Fixed Income

BCA Research's Global Fixed Income Strategy service concludes that the growing divide between falling negative real bond yields and rising inflation expectations in major developed economies may be a sign of investors pricing in slower long-run potential…

Highlights Global Bond Yields: The growing divide between falling negative real bond yields and rising inflation expectations in the US and other major developed economies may be a sign of investors pricing in slower long-run potential economic growth in the aftermath of the COVID-19 recession – and, thus, lower equilibrium real interest rates. Stay overweight inflation-linked bonds versus nominal equivalents. Currency-hedged spread product: A broad ranking of currency-hedged global spread product yields, adjusted for volatility and credit quality, shows that the most attractive yields (hedged into USD, EUR, GBP and JPY) are on offer in emerging market USD-denominated investment grade corporates and high-yield company debt in the US and UK. Feature Global bond yields are testing the downside of the narrow trading ranges that have persisted since May. As of last Friday, the yield on the Bloomberg Barclays Global Treasury index was at 0.41%, only 3 basis points (bps) above the 2020 low seen back in March. The 10-year US Treasury yield closed yesterday at 0.56%, only 6bps above the year-to-date low. Chart of the Week

A Massive Shock To Growth ... And Interest Rates

A Massive Shock To Growth ... And Interest Rates

Concerns about global growth, with the number of new COVID-19 cases still surging in the US and new breakouts occurring in countries like Spain and Australia, would seem to be the logical culprit for the decline in yields. The first reads on global GDP data for the 2nd quarter released last week were historically miserable, with declines of -33% (annualized) in the US and -10% in the euro area (non-annualized). That represents a very deep hole of lost output, literally wiping out several years of growth. Even with the sharp improvements seen recently in cyclical indicators like global manufacturing PMIs, especially in China and Europe, a return to pre-pandemic levels of global economic output is many years away. Central banks will have no choice but to keep policy rates near 0% for at last the next couple of years, as is the current forward guidance provided by the Fed, ECB and others. Lower global bond yields may simply be reflecting the reality that it will take a long time to heal the economic wounds from the pandemic. However, there may be a more insidious reason why bond yields are falling. Investors may be permanently marking down their expectations for long-term potential economic growth, and equilibrium interest rates, in response to the devastation caused by the COVID-19 recession. Last week, Fitch Ratings lowered its estimates for long-term potential GDP growth, used to determine sovereign credit ratings, by 0.5 percentage points for the US (now 1.4%), 0.5 percentage points for the euro area (now 0.7%) and 0.7 percentage points in the UK (now 0.7%).1 These are declines similar in magnitude to the plunge in the OECD’s potential growth rate estimates seen after the 2009 Great Recession (Chart of the Week). Bond yields in the US and Europe witnessed a fundamental repricing in response, with nominal 5-year yields, 5-years forward breaking 200bps below the 4-6% range that prevailed in the US and Europe during the decade prior to the Great Recession. A similar re-rating of global bond yields to structurally lower levels may now be happening, with investors now believing that central banks will have difficulty raising rates much (if at all) in the future - even after the pandemic has ended. The Message From Declining Negative Real Bond Yields Chart 2The Real Rate/Breakevens Divergence Continues

The Real Rate/Breakevens Divergence Continues

The Real Rate/Breakevens Divergence Continues

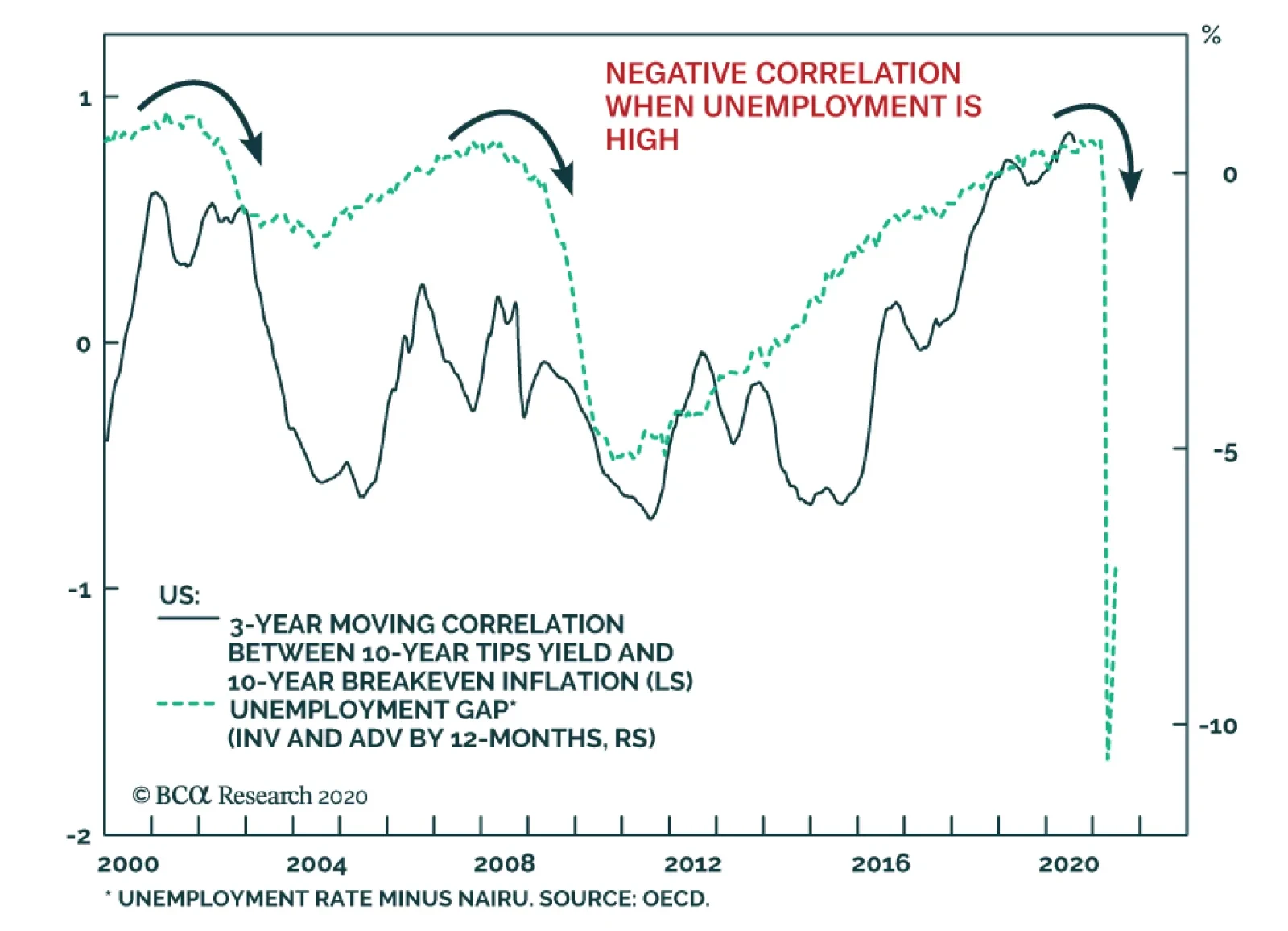

The typical signals about economic growth from government bond yields are now less clear because of the aggressive policy responses to the COVID-19 crisis. 0% policy rates, dovish forward guidance on the timing of any future rate increases, large scale asset purchases (QE), and more extreme measures like yield curve control to peg bond yields, have all acted to suppress the level and volatility of nominal global bond yields. Within those calm nominal yields, however, the dynamic that has been in place since May - rising inflation breakevens and falling real bond yields – is growing in intensity. The 10-year US TIPS real yield is now at a new all-time low of -1.02%, while the 10-year TIPS breakeven is now up to 1.58%, the highest since February before the pandemic began to roil financial markets (Chart 2). Similar trends are evident in most other major developed economy bond markets, with the gap between falling real yields and widening breakevens growing at a notably faster pace in Canada and Australia. More often than not, longer-term real yields tend to move in the same direction as inflation expectations when economic growth is improving. The former responds to faster economic activity, often with an associated pick up in private sector credit demand. At the same time, rising inflation expectations discount higher economic resource utilization (i.e. lower unemployment) and confidence that inflation will start to pick up. A deeply negative correlation between longer-term real yields and inflation expectations is unusual, but not unprecedented. A deeply negative correlation between longer-term real yields and inflation expectations is unusual, but not unprecedented. In Chart 3, we show the range of rolling three-year correlations between 10-year inflation-linked (real) government bond yields and 10-year inflation breakevens in the US, Germany, France, Italy, the UK, Japan, Canada and Australia for the post-crisis period. The triangles in the chart are the latest three-year correlation, while the diamonds are a more recent measure showing the 13-week correlation. There are a few key takeaways from this chart: Chart 3Negative Real Yield/Breakevens Correlations Are Not Unprecedented

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

All countries shown have experienced a sustained period of negative correlation between real yields and inflation breakevens; The correlation has mostly been positive in Australia and has always been negative in Japan; Most importantly, the deeply negative correlations seen over the past three months – with rising breakevens all but fully offsetting falling real yields – are at or below the range of historical experience for all countries shown. Chart 4TIPS Yields May Stay Negative For Some Time

TIPS Yields May Stay Negative For Some Time

TIPS Yields May Stay Negative For Some Time

In the current virus-stricken world, where many businesses that have closed during the pandemic may never reopen, there will be abundant spare global economic capacity for several years. In the US, measures of spare capacity like the unemployment gap (the unemployment rate minus the full-employment NAIRU rate) have been a reliable leading directional indicator of the long-run correlation between real TIPS yields and TIPS breakevens over the past decade (Chart 4). The surge in US unemployment seen since the spring, which has pushed the jobless rate into double-digit territory, suggests that the current deeply negative correlation between US real yields and inflation breakevens can persist over the next 6-12 months. Given the large increases in unemployment seen in other countries, the negative correlations between real yields and inflation breakevens should also continue outside the US. As for inflation expectations, those remain correlated in the short-run to changes in oil prices and exchange rates in all countries. On that front, there is still some room for breakevens to widen to reach the fair value levels implied by our models.2 A good conceptual way to think about inflation breakevens on a more fundamental level, however, is as a “vote of confidence” in a central bank’s monetary policy stance. If investors perceive policy settings to be too tight, markets will price in slower growth and lower inflation expectations, and vice versa. Every developed market central bank is now setting policy rates near or below 0% - and promising to keep them there until at least the end of 2022. Thus, the trend of rising global inflation breakevens can continue as a reflection of very dovish central banks that will be more tolerant of increases in inflation and not tighten policy pre-emptively. Currently, real 10-year inflation-linked bond yields are below the New York Fed’s estimates of the neutral real short-term rate, or “r-star”, in the US and the UK (Chart 5), as well as in the euro area and Canada (Chart 6).3 In the US and euro area, real yields have followed the broad trend of r-star, but the gap between the two is relatively moderate with r-star estimated to be only 0.5% in the US and 0.2% in the euro zone (where the ECB is setting a negative nominal interest rate on European bank deposits at the central bank – a policy choice that the Fed has been very reluctant to consider). Chart 5Negative Real Bond Yields Are Below R* In The US & UK ...

Negative Real Bond Yields Are Below R* In The US & UK ...

Negative Real Bond Yields Are Below R* In The US & UK ...

Chart 6... As Well As In The Euro Area & Canada

... As Well As In The Euro Area & Canada

... As Well As In The Euro Area & Canada

A more interesting study is in the UK where 10yr inflation-linked Gilt yields have fallen below -2.5%, but without the Bank of England implementing any negative nominal policy rates. In the UK, inflation expectations have been relatively high – running in the 2.5-3% range prior to the COVID-19 recession – as the Bank of England has consistently kept overnight interest rates below actual CPI inflation since the 2008 financial crisis. Thus, nominal Gilt yields have stayed relatively low for longer, as real yields and inflation expectations have remained negatively correlated for a long period with the Bank of England maintaining a consistently negative real policy rate. Chart 7Spillovers From Negative TIPS Yields Into Other Assets

Spillovers From Negative TIPS Yields Into Other Assets

Spillovers From Negative TIPS Yields Into Other Assets

If the Fed were to do the same in the US, keeping the funds rate very low even as inflation rises, then a similar dynamic could take place where real TIPS yields continue to fall and TIPS breakevens continue to rise as the market prices in a sustained negative real fed funds rate. That may already be happening, with Fed Chair Jerome Powell hinting last week that the Fed is in the process of completing its inflation strategy review – with a shift towards rate hikes occurring only after realized inflation has sustainably increased to the Fed’s 2% target. A forecast of inflation heading to 2% because of falling unemployment will no longer be enough.4 Other factors may be at work depressing real bond yields while boosting inflation expectations, such as the massive QE bond buying programs of the Fed, ECB and other central banks. Yet even QE programs are essentially an aggressive form of forward guidance designed to drive down longer-term bond yields by lowering expectations of future interest rates. In sum, it is increasingly likely that the current phase of negative global real bond yields may become longer lasting if markets believe that equilibrium real policy rates are now negative. Bond investors will expect central banks to sit on their hands and do nothing in that environment, even if inflation starts to increase. This not only has implications for bond markets, but other asset classes as well based on what is happening in the US. The steady decline in the in the 10-year US TIPS yield has boosted the valuation of assets that typically have been considered inflation hedges, like equities and gold (Chart 7). The fall in TIPS yields also suggests that more weakness in the US dollar is likely to come over the next 6-12 months – another reflationary factor that should help lift global inflation expectations and boost the attractiveness of inflation-linked bonds. The current phase of negative global real bond yields may become longer lasting if markets believe that equilibrium real policy rates are now negative. Bottom Line: The growing divide between falling negative real bond yields and rising inflation expectations in the US and other major developed economies may be a sign of investors pricing in slower long-run potential economic growth in the aftermath of the COVID-19 recession – and, thus, lower equilibrium real interest rates. Stay overweight inflation-linked bonds versus nominal equivalents. Searching For Value In Global Spread Product Last week, we looked at the impact of currency hedging on the attractiveness of government bond yields across the developed markets.5 We concluded that US Treasuries still offered superior yields to most other countries’ sovereign bonds, even with the US dollar in a weakening trend and after hedging out currency risk. We also presented a cursory look at the relative attractiveness of the major global spread product categories in that report, but without factoring in any considerations on the relative credit quality or volatility between sectors. This week, we will look at the relative value of global spread products hedged into USD, GBP, EUR and JPY, but after controlling for those credit and volatility risks. We conducted a similar analysis in early 2018,6 ranking the currency-hedged yields for a wide variety of global spread products by the ratio of yields to trailing volatility. This time, instead of looking at the just that simple valuation metric, we use regression models to make a judgment on how under- or over-valued spread products are relative to their “fair value”. To recap the methodology of this analysis, we take the Bloomberg Barclays index yield-to-maturity (YTM) for each spread product category, hedged into the four currencies used in this analysis, and divide it by the annualized trailing volatility of those yields over both short-term (1-year) and long-term (3-year) windows. In order to hedge the yields into each currency, we used the annualized differentials between spot and 3-month forward exchange rates, which is the all-in cost of hedging. We then compare those currency-hedged, volatility-adjusted yields to two measures of risk: the index credit rating and duration times spread (DTS) for each spread product. Table 1 summarizes the attractiveness of each product when hedged into different currencies. The rank is based on the average of four different valuation measures.7 The higher the rank, the more attractive the sector is in terms of yield relative to risk measures such as both short-term and long-term volatilities, credit ratings, and DTS. Table 1Ranking Currency-Hedged, Risk-Adjusted Global Spread Product Yields

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

A few interesting points come from the table: Emerging market (EM) USD-denominated investment grade (IG) corporate debt ranks at or near the top of the rankings, for all currencies; the opposite holds true for EM USD-denominated sovereign bonds Almost all European spread products rank poorly for non-euro denominated investors US & UK high-yield (HY) rank highly for all currencies US real estate related assets (MBS and CMBS) also rank well for all investor groups In general, US products are more attractive than European credit sectors. This is mainly because US spread products offer higher yields than European ones even after accounting for volatility and the weakening US dollar. Almost all European spread products rank poorly for non-euro denominated investors. Chart 8 shows the unhedged YTM on the x-axis and the option-adjusted spread (OAS) on the y-axis (Table 2 contains the abbreviations used in this chart and all remaining charts in this report). Unsurprisingly, the YTM and OAS follow a very tight linear relationship. However, when yields are hedged into different currencies and risk measures are factored in, the result changes. Chart 8Global Spread Product Yields & Spreads

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Charts 9A to 12B show the details of spread product analysis with different currency hedges and risk factors. To limit the number of charts shown, we show only currency-hedged yields adjusted by long-term trailing volatility (the rankings do not change significantly when using a shorter-term volatility measure). The y-axis in all charts shows the volatility-adjusted yields, while the x-axis shows credit ratings and DTS. Sectors that are close to upper-right in each chart are more attractive (undervalued), while spread products that are close to bottom-left are less attractive (overvalued). Chart 9AGlobal Spread Product Yields, Hedged Into USD, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 9BGlobal Spread Product Yields, Hedged Into USD, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 10AGlobal Spread Product Yields, Hedged Into EUR, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 10BGlobal Spread Product Yields, Hedged Into EUR, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 11AGlobal Spread Product Yields, Hedged Into GBP, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 11BGlobal Spread Product Yields, Hedged Into GBP, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 12AGlobal Spread Product Yields, Hedged Into JPY, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 12BGlobal Spread Product Yields, Hedged Into JPY, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Table 2Global Spread Products In Our Analysis

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

An interesting result is that when comparing the three major high-yield products (US-HY, EMU-HY and UK-HY), US-HY is the most attractive in USD terms, but UK-HY is more attractive when hedged into GBP, EUR, and JPY. Another observation is that higher quality bonds such as government-related and agency debt in the US and euro area are overvalued and less attractive given how low their yields are, regardless of their low volatility. The results from this analysis may differ from our current recommendations. For example, we currently only have a neutral recommendation on EM corporates, but based on this analysis, EM corporates offer the most attractive return in USD terms. This analysis is purely based on YTM and traditional risk factors without considering other concerns that could make EM assets riskier such as the spread of COVID-19 in major EM countries. However, these rankings do line up with our major spread product call of overweighting US IG and HY corporate debt versus euro area equivalents. Based on this analysis, EM corporates offer the most attractive return in USD terms. Bottom Line: A broad ranking of currency-hedged global spread product yields, adjusted for volatility and credit quality, shows that the most attractive yields (hedged into USD, EUR, GBP and JPY) are on offer in emerging market USD-denominated investment grade corporates and high-yield company debt in the US and UK. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Footnotes 1https://www.fitchratings.com/research/sovereigns/coronavirus-impact-on-gdp-will-be-felt-for-years-to-come-27-07-2020 2 Please see BCA Global Fixed Income Strategy Weekly Report, "How To Play The Revival Of Global Inflation Expectations", dated June 23, 2020, available at gfis.bcaresarch.com. 3 We use the French 10-year inflation-linked bond as the proxy for the entire euro area, as this is the oldest inflation-linked bond market in the region and thus has the most data history. 4https://www.wsj.com/articles/fed-weighs-abandoning-pre-emptive-rate-moves-to-curb-inflation-11596360600?mod=hp_lead_pos6 5 Please see BCA Research Weekly Report, “What A Weaker US Dollar Means For Global Bond Investors”, dated July 28, 2020, available at gfis.bcaresarch.com. 6 Please see BCA Global Fixed Income Strategy Weekly Report, "Policymakers Are Now Selling Put Options On Volatility, Not Asset Prices", dated March 6, 2018, available at gfis.bcareseach.com. 7 Hedged YTM/Short-term trailing volatility vs. Credit Rating; Hedged YTM/Long-term trailing volatility vs. Credit Rating; Hedged YTM/Long-term trailing volatility vs. Duration; Hedged YTM/Long-term trailing volatility vs. Duration. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Chart 1How Much Lower For Real Yields?

How Much Lower For Real Yields?

How Much Lower For Real Yields?

Treasury yields moved lower last month even as the overall bond market priced-in a more reflationary economic environment. Spread product outperformed Treasuries and inflation expectations rose, but nominal bond yields still fell as plunging real yields offset the rising cost of inflation compensation (Chart 1). This sort of market behavior is unusual, but it is also easily explained. The market is starting to believe in the economic recovery, and it is pushing inflation expectations higher as a result. However, it also believes that the Fed will keep the nominal short rate pinned at zero even as inflation rises. Falling real yields result from rising inflation expectations and stable nominal rate expectations. This combination of market moves can’t go on forever. Eventually, inflation expectations will rise enough that the market will price-in policy tightening. This will push real yields higher, starting at the long-end of the curve. However, it’s difficult to know when this will occur, especially with the Fed doing its best to convey a dovish bias. In this environment, we advise investors to keep portfolio duration near benchmark and to play the reflation trade through real yield curve steepeners (see page 11). Real yield curve steepeners will profit in both rising and falling real yield environments, as long as the reflation trade remains intact. Feature Investment Grade: Overweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 177 basis points in July, bringing year-to-date excess returns up to -361 bps. Spreads continue to tighten and investment grade corporate bond valuation is turning expensive, particularly for the highest credit tiers. The 12-month breakeven spread for the overall corporate index has been tighter 29% of the time since 1996 (Chart 2). The similar figure for the Baa credit tier is a relatively cheap 38% (panel 3). With the Fed providing a strong back-stop for investment grade corporates – one that has now officially been extended until the end of the year – we should expect spreads to turn even more expensive, likely returning to the all-time stretched valuations seen near the end of 2019. With that in mind, we want to focus our investment grade corporate bond exposure on high quality Baa-rated bonds. These are bonds that offer greater expected returns than those rated A and above, but that are also unlikely to be downgraded into junk (panel 4). Subordinate bank bonds are prime examples of securities that exist within this sweet spot.1 At the sector level, we also recommend overweight allocations to Healthcare and Energy bonds,2 as well as underweight allocations to Technology3 and Pharmaceutical bonds.4 Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

Table 3BCorporate Sector Risk Vs. Reward*

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

High-Yield: Neutral Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 425 basis points in July, bringing year-to-date excess returns up to -466 bps. All junk credit tiers delivered strong returns on the month with the exception of the lowest-rated (Ca & below) bonds (Chart 3). These securities underperformed Treasuries by 267 bps, as a rising default rate weighs on the weakest credits. We are sticking with our relatively cautious stance toward high-yield, favoring bonds only from those issuers that will be able to access the Fed’s emergency lending facilities if need be. This includes most of the Ba-rated credit tier, some portion of the B-rated credit tier, and very few bonds rated Caa & below. We view the Fed back-stop as critically important because junk spreads are far too tight based on fundamentals alone. For example, current market spreads imply that the default rate must come in below 4.5% during the next 12 months for the junk index to deliver a default-adjusted spread consistent with positive excess returns versus Treasuries (panel 3).5 This would require a rapid improvement in the economic outlook. At the sector level, we advise overweight allocations to high-yield Technology6 and Energy7 bonds. We are underweight the Healthcare and Pharmaceutical sectors.8 MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 2 basis points in July, dragging year-to-date excess returns down to -46 bps. The conventional 30-year MBS index option-adjusted spread (OAS) tightened 12 bps in July, but it still offers a pick-up relative to other comparable sectors. The MBS OAS of 86 bps is greater than the 75 bps offered by Aa-rated corporate bonds (Chart 4), the 47 bps offered by Aaa-rated consumer ABS and the 72 bps offered by Agency CMBS. Despite this spread advantage, we are concerned that the elevated primary mortgage spread is a warning that refinancing risk could flare later this year (bottom panel). Even if Treasury yields are unchanged, a further 50 bps drop in the mortgage rate due to spread compression cannot be ruled out. Such a move would lead to a significant increase in prepayment losses. With that in mind, we are concerned about the low level of expected prepayment losses (option cost) priced into the MBS index (panel 3). A refi wave in the second half of this year would undoubtedly send that option cost higher, eating into the returns implied by the lofty OAS. Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 77 basis points in July, bringing year-to-date excess returns up to -325 bps. Sovereign debt outperformed duration-equivalent Treasuries by 285 bps on the month, bringing year-to-date excess returns up to -567 bps. Foreign Agencies outperformed the Treasury benchmark by 62 bps in July, bringing year-to-date excess returns up to -706 bps. Local Authority debt outperformed Treasuries by 74 bps in July, bringing year-to-date excess returns up to -368 bps. Domestic Agency bonds underperformed by 4 bps, dragging year-to-date excess returns down to -62 bps. Supranationals outperformed by 5 bps, bringing year-to-date excess returns up to -14 bps. The US dollar’s recent weakness, particularly against EM currencies, is a huge boon for Sovereign and Foreign Agency returns (Chart 5). However, US corporate spreads will also perform well in an environment of improving global growth and dollar weakness and, for the most part, value remains more compelling in the US corporate space (panel 3). Within the Emerging Market Sovereign space: South Africa, Mexico, Colombia, Malaysia, UAE, Saudi Arabia, Qatar, Indonesia, Russia and Chile all offer a spread pick-up relative to quality and duration-matched US corporate bonds. Of those attractively priced countries, Mexico stands out as particularly compelling on a risk/reward basis.9 Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds outperformed the duration-equivalent Treasury index by 115 basis points in July, bringing year-to-date excess returns up to -473 bps (before adjusting for the tax advantage). Municipal bond spreads versus Treasuries tightened in July, but remain elevated compared to typical historical levels. In fact, both the 2-year and 10-year Aaa Muni yields are above equivalent-maturity Treasury yields, despite municipal debt’s tax exempt status (Chart 6). Municipal bonds are also attractively priced relative to corporate bonds across the entire investment grade credit spectrum, as we demonstrated in a recent report.10 In that report we also mentioned our concern about the less-than-generous pricing offered by the Fed’s Municipal Liquidity Facility (MLF). At present, MLF funds are only available at a cost that is well above current market prices (panel 3). This means that the MLF won’t help push Muni yields lower from current levels. Despite the MLF’s shortcomings, we stick with our overweight allocation to municipal bonds. For one thing, federal assistance to state & local governments will be included in the forthcoming stimulus bill. The Fed will also feel increased pressure to reduce MLF pricing the longer the passage of that bill is delayed. Further, while the budget pressure facing municipal governments is immense, states hold very high rainy day fund balances (bottom panel). This will help cushion the blow and lessen the risk of ratings downgrades. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve bull flattened in July. The 2/10 and 5/30 Treasury slopes flattened 6 bps and 13 bps, reaching 44 bps and 99 bps, respectively. Unusually, the bull flattening of the Treasury curve that occurred last month was not the result of a deflationary market environment. Rather, the inflation compensation curve bear flattened – the 2-year and 10-year CPI swap rates increased 25 bps and 16 bps, respectively – while the real yield curve underwent a large parallel shift down. It will be difficult for the nominal yield curve to keep flattening if this reflationary back-drop continues. Eventually, rising inflation expectations will pull up real yields at the long-end of the curve. For this reason, we retain our bias toward duration-neutral yield curve steepeners on a 6-12 month horizon. Specifically, we advise going long the 5-year bullet and short a duration-matched 2/10 barbell. In a recent report we noted that valuation is a concern with this positioning.11 The 5-year yield is below the yield on the duration-matched 2/10 barbell (Chart 7), and the 5-year bullet looks expensive on our yield curve models (Appendix B). However, the 5-year bullet traded at much more expensive levels during the last zero-lower-bound period between 2010 and 2013 (bottom panel). With short rates once again pinned at zero, we expect the 5-year to once again hit extreme levels of overvaluation. TIPS: Overweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 95 basis points in July, bringing year-to-date excess returns up to -309 bps. The 10-year TIPS breakeven inflation rate rose 21 bps on the month to hit 1.56%. The 5-year/5-year forward TIPS breakeven inflation rate rose 18 bps on the month to hit 1.71%. TIPS breakeven inflation rates have moved up rapidly during the past couple of months, and the 10-year breakeven is now within 6 bps of the fair value reading from our Adaptive Expectations Model (Chart 8).12 TIPS will soon turn expensive if current trends continue. That is, unless stronger CPI inflation sends our model's fair value estimate higher. We place strong odds on the latter occurring. Month-over-month core CPI bottomed in April, as did the oil price. In addition, trimmed mean inflation measures suggest that core has room to play catch-up (panel 3). As mentioned on page 1, we continue to recommend real yield curve steepeners as a way to take advantage of the ongoing reflation trade. With the Fed now targeting a temporary overshoot of its 2% inflation goal, we would expect the cost of 2-year inflation protection to eventually trade above the cost of 10-year inflation protection (panel 4). With the Fed also keeping a firmer grip over short-dated nominal yields than over long-dated ones, this means that short-maturity real yields will come under downward pressure relative to the long-end (bottom panel).13 ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 25 basis points in July, bringing year-to-date excess returns up to +23 bps. Aaa-rated ABS outperformed the Treasury benchmark by 15 bps on the month, bringing year-to-date excess returns up to +22 bps. Non-Aaa ABS outperformed by 111 bps, bringing year-to-date excess returns up to +22 bps. Aaa ABS are a high conviction overweight, given that spreads remain elevated compared to historical levels and that the sector benefits from Fed support through the Term Asset-Backed Securities Loan Facility (TALF). However, spreads are even more attractive in non-Aaa ABS (Chart 9) and we recommend owning those securities as well. This is despite the fact that only Aaa-rated bonds are eligible for TALF. We explained our rationale for owning non-Aaa consumer ABS in a recent report.14 We noted that the stimulus received from the CARES act caused real personal income to increase significantly during the past four months and, faced with fewer spending opportunities, households used that windfall to pay down consumer debt (bottom panel). Granted, further fiscal stimulus is needed to sustain recent income gains. But we expect the follow-up stimulus bill to be passed soon. Our Geopolitical Strategy service has shown that the new bill will likely contain sufficient income support for households.15 Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 112 basis points in July, bringing year-to-date excess returns up to -395 bps. Aaa CMBS outperformed Treasuries by 43 bps on the month, bringing year-to-date excess returns up to -111 bps. Non-Aaa CMBS outperformed by 256 bps, bringing year-to-date excess returns up to -1042 bps (Chart 10). We continue to recommend an overweight allocation to Aaa non-agency CMBS and an underweight allocation to non-Aaa CMBS. Our reasoning is simple. Aaa CMBS are eligible for TALF, meaning that spreads can still tighten even as the hardship in commercial real estate continues. Without Fed support, non-Aaa CMBS will struggle as the delinquency rate continues to climb (panel 3).16 Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 17 basis points in July, bringing year-to-date excess returns up to -42 bps. The average index spread tightened 5 bps on the month to 72 bps, still well above typical historical levels (bottom panel). The Fed is supporting the Agency CMBS market by directly purchasing the securities as part of its Agency MBS purchase program. The combination of strong Fed support and elevated spreads makes the sector a high conviction overweight. Appendix A: Buy What The Fed Is Buying The Fed rolled out a number of aggressive lending facilities on March 23. These facilities focused on different specific sectors of the US bond market. The fact that the Fed has decided to support some parts of the market and not others has caused some traditional bond market correlations to break down. It has also led us to adopt of a strategy of “Buy What The Fed Is Buying”. That is, we favor those sectors that offer attractive spreads and that benefit from Fed support. The below Table tracks the performance of different bond sectors since the March 23 announcement. We will use this to monitor bond market correlations and evaluate our strategy’s success. Table Performance Since March 23 Announcement Of Emergency Fed Facilities

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of July 31, 2020)

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of July 31, 2020)

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 57 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 57 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of July 31, 2020)

A Different Kind Of Reflation Trade

A Different Kind Of Reflation Trade

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “The Case Against The Money Supply”, dated June 30, 2020, available at usbs.bcaresearch.com 2 For our outlook on Energy bonds please see US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 1: A Model Of Energy Bond Excess Returns”, dated July 14, 2020 and US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 2: Buy The Dip In High-Yield Energy”, dated July 21, 2020, available at usbs.bcaresearch.com 3 Please see US Bond Strategy Weekly Report, “Take A Look At High-Yield Technology Bonds”, dated June 23, 2020, available at usbs.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “Assessing Healthcare & Pharma Bonds In A Pandemic”, dated June 9, 2020, available at usbs.bcaresearch.com 5 We assume a 25% recovery rate and target a spread of 150 bps in excess of default losses. For more details on this calculation please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com 6 Please see US Bond Strategy Weekly Report, “Take A Look At High-Yield Technology Bonds”, dated June 23, 2020, available at usbs.bcaresearch.com 7 Please see US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 1: A Model Of Energy Bond Excess Returns”, dated July 14, 2020 and US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 2: Buy The Dip In High-Yield Energy”, dated July 21, 2020, available at usbs.bcaresearch.com 8 Please see US Bond Strategy Weekly Report, “Assessing Healthcare & Pharma Bonds In A Pandemic”, dated June 9, 2020, available at usbs.bcaresearch.com 9 Please see US Bond Strategy Weekly Report, “The Treasury Market Amid Surging Supply”, dated May 12, 2020, available at usbs.bcaresearch.com 10 Please see US Bond Strategy Weekly Report, “Bonds Are Vulnerable As North America Re-Opens”, dated May 26, 2020, available at usbs.bcaresearch.com 11 Please see US Bond Strategy Weekly Report, "Take A Look At High-Yield Technology Bonds”, dated June 23, 2020, available at usbs.bcaresearch.com 12 For more details on our model please see US Bond Strategy Weekly Report, “How Are Inflation Expectations Adapting?”, dated February 11, 2020, available at usbs.bcaresearch.com 13 For more details on our recommended real yield curve steepener trade please see US Bond Strategy Weekly Report, “Negative Oil, The Zero Lower Bound And The Fisher Equation”, dated April 28, 2020, available at usbs.bcaresearch.com 14 Please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com 15 Please see Geopolitical Strategy Weekly Report, “A Tech Bubble Amid A Tech War (GeoRisk Update)”, dated July 31, 2020, available at gps.bcaresearch.com 16 We discussed our CMBS outlook in more detail in US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

Markets have shrugged off the rise in COVID-19 cases in the US and new clusters in other places such as Spain, Hong Kong, Melbourne, and Tokyo (Chart 1). The MSCI All-Country World Index is now only 4% off its all-time high in February. We don’t see the markets ignoring reality for much longer. Economic activity remains very subdued (Chart 2), which will eventually cause a significant rise in bankruptcies and problems for banks. Nevertheless, the unprecedented monetary and fiscal stimulus will be increased further in coming weeks, which should prevent a big shift towards pessimism for a while. The crunch time will come in the northern-hemisphere winter, when COVID cases in North America and Europe are likely to rise sharply again. Risk assets at their current levels are not pricing in those risks. Recommended Allocation

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Chart 1COVID Cases Are Still On The Rise

COVID Cases Are Still On The Rise

COVID Cases Are Still On The Rise

Chart 2Activity Remains Subdued

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Markets are driven by the second derivative of growth. It is not surprising, then, that equities began to rally in March, exactly when economic data stopped deteriorating, even though it remained atrocious (Chart 3). Real interest rates have also continued to fall, even as risk assets rallied; this further fueled the rally, since the theoretical value of equities rises as the rate at which they are discounted falls (Chart 4). Chart 3Data Stopped Deteriorating In March

Data Stopped Deteriorating In March

Data Stopped Deteriorating In March

Chart 4Real Interest Rates Have Continued To Fall

Real Interest Rates Have Continued To Fall

Real Interest Rates Have Continued To Fall

But the question now is: Can the data continue to improve? PMIs will fall back towards 50, and economic releases are unlikely to surprise so strongly on the upside. In the US, as a result of the rise in COVID-19 cases and renewed (albeit mostly moderate) government restrictions on activity, consumer confidence has started to weaken again and initial unemployment claims to pick up (Charts 5 and 6). Even though the Fed will remain ultra-dovish, real rates will not fall much further from their current level, which is the lowest since TIPS started trading in the late 1990s. Chart 5Consumer Confidence Is Weakening Again

Consumer Confidence Is Weakening Again

Consumer Confidence Is Weakening Again

Chart 6The Jobs Market Has Stopped Improving

The Jobs Market Has Stopped Improving

The Jobs Market Has Stopped Improving

Chart 7Will Money Supply Growth Peak?

Will Money Supply Growth Peak?

Will Money Supply Growth Peak?

Money supply growth has grown rapidly, as a result of the increase in central-bank balance-sheets and the rush of companies to borrow to shore up their cash positions (Chart 7). The increase in excess liquidity has also been a force behind the rise in risk assets. But money supply growth is likely to slow from now. At least partly offsetting these risks will be further fiscal stimulus. BCA Research’s Geopolitical strategists see Congress approving a big new package of around $2.5 trillion, mainly because of widespread popular support for an extension of more generous unemployment benefits (Table 1). Agreement should come before the scheduled recess on August 10 (if it doesn’t, this would trigger a market selloff). The recent agreement between European Union leaders on a EUR750 billion fiscal package was a major breakthrough, since it represented joint borrowing backed by the rich northern European countries to provide transfers to the poorer periphery. Table 1There Is Much Public Support For Fiscal Stimulus

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Further upside may come as the many investors who have missed the rally since March capitulate and buy risk assets. Investor sentiment is currently unusually polarized. Speculative individuals and hedge funds are very bullish (Chart 8). But more conservative pension funds, wealth managers, and individual investors, mostly remain cautious, as evidenced by the AAII weekly survey, in which many more investors say they expect the stock market to fall over the next six months than to rise (Chart 9). Cash levels remain high by historical standards (Chart 10). Although only a minority of investors turned positive in March, a recent academic study demonstrated how hedge funds and small active institutions have a disproportionate influence on price movements (Chart 11). A downside risk, then, would be if these investors decided to take profits or turned more bearish. Chart 8Hedge Funds Are Bullish...

Hedge Funds Are Bullish...

Hedge Funds Are Bullish...

Chart 9...But Retail Investors Very Cautious

...But Retail Investors Very Cautious

...But Retail Investors Very Cautious

Chart 10Cash Holdings Remain Elevated

Cash Holdings Remain Elevated

Cash Holdings Remain Elevated

Chart 11Some Smaller Investors Have A Big Impact

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

We have argued, since the pandemic began, that investors should not take high-conviction bets in such an uncertain environment. They should, rather, design portfolios which are robust under various scenarios. After the 43% rise in global equities since March, we cannot recommend an above-benchmark weighting, since downside risks are not priced in. We remain neutral on global equities. However, fixed-income instruments look even more unattractive at the current low level of rates; we remain underweight. We recommend hedging via a large overweight in cash, which leaves dry powder for when a better buying opportunity arises. Currencies: A key (as always) to the macro view is what happens to the US dollar. Many of the drivers of the dollar – interest-rate differentials, valuation, momentum, and relative money-supply growth – point to it weakening further (Chart 12). The trade-weighted dollar is already off 9% from its March peak. We turned bearish on the USD in our Quarterly published at the beginning of July. It is too early, however, to declare that the dollar bull market, which began in 2012, is definitely over. Chart 12Dollar Indicators Are Bearish...

Dollar Indicators Are Bearish...

Dollar Indicators Are Bearish...

Chart 13…But Short USD Is Now A Consensus

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

A new downturn in the global economy would push the dollar back up again, since it is a safe-haven currency. Shorting the dollar, especially against the euro, is now a consensus position, and so a near-term reversal is quite likely (Chart 13). But, over the next 12-18 months, a move above 1.22 for the euro and towards 100 for the yen is possible. We will continue to analyze whether the dollar could be entering a bear market, since this would necessarily make us more structurally positive on commodities and emerging markets. Equities: A pickup in global growth and a weakening US dollar might prove positive for cyclicals and value stocks in the long run, which would cause European and EM equities to outperform. Given the current uncertainty, however, we cannot recommend that stance and therefore continue to prefer “growth defensives” such as Health Care and Technology, which implies an overweight on the overall US market. Valuations in the Health Care sector remain attractive (Chart 14). Companies in the (broadly defined) Tech sector are beneficiaries of the pandemic, generally have robust balance-sheets, and should continue to see strong earnings growth for some years. And, while Technology is clearly expensive, valuations are still nowhere as excessive as in 2000 (Chart 15). For Tech to crash would require either that it go ex-growth, or that there is significant regulatory action. Chart 14Health Care Still Attractively Valued

Health Care Still Attractively Valued

Health Care Still Attractively Valued

Chart 15Tech Still Way Below Bubble Levels

Tech Still Way Below Bubble Levels

Tech Still Way Below Bubble Levels

Chart 16Europe No Longer So Dominated By Financials

Europe No Longer So Dominated By Financials

Europe No Longer So Dominated By Financials

Neither of these seems likely for now. Euro zone equities are less dominated than they were by Financials, but remain more cyclical than the US, with very few internet-related names (Chart 16). Fixed Income: Central banks will remain very dovish and, as Fed chair Jerome Powell has emphasized, are not even thinking about thinking about tightening policy. This suggests that nominal rates will rise only moderately, even if growth continues to pick up. The Fed still has plenty of room to ease further if needed, since the programs it rolled out in March have barely been taken up yet (Table 2). We thus recommend a neutral position on duration. We find TIPS attractive as a hedge against an eventual spike in inflation. The 10-year breakeven inflation rate implied in TIPS remains around 100 basis points below being compatible with the Fed achieving its 2% PCE inflation target in the long run (Chart 17). The announcement in September of the results of the Fed’s 18-month review of its policy framework, which is likely to intensify its efforts to achieve the inflation target, could push breakevens up a bit further. In credit, we continue to recommend buying whatever central banks are buying, mostly investment-grade corporate bonds and the top end of the US junk bond market. Though spreads have fallen a long way, they are still well above end-2019 levels, and look attractive in a world of such low government bond yields (Chart 18). Table 2Usage Of The 2020 Federal Reserve Emergency Lending Facilities

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Chart 17TIPS Still Pricing Low Inflation For A Decade

TIPS Still Pricing Low Inflation For A Decade

TIPS Still Pricing Low Inflation For A Decade

Chart 18Credit Spreads Could Fall Further

Credit Spreads Could Fall Further

Credit Spreads Could Fall Further

Commodities: The weakening US dollar and continued expansion of Chinese stimulus (Chart 19) should be positive for industrial metals prices over the next six to nine months. Oil prices also have some further upside, since the OPEC 2.0 agreement to restrict supply is being adhered to, and demand will gradually pick up (although air travel will remain depressed, more commuters are using their cars as they avoid public transport). BCA Research’s Energy Service forecasts Brent crude to average $44 in the second half of this year, and $65 in 2021 (up from the current $43). Gold has already run up a lot and is now close to a record high price in real terms, with sentiment very optimistic (Chart 20). Chart 19China Stimulus Positive For Metals

China Stimulus Positive For Metals

China Stimulus Positive For Metals

Nonetheless, in an environment of very low real rates, it represents a good hedge against extreme tail risks, and therefore we continue to recommend a moderate position as an insurance. Chart 20Gold Looking Rather Toppish

Gold Looking Rather Toppish

Gold Looking Rather Toppish

Garry Evans, Senior Vice President Global Asset Allocation garry@bcaresearch.com Recommended Asset Allocation

BCA Research's Global Fixed Income Strategy service recommends investors underweight German, French, the British, Swedish and Japanese sovereign markets versus the US in USD-hedged portfolios, because both their unhedged and USD-hedged yields are below…

Highlights The Fed’s emergency lending facilities have successfully stabilized markets … : Credit spreads have tightened dramatically since March and liquidity has been restored to the US Treasury market. … at very little cost to the central bank: Just the announcement of Fed lending facilities has been enough to push spreads lower in most cases. The facilities themselves have seen very little actual uptake. The only cost borne by the Fed has been a dramatic expansion of its balance sheet due to purchases of Treasury securities. We still want to “buy what the Fed is buying”: In US fixed income, we want to favor those sectors that are eligible for Fed support. This includes corporate bonds rated Ba and higher, municipal bonds and Aaa-rated securitizations. Keep portfolio duration at neutral: The Fed will be much more cautious about raising interest rates than in the past, and could wait until inflation is above its target before lifting off zero. Feature Back in April, we published a detailed explainer of the extraordinary actions taken by the Federal Reserve to combat the pandemic-induced recession.1 This week, we re-visit that Special Report to assess what the Fed has accomplished during the past three months and to speculate about what lies ahead. Overall, the Fed’s response has been highly effective. Stability was restored to financial markets almost immediately after the most dramatic policy interventions were announced, and it turns out that the announcements themselves did most of the work. The ultimate usage of the Fed’s Section 13(3) emergency lending facilities has been extremely low relative to their stated maximum capacities (Table 1). If you are the Fed, it is apparently enough to marshal overwhelming force and announce your willingness to deploy it. Like the ECB demonstrated in the fraught Eurozone summer of 2012, a bazooka can restore order without being fired.2 Table 1Usage Of The 2020 Federal Reserve Emergency Lending Facilities

Alphabet Soup, Part 2: Shocked And Awed

Alphabet Soup, Part 2: Shocked And Awed

The only possible cost borne by the Fed has been an explosion in the size of its balance sheet, mostly attributable to purchases of Treasury securities. The ultimate usage of the Fed’s facilities has been extremely low relative to their stated maximum capacities. This report looks at how the Fed’s actions have influenced (and will influence) interest rates, Treasury market liquidity, the corporate bond market and other fixed income spread products. It also considers the potential impact of the size of the Fed’s balance sheet on the economy and financial markets. Interest Rates The Fed dropped the funds rate to a range of 0% to 0.25% on March 15, and since then it has aggressively signaled that rates will stay pinned at the zero-lower-bound for a long time. Investors quickly took this message on board (Chart 1). The median estimate from the New York Fed’s Survey of Market Participants has the funds rate holding steady at least through the end of 2022. Meanwhile, the overnight index swap curve isn’t pricing-in a rate hike until 2024. Chart 1The Fed And Market Agree: No Hikes Through 2022

The Fed And Market Agree: No Hikes Through 2022

The Fed And Market Agree: No Hikes Through 2022

Chart 2Better Signaling From The Fed

Better Signaling From The Fed

Better Signaling From The Fed

The market adjusted much more quickly to the Fed’s zero interest rate policy this year than it did during the last zero-lower-bound episode (Chart 2). The MOVE index of Treasury yield volatility has already plunged to below 50. It took several years for it to reach those levels after the Fed cut rates to zero at the end of 2008. Similarly, the yield curve is much flatter today than it was during the last zero-lower-bound episode. This partly reflects the market’s expectation that rates will stay at zero for longer and partly the downward revisions to estimates of the long-run neutral fed funds rate that have occurred during the past few years. The bottom line is that the Fed has successfully achieved its goal on interest rate policy. The funds rate is at its effective lower bound and the entire term structure is priced for it to stay there for a very long time. There are two main reasons for this success. First, the Fed’s forward guidance has been more dovish this year than at any point during the last zero-lower-bound episode, with many FOMC participants calling for the Fed to target a temporary overshoot of the 2% inflation target. Second, the market is more skeptical about inflation ever returning to that target, as evidenced by much lower long-dated inflation expectations (Chart 2, bottom panel). What’s Next? The Fed has already made it clear that it won’t pursue negative interest rates. With those off the table, the next step will be for the Fed to make its forward rate guidance more explicit. In all likelihood this will involve the return of some form of the Evans Rule that was in place between 2012 and 2014. The Evans Rule was a commitment to not lift rates at least until the unemployment rate moved below 6.5% or inflation moved above 2.5%.3 The new version of the Evans Rule will be much more dovish. In a recent speech, Governor Lael Brainard favorably cited research suggesting that the Fed should refrain from liftoff until inflation reaches the 2% target.4 That may very well be the rule that ends up becoming official Fed guidance. If the Fed wants to strengthen its commitment to low rates even more, it could follow the Reserve Bank of Australia’s lead and implement a Yield Curve Control policy. This policy would involve setting caps for Treasury yields out to a 2-year or 3-year maturity. The Fed would pledge to buy as many securities as necessary to enforce the caps and would only lift the caps when the criteria of its new Evans Rule are met. While spreads have tightened across all credit tiers, investment grade corporates have become much more expensive than high-yield. For the time being, there is no rush for the Fed to deliver more explicit forward guidance and/or Yield Curve Control. As we noted above, bond yields are already pricing-in an extremely lengthy period of zero rates. But these policies will become more important as the economic recovery progresses and market participants start to speculate about an eventual exit from the zero bound. Explicit forward guidance and/or Yield Curve Control would then prevent a premature rise in bond yields and tightening of financial conditions. With all that in mind, we would not be surprised to see more explicit (Evans Rule-style) forward guidance rolled out at some point this year, but unless bonds sell off significantly beforehand, it probably won’t have an immediate impact on yields. The same is true for Yield Curve Control, though the odds of that being announced this year are lower as it is a tool with which the Fed is less comfortable. Treasury Market Liquidity Chart 3When Treasury Market Liquidity Evaporated

When Treasury Market Liquidity Evaporated

When Treasury Market Liquidity Evaporated

As the COVID-19 crisis flared in March, there were several tense days when liquidity in the US Treasury market evaporated. Bond yields jumped even as the equity market plunged (Chart 3). Meanwhile, liquidity markers showed that it had become much more difficult to transact in US Treasuries. Treasury Bid/Ask spreads widened dramatically and the iShares 20+ Year Treasury ETF (TLT) traded at a huge discount to its net asset value (Chart 3, panel 3). During the past four months, researchers have identified hedge fund selling of Treasuries to meet margin calls and foreign bank selling of Treasuries to meet demands for US dollar funding as the proximate causes of March’s Treasury rout. However, it is clearly a failure of market structure that the Treasury market was unable to accommodate that selling pressure without liquidity disappearing. In a recent paper from The Brookings Institution, Darrell Duffie explains why the Treasury market was unable to maintain its liquidity during this tumultuous period.5 Essentially, he argues that it is the combination of rising Treasury supply and post-2008 regulations imposed on dealer banks that has led to an environment where there is a large and growing amount of Treasury supply, but where dealers have less balance sheet capacity to intermediate trading. To illustrate, Chart 4 shows the ratio between the outstanding supply of Treasury securities and the quantity of Treasury inventories for which primary dealers obtained financing. Quite obviously, the dealers’ intermediation activities have not kept pace with the expanding size of the market. Chart 4Primary Dealers Have Not Kept Up With Treasury Issuance

Primary Dealers Have Not Kept Up With Treasury Issuance

Primary Dealers Have Not Kept Up With Treasury Issuance

What’s Next? Without changes to Treasury market structure or bank capital requirements (Duffie recommends abandoning the system of competing dealer banks altogether and moving all Treasury trades through one central clearinghouse), we are likely to see more episodes like March where a spate of Treasury selling leads to an evaporation of market liquidity. When that happens, the Fed will be forced to step in and buy Treasuries, as it did in March (Chart 3, bottom panel). The goal of that intervention is simply to remove enough supply from the market so that the remaining trading volume can be handled by the dealers. As this pattern repeats itself over time, it will cause the Fed’s presence in the Treasury market to grow. Bottom Line: Unless structural changes are made to the Treasury market or bank capital regulations are rolled back, we should expect more episodes of Treasury market illiquidity like we saw in March. We should also expect the Fed to respond to those episodes with aggressive Treasury purchases, and for the Fed’s presence in the Treasury market to grow over time. Corporate Bonds The Fed’s intervention in the corporate bond market consists of three lending facilities: The Secondary Market Corporate Credit Facility (SMCCF) where the Fed purchases investment grade corporate bonds and recent Ba-rated fallen angels in the secondary market. This facility also purchases investment grade and high-yield ETFs. The Primary Market Corporate Credit Facility (PMCCF) where the Fed buys new issuance from investment grade-rated issuers (and recent fallen angels) in the primary market. The Main Street Lending Facility (MSLF) where the Fed purchases loans off of bank balance sheets. The loans must be made to small or medium-sized firms with Debt-to-EBITDA ratios below 6.0. Chart 5Corporate Issuance Surged Following The Fed's Announcements

Corporate Issuance Surged Following The Fed's Announcements

Corporate Issuance Surged Following The Fed's Announcements

As mentioned above, these facilities have barely been tapped. As of July 1, the Fed had purchased $1.5 billion of corporate bonds and just under $8 billion of ETFs through the SMCCF, while the PMCCF had not been used at all. However, the impact of the Fed’s promise to back-stop such a large portion of the corporate debt market has been immense. Corporate bond issuance surged following the announcement of the Fed’s facilities, and set monthly post-2008 records in March, April and May (Chart 5). The effect on corporate bond spreads has been just as dramatic. Spreads peaked on March 23, the day that the SMCCF and PMCCF were announced, and have tightened significantly since then. Further underscoring the importance of the SMCCF, PMCCF and MSLF announcements is that those segments of the corporate bond market most likely to have access to the Fed’s lending facilities have seen the most spread compression. Recall that investment grade issuers and recent fallen angels have access to the SMCCF and PMCCF, while the MSLF will benefit most issuers rated Ba or higher. Some B-rated issuers are able to tap the MSLF, but not the majority. Issuers rated Caa or below are much less likely to benefit from any of the Fed’s programs. Table 2 shows how the impact of the Fed’s facilities has played out across the different corporate credit tiers. It shows each credit tier’s option-adjusted spread and 12-month breakeven spread as of March 23 and today. It also shows the percentile rank of those spreads since 2010 (100% indicating the widest spread since 2010 and 0% indicating the tightest). While spreads have tightened across all credit tiers, investment grade corporates have become much more expensive than high-yield. The B-rated and below credit tiers are particularly cheap, with 12-month breakeven spreads all above their 80th percentiles since 2010. Table 2The Fed's Impact On Corporate Spreads

Alphabet Soup, Part 2: Shocked And Awed

Alphabet Soup, Part 2: Shocked And Awed

Chart 6Spread Curve Back To Normal

Spread Curve Back To Normal

Spread Curve Back To Normal

The market impact of the Fed’s corporate lending facilities is also apparent across the corporate bond term structure. In March, the investment grade corporate bond spread slope inverted, as 1-5 year maturity corporate bond spreads widened relative to spreads of securities with more than 5 years to maturity (Chart 6).6 The Fed concentrated its lending facilities on securities with less than 5 years to maturity, and it has successfully re-steepened the corporate spread curve. But the Fed’s corporate lending facilities are not all powerful. As Chair Powell likes to say: “the Fed has lending powers, not spending powers”. So while the promise of Fed lending is a big help, it still means that troubled firms will have to increase their debt loads to survive the economic downturn. Those firms that take on debt may still see their credit ratings downgraded as their balance sheet health deteriorates. Indeed, this is exactly what has happened. Ratings downgrades have jumped during the past few months, as have defaults (Chart 7). There has also been a spike in the number of fallen angels – firms downgraded out of investment grade – but not as big a jump as was seen during the last recession (Chart 7, panel 2). The Fed’s emergency lending facilities have likely prevented some downgrades, but not all. Chart 7Fed Can't Prevent Downgrades

Fed Can't Prevent Downgrades

Fed Can't Prevent Downgrades

What’s Next? The Fed’s lending facilities are responsible for a huge portion of the spread compression we’ve seen since late March. That said, it is a potential problem for corporate bonds that those facilities are scheduled to expire at the end of September. Our sense is that the expiry date will be extended, and that the facilities will only be wound down after a significant period of time where they see zero usage. At that point, the Fed should be able to halt the facilities without unduly impacting markets. In terms of investment implications, we think that the Fed’s back-stop will continue to be the most important driver of corporate bond spreads during the next few months. This means we would avoid chasing the attractive valuations in bonds rated B & below, and would continue to focus our corporate bond exposure on bonds rated Ba and above. We make an exception to our “buy what the Fed is buying” rule when it comes to positioning across the corporate bond term structure. Here, we are inclined to grab the extra spread offered by longer-maturity securities even though Fed secondary market purchases are concentrated at the front-end. Our rationale is that the Fed’s secondary market purchases are already low and will likely decline as time goes on. Meanwhile, if firms with long-maturity debt outstanding need help they can still access the PMCCF if needed. Other Fed Lending Facilities & Fixed Income Sectors Outside of the three programs geared toward the corporate bond market, the Fed also rolled out emergency lending facilities meant to back-stop: money market mutual funds (MMLF), the commercial paper market (CPFF), the asset-backed securities market (TALF), the municipal bond market (MLF) and the federal government’s new Paycheck Protection Program (PPPLF). Once again, the announcement effect did most of the work for all of these facilities and the Fed managed to quickly restore stability to each targeted market without doing much actual lending. For starters, the MMLF successfully halted a flight out of prime money market funds with a relatively modest $53 billion in loans (Chart 8). The CPFF caused the commercial paper/T-bill spread to normalize with only $4 billion of lending, and the LIBOR/OIS spread also tightened soon after the Fed rolled out its facilities (Chart 8, bottom panel). The Fed has dramatically expanded the size of its balance sheet through purchases of Treasury securities and agency MBS. In the asset-backed securities market, the Fed decided that only Aaa-rated securitizations are eligible for TALF. With that in mind, Aaa-rated consumer ABS and CMBS spreads have tightened considerably since TALF’s announcement (Chart 9). Non-Aaa consumer ABS spreads have tightened modestly despite the lack of Fed support. This is because fiscal stimulus has, so far, kept households flush with cash and prevented a wave of consumer bankruptcies. Non-Aaa CMBS, on the other hand, have struggled due to lack of Fed support and a sharp increase in commercial real estate delinquencies. Chart 8Stability Restored

Stability Restored

Stability Restored

Chart 9Consumer ABS & CMBS Spreads Tightened Considerably...

Consumer ABS & CMBS Spreads Tightened Considerably...

Consumer ABS & CMBS Spreads Tightened Considerably...

The announcement of the MLF also successfully led to compression in municipal bond spreads (Chart 10), though the Aaa muni curve still trades cheap relative to Treasuries. Like the other facilities, the MLF has seen very low take-up. In this instance, low MLF usage results from its expensive pricing. Municipal governments can access loans through the MLF for a period of up to three years at a cost of 3-year OIS plus a fixed spread that varies depending on the municipality’s credit rating. However, current market pricing is well below the MLF rate for all credit tiers (Chart 10, bottom 2 panels). This means that the MLF provides a nice back-stop in case muni spreads widen again, but it is not currently an effective means of getting cash to struggling state & local governments. Chart 10...As Have Municipal Bond Spreads

...As Have Municipal Bond Spreads

...As Have Municipal Bond Spreads

Finally, the PPPLF is a facility that purchases loans made through the Paycheck Protection Program (PPP) off of bank balance sheets. Essentially, it is an insurance policy designed to make sure that banks have the necessary balance sheet capacity to deliver all of the PPP loans authorized by Congress. It has achieved this goal with relatively little usage. Banks have doled out more than $500 billon of PPP loans and the Fed has purchased only $68 billion. What’s Next? As with the corporate lending facilities discussed above, there is a risk surrounding the scheduled expiry of these other lending facilities at the end of September. Once again, we see the Fed being very cautious in this regard. All facilities will be extended until they have seen long periods of no usage. In the near-term, we think it’s possible that the Fed will make MLF loans cheaper. They will likely feel intense pressure to do so if Congress fails to pass sufficient stimulus to state & local governments in the next bailout package. In terms of investment strategy, we want to stick with what has worked so far. We are overweight Aaa consumer ABS and Aaa CMBS due to the TALF back-stop. We are also overweight municipal bonds, especially in the Aaa-rated space where yields are attractive versus Treasuries and the risk of default is low. We would also advise taking some extra risk in non-Aaa consumer ABS. These securities have no TALF back-stop, but we expect Congress to deliver enough government stimulus to keep the underlying borrowers solvent. The Size Of The Fed’s Balance Sheet As this report has made clear, the Fed’s emergency lending facilities have accomplished a lot during the past four months with the Fed taking very little actual risk onto its balance sheet. But while its usage of the emergency lending facilities has been low, the Fed has dramatically expanded the size of its balance sheet through purchases of Treasury securities and agency MBS. To restore stability to the Treasury and MBS markets, the Fed avidly bought Treasuries and agency MBS from mid-March to mid-April, ballooning the size of its balance sheet by $2 trillion in just five weeks. Tacked onto the QE programs undertaken to battle the GFC, the Fed’s balance sheet expansion has been massive, and it is roughly six times larger as a share of GDP than it was in the three decades preceding the subprime crisis (Chart 11). Chart 11Massive Expansion Of The Fed's Balance Sheet

chart 11

Massive Expansion Of The Fed's Balance Sheet

Massive Expansion Of The Fed's Balance Sheet

Investors and citizens may ask what that balance sheet expansion has achieved so far, and what it’s likely to achieve going forward. Are there unintended consequences that haven’t yet made their presence felt? What constitutes a normalized Fed balance sheet, and when will the Fed be able to get back to it? The immediate consequence many investors attribute to the balance sheet expansion is higher stock prices (Chart 12). Fans of the balance sheet/equities link are undeterred by the decoupling after 2015, arguing that standing pat/tapering the balance sheet by 15% helped precipitate its vicious sell-off in the fourth quarter of 2018. It probably has not escaped their notice that the spectacular bounce from March’s lows has occurred alongside a 70% balance sheet expansion. The money supply boost may prove short-lived, though, as it appears that businesses are borrowing to ensure their continued liquidity, rather than to spend or invest. We don’t think there is much to the observed relationship, however. Correlation is not causation and we have a hard time seeing how the Fed’s purchases of Treasuries, agencies and agency MBS flowed into the equity market. While the Fed’s pre-pandemic QE purchases turbo-charged the size of the monetary base, it only gently expanded the money supply, because the banks that sold securities to the Fed largely handed the proceeds right back to it as deposits (Chart 13). The net effect mainly filled the Fed’s vaults with the new money it had conjured up via its open-market operations. Chart 12Fed Balance Sheet & Stock Prices: Correlation Is Not Causation

Fed Balance Sheet & Stock Prices: Correlation Is Not Causation

Fed Balance Sheet & Stock Prices: Correlation Is Not Causation

Chart 13Only A Modest Expansion Of Money Supply

Only A Modest Expansion Of Money Supply