Fixed Income

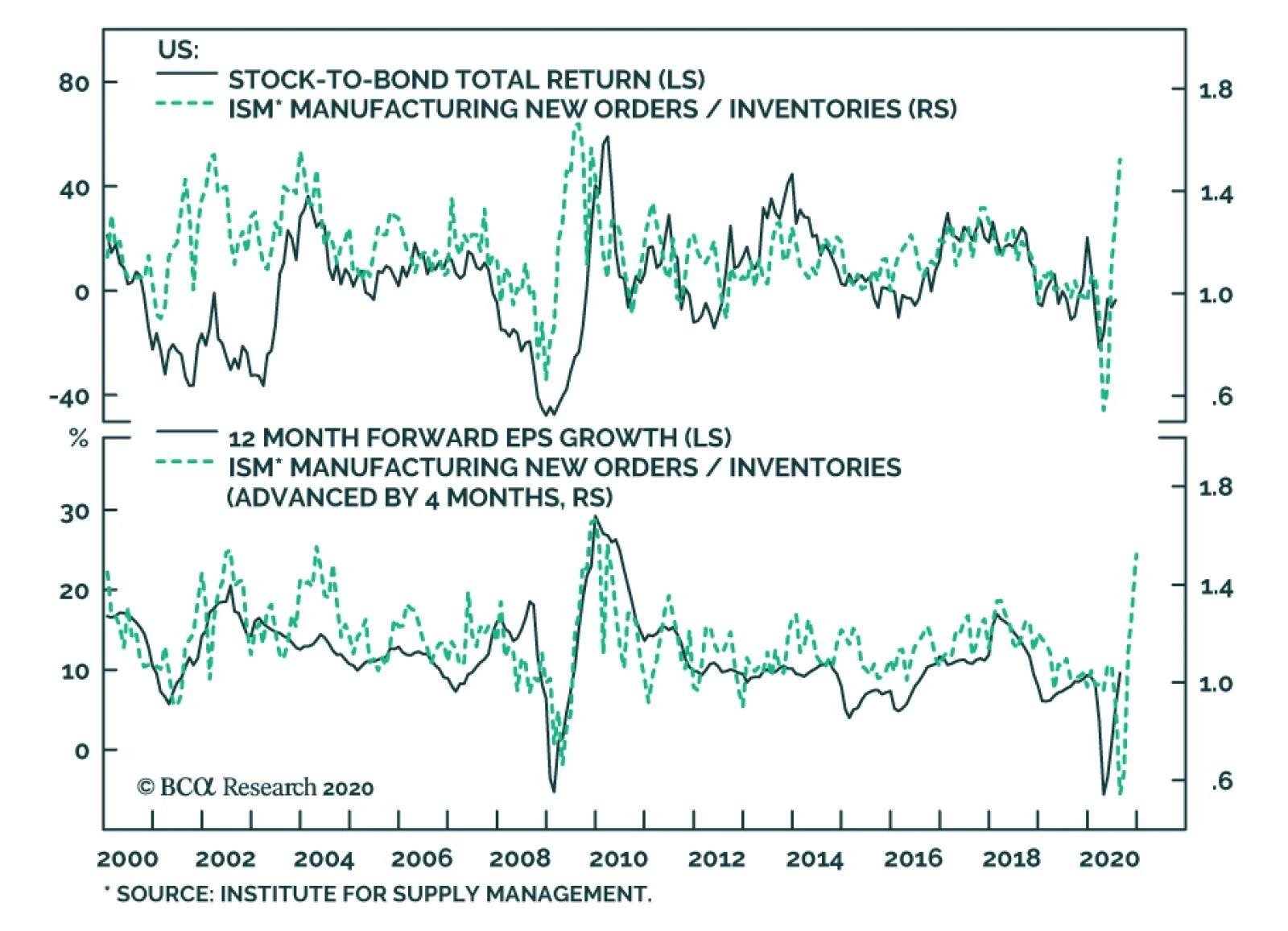

Highlights Achieving 2 percent inflation, whether as a point-target or as an average over time, will continue to be a mission impossible. As central banks continue to push the monetary policy pedal to the metal, it will underpin the valuation of equities and other risk-assets. So long as bond yields do not spike, stock market sell offs will be short-lived rather than an outright bear market. Within bonds, steer towards those where the monetary policy toolbox is not fully depleted, namely US T-bonds. Within currencies, steer towards those where the monetary policy toolbox is already depleted, namely the Swiss franc and the yen. Inflationary fiscal policy, by spiking bond yields, risks collapsing the valuation underpinning of $450 trillion of global risk-assets and catalysing a deflationary bear market. Fractal trade: Euro strength is vulnerable. Feature Chart of the WeekUltra-Low Bond Yields Do Not Create Consumer Price Inflation, They Create Asset Price Inflation

Ultra-Low Bond Yields Do Not Create Consumer Price Inflation, They Create Asset Price Inflation

Ultra-Low Bond Yields Do Not Create Consumer Price Inflation, They Create Asset Price Inflation

Five years ago, we published a Special Report, Mission Impossible: 2% Inflation. We predicted that 2 percent inflation would remain elusive. Or that in the rare economies that it did appear, it would be runaway, rather than a sedate 2 percent. Either way, the 2 percent inflation point-target that had become a quasi-religious commandment for the world’s central banks would be a ‘mission impossible’.1 Our August 2015 report was heterodox and provocative. Some people pushed back, arguing that the all-powerful central banks could pick and hit whatever inflation target they desired. Yet five years on, we have been vindicated. Last week, the Federal Reserve finally threw in the towel on the 2 percent inflation point-target (Chart I-2). Chart I-2"Forecasts For 2 Percent Inflation Were Never Realised On A Sustained Basis"

"Forecasts For 2 Percent Inflation Were Never Realised On A Sustained Basis"

"Forecasts For 2 Percent Inflation Were Never Realised On A Sustained Basis"

“Over the years, forecasts from FOMC participants and private-sector analysts routinely showed a return to 2 percent inflation, but these forecasts were never realised on a sustained basis… (hence) our new statement indicates that we will seek to achieve inflation that averages 2 percent over time…”2 We suspect that, just like the Fed, European central banks will soon move their goal posts. Nevertheless, today we are doubling down on our August 2015 prediction. Achieving 2 percent inflation, whether as a point-target or as an average over time, will continue to be a mission impossible (Chart I-3). Chart I-3Mission Impossible: 2 Percent Inflation

Mission Impossible: 2 Percent Inflation

Mission Impossible: 2 Percent Inflation

Price Stability Is A State, Not A Number The current school of central bankers have misunderstood price stability. They have defined it as an over-precise inflation rate: two point zero. Yet most people feel price stability imprecisely and intuitively. A recent IFO paper points out that households’ inflation perceptions are “more in line with the imperfect information view prevailing in social psychology than with the rational actor view assumed in mainstream economics.”3 The human brain cannot distinguish between very low rates of inflation or deflation, a range we just perceive as ‘price stability’. In Real-Feel Inflation: Quantitative Estimation of Inflation Perceptions, Michael Ashton confirms that “it would be challenging for a consumer to distinguish 1 percent inflation from 2 percent inflation – that fine of a gradation in perception would be extremely unusual to find.”4 The human brain cannot distinguish between very low rates of inflation or deflation. As the entire range of ultra-low inflation just feels like one state of price stability, it is impossible for central banks to fine-tune our inflation expectations within that range. Therefore, our behaviour in terms of wage demands and willingness to borrow also stays unchanged. And if our behaviour is unchanged, what is the transmission mechanism to 2 percent inflation – or for that matter, any arbitrarily chosen inflation rate? Hence, inflation targeting can ‘phase-shift’ an economy between the states of price instability and price stability. Most notably, its inception in the 1990s ultimately phase-shifted many advanced economies into the state of price stability (Chart I-4). But once in either state, inflation targeting cannot fine-tune inflation to a desired number such as 2 percent, 4 percent, or 10 percent. Chart I-4Inflation Targeting Phase-Shifted Advanced Economies Into Price Stability

Inflation Targeting Phase-Shifted Advanced Economies Into Price Stability

Inflation Targeting Phase-Shifted Advanced Economies Into Price Stability

A recent NBER paper Inflation Expectations As A Policy Tool? points out that in advanced economies, “the inattention of households and firms to inflation is likely a reflection of policy-makers’ success in stabilizing inflation around a low level for decades. This price stability has reduced the benefit to being informed about aggregate inflation, leading many to rely on readily available price signals.”5 The ultimate proof is that even market-based inflation expectations just track realised inflation. Central Banks Have Gone Backwards In his must-read What’s Wrong With The 2 Percent Inflation Target, the late and great Paul Volcker argued that price stability is “that state in which expected changes in the general price level do not effectively alter business or household decisions. It is ill-advised to define that state with a point target, such as 2 percent, as false precision can lead to dangerous policies.”6 The irony, and tragedy, is that both the Fed and the ECB have gone backwards. Their original definitions of price stability were more correct than their more recent iterations. False precision can lead to dangerous policies. At the Federal Reserve’s July 1996 policy meeting, Chairman Alan Greenspan argued that if the aim of inflation targeting was a truly stable price level, it entailed an inflation target of 0-1 percent. But one of the persons present was not so sure. The dissenter was a Fed governor called Janet L. Yellen. She countered that if inflation ended up at 0-1 percent, the zero-bound of interest rates would prevent “real interest rates becoming negative on the rare occasions when required to counter a recession”, an argument that Jay Powell repeated last week. “Expected inflation feeds directly into the general level of interest rates… so if inflation expectations fall below our 2 percent objective, interest rates would decline in tandem. In turn, we would have less scope to cut interest rates to boost employment during an economic downturn.” Meanwhile in Europe, the ECB’s original inflation target of below 2 percent was close to Greenspan’s proposal of 0-1 percent. But in 2003 the ECB changed its inflation target to its current “below but close to 2 percent.” The reason, according to Mario Draghi: “The founding fathers of the ECB thought about the rebalancing of the different members. To rebalance these disequilibria, since the countries do not have the exchange rate, they must readjust their prices. This readjustment is much harder if you have zero inflation than if you have 2 percent.” Hence, the Fed, ECB and other central banks are targeting inflation at an arbitrary 2 percent to always allow some leeway for negative real rates. The central bank argument can be summarised as: we desperately need you to expect 2 percent inflation. Because otherwise, we won’t be able to help you by cutting real interest rates in a downturn. Yet this argument is facile, as it takes no account of the true science of inflation expectation formation (Chart I-5 and Chart I-6). And it is dangerous, as it takes no account of the financial and economic risks of pushing the monetary policy pedal to the metal. Chart I-5Inflation Expectations Just Track Realised Inflation

Inflation Expectations Just Track Realised Inflation

Inflation Expectations Just Track Realised Inflation

Chart I-6Inflation Expectations Just Track Realised Inflation

Inflation Expectations Just Track Realised Inflation

Inflation Expectations Just Track Realised Inflation

Beware The Twists In The Inflation Story Now we come to a couple of twists in the story. When bond yields become ultra-low, their impact on consumer price inflation breaks down – because the economy is already in the state of price stability – but the impact on stock market inflation increases exponentially (Chart of the Week). We refer readers to previous reports in which we have detailed this dynamic.7 The good twist is that as central banks continue to push the monetary policy pedal to the metal, it will underpin the valuation of equities and other risk-assets. So long as bond yields do not spike, stock market sell offs will be short-lived rather than an outright bear market. Remarkably, this has held true even this year in the worst economic downturn since the Depression. The current school of central bankers have misunderstood price stability. Within bonds, steer towards those where the monetary policy toolbox is not fully depleted, namely US T-bonds (Chart I-7 and Chart I-8). Conversely, within currencies, steer towards those where the monetary policy toolbox is already depleted, namely the Swiss franc and the yen. Chart I-7Steer Towards Bonds Where Monetary Policy Is Not Fully Depleted...

Steer Towards Bonds Where Monetary Policy Is Not Fully Depleted...

Steer Towards Bonds Where Monetary Policy Is Not Fully Depleted...

Chart I-8...Namely US ##br##T-Bonds

...Namely US T-Bonds

...Namely US T-Bonds

Finally, given that any economy can ultimately phase-shift to price instability, when should we worry about inflation in advanced economies? Not yet. To expand the broad money supply, somebody must borrow and spend money. If policymakers really want to create rampant inflation, that somebody is the government. It must borrow and spend money at will, with the central bank creating the money. In other words, the central bank loses its independence and government spending goes vertical. So far, we are not remotely close to this situation because government spending has barely replaced the lost incomes and livelihoods of the pandemic. Indeed, things could get worse once the current income replacement schemes end. Yet, in theory at least, government spending could ultimately go vertical. This would lead to the final bad twist. As bond yields spiked in response, the entire valuation support of global risk-assets would collapse, catalysing a devastating bear market. Given that the $450 trillion worth of global risk-assets (including real estate) is five times the size of the $90 trillion global economy, we reach an important conclusion. The road to inflation, if ever taken, goes via deflation. Fractal Trading System* This week we note that the recent strength in EUR/USD is vulnerable to a countertrend pullback. However, as we are already exposed to this via the correlated position in long USD/PLN, there is no new trade. The rolling 1-year win ratio now stands at 59 percent. Chart I-9EUR/USD

EUR/USD

EUR/USD

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 Please see the European Investment Strategy Special Report ‘Mission Impossible: 2% Inflation’, dated August 20, 2015, available at eis.bcaresearch.com. 2 Please see New Economic Challenges and the Fed's Monetary Policy Review, August 27, 2020 available at https://www.federalreserve.gov/newsevents/speech/powell20200827a.htm 3 Please see Households’ Inflation Perceptions and Expectations: Survey Evidence from New Zealand, IFO Working Paper, February 2018 available at https://www.ifo.de/DocDL/wp-2018-255-hayo-neumeier-inflation-perceptions-expectations.pdf 4 Please see Real-Feel Inflation: Quantitative Estimation of Inflation Perceptions by Michael Ashton, National Association for Business Economics available at https://link.springer.com/content/pdf/10.1057/be.2011.35.pdf 5 Please see Inflation Expectations As A Policy Tool? NBER, May 28th, 2018 available at http://conference.nber.org/conf_papers/f117592.pdf 6 Please see https://www.bloomberg.com/opinion/articles/2018-10-24/what-s-wrong-with-the-2-percent-inflation-target 7 Please see the European Investment Strategy Weekly Report ‘Risk: The Great Misunderstanding Of Finance’, dated October 25, 2018, available at eis.bcaresearch.com. Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

While the market PMIs for August were slightly revised down relative to their flash estimates, the ISM manufacturing survey, which has more weight toward smaller businesses, rose vigorously from 54.2 to 56, handily beating expectations of 54.8. The…

Recommended Allocation

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Chart 1Only Internet Stocks Have Kept On Rising

Only Internet Stocks Have Kept On Rising

Only Internet Stocks Have Kept On Rising

It has been a very strange bull market. Although global equities are up 52% since their bottom on March 23rd, the rally has been limited largely to internet-related stocks. Excluding the three sectors (IT, Consumer Discretionary, and Communications) which house the internet names, equities have moved only sideways since May (Chart 1). Moreover, the rally comes amid sporadic serious new outbreaks of COVID-19 cases, most recently in Europe (Chart 2). Fears of the pandemic and much-reduced business activity in leisure-related industries have caused consumer confidence to diverge from the stock market in an unprecedented way (Chart 3). Chart 2New Outbreaks Of COVID-19 In Europe

New Outbreaks Of COVID-19 In Europe

New Outbreaks Of COVID-19 In Europe

Chart 3Why Are Stocks Rising When Consumers Are So Wary?

Why Are Stocks Rising When Consumers Are So Wary?

Why Are Stocks Rising When Consumers Are So Wary?

The only explanation for these phenomena is the unprecedented amount of monetary stimulus, which is causing excess liquidity to flow into risk assets. Since March, the balance-sheets of major central banks have increased by $7 trillion (Chart 4), and M2 money supply growth has soared (Chart 5). Chart 4Central Banks Have Grown Their Balance-Sheets...

Central Banks Have Grown Their Balance-Sheets...

Central Banks Have Grown Their Balance-Sheets...

Chart 5...Leading To A Big Rise in Money Growth

...Leading To A Big Rise in Money Growth

...Leading To A Big Rise in Money Growth

Moreover, the Fed’s new strategic framework announced in late August represents a commitment to keep monetary policy loose even when the economy begins to overheat. The Fed will (1) target 2% inflation on average over time which means that, after a period of low inflation, it will “aim to achieve inflation moderately above 2 percent for some time”; and (2) treat its employment mandate as asymmetrical, so that when employment is below potential the Fed will be accommodative, but that a rise in employment above its “maximum level” will not necessarily trigger tightening. Historically the Fed has raised rates when unemployment approached its natural rate (Chart 6). The new policy implies it will no longer do so. The aim of the policy is to raise inflation expectations which have become unanchored, with headline PCE inflation above the Fed’s 2% target for only 14 out of 102 months since the target was introduced in February 2012 (Chart 6, panel 3). Chart 6The Fed's Behavior Will Be Different In Future

The Fed's Behavior Will Be Different In Future

The Fed's Behavior Will Be Different In Future

Chart 7More Permanent Job Losses To Come

More Permanent Job Losses To Come

More Permanent Job Losses To Come

This commitment to easier monetary policy for longer will certainly help risk assets. But will it be enough? The global economic environment remains weak. Permanent job losses continue to increase, as workers initially put on furlough or dismissed temporarily, are fired (Chart 7). A second wave of COVID-19 cases in the Northern Hemisphere winter would worsen the situation. While central banks everywhere remain committed to aggressive policy, fiscal policy decision-makers are getting cold feet, with the UK’s wage-replacement scheme due to end in October, and government support in the US set to decline absent a big new fiscal package agreed by Congress (Chart 8). Credit risks are beginning to emerge, with bankruptcies surging (Chart 9), and mortgage delinquencies starting to rise (Chart 10). As a result, banks are becoming significantly more reluctant to lend (Chart 11). Chart 8Fiscal Support Is Starting To Slide

Fiscal Support Is Starting To Slide

Fiscal Support Is Starting To Slide

Chart 9Bankruptcies Are Surging…

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Chart 10...Along With Mortgage Delinquencies

...Along With Mortgage Delinquencies

...Along With Mortgage Delinquencies

Chart 11Banks Turning Increasingly Cautious

Banks Turning Increasingly Cautious

Banks Turning Increasingly Cautious

To those concerns, we should add political risk ahead of the US presidential election. President Trump is probably not as far behind as the 7-percentage point gap in opinion polls suggests: After the Republican National Convention, online betting sites give him a 46% probability of being reelected (Chart 12). Over the next two months, he could be aggressive in foreign policy, particularly towards China. A disputed election is not unlikely. Investors might be wise to hedge against that possibility: BCA Research’s Geopolitical service recommends buying December VIX futures, which are still cheaply priced, and selling January VIX futures (Chart 13). 1 Chart 12Trump Could Still Pull It Off

Trump Could Still Pull It Off

Trump Could Still Pull It Off

Chart 13Hedge Against A Disputed Election Result

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Given the power of monetary stimulus, we are reluctant to bet against equities – not least since the yield on fixed-incomes assets is so low. Nonetheless, we see the risk of a sharp correction over the coming six months, driven by a second pandemic wave, a renewed downturn in the global economy, or political events. We continue to recommend, therefore, only a neutral position on global equities. We would hold a large overweight in cash, to keep powder dry for when a better buying opportunity for risk assets arises. But a warning: The long-run return from all asset classes will be poor. The global bond index is unlikely to produce a nominal return much above zero over the coming decade. While equities look more attractive, our valuation indicator points to a nominal annual return of only around 3% (Chart 14). For the US, valuation suggests a return of zero. Investors will need to become more realistic about their return assumptions. The 7% annual return still assumed by the average US pension fund might have made sense when the yield on BBB-rated corporate bonds was 8%, but it no longer does when it has fallen to 2.3% (Chart 15). Chart 14Long-Term Equity Returns Will Be Poor

Long-Term Equity Returns Will Be Poor

Long-Term Equity Returns Will Be Poor

Chart 15Investors' Return Assumptions Are Unrealistic

Investors' Return Assumptions Are Unrealistic

Investors' Return Assumptions Are Unrealistic

Chart 16Value Sectors' Profits Have Been Terrible

Value Sectors' Profits Have Been Terrible

Value Sectors' Profits Have Been Terrible

Equities: The most vigorous debate among BCA Research strategists currently is over whether growth stocks will continue to outperform, or whether value will take over leadership. The Global Asset Allocation service is on the side of growth. The poor performance of value stocks (concentrated in Financials, Energy, and Materials) is explained by the structural decline in their profits for the past 12 years (Chart 16). With the yield curve unlikely to steepen and non-performing loans set to rise, we do not see Financials’ earnings recovering. China’s economic shifts represent a long-term headwind for Materials. Internet stocks are expensively valued, but we do not see them underperforming until (1) their earnings’ growth slows sharply, (2) regulation on them is significantly tightened, or (3) long-term bond yields rise, lowering the NPV of their future earnings. This view drives our Overweight on US equities versus Europe and Japan. US stocks have continued to outperform even in the risk-on rally since March (Chart 17). We are a little more enthusiastic (with a Neutral recommendation) about Emerging Market stocks, which are very cheaply valued (Chart 18). Chart 17US Stocks Have Outperformed Even In A Risk-On Market

US Stocks Have Outperformed Even In A Risk-On Market

US Stocks Have Outperformed Even In A Risk-On Market

Chart 18EM Stocks Are Cheap

EM Stocks Are Cheap

EM Stocks Are Cheap

Chart 19Short USD Is Now A Consensus Trade

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Monthly Portfolio Update: Can Monetary Policy Alone Propel The Market?

Currencies: The US dollar has depreciated by 10% since mid-March. Over the next 12 months, the trend for the USD is likely to continue to be down. The new Fed policy emphasizes that real rates will stay low, and US inflation will probably be higher than in other developed economies. Nonetheless, short-USD/long-euro positions have become consensus (Chart 19) and, given the safe-haven nature of the dollar, a period of risk-off could push the dollar back up temporarily. Chart 20IG Spreads Are No Longer Attractive

Investment Grade Breakeven Spreads IG Spreads Are No Longer Attractive

Investment Grade Breakeven Spreads IG Spreads Are No Longer Attractive

Fixed Income: We don’t expect to see a sustained rise in nominal US Treasury yields, despite the Fed’s new monetary policy framework. The Fed has an implicit yield curve control policy, and would react if yields showed signs of rising significantly. TIPS breakevens should eventually rise further to reflect the likelihood of higher inflation in the longer term, though the recent sharp rise in inflation (core CPI rose by 0.6% month-on-month in July, the largest increase since 1991) will likely subside and so the upside for breakeven yields might be limited over the next six months. We are becoming a little more cautious on credit. Investment-grade spreads are now close to historic lows and so returns are likely to be limited (Chart 20). We lower our recommendation to Neutral. Ba-rated bonds still offer attractive yields and are supported by Fed purchases. But we would not go further down the credit curve, and so stay Neutral on high yield. This by definition means that we must also be Neutral within fixed income on government bonds, which is compatible with our view that rates will not rise much. Note, though, that we remain Underweight the fixed-income asset class overall, but no longer have a preference for spread product within it. One exception is EM dollar-denominated debt, both sovereign and corporate, which offers spreads that are attractive in a world of low returns from fixed income. Chart 21Crude Prices Can Rise Further As Demand Recovers

Crude Prices Can Rise Further As Demand Recovers

Crude Prices Can Rise Further As Demand Recovers

Commodities: Industrial metals prices have further to run up, as China continues its credit stimulus, which should lead to a rise in infrastructure investment and increased imports of commodities. The outlook for crude oil will be dominated by the demand side: OPEC forecasts demand destruction this year of 9 million barrels per day (compared to consensus expectations of 8 million) and so will be cautious about loosening its supply constraints. Demand should be boosted by increased driving, as people avoid using public transport for commuting and airlines for vacations. Based on a robust demand forecast (Chart 21), BCA Research’s energy strategists see Brent crude stable at around current levels through to the end of 2020 but averaging $65 a barrel next year. Garry Evans, Senior Vice President Global Asset Allocation garry@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Special Report, “What Is The Risk Of A Contested US Election?” dated July 27, 2020. GAA Asset Allocation

Highlights Fed Policy Changes: The official shift to an average inflation targeting regime represents a massive structural break relative to how the Fed conducted monetary policy in the past. The main takeaway for investors should be that inflation expectations will carry more weight than ever in the Fed’s thinking, with far less emphasis on estimated measures like the output gap. Investment Implications: The Fed’s new policy framework supports our current US fixed income recommendations: a neutral duration stance; overweighting TIPS versus nominal US Treasuries; positioning for real yield curve steepeners; and overweighting US spread product most directly supported by the Fed’s balance sheet (i.e. investment grade corporates and Ba-rated high-yield). Feature The pandemic forced the Federal Reserve to move its annual Jackson Hole Economic Policy Symposium online this year. That change deprived policymakers of a late-August vacation in the mountains of Wyoming, but offered the public a rare glimpse at the full proceedings live on YouTube.1 Federal Reserve Chairman Jerome Powell took advantage of that larger audience to announce significant changes to the Fed’s Statement on Longer-Run Goals and Monetary Policy Strategy. Though many of the basic elements of the new strategy were well telegraphed in advance, the adjustments are hugely significant and will shape the conduct of US – and, potentially, global - monetary policy for years to come. This Special Report presents the most important takeaways – and fixed income investment implications - from the Fed’s new approach to setting monetary policy. Say Hello To Average Inflation Targeting The most significant change has to do with how the Fed defines its price stability mandate. In its old Statement, the Fed defined its 2% inflation target as “symmetrical”, meaning that the Fed would be equally concerned if inflation were running persistently above or below the target. In the Fed’s words, communicating this symmetry was enough to “keep longer-term inflation expectations firmly anchored.” The Fed now believes that a more aggressive approach is required to keep inflation expectations anchored. The new Statement reads: In order to anchor longer-term inflation expectations at [2 percent], the Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.2 In other words, the Fed’s 2% inflation target is no longer purely forward-looking. It is now dependent on the history of realized US inflation, and thus is now much more like a price level target than an inflation target. We will know that the Fed has seen enough inflation overshooting when long-term expectations are anchored at levels consistent with its 2% inflation target. For example, Chart 1 shows how the headline PCE price index would have evolved since the end of 2007 had it averaged 2% growth per year, exactly equal to the Fed’s target. Starting from today, PCE inflation would need to average 3% for the next seven years, or 2.5% for the next fourteen years, for the index to converge with this target. In other words, if the Fed seeks to achieve average 2% inflation since 2007, we are in for a prolonged period of overshooting the old 2% target. Chart 1An Illustration Of Average Inflation Targeting

An Illustration Of Average Inflation Targeting

An Illustration Of Average Inflation Targeting

Notice that we had to make several assumptions in our above example. First, we had to assume that the Fed will seek to achieve average 2% inflation since the end of 2007. The Fed could just as easily choose a different start date for calculating the 2% average. We also assumed that the year-over-year PCE inflation rate never breaks above 3% during the overshooting phase. As of now, we have no sense of whether the Fed would act to make sure that inflation only overshoots 2% by a small amount (say, between 0.5 and 1 percentage point) or whether it would tolerate a larger overshoot. A larger overshoot would potentially be more de-stabilizing, but it would allow the Fed to catch up to its price level target more quickly. We will probably get some more information about these missing details when the Fed translates its new framework into more explicit forward rate guidance (see section titled "Are There Any Additional Changes Coming?" below), but the Fed will still want to retain some flexibility. That is, we shouldn’t expect the Fed to tie its hands with a strict policy rule. This means that the question of how much inflation would prompt any future Fed tightening could linger for some time. Faced with this ambiguity, investors are advised to focus more keenly than ever on inflation expectations (Chart 2). Note that in the above excerpt from the revised Statement on Longer-Run Goals and Monetary Policy Strategy, the explicit goal of average inflation targeting is to “anchor long-term inflation expectations at [2 percent]”. This means that we will know that the Fed has seen enough inflation overshooting when long-term expectations are anchored at levels consistent with its 2% inflation target. We view this “well anchored” level as a range between 2.3% and 2.5% for long-dated TIPS breakeven inflation rates (top two panels). When TIPS breakevens reach those levels, we should expect the Fed to shift toward a more restrictive policy stance. Chart 2The Fed Wants Higher Inflation Expectations

The Fed Wants Higher Inflation Expectations

The Fed Wants Higher Inflation Expectations

How long will it take for TIPS breakevens to reach our target range? We expect it will take quite some time because Fed communications alone cannot drive long-term TIPS breakevens back to target. Rather, inflation expectations tend to follow trends in the actual inflation data, so expectations will only return to well-anchored levels once inflation has risen significantly. Further, long-dated inflation expectations tend to adapt slowly to changes in the actual inflation data. Notice in Chart 3 that the 5-year/5-year forward CPI swap rate correlates much more strongly with the 8-year rate of change in CPI inflation than it does with the 1-year rate of change. This suggests that, most likely, 12-month inflation will have to run above 2% for some time before long-term TIPS breakevens sustainably return to our target range. One way to understand the link between actual inflation and inflation expectations is to look at the distribution of individual inflation forecasts. Chart 4 shows the distribution of 10-year headline CPI inflation forecasts from the Survey of Professional Forecasters from 2004 – a year when inflation expectations were well anchored around 2% – and from August 2020. Notice that a similar proportion of respondents at both points in time expect inflation to be near the Fed’s target, in a range of 2% to 2.5%. The difference is that, in 2004, a large minority of respondents anticipated a significant overshoot of the inflation target. Today, hardly anyone anticipates a significant overshoot, and many expect a significant undershoot. Chart 3Inflation Expectations Adapt Slowly To The Actual Data

Inflation Expectations Adapt Slowly To The Actual Data

Inflation Expectations Adapt Slowly To The Actual Data

Chart 4Distribution Of Inflation Forecasts ##br##(2004 & Today)

A New Dawn For US Monetary Policy

A New Dawn For US Monetary Policy

Since market prices can be thought of as a weighted average of the entire distribution of inflation forecasts, it follows that to drive TIPS breakevens higher we need to see investors shift their forecasts from the left tail of the distribution to the right tail. This will only happen if actual inflation rises, and probably only if it stays durably above 2% for a prolonged period. Chart 5shows that the percentage of respondents that expect inflation to average above 3% for the next ten years tends to follow both the long-run inflation rate and the median inflation forecast. Chart 5Few Expect Inflation To Be Above 3%

Few Expect Inflation To Be Above 3%

Few Expect Inflation To Be Above 3%

Bottom Line: The official shift to an average inflation targeting regime represents a massive structural break relative to how the Fed conducted monetary policy in the past. The main takeaway for investors should be that inflation expectations carry more weight than ever in the Fed’s thinking. In particular, we should expect the Fed to move to a more restrictive policy stance only when long-maturity TIPS breakeven inflation rates return to a well-anchored range of 2.3% to 2.5%. Some Key Questions Following The Fed’s Big Shift Does The Phillips Curve Still Matter? The second big change that the Fed made to its official Statement on Longer-Run Goals and Monetary Policy Strategy is in how it views the unemployment rate relative to its “natural” level. Specifically, the change has to do with making estimates of the natural rate of unemployment (NAIRU) less important in the Fed’s reaction function. In its old Statement, the Fed talked about minimizing “deviations of employment from the Committee’s assessments of its maximum level”. The revised Statement talks about mitigating “shortfalls of employment from the Committee’s assessment of its maximum level.” This one word change says a lot about the Fed’s faith in the Phillips curve. In the past, the Fed viewed an unemployment rate below its estimate of NAIRU as a signal that inflation was poised to accelerate. This often led to premature tightening, and over time, a pattern of missing the inflation target to the downside. Now, the Fed is explicitly saying that it only cares about shortfalls of employment from its estimated maximum level. If the labor market appears overheated, the Fed will not take this as a sign that inflation is about to accelerate. Rather, it will wait for the evidence to show up in the actual inflation data. The percentage of respondents that expect inflation to average above 3% for the next ten years tends to follow both the long run inflation rate and the median inflation forecast. This change sends a very clear signal that the Fed will put much less emphasis on expected “Phillips curve effects” in the future than it has in the past. In addition to long-term implications, this change will likely also impact the type of forward rate guidance the Fed provides this year. What’s Missing? It is also interesting to touch on the things that Powell did not mention in his Jackson Hole speech. First, as noted above, Powell provided few details on the length of time over which the Fed will seek to hit average 2% inflation and did not specify any upper limit to the amount of inflation the Fed would tolerate during the overshooting phase. Perhaps more importantly, Powell also did not say much about how the Fed will seek to drive inflation higher, and whether there are additional tools at his disposal that have not yet been rolled out. We think there is good reason for this. In effect, we think the Fed is more or less tapped out in terms of the amount of additional monetary easing it can provide. Negative interest rates have already been ruled out. A Yield Curve Control policy of capping intermediate-maturity bond yields has been discussed, but this policy doesn’t accomplish much beyond what the Fed is already doing with its forward rate guidance. For example, a policy of capping the 2-year Treasury yield at the current level of 0.13% has essentially the same impact on bond prices as convincing the market that the fed funds rate will stay in a range between 0% and 0.25% for the next two years or more. The notion that the Fed is “out of bullets” was hammered home during the final Jackson Hole panel on Friday. The speakers for the panel titled “Post-Pandemic Monetary Policy and the Effective Lower Bound” shifted much of the onus for boosting growth, with policy interest rates at the effective lower bound, toward fiscal policymakers. Given the limitations on the amount of additional easing that the Fed can deliver, the potent impact of the changes announced last week will not really be felt until the economic recovery is further underway. Only once inflation starts to rise will we get a test of the Fed’s resolve to stay on the sidelines. Now that the changes have been enshrined in an official Fed document, we have no doubt that they will follow through. What About The Role Of QE? Chart 6The Future Of QE: Go Big & Go Fast

The Future Of QE: Go Big & Go Fast

The Future Of QE: Go Big & Go Fast

Not every speaker at Jackson Hole, however, felt that central banks had run out of policy options. Bank of England (BoE) Governor Andrew Bailey gave a speech on Day Two of the conference that focused on the use of central bank balance sheets as a more regular part of policymakers’ toolkits over the next decade with policy rates at the effective lower bound. Bailey noted that the use of quantitative easing (QE) in the future would be less about signaling future central bank intentions on interest rates, or forcing changes to the composition of assets held by the private sector, and would be more about “going big and going fast” to calm financial markets during periods of instability.3 Some past examples of such use of QE include the 2008 Global Financial Crisis, the 2011/12 European Debt Crisis and the 2016 UK Brexit shock (Chart 6). In Bailey’s view, QE will now have to be “state contingent”, based on the nature of the financial market shock and where liquidity (cash) needs are greatest at that time. In 2008, it was the banking system that needed liquidity, so central banks expanded their balance sheets in ways that got cash directly to the banks – like repos and government bond purchases. In 2020, the demand for liquidity from the COVID-19 shock came more from non-bank entities, like investment funds or the corporate sector itself. Therefore, central bank balance sheets had to be used to support loans to the private sector or even buying private assets like corporate debt, on top of the usual QE buying of sovereign debt to help drive down risk-free bond yields. What does that mean for the new policy regime of the Fed? It means that the type of market intervention we saw earlier this year – with the Fed announcing a variety of measures to support liquidity like corporate bond purchases when markets were not functioning – will become more commonplace during periods of severe market stress. This is because there cannot be any “emergency” Fed rate cuts to calm markets if the Fed is keeping rates at very low levels to try and make up for past undershoots of its inflation target. Chart 7The Fed Has Room To Do More QE In The Future

The Fed Has Room To Do More QE In The Future

The Fed Has Room To Do More QE In The Future

This also means that the balance sheets of the Fed, and other major global central banks, will likely continue to get larger over time. Tapering of balance sheets, as the Fed engineered during 2014-19, will become very rare events before inflation expectations are stabilized at policymaker targets. That does raise issues of capacity constraints for QE programs, as Bailey mentioned in his speech, where the central bank footprint in financial markets becomes so large as to impair market functionality. That is the case today where the Bank of Japan now owns nearly 50% of all outstanding Japanese government bonds (JGB) and the day-to-day liquidity in the JGB market is extremely challenging for market participants that need to buy and trade JGBs, like Japanese banks and investment funds. Bailey noted that there was still ample capacity for the BoE to ramp up its buying of UK Gilts (and even UK corporate debt) before the sheer size of its presence became a BoJ-like problem for the UK bond market (Chart 7). The same can be argued in the US, where the Fed only owns a little over 20% of outstanding US Treasuries – the supply of which is growing rapidly thanks to large US budget deficits. Are There Any Additional Changes Coming? As we outlined in a recent US Bond Strategy Webcast, after revising the Statement on Longer-Run Goals and Monetary Policy Strategy, the Fed’s next step will be to provide more explicit guidance about the economic conditions that will have to be in place before it considers lifting the fed funds rate.4 We speculate that this next announcement will occur before the end of the year, possibly at this month’s FOMC meeting, and that the guidance will be similar to the Evans Rule employed in 2012. The Evans Rule was a promise that the Fed would not lift rates at least until the unemployment rate was below 6.5% or inflation was above 2.5%. For the 2020 version of the Evans Rule, policymakers had been debating whether to specify both an unemployment target and an inflation target, as was done in 2012, or whether to specify only an inflation target. With the Fed’s new Statement putting much less emphasis on Phillips curve effects and estimates of NAIRU, it now appears much more likely that the 2020 version of the Evans Rule will have only an inflation trigger, or perhaps an inflation trigger and an inflation expectations trigger. Bottom Line: There are still many lingering unanswered questions about the new Fed strategy, but what we do know is that the Fed will focus more on inflation, rather than forecasts of inflation, when making future interest rate decisions. The Fed will also likely use its balance sheet more as a market stability tool during times of crisis. Investment Implications Chart 8Financial Conditions

Financial Conditions

Financial Conditions

The first implication of the Fed’s big shift has to do with the long-run outlook for risk asset prices (corporate bonds, equities and other fixed income spread product). With the Fed committing to give the economic recovery more runway before choking it off, risk asset valuations have been provided with a massive tailwind. In fact, the longer it takes for inflation to move up, the longer the Fed will stay on hold and the more expensive risk asset valuations will become. It is even possible that, if inflation remains subdued for a few more years, risk asset valuations will become so stretched that the Fed might have to exercise its financial stability “out clause”. That is, if the Fed viewed a growing asset bubble as a threat to the economic recovery and/or financial system, it could abandon its inflation target and lift interest rates to deflate that bubble. This out clause is specifically enshrined in the Fed’s Statement on Longer-Run Goals and Monetary Policy Strategy: Moreover, sustainably achieving maximum employment and price stability depends on a stable financial system. Therefore, the Committee’s policy decisions reflect its longer-run goals, its medium-term outlook, and its assessments of the balance of risks, including risks to the financial system that could impede the attainment of the Committee’s goals. We should stress that US financial asset valuations are currently nowhere near expensive enough to prompt this sort of move (Chart 8). However, that picture could change after a few more years of low inflation and zero interest rates. We have been saying since March 2019 that the two most important indicators to watch for gauging the eventual pace of Fed tightening are inflation expectations and financial conditions.5 Last week’s announcement serves to reinforce that view. The Fed could abandon its inflation target and lift interest rates to combat a growing asset bubble. A second investment implication of the Fed’s announcement is that TIPS will continue to outperform nominal US Treasuries until there is an eventual re-anchoring of long-run TIPS breakeven inflation rates in a range between 2.3% and 2.5%. As noted above, this structural investment position could take some time to pan out, and we may even get an opportunity to tactically position for periods of TIPS underperformance if breakevens start to look too high compared to the actual inflation data.6 For now, our models suggest that TIPS breakevens are fairly valued relative to the actual inflation data, and we recommend staying overweight TIPS versus nominal Treasuries as a core allocation in fixed income portfolios. We would also advise investors to enter flatteners along the inflation protection curve (TIPS breakevens or CPI swaps). This recommendation flows directly from the Fed’s announcement. If the Fed is eventually successful at achieving a temporary overshoot of its 2% inflation target, then the cost of short-maturity inflation protection should rise above the cost of long-maturity inflation protection. That is, the inflation protection curve should invert (Chart 9). This would be a stark dislocation compared to the past, but it is a logical one if the Fed is to be attacking its inflation target from above instead of from below. As for nominal Treasury yields, our baseline view is that yields will be flat-to-higher over the next 12 months, with the amount of upside dictated by the pace of economic recovery. The Fed’s extraordinarily dovish monetary policy will keep some downward pressure on nominal yields, but expectations of Fed tightening will eventually infiltrate the long end of the curve. Given that the Fed’s grip is much firmer at the short end of the curve than at the long end, we prefer to play the nominal Treasury curve through yield curve steepeners rather than through outright duration bets (Chart 10). Chart 9Position For Inflation Curve Inversion

Position For Inflation Curve Inversion

Position For Inflation Curve Inversion

Chart 10Enter Nominal Curve Steepeners

Enter Nominal Curve Steepeners

Enter Nominal Curve Steepeners

Finally, the level of real yields is perhaps the trickiest to get right in the current environment. The Fed’s dovish policies are clearly meant to push real yields down, but now that those policies have been announced, it may signal that we are near the trough. In fact, real yields actually rose somewhat on Thursday after the Fed’s announcement. As with nominal yields, we prefer to play the real Treasury (TIPS) curve via steepeners (Chart 11). Whether or not the Fed is able to apply further downward pressure on real yields, as long as its policies are viewed as reflationary and the economic recovery is maintained, then the real yield curve has ample room to steepen. Chart 11Enter Real Curve Steepeners

Enter Real Curve Steepeners

Enter Real Curve Steepeners

Bottom Line: The Fed’s new policy framework supports our current US fixed income recommendations: a neutral duration stance; overweighting TIPS versus nominal US Treasuries; positioning for real yield curve (TIPS) steepeners; and overweighting US spread product most directly supported by the Fed’s balance sheet (i.e. investment grade corporates and Ba-rated high-yield). Ryan Swift US Bond Strategist rswift@bcaresearch.com Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 https://www.youtube.com/user/KansasCityFed 2 https://www.federalreserve.gov/monetarypolicy/guide-to-changes-in-statement-on-longer-run-goals-monetary-policy-strategy.htm 3 The full text of BoE Governor Bailey’s speech can be found here: https://www.bankofengland.co.uk/speech/2020/andrew-bailey-federal-reserve-bank-of-kansas-citys-economic-policy-symposium-2020 4 https://www.bcaresearch.com/webcasts/detail/338 5 Please see US Bond Strategy Weekly Report, “The New Battleground For Monetary Policy”, dated March 26, 2019, available at usbs.bcaresearch.com 6 This possibility is discussed in US Bond Strategy Weekly Report, “Positioning For Reflation And Avoiding Deflation”, dated August 11, 2020, available at usbs.bcaresearch.com

Highlights A weak dollar and low bond yields have pushed up the S&P 500 more than anticipated. Cyclical forces favor loftier stock prices in 12 months. Froth creates short-term vulnerabilities that higher yields could catalyze. The lack of yield curve control along with an improving economic outlook and a decline in deflationary risks indicate that Treasury yields will move toward 1% in the coming months. Long-term investors should begin to add small-cap stocks to their core US holdings. Feature The S&P 500 recent all-time high flies in the face of a long list of tactical indicators that flag an elevated risk of correction. The strength of the US equity market is a testament to the power of policy stimulus, the perceived invincibility of tech titans and the hopes that the powerful economic recovery will continue. Although equities will climb in the coming year, a move up in yields should transfer the leadership from tech and growth stocks to value and traditional cyclicals. While these shifts usually do not spell the end of bull runs, often they generate periods of elevated volatility, especially when the displaced leaders account for 40% of market capitalization. Small-cap stocks look increasingly attractive. A Post Mortem We have been cyclically bullish since late March,1 but on June 25th we warned that the S&P 500 would churn between 2800 and 3200 for the rest of the summer.2 This view did not materialize for several reasons. We underestimated the impact of a weak dollar, which has given a second life to the equity bull market. When expressed in euros, the S&P 500 has been flat since June 5 (Chart I-1). Relative to gold, the S&P 500 is down by 9% since June 8, which further highlights how equities have been supported by a weak US currency and a plentiful money supply. Meanwhile, the S&P 500 has outperformed the EURO STOXX 50 by 7.8% since June 5; however, when we factor in the effect of the strong euro, US equities have steadily underperformed the Eurozone benchmark since early May (Chart I-1, bottom panel). Low bond yields have also buttressed US equities. Near-zero interest rates have allowed the valuation of growth stocks to hit extraordinary levels. The NASDAQ trades at 32-times 2020 earnings and 27-times 2021 EPS. The S&P tech is valued at 29-times 2020 EPS and 25-times next year’s profits. In the most extreme cases, the five tech stocks that have accounted for 31.7% of market gains since March 23 (Apple, Amazon, Microsoft, Alphabet and Facebook) trade on average at 40-times 2020 EPS and 32-times 2021 earnings. Low bond yields have also buttressed US equities. Importantly, COVID-19 has had a positive influence on these same tech stocks. According to our European Investment Strategy colleagues, while spending on restaurant, entertainment and retail collapsed during the pandemic, outlays surged on Amazon, Apple products, Netflix subscriptions, etc.3 At the apex of the crisis, online retail sales expanded by 26.3% annually in the US, while bricks-and-mortar sales contracted by an unprecedented -17.7%. Meanwhile, global shipments of personal computers and servers are expanding by 11.2% and 21.5% annually, respectively (Chart I-2, top panel). Therefore, the largest sector of the S&P 500 is outperforming relative to the rest of the market (Chat I-2, bottom panel). As long as investors continue to expect COVID-19 to affect consumer behavior, they will pay a premium for tech stocks that benefit from the pandemic. Chart I-1The Weak Dollar Is Fueling The Recent Rally

The Weak Dollar Is Fueling The Recent Rally

The Weak Dollar Is Fueling The Recent Rally

Chart I-2Earnings Have Supported Tech Stocks

Earnings Have Supported Tech Stocks

Earnings Have Supported Tech Stocks

Can Stocks Remain Unscathed? The outlook for stocks is positive, but near-term risks have not dissipated because short-term market conditions remain frothy. Watch for higher bond yields as the force to concretize the tactical risks. The following cyclical forces continue to act as crucial tailwinds for equities: The equity risk premium (ERP) remains low. Computations of ERP must factor in the expected expansion of earnings. To incorporate this alteration, we assume that long-term cash flows will grow in line with potential nominal GDP growth. However, we must also consider the absence of stability of the ERP’s mean. After this adjustment, the ERP is still consistent with significant additional gains for the S&P 500 (Chart I-3). Monetary policy is extraordinarily accommodative. Even when we account for the S&P 500’s elevated multiples, the exceptional jump in the BCA Monetary Indicator is large enough to push up equity prices (Chart I-4). Moreover, the strength of US housing activity indicators confirms that the Federal Reserve has pulled the right levers to boost domestic economic activity. For example, the NAHB Housing Market Index has reached a 22-year record, building permits in July grew at their fastest monthly rate in 30 years, and the Mortgage Applications Index for purchases rocketed to a 11-year high in August. Chart I-3A Low ERP Underpins Equities...

A Low ERP Underpins Equities...

A Low ERP Underpins Equities...

Chart I-4...So Does Monetary Policy

...So Does Monetary Policy

...So Does Monetary Policy

The US economy continues to heal. For stocks to climb further on a cyclical basis, the market will need more than five tech giants leading the charge. Hence, earnings expectations for the rest of the market must also mount. Practically, the economy must recover its output loss and the pandemic must ebb. For now, the four-week moving average of initial unemployment claims is drifting lower, and the ISM New Orders-to-Inventories spread is consistent with a faster and more solid business cycle upswing. The ERP is still consistent with significant additional gains for the S&P 500. The global industrial sector outlook is brightening. Manufacturing and trade disproportionately contribute to fluctuations in global economic activity, therefore, they exert an outsized influence on the earnings of non-tech multinationals. The strength in Singapore’s electronics shipments indicates that our Global Industrial Activity Nowcast will accelerate (Chart I-5, top panel). Moreover, the rapid expansion in China’s credit flows points to a marked increase in Chinese imports, which will help industrial and commodity exporters around the world (Chart I-5, bottom panel). Core producer prices have bottomed. Core producer prices are a direct input in the corporate sector’s pricing power. A trough in this inflation gauge leads to stronger EPS and widening profit margins for the S&P 500 (Chart I-6). Chart I-5The Global Industrial Cycle Is Turning The Corner

The Global Industrial Cycle Is Turning The Corner

The Global Industrial Cycle Is Turning The Corner

Chart I-6Easing Deflationary Pressures Will Help Profits

Easing Deflationary Pressures Will Help Profits

Easing Deflationary Pressures Will Help Profits

Investors should still wait to allocate new funds to the stock market. The stock market’s near-term outlook remains marked by short-term froth that dampens our cyclical optimism, especially because the market advance has been concentrated in a small group of equities. Chart I-7Tactical Froth

Tactical Froth

Tactical Froth

The Exposure Index of the National Association of Active Investment Managers has hit 100.1 (Chart I-7). Such a lofty reading indicates that the price of stocks already incorporates optimistic expectations. From a contrarian perspective, this development boosts the probability that swing traders will face disappointments in the near future and will sell their equity holdings. Similarly, the put/call ratio is near a 10-year low, which confirms that traders have bought a lot of upside exposure to stocks without much protection against a pullback. This level of confidence is often a precursor to a significant correction. Finally, our Tactical Strength Indicator is 1.7-sigma above its mean. Historically, when this risk gauge has hit a reading above 1.3, there is a good probability that the S&P 500 will correct or move sideways (Chart I-8). A catalyst must emerge for those aforementioned vulnerabilities to morph into a correction. If Treasury yields move closer to 1%, then stocks will experience a significant pullback of 10% or more as the market rotates away from the leadership of growth stocks. This risk would be especially salient if real yields move up. As Chart I-9 illustrates, falling TIPS yields have been a pillar of the powerful rally of growth stocks. Moreover, low real yields are arithmetically necessary to justify the current level of market multiples exhibited by the S&P 500 (Chart I-9, bottom panel). Chart I-8The S&P 500 Is Vulnerable To A Correction

The S&P 500 Is Vulnerable To A Correction

The S&P 500 Is Vulnerable To A Correction

Chart I-9Falling Real Yields Have Helped Growth Stocks

Falling Real Yields Have Helped Growth Stocks

Falling Real Yields Have Helped Growth Stocks

Growth and high-P/E ratio stocks are heavily represented in the tech and healthcare sectors, which together account for 42% of the S&P 500. This means that higher yields will likely temporarily drag down the entire market. Ultimately, leadership changes are painful events, but they rarely mark the end of bull markets. Can Yields Move Up? Chart I-10Positive Signs For Inflation

Positive Signs For Inflation

Positive Signs For Inflation

It is time to tweak our bond market view because yields should soon move higher. For the past five months, we have written that yields offer minimal downside and that their asymmetric risk profile made government bonds an unappealing investment. We underweighted this asset class relative to stocks and recommended investors bet on higher inflation breakeven rates. However, forces are aligning to expect real rates to rise and thus, nominal yields should move up. The sequencing of the market’s response to QE increasingly favors lower bond prices. Our US Equity Strategy team recently highlighted that in 2009 stocks were the first asset to reflect the implementation of QE1 by the Fed.4 A weaker dollar followed. Bond yields started to perk up only after the USD deteriorated by enough, after stock prices had climbed by enough and after corporate spreads had narrowed by enough to ease financial conditions to stimulate the economy. So far, 2020 echoes the 2009 pattern and our Financial Conditions Index is more stimulatory than it was prior to the COVID-19 outbreak (see Chart III-36 in Section III). Chart I-11Commodities Point To Higher Yields...

Commodities Point To Higher Yields...

Commodities Point To Higher Yields...

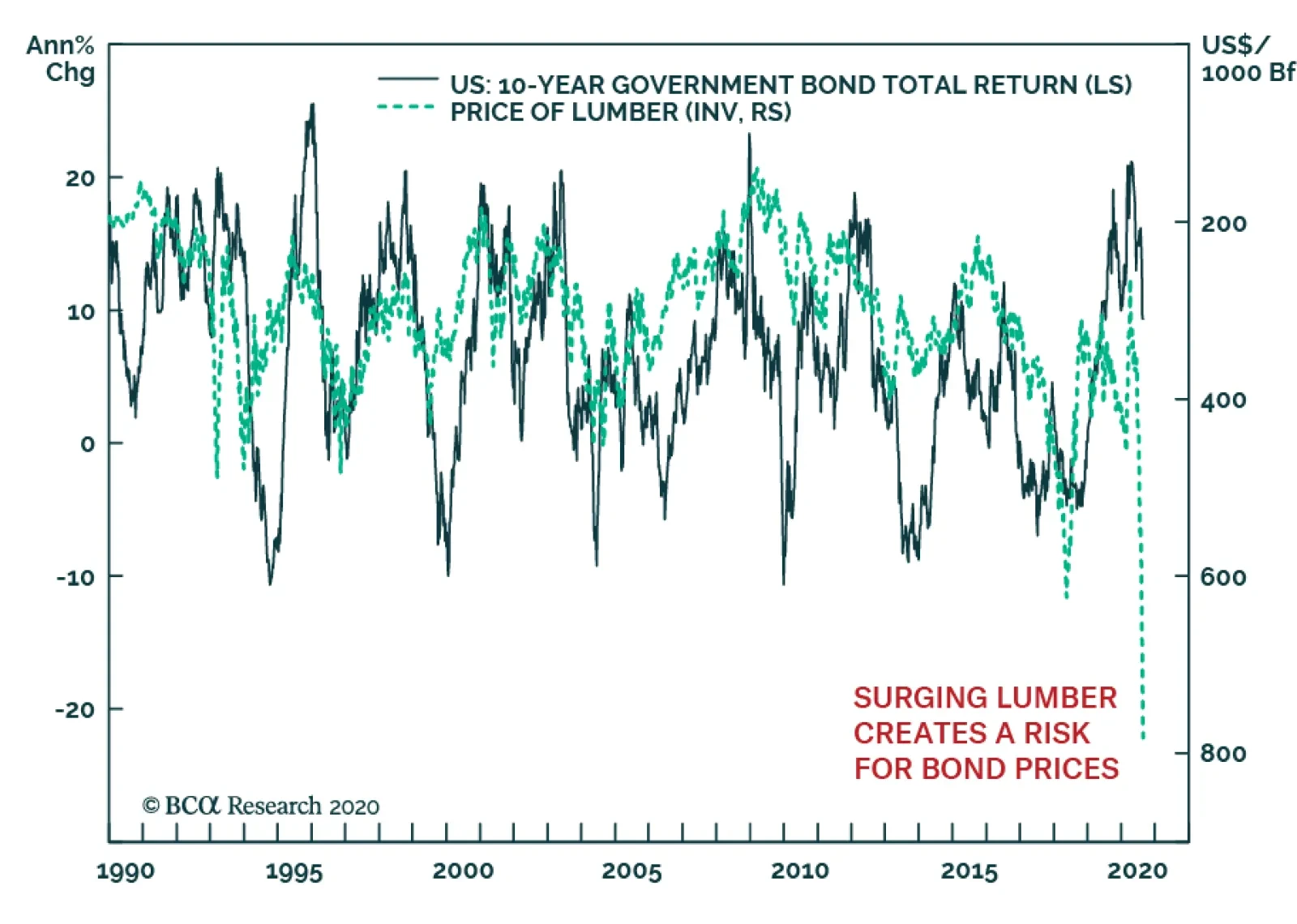

Inflation momentum confirms the risks to bonds. The apex of the deflationary shock has already passed. In July, core CPI excluding shelter rose by 0.84% month-on-month, which was the highest reading since 1981 when the Fed was combating the most violent inflation outbreak in generations. The upturn in core producer prices also warns that the annual inflation rate of core CPI should accelerate meaningfully by early 2021 (Chart I-10). The dollar’s weakness is another inflationary force. Import prices from China have already bottomed, which points to an escalation in goods inflation in the coming months. Firming commodity prices constitute another risk for yields. Our Commodities Advance/Decline line has recently broken out. This technical development is consistent with higher commodity prices and higher bond yields (Chart I-11). Rallying natural resources are inflationary, but they also indicate that the global economy is strengthening, which should put upward pressure on real interest rates. Strength in the housing sector also confirms that government bond yields have upside. As we highlighted above, a robust housing market is an important validation that monetary policy is very accommodative. By definition, the objective of loose policy is to boost future economic activity and eradicate deflationary pressures. The surge in lumber indicates bond prices are showing downside risk (Chart I-12). Additionally, the upswing in mortgage issuance is occurring as the Treasury and corporations boost their borrowings, which will generate more demand to use savings generated in the economy. The price of those savings will be higher real interest rates. Chart I-12...Especially Lumber

...Especially Lumber

...Especially Lumber

The ebbing of COVID-19 also suggests that economic activity has scope to accelerate. Moreover, the House of Representatives reconvened to address the problems plaguing the US Postal Service ahead of the November elections. This early return to work gives Washington another opportunity to negotiate the stimulus bill that it failed to pass earlier this month. We still expect such a bill to ultimately become law because both Democrats and Republicans have too much to lose in November if the economy relapses in response of political paralysis. Declining infections and increased government support will bolster aggregate demand and put upward pressure on rates. The stock market’s near-term outlook remains marked by short-term froth that dampens our cyclical optimism. Market dynamics are also very negative for bonds. Our Valuation Index highlights that Treasurys are incredibly expensive (Chart I-13, top panel). Moreover, our Composite Technical Indicator remains overbought, though it has lost momentum. In this context, the lack of appetite for yield curve control or more QE demonstrated by the Federal Open Market Committee creates a genuine danger for bonds. Without these policies, bond yields will have trouble resisting the upward push created by our rising US Pipeline Inflation Pressures Index, our rebounding Nominal Cyclical Spending proxy (which is an average of the ISM Manufacturing headline index and Prices Paid component), and the uptick in the amount of liquidity sitting on commercial banks’ balance sheets (Chart I-14). Chart I-13Treasurys Are Expensive And Losing Momentum

Treasurys Are Expensive And Losing Momentum

Treasurys Are Expensive And Losing Momentum

Chart I-14Building Cyclical Risks For Bonds

Building Cyclical Risks For Bonds

Building Cyclical Risks For Bonds

Thus, equities are at risk on a tactical basis because we anticipate that 10-year Treasury yields may climb towards 1%, including a rise in TIPS yields. The US election creates an additional near-term hurdle for stocks. As we wrote last month, President Trump will likely become more belligerent toward the US’s trading partners in the coming months. Moreover, Vice-President Joe Biden, who has a comfortable lead in the polls including in key swing states such as Florida, Michigan, Pennsylvania, and Wisconsin wants to cancel half of the 2017 tax cuts.5 Small Over Big Long-term investors should expect stocks to beat bonds on a 5- to 10-year horizon, but equities will generate paltry real returns compared with the past 40 years. Elevated valuations for US equities are consistent with long-term annualized real rates of return of only 0.5% (Chart I-15). Moreover, the long-term outlook for profit margins is poor. As we wrote three months ago, mounting populism will result in redistributive policies that will lift the share of wages relative to GDP.6 Moreover, the shift of the US population to the left on economic matters will push up corporate tax rates. Increased labor costs and corporate taxes are negative for profit margins. If profit margins normalize, then equities will probably underperform the uninspiring expected returns implied by current market multiples. The surge in lumber indicates bond prices are showing downside risk. Investors can still generate generous returns through geographical and sectoral selection. We have highlighted how value stocks, industrials and materials, and EM and European equities will likely beat US equities.7 This month we will explore how US small-cap equities are also well placed to best the dismal projected real returns offered by their large-cap counterparts. Our BCA Relative Technical Indicator shows that small-cap stocks are 1.8-sigma oversold when compared with the S&P 500, which indicates a capitulation among investors toward these equities. The bifurcation is even greater if we compare small-cap equities with the S&P 100’s mega-caps that have driven up the US market in recent years. Incorporating these influences, our Cyclical Capitalization Indicator has moved in favor of small-cap stocks, which suggests that small-cap stocks will be rerated if the yield curve can steepen further (Chart I-16). Equities are at risk on a tactical basis because we anticipate that 10-year Treasury yields may climb towards 1%. Chart I-15Valuations And Profit Margins Threaten Long-Term Stock Returns

Valuations And Profit Margins Threaten Long-Term Stock Returns

Valuations And Profit Margins Threaten Long-Term Stock Returns

Chart I-16Indicators Favor Small Cap Stocks

Indicators Favor Small Cap Stocks

Indicators Favor Small Cap Stocks

Chart I-17A Debt Turnaround Would Help Small Cap Stocks

A Debt Turnaround Would Help Small Cap Stocks

A Debt Turnaround Would Help Small Cap Stocks

Debt dynamics could also increasingly beneficial to small-cap equities. In the past few years, the heavy debt-to-EBITDA of smaller firms created a major headwind for small-cap investors. The indebtedness of small-cap stocks often decreases relative to large-caps when an economic recovery begins. This shift in leverage portends an increase in small-caps’ relative future returns (Chart I-17). Our negative bias toward the dollar and our positive view on commodities also benefit small-cap stocks. Since the early 1990s, increasing real commodity prices and a falling Dollar Index have coexisted with a robust performance of small-cap firms (Chart I-18). The negative US balance-of-payment dynamics, coupled with escalating inflation risks, will continue to weigh on the dollar, especially as various large EM nations try to diversify their reserves and payment systems away from the dollar.8 Meanwhile, a declining dollar, expanding global growth, monetary debasement, populism, inflation and a lack of investment in supply, all will accentuate the appeal of natural resources. The sectoral bias of small-cap indices will capitalize on these trends. Chart I-18Small Is Beautiful

Small Is Beautiful

Small Is Beautiful

Chart I-19Small Cap Stocks Like Higher Yields

Small Cap Stocks Like Higher Yields

Small Cap Stocks Like Higher Yields

Finally, cyclical timing is also moving in favor of small-cap firms. Since 2014, the Russell 2000 has outperformed the S&P 500 when real yields moved higher (Chart I-19). Small-cap firms display a more marked pro-cyclicality than large firms. Additionally, the S&P 500 growth bias implies that the US large-cap benchmark underperforms the small cap indices when real yields increase. Mathieu Savary Vice President The Bank Credit Analyst August 27, 2020 Next Report: September 24, 2020 II. Global Semiconductor Stocks: A Hiatus Is Overdue In A Structural Bull Market The strength in global semiconductor sales in recent months has been due to one-off factors stemming from pandemic-related lockdowns. As the one-off demand surge subsides, global semiconductor sales will decline modestly toward the end of this year. In the near term, global semiconductor stock prices are vulnerable due to overbought conditions, excessive valuations and demand disappointment. The global semiconductor industry is at the epicenter of the US-China confrontation, and more US restrictions on chips sales to China are probable. This is another risk for this sector's share prices. Nevertheless, the structural outlook for global semiconductor demand is constructive. Its CAGR may rise from 3% during 2014-2019 to 5% during 2020-2024. Investor euphoria has taken hold of semiconductor stocks. Global semiconductor stock prices have skyrocketed by 68% from March lows and 96% from December 2018 lows. Meanwhile, global semiconductor sales during March-June rose only by 5% from a year ago. As a result, the ratio of market cap for global semiconductor stocks relative to global semiconductor sales has reached its highest level since at least the inception of data in 2003 (Chart II-1). Chart II-1Global Semi Sector: Market Cap-To-Sales Ratio Has Surged

Global Semi Sector: Market Cap-To-Sales Ratio Has Surged

Global Semi Sector: Market Cap-To-Sales Ratio Has Surged

With semi equity multiples very elevated, their share prices have become even more sensitive to global semiconductor demand growth. Hence, the focus of this report is to try to gauge the strength of global semiconductor demand, both in the near term and structurally. The strength in global semiconductor sales in recent months has been due to one-off factors stemming from the lockdowns. Near-term semiconductor stock prices could disappoint due to weak chip demand from the smartphone sector and diminishing purchases of personal computers (PCs) and servers. However, structurally, we are positive on global semiconductor demand, which is underpinned by the continuing rollout of 5G networks and phones, a wider adoption of data centers, and further technological advancements in artificial intelligence (AI), cloud computing, edge computing and smaller nodes for chip manufacturing (Box II-1). Box II-1 Key Technologies Underpinning Potential Global Semiconductor Demand AI refers to the simulation of human intelligence in machines, for example, computers that play chess and self-driving cars. The goals of AI include learning, reasoning and perception. Cloud computing is the delivery of computing services – including servers, storage, databases, networking, software, analytics and intelligence – over the Internet (“the cloud”) to offer faster innovation, flexible resources and economies of scale. Edge computing is a form of distributed computing, which brings computation and data storage closer to where it is needed, to improve response times and save bandwidth. Technology node refers to the width of line that can be processed with a minimum width in the semiconductor manufacturing industry, such as technology nodes of 10 nanometers (nm), 7nm, 5nm and 3nm. The smaller the nodes are, the more advanced they are. Near-Term Headwinds Semiconductor demand worldwide grew by 6% year-on-year in the first half of this year. There has been a remarkable divergence between world semiconductor sales and the global business cycle (Chart II-2). The divergence between semiconductor sales and economic activity was most striking in the US and China. Semiconductor sales in China rose by 5% year-on-year in Q12020, and in the US they grew by 29% year-on-year in Q22020, despite a contraction in their aggregate demand during the same period. By contrast, Q2 annual growth of semiconductors sales was -2.2% for Japan, -17% for Europe and 1.8% for Asia ex. China and Japan (Chart II-3). Chart II-2World Semi Sales Diverged From The Global Business Cycle

World Semi Sales Diverged From The Global Business Cycle

World Semi Sales Diverged From The Global Business Cycle

Chart II-3Strong Semi Sales In The US And China, But Not Elsewhere

Strong Semi Sales In The US And China, But Not Elsewhere

Strong Semi Sales In The US And China, But Not Elsewhere

The reasons why the US and China posted a surge in semiconductor demand while Europe and Japan experienced a contraction in domestic semiconductor sales are as follows: Most data center investment is occurring in the US and China. Chart II-4 shows that 40% of global hyperscale data centers are operating in the US, much larger than any other countries/regions. China, in turn, ranked second, with a global share of 8%. Chart II-4The US Has The Most Global Hyperscale Data Centers

September 2020

September 2020

Demand contraction in Europe and Japan is due to semiconductor demand in these regions mainly originating from the automobile sector, where production was severely hit by the global pandemic. About 37% of European semiconductor sales were from last year’s automotive market. We believe the divergence between global economic activity and semiconductor sales, as demonstrated by Chart II-2 on page 3, has been due to one-off factors, as the global pandemic lockdowns have spurred semiconductor demand. Such a one-off demand boost will likely dissipate in the coming months. Traditional PCs and tablets: There has been a surge in demand for traditional PCs9 and tablets in the past six months. This was due to the significant increase in online activities, such as working from home, education, e-commerce, gaming and entertainment. Data from the International Data Corporation (IDC) has revealed that shipments of traditional PCs and tablets in volume terms had a strong year-on-year growth of 11.2% and 18.6%, respectively, in the period of April-June (Chart II-5). Looking forward, even renewed lockdowns will not lead to a similar rush to buy these products. Many households are already equipped to work from home and for other online activities. With many countries gradually opening their economies, such demand will diminish. The traditional PC and tablet sectors together account for about 13% of global chip demand (Chart II-6). Chart II-5Personal Computers Sales Have Surged Amid Lockdowns

Personal Computers Sales Have Surged Amid Lockdowns

Personal Computers Sales Have Surged Amid Lockdowns

Server demand: Another major semiconductor demand contribution in Q2020 was from the server sector, which spiked by 21% year-on-year (Chart II-7). The surge in online activities triggered a strong demand for cloud services and remote work applications, both of which require computer servers to run on. Chart II-6The Breakdown Of Global Semiconductor Sales By Type Of Usage

September 2020

September 2020

However, demand from the server sector is also set to diminish in 2H2020 and Q1 2021. Provided the inventories at major data center operators, including Microsoft, Google and Amazon, remain at high levels,10 global cloud service providers will likely reduce their orders of servers next quarter.11 Enterprises will also likely cut their investment in computer servers in 2H2020, as many of them had already increased their purchases of servers to prepare employees and business processes for remote working. We expect global server demand growth to soften in 2H2020. The Digitimes Research forecasted a 5.6% quarter-on-quarter contraction in 3Q2020 and a further cut in global sever shipment in the 4Q2020.10 The global server sector accounts for about 10% of global chip demand and, together with PCs and tablets, they make for 23% (please refer to Chart II-6 on page 5). Further, the smartphone sector – accounting for 27% of global semiconductor demand – will continue struggling in H2 this year. Chart II-7Server Sales Have Surged Amid Lockdowns

Server Sales Have Surged Amid Lockdowns

Server Sales Have Surged Amid Lockdowns

Chart II-8Global Smartphone Shipments Will Likely Remain Weak In 2020H2

Global Smartphone Shipments Will Likely Remain Weak In 2020H2

Global Smartphone Shipments Will Likely Remain Weak In 2020H2