Fixed Income

Highlights Recommended Allocation

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

The coronavirus pandemic is not over. Enormous fiscal and monetary stimulus will soften the blow to the global economy, but there remain significant risks to growth over the next 12 months. The P/E ratio for global equities is near a record high. This suggests that the market is pricing in a V-shaped recovery, and ignoring the risks. We can, therefore, recommend no more than a neutral position on global equities. But government bonds are even more expensive, with yields having largely hit their lower bound. Stay underweight government bonds, and hedge downside risk via cash. The US dollar is likely to depreciate further: It is expensive, US liquidity has risen faster than elsewhere, interest-rate differentials no longer favor it, and momentum has swung against it. A weakening dollar – plus accelerating Chinese credit growth – should help commodities. We raise the Materials equity sector to neutral, and put Emerging Market equities on watch to upgrade from neutral. Corporate credit selectively remains attractive where central banks are providing a backstop. We prefer A-, Baa-, and Ba-rated credits, especially in the Financials and Energy sectors. Defensive illiquid alternative assets, such as macro hedge funds, have done well this year. But investors should start to think about rotating into private equity and distressed debt, where allocations are best made mid-recession. Overview Cash Injections Vs. COVID Infections The key to where markets will move over the next six-to-nine months is (1) whether there will be a second wave of COVID-19 cases and how serious it will be, and (2) how much appetite there is among central banks and fiscal authorities to ramp up stimulus to offset the damage the global economy will suffer even without a new spike in cases. A new wave of COVID-19 in the northern hemisphere this fall and winter is probable. It is not surprising, after such a sudden stop in global activity between February and May, that economic data is beginning to return to some sort of normality. PMIs have generally recovered to around 50, and in some cases moved above it (Chart 1). Economic data has surprised enormously to the upside in the US, although it is lagging in the euro zone and Japan (Chart 2). Chart 1Data Is Rebounding Sharply

Data Is Rebounding Sharply

Data Is Rebounding Sharply

Chart 2US Data Well Above Expectations

US Data Well Above Expectations

US Data Well Above Expectations

New COVID-19 cases continue to rise alarmingly in some emerging economies and in parts of the US, but in Europe and Asia the pandemic is largely over (for now) and lockdown regulations are being eased, allowing economic activity to resume (Chart 3). Nonetheless, consumers remain cautious. Even where economies have reopened, people remain reluctant to eat in restaurants, to go on vacation, or to visit shopping malls (Chart 4). While shopping and entertainment activities are now no longer 70-80% below their pre-pandemic levels, as they were in April and May, they remain down 20% or more (Chart 5). Chart 3Few COVID-19 Cases Now In Europe And Asia

Few COVID-19 Cases Now In Europe And Asia

Few COVID-19 Cases Now In Europe And Asia

Chart 4Consumers Still Reluctant To Go Out

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Chart 5Spending Well Below Pre-Pandemic Levels

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

So how big is the risk of further spikes in COVID-19 cases? Speaking on a recent BCA Research webcast, the conclusion of Professor Peter Doherty, a Nobel prize-winning immunologist connected to the University of Melbourne, was that, “It’s not unlikely we’ll see a second wave.”1 But experts can’t be sure. It seems that the virus spreads most easily when people group together indoors. That is why US states where it is hot at this time of the year, such as Arizona, have seen rising infections. This suggests that a new wave in the northern hemisphere this fall and winter is probable. Offsetting the economic damage caused by the coronavirus has been the staggering amount of liquidity injected by central banks, and huge extra fiscal spending. Major central bank balance-sheets have grown by around 5% of global GDP since March, causing a spike in broad money growth everywhere (Chart 6). Fiscal spending programs also add up to around 5% of global GDP (Chart 7), with a further 5% or so in the form of loans and guarantees. Chart 6Remarkable Growth In Money Supply...

Remarkable Growth In Money Supply...

Remarkable Growth In Money Supply...

Chart 7...And Unprecedented Fiscal Spending

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

But is it enough? Considerable damage has been done by the collapse in activity. Bankruptcies are rising (Chart 8) and, with activity still down 20% in consuming-facing sectors, pressure on companies’ business models will not ease soon – particularly given evidence that banks are tightening lending conditions. Household income has been buoyed by government wage-replacement schemes, handout checks, and more generous unemployment benefits (Chart 9). But, when these run out, households will struggle if the programs are not topped up. Central banks are clearly willing to inject more liquidity if need be. But the US Congress is prevaricating on a second fiscal program, and the Merkel/Macron proposed EUR750 billion spending package in the EU is making little progress. It will probably take a wake-up call from a sinking stock market to push both to take action. Chart 8Companies Feeling The Pressure

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Considerable damage has been done by the collapse in activity. We lowered our recommendation for global equities to neutral from overweight in May. We are still comfortable with that position. Given the high degree of uncertainty, this is not a market in which to take bold positioning in a portfolio. When you have a high conviction, position your portfolio accordingly; but when you are unsure, stay close to benchmark. With stocks up by 36% since their bottom on March 23rd, the market is pricing in a V-shaped recovery and not, in our view, sufficiently taking into account the potential downside risks. P/E ratios for global stocks are at very stretched levels (Chart 10). Chart 9Households Dependent On Handouts

More Stimulus Forthcoming? Households Dependent On Handouts

More Stimulus Forthcoming? Households Dependent On Handouts

Chart 10Global Equities Are Expensive...

Global Equities Are Expensive...

Global Equities Are Expensive...

Nonetheless, we would not bet against equities. Simply, there is no alternative. Most government bond yields are close to their effective lower bound. Gold looks overbought (in the absence of a significant spike in inflation which, while possible, is unlikely for at least 12 months). No sensible investor in, say, Germany would want to hold 10-year government bonds yielding -50 basis points. Assuming 1.5% average annual inflation over the next decade, that guarantees an 18% real loss over 10 years. The only investors who hold such positions have them because their regulators force them to. Chart 11...But They Are Cheap Against Bonds

...But They Are Cheap Against Bonds

...But They Are Cheap Against Bonds

The Sharpe ratio on 10-year US Treasurys, which currently yield 70 BPs, will be 0.16 (assuming volatility of 4.5%) over the next 10 years. A simple calculation of the likely Sharpe ratio for US equities (earnings yield of 4.5% and volatility of 16%) comes to 0.28. One would need to assume a disastrous outlook for the global economy to believe that stocks will underperform bonds in the long run. Though equities are expensive, bonds are even more so. The equity risk premium in most markets is close to a record high (Chart 11). With such mathematics, it is hard for a long-term oriented investor to be underweight equities. Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Chart 12Premature Opening Of The Economy Is Risky

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

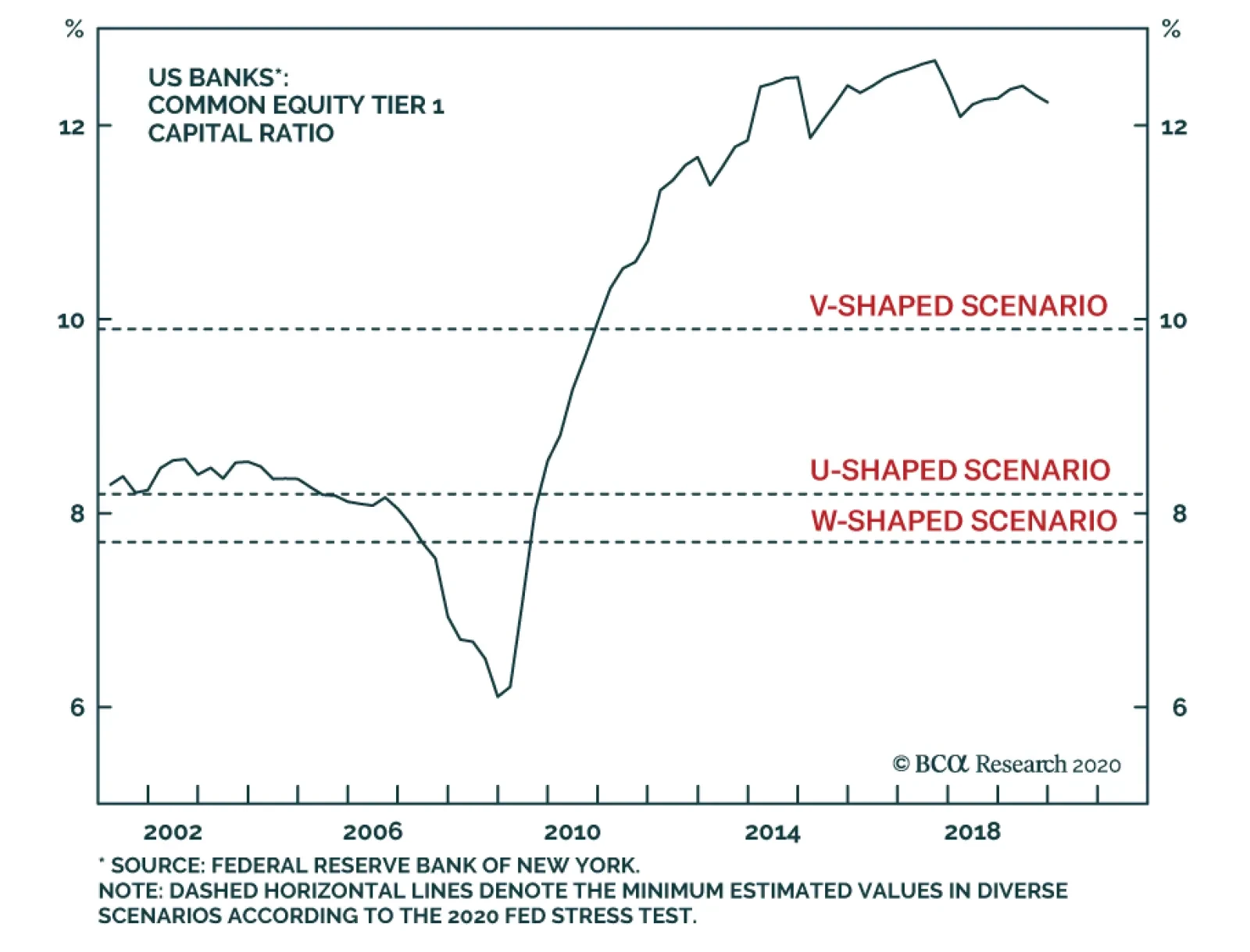

COVID-19: How Risky Is Reopening? Countries around the world are rushing to reopen their economies, claiming victory over the pandemic. It is hard to be sure whether a second wave of COVID-19 will hit. What is certain, however, is that a premature relaxation of measures is as risky as a tardy initial response. That was the lesson from our Special Report analyzing the Spanish Flu of 1918. The risk is certainly still there: Herd immunity will require around 70% of the population to get sick, and a drug or vaccine will (even in an optimistic scenario) not be available until early next year. China and South Korea, for example, after reporting only a handful of daily new cases in early May, were forced to impose new restrictions over the past few weeks as COVID-19 cases spiked again (Chart 12, panel 1). We await to see if other European countries, such as Italy, Spain, and France will be forced to follow. Some argue that even if a second wave hits, policy makers – to avoid a further hit to economic output – will favor the “Swedish model”: Relying on people’s awareness to limit the spread of the virus, without imposing additional lockdowns and restrictions. This logic, however, is risky since Sweden suffered a much higher number of infections and deaths than its neighboring countries (panel 2). The US faces a similar fate. States such as Florida, Arizona, and Texas are recording a sharp rise in new infections as lockdowns are eased. In panel 3, we show the daily number of new infections during the stay-at-home orders (the solid lines) and after they were lifted (dashed lines). To an extent, increases in infections are a function of mass testing. However, what is obvious is that the percentage of positive cases per tests conducted has started trending upwards as lockdown measures were eased (panel 4). Our base case remains that new clusters of infections will emerge. Eager citizens and rushed policy decisions will fuel further contagion. If the Swedish model is implemented, lives lost are likely to be larger than during the first wave. Chart 13W Or U, Says The OECD

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

What Shape Will The Recovery Be: U, V, W, Or Swoosh? The National Bureau of Economic Research (NBER) Business Cycle Dating Committee has already declared that the US recession began in March. The economists’ consensus is that Q2 US GDP shrank by 35% QoQ annualized. But, after such a momentous collapse and with a moderate move back towards normalcy, it is almost mathematically certain that Q3 GDP will show positive quarter-on-quarter growth. So does this mean that the recession lasted only one quarter, i.e. a sharp V-shape? And does this matter for risk assets? The latest OECD Economic Outlook has sensible forecasts, using two “equally probable” scenarios: One in which a second wave of coronavirus infections hits before year-end, requiring new lockdowns, and one in which another major outbreak is avoided.2 The second-wave scenario would trigger a renewed decline in activity around the turn of 2020-21: a W-shape. The second scenario looks more like a U-shape or swoosh, with an initial rebound but then only a slow drawn-out recovery, with OECD GDP not returning to its Q4 2019 level before the end of 2021 (Chart 13). Chart 14Unemployment Will Take A Long Time To Come Down

Unemployment Will Take A Long Time To Come Down

Unemployment Will Take A Long Time To Come Down

Why is it likely that, in even the absence of a renewed outbreak of the pandemic, recovery would be faltering? After an initial period in which many furloughed workers return to their jobs, and pent-up demand is fulfilled, the damage from the sudden stop to the global economy would kick in. Typically, unemployment rises rapidly in a recession, but recovers only over many years back to its previous low (Chart 14). This time, many firms, especially in hospitality and travel, will have gone bust. Capex plans are also likely to be delayed. Chart 15Sub-Potential Output Can Be Good For Risk Assets

Sub-Potential Output Can Be Good For Risk Assets

Sub-Potential Output Can Be Good For Risk Assets

However, a slow recovery is not necessarily bad for risk assets. Periods when the economy is recovering but remains well below potential (such as 2009-2015) are typically non-inflationary, which allows central banks to continue accommodation (Chart 15). Is This Sharp Equity Rebound A Retail Investor Frenzy? The answer to this question is both Yes and No. From a macro fundamental perspective, the answer is No, because coordinated global reflationary policies and medical developments to fight the coronavirus have been the key drivers underpinning this equity rebound. “COVID-on” and “COVID-off” have been the main determinants for equity rotations. Chart 16Active Retail Participation Lately

Retail Investors Have Driven Up Trading Volumes Active Retail Participation Lately

Retail Investors Have Driven Up Trading Volumes Active Retail Participation Lately

But at the individual stock level, the answer is Yes. Some of the unusual action in beaten-down stocks over the past few weeks may have its origin in an upsurge of active retail participation (Chart 16). Retail investors on their own are not large enough to influence the market direction. Many online brokerages do not charge any commission for trades, but make money by selling order flows to hedge funds. As such, the momentum set in motion by retail investors may have been amplified by fast-money pools of capital. Retail participation in some beaten-down stocks has also provided an opportunity for institutions to exit. BCA’s US Investment Strategy examined the change in institutional ownership of 12 stocks in three stressed groups between February 23 and June 14, as shown in Table 1. In the case of these stocks, retail investors have served as liquidity providers to institutional sellers seeking to exit their holdings. The redeployment of capital by institutions into large-cap and quality names may have pushed up the overall equity index level. Table 1Individuals Have Replaced Institutions

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

How Will Inflation Behave After COVID? Some clients have asked us about the behavior of inflation following the COVID epidemic. Over the very short term, inflation could have more downside. However, this trend is likely to reverse rapidly. Headline inflation is mainly driven by changes in the oil price and not by its level. Thus, even if oil prices were to stay at current low levels, the violent recovery of crude from its April lows could bring headline inflation near pre-COVID levels by the beginning of 2021 (Chart 17, top panel). This effect could become even larger if our Commodity strategist price target of 65$/barrel on average in 2021 comes to fruition. Chart 17Rising Oil Prices And Fiscal Stimulus Will Boost Inflation

Rising Oil Prices And Fiscal Stimulus Will Boost Inflation

Rising Oil Prices And Fiscal Stimulus Will Boost Inflation

But will this change in inflation be transitory or will it prove to be sustainable? We believe it will be the latter. The COVID crisis may have dramatically accelerated the shift to the left in US fiscal policy. Specifically, programs such as universal basic income may now be within the Overton window3 of acceptable fiscal policy, thanks to the success of the CARES Act in propping up incomes amid Depression-like levels of unemployment (middle panel). Meanwhile there is evidence that this stimulus is helping demand to recover rapidly: Data on credit and debit card trends show that consumer spending in the US has staged a furious rally, particularly among low-income groups, where spending has almost completely recovered (bottom panel). With entire industries like travel, restaurants and lodging destroyed for the foreseeable future, the political will to unwind these programs completely is likely to be very low, given that most policymakers will be queasy about an economic relapse, even after the worst of the crisis has passed. Such aggressive fiscal stimulus, coupled with extremely easy monetary policy will likely keep inflation robust on a cyclical basis. Global Economy Overview: March-May 2020 will probably prove to be the worst period for the global economy since the 1930s, as a result of the sudden stop caused by the coronavirus pandemic and government-imposed restrictions on movement. As the world slowly emerges from the pandemic, data has started to improve. But there remain many risks, and global activity is unlikely to return to its end-2019 level for at least another two years. That means that further fiscal and monetary stimulus will be required. The speed of the recovery will be partly determined by how much more aggressively central banks can act, and by how much appetite there is among fiscal authorities to continue to bail out households and companies which have suffered a catastrophic loss of income. US: The economy has shown signs of a strong rebound from the coronavirus slump in March and April. Q2 GDP probably fell around 35% quarter-on-quarter annualized, but Q3 will almost certainly show positive growth. The Economic Surprise Index (Chart 18, panel 1) has bounced to a record high, after stronger-than expected May data, for example the 16% month-on-month growth in durable goods orders, and 18% in retail sales. But the next stage of the recovery will be harder: continuing unemployment claims in late June were still 19.5 million. Bankruptcies are rising, and banks are tightening lending conditions. One key will be whether Congress can pass a further fiscal program before the emergency spending runs out in July. Euro Area: Although pandemic lockdowns ended in Europe earlier than in the US, recovery has been somewhat slower. The euro zone PMI rebounded to close to 50 in June but, given that activity had collapsed in February-May, it is surprising (since the PMI measures month-on-month change) that it is not well above 50 (Chart 19, panel 1). Fiscal and monetary stimulus, while large, has not been as aggressive as in the US. The ECB remains circumscribed (as least psychologically) by the German constitutional court’s questioning the justification for previous QE. Germany and France have agreed a EUR750 billion additional package to help the periphery, but this has still to be finalized, due to the opposition of some smaller northern EU members. Chart 18Economic Data Has Started To Surprise To The Upside...

Economic Data Has Started To Surprise To The Upside...

Economic Data Has Started To Surprise To The Upside...

Chart 19...But From Dramatically Low Levels

...But From Dramatically Low Levels

...But From Dramatically Low Levels

Japan: Although Japan escaped relatively easily from pandemic deaths and lockdowns, its economy remains notably weak. New machinery orders in April were still falling 18% YoY, and exports in May were down 28% YoY. The poor economic performance is due to its dependence on overseas demand, distrust in the government, the lingering effects of the ill-timed consumption tax rise last October, and limited room for manoeuvre by the Bank of Japan. The government has announced fiscal stimulus equal to a barely credible 40% of GDP, but much of this is double-counting, and less than half of the household and small-company income-replacement handouts announced in March have so far been paid out. Emerging Markets: India, Brazil, and other Latin American countries are now bearing the brunt of the coronavirus pandemic. Economies throughout Emerging Markets have weakened dramatically as a result. Two factors may come to their aid, though. China is again ramping up monetary stimulus, with a notable acceleration of credit growth over the past three months. Its economy has stabilized as a result, as PMIs show (panel 3). And the US dollar has begun to depreciate, which will take pressure off EM borrowers in foreign currencies, and boost commodities prices. The biggest risk is that many EM central banks have now resorted to printing money, which could result in currency weakness and inflation at a later stage. Interest Rates: Central banks in advanced economies have lowered policy rates to their effective lower bound. It is unlikely the Fed will cut into negative territory, having seen the nefarious effects of this on the banking systems in Japan and the euro zone, and particularly due to the large money-market fund industry in the US, which is unviable with negative rates. Reported inflation everywhere, both headline and core, has fallen sharply, but this is somewhat misleading since the price of items that households in lockdown have actually been buying has risen sharply. Markets have started to sniff out the possibility of inflation once the pandemic is over, and inflation expectations have begun to rise (panel 4). For now, deflation is likely to be the bigger worry and so we do not expect long-term rates to rise much this year. But a sharp pickup in inflation is a definite risk on the 18-24 month time horizon. Global Equities Chart 20Stretched Valuation

Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Valuation Concern: Global equities staged an impressive rebound of 18% in Q2 after the violent selloff in Q1, thanks to the “whatever-it-takes” support from central banks, and massive fiscal stimulus packages around the globe. Within equities, our country allocation worked well, as the US outperformed both the euro Area and Japan. Our sector performance was mixed: The overweight in Info Tech and underweight in Utilities and Real Estate generated good profits, but the overweights in Industrials and Healthcare and the underweight in Materials suffered losses. As shown in Chart 20, even before the pandemic-induced profit contraction, forward earnings were already only flattish in 2019. The sharp selloff in Q1 brought the valuation multiple back down only to the same level as at the end of 2018. Currently, this valuation measure stands at the highest level since the Great Financial Crisis after a 37% increase in Q2 2020 alone. Such a rapid multiple expansion was one of the key reasons why we downgraded equities to Neutral in May at the asset-class level. Going forward, BCA’s house view is that easy monetary policies and stimulative fiscal policies globally will help to revive economic activity, and that a weakening US dollar will give an additional boost to the global economy, especially Emerging Markets. Consequently, we upgrade global Materials to neutral from underweight and put Emerging Market equities (currently neutral) on an upgrade watch (see next page). Warming To Reflation Plays Chart 21EM On Upgrade Watch

EM On Upgrade Watch

EM On Upgrade Watch

Taking risk where risks will most likely be rewarded has been GAA’s philosophy in portfolio construction. As equity valuation reaches an extreme level, the natural thing to do is to rotate into less expensive areas within the equity portfolio. As shown in panel 2 of Chart 21, EM equities are trading at a 31% discount to DM equities based on forward P/E, which is 2 standard deviations below the average discount of past three years. Valuation is not a good timing tool in general, but when it reaches an extreme, it’s time to pay attention and check the fundamental and technical indicators. We are putting EM on upgrade watch (from our current neutral stance, and also closing the underweight in Materials given the close correlation of the two (Chart 21, panel 1). Three factors are on our radar screen: First, reflation efforts in China. The change in China’s total social financing as a % of GDP has been on the rise and BCA’s China Investment Strategy Team expects it to increase further. This bodes well for the momentum of the EM/DM performance, which is improving, albeit still in negative territory (panel 3). Second, a weakening USD is another key driver for EM/DM and the Materials sector relative performance as shown in panel 4. According to BCA’s Foreign Exchange Strategy, the US dollar is likely to churn on recent weakness before a cyclical bear market fully unfolds.4 Last but not least, the recent surge in the number of the coronavirus infections in EM economies, especially Brazil and India, has increased the likelihood of a second wave of lockdowns. Government Bonds Chart 22Bottoming Bond Yields

Bottoming Bond Yields

Bottoming Bond Yields

Maintain Neutral Duration. Global bond yields barely moved in Q2 as the global economy rebounded from the COVID-induced recession low (Chart 22, panel 1). The upside surprise in economic data releases implies that global bond yields will likely go up in the near term (panel 2). For the next 9-12 months, however, the upside in global bond yields might be limited given the increasing likelihood of a new set of COVID-19 lockdowns due to the recent surge in new infections globally, especially in the US, Brazil, and India. As such, a neutral duration stance is still appropriate (Chart 22). Chart 23Inflation Expectations On The Rise

Inflation Expectations On The Rise

Inflation Expectations On The Rise

Favor Linkers Vs. Nominal Bonds. To fight off the risk of an extended recession, policymakers around the world are determined to continue to use aggressive monetary and fiscal stimulus to boost the global economy. The combined effect of extremely accommodative policy settings and the rebound in global commodity prices, especially oil prices, will push up inflation expectations (Chart 23). Higher inflation expectations will no doubt push up nominal bond yields somewhat, but according to BCA’s Global Fixed Income Strategy (GFIS), positioning for wider inflation breakevens remains the “cleaner” way to profit for the initial impact of policy reflation.5 According to GFIS valuation models, inflation-linked bonds in Canada, Italy, Germany, Australia, France, and Japan should be favored over their respective nominal bonds. Corporate Bonds Chart 24Better Value In A-rated and Baa-rated Credit

Better Value In A-rated and Baa-rated Credit

Better Value In A-rated and Baa-rated Credit

Investment-grade: Since we moved to overweight on investment-grade credit within the fixed-income category, it has produced 8.8% in excess returns over duration-matched government bonds. We remain overweight, given that the Federal Reserve has guaranteed to rollover debt for investment-grade issuers, essentially eliminating the left tail of returns. Moreover, the Fed has begun buying both ETFs and individual bond issues, in an effort to keep financial stress contained during the pandemic. However, there are some sectors within the investment-grade space that are more attractive than others. Specifically, our Global Fixed Income Strategy team has shown that A-rated and Baa-rated bonds are more attractive than higher-rated credits (Chart 24). Meanwhile, our fixed-income strategist are overweight Energy and Financials at the sector level.6 High-yield: High-yield bonds – where we have a neutral position - have delivered 11.5% of excess return since April. We are maintaining our neutral position. At current levels, spreads no longer offer enough value to justify an overweight position, specially if one considers that defaults in junk credits could be severe, since the Fed doesn’t offer the same level of support that it provides for investment-grade issuers. Within the high-yield space, we prefer Ba-rated credit. Fallen angels (i.e. bonds which fell to junk status) are particularly attractive given that most qualify for the Fed’s corporate buying program, since issuers which held at least a Baa3 rating as of March 22 are eligible for the Fed’s lending facilities.7 Commodities Chart 25Commodity Prices Will Rise As Growth Revives

Commodity Prices Will Rise As Growth Revives

Commodity Prices Will Rise As Growth Revives

Energy (Overweight): A near-complete lack of storage led WTI prices to go into freefall and trade at -$40 in mid-April: The largest drawdown in oil prices over the past 30 years (Chart 25, panel 1). Since then, oil prices have picked up, reaching their pre-“sudden stop” levels, as the OPEC 2.0 coalition slashed production. Nevertheless, excess supply remains a key issue. Crude inventories have been on the rise as global crude demand weakens. Year-to-date inventories have increased by over 100 million barrels, and current inventories cover over 40 days of supply (panel 2). As long as the OPEC supply cuts hold and demand picks up over the coming quarters, the excess inventories are likely to be worked off. BCA’s oil strategists expect Brent crude to rise back above $60 by year-end. Industrial Metals (Neutral): Last quarter, we flagged that industrial metals face tailwinds as fiscal packages get rolled out globally – particularly in China where infrastructure spending is expected to increase by 10% in the latter half of the year. Major industrial metals have yet to recover to their pre-pandemic levels but, as lockdown measures are lifted and activity is restored, prices are likely to start to rise strongly (panel 3). Precious Metals (Neutral): The merits of holding gold were not obvious during the first phase of the equity sell-off in February and March. Gold prices tumbled as much as 13%, along with the decline in risk assets. Since the beginning of March, however, there have been as many positive return days as there has been negative (panel 4). However, given the uncertainty regarding a second wave of the pandemic, and the rise in geopolitical tensions between the US and China, as well as between India and China, we continue to recommend holding gold as a hedge against tail risks. Currencies Chart 26Momentum For The Dollar Has Turned Negative

Momentum For The Dollar Has Turned Negative

Momentum For The Dollar Has Turned Negative

US Dollar: The DXY has depreciated by almost 3% since the beginning of April. Currently, there are multiple forces pushing the dollar lower: first, interest-rate differentials no longer favor the dollar Second, liquidity conditions have improved substantially thanks to the unprecedented fiscal and monetary stimulus, as well as coordinated swap lines between the Fed and other central banks to keep USD funding costs contained. Third, momentum in the DXY – one of the most reliable indicators for the dollar – has turned negative (Chart 26– top & middle panel). Taking all these factors into account, we are downgrading the USD from neutral to underweight. Euro: The euro should benefit in an environment where the dollar weakens, and global growth starts to rebound. Moreover, outperformance by cyclical sectors as well as concerns about over-valuation in US markets should bring portfolio flows to the Euro area. Therefore, we are upgrading the euro from neutral to overweight. Australian dollar: Last quarter we upgraded the Australian dollar to overweight due to its attractive valuations, as well as the effect of the monetary stimulus coming out of China. This proved to be the correct approach: AUD/USD has appreciated by a staggering 13% since our upgrade – the best performance of any G10 currency versus the dollar this quarter (bottom panel). Overall, while we believe that Chinese stimulus should continue to prop up the Aussie dollar, valuations are no longer attractive with AUD/USD hovering around PPP fair value. This means that the risk-reward profile of this currency no longer warrants an overweight position. Thus, we are downgrading the AUD to neutral. Alternatives Chart 27Opportunities Will Emerge In Private Equity

Opportunities Will Emerge In Private Equity

Opportunities Will Emerge In Private Equity

Return Enhancers: Over the past year, we have flagged that hedge funds, particularly macro funds, will outperform other risk assets during recessions and periods of high market stress. This played out as we expected: macro hedge funds’ drawdown from January to March 2020 was a mere 1.4%, whereas other hedge funds’ drawdown ranged between 9% and 19% and global equities fell as much as 35% from their February 2020 peak. (Chart 27, panel 1). However, unlike other recessions, the unprecedented sum of stimulus should place a floor under global growth. Given the time it takes to move allocations in the illiquid space, investors should prepare for new opportunities within private equity as global growth bottoms in the latter half of this year. In an earlier Special Report, we stressed that funds raised in late-cycle bull markets tend to underperform given their high entry valuations. If previous recessions are to provide any guidance, funds raised during recession years had a higher median net IRR than those raised in the latter year of the preceding bull market (panel 2). Inflation Hedges: Over the past few quarters, we have been highlighting commodity futures as a better inflation hedge relative to other assets (e.g. real estate). Within the asset class, assuming a moderate rise in inflation over the next 12-18 months as we expect, energy-related commodities should fare best (panel 3). This corroborates with our overweight stance on oil over the next 12 months (see commodities section). Volatility Dampeners: We have been favoring farmland and timberland since Q1 2016. While both have an excel track record of reducing volatility, farmland’s inelastic demand during slowdowns will be more beneficial. Investors should therefore allocate more to farmland over timberland (panel 4). Risks To Our View The risks are skewed to the downside. After such a big economic shock, damage could appear in unexpected places. Banking systems in Europe, Japan, and the Emerging Markets (but probably not the US) remain fragile. Defaults are growing in sub-investment grade debt; mortgage-backed securities are experiencing rising delinquencies; student debt and auto loans are at risk. Emerging Market borrowers, with $4 trn of foreign-currency debt, are particularly vulnerable. The length and depth of recessions and bear markets are determined by how serious are the second-round effects of a cyclical slowdown. If the current recession really lasted only from March to July, and the bear market from February to March, this will be very unusual by historical standards (Chart 28). Chart 28Can The Recession And Bear Market Really Be All Over Already?

Can It Really Be Over Already?

Can It Really Be Over Already?

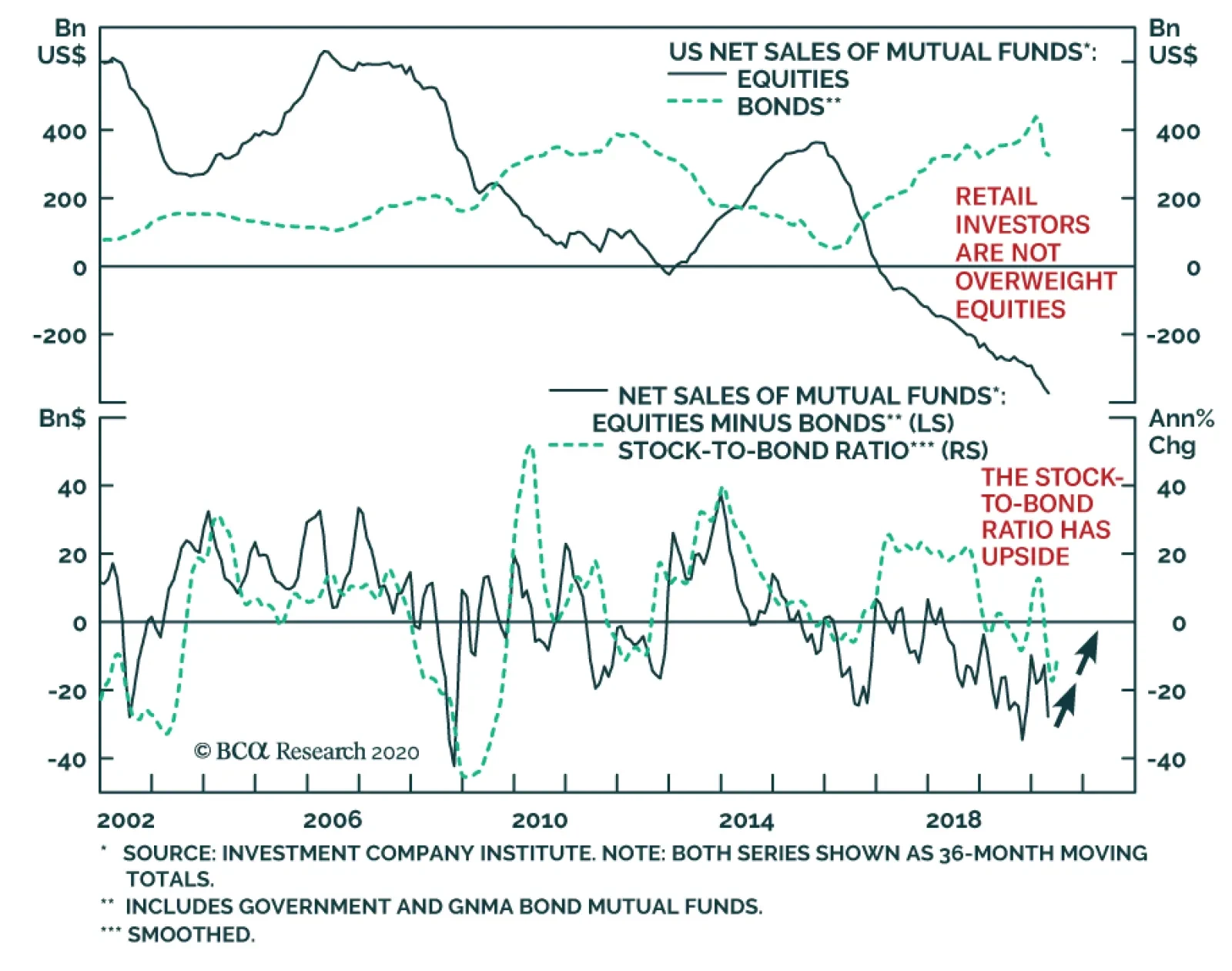

Upside surprises are not impossible. A vaccine could be developed earlier than the mid-2021 that most specialists predict. But this is unlikely since the US Food and Drug Administration will not fast-track approval given the need for proper safety testing. If economies continue to improve and newsflow generally remains positive over the coming months, more conservative investors could be sucked into the rally. Evidence suggests that the rebound in stocks since March was propelled largely by hedge funds and individual day-traders. More conservative institutions and most retail investors remain pessimistic and have so far missed the run-up (Chart 29). One key, as so often, is the direction of US dollar. Further weakness in the currency would be a positive indicator for risk assets, particularly Emerging Market equities and commodities. In this Quarterly, we have moved to bearish from neutral on the dollar (see Currency section for details). Momentum has turned negative, and both valuation and relative interest rates suggest further downside. But it should be remembered that the dollar is a safe-haven, counter-cyclical currency (Chart 30). Any rebound in the currency would not only signal that markets are entering a risk-off period, but would cause problems for Emerging Market borrowers that need to service debt in an appreciating currency. Chart 29Many Investors Are Still Pessimistic

Many Investors Are Still Pessimistic

Many Investors Are Still Pessimistic

Chart 30Dollar Direction Is Key

Dollar Direction Is Key

Dollar Direction Is Key

Footnotes 1 Please see BCA Webcast, "The Way Ahead For COVID-19: An Expert's Views," available at bcaresearch.com. 2 OECD Economic Outlook, June 2020, available at https://www.oecd-ilibrary.org/economics/oecd-economic-outlook/volume-2020/issue-1_0d1d1e2e-en 3 The Overton window, named after Joseph P. Overton, is the range of policies politically acceptable to the mainstream population at a given time. It frames the range of policies that a politician can espouse without appearing extreme. 4 Please see Foreign Exchange Strategy Weekly Report, “DXY: False Breakdown Or Cyclical Bear Market?” dated June 5, 2020 available at fes.bcaresearch.com 5 Please see Global Fixed Income Strategy Weekly Report, “How To Play The Revival Of Global Inflation Expectations” dated June 23, 2020 available at gfis.bcaresearch.com 6 Please see Global Fixed Income Strategy, "Hunting For Alpha In The Global Corporate Bond Jungle," dated May 27, 2020, available at gfis.bcaresearch.com. 7 Fallen angels also outperform during economic recoveries. Please see Global Asset Allocation Special Report, "Even Fallen Angels Have A Place In Heaven," dated November 15, 2020, available at gaa.bcaresearch.com. GAA Asset Allocation

BCA Research's US Bond Strategy service makes the case for owning subordinate bank bonds. We expect that extraordinary Fed support for the market will cause investment-grade corporate bond spreads to tighten during the next 6-12 months. In that…

BCA Research's Global Fixed Income Strategy service's current recommended overall stance on global corporate credit is neutral. Aggressively easy monetary policies, combined with some recovery in global economic growth, will help minimize the risk premium…

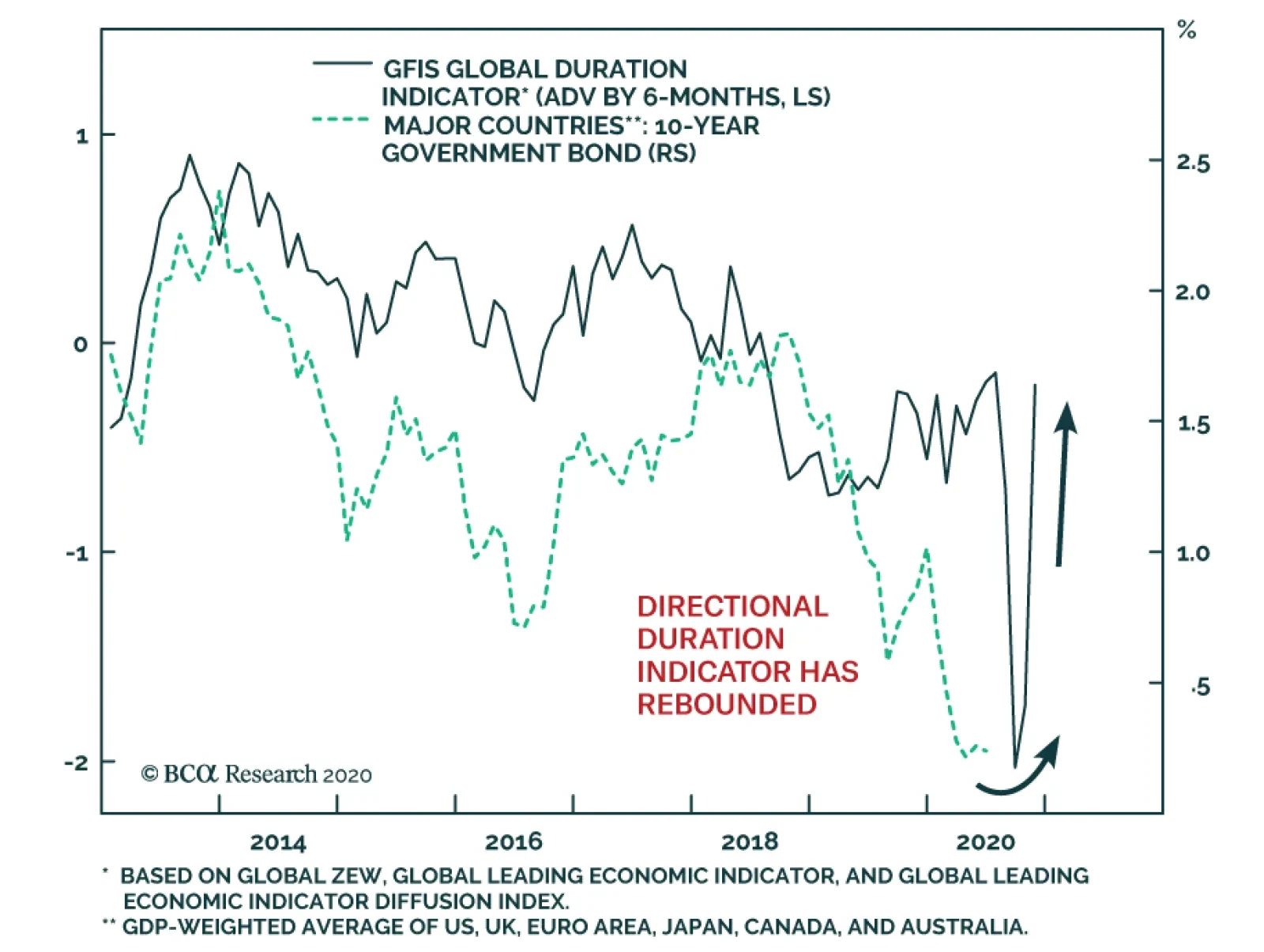

BCA Research's Global Fixed Income Strategy service's current recommended overall global duration stance is neutral. Our Global Duration Indicator, comprised of three elements - our global leading economic indicator and its diffusion index, along with the…

Highlights Global Growth & Inflation: An increasing number of growth indicators worldwide are tracing out a “v”-shaped pattern from the COVID-19 recession. However, high unemployment and a lack of inflationary pressure will ensure that global monetary policies remain highly stimulative for some time. Duration: Maintain a neutral duration stance in global fixed income portfolios, as the recent negative correlation between inflation expectations and real yields is likely to continue. Stay overweight higher-yielding government bonds in the US, Canada and Italy versus core Europe and Japan. Also, favor inflation-linked bonds over nominals - particularly in the US, Canada and euro area – as breakevens will continue drifting higher over the next 6-12 months. Corporate Credit: Maintain a neutral overall allocation to global spread product, focused on overweights in markets directly supported by central bank purchases (US investment grade corporates of maturities up to five years, US Ba-rated high-yield). Feature Today marks the midway point of what has already become one the most eventful years of our lifetimes. Investors have had to process multiple massive shocks: a global pandemic; a historically deep worldwide recession; and in the US, nationwide social unrest and a now politically vulnerable president. Yet despite the severe economic shock and persistent uncertainties, financial market performance over the entire first six months of the year has not been terrible. The S&P 500 index is only down -5.5% year-to-date, while the NASDAQ index is up +10.5% over the same period. Meanwhile, the Barclays Global Aggregate benchmark fixed income index is up +3.9% so far in 2020 (in hedged US dollar terms). In light of the magnitude of losses suffered by global equity and credit markets in February and March, those are impressive year-to-date returns. CHART OF THE WEEKA Tug Of War

A Tug Of War

A Tug Of War

Falling government bond yields, driven lower by an aggressive easing of global monetary policies through rate cuts and quantitative easing (QE), have played a major role in driving the recovery in risk assets. With the number of global COVID-19 cases now accelerating rapidly once again, however, the odds are increasing that investors become more reluctant to drive equity and credit valuations even higher (Chart of the Week). At the halfway point of the calendar year, this is a good time to review our most trusted indicators, and current investment recommendations, for global government debt and corporate credit. Duration Allocation: A Non-Inflationary Growth Recovery – But With Higher Inflation Expectations Our current recommended overall global duration stance is NEUTRAL. Global growth has started to recover from the sharp COVID-19 recession. Survey data like manufacturing and services purchasing managers indices (PMIs) have rapidly rebounded from the huge March/April drops, although most PMIs remain below the 50 level suggesting accelerating economic growth (Chart 2). While there is less timely “hard data” available due to reporting lags, there are signs of improvement in critical measures like US durable goods orders, which soared +15.8% in May after falling by similar amounts in both March and April. Global realized inflation data remains very weak, however, with headline CPI flirting with deflation in most major develop economies. Combined with still very high levels of unemployment, which will take years to return anywhere close to pre-COVID levels, the backdrop will keep central banks highly dovish for a long time. The US Federal Reserve has already signaled that the fed funds rate will remain near 0% until the end of 2022, while the Bank of Japan has said no rate hikes will happen before 2023 at the earliest. Our Global Duration Indicator, comprised of three elements - our global leading economic indicator and its diffusion index, along with the global ZEW measure of economic expectations - has already returned to pre-COVID levels (Chart 3). This leading, directional indicator of bond yields suggests that the downward pressure on yields seen over the first half of 2020 is over. Chart 2Growth, But Not Inflation, Is Recovering

Growth, But Not Inflation, Is Recovering

Growth, But Not Inflation, Is Recovering

Chart 3Our Global Duration Indicator Says Bond Yields Will Bottom Out In H2/2020

Our Global Duration Indicator Says Bond Yields Will Bottom Out In H2/2020

Our Global Duration Indicator Says Bond Yields Will Bottom Out In H2/2020

However, it is far too soon to expect a big bond selloff, with nominal government bond yields now pulled in opposing directions by their real yield and inflation expectations components. As we discussed in last week’s report, our models for market-based inflation expectations indicate that breakevens derived from inflation-linked bonds are too low.1 Hyper-easy monetary policies from the Fed, ECB and other major central banks will help lift inflation expectations, especially with oil prices likely to continue rising over the next 12-18 months according to BCA’s commodity strategists. Chart 4Higher Inflation Breakevens Should Eventually Help Steepen Yield Curves

Higher Inflation Breakevens Should Eventually Help Steepen Yield Curves

Higher Inflation Breakevens Should Eventually Help Steepen Yield Curves

The rise in inflation breakevens already seen over the past three months in places like the US, Canada and Australia – combined with dovish forward guidance on future interest rates that has kept shorter-maturity bond yields anchored - should have resulted in a bearish steepening of government bond yield curves. Yet the differences between 10-year and 2-year yields across the major developed markets have gone sideways since the beginning of April, even as 10-year inflation breakevens have increased (Chart 4). This has also kept the overall level of nominal 10-year yields nearly unchanged over the same period; for example, the 10-year US Treasury yield is now at 0.64% compared to the 0.58% closing level seen back on April 1. An outcome of rising inflation expectations with stable nominal yields must mean that real bond yields have declined by nearly as much as breakeven inflation rates have increased. That is exactly what has happened when looking at the actual real yield on 10-year inflation-linked bonds in the US, euro area, Canada, Japan, the UK and Australia. Using the US as an example, the 10-year inflation breakeven has increased +44bps since April 1, while the 10-year real yield has declined by -38bps. The decline in global real bond yields has coincided with the major central banks aggressively easing monetary policy, including large-scale purchases of government bonds. This occurred even in countries that had not engaged in major QE programs before, like Australia and Canada. The sizes involved for the new QE purchases have been massive, given the significant increase in the size of central bank balance sheets in absolute terms and relative to GDP (Chart 5). An outcome of rising inflation expectations with stable nominal yields must mean that real bond yields have declined by nearly as much as breakeven inflation rates have increased. Chart 5Global QE Is Helping Drive Real Bond Yields Lower

Global QE Is Helping Drive Real Bond Yields Lower

Global QE Is Helping Drive Real Bond Yields Lower

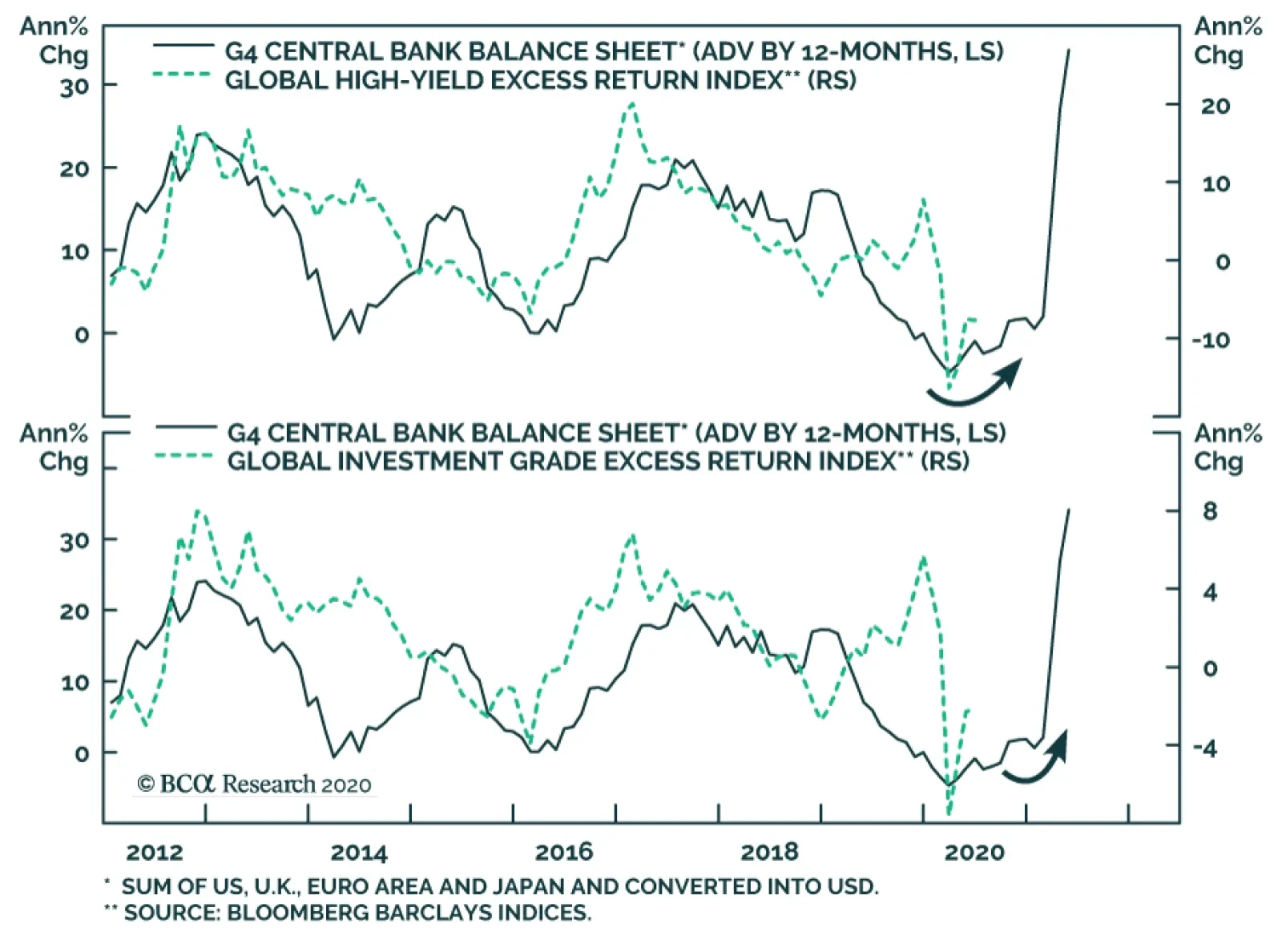

It is possible that the decline in real yields is due to other factors besides QE purchases, like markets pricing in structurally slower economic growth (and lower neutral interest rates) following the severe COVID-19 recession. Or perhaps it is more fundamentally economic in nature, reflecting a surge in domestic savings at a time of falling investment spending. The key takeaway for investors is that rising inflation expectations do not necessarily have to translate into higher nominal bond yields if the markets do not expect central banks to signal a need to tighten monetary policy in the near future, which would push real bond yields higher. For this reason, we continue to prefer structural allocations to inflation-linked bonds out of nominal government debt, rather than maintaining below-benchmark duration exposure in fixed income portfolios. That is a position that benefits from both higher inflation breakevens and lower real yields, while still having the benefit of maintaining a neutral level of safe-haven duration exposure given the lingering uncertainties over the accelerating global spread of COVID-19. At the specific country level, we recommend overweighting inflation-linked bonds over nominals in the US, Italy and Canada where breakevens appear most cheap on our models. Bottom Line: Maintain a neutral duration stance in global fixed income portfolios, as the recent negative correlation between inflation expectations and real yields is likely to continue. Stay overweight higher-yielding government bonds in the US, Canada and Italy versus core Europe and Japan. Also, favor inflation-linked bonds over nominals - particularly in the US, Canada and euro area – as breakevens will continue drifting higher over the next 6-12 months. Corporate Credit Allocation: Keep Buying What The Central Banks Are Buying Our current recommended overall stance on global corporate credit is NEUTRAL. The same reflationary arguments underlying our recommended inflation-linked bond positions also help support our views on global corporate debt. Aggressively easy monetary policies, combined with some recovery in global economic growth, will help minimize the risk premium on corporate debt. Yield-starved investors will continue to have no choice but to look to corporate bond markets for income over the next 6-12 months. The same reflationary arguments under-lying our recommended inflation-linked bond positions also help support our views on global corporate debt. The combined growth rate of the balance sheets for the major central banks (the Fed, ECB, Bank of Japan and Bank of England) has been a reliable leading indicator of excess returns for global investment grade and high-yield debt since the 2008 financial crisis (Chart 6). With that combined balance sheet now expanding at a 34% year-over-year pace after the ramp up of global QE, this suggests continued support for global corporate outperformance versus government bonds over the next year. Corporate debt is also benefitting from direct central bank purchases by the Fed, ECB and Bank of England. Unsurprisingly, the 2020 peak in US investment grade and high-yield corporate spreads occurred on March 20, literally the last trading day before the Fed announced its corporate bond purchase programs (Chart 7). Chart 6Global QE Will Continue To Support Risk Assets

Global QE Will Continue To Support Risk Assets

Global QE Will Continue To Support Risk Assets

Chart 7The Fed Has Removed The 'Left Tail' Risk Of US Credit

The Fed Has Removed The 'Left Tail' Risk Of US Credit

The Fed Has Removed The 'Left Tail' Risk Of US Credit

The Fed’s announced plan for its corporate bond buying was to have it focused on shorter maturity (1-5 year) investment grade credit. Later, the Fed allowed the programs to buy high-yield ETFs while also allowing “fallen angel” debt of investment grade credits downgrade to junk to be held within the programs. Since that announcement in late March, risk premiums for US corporate debt across all credit tiers and maturities have narrowed. However, the limits of that broad-based spread tightening may have now been reached, as some of the dislocations in US corporate bond markets created by the global market rout in February and early March have now been corrected. Chart 8Relative US Corporate Spread Relationships Have Normalized

Relative US Corporate Spread Relationships Have Normalized

Relative US Corporate Spread Relationships Have Normalized

For example, the spread on the Bloomberg Barclays 1-5 year US investment grade index – a proxy for the universe of bonds the Fed is buying – has moved from a level 25bps above that of the 5-10 year US investment grade index, seen before the Fed announced its purchase programs, to 53bps below the longer maturity index (Chart 8, top panel). This is a more normal “slope” for that spread maturity curve relationship, in line with levels seen over the past decade. This suggests that additional spread tightening in US investment grade corporates may be more widespread across all maturities, even with the Fed still focusing its own purchases on shorter-maturity bonds. A similar dynamic is evident in the US high-yield universe. The spread between the riskier B-rated and Caa-rated credit tiers to Ba-rated names has narrowed since late March to the lower bound of a rising trend channel in place since mid-2018 (bottom panel). The market appears to be pricing in a structurally rising risk premium between lower-rated junk and higher-rated US high-yield debt – likely a sign of a US credit cycle that was already maturing before COVID-19. The implication going forward is that additional outperformance of lower-rated US junk bonds will be difficult to achieve. The market appears to be pricing in a structurally rising risk premium between lower-rated junk and higher-rated US high-yield debt – likely a sign of a US credit cycle that was already maturing before COVID-19. European corporate debt has also been witnessing similar trends to those seen in the US. Euro area investment grade corporate spreads have tightened alongside US spreads since the March 20 peak, but that trend has now stabilized given the recent uptick in market volatility measures like the VIX and VStoxx index (Chart 9). The spread tightening in euro area high yield has also stalled, with spreads seeing a slight uptick alongside the recent increase in market volatility (Chart 10). Chart 9Global IG Spread Tightening Has Stalled

Global IG Spread Tightening Has Stalled

Global IG Spread Tightening Has Stalled

Chart 10Have Global HY Spreads Bottomed?

Have Global HY Spreads Bottomed?

Have Global HY Spreads Bottomed?

Given the renewed uncertainty over the accelerating number of global COVID-19 cases, hitting large US population areas in the US southern states and across the emerging economies, it will be difficult for global market volatility and credit spreads to return to even the recent lows, much less the pre-COVID levels. Thus, we continue to recommend a “selective” approach to global corporate bond allocations, based on valuations, while maintaining a neutral exposure to credit versus government bonds. Our preferred method for evaluating the attractiveness of credit spreads is to look at 12-month breakeven spreads, or the amount of spread widening that would make corporate bond returns equal to duration-matched government debt over a one-year horizon. We compare those breakeven spreads to their own history to determine if the current level of credit spreads offer value, while adjusting for the underlying spread volatility backdrop. In the US, the 12-month breakeven spread for investment grade corporates is now less attractive than was the case back in March, now sitting at the long-run median level (Chart 11, top panel). The 12-month breakeven for US high-yield is much more attractive, sitting near the highest readings dating back to the mid-1990s (bottom panel). Of course, this approach only looks at spreads relative to their volatility and does not incorporate credit risk, which is an obvious risk after the recent collapse in US economic growth. In other words, high-yield needs to offer very high 12-month breakeven spreads to be attractive in the current environment. In the euro area, 12-month breakevens for high-yield are only at long-run median levels, while the breakevens for investment grade are a bit more attractive sitting at the 65th percentile of its own history (Chart 12). Chart 11US Corporate Breakeven Spreads: HY Looks Attractive, But Beware Defaults

US Corporate Breakeven Spreads: HY Looks Attractive, But Beware Defaults

US Corporate Breakeven Spreads: HY Looks Attractive, But Beware Defaults

Chart 12European Corporate Breakeven Spreads: Now At Median Levels

European Corporate Breakeven Spreads: Now At Median Levels

European Corporate Breakeven Spreads: Now At Median Levels

Importantly, 12-month breakeven spreads in both the US and euro area, for investment grade and high-yield, have not fallen into the lower quartile rankings, even after the sharp tightening of spreads since late March. This is a sign the current rally in global corporates has more room to run, strictly from a spread compression perspective. For high-yield credit, however, the risk of default losses coming after a short, but intense, recession must be factored into any assessment of valuation. Chart 13Default-Adjusted HY Spreads In The US & Europe Are Unattractive

Default-Adjusted HY Spreads In The US & Europe Are Unattractive

Default-Adjusted HY Spreads In The US & Europe Are Unattractive

Looking at default-adjusted spreads – spread in excess of realized and expected credit losses – shows that the current level of junk spreads on both sides of the Atlantic offers little-to-no compensation for credit losses (Chart 13). Default-adjusted spreads are already well below long-run median levels, but if a typical 10-12% recessionary default rate is applied, expected credit losses over the next twelve months will exceed the current level of spreads, thus ensuring negative excess returns on allocations to junk bonds versus government bonds. Tying it all together, our valuation metrics for corporates suggest the following recommended allocations: Overweight US investment grade corporates, but focused on the 1-5 year maturity range that is supported by Fed purchases Overweight US Ba-rated high-yield (also eligible for Fed holdings), while underweighting lower-rated B- and Caa-rated junk Neutral allocation to euro area investment grade Underweight euro area high-yield across all credit tiers This allocation is in line with our current allocations within our model bond portfolio, which are on pages 13-14. Bottom Line: Maintain a neutral overall allocation to global spread product, focused on overweights in markets directly supported by central bank purchases (US investment grade corporates of maturities up to five years, US Ba-rated high-yield). Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Weekly Report, “How To Play The Revival Of Global Inflation Expectations”, dated June 23, 2020, available at gfis.bcaresearch.com Recommendations

Contagion Vs. Reflation: The Battle Of 2020 Rages On

Contagion Vs. Reflation: The Battle Of 2020 Rages On

Contagion Vs. Reflation: The Battle Of 2020 Rages On

Contagion Vs. Reflation: The Battle Of 2020 Rages On

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Dear client, We are sending you our Quarterly Strategy Outlook today, where we outline our thoughts on the macro landscape and the direction of financial markets for the rest of the year and beyond. Next week, please join me for a webcast on Thursday, July 9 at 10:00 AM EDT (3:00 PM BST, 4:00 PM CEST, 10:00 PM HKT) where I will discuss the outlook. Best regards, Peter Berezin, Chief Global Strategist Highlights Markets will trade nervously over the coming weeks in response to the second wave of the pandemic and the looming US fiscal cliff. Nevertheless, we would “buy the dip” if global equities were to fall 5%-to-10% from current levels. While the pace of reopening will slow, there is little appetite for the sort of extreme lockdown measures that were implemented in March. The US Congress will ultimately extend fiscal support for households and firms. Around the world, both fiscal and monetary policy will remain highly accommodative, which should provide a supportive backdrop for stocks. Many institutional investors missed the rebound in stocks and are eager to get back in. High levels of “cash on the sidelines” will further buttress equities. Remain overweight stocks versus bonds on a 12-month horizon. Favor cyclical sectors over defensives and non-US stocks over their US peers. The US dollar has entered a bear market. A weaker greenback will boost commodity prices and EM assets. Global bond yields will rise modestly over the next few years. However, they will remain extremely low by historic standards. Bond yields will only surge once inflation reaches uncomfortably high levels. At that point, the equity bull market will end. Fortunately, this is unlikely to happen for at least three years. I. Macro And Markets Financial markets’ response to the pandemic has followed three distinct phases: Phase One: Hope and Denial. While equities did buckle on the news that a previously unknown coronavirus had emerged in China, they quickly recovered in the hope that the epidemic would be contained. Equities remained resilient even as the virus resurfaced in South Korea and Iran, prompting us to pen a report in February entitled “Markets Too Complacent About The Coronavirus.”1 Phase Two: The Wile E. Coyote Moment.2 The second phase began with the outbreak in Italy. Scenes of overflowing emergency rooms prompted governments to order all non-essential workers to stay home. The resulting decline in commerce caused equities to plummet. Credit spreads widened, while funding markets began to seize up (Chart 1). Phase Three: Recovery. With memories of the 2008 global financial crisis still fresh in their minds, policymakers sprung into action. The combination of massive monetary and fiscal easing helped stabilize financial markets. Risk assets received a further boost as the number of new cases in Italy, Spain, New York City and other hotspots began to decline rapidly in April (Chart 2). The hope that lockdown measures would be relaxed continued to power stocks in May and early June. Chart 1Echos Of The Global Financial Crisis Prompted A Powerful Policy Response

Echos Of The Global Financial Crisis Prompted A Powerful Policy Response

Echos Of The Global Financial Crisis Prompted A Powerful Policy Response

Chart 2Sharp Decline Of New COVID-19 Cases In April Allowed Equities To Recover

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Fast forward to the present and things do not seem as straightforward. Despite today’s rally, global equities are still down 4.7% from their June 8th high. The key immediate question for investors is whether the recent bout of volatility marks the end of Phase Three or just a temporary pause in a new cyclical bull market for stocks. On balance, we lean towards the latter scenario. As we discuss in greater detail below, while we do think that the next few months will be more treacherous for investors due to a resurgence in the number of Covid cases in some countries, as well as uncertainty over how the looming US fiscal cliff will be resolved, we expect global equities to be higher 12 months from now. Stocks And The Economy Pundits such as Paul Krugman often like to recite the mantra that “the stock market is not the economy.” While there is some truth to that, equities still tend to track the ups and downs of the business cycle. This can be observed simply by looking at the strong correlation between the US ISM manufacturing index and the S&P 500 (Chart 3). Chart 3Strong Correlation Between Economic Growth And Stocks

Strong Correlation Between Economic Growth And Stocks

Strong Correlation Between Economic Growth And Stocks

As happened in 2009 and during prior downturns, stocks bottomed this year at roughly the same time as leading economic indicators such as initial unemployment insurance claims peaked (Chart 4). Chart 4Equities Bottomed This Year At Around The Same Time As Leading Economic Indicators Peaked

Equities Bottomed This Year At Around The Same Time As Leading Economic Indicators Peaked

Equities Bottomed This Year At Around The Same Time As Leading Economic Indicators Peaked

Will the economic data continue to improve, allowing equities to move higher? In the past, recoveries following exogenous shocks have tended to be more rapid than those following recessions that arose from endogenous problems. The pandemic would seem to qualify as an exogenous shock. Temporarily furloughed workers have accounted for the vast majority of the increase in US unemployment this year (Chart 5). As lockdown measures are relaxed, the hope is that most of these workers will return to their jobs. Chart 5Temporarily Laid Off Workers Account For The Vast Majority Of The Increase In US Unemployment This Year

Temporarily Laid Off Workers Account For The Vast Majority Of The Increase In US Unemployment This Year

Temporarily Laid Off Workers Account For The Vast Majority Of The Increase In US Unemployment This Year

Bumps In The Road Nevertheless, the recovery will be a bumpy one. In the near term, the main barrier will be the virus itself. Globally, the number of new cases has been trending higher since early May. The number of deaths has also reaccelerated (Chart 6). In the US, the epicenter of the pandemic has shifted from the Northeastern tri-state corridor to the southern states. Florida, Texas, and Arizona have been particularly hard hit. Contrary to President Trump’s claims, more testing does not explain the rise in case counts. As Chart 7 shows, the fraction of tests coming back positive has actually been trending higher in all three states. Chart 6Globally, The Number Of New Cases Has Been Trending Higher Since Early May, While The Number Of Deaths Has Moved Off Its Recent Lows

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Chart 7Fraction Of Tests Coming Back Positive Has Been Moving Higher In Certain States

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

It did not have to be this way. The evidence suggests that the widespread use of masks could have kept the virus at bay while still allowing most economic activities to resume (Chart 8). Unfortunately, the question of whether to wear a mask, like almost everything else in the US, has become another front in the culture war. Chart 8Masks On!

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Mask wearing is much more common in China and the rest of east Asia, which is one key reason why the region has suffered far fewer casualties than elsewhere. Hence, a second wave is likely to be much more muted there. Western Europe, Australia, and New Zealand should also remain largely unscathed going forward. Luckily, treatment options have improved over the past few months, as medical professionals have learned more about the virus. Hospitals have also built up capacity to deal with an influx of patients. Another less well recognized development is that protocols have been put in place to protect residents in long-term care facilities. In Canada, more than 80% of COVID deaths have occurred in nursing homes. All this suggests that while a second wave will weigh on global growth over the coming months, we are unlikely to see the sort of broad-based economic dislocations experienced in March. A Structural Break Even if a second wave does not turn out to be as disruptive as the first, it probably will be several years before spending in the sectors most affected by the virus returns to pre-pandemic levels. Indeed, there is a chance that some sectors may not ever fully recover. The technology to work from home was in place before the pandemic began. Many workers chose not to do so because they did not want to be the odd ones out. The pandemic may have nudged society to a new equilibrium where catching a red-eye flight to attend a business meeting becomes more the exception than the rule, while working from home is seen as perfectly acceptable (and safer) than going to the office. If that happens, there will be, among other things, less business travel going forward, as well as less demand for office space. Such a transformation could end up boosting productivity down the road by allowing companies to slash overhead costs and unnecessary expenses. However, it will impose considerable near-term dislocations, particularly for airlines, hotels, commercial real estate operators and developers, and associated lenders to these sectors. The Role Of Policy It would be unwise for policymakers to try to prevent the shift of capital and labor towards sectors of the economy where they can be more efficiently deployed. However, policy can and should smooth the transition. Chart 9Residential Construction Accounted For Less Than 20% Of The Job Losses During The Great Recession

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Most of the suffering during recessions comes in the form of collateral damage. For example, more than 80% of the jobs lost during the Great Recession were outside the residential real estate sector (Chart 9). One does not have to fill a half-empty swimming pool through the same pipe from which the water escaped. As long as there is enough demand throughout the economy, workers who lose their jobs will likely find new jobs in other sectors. This is where the role of monetary and fiscal policy takes center stage. Central banks moved quickly to ease monetary policy as soon as the pandemic began. Unfortunately, with rates already quite low in most countries, there was only so much that conventional monetary policy could achieve. The Federal Reserve, which had more scope to cut rates than most, brought the fed funds rate down 150 bps to a range of 0%-to-0.25%. As helpful as this action was, it fell well short of the more than five percentage points in easing that the Fed has delivered, on average, during past recessions (Chart 10). Chart 10Fed Easing Has Fallen Short This Time Around

Fed Easing Has Fallen Short This Time Around

Fed Easing Has Fallen Short This Time Around

With conventional monetary policy constrained by the zero lower bound, central banks turned to unconventional tools, the most important of which were asset purchases, lending backstops, and forward guidance. These tools blurred the line between fiscal and monetary policy. To some extent, this was by design. By offering to buy government debt in unlimited quantities and at extremely low rates, central banks incentivized governments to run larger budget deficits. Even if one excludes loan guarantees, governments have eased fiscal policy by an extraordinary degree this year (Chart 11). The G7 as a whole has delivered 11.7% of GDP in fiscal stimulus, compared to 4% of GDP in 2008-10. In China, we expect the credit impulse to reach the highest level since the Global Financial Crisis, and the budget deficit to hit the highest level on record (Chart 12). Chart 11Fiscal Stimulus Is Greater Today Than It Was During The Great Recession

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Chart 12China Has Opened The Spigots

China Has Opened The Spigots

China Has Opened The Spigots

Fiscal Austerity? Don’t Bet On It The recovery following the Great Recession was hampered by the decision of many governments, including the US, Germany, and Japan, to tighten fiscal policy prematurely, despite a lack of pressure from bond markets to do so. While a repeat of such an outcome cannot be excluded, we think it is quite unlikely. Politically, stimulus remains very popular (Table 1). Unlike during the housing bust, there has been little moral handwringing about bailing out households and firms that “don’t deserve it.” Thus, while the US faces a daunting fiscal cliff over the next two months – including 3% of GDP in expiring Paycheck Protection Program funding and over 1% of GDP in expanded unemployment benefits and direct payments to individuals – we expect Congress to ultimately take action to avert most of the cliff. Table 1There Is Much Public Support For Fiscal Stimulus

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

This will probably involve rolling over some existing programs and supplanting others with new measures such as increased aid to state and local governments. The same pattern is likely to be repeated globally. II. Long-Term Focus: Inflation And The Fiscal Hangover The combination of large budget deficits and falling output has caused the ratio of government debt-to-GDP to explode. The IMF now expects net government debt to reach 132% of GDP in advanced economies in 2021, up from an earlier estimate of 104% made last October (Chart 13). What will happen to all that debt? The answer partly hinges on what happens to the neutral rate of interest, or more precisely, the difference between the neutral rate and the trend growth rate of the economy. The neutral rate of interest is the interest rate that is consistent with full employment and stable inflation. When policy rates are above the neutral rate, unemployment will tend to rise, and vice versa. Most estimates of the neutral rate, such as those produced by the widely used Laubach-Williams model, suggest that it is currently quite low — certainly lower than the potential growth rate of most economies (Chart 14). Theoretically, when GDP growth exceeds the interest rate the government pays on its borrowings, the debt-to-GDP ratios will eventually converge to a stable level, even if the government keeps running a huge budget deficit.3 Chart 13Ratio Of Government Debt-To-GDP Is Exploding Higher On The Back Of Large Budget Deficits And Falling Output

Government Debt Levels Have Surged In The Wake Of The Pandemic Ratio Of Government Debt-To-GDP Is Exploding Higher On The Back Of Large Budget Deficits And Falling Output

Government Debt Levels Have Surged In The Wake Of The Pandemic Ratio Of Government Debt-To-GDP Is Exploding Higher On The Back Of Large Budget Deficits And Falling Output

Chart 14The Neutral Rate Is Lower Than The Potential Growth Rate In Most Economies

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

The catch is that this “stable” level of the debt-to-GDP ratio could turn out to be very high. This would leave the government extremely vulnerable to any future change in interest rates. Specifically, if at some point the neutral rate were to rise above the trend growth rate of the economy – and the central bank were to align policy rates with the new higher neutral rate – the government’s borrowing costs would soar. The government would then need to cut spending and/or increase in taxes to make room for additional interest payments.4 The Inflation Solution What if highly indebted governments refuse to tighten fiscal policy? At that point, they would either have to: 1) allow debt levels to spiral out of control; 2) default on the debt; or 3) lean on their central banks to keep rates low. The first two options are unlikely to be politically feasible, implying that the third one would be chosen. By definition, the third option would entail keeping policy rates below their neutral level, or in other words, keeping monetary policy more stimulative than is necessary to maintain full employment and stable inflation. Eventually, this would result in rising inflation. In theory, the increase in inflation can be temporary and limited. Rising consumer prices will lift nominal GDP, causing the ratio of debt-to-GDP to decline. Once the ratio shrinks by enough, central banks could raise interest rates to a suitably high level in order to bring inflation back down. Unfortunately, in practice, the whole process of driving inflation up in order to erode the real value of a government’s bond obligations could be quite destabilizing. This would be especially the case if, as is likely, a period of high inflation leads to a significant repricing of inflation expectations. Long-Term Inflation Risk Is Underpriced Chart 15Long-Term Inflation Expectations Remain Very Depressed

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Third Quarter 2020 Strategy Outlook: Navigating The Second Wave

Investors are not too worried that inflation will accelerate anytime soon. The CPI swap market expects inflation to remain subdued for decades to come (Chart 15). This could turn out to be an erroneous assumption. While central banks do not want inflation to get out of hand, they would be happy for it to increase from current levels. After all, they have been obsessing about the zero-lower bound constraint for the better part of two decades. If inflation is, say, 4% going into a downturn, central banks could cut nominal rates to zero, taking real rates to -4%. That would be quite stimulative. Such a deeply negative real rate would not be achievable if inflation were running at 1% going into a downturn. As noted above, heavily indebted governments would also prefer higher inflation to higher interest rates. The former would erode the real value of debt, while the latter would require that tax dollars be diverted from social program to bondholders. The Neutral Rate May Rise The catch is that for inflation to rise, the neutral rate has to increase well above current policy rates. Will that happen? Our guess is that such an outcome is more likely than most investors believe. For one thing the neutral rate itself depends on the stance of fiscal policy. Looser fiscal policy will generate more demand in the economy. Since one can think of the neutral rate as the interest rate that equalizes aggregate demand with aggregate supply, this implies that larger budget deficits will increase the neutral rate. If, as seems likely, we are entering an era where political populism promotes big budget deficits, this makes it more likely that economies will, at some point, overheat. Savings Glut May Dissipate The structural forces that have depressed the neutral rate over the past few decades could also abate, and perhaps even reverse course. Take the example of demographics. Starting in the mid-1970s, the ratio of workers-to- consumers – the so-called “support ratio” – began to steadily increase as more women entered the labor force and the number of dependent children per household declined (Chart 16). An increase in the number of workers relative to consumers is equivalent to an increase in the amount of production relative to consumption. A rising support ratio is thus deflationary. More recently, however, the global support ratio has begun to decline as baby boomers leave the labor force in droves. Consumption actually increases in old age once health care spending is included in the tally (Chart 17). As populations continue to age, the global savings glut could dissipate, pushing up the neutral rate of interest in the process. Chart 16The Ratio Of Workers-To-Consumers Is Now Falling

The Ratio Of Workers-To-Consumers Is Now Falling

The Ratio Of Workers-To-Consumers Is Now Falling

Chart 17As Populations Continue To Age, The Global Savings Glut Will Dissipate

As Populations Continue To Age, The Global Savings Glut Will Dissipate

As Populations Continue To Age, The Global Savings Glut Will Dissipate