Fixed Income

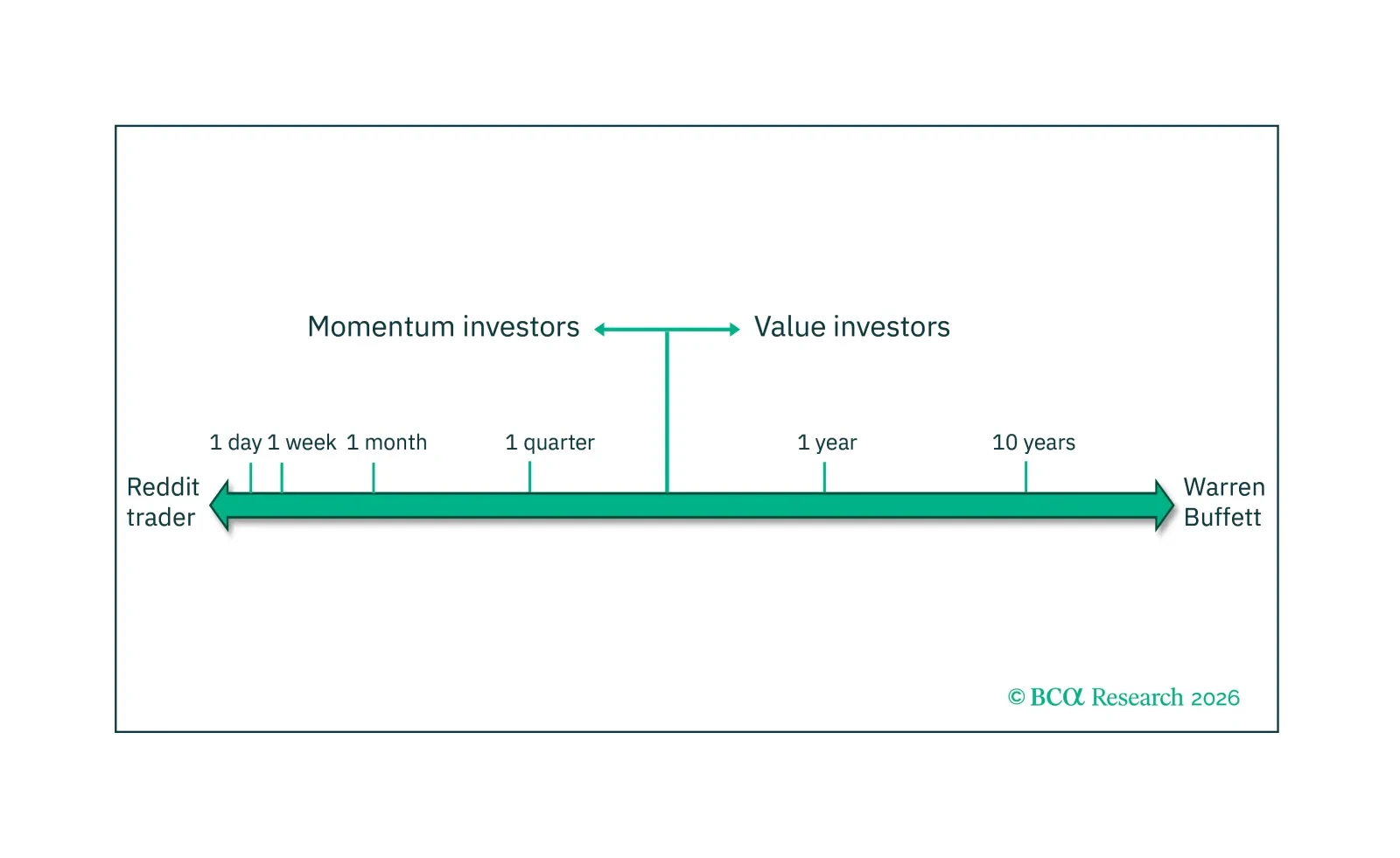

A market becomes inefficient, illiquid, and vulnerable to a phase transition when the ‘wisdom of crowds’ switches to the ‘madness of crowds.’ This switch from market wisdom to market madness may be the most significant recurring behavioural opportunity in active fund management and can be exploited in real-time by measuring the market’s complexity.

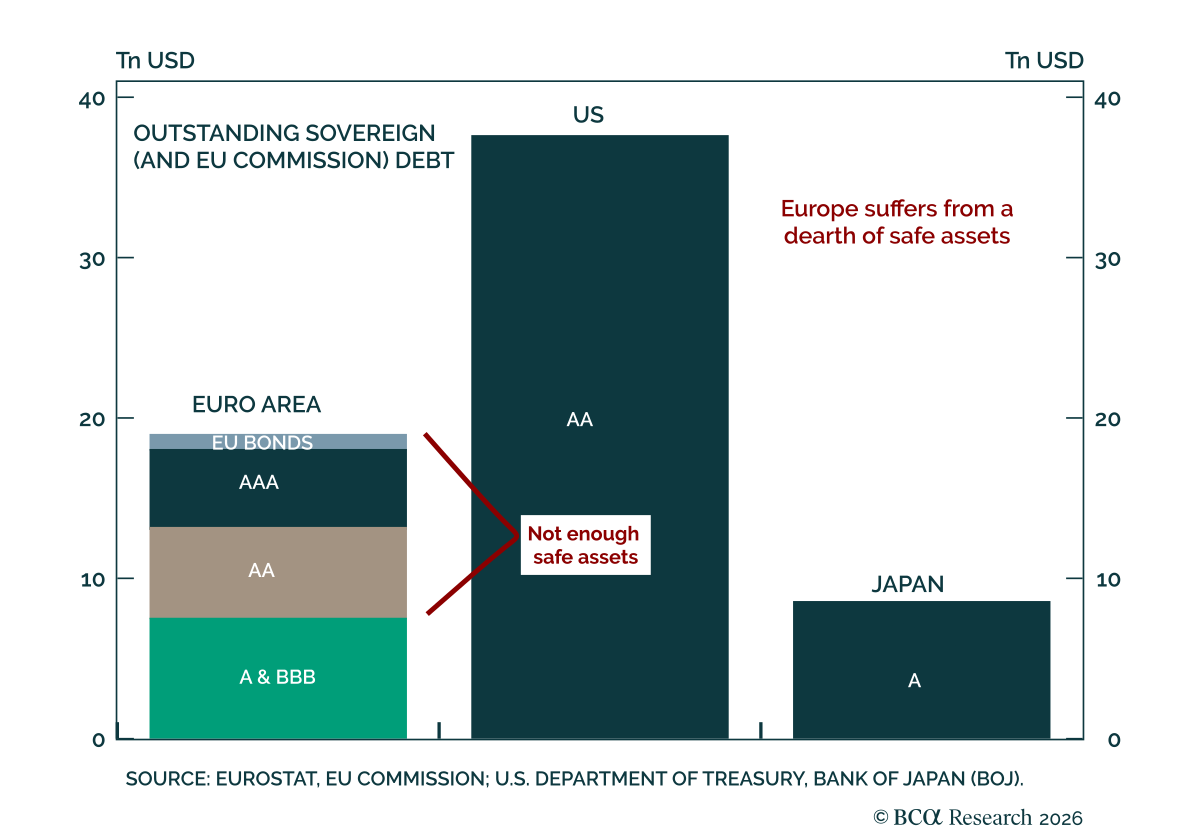

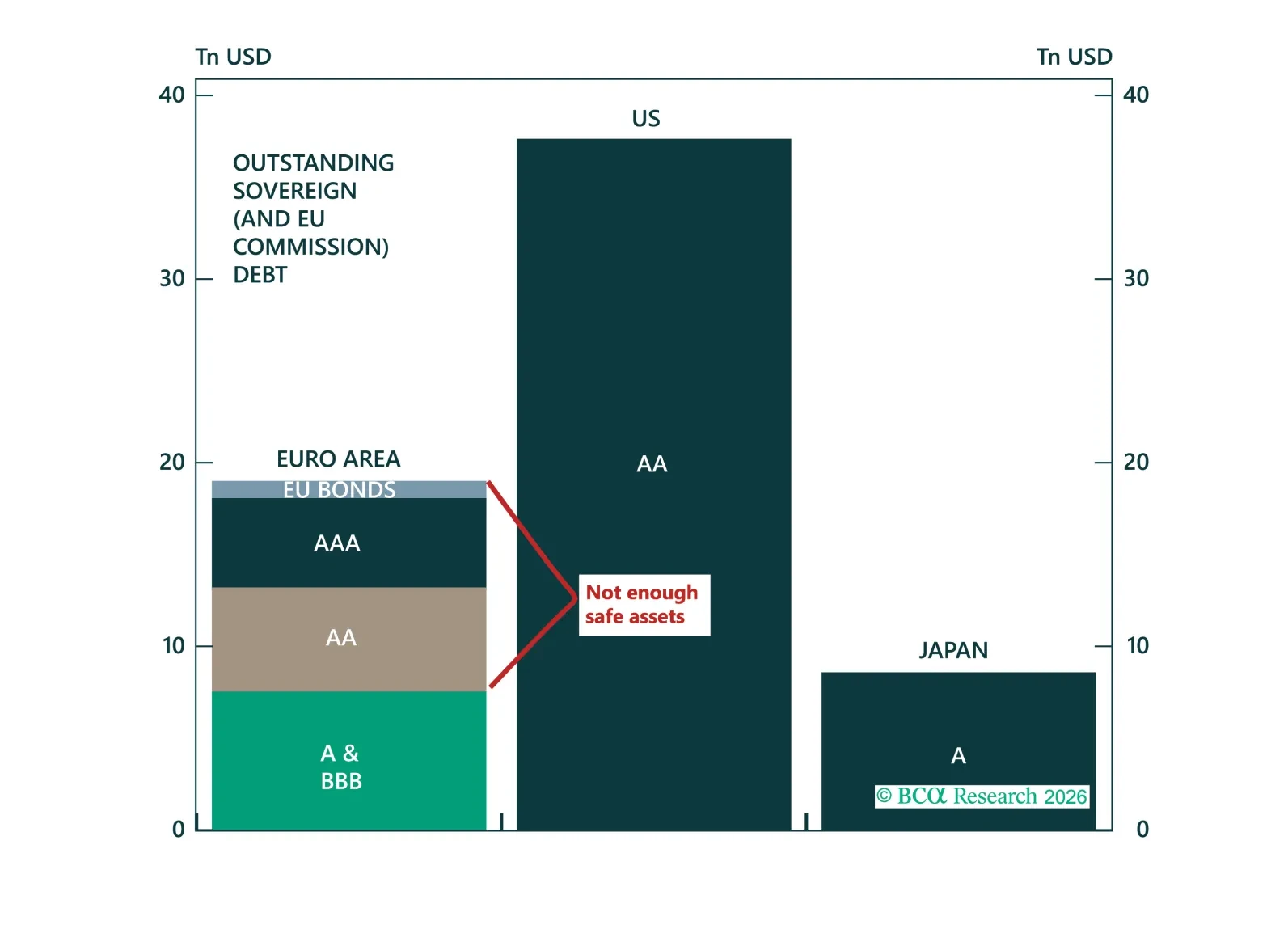

The dollar's retreat is creating the most compelling window for euro internationalisation since Maastricht, but Europe is missing the one instrument that would make it real. In this report, we make the case for the Eurobond, assess which model is most likely to prevail, and explain why the trade is long euro on dips and overweight Central and Eastern European sovereign spreads.

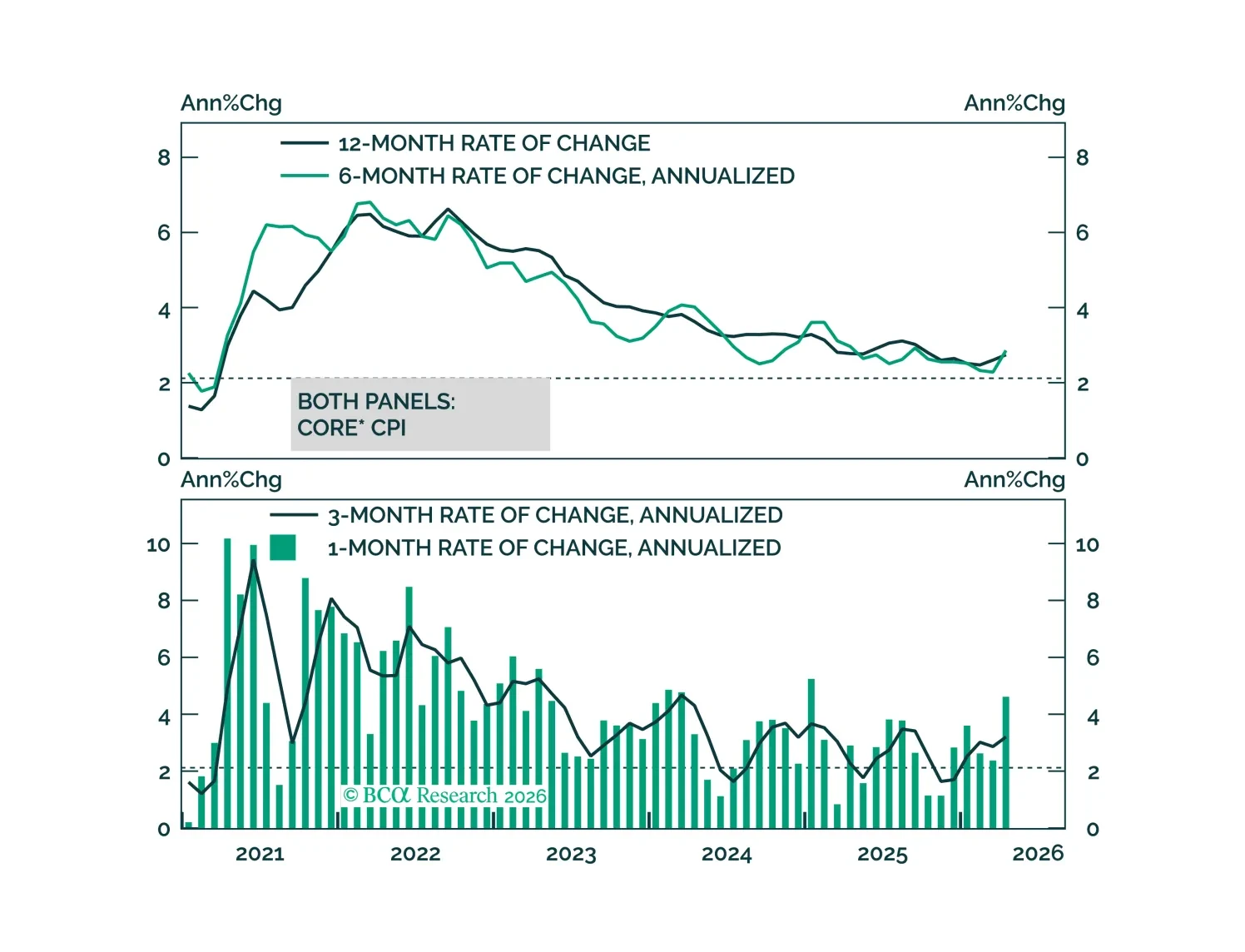

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

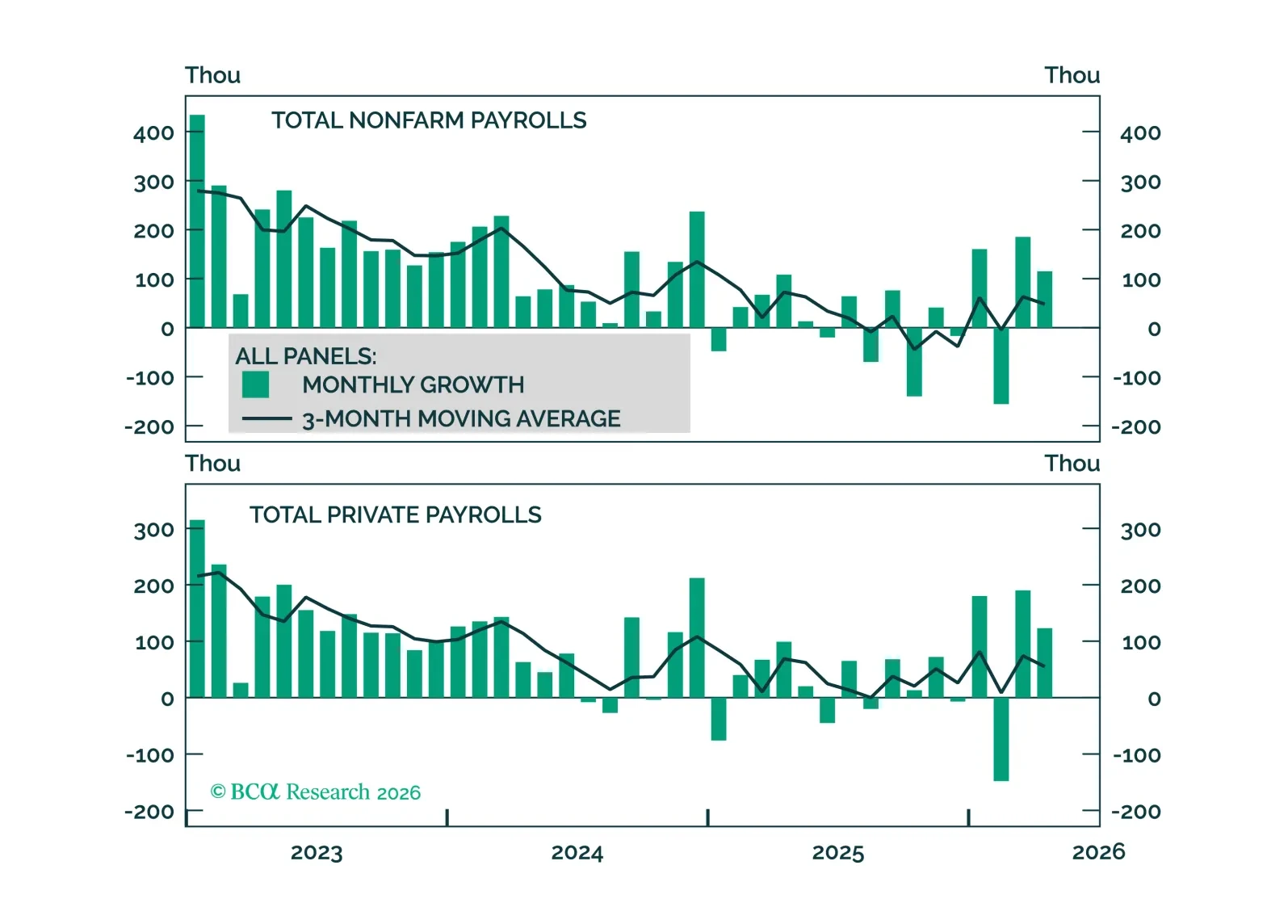

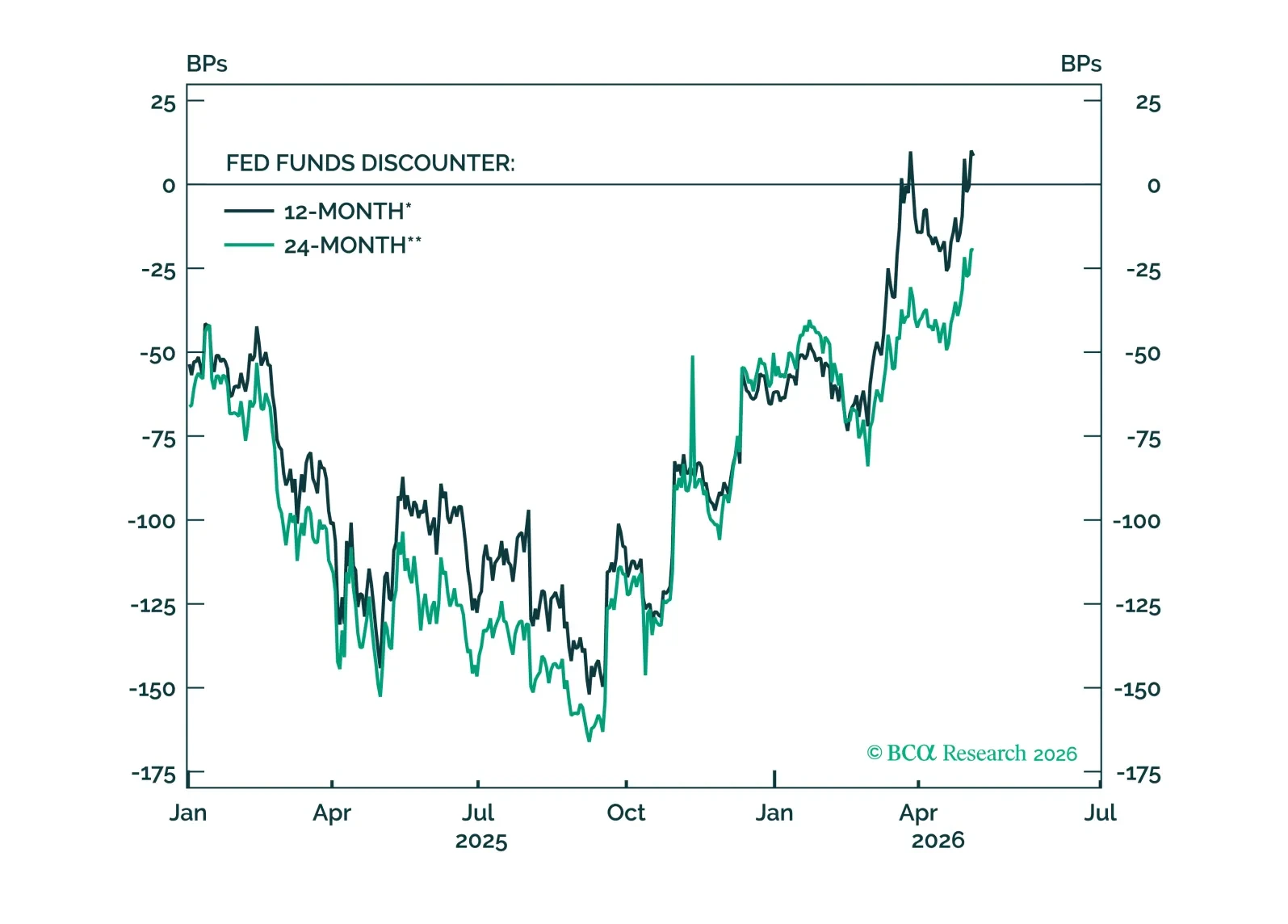

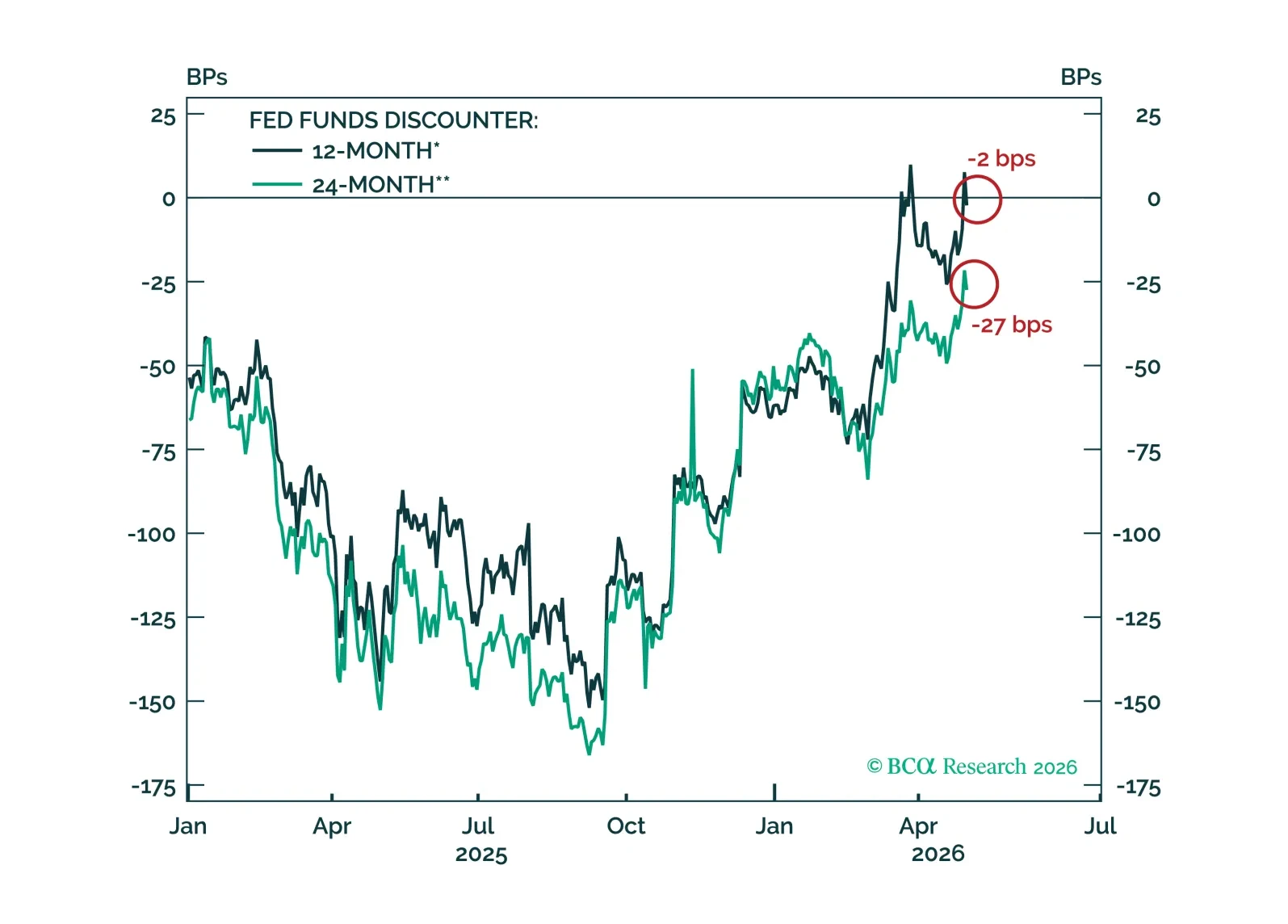

Improving job growth keeps Fed rate cuts off the table, but evidence of labor market tightening will be required before rate hikes become part of the discussion.

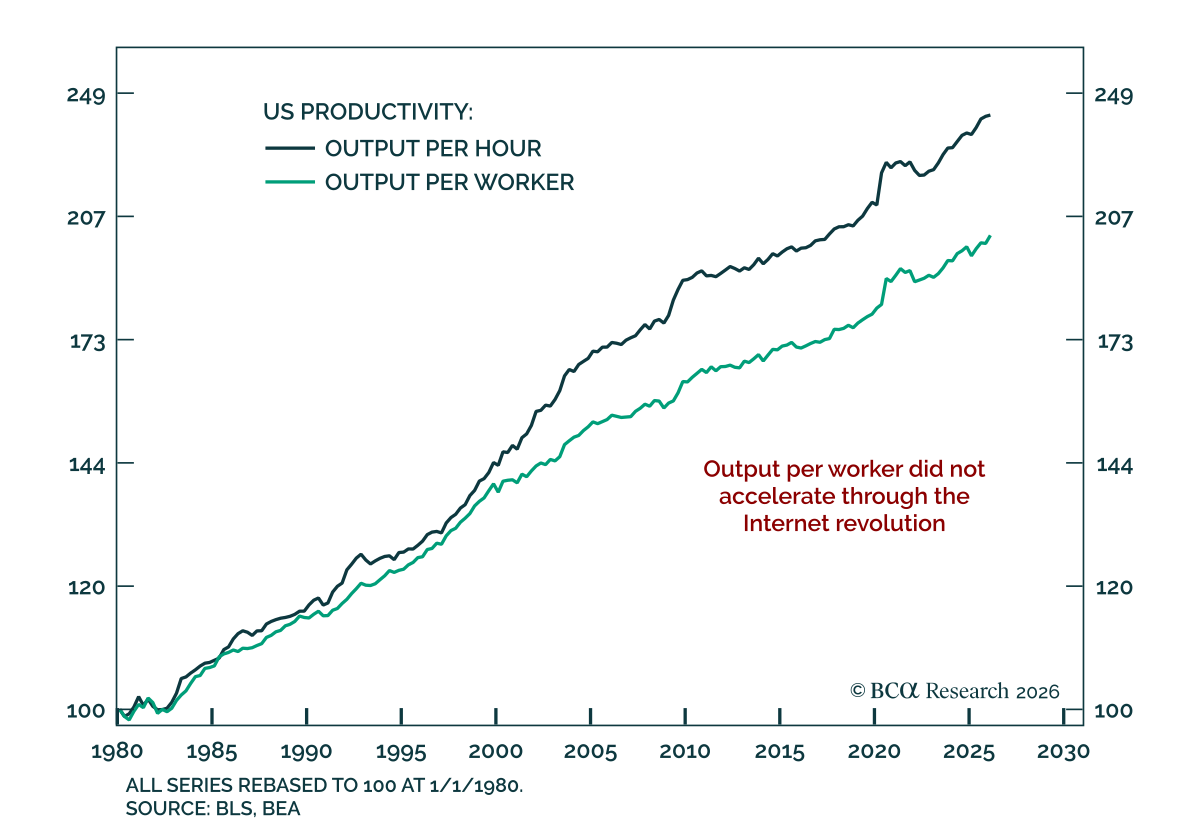

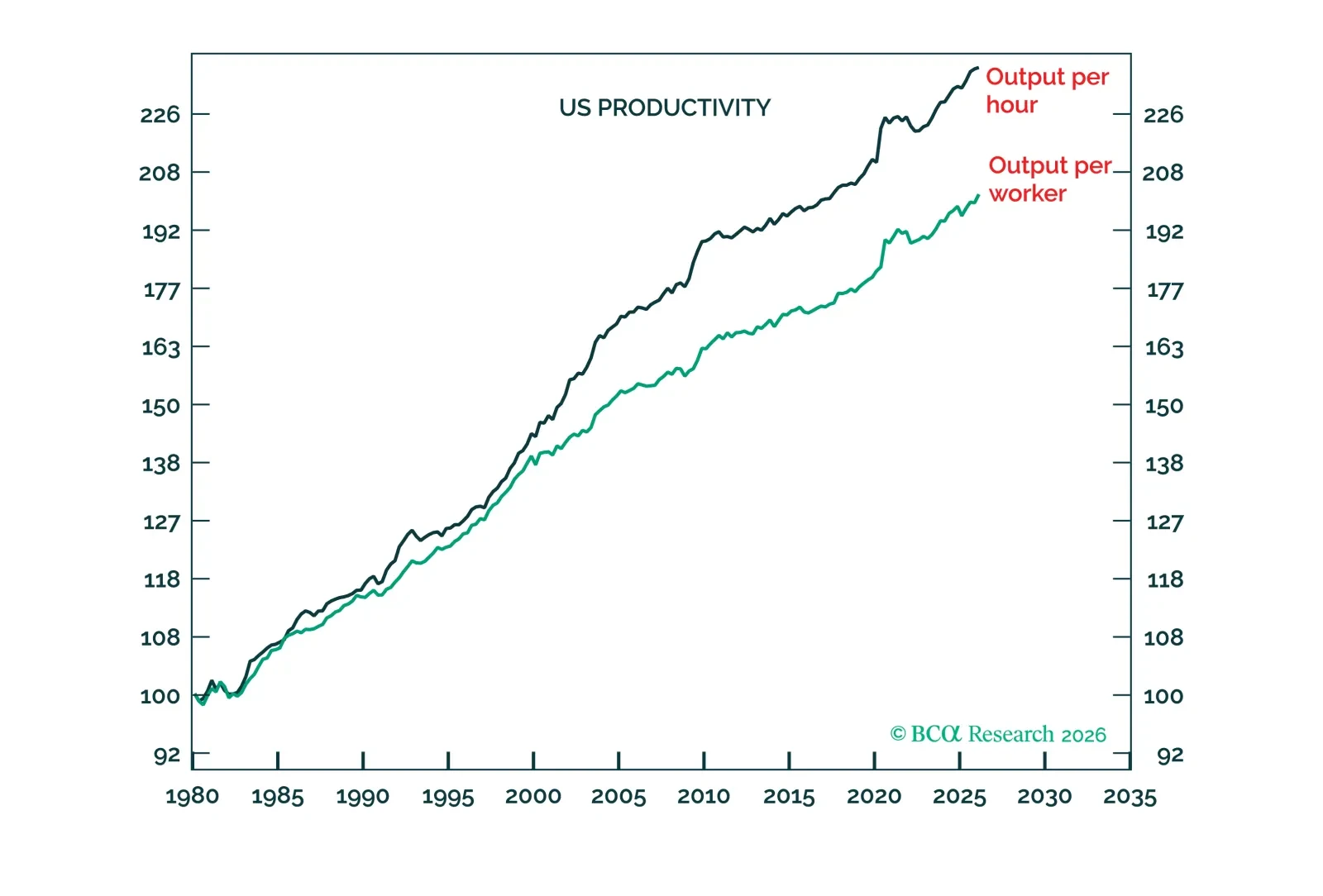

New Fed Chair, Kevin Warsh, is betting that an AI-driven productivity acceleration will get the Fed out of jail for persistently missing its 2 percent inflation target. But history informs us that while new technology adoption is exponential, total productivity growth is not. So, if Warsh’s bet goes wrong, as is likely, the US inflation overshoot will persist. We discuss the investment implications. Plus, a new trade is short cotton.

Our Portfolio Allocation Summary for May 2026.

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.