Fixed Income

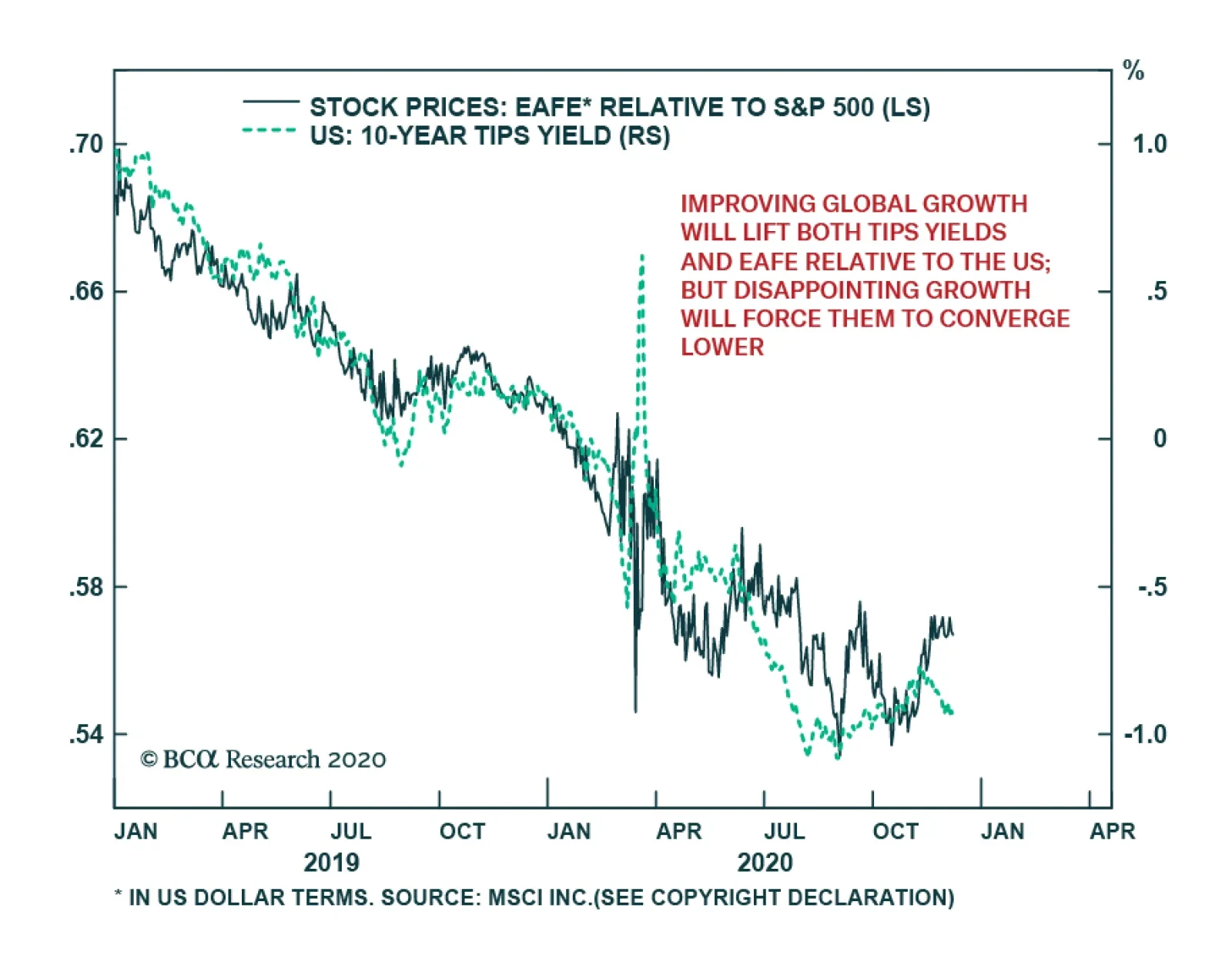

Over the past two years, the performance of EAFE equities relative to the US has tightly followed real bond yields. This is because both the relative performance of foreign equities and real interest rates are extremely sensitive to the global economic…

Highlights Chart 1Bond Yields & The CRB/Gold Ratio

Bond Yields & The CRB/Gold Ratio

Bond Yields & The CRB/Gold Ratio

In our last report of November, we noted that the rising COVID case count was likely to lead to a challenging few months for the US economy, but we also questioned whether financial markets would pay attention or whether they would stay focused on the vaccine roll-out and eventual economic recovery. We now have our answer. November’s employment report was the worst since April, but the Treasury curve has bear-steepened, credit spreads have come in and TIPS have outperformed nominals. What’s more, the jump in the CRB Raw Industrials / Gold ratio suggests that the 10-year Treasury yield has even more near-term upside (Chart 1). With a vaccine on the horizon and Congress closing in on a fiscal relief package, investors should stay positioned for the reflation trade on a 6-12 month horizon: below-benchmark portfolio duration, nominal and real yield curve steepeners, inflation curve flatteners, overweight TIPS versus nominals and overweight corporate bonds rated Ba and higher. Feature Investment Grade: Overweight Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 233 basis points in November, bringing year-to-date excess returns up to -74 bps. The strong rally in corporate bonds since March has culminated in extremely tight valuations for investment grade corporates. The 12-month breakeven spread for the Bloomberg Barclays Corporate Index (adjusted to keep the average credit rating constant) has only been tighter 4% of the time since 1995 (Chart 2). The same figure for the Baa-rated credit tier is 5%. We retain a positive outlook on corporate credit despite these stretched valuations. In our view, an environment where the economy is recovering and where the Fed will be very cautious about scaling back accommodation is the exact sort of environment where we should expect a lot of enthusiasm for spread product and, as a result, extremely tight spreads. We will not be surprised if our 12-month breakeven spread percentile rank valuation measure reaches its all-time expensive level within the next couple of months. While the macro environment makes it difficult to turn negative on investment grade corporates, we acknowledge that other sectors may offer better opportunities, particularly in the higher credit tiers. Specifically, we find better value in tax-exempt municipal bonds than in corporates and recommend that investors favor the former over the latter. At the sector level, we continue to recommend overweight allocations to subordinate Bank bonds, Healthcare and Energy bonds. We also advise underweight allocations to Technology and Pharmaceutical bonds. Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

Stay Positioned For Reflation

Stay Positioned For Reflation

Table 3BCorporate Sector Risk Vs. Reward*

Stay Positioned For Reflation

Stay Positioned For Reflation

High-Yield: Neutral High-Yield outperformed the duration-equivalent Treasury index by 382 basis points in November, bringing year-to-date excess returns up to -5 bps. After last month’s strong outperformance, Ba-rated junk bonds are now beating duration-equivalent Treasuries by 267 bps, year-to-date. The B and Caa credit tiers are lagging by 179 bps and 548 bps, respectively. We still view Ba-rated junk bonds as the sweet spot within the corporate credit space. The sector is relatively insulated from default risk and yet still offers a sizeable spread pick-up over investment grade corporates (Chart 3). We remain underweight B-rated and lower junk bonds for now as those securities are pricing-in a relatively optimistic outlook for the default rate. But, an imminent vaccine roll-out makes that outlook appear more realistic and we could soon upgrade the lower-rated junk credit tiers when we think the value is exhausted in the Ba-rated and higher securities. Looking at value for the junk index as a whole, we see that the index is pricing-in a default rate of 3% for the next 12 months, significantly below the 8.3% that was observed during the most recent 12-month period (panel 3). However, only four corporate issuers defaulted in October down from a monthly peak of 22 in July. Job cut announcements, an excellent indicator of the default rate, are also falling rapidly (bottom panel). At the sector level, we advise overweight allocations to high-yield Technology and Energy bonds. We are underweight the Healthcare and Pharmaceutical sectors. Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

MBS: Underweight Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by one basis point in November, dragging year-to-date excess returns down to -39 bps. The conventional 30-year MBS index option-adjusted spread (OAS) tightened 1 bp on the month, and it currently sits at 64 bps (Chart 4). This is significantly higher than the 59 bps offered by Aa-rated corporate bonds, the 53 bps offered by Agency CMBS and the 25 bps offered by Aaa-rated consumer ABS. Despite the relatively attractive OAS, we continue to view the elevated primary mortgage spread as a risk for MBS investors. It suggests that mortgage rates need not rise alongside Treasury yields in the near-term, meaning that mortgage refinancings can continue at their current rapid pace (panel 3). All else equal, this elevated refinancing activity will pressure MBS spreads wider. The recent spike in the mortgage delinquency rate does not pose a near-term risk to spreads as it is being driven by households that have been granted forbearance from the federal government (panel 4). The risk for MBS holders only comes into play if many households are unable to resume their regular mortgage payments when the forbearance period expires early next year. But even in that case, further government intervention to either support household incomes or extend the forbearance period would mitigate the risk. Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Government-Related: Underweight The Government-Related index outperformed the duration-equivalent Treasury index by 64 basis points in November, bringing year-to-date excess returns up to -222 bps. Sovereign debt outperformed duration-equivalent Treasuries by 157 bps on the month, bringing year-to-date excess returns up to -269 bps. Foreign Agencies outperformed the Treasury benchmark by 46 bps in November, bringing year-to-date excess returns up to -647 bps. Local Authority debt outperformed Treasuries by 139 bps in November, bringing year-to-date excess returns up to -228 bps. Domestic Agency bonds outperformed by 10 bps, bringing year-to-date excess returns up to -23 bps. Supranationals outperformed by 9 bps, bringing year-to-date excess returns up to +2 bps. US dollar weakness is usually a boon for Emerging Market (EM) Sovereign and Foreign Agency returns. However, this year’s dollar weakness has occurred mostly relative to other Developed Market currencies (Chart 5). Value has improved somewhat for EM Sovereigns during the past few weeks, but the index continues to offer less spread than the Baa-rated US Credit index (panel 4). At the country level, Turkey, Colombia, Mexico, Russia and South Africa are the only countries that offer a spread pick-up relative to duration and quality-matched US corporates. Of those, only Mexico looks attractive on a risk/reward basis. Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

Municipal Bonds: Overweight Municipal bonds outperformed the duration-equivalent Treasury index by 130 basis points in November, bringing year-to-date excess returns up to -340 bps (before adjusting for the tax advantage). Municipal bond spreads tightened sharply relative to both Treasuries and Corporates in November, but they remain exceptionally attractive relative to history (Chart 6). In fact, as we showed in a recent report, the Bloomberg Barclays Revenue Bond index offers a greater yield than the quality-matched Credit index across the entire maturity spectrum (before adjusting for the tax advantage).1 This is also true for the Bloomberg Barclays General Obligation (GO) index beyond the 12-year maturity point. Eight-to-twelve-year maturity GO bonds trade only 1 basis point through the Credit index, implying a breakeven effective tax rate of 4%. Six-to-eight-year maturities trade 11 bps through the Credit index, implying a breakeven effective tax rate of 16%. Extraordinary valuation is the main reason for our recommendation to overweight municipal bonds. The severe ongoing state & local government credit crunch is a concern, but it is a risk we are willing to take. It now looks possible that a relief package containing some federal funds for state & local governments will be passed before the end of the year. This would alleviate a lot of the concern. But even in the absence of federal assistance, the combination of austerity measures (bottom panel) and all-time high State Rainy Day Fund balances should help stave off a wave of municipal downgrades. Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell The Treasury curve bull-flattened in November, but then bear-steepened sharply during the first week of December. All told, the 2/10 Treasury slope is currently 81 bps, 7 bps steeper than at the end of October. The 5/30 Treasury slope is 131 bps, 4 bps steeper than at the end of October. Our expectation is that continued economic recovery will cause investors to price-in eventual monetary tightening at the long-end of the Treasury curve. With the Fed maintaining a firm grip on the front end, this will lead to Treasury curve bear steepening. A timely vaccine roll-out and/or further fiscal stimulus will speed this process up. We recommend positioning for a steeper curve by owning the 5-year Treasury note and shorting a duration-matched barbell consisting of the 2-year note and 10-year notes. This position is designed to profit from 2/10 curve steepening. Valuation is a concern with our recommended steepener, as the 5-year yield is below the yield on the duration-matched 2/10 barbell (Chart 7). However, the 5-year looked much more expensive during the last zero-lower-bound period between 2010 and 2013 (bottom 2 panels). We anticipate a return to similar levels. Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

TIPS: Overweight TIPS outperformed the duration-equivalent nominal Treasury index by 70 basis points in November, bringing year-to-date excess returns up to -23 bps. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates rose 8 bps and 5 bps on the month. They currently sit at 1.91% and 1.96%, respectively. Core CPI was flat in October and the year-over-year rate dropped from 1.73% to 1.63%. The 12-month trimmed mean CPI fell even more – from 2.37% to 2.22% – so the gap between core and trimmed mean inflation continued to narrow (Chart 8). We expect further narrowing in the months ahead, and therefore expect core CPI to come in relatively hot. For this reason, we recommend maintaining an overweight allocation to TIPS versus nominal Treasuries for the time being, even though the 10-year TIPS breakeven rate is now somewhat expensive according to our Adaptive Expectations Model (panel 2).2 Inflation pressures may moderate once core and trimmed mean inflation measures converge, and this could give us an opportunity to tactically reduce TIPS exposure sometime next year. We also recommend holding real yield curve steepeners and inflation curve flatteners. With the Fed now officially targeting an overshoot of its 2% inflation goal, we would expect the cost of 2-year inflation protection to rise above the cost of 10-year inflation protection (panel 4). With the Fed also exerting more control over short-dated nominal yields than over long-term ones, we expect that short-maturity real yields will come under downward pressure relative to the long end (bottom panel). Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

ABS: Overweight Asset-Backed Securities outperformed the duration-equivalent Treasury index by 11 basis points in November, bringing year-to-date excess returns up to +82 bps. Aaa-rated ABS outperformed the Treasury benchmark by 10 bps on the month, bringing year-to-date excess returns up to +68 bps. Non-Aaa ABS outperformed by 17 bps, bringing year-to-date excess returns up to +174 bps (Chart 9). On paper, the Treasury department’s decision to let the Term Asset-Backed Loan Facility (TALF) expire at the end of the year is quite negative for ABS. However, as we explained in a recent report, we don’t expect a material impact on spreads.3 For one thing, Aaa ABS spreads are already well below the borrowing cost offered by TALF. But more importantly, consumer credit quality remains quite robust. As we first explained back in June, the stimulus received from the CARES act led to a significant increase in disposable income and a jump in the savings rate (panel 4).4 Faced with an income boost and few spending opportunities, many households took the opportunity to pay down consumer debt. Granted, further income support from Congress is needed now that the CARES act’s enhanced unemployment benefits have expired. But given the substantial boost to savings that has already occurred, we are confident that more stimulus will arrive in time to prevent a wave of consumer bankruptcies. Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 85 basis points in November, bringing year-to-date excess returns up to -168 bps. Aaa Non-Agency CMBS outperformed Treasuries by 71 bps on the month, bringing year-to-date excess returns up to -2 bps. Non-Aaa Non-Agency CMBS outperformed by 127 bps, bringing year-to-date excess returns up to -620 bps (Chart 10). We continue to recommend an overweight allocation to Aaa-rated Non-Agency CMBS and an underweight allocation to non-Aaa CMBS. Even with the imminent expiry of TALF, Aaa CMBS spreads are already well below the cost of borrowing through TALF and thus will not be negatively impacted.5 Meanwhile, the structurally challenging environment for commercial real estate could lead to problems for lower-rated CMBS (panels 3 & 4). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 38 basis points in November, bringing year-to-date excess returns up to +55 bps. The average index spread tightened 6 bps on the month. It currently sits at 53 bps, above typical historical levels (bottom panel). At its September meeting, the Fed decided to slow its pace of Agency CMBS purchases. It is no longer looking to increase its Agency CMBS holdings, but rather, it is only purchasing what is “needed to sustain smooth market functioning”. This is nonetheless a Fed back-stop of the market, and it does not change our overweight recommendation. Appendix A: Buy What The Fed Is Buying The Fed rolled out a number of aggressive lending facilities on March 23. These facilities focused on different specific sectors of the US bond market. The fact that the Fed has decided to support some parts of the market and not others has caused some traditional bond market correlations to break down. It has also led us to adopt of a strategy of “Buy What The Fed Is Buying”. That is, we favor those sectors that offer attractive spreads and that benefit from Fed support. The below Table tracks the performance of different bond sectors since the March 23 announcement. We will use this to monitor bond market correlations and evaluate our strategy’s success. Table Performance Since March 23 Announcement Of Emergency Fed Facilities

Stay Positioned For Reflation

Stay Positioned For Reflation

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of December 4TH, 2020)

Stay Positioned For Reflation

Stay Positioned For Reflation

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of December 4TH, 2020)

Stay Positioned For Reflation

Stay Positioned For Reflation

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 70 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 70 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

Stay Positioned For Reflation

Stay Positioned For Reflation

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Chart 11Excess Return Bond Map (As Of December 4TH, 2020)

Stay Positioned For Reflation

Stay Positioned For Reflation

Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “Political Risk Will Dominate In A Pivotal Month For The Bond Market”, dated October 13, 2020, available at usbs.bcaresearch.com 2 For more details on our model please see US Bond Strategy Weekly Report, “How Are Inflation Expectations Adapting?”, dated February 11, 2020, available at usbs.bcaresearch.com 3 Please see US Bond Strategy Weekly Report, “Preparing For A Dark Winter … But Do Markets Care?”, dated November 24, 2020, available at usbs.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com 5 Please see US Bond Strategy Weekly Report, “Preparing For A Dark Winter … But Do Markets Care?”, dated November 24, 2020, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

Highlights Every year we review our best and worst calls – both in terms of geopolitics and markets. This year our geopolitical forecasting and strategic market recommendations performed well, given the COVID-19 shock, but our tactical trades often went awry. We correctly forecast the presidency, Senate, Democratic nomination, and impeachment outcome. We anticipated “stimulus hiccups” but expected them to be resolved by November 3. The Georgia runoff on January 5 presents a 30% risk to our Senate prediction. In the main, we were right on Chinese politics, EU politics, US-Iran tensions, and Russian politics. US-China tensions kept rising, as expected, but the market ignored it. We missed the Saudi-Russia cartel break-up in Q1. The jury is still out on Brexit. Strategically, we got the big market moves right, but we were too risk-averse during the summer and after the election. Stay long cyber-security stocks in general, but close the pair trade versus Big Tech. Close the 10-year Treasury hedge. Feature Chart 1The Black Swan

The Black Swan

The Black Swan

The COVID-19 pandemic took investors by surprise, defined the year 2020, and caused the shortest bear market in history, lasting 33 days (Chart 1). On the whole this year’s crisis illustrates how geopolitical analysis is not primarily concerned with “black swan” events, which are inherently unpredictable. Rather the wholly unexpected pandemic reinforced several of our pre-existing geopolitical themes and trends: de-globalization, American sociopolitical instability, European integration, and US-China conflict. This year our geopolitical forecasting and strategic market recommendations performed well, given the COVID-19 shock, but our tactical trades often went awry. Whether these and other trends will continue in 2021 will be the subject of our strategic outlook due next week. This week we offer our annual report card, which reviews our best and worst calls for the year with a desire to hold ourselves accountable to clients, learn investment lessons from mistakes, and hone our geopolitical method of analysis. Successful Strategy, Debatable Tactics Overall our performance this year was good. Specifically, our political forecasting was on target and our investment recommendations got the big moves correct. But our risk-averse tactical trades were less successful. In last year’s annual outlook, “2020 Key Views: The Anarchic Society,” our main investment recommendation was long gold – based on sky-high geopolitical risk and a shift toward reflationary policy by the Federal Reserve, China, and the European Union (Chart 2). We maintain this trade today, despite its losing some altitude recently, as we expect to see low real rates, reflationary global policy, and rising inflation expectations. Geopolitical risk will also remain elevated despite dropping off from recent peaks, and not only during President Trump’s “lame duck” final days in office. We sounded the alarm for clients in our January 24 report, “Market Hurdles: From Sanders To Iran,” warning that global equities and risk appetite would suffer “in the very near term” due to conventional political risks as well as the new coronavirus, which we feared would explode as a result of Chinese New Year. In retrospect we were not bearish enough even in these reports. In our March 27 report, “No Depression,” we advised that the extraordinary monetary and fiscal response to the crisis would reflate the global economy and thus went long Brent crude oil. From this point onward we gradually added risk to our strategic portfolio, including by going long global equities relative to bonds in June (Chart 3). Chart 2Gold Paid Off When Black Swan Arose

Gold Paid Off When Black Swan Arose

Gold Paid Off When Black Swan Arose

Of course, despite getting these big moves right, we abandoned several of our strategic recommendations during the crisis and some of our tactical trades went awry throughout the year. Chart 3When Crisis Hits, Buy Risk Assets!

When Crisis Hits, Buy Risk Assets!

When Crisis Hits, Buy Risk Assets!

Our Worst Calls Of 2020 We chose a very bad time, last December, to bet heavily on global equity rotation from growth to value and away from tech sector leadership. US equities and tech stocks surged ahead of global equities on the back of the pandemic. Our long energy / short tech trade proved disastrous. Only now, with a vaccine on the horizon, are these recommendations coming to fruition. On the other hand, we should have remained committed to our long EUR-USD position rather than cutting it short when the crisis erupted (Chart 4). Global stimulus and the Fed’s sharp reduction in interest rates and gigantic infusion of US dollar liquidity ensured that the dollar would plummet. Strategically, we got the big market moves right, but we were too risk-averse during the summer and after the election. In some cases our geopolitical forecast proved dead-on while our market recommendation faltered. One of biggest geopolitical forecasts, in September 2019, was that the US and China could well conclude a trade deal but that it would be extremely limited in scope and strategic tensions would continue to rise dangerously. This prediction has proved accurate, judging by US high-tech export controls and China’s suppression of Hong Kong this year. But we misjudged the market response, particularly after China contained the virus: the renminbi saw a tremendous rally this year while we remained short, suffering a 4.96% loss so far (Chart 5). Chart 4Stick With Your Guns...Even Amidst Crisis

Stick With Your Guns...Even Amidst Crisis

Stick With Your Guns...Even Amidst Crisis

Chart 5US-China Tensions Persisted, But The Market Didn't Care

US-China Tensions Persisted, But The Market Didn't Care

US-China Tensions Persisted, But The Market Didn't Care

Along these lines, President-elect Joe Biden’s statement that he will maintain President Trump’s tariffs is another confirmation of one of our most contrarian views over the past year.1 We would expect the People’s Bank to allow the yuan to slip both to deal with lingering deflationary pressures and to build up some poker chips for the coming negotiations with Biden. We also would expect the US dollar to witness a near-term tactical bounce. However, if we are wrong, our short CNY-USD trade will fall further and we will have to cut our losses. Chart 6You Can't Time The Market

You Can't Time The Market

You Can't Time The Market

Other mistakes occurred when solid economic and political views combined with bad market timing. Our long position in cyber-security stocks is well grounded – we remain invested – but once again we jumped the gun on the rotation away from Big Tech, which constituted the short end of two of our pair trades, now closed. Separately, we coupled our long gold bet with a long silver bet that came far too late into the rally – though we remain strategically optimistic on silver due to its industrial uses, which should revive in the post-pandemic context. Lamentably, we ran up against our stop-loss threshold on our structural position in US aerospace and defense stocks not long before the vaccine announcement would have begun the arduous process of recuperating losses (Chart 6). We have reinitiated the latter trade, albeit in global defense stocks rather than just American. The inverse also occurred, in which our political forecasting proved faulty but our market implications worked out quite well. One of our biggest political forecasting failures stemmed from an initial success. Beginning in May, we signaled that the US Congress would experience “stimulus hiccups” in trying to pass additional fiscal relief for the economy. This view proved prescient as negotiations fell through in July and a range of benefits expired. Real rates began to recuperate at this time. The problem is that we also predicted that the fiscal impasse was merely a hiccup, i.e. would be resolved prior to the election. It remains unresolved to this day. Fortunately, our market recommendation – to go long US municipal bonds relative to duration-matched treasuries – was rooted in the principle of “buy what the Fed is buying” and therefore continued to appreciate, along with our similarly justified position in investment grade bonds (Chart 7). Chart 7Stimulus Hiccup Occurred, But Was Not Resolved

Stimulus Hiccup Occurred, But Was Not Resolved

Stimulus Hiccup Occurred, But Was Not Resolved

Our biggest error of political forecasting was the collapse of OPEC 2.0 at the beginning of the year. We signaled to clients in January that Russia was growing internally unstable and that this would result in an external action that would prove market-negative. This was correct, but we failed to anticipate that the most important consequence would be a temporary Russian rejection of Saudi demands for oil production cuts. Still, we advised clients to stay the course, arguing that the Russians and Saudis were geopolitically constrained and would return to their cartel, which proved to be the case, thus hastening the restoration of balance to oil markets. This view supported our long spot oil recommendation in late March, though the idea that US producers might collaborate proved fanciful. Alternatively we suggested that clients go long oil relative to gold, which has performed well. Other mistakes stemmed from our tactical trades. Generally, we were insufficiently bullish both during the summer and after the US election. In both cases we overemphasized the absence of US fiscal stimulus as a risk to the rally. In reality the first stimulus was sufficient and the V-shaped recovery of the private economy reduced the need for additional support over the course of the year. Our long tactical positions in US treasuries, consumer staples, and JPY-EUR did not pan out. The takeaway going forward, given that the market is not pressuring politicians to act, is that the risk of another congressional fiscal failure prior to Christmas is underrated. Lastly, some minor emerging market trades went awry, such as our long positions in Thai and Malay equities and our shorting the South African rand. We wrongly predicted that Michelle Obama would be Joe Biden’s pick for vice president, when in fact that honor went to Senator Kamala Harris. Our Best Calls Of 2020 While we got the big market moves right in 2020, our best calls were political and geopolitical in nature: Joe Biden won the US election. He won through his ability to win back blue-collar workers and compete in the Sun Belt as well as the Rust Belt, which we outlined as a key geographic strength during his run in the Democratic primary election (Map 1). We downgraded Trump from 55% odds of re-election to 35% in March, when the lockdowns occurred, and we upgraded Trump only to 45% in October when he rallied. The thin margins in the swing states confirmed this higher-than-consensus probability of a Trump win. Map 1Joe Biden Won The Rust Belt And The Sun Belt

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Republicans retained the Senate. Beginning in late September, we saw that President Trump was rallying and that this would increase the odds of a Republican Senate even if Trump himself fell short. On October 16 we signaled that the Senate was too close to call, and on October 30 we upgraded the GOP again and argued that a Democratic White House plus a Republican Senate was the most likely scenario (Chart 8). There is a lingering risk to this view: a double Democratic victory in the Georgia runoffs on January 5, 2021. But we put the odds of that at 30% at best. Chart 8Republicans Held The Senate (Pending Georgia Runoffs)

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Chart 9Biden Won The Democratic Primary Nomination

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Biden won the Democratic nomination, which we first highlighted in November 2018 and June 2019 and consistently thereafter, though we never underrated his challengers (Chart 9). Trump was acquitted of impeachment charges, which seems like ages ago. We said from the start that Democrats did not have the votes (Chart 10). China stimulated the economy massively and avoided massive domestic unrest. Investors doubted that Beijing would stimulate enough to lead to a global recovery, given the leadership’s preference to avoid systemic financial risk. We insisted that constraints would prevail over preferences and the stimulus would be gigantic. Our “China Play Index” skyrocketed, though it did not outperform global equities (Chart 11). We also argued that President Xi Jinping would not face significant domestic unrest after the crisis erupted, though we view domestic political risk as underrated for the coming years. Chart 10Impeachment Failed

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Long Emerging markets and deep cyclicals recovered. The combination of Chinese stimulus and a US “return to normalcy” led us to go long emerging markets after the election. We articulated this trade by going long Trans-Pacific Partnership countries, on the expectation that Washington will remain hawkish toward China over trade (Chart 12). We also went long deep cyclicals and US infrastructure plays on the basis of Chinese stimulus and the Biden-Trump common denominator on building projects (Chart 13). Chart 11China Stimulated Massively

China Stimulated Massively

China Stimulated Massively

Chart 12Long Trans-Pacific Partnership Worked As EM Play

Long Trans-Pacific Partnership Worked As EM Play

Long Trans-Pacific Partnership Worked As EM Play

The Taiwan Strait was a bigger geopolitical risk than the Korean peninsula, which markets are at last recognizing (Chart 14). Unfortunately for investors Taiwan remains a serious geopolitical risk regardless of Trump’s exit. Hong Kong attracted investors’ attention more than Taiwan in 2020, whereas we have treated Hong Kong as a red herring. Chart 13Long Infrastructure And Cyclicals Paid Off

Long Infrastructure And Cyclicals Paid Off

Long Infrastructure And Cyclicals Paid Off

Chart 14Hong Kong Was A Red Herring, Korea Beat Taiwan

Hong Kong Was A Red Herring, Korea Beat Taiwan

Hong Kong Was A Red Herring, Korea Beat Taiwan

Brexit has been a red herring throughout 2020, as expected, though an end-of-year failure to agree to a UK-EU trade deal would upend our predictions (Chart 15). Chart 15Brexit Was A Sideshow

Brexit Was A Sideshow

Brexit Was A Sideshow

Germany’s shift to more dovish fiscal policy strengthened European solidarity, keeping peripheral bond yields and “break-up risk” contained (Chart 16). In August 2019 we argued that Germany was easing fiscal policy but would not surge spending until a crisis happened – which proved to be the case when the coronavirus prompted Olaf Scholz to wheel out the “bazooka” this year. We also argued that Europe would be willing to mutualize debt, which was officially confirmed when outgoing Chancellor Angela Merkel forged an agreement on an EU Recovery Fund with French President Emmanuel Macron (though not exactly a “Hamiltonian moment”). Chart 16European Solidarity Strengthened

European Solidarity Strengthened

European Solidarity Strengthened

Chart 17Peak Shinzo Abe' Theme Boosted The Yen

Peak Shinzo Abe' Theme Boosted The Yen

Peak Shinzo Abe' Theme Boosted The Yen

Japan saw “Peak Abenomics,” which was confirmed this year when he handed the helm over to his deputy, Yoshihide Suga, whose policies are continuous. Abe’s late-2019 tax hike was only one of many reasons we anticipated a rally in the yen, which was supercharged by this year’s crisis (Chart 17). Russia’s political risk premium spiked, as we expected, though we did not anticipate that the cause would be a temporary breakdown in OPEC 2.0 (Chart 18). We were more prepared for an event like the poisoning of Alexei Navalny and US sanctions against the Nordstream II pipeline. Our argument that Russia would lie low, for fear of domestic unrest, has so far borne out in the Belarus protests and the conflict in Nagorno-Karabakh. Whether it will continue to do so in the face of what will likely be a pro-democracy assault in eastern Europe from the US Democratic Party remains to be seen. Chart 18Russian Geopolitical Risk Spiked As Predicted

Russian Geopolitical Risk Spiked As Predicted

Russian Geopolitical Risk Spiked As Predicted

India-China tensions were a red herring. India benefited from the western world’s turn against China. Partnerships and alliances were already taking shape before the coronavirus spurred a move in the West to diminish reliance on China’s health care exports. Our long Indian pharmaceuticals trade was highly profitable, though our overweight in Indian bonds was less so (Chart 19). Chart 19India Benefited From West's Anti-China Turn

India Benefited From West's Anti-China Turn

India Benefited From West's Anti-China Turn

Brazilian political risk surged to the highest levels since the 2018 election, and President Jair Bolsonaro suffered a setback in municipal elections, as we expected, especially after witnessing his cavalier attitude toward the pandemic (Chart 20). However, his approval rating rose on the back of fiscal largesse, implying that debt dynamics will continue to trouble this market despite the bullish backdrop for emerging markets in 2021. Chart 20Brazil Remained A Muddle

Brazil Remained A Muddle

Brazil Remained A Muddle

Chart 21Turkish Populism Exacted A Toll

Turkish Populism Exacted A Toll

Turkish Populism Exacted A Toll

Chart 22A Bull Market In Iran Tensions

Bull Market In US-Iran Tensions

Bull Market In US-Iran Tensions

The Turkish lira collapsed, as Turkish President Recep Erdogan maintained reckless domestic economic policies and foreign adventurism (Chart 21). As we go to press, Erdogan appears to be backing down from his aggressive approach to maritime-territorial disputes in the Mediterranean, for fear of European sanctions, which would be a positive surprise, albeit temporary. The “bull market in Iran tensions” continued, with US-Israeli sabotage and assassinations of key Iranian figures bookending the year (Chart 22). With Trump still in office for another 45 days, we would not be surprised to see another move on Iran, where hardliners are ascendant in the unstable advance of the Supreme Leader Ali Khamenei’s eventual succession. So far, Trump has taken market-negative actions in his “lame duck” period on Iran, China, and Big Tech, as we argued, which means more is coming despite the market’s enthusiasm over the partly sunny outlook for 2021. Investment Takeaways Geopolitical analysis is about structural themes and trends – not unpredictable black swans, which may even further entrench structural trends. When a crisis triggers a massive selloff, buy risk assets, then reassess. The gargantuan, coordinated monetary and fiscal response to this year’s crisis presented a clear buy signal. Once the virus was revealed not to be as deadly as first suspected, the rally gained steam. Political and geopolitical forecasts may be dead-on and yet fail to drive the market. There is a constant need to refine the ability to articulate and implement trades that seek to generate alpha from policy insight. Tactical views and attempts at cleverness are a liability when one’s strategic views – geopolitical, macro-economic, financial – are firmly grounded. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Thomas L. Friedman, "Biden Made Sure ‘Trump Is Not Going To Be President For Four More Years,’" New York Times, December 2, 2020, nytimes.com.

Our semi-annual virtual meeting with the long-standing client Ms. Mea took place on December 1. Given it is the end of the year, Ms. Mea inquired about our strategies for 2021 and reviewed the evolution of our views during 2020. Below is a transcript of our discussion, which we hope will help clients better grasp our views and analysis. Chart 1EM Relative Equity Performance And EM Currencies Versus DM ex-US

EM Relative Equity Performance And EM Currencies Versus DM ex-US

EM Relative Equity Performance And EM Currencies Versus DM ex-US

Ms. Mea: Before we get to investment recommendations for next year, let’s review which of your views have worked in 2020 and which have not. Answer: From a big picture perspective, we went from being very negative on EM over the last decade to being neutral on EM risk assets in both absolute terms and relative to DM peers. Since April, we have been waiting for a pullback to go long and overweight EM, but a meaningful setback has not materialized. That said, although EM risk assets and currencies have rallied substantially in absolute terms, they have not outperformed their DM peers, as shown in Chart 1. Concerning the evolution of our strategy, as you might recall, we had to chase EM stocks higher late last year after the trade deal between the US and China created euphoria in financial markets, pushing EM assets higher. But even then, we did not change our bullish view on the US dollar and continued recommending an underweight allocation in EM versus DM in global equity and credit portfolios. In our January 23, 2020 report we contended that the risk premium in global markets was extremely low and that risk assets were extremely overbought. The following week, as news of the COVID-19 outbreak in China emerged, we recommended closing the long position in EM stocks. On February 20, we asserted that odds of a breakdown were substantial and recommended shorting EM stocks outright. We closed this position on March 19 with a substantial gain. On March 26, we argued that it was too late to sell but too early to buy. In retrospect, the latter part of this assessment was incorrect. Then, on April 23, we recommended going long duration in EM local currency bonds or buying domestic EM bonds while hedging currency risk. We recommended receiving 10-year swap rates in several EM countries. We changed our long-standing strategic bullish stance on the US dollar to bearish on July 9. Simultaneously, we closed our shorts in various EM currencies versus the greenback and recommended shorting many of these EM currencies versus an equal-weighted basket of the euro, CHF and JPY (please refer to the bottom panel of Chart 1). We upgraded EM credit from underweight to neutral on June 4 and lifted the allocation to EM stocks from underweight to neutral on July 30. EM relative equity performance versus DM has been in a broad trading range for the whole of 2020 (please refer to the top panel of Chart 1). Chart 2Facing Technical Resistance

Facing Technical Resistance

Facing Technical Resistance

Ms. Mea: What is your EM outlook going into 2021? Answer: The odds of a major breakout in EM equities, currencies and fixed-income markets have risen, yet there could be a shakeout before the breakout. Both EM equity and the global ex-US equity indexes have risen to their previous highs which proved to be a formidable resistance level (Chart 2). The main reasons to expect a major breakout in EM and global ex-US share prices are as follows: First, the global economy could experience periodic setbacks, but things cannot be worse than they were during the pandemic-induced lockdowns in early 2020. The deployment of vaccines is likely to improve global economic conditions in 2021, especially in hard hit services sectors. Second, asset purchases by major central banks around the world have effectively removed many securities (mostly government bonds) from the marketplace while creating an enormous supply of money (Chart 3). The upshot is that too much money is chasing fewer assets. Chart 4 illustrates this phenomenon in the case of US dollar securities. Cash in both US institutional and retail money market funds is still elevated. As a share of market value of US dollar denominated equities and bonds, the amount in US money market funds has declined but it is still above its February lows. Provided that US money market rates are zero, one can make the case for more flows from money markets into both equities and bonds. Chart 3Booming Money Supply Worldwide

Booming MoneySupply Worldwide

Booming MoneySupply Worldwide

Chart 4How Much Cash On-SidelinesIs There Left In The US?

How Much Cash On-SidelinesIs There Left In The US?

How Much Cash On-SidelinesIs There Left In The US?

Finally, odds that EM equities will break above the trading range they have been in over the last 10 years have increased. As we discussed in our previous reports, EM ex-China, Korea and Taiwan have been facing hard budget constraints due to limited fiscal stimulus packages, a breakdown in their monetary transmission mechanism, and massive foreign capital outflows in early 2020. These harsh conditions have forced many companies to restructure to boost their efficiency. The banking system has been recognizing and provisioning for bad assets. Finally, some governments have adopted difficult structural reforms. These could be sowing seeds of structural transformation in these economies, in turn producing a secular bull market in their equities and currencies. As was discussed in a recent Country In-Depth report, India is one example where structural reforms stand to have a positive effect on its long-term outlook. Indonesia, Colombia, Mexico, and Brazil are other candidates that could undergo similar transformations. In a nutshell, unless the global economy craters – which has low odds – one can envision a scenario in which risk assets continue marching higher. Ms. Mea: However, you mentioned that there could be a shakeout before the breakout. What makes you say that? Answer: A potential shakeout before the breakout may occur due to the following three peaks: Peak investor sentiment: Investor sentiment is very elevated and risk assets are overbought. The ZEW global growth expectations index (a survey of analysts on DM economies) has rolled over after reaching an all-time high (Chart 5, top panel). The Sentix survey of investor future expectations has reached an apex (Chart 5, bottom panel). Importantly, net long positions in copper and net bullish sentiment on copper are at their previous highs (Chart 6). This is a plausible proxy for investor sentiment on both China and global growth. Chart 5Investor Expectations Are Elevated Edited

Investor Expectations Are ElevatedEdited

Investor Expectations Are ElevatedEdited

Chart 6Investors Are Super Bullish On And Very Long Copper

Investors Are Super Bullish On And Very Long Copper

Investors Are Super Bullish On And Very Long Copper

Chart 7Investors Are Bullish On US Equities

Investors Are Bullish On US Equities

Investors Are Bullish On US Equities

Finally, sentiment among US equity investors is also elevated (Chart 7). Peak stimulus: In China, both credit and fiscal stimulus will likely peak in Q4 2020, as demonstrated in Charts 8 and 9. The US and the euro area will experience a negative fiscal thrust in 2021 equal to 7.4% and 3.8% of GDP, respectively. A new fiscal package worth $1.5 trillion is needed in order for the US fiscal thrust to be neutral. As Republicans are likely to retain control of the Senate, even after Georgia’s Senate election vote on January 5, 2021, a new fiscal package larger than $500-750 billion is unlikely. On the whole, many countries in DM and EM are experiencing peak stimulus in 2020. Chart 8China: Peak Credit Stimulus

China: Peak Credit Stimulus

China: Peak Credit Stimulus

Chart 9China: Peak Fiscal Stimulus

China: Peak Fiscal Stimulus

China: Peak Fiscal Stimulus

Peak manufacturing growth: We should differentiate between the top in a business cycle and an end in growth acceleration. As far as global manufacturing is concerned, we are likely currently experiencing growth acceleration at its height. Global manufacturing will continue to expand, but at a slower rate. Share prices could either rally or correct when growth begins to decelerate. The stock market reaction is contingent upon how overbought and how expensive equity prices are. The top panel of Chart 10 illustrates that the tops in the US ISM manufacturing new orders-to-inventory ratio have historically marked setbacks in global cyclical stocks. Similarly, EM share prices and industrial metals fluctuate with the EM and China manufacturing PMI (Chart 10, middle and bottom panels). Having risen sharply to very elevated levels, odds are that global and China manufacturing PMIs are probably topping out. Granted, these are diffusion indexes, and declines/rollovers in global manufacturing PMIs do not necessarily imply that a recession is on the horizon. Rather, they signal the end of the acceleration phase in a cycle. Bottom Line: Given how overbought and expensive they are, share prices might react negatively to peak stimulus. Ms. Mea: Your outlook on the Chinese economy has become more nuanced since the spring. How do you see China’s business cycle and financial markets evolving? Answer: We upgraded our view on the Chinese business cycle in late May after it had become apparent that China had again injected enormous credit and fiscal stimulus into the economy. On June 18, we upgraded Chinese stocks to overweight within an EM equity portfolio. We continue to expect decent growth numbers and reviving corporate profits in most of H1 2021. That said, authorities have been tightening monetary policy since May. Policymakers realize that China’s credit excesses have become even larger and they have been proactive in policy tightening to rein in leverage and speculative activities. The central bank has siphoned off banks’ excess reserves causing interbank rates to rise considerably (Chart 11). With a time lag, money/credit will decelerate and the business cycle will follow. We expect the Chinese business cycle to crest around the middle of 2021. Chart 10Cyclical Assets Fluctuate With Manufacturing PMIs

Cyclical Assets Fluctuate With Manufacturing PMIs

Cyclical Assets Fluctuate With Manufacturing PMIs

Chart 11China: Liquidity Tightening Works With A Time Lag

China: Liquidity Tightening Works With A Time Lag

China: Liquidity Tightening Works With A Time Lag

The recent shakeout in the onshore corporate bond market will lead to a reduction in corporate bond issuance as investors now require higher yields to finance SOEs. In addition, banks and non-bank financial institutions have to comply with the asset management regulation by the end of 2021. This will restrict banks’ ability to expand their balance sheets and curb NBFI risk appetite. All in all, credit-sensitive sectors like capital spending and the property market will decelerate considerably in H2 2021. Provided that they make up a large share in the mainland economy, overall income growth will also slump. Concerning financial markets, if there is a selloff in Chinese stocks in the coming weeks or months, it will give way to another upleg later in H1 2021. Ms. Mea: Going forward, what will be the driving forces of EM risk assets and how will they shape up? Answer: EM risk assets – equities, credit markets and high-yielding domestic bonds – are by and large driven by three factors: (1) China’s import and commodities cycles (which often move in tandem); (2) domestic fundamentals in EM ex-China; and (3) sharp swings in US growth and the S&P500. (1) We elaborated on the intricacies of the Chinese business cycle above and will now offer a few insights on commodities prices. There has been a broad-based recovery in Chinese demand for commodities and various commodities prices have risen substantially. Nevertheless, the outlook for commodities prices is less certain going forward. Chart 12China's Booming Copper Imports Imply Inventory Accumulation

China's Booming Copper Imports Imply Inventory Accumulation

China's Booming Copper Imports Imply Inventory Accumulation

In particular, copper prices have surged but the rally is only partially attributable to recovering real demand in China. Other forces, namely inventory restocking in China and financial (investor) demand, have been responsible for the massive rise in copper prices. The mainland’s imports of copper and copper products have boomed since spring, growing at a rate of 70-80% from a year ago. Meanwhile, the recovery in Chinese infrastructure investment in electricity, water, and gas – which are the largest consumers of copper – has been considerable but not extraordinary (Chart 12). This surge leads us to infer that a sizable inventory restocking cycle has been taking place in China since last spring. Such large inventory accumulation has likely been prompted by the easy availability of credit and rising copper prices. Besides, investors hold record net long positions in copper on the New York Mercantile Exchange (refer to Chart 6). In brief, as we discussed in detail in the Special Report from November 25, Chinese purchases of copper will decline even as its real demand for copper continues to expand. Oil prices are at risk of excess supply as many producers are reluctant to continue suppressing their crude output. Saudi Arabia has been trying hard to limit OPEC+ production. However, it will be increasingly difficult for it to do so. The basis is that many producers are naturally looking to maximize the net present value of cash flow from their oil reserves. Due to inflation, $45 today is worth more than $45 in five years. As and when oil producers accept that global demand for oil will stagnate as the world switches to more environmentally friendly sources of energy, they will have an incentive to produce and sell as much crude as possible at current prices. Chart 13EM Sovereign Credit Spreads (Shown Inverted) Fluctuate With Commodities Prices

EM Sovereign Credit Spreads (Shown Inverted) Fluctuate With Commodities Prices

EM Sovereign Credit Spreads (Shown Inverted) Fluctuate With Commodities Prices

If Saudis lose control over output, they will ramp up their own production to increase their market share. Crude prices will plunge anew. The timing is uncertain, but we expect it to happen sooner rather than later. Overall, even though China’s business cycle recovery will continue in H1 2021, prices for certain important commodities like oil and copper will likely struggle. Setbacks in commodities prices will have ramifications for financial markets in resource-producing EM countries. EM currencies, as well as their sovereign spreads, correlate with commodities prices (Chart 13). (2) Domestic demand in EM ex-China, Korea and Taiwan will gradually improve but from a very low point. Many developing countries still face major hurdles, including banking systems that are struggling with non-performing loans, a looming fiscal drag, and a lack of control over the pandemic. Further, EM outside North Asia will lag behind advanced countries in procuring and deploying COVID-19 vaccines. Consequently, consumer and business confidence will be slow to recover in these countries, and their business cycle revival will continue to trail that of North Asia (China, Korea and Taiwan) and advanced economies. (3) Finally, any shakeout in the S&P500 will reverberate through EM. Having rallied considerably, North Asian equity and currency markets have already priced in a great deal of good news. In EM ex-North Asia, the level of economic activity, albeit reviving, remains low. This makes these EM ex-North Asian financial markets very sensitive to fluctuations in global/US financial markets. Chart 14EM Equities Have Been A Low-Beta Play On The S&P500

EM Equities Have Been A Low-Beta Play On The S&P500

EM Equities Have Been A Low-Beta Play On The S&P500

The resilience of US equity and credit markets in recent months in the face of numerous challenges has surprised us. US share prices and credit markets have not corrected meaningfully despite (1) the third wave of COVID-19 which has resulted in partial lockdowns and a deterioration in consumer sentiment; (2) the lack of a second fiscal stimulus package and (3) uncertainty surrounding the presidential elections. In retrospect, investors have been willing to buy any small dip. Interestingly, in the past three years, EM share prices outperformed DM share prices when the S&P500 sold off and underperformed when US stocks rallied (Chart 14). EM versus DM relative share prices are shown inverted on this chart. This reveals that EM stocks are not a high beta on the S&P 500 and rising US equity markets do not guarantee that EM share prices will outperform their DM peers. Overall, the outlook for EM risk assets is convoluted, warranting a neutral stance for now both in absolute terms and relative to DM. Chart 15The US Dollar Is Oversold

The US Dollar Is Oversold

The US Dollar Is Oversold

Ms. Mea: Where and how does the US dollar enter your analysis? Answer: The dynamics between EM and the US dollar is push-pull in nature, i.e., the causality runs both ways. EM fundamentals – that could be broadly defined as return on capital in these economies – drive their exchange rates’ trends versus the US dollar. Further, US dollar trends are also shaped by several global macro forces, including the global business cycle. The US fiscal position and monetary policy stance also drive fluctuations in the value of the greenback. Over the next several years, the US dollar will likely be in a bear market because US inflation will rise and the Federal Reserve will fall behind the inflation curve. US real rates will remain negative, which will continue to undermine the dollar’s value. All that said, the US dollar has become very oversold and investor sentiment is bearish on the greenback (Chart 15). From a contrarian perspective, the dollar might be set up for a countertrend rebound. Interestingly, after the 2016 US elections, the US dollar rallied strongly for several weeks before selling off violently. It seems that the broad trade-weighted dollar is now following a reverse pattern (Chart 16). The US dollar in 2016 is shown inverted in this chart. The greenback was selling off before the 2020 US elections and has continued weakening since. If this reverse pattern were to play out, the US dollar will near its bottom soon and then stage a playable rebound. Chart 16The US Dollar Before And After 2016 And 2020 Presidential Elections

The US Dollar Before And After 2016 And 2020 Presidential Elections

The US Dollar Before And After 2016 And 2020 Presidential Elections

Chart 17EM Stocks Are Cheap If The Structural EPS Trend Is Up

EM Stocks Are Cheap If The Structural EPS Trend Is Up

EM Stocks Are Cheap If The Structural EPS Trend Is Up

In short, a long-term bear market but near-term rebound in the US dollar is consistent with our view of a shakeout before a breakout for EM equities and risk assets. Ms. Mea: What about EM equity and currency valuations? Are they not still cheap despite their recent rally? Answer: From a secular perspective, EM equities appear modestly cheap as illustrated by our cyclically-adjusted P/E (CAPE) ratio (Chart 17). However, it is vital to realize that this CAPE valuation model assumes that EPS (earnings per share) in real (inflation-adjusted) US dollar terms will revert to its long-term trend sooner rather than later (Chart 17, bottom panel). There is a lot of uncertainty regarding the structural trend in EM EPS. For the past decade – and therefore well before the pandemic – EM EPS in nominal US dollar terms has been fluctuating in a wide range (Chart 18). Not surprisingly, EM share prices have been flat for the past ten years. Further, EM EPS has massively underperformed US EPS in local currency terms for the past ten years (Chart 19). Consistently, EM share prices have underperformed the S&P 500 even in local currency terms. Chart 18EM EPS: No Growth For 10 years

EM EPS: No Growth For 10 years

EM EPS: No Growth For 10 years

Chart 19EM Versus US: Relative Stock Prices And Relative EPS

EM Versus US: Relative Stock Prices And Relative EPS

EM Versus US: Relative Stock Prices And Relative EPS

As for EM currencies, the aggregate real effective exchange rate of EM ex-China, Korea, Taiwan currencies suggests that they are cheap (Chart 20). Overall, to argue that EM stocks are cheap, one should be confident that EM EPS in real (inflation-adjusted) USD terms will be expanding in the years to come (Chart 17, bottom panel). While some EM economies have undertaken some restructuring, there is currently no strong evidence to suggest that EM EPS will be in a structural uptrend. From a cyclical perspective, EM EPS will certainly be recovering in 2021 (Chart 21). However, a notable chunk of this profit recovery has already been largely priced in. Chart 20EM ex-China, Korea, Taiwan: Currency Valuations

EM ex-China, Korea, Taiwan: Currency Valuations

EM ex-China, Korea, Taiwan: Currency Valuations

Chart 21EM Profits Will Recover In 2021

EM Profits Will Recover In 2021

EM Profits Will Recover In 2021

To sum up, a bet on EM share prices breaking out above their decade-long trading range implies betting on EM EPS entering a period of structural growth. Over the past ten years, EM companies have not delivered the secular growth needed to warrant higher equity multiples. We are open to the idea that structural reforms carried out in several nations will allow for higher productivity, income and profit growth. However, it is still too early to jump to that conclusion. Chart 22Will Asian Markets Finally Break Out?

Will Asian Markets Finally Break Out?

Will Asian Markets Finally Break Out?

Ms. Mea: Where in your analysis and strategy might you be wrong? Answer: The key risks to our view are twofold: First, FOMO (fear of missing out) on the part of investors continues to propel EM risk assets higher while either their fundamentals remain mediocre or they are already very expensive. As we have shown in Chart 4, there is still a lot of US dollar cash sitting in US money market funds and these could feed the EM rally, preventing the materialization of a shakeout. Second, we might be late to recognize structural shifts in certain EM economies and, might therefore miss breakouts in those bourses. Notably, there is no single EM equity market that has clearly broken above its previous highs (Chart 22). Ms. Mea: What are your overweights and underweights for equity, currency and fixed-income portfolios? Answer: For an EM equity portfolio, our strong conviction overweights have been and remain China, Korea and Mexico. Chart 23 shows the performance of our fully-invested EM equity portfolio based on our recommended country allocation. It has outperformed the EM MSCI equity benchmark by 3.7% in 2020 and by 74% since its initiation in May 2008. The latter translates into a 4.7% CAGR outperformance versus the EM MSCI equity benchmark in 10.5 years. Critically, this outperformance has been achieved with very low volatility and small drawdowns. Chart 23Performance Of Our EM Equity Country Allocation Portfolio (Country Recommendations)

Performance Of Our EM Equity Country Allocation Portfolio (Country Recommendations)

Performance Of Our EM Equity Country Allocation Portfolio (Country Recommendations)

As for EM local bonds, we continue to recommend receiving ten-year swap rates in Korea, Malaysia, Russia, Mexico, Colombia, South Africa, China and India. We are looking for a setback in their currencies to switch to holding cash bonds, i.e., without hedging currency risk. Among EM currencies, our short basket consists of BRL, CLP, ZAR, TRY and IDR while our favored ones have been MXN, RUB, CZK, INR THB and SGD. All these country recommendations and positions as well as the one in the EM sovereign credit space (US dollar bonds) are always presented at the end of our reports (please refer to the following pages). Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights Don’t trust market inflation expectations or real interest rates. When inflation is near-zero, think in nominal terms not in real terms. New structural recommendation: Underweight inflation protected bonds versus conventional bonds. For the time being stay overweight stocks versus bonds, but sell stocks if the 10-year T-bond yield rises by 0.3 percent. We address four concerns about inflation raised by clients. Fractal trade: short copper versus gold. Don’t Trust Market Inflation Expectations Or Real Interest Rates Are the markets any good at predicting inflation? No, they are not (Chart of the Week). Both the inflation forwards market and the breakeven inflation rate implied in inflation protected bonds have been lousy predictors of inflation.1 We can forgive that. What we cannot forgive is how these markets derive their inflation forecasts. Chart of the Week AThe Markets Are Lousy At Predicting Inflation

The Markets Are Lousy At Predicting Inflation

The Markets Are Lousy At Predicting Inflation

Chart of the Week BThe Markets Are Lousy At Predicting Inflation

The Markets Are Lousy At Predicting Inflation

The Markets Are Lousy At Predicting Inflation

Expected inflation in the UK just tracks the commodity price index (Chart I-2), and expected inflation in the US just tracks the oil price (Chart I-3 and Chart I-4). This link between expected inflation and the level of commodity prices is absurd, for three reasons: Chart I-2UK Bond Markets' Expected Inflation Just Tracks Commodity Prices

UK Bond Markets' Expected Inflation Just Tracks Commodity Prices

UK Bond Markets' Expected Inflation Just Tracks Commodity Prices

Chart I-3US Bond Markets' Expected Inflation Just Tracks The Oil Price

US Bond Markets' Expected Inflation Just Tracks The Oil Price

US Bond Markets' Expected Inflation Just Tracks The Oil Price

Chart I-4US Inflation Swaps' Expected Inflation Just Tracks The Oil Price

US Inflation Swaps' Expected Inflation Just Tracks The Oil Price

US Inflation Swaps' Expected Inflation Just Tracks The Oil Price

Inflation measures a change in a price. Therefore, inflation expectations should not track the price level of anything. Even if expected inflation is incorrectly tracking a price level, a lower price today will increase the scope for future inflation, and vice-versa. Hence, any relationship with the current price level should be an inverse relationship, not a positive relationship. Most absurd of all, how can the level of commodity prices today conceivably forecast the inflation rate five years ahead through 2026-31, as the inflation forwards seem to be suggesting? There are two important takeaways from the absurdity of inflation expectations. First, it follows that the market’s estimates of the real interest rate must also be lousy, and taken with a huge dose of salt. The market’s estimates of the real interest rate must be taken with a huge dose of salt. Second, as the market’s inflation expectations just track commodity prices, the relative performance of UK index-linked gilts versus conventional gilts just tracks commodity prices too (Chart I-5); and the performance of US TIPS versus T-bonds just tracks the oil price. Nothing more and nothing less (Chart I-6). As we expect the structural bear market in commodities has much further to run, the structural recommendation for bond investors is: Chart I-5UK Index-Linked Gilts Vs. Conventional Gilts = Commodity Prices

UK Index-Linked Gilts Vs. Conventional Gilts = Commodity Prices

UK Index-Linked Gilts Vs. Conventional Gilts = Commodity Prices

Chart I-6US TIPS Vs. T-Bonds = The Oil Price

US TIPS Vs. T-Bonds = The Oil Price

US TIPS Vs. T-Bonds = The Oil Price

Underweight inflation protected bonds versus conventional bonds. When Inflation Is Near-Zero, Think In Nominal Terms Not In Real Terms If the market is lousy at predicting long-term inflation, then it might also be lousy at predicting the long-term nominal return on equities. After all, shouldn’t prospective inflation impact the prospective 10-year nominal return on equities? The surprising answer is no. The prospective 10-year nominal return on the stock market depends only on the stock market’s starting valuation. The 10-year nominal return on the stock market does not depend on prospective inflation, it depends only on the stock market’s starting valuation. The same relationship between the stock market’s starting valuation and prospective nominal return applied in the high-inflation 1970s and 1980s as it did in the low-inflation 2000s (Chart I-7). Chart I-7The Stock Market's Starting Valuation Establishes The Prospective Nominal Return, Irrespective Of The Inflation Backdrop

The Stock Market's Starting Valuation Establishes The Prospective Nominal Return, Irrespective Of The Inflation Backdrop

The Stock Market's Starting Valuation Establishes The Prospective Nominal Return, Irrespective Of The Inflation Backdrop

The reason is that the stock market’s 10-year nominal return has two components: the income through the 10 years, and the terminal value at the end of the 10 years. When inflation is high, the income component is larger, but the terminal value component is smaller – because in an inflationary environment the market will demand a higher subsequent return, requiring a lower price. When inflation is low, the opposite is true: lower income, but higher terminal value. These effects cancel out, so the result is a prospective nominal return that is independent of prospective inflation. Crucially, the required prospective return on equities in excess of bonds is also established in nominal terms. This is because the bond yield’s lower limit is nominal, at say -1 percent. Proximity to this nominal yield limit makes bonds very risky because there is no longer any upside to price, only downside. Witness Swiss bonds this year. As the riskiness of equities and bonds converges, the required prospective nominal return on equities collapses towards the ultra-low bond yields. The upshot is that both the prospective return on equities and the required prospective return on equities should always be calculated in nominal terms, never in real terms. Right now, the high valuation of the aggregate stock market means a very low prospective nominal return, and this valuation is hypersensitive to ultra-low bond yields (Chart I-8 and Chart I-9). Chart I-8The Stock Market Is Priced To Generate A Feeble Long-Term Return

The Stock Market Is Priced To Generate A Feeble Long-Term Return

The Stock Market Is Priced To Generate A Feeble Long-Term Return

Chart I-9AUltra-Low Bond Yields Have Created The Greatest Asset-Price Inflation Of All Time

The Absurdity Of Inflation Expectations

The Absurdity Of Inflation Expectations

Chart I-9BUltra-Low Bond Yields Have Created The Greatest Asset-Price Inflation Of All Time

Ultra-Low Bond Yields Have Created The Greatest Asset-Price Inflation Of All Time

Ultra-Low Bond Yields Have Created The Greatest Asset-Price Inflation Of All Time

For the time being stay overweight stocks versus bonds, but as we warned two weeks ago, Sell Stocks If The Bond Yield Rises By 0.3 Percent. Four Concerns About Inflation Raised By Clients In this section, which is in question and answer format, we will address four concerns about long-term inflation that our clients have raised. 1, Isn’t the unprecedent fiscal stimulus in 2020 setting us up for inflation down the road? No, not in itself. Understand that the unprecedented stimulus is in response to unprecedented shocks to incomes that have come from the rolling waves of the pandemic. As incomes disappeared, governments provided income-substitution. As and when incomes reappear, governments will withdraw the income-substitution. Indeed, the UK government tried to withdraw its income-substitution (furlough) scheme prematurely and had to backtrack when the virus resurged. This illustrates that the unprecedented fiscal stimulus is a much-needed stabiliser of the economy, rather than a source of inflation. 2. But if governments want a bit of inflation, they can get it, can’t they? No. Understand that inflation is a non-linear system with two states, price stability and price instability. You can shift between these two states, but you cannot get a ‘little bit of inflation’ in a controlled fashion, or hit an arbitrary inflation target like 2 percent, 3 percent, or 5 percent. This is something that we have been arguing for years, and it is comforting that some great thinkers – like (the late) Paul Volker and William White – fully support our non-linear system thesis. You cannot get a ‘little bit of inflation’ in a controlled fashion. Any government can take its economy into the state of price instability if it so chooses. Witness Turkey and Argentina. But price stability is the much better state to be in. Given that developed economies have expended decades of blood, sweat, and tears to reach the state of price stability, we think that it would be a monumental policy error to embark on the road to price instability (Chart I-10). Chart I-10Inflation Is A Non-Linear System With Two States, Price Stability And Price Instability

The Absurdity Of Inflation Expectations

The Absurdity Of Inflation Expectations

3. But doesn’t rampant Argentina-type inflation bail out the heavily indebted? No, not necessarily. It will only bail you out if your debt is a one-off lump sum payment in the distant future. If your debt requires ongoing refinancing, then inflation will not bail you out, because the refinancing interest rate could rise in line with, or even faster than, the inflation rate. Therefore, those highly indebted governments, firms, and households that need to refinance their debts would not benefit from rampant inflation. 4. In which case, isn’t the solution to let inflation rip while keeping interest rates depressed – so-called ‘financial repression?’ No. While it is conceivable that a government could corner its government bond market and thereby repress it, it would be near-impossible to repress the much larger asset-classes of equities and real estate. Once these large and privately priced markets sniffed out the government’s nefarious plan, the required prospective nominal return would surge as a compensation for the higher inflation. The result being an almighty crash in stock and real estate markets. Given that the near $500 trillion combined worth of such markets dwarfs the $90 trillion global economy, the impact of such a crash would make this year’s pandemic feel like a waltz in the park. Fractal Trading System* This week’s recommended trade is short copper versus gold, given that the spectacular relative outperformance is showing fragility in both its 65-day and 130-day fractal structures. The profit target and symmetrical stop-loss is set at 10 percent. Chart I-11Copper Vs. Gold

Copper Vs. Gold

Copper Vs. Gold

In other trades, long RUB/CZK reached the end of its holding period with a marginal partial loss. The rolling 12-month win ratio now stands at 53 percent. When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 Europe and the US have deep and liquid markets in 5-year 5-year inflation swaps (or forwards), which price the expected 5-year inflation rate 5 years ahead. The current swap measures the annual inflation rate expected through 2026-31. The UK and the US also have deep and liquid markets in inflation-protected government bonds: UK index-linked gilts, and US Treasury Inflation Protected Securities (TIPS). The yield offered on such a security is real, which means in excess of inflation. The yield offered on a similar-maturity conventional bond is nominal. This means that the difference between the two yields equates to the market’s expectation for inflation over the maturity, known as the ‘breakeven inflation rate.’ Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

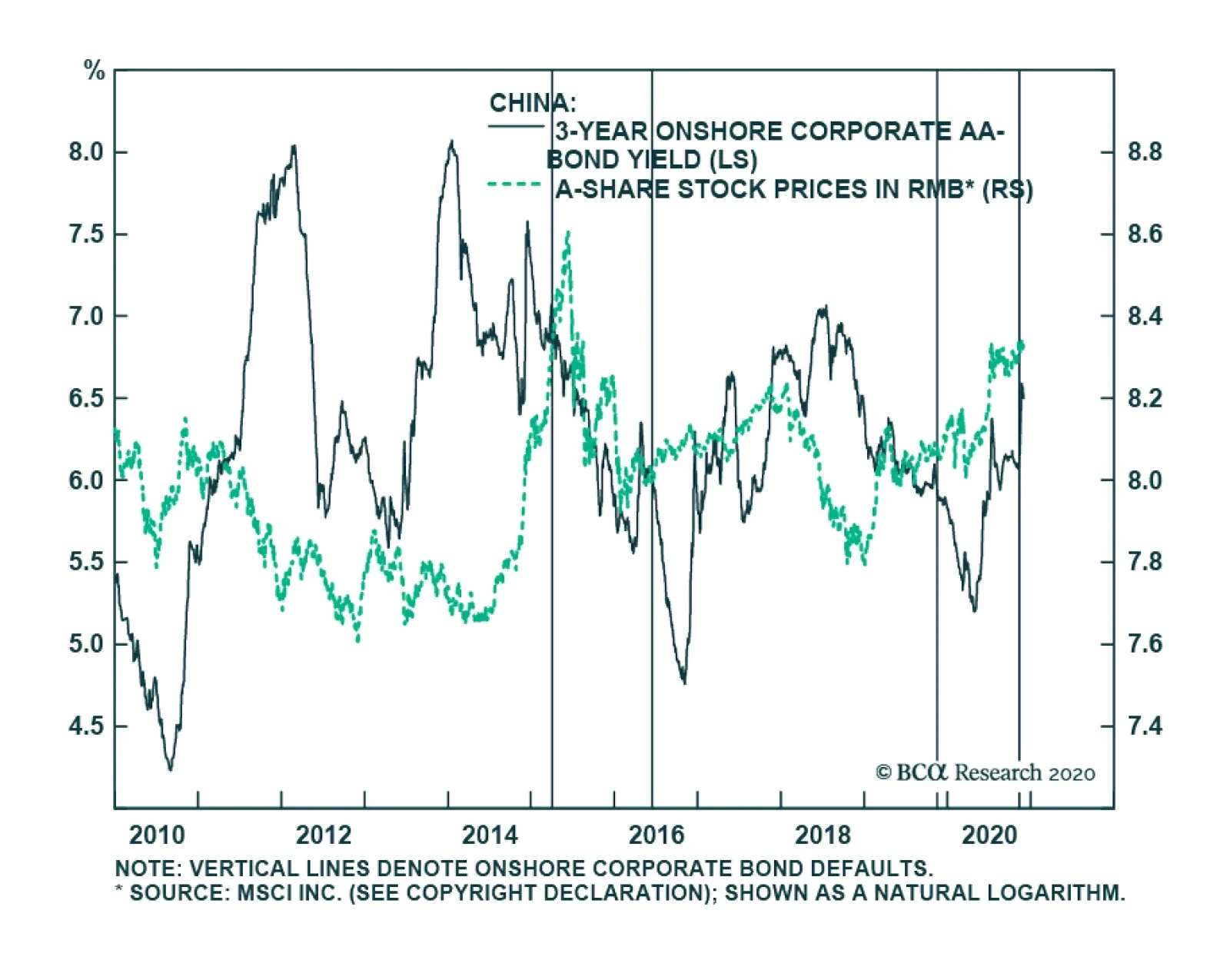

Although the onshore corporate bond market is under stress, BCA Research’s China Investment Strategy service concludes that it will not be the force that buckles Chinese equities. Recent bond payment defaults by several SOEs have led to a spike in onshore…