imbued their sagging fellow citizens with a sense of comfort and security that made them willing to try something very different. 1980 was hardly 1932 on the distress scale, but America was in a funk after the upheaval of the sixties, the humiliating end to Vietnam, Watergate, stagflation and a term and a half of uninspiring and ineffectual presidential leadership. Enter the Great Communicator, whose initial weekly radio address evoked the FDR of the Fireside Chats – jovial, resolute and confident, with palpable can-do energy – buffed to a shine by a professional actor and broadcaster whose vocal inflections hit every mark.3 The Gipper,4 with his avuncular bearing, physical robustness and ever-present twinkle in his eye, was just what the country needed to feel better about itself. Reaganomics 101 Government does not tax to get the money it needs; government always finds a need for the money it gets.5 President Reagan’s economic plan had three simple goals: cut taxes, tame government spending and reduce regulation. From the start of his entry into politics in the mid-sixties, Reagan cast himself as a defender of hard-working Americans’ right to keep more of the fruits of their labor from a grasping federal government seeking funding for wasteful, poorly designed programs. He harbored an intense animus for LBJ’s Great Society, which extended the reach of the federal government in ways that he characterized as a drag on initiative, accomplishment and freedom, no matter how well intentioned it may have been. That message hung a historic loss on Barry Goldwater in 1964 when inflation was somnolent but it proved to be far more persuasive after the runaway inflation of the seventies exposed the perils of excessive government (Chart II-2). Chart II-2Inflation Rises When The Labor Market Heats Up

Inflation Rises When The Labor Market Heats Up

Inflation Rises When The Labor Market Heats Up

As the Reagan Foundation website describes the impact of his presidency’s economic policies, “Millions … were able to keep more of the money for which they worked so hard. Families could reliably plan a budget and pay their bills. The seemingly insatiable Federal government was on a much-needed diet. And businesses and individual entrepreneurs were no longer hassled by their government, or paralyzed by burdensome and unnecessary regulations every time they wanted to expand.” “In a phrase, the American dream had been restored.” The Enduring Reach Of Reaganomics I’m not in favor of abolishing the government. I just want to shrink it down to the size where we can drown it in the bathtub. – Grover Norquist Though President-Elect Clinton bridled at limited government’s inherent restrictions, bursting out during a transition briefing, “You mean to tell me that the success of the economic program and my re-election hinges on the Federal Reserve and a bunch of f***ing bond traders?” his administration largely observed them. This was especially true after the drubbing Democrats endured in the 1994 midterms, when the Republicans captured their first House majority in four decades behind the Contract with America, a skillfully packaged legislative agenda explicitly founded on Reagan principles. Humbled in the face of Republican majorities in both houses of Congress, and hemmed in by roving bands of bond vigilantes, Clinton was forced to tack to the center. James Carville, a leading architect of Clinton’s 1992 victory, captured the moment, saying, “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or … a .400 … hitter. But now I would like to come back as the bond market. You can intimidate everybody.” Reagan’s legacy informed the Bush administration’s sweeping tax cuts (and its push to privatize social security), and forced the Obama administration to tread carefully with the stimulus package it devised to combat the Great Recession. Although the administration’s economic advisors considered the $787 billion (5%-of-peak-GDP) bill insufficient, political staffers carried the day and the price tag was kept below $800 billion to appease the three Republican senators whose votes were required to pass it. Even with the economy in its worst state since the Depression, the Obama administration had to acquiesce to Reaganite budget pieties if it wanted any stimulus bill at all. Its leash got shorter after it agreed with House Republicans to “sequester” excess spending under the Budget Control Act of 2011. On the Republican side of the aisle, Grover Norquist, who claims to have founded Americans for Tax Reform (ATR) at Reagan’s request, enforced legislative fealty to the no-new-tax mantra. ATR, which opposes all tax increases as a matter of principle, corrals legislators with the Taxpayer Protection Pledge, “commit[ting] them to oppose any effort to increase income taxes on individuals and businesses.” ATR’s influence has waned since its 2012 peak, when 95% of Republicans in Congress had signed the pledge, and Norquist no longer strikes fear in the hearts of Republicans inclined to waver on taxes. His declining influence is testament to Reaganism’s success on the one hand (the tax burden has already been reduced) and the fading appeal of its signature fiscal restraint on the other. Did Government Really Shrink? When the legend becomes fact, print the legend. – The Man Who Shot Liberty Valance For all of its denunciations of government spending, the Reagan administration ran up the largest expansionary budget deficits (as a share of GDP) of any postwar administration until the global financial crisis (Chart II-3). Although it aggressively slashed non-defense discretionary spending, it couldn’t cut enough to offset the Pentagon’s voracious appetite. The Reagan deficits were not all bad: increased defense spending hastened the end of the Cold War, so they were in a sense an investment that paid off in the form of the ‘90s peace dividend and the budget surpluses it engendered. Chart II-3Cutting The Federal Deficit Is Harder Than It Seems

Cutting The Federal Deficit Is Harder Than It Seems

Cutting The Federal Deficit Is Harder Than It Seems

Nonetheless, the Reagan experience reveals the uncomfortable truth that there is little scope for any administration or Congressional session to cut federal spending. Mandatory entitlement spending on social security, Medicare and Medicaid constitutes the bulk of federal expenditures (Chart II-4) and they are very popular with the electorate, as the Trump campaign shrewdly recognized in the 2016 Republican primaries (Table II-1). Discretionary spending, especially ex-defense, is a drop in the bucket, thanks largely to a Reagan administration that already cut it to the bone (Chart II-5). Chart II-4The Relentless Rise In Mandatory Spending ...

The Relentless Rise In Mandatory Spending ...

The Relentless Rise In Mandatory Spending ...

Chart II-5Overwhlems Any Plausible Discretionary Cuts

Overwhlems Any Plausible Discretionary Cuts

Overwhlems Any Plausible Discretionary Cuts

Table II-1How Trump Broke Republican Orthodoxy On Entitlement Spending

March 2021

March 2021

The Reagan tax cuts therefore accomplished the easy part of the “starve the beast” strategy but his administration failed to make commensurate cuts in outlays (Chart II-6). If overall spending wasn’t cut amidst oppressive inflation, while the Great Communicator was in the Oval Office to make the case for it to a considerably more fiscally conservative electorate, there is no chance that it will be cut this decade. As our Geopolitical Strategy service has flagged for several years, the median US voter has moved to the left on economic policy. Reagan-era fiscal conservatism has gone the way of iconic eighties features like synthesizers, leg warmers and big hair, even if it had one last gasp in the form of the post-crisis “Tea Party” and Obama’s compromise on budget controls. Chart II-6Grover Norquist Is Going To Need A Bigger Bathtub

Grover Norquist Is Going To Need A Bigger Bathtub

Grover Norquist Is Going To Need A Bigger Bathtub

Do Republicans Still Want The Reagan Mantle? Chart II-7“Limited Government” Falling Out Of Fashion

March 2021

March 2021

Reaganism is dead, killed by a decided shift in broad American public opinion, and within the Republican and Democratic parties themselves. Americans are just as divided today as they were in Reagan’s era about the size of the government but the trend since the late 1990s is plainly in favor of bigger government (Chart II-7). Recent developments, including the 2020 election, reinforce our conviction that trend will not reverse any time soon. The Republicans are the natural heirs of Reagan’s legacy. Much of President Trump’s appeal to conservatives lay in his successful self-branding as the new Reagan. Though he lacked the Gipper’s charisma and affability, his unapologetic assertion of American exceptionalism rekindled some of the glow of Morning-in-America confidence. Following the outsider trail blazed by Reagan, he lambasted the Washington establishment and promised to slash bureaucracy, deregulate the economy and shake things up. Trump’s signature legislative accomplishment was the largest tax reform since Reagan’s in 1986. He oversaw defense spending increases to take on China, which he all but named the new “evil empire.”6 Like Reagan, he was willing to weather criticism for face-to-face meetings with rival nations’ dictators. Even his trade protectionism had more in common with the Reagan administration than is widely recognized.7 Chart II-8Reagan’s Amnesty On Immigration

March 2021

March 2021

But major differences in the two presidents’ policy portfolios underline the erosion of the Reagan legacy’s hold. President Trump outflanked his Republican competitors for the 2016 nomination by running against cutting government spending – he was the only candidate who opposed entitlement reform. His signature proposal was to stem immigration by means of a Mexican border wall. While Reagan had sought to crack down on illegal immigration, he pursued a compromise approach and granted amnesty to 2.9 million illegal immigrants living in America to pass the Immigration Reform and Control Act of 1986, sparing businesses from having to scramble to replace them (Chart II-8). While Reagan curtailed non-defense spending, Trump signed budget-busting bills with relish, even before the COVID pandemic necessitated emergency deficit spending. Trump tried to use the power of government to intervene in the economy and alienated the business community, which revered Reagan, with his scattershot trade war. Trump’s greater hawkishness on immigration and trade and his permissiveness on fiscal spending differentiated him from Reagan orthodoxy and signaled a more populist Republican Party. Chart II-9Trump Could Start Third Party, Give Democrats A Decade-Plus Ascendancy

March 2021

March 2021

More fundamentally, Trump represents a new strain of Republican that is at odds with the party’s traditional support for big business and disdain for big government. If he leads that strain to take on the party establishment by challenging moderate Republicans in primary elections and insisting on running as the party’s next presidential candidate, the GOP will be swimming upstream in the 2022 and 2024 elections. It is too soon to make predictions about either of these elections other than to say that Trump is capable of splitting the party in a way not seen since Ross Perot in the 1990s or Theodore Roosevelt in the early 1900s (Chart II-9).8 If he does so, the Democrats will remain firmly in charge and lingering Reaganist policies will be actively dismantled. Even if the party manages to preserve its fragile Trumpist/traditionalist coalition, it is hard to imagine it will recover its appetite for shrinking entitlements, siding against labor or following a laissez-faire approach to corporate conduct and combinations. Republicans will pay lip service to fiscal restraint but Trump’s demonstration that austerity does not win votes will lead them to downplay spending cuts and entitlement reform as policy priorities – at least until inflation again becomes a popular grievance (Chart II-10). Republicans will also fail to gain traction with voters if they campaign merely on restoring the Trump tax cuts after Biden’s likely partial repeal of them. Support for the Tax Cut and Jobs Act hardly reached 40% for the general public and 30% for independents and it is well known that the tax reform did little to help Republicans in the 2018 midterm elections, when Democrats took the House (Chart II-11). Chart II-10Republicans Have Many Priorities Above Budget Deficits

March 2021

March 2021

Chart II-11Trump Tax Cuts Were Never Very Popular

March 2021

March 2021

On immigration the Republican Party will follow Trump and refuse amnesty. Immigration levels are elevated and Biden’s lax approach to the border, combined with a looming growth disparity with Latin America, will generate new waves of incomers and provoke a Republican backlash. On trade and foreign policy, Republicans will follow a synthesis of Reagan and Trump in pursuing a cold war with China. The Chinese economy is set to surpass the American economy by the year 2028 and is already bigger in purchasing power parity terms (Chart II-12). The Chinese administration is becoming more oppressive at home, more closed to liberal and western ideas, more focused on import substitution, and more technologically ambitious. The Chinese threat will escalate in the coming decade and the Republican Party will present itself as the anti-communist party by proposing a major military-industrial build-up. Yet it is far from assured that the Democrats will be soft on China, which is to say that they will not be able to cut defense spending substantially. Chart II-12China Is the New "Evil Empire" For GOP

China Is the New "Evil Empire" For GOP

China Is the New "Evil Empire" For GOP