Fixed Income

Highlights Please note that we are publishing an analysis on Vietnam below. The unprecedented depth of this recession entails that many businesses will likely be operating below their break-evens for a while, even after the confinement measures are eased. Consequently, the process of bottoming in this bear market will be drawn out, and share prices will gyrate substantially in the interim. Elevated foreign currency debt levels among some EM corporations, plunging revenues and local currency depreciation combine for a perfect storm in EM corporate credit. Continue underweighting EM stocks and credit within global equity and credit portfolios, respectively. Take profits on the long EM currency volatility trade. Feature If history is any guide, the speed of the rebound in global equities is more consistent with a bear market rally than the beginning of a new bull market. Typically, for a new durable bull market to emerge after a vicious bear market, a consolidation period or a base-building phase is needed. As of now, share prices have not formed such a base. Playing bear market rallies is all about timing, in which fundamental analysis is not useful. Rebounds die as abruptly as they begin. Hence, it is all about chasing momentum on either side. The unprecedented depth of this recession heralds that many businesses will likely be operating below their break-evens for a while, even after the confinement measures are eased. We closed our absolute short position in EM equities on March 19 but we have continued shorting EM currencies versus the US dollar. Even though EM share prices have become cheap based on their cyclically-adjusted P/E ratio (Chart I-1), valuation is not a good timing tool. This is especially true for this structural valuation indicator. Chart I-1EM Equities Are As Cheap As In Previous Bottoms

EM Equities Are As Cheap As In Previous Bottoms EM Equities Are Cheap According To The Cyclically-Adjusted P/E Ratio

EM Equities Are As Cheap As In Previous Bottoms EM Equities Are Cheap According To The Cyclically-Adjusted P/E Ratio

Why The Rebound? After the massive selloff, investor sentiment on risk assets in general, and cyclicals specifically, has become very depressed. In particular: Sentiment of traders and investment advisors on US stocks has plummeted (Chart I-2). That said, net long positions in US equity futures are still above their 2016 and 2011 lows, as we noted last week. Traders’ sentiment on cyclical currencies such as the CAD and AUD as well as on copper and oil has dropped to their previous lows (Chart I-3). Chart I-2Investor Sentiment On US Equities Is Poor

Investor Sentiment On US Equities Is Poor

Investor Sentiment On US Equities Is Poor

Chart I-3Investor Sentiment On Copper And Oil Is Depressed

Investor Sentiment On Copper And Oil Are Depressed

Investor Sentiment On Copper And Oil Are Depressed

Consistently, net long positions of investors in both copper and oil have been trimmed substantially (Chart I-4A and I-4B). Chart I-4AInvestors’ Net Long Positions In Copper...

Investors Net Long Positions In Copper...

Investors Net Long Positions In Copper...

Chart I-4B…And Oil

...And Oil

...And Oil

On the whole, it should not be surprising that after having become very oversold, risk assets rebounded in the past two weeks. Nevertheless, depressed investor sentiment is a necessary but not sufficient condition for a major bear market bottom. As illustrated in Chart I-3, sentiment on oil and copper was extremely depressed in late 2014. Yet with the exception of brief rebounds, both oil and copper prices continued to plunge for about a year before bottoming in January 2016. The necessary and sufficient condition for a durable bottom in global cyclical assets is an improvement in global demand. Chart I-5The S&P 500 And VIX In The Last Two Bear Markets

The S&P 500 And VIX In The Last Two Bear Markets

The S&P 500 And VIX In The Last Two Bear Markets

Given the US and Europe are still in strict confinement and the Chinese economy remains quite weak (please see our more detailed discussion on this below), the global recession is still deepening. Further, while the enormous amounts of stimulus injected by policymakers is certainly positive, it is not yet clear whether these efforts are sufficient to entirely offset the collapse in the level of economic activity and its second round effects. Nevertheless, the Federal Reserve and the European Central Bank have probably contained the acute phase of the financial market crisis by buying financial assets and providing credit to the real economy. Odds are that the VIX and other volatility measures will not retest their recent highs. However, this does not mean that risk assets cannot retest their lows or make fresh ones. For example, in the previous 2001-2002 and 2008 bear markets, the S&P 500 re-tested its low in early 2003 and made a deeper trough in early 2009 even though the VIX drifted lower (Chart I-5). Finally, as we discuss below, a unique feature of this recession makes it unlikely that a definite equity market bottom has been established so quickly. How This Recession Is Distinct From an investor viewpoint, this global recession stands out from others in a particularly distinct way: In an average recession, nominal output levels do not contract. In the US, since 1960 it was only during 2008 that the level of nominal GDP contracted (Chart I-6). Presently, we are experiencing the gravest collapse in nominal output/sales since the 1930s – much worse than what transpired in 2008. Chart I-6US Nominal GDP And Corporate Profits Growth

US Nominal GDP And Corporate Profits Growth

US Nominal GDP And Corporate Profits Growth

When a company’s sales shrink, a critical threshold for sustainability is the level of its revenues relative to its break-even point. The latter is the level of sales where total revenue is equal to total cost – i.e., where profits are nil. Break-even points have ramifications for share prices and the shape of a potential recovery. In an average recession, break-even points for the majority of companies are not breached – i.e., they remain profitable. As a result, a moderate and sequential revival in sales boosts profits, often exponentially. Share prices react positively to even modest sequential growth. Besides, when profits are expanding, managers and owners of these businesses are often quick to augment their capital spending and hiring. A marginal and sequential recovery from this very low point is not sufficient to produce a durable bull market for stocks or corporate credit. When a company’s sales drop below its break-even level, a moderate sequential recovery in sales could be insufficient to make the company profitable. In such a case, the share price may not rally vigorously unless they had priced in a much worse outcome – i.e., a bankruptcy. Crucially, a moderate sequential revival in activity may not lead to more capital spending and hiring. Given US and global nominal GDP are presently contracting at an unprecedented double-digit pace, the revenue of a majority of companies has fallen below costs – i.e., they are presently operating below their break-evens (experiencing losses). This makes this recession distinct from others. On the whole, the loosening of confinement measures and the resumption of business operations may not be sufficient reasons to turn bullish on equities. So long as a company operates below its break-even, its share price may not rally much in response to marginal sequential growth. In short, the pace of recovery will be crucial. Yet, there is considerable uncertainty with respect to these dynamics. Such uncertainty also warrants a high equity risk premium. A U-shaped recovery is most likely, but the latter assumes that many companies will be operating with losses for some time. Consequently, odds are that the process of bottoming in this bear market will be drawn out, and share prices will gyrate substantially in the interim. Taking Pulse Of The Global Economy In our March 19 report, we argued that this global recession is much worse than the one in 2008. High-frequency data are confirming our view: The weekly US economic index from the New York Fed has plunged more than it did in 2008 (Chart I-7). Capital spending plans have been shelved around the world. Odds are many businesses will be operating below their break-evens even after confinement measures are eased. Therefore, they will not rush to invest in new capacity and equipment, or rush to hire. China is a case in point. Commodities prices on the mainland remain in a downtrend, despite the resumption of business activity (Chart I-8). This is a sign of lingering weakness in construction/capital spending. Chart I-7An Unprecedented Plunge In Economic Activity

An Unprecedented Plunge In Economic Activity

An Unprecedented Plunge In Economic Activity

Chart I-8Commodities Prices In China Are Drifting Lower

Commodities Prices In China Are Drifting Lower

Commodities Prices In China Are Drifting Lower

The world’s oil consumption is presently probably down by more than 35%. According to INRIX, US car traffic last week was 47% below its level in late February before the confinement measures were introduced. Plus, airline travel has literally ground to a halt worldwide. In China’s major cities, traffic during rush hour is re-approaching its pre-pandemic levels. However, automobile congestion data from TomTom shows that in the afternoons and evenings, traffic remains well below where it was before the lockdown. This reveals that people go to work, spend most of their time at the office, and then quickly return home. They do not go out during lunch time or in the evenings. Hence, we infer that China’s service sector remains in recession. Chart I-9EM ex-China, Korea And Taiwan: Nominal Growth Was Very Weak Before The Pandemic

EM ex-China, Korea And Taiwan: Nominal Growth Was Very Weak Before The Pandemic

EM ex-China, Korea And Taiwan: Nominal Growth Was Very Weak Before The Pandemic

The Chinese manufacturing and service PMI indexes registered 51 and 47 respectively in March, revealing that their economic recoveries are very subdued. As per our discussion above, we suspect revenues for many businesses in February dropped below break-even levels. The fact that only about a half of both manufacturing and service sector companies said their March activity improved from February is rather underwhelming. EM ex-China, Korea and Taiwan nominal GDP and core consumer price inflation were at very low levels before the pandemic (Chart I-9). The ongoing plunge in economic activity will produce the worst nominal output recession for many developing economies. Consequently, corporate profits of companies exposed to domestic demand will crash in local currency terms. Bottom Line: The unprecedented depth of this recession heralds that many businesses will likely be operating below their break-evens for a while, even after the confinement measures are eased. Thus, a marginal and sequential recovery from this very low point is not sufficient to produce a durable bull market for stocks or corporate credit. Credit Markets Hold The Key Solvency concerns for companies become acute and doubt about their debt sustainability persist when their revenues drop below their break-evens. Thus, a marginal improvement in revenue – as lockdowns worldwide are relaxed – may not suffice to produce a material tightening in EM corporate credit spreads. Playing bear market rallies is all about timing, in which fundamental analysis is not useful. Rebounds die as abruptly as they begin. Interestingly, equity markets often take their cues from credit markets. Chart I-10 demonstrates that EM US dollar corporate bond yields (inverted on the chart) correlate with equity prices. This chart unambiguously expounds that what matters for EM share prices is not US Treasurys yields but rather their own borrowing costs in US dollars. Chart I-10EM US Dollar Corporate Bond Yields And Stock Prices

EM US Dollar Corporate Bond Yields And Stock Prices

EM US Dollar Corporate Bond Yields And Stock Prices

Presently, there are no substantive signs that US dollar borrowing costs for EM companies or sovereigns are declining. Chart I-11 illustrates that investment and high-yield corporate bond yields for aggregate EM and emerging Asia remain elevated. Remarkably, bank bond yields in overall EM and emerging Asia have not eased much (Chart I-12). The latter is crucial as banks’ external high borrowing costs will dampen their appetite to originate credit domestically. Chart I-11EM US Dollar Corporate Bond Yields

EM US Dollar Corporate Bond Yields

EM US Dollar Corporate Bond Yields

Chart I-12EM Banks US Dollar Bond Yields

EM Banks US Dollar Bond Yields

EM Banks US Dollar Bond Yields

Chart I-13EM Credit Spreads, Currencies And Commodities

EM Credit Spreads, Currencies And Commodities

EM Credit Spreads, Currencies And Commodities

In turn, the direction of EM corporate and sovereign credit spreads is contingent on EM exchange rates and commodities prices, as demonstrated in Chart I-13. Credit spreads are shown inverted in both panels of this chart. We remain negative on both EM currencies and commodities prices, and argue for a cautious approach to EM credit markets. Bottom Line: Elevated foreign currency debt levels among some EM corporations, plunging revenues and local currency depreciation combine for a perfect storm in EM corporate credit. To make matters worse, this asset class as well as EM sovereign credit were extremely overbought before this selloff. Therefore, there could be more outflows from these markets as adverse fundamentals persist. Investment Strategy And Positions We continue to recommend underweighting EM stocks and credit versus their DM counterparts. Importantly, the EM equity index has been underperforming the global equity benchmark in the recent rebound (Chart I-14). Aggressive policy stimulus in the US and Europe have improved investor sentiment towards their credit and equity markets. Yet, the Chinese stimulus has so far been less aggressive than in the past. This will weigh on the growth outlook for emerging Asia and Latin America. The outlook for oil prices is currently a coin toss. Price volatility will remain enormous and it is not worth betting on either the long or short side of crude. Apart from oil, industrial metal prices remain at risk due to subdued demand from China. In general, this is consistent with lower EM currencies (Chart I-15). Chart I-14Continue Underweighting EM Stocks Versus The Global Benchmark

Continue Underweighting EM Stocks Versus The Global Benchmark

Continue Underweighting EM Stocks Versus The Global Benchmark

Chart I-15EM Currencies Correlate With Industrial Metals Prices

EM Currencies Correlate With Industrial Metals Prices

EM Currencies Correlate With Industrial Metals Prices

Chart I-16Book Profits On Long EM Currency Volatility Trade

Book Profits On Long EM Currency Volatility Trade

Book Profits On Long EM Currency Volatility Trade

In accordance with our discussion above that the most acute phase of this crisis might be over, we are booking profits on our long EM currency volatility trade. We recommended this trade on January 23, 2020 and the JP Morgan EM currency implied volatility measure has risen from 6% to 12% (Chart I-16). While EM currencies could still sell off, we doubt this volatility measure will make a new high. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Vietnamese Stocks: Stay Overweight Like many EM bourses, Vietnamese stocks have plunged 35% over the past two months in US dollar terms. How should investors now position themselves with regard to Vietnamese equities, in both absolute and relative terms? In absolute terms, there are near-term risks to Vietnamese equities: Vietnam’s economy is highly dependent on exports, which amount to more than 100% of the country’s GDP. The deepening global recession entails that overseas demand for Vietnamese exports will be decimated. Chart II-1 illustrates how share prices often swing along with export cycles. Customers from the US and EU, which together account for 40% of Vietnamese exports, have been cancelling their orders. In addition, the number of visitor arrivals has already dropped significantly, and tourism revenue – which amounts to about 14% of GDP – will continue to contract (Chart II-2). Chart II-1Vietnamese Stocks: Risks Are External

Vietnamese Stocks: Risks Are External

Vietnamese Stocks: Risks Are External

Chart II-2Tourism Has Crashed

Tourism Has Crashed

Tourism Has Crashed

Nevertheless, we expect Vietnamese stocks to outperform the EM benchmark, in USD terms, both cyclically and structurally. First, Vietnam has solid macro fundamentals. The country’s annualized trade surplus has ballooned, reaching $12 billion in March (Chart II-3). Even as exports contract, the current account balance is unlikely to turn negative. Notably, Vietnam imports many of the materials required to produce its exported goods. As such, its imports will shrink along with its exports, which will support its current account balance. Meanwhile, the year-on-year growth of domestic nominal retail sales of goods has slowed down, but remains at 8% as of March, which is quite remarkable (Chart II-4). Chart II-3Vietnam Has Large Trade Surplus

Vietnam Has Large Trade Surplus

Vietnam Has Large Trade Surplus

Chart II-4Consumer Spending To Slow But Not Contract

Consumer Spending To Slow But Not Contract

Consumer Spending To Slow But Not Contract

Second, the government has announced a sizable policy stimulus package. On March 16, the State Bank of Vietnam cut its policy rate by 50bps, from 4% to 3.5%, and its refinancing rate by 100bps, from 6% to 5%. On April 3, Vietnam's Ministry of Finance passed a fiscal stimulus package worth VND180 trillion (equal to US$7.64 billion, or 2.9% of its GDP). Third, Vietnam has contained the COVID-19 outbreak better than many other countries. With aggressive testing and isolation, the country has so far limited the infection rate to only three out of one million citizens, and reported zero deaths. This reduces the probability that Vietnam will be forced to adopt severe confinement measures that would derail its economy. This nation’s success also contrasts with the difficulties that many emerging and frontier economies are having in their struggle with COVID-19 containment. We continue to overweight Vietnamese stocks relative to EM due to healthy fundamentals, attractive valuations, a large current account balance and a successful economic and health response to the COVID-19 outbreak. Fourth, the country remains quite competitive in global trade. For some time, multinational companies have been moving their supply chains to Vietnam in order to take advantage of its cheap and productive labor, inexpensive land and supportive government policies. As a result, Vietnamese exports have been outpacing those of China across many industries (Chart II-5). Given the geopolitical confrontation between the US and China is likely to persist over many years, more manufacturing will shift from China to Vietnam. Investment Recommendations In absolute terms, we believe Vietnamese stocks are still at risk. Stock prices falling to their 2016 low is possible over the coming weeks and months, which corresponds to a 10-15% downslide from current levels (Chart II-6, top panel). Chart II-5Vietnam Continues Gaining Export Market Share

Vietnam Continues Gaining Export Market Share

Vietnam Continues Gaining Export Market Share

Chart II-6Vietnamese Stocks: Absolute & Relative Performance

Vietnamese Stocks: Absolute & Relative Performance

Vietnamese Stocks: Absolute & Relative Performance

Relative to the EM equity benchmark, however, we continue overweighting Vietnam equities, both cyclically and structurally. Technically, this bourse’s relative performance has declined to a major support line and it could be bottoming at current levels (Chart II-6, bottom panel). Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

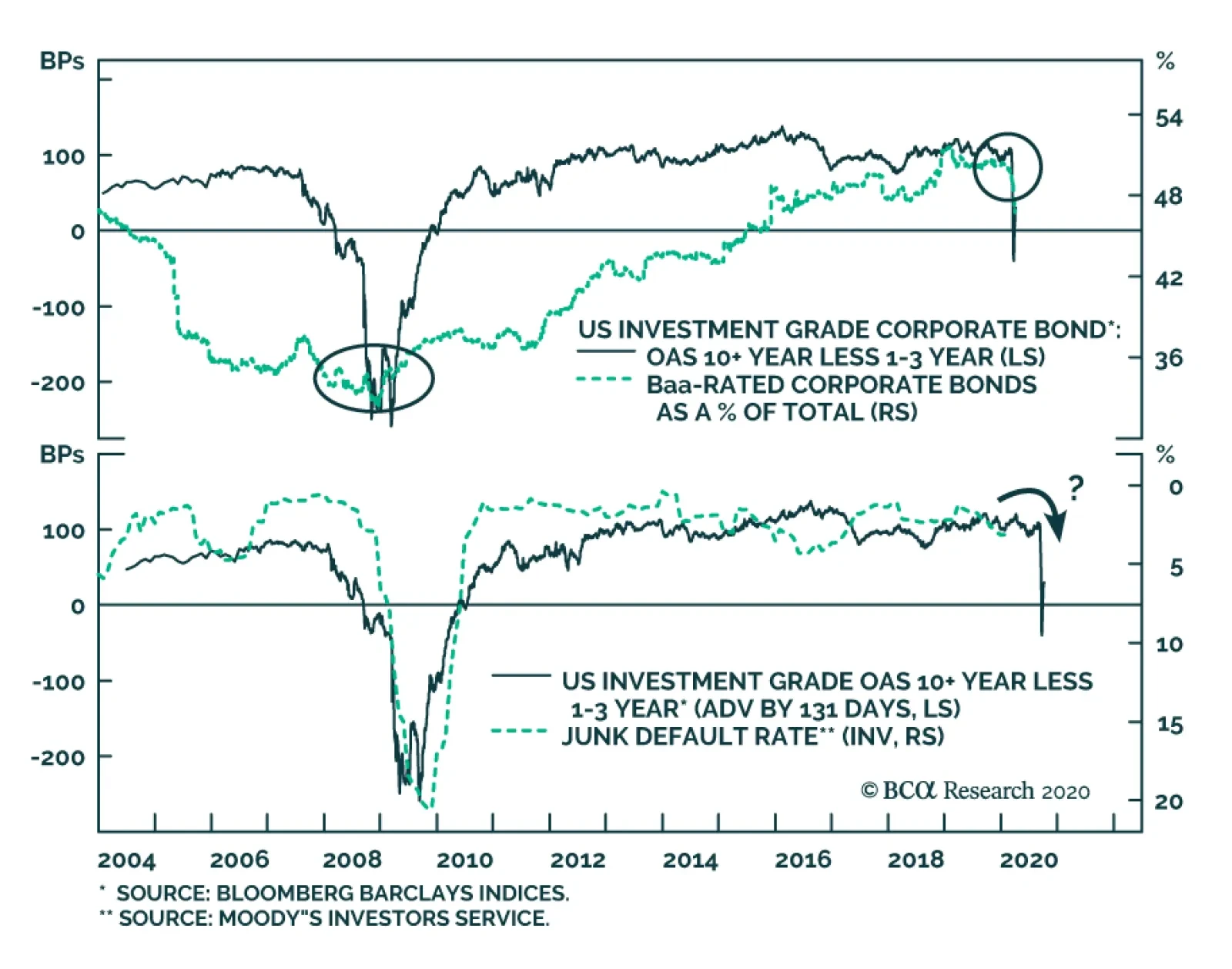

Recently, BCA Research's Global Fixed Income Strategy and US Bond Strategy services advocated an overweight allocation to US investment-grade corporate bonds, especially on securities eligible for the Fed's programs. Prior to the Fed’s announcement of…

Highlights Bond Yield Differentials: The deepening global recession has prompted aggressive monetary easing measures by virtually every developed economy central bank. With policy rates now near zero everywhere, government bond yield differentials between countries have been reduced substantially. Currency Hedged vs Unhedged Yields: Opportunities still exist in some countries to create synthetically “higher” yields relative to low local rates by hedging the currency exposure of foreign bonds. Country Allocation: Italy and Spain government bonds offer the most attractive yields, hedged into any of the major currencies (USD, EUR, GBP, JPY). Among the lower yielders, Canadian, Australian, French and Japanese government bonds offer the most attractive yield pickups, on a currency-hedged basis, versus yields in the US, Germany, and the UK. Feature Chart 1A Synchronized Collapse

A Synchronized Collapse

A Synchronized Collapse

The COVID-19 economic downturn is already shaping up to be one of the deepest global recessions in history. While there have been worldwide industrial slowdowns and manufacturing recessions in the past, what is happening now is different in that all countries are suffering sharp contractions in activity in the much larger services sectors that employ far more workers. The result will be massive increases in unemployment, as is already happening in the US where a staggering 10 million workers have filed for jobless benefits over just the past two weeks. Central bankers have responded to the shock to growth by following essentially the same playbook: cutting interest rates to zero as rapidly as possible, followed up with quantitative easing and other programs to support financial markets. With a synchronized economic collapse leading to policy convergence, government bond yields have plunged worldwide, but yield differentials between countries have also fallen sharply as a result (Chart of the Week). In this report, we will present the case for using currency hedging more actively than usual to create more attractive global bond yields. What can a global government bond investor do in this environment of tiny-but-highly-correlated bond yields to squeeze out some incremental additional return? In this report, we will present the case for using currency hedging more actively than usual to create more attractive global bond yields. A Fundamentally Driven Yield Convergence Chart 2Yields Are Low Everywhere

Yields Are Low Everywhere

Yields Are Low Everywhere

As a simple starting point, just looking at the level of government bond yields in the developed economies is a good indication of how little there is to choose from between countries right now. For example, a 10-year government bond in the US was yielding 0.67% yesterday, compared to a 10-year yield in Australia, Canada and the UK of 0.82%, 0.75%, and 0.33% respectively (Chart 2). Not only are those low absolute yields, but those spreads versus US Treasuries are very narrow in an historical context. Another way to see how similar interest rate structures have become within the major developed markets is by looking at market expectations of future policy rates. Our proxy for the market’s pricing of the terminal nominal policy rate – the 5-year overnight index swap (OIS) rate, 5-years forward – shows that interest rate markets are expecting policy rates to stay very low over the next few years. The fall in the terminal rate estimate has been the largest in the US and Canada, where the markets were still pricing in a “peak” policy rate level around 2% as late as December – the figure is now 0.6% in the US and 1.1% in Canada (Chart 3). Chart 3Global Policy Rate Convergence

Global Policy Rate Convergence

Global Policy Rate Convergence

So if the bond markets now believe that the current levels of bond yields will be sustained for longer, is that a realistic belief? There is already a considerable amount of both monetary and fiscal stimulus that has been introduced by policymakers. At some point, this stimulus should begin to stabilize and boost economic growth, but only after the immediate public health crisis of the COVID-19 outbreak has begun to subside. That will eventually help put a floor under developed market government bond yields. Chart 4The Backdrop Remains Conducive To Global Bond Yields Staying Low

The Backdrop Remains Conducive To Global Bond Yields Staying Low

The Backdrop Remains Conducive To Global Bond Yields Staying Low

As we discussed in a recent weekly report, three elements must all happen before a true and lasting bottom for both risk assets and bond yields can begin to take place (Chart 4):1 The net number of new COVID-19 cases must begin to slow in critical countries like the US and Italy, a first step before the lockdown restrictions can start to be lifted; The US dollar (USD) must peak out and begin to roll over, taking stress off non-US borrowers of USD-denominated debt; The VIX must sustainably fall back from the levels above 40 that imply very volatile markets and continued investor nervousness about the future. Global government bond yields are likely to remain relatively range bound over the next month or two, at least. Out of this list, the slowing in the number of new cases of the virus in Italy is a positive sign, as is the VIX falling back to the mid-40s. The sticky USD is still a major issue, however, particularly for borrowers with major dollar debts in the emerging world. There is not yet an “all clear” from this checklist, suggesting that global government bond yields are likely to remain relatively range bound over the next month or two, at least. This means bond investors need to consider alternative strategies to boost the yield of their government bond portfolios. Bottom Line: The deepening global recession has prompted similar monetary easing measures by virtually every developed economy central bank. With policy rates near zero everywhere, government bond yield differentials between countries have been largely eliminated. Searching For More Attractive Yields - With Currency Hedging When discussing our country allocation strategy, we have always looked at the yields and relative returns of government bonds in each country in hedged currency terms rather than in local currency terms. This is to remove the significant return volatility coming from currency exposure, while also making an appropriate “apples-to-apples” comparison of the yields on offer in each country. We have chosen the USD as the “base currency” for all these comparisons. In Chart 5, we show a static snapshot of the government bond yield curves, in local currency terms, for the US, Germany, France, Italy, the UK, Japan, Canada and Australia. The US, Canada and Australia remain the relative high-yielders within the major developed markets, although the “riskier” credits of Italy and Spain offer the highest outright yields. Unhedged German yields look particularly unattractive here, with the entire yield curve offering yields below 0%. Chart 5Currency-Unhedged Global Government Bond Yield Curves

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Chart 6USD-Hedged Global Government Bond Yield Curves

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

In Chart 6, we show those same yield curves, but with the non-US yields all shown on a USD-hedged basis. The yields include the net gain/cost of hedging foreign currency back into US dollars using 3-month currency forwards. Shown this way, the non-US yield curves can be more directly compared to the “base” US Treasury curve. Looking at those yields shows that there is a much tighter convergence of yields with the US for most countries, but in a relative narrower range between 0.5% and 1.25% across the full maturity spectrum. The Fed’s rapid easing cycle, which started with the 75bps of rate cuts in the summer of 2019 and continued with the rapid move to a near-zero funds rate during the COVID-19 crisis, has dramatically altered the calculus for both global bond country allocation and currency hedging. Chart 7Fed Rate Cuts Have Reduced The Yield Advantage of USTs

Fed Rate Cuts Have Reduced The Yield Advantage of USTs

Fed Rate Cuts Have Reduced The Yield Advantage of USTs

Chart 8Fed Rate Cuts Have Taken The Carry Out Of The USD

Fed Rate Cuts Have Taken The Carry Out Of The USD

Fed Rate Cuts Have Taken The Carry Out Of The USD

First, the Fed’s easing cycle triggered a major decline in US Treasury yields that was not matched in other countries, eliminating much of the unhedged yield advantage of Treasuries over non-US peers (Chart 7). At the same time, the Fed’s rate cuts eliminated much of the interest rate “carry” of owning US dollars versus other currencies. The amount of that reduction was significant, with the gain of hedging a euro or yen currency exposure into dollars reduced from nearly around 250bps in the spring of 2019 to just over 100bps today (Chart 8). That dramatically alters the attractiveness of even negative-yielding German and Japanese government bonds, whose yields could once have been transformed into a relatively high USD-based yield via currency hedging. The Fed’s easing cycle triggered a major decline in US Treasury yields that was not matched in other countries, eliminating much of the unhedged yield advantage of Treasuries over non-US peers. At the same time, the Fed’s rate cuts eliminated much of the interest rate “carry” of owning US dollars versus other currencies. Country Allocation Strategy Implications For dedicated global government bond investors, the only way to earn meaningfully higher yields in the current environment is to consider selective currency hedging of bond exposures. In Tables 1-4, we show 2-year, 5-year, 10-year and 30-year government bond yields for the major developed economy bond markets. The yields are hedged into USD, EUR, GBP and JPY, to allow comparisons of foreign yields for investors with those four base currencies. Table 1Currency-Hedged 2-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 2Currency-Hedged 5-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 3Currency-Hedged 10-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 4Currency-Hedged 30-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

For USD-based investors, there are still some interesting opportunities available to find a USD-hedged foreign yield that can exceed that of US Treasuries. The higher-yielding European markets like Italy and Spain are the obvious places to find yield, and we continue to recommend those bonds with the ECB now buying more of the riskier euro area government bonds as part of its new Pandemic Emergency Purchase Program. However, Canadian, Australian and French bonds – hedged into USD – all offer intriguing yield pickups over US Treasuries. Even the negative yields available in Japan and Switzerland look interesting when expressed in USD terms, although that is not the case for negative yielding German bonds. Canadian, Australian and French bonds – hedged into USD – all offer intriguing yield pickups over US Treasuries. Even the negative yields available in Japan and Switzerland look interesting when expressed in USD terms, although that is not the case for negative yielding German bonds. In Tables 5-8, the currency-hedged yields for each country are shown as a spread to the relevant “base” bond yield for each currency. For example, under the “EUR” column in Table 6, the cells show the yield spread between 5-year government bonds hedged into euros and 5-year German bonds. Here, we can see that there are far fewer opportunities for euro-based bond investors to find non-European yields that offer adequate yield pickups versus German yields. The pickings are even less slim for Japanese investors, with many non-Japanese yields trading below Japanese yields on a JPY-hedged basis. Table 5Currency-Hedged 2-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 6Currency-Hedged 5-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 7Currency-Hedged 10-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 8Currency-Hedged 30-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

In sum, looking across all eight tables shown, the most consistently attractive yields, across all currencies and maturities, can be found in Australia, Canada, France, Italy and Spain. Bottom Line: Opportunities still exist in some countries to create synthetically “higher” yields relative to low local rates by hedging the currency exposure of foreign bonds. Italy and Spain government bonds offer the most attractive yields, hedged into any of the major currencies (USD, EUR, GBP, JPY). Among the lower yielders, Canadian, Australian, French and Japanese government bonds offer the most attractive yield pickups, on a currency-hedged basis, versus yields in the US, Germany, and the UK. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, "Central Banks To Markets: Redefining "Whatever It Takes"", dated March 24, 2020, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

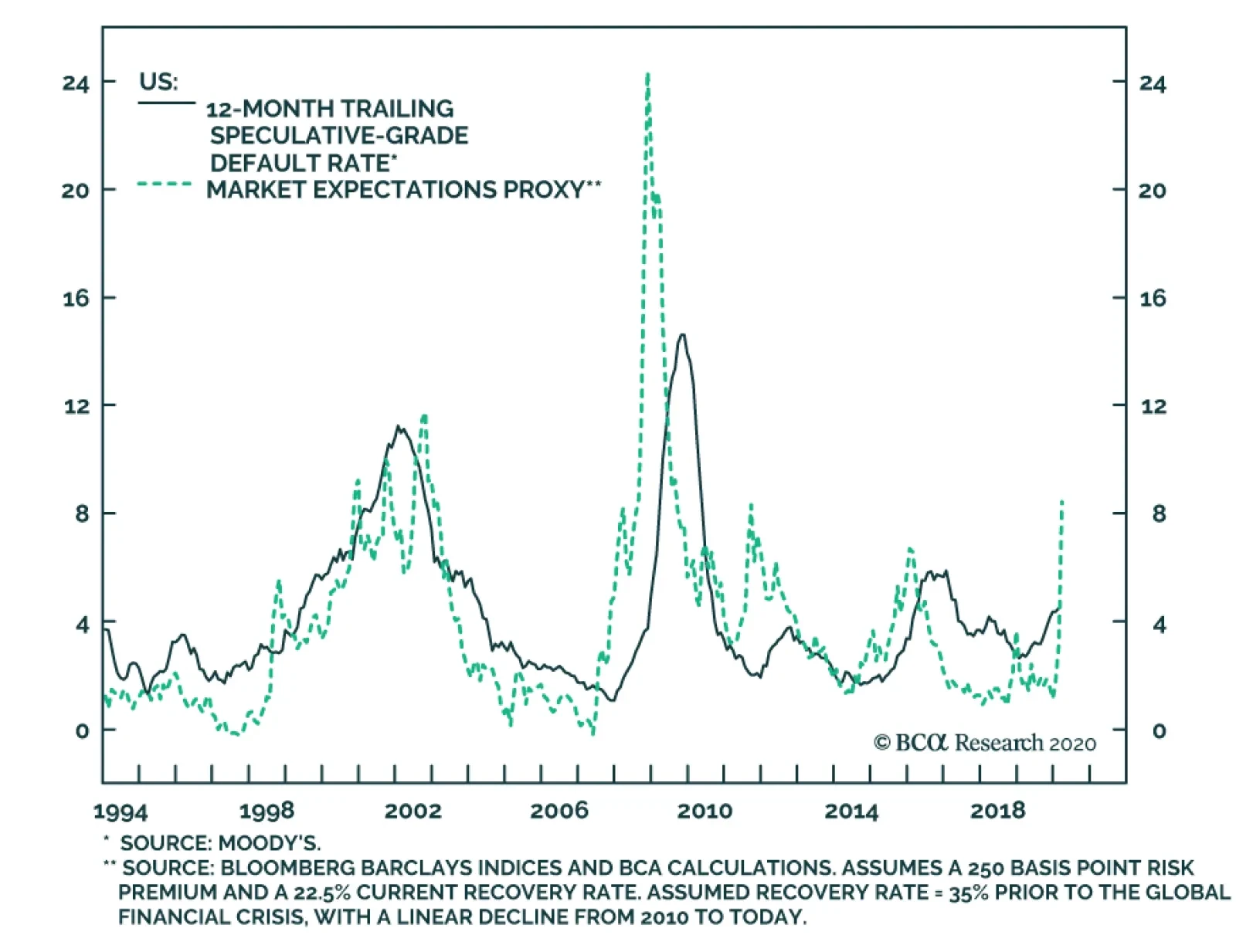

Highlights Chart 1Will Fed Purchases Mark The Top?

Will Fed Purchases Mark The Top?

Will Fed Purchases Mark The Top?

Policymakers can’t do much to boost economic activity when the entire population is under quarantine, but they can take steps to contain the ongoing credit shock and mitigate the risk of widespread corporate bankruptcy. If most firms can stay afloat, then at least there will be jobs to return to when shelter in place restrictions are lifted. Are the steps taken so far by the Federal Reserve and Congress sufficient in this regard? We expect that the Fed’s announcement of investment grade corporate bond purchases will mark the peak in investment grade corporate bond spreads (Chart 1). However, the Fed is doing nothing for high-yield issuers and its purchases only lower borrowing costs for investment grade firms, they don’t clean up highly levered balance sheets. Similarly, much of Congress’ fiscal stimulus package comes in the form of loans instead of grants. As such, ratings downgrades will surge and high-yield spreads probably have more near-term upside. Investors should keep portfolio duration close to benchmark, overweight investment grade corporate bonds and remain cautious vis-à-vis high-yield. Investors should also take advantage of the attractive long-run value in TIPS. Investment Grade: Overweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds underperformed the duration-equivalent Treasury index by 1040 basis points in March, dragging year-to-date excess returns down to -1268 bps. The average index spread widened 251 bps from the beginning of the month until the Fed announced its corporate bond purchase programs. It then tightened by 90 bps. It currently sits at 283 bps. Even after the recent tightening, investment grade spreads are extremely high relative to history. Our measure of the 12-month breakeven spread adjusted for changing index credit quality ranks at its 89th percentile since 1989 (Chart 2).1 This means that the sector has only been cheaper 11% of the time since 1989. As we wrote in last week’s Special Report, the Fed’s two new corporate bond purchase programs could be thought of as adding an agency guarantee to eligible securities (those with 5-years to maturity or less).2 We would also expect ineligible (longer maturity) securities to benefit from some knock-on effects, since many firms issue at both the short and long ends of the curve. As such, we recommend an overweight allocation to investment grade corporate bonds, with a preference for the short-end of the curve (5-years or less). The Fed’s purchases should lead to spread tightening, and a steepening of the spread curve (panel 4). Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

Containing The Credit Shock

Containing The Credit Shock

Table 3BCorporate Sector Risk Vs. Reward*

Containing The Credit Shock

Containing The Credit Shock

High-Yield: Neutral Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield underperformed the duration-equivalent Treasury index by 1330 basis points in March, dragging year-to-date excess returns down to -1659 bps. The average index spread widened 600 bps from the beginning of the month until the Fed announced its corporate bond purchase programs. It then tightened by 158 bps. It currently sits at 942 bps. As we wrote in last week’s Special Report, the Fed’s corporate bond purchases will cause investment grade corporate spreads to tighten, but so far, high-yield has been left out in the cold.3 This means that we must view high-yield spreads in the context of what sort of default cycle we expect for the next 12 months. To do that, we use our Default-Adjusted Spread – the excess spread available in the index after accounting for default losses. At current spreads, our base case expectation of an 11%-13% default rate and 20%-25% recovery rate implies a Default-Adjusted Spread between -98 bps and +117bps (Chart 3). For a true buying opportunity, we would prefer a Default-Adjusted Spread above its historical average of 250 bps. This means that we would consider upgrading high-yield to overweight if the index spread widens to a range of 1075 bps – 1290 bps, in the near-term. Until then, junk investors should stay cautious. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 22 basis points in March, dragging year-to-date excess returns down to -81 bps. The conventional 30-year zero-volatility spread widened 13 bps on the month, driven by a 16 bps widening of the option-adjusted spread that was offset by a 3 bps decline in expected prepayment losses (aka option cost). Like investment grade corporates, MBS spreads will benefit from aggressive Fed purchases for the foreseeable future. However, we prefer investment grade corporates over MBS because of much more attractive valuations. Notice that the option-adjusted spread offered by a Aa-rated corporate bond is 98 bps greater than that offered by a conventional 30-year MBS (Chart 4). Further, servicer back-log is currently keeping primary mortgage rates elevated compared to both Treasury and MBS yields (panels 4 & 5). This is preventing many homeowners from refinancing, despite the Fed’s dramatic rate cuts. However, we expect these homeowners will eventually get their chance. The Fed will be very cautious about raising rates in the future, and primary mortgage spreads will tighten as servicers add capacity. This means that there is a significant amount of refi risk that is not yet priced into MBS. Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related Index underperformed the duration-equivalent Treasury index by 574 basis points in March, dragging year-to-date excess returns down to -667 bps. Sovereign debt underperformed duration-equivalent Treasuries by 1046 bps in March, dragging year-to-date excess returns down to -1375 bps. Foreign Agencies underperformed the Treasury benchmark by 850 bps on the month, dragging year-to-date excess returns down to -1023 bps. Local Authority debt underperformed Treasuries by 990 bps in March, dragging year-to-date excess returns down to -948 bps. Domestic Agency bonds underperformed by 96 bps in March, dragging year-to-date excess returns down to -103 bps. Supranationals underperformed by 70 bps on the month, dragging year-to-date excess returns down to -63 bps. USD-denominated Sovereigns handily outperformed Baa-rated corporate bonds during last month’s market riot (Chart 5). But going forward, we prefer to grab the extra spread available in Baa-rated corporates, with the added bonus that the corporate sector now benefits from direct Fed purchases. The Fed’s dollar swap lines should remove some of the liquidity premium priced into sovereign spreads, but these swap lines only extend to 14 countries (Euro Area, Canada, UK, Japan, Switzerland, Australia, Brazil, Denmark, Korea, Mexico, Norway, New Zealand, Singapore and Sweden) and further dollar appreciation is possible until global growth recovers. One silver lining of last month’s indiscriminate spread widening is that some value has been created in traditionally low-risk sectors. Specifically, the Domestic Agency and Supranational option-adjusted spreads are at 46 bps and 31 bps, respectively (bottom panel). Both look like attractive buying opportunities. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by a whopping 649 basis points in March, dragging year-to-date excess returns down to -755 bps (before adjusting for the tax advantage). In fact, Aaa-rated Municipal / Treasury yield ratios have blown out across the entire curve and have made new all-time highs, above where they were during the 2008 financial crisis (Chart 6). While the spread levels are alarming, it’s not hard to understand why muni spread widening has been so dramatic. State and local governments are not only shouldering massive expenses fighting the COVID-19 crisis, but will also see tax revenues plunge as economic activity grinds to a halt. This opens up a massive whole in state & local government budgets and municipal bond prices are reacting in kind. Support in the form of Fed municipal bond purchases and direct cash injections from the federal government is required to right the ship. So far, the Fed is only supporting municipal debt with less than six months to maturity and federal government aid has come in the form of grants directed at specific spending areas. Ideally, the Fed will start purchasing long-dated municipal bonds (as it is doing with corporates) and the federal government will provide more direct aid to fill budget gaps. We expect both of those policies to be launched in the coming weeks, and thus think it is a good time to buy municipal bonds on the expectation that the “policy put” will drive spreads lower. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve underwent a massive bull-steepening in March, as the Fed cut rates by 100 bps, all the way back to the zero bound. The 2-year/10-year Treasury slope steepened 20 bps on the month. It currently sits at 39 bps. The 5-year/30-year Treasury slope steepened 22 bps on the month. It currently sits at 85 bps. One good thing about the fed funds rate being pinned at zero is that it greatly simplifies yield curve strategy. As we showed in a recent report, when the funds rate is at its lower bound the Treasury slope will trade directionally with yields.4 That is, the yield curve will steepen when yields rise and flatten when they fall. Therefore, if you want to put on a position that will profit from lower yields but that doesn’t increase the average duration of your portfolio, you can enter a duration-neutral flattener: long a 2/10 or 2/30 barbell and short the 5-year or 7-year bullet, in duration-matched terms. Or, if like us, you do not want to make a large duration bet but suspect that Treasury yields will be higher in 12 months, you can enter a duration-neutral steepener: long the 5-year bullet and short a duration-matched 2/10 barbell.5 In terms of value, the 5-year yield no longer trades deeply negative relative to the 2/10 and 2/30 barbells (Chart 7), though it remains somewhat expensive according to our models (see Appendix B). TIPS: Overweight Chart 8Inflation Compensation

Inflation Compensation

Inflation Compensation

TIPS underperformed the duration-equivalent nominal Treasury index by 515 basis points in March, dragging year-to-date excess returns down to -735 bps. The 10-year TIPS breakeven inflation rate fell 55 bps on the month. It currently sits at 1.09%. The 5-year/5-year forward TIPS breakeven inflation rate fell 24 bps on the month. It currently sits at 1.39%. As we noted in a recent report, the market crash has created an extraordinary amount of long-run value in TIPS.6 For example, the 10-year and 5-year TIPS breakeven inflation rates have fallen to 1.09% and 0.78%, respectively. This means that a buy & hold position long the TIPS and short the equivalent-maturity nominal Treasury will make money if average annual inflation is greater than 0.78% for the next five years, or greater than 1.09% for the next ten (Chart 8). This seems like a slam dunk. Even on a 1-year horizon, we would argue that TIPS trades make sense. We calculate that the TIPS note maturing in April 2021 will deliver greater returns than a 12-month T-bill as long as headline CPI inflation is above -1.25% during the next 12 months (panel 4). Granted, the oil price collapse is a significant drag on CPI (bottom panel). But, we would also note that the worst year-over-year CPI print during the 2008 financial crisis was -2.1% and this included deflation in the shelter component. Shelter accounts for 33% of the CPI, compared to only 7% for Energy. ABS: Underweight Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 342 basis points in March, dragging year-to-date excess returns down to -317 bps. The index option-adjusted spread for Aaa-rated ABS soared 158 bps on the month. It currently sits at 163 bps, well above average historical levels (Chart 9). Aaa-rated consumer ABS were not immune to the recent sell-off, but we think today’s elevated spreads signal an opportunity to increase exposure to the sector. In addition to the value argument, the Fed’s re-launched Term Asset-Backed Securities Loan Facility (TALF) should cause Aaa-rated ABS spreads to tighten in the coming months. Through TALF, eligible private investors can take out non-recourse loans from the Fed and use the proceeds to purchase Aaa-rated ABS. In our view, the combination of elevated spreads and direct Fed support for the sector suggests a buying opportunity in Aaa-rated consumer ABS. Non-Agency CMBS: Neutral Underweight Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-agency Commercial Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 786 basis points in March, dragging year-to-date excess returns down to -785 bps. The index option-adjusted spread for non-agency Aaa-rated CMBS widened 133 bps on the month. It currently sits at 217 bps, well above typical historical levels (Chart 10). Despite wide spreads, we are hesitant about stepping into the sector. The Fed has so far not extended its asset purchases to non-agency CMBS. There are other sectors – such as consumer ABS, Agency CMBS, and investment grade corporate bonds – that also offer attractive spreads and are benefitting directly from Fed support. Agency CMBS: Overweight Agency CMBS underperformed the duration-equivalent Treasury index by 394 basis points in March, dragging year-to-date excess returns down to -361 bps. The average index spread for Agency CMBS widened 74 bps on the month. It currently sits at 121 bps, well above typical historical levels (panel 3). Unlike its non-agency counterpart, the Fed is buying Agency CMBS as part of its mortgage-backed securities purchase program. The combination of an elevated spread and direct Fed support makes the Agency CMBS sector a high conviction overweight. Appendix A: The Golden Rule Of Bond Investing With the federal funds rate pinned at its effective lower bound for the foreseeable future, yield volatility at the front-end of the curve will decline markedly. This means that the 12-month fed funds rate expectations embedded in the yield curve provide little useful information. As such, our Golden Rule of Bond Investing is not a useful framework for implementing duration trades when the fed funds rate is pinned at zero. We will therefore temporarily stop updating the Golden Rule tables that were previously shown in Appendix A of our monthly Portfolio Allocation Summary. The Golden Rule framework will return when the fed funds rate is close to lifting off from zero. Please feel free to contact us if you have any questions. Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of April 3, 2020)

Containing The Credit Shock

Containing The Credit Shock

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of April 3, 2020)

Containing The Credit Shock

Containing The Credit Shock

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 46 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 46 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

Containing The Credit Shock

Containing The Credit Shock

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of April 3, 2020)

The Golden Rule's Track Record

The Golden Rule's Track Record

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 The 12-month breakeven spread is the spread widening required to deliver negative excess returns versus duration-matched Treasuries on a 12-month horizon. 2 Please see US Bond Strategy/Global Fixed Income Strategy Special Report, “Trading The US Corporate Bond Market In A Time Of Crisis”, dated March 31, 2020, available at usbs.bcaresearch.com 3 Please see US Bond Strategy/Global Fixed Income Strategy Special Report, “Trading The US Corporate Bond Market In A Time Of Crisis”, dated March 31, 2020, available at usbs.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “Life At The Zero Bound”, dated March 24, 2020, available at usbs.bcaresearch.com 5 The rationale for why barbell positions profit from curve flattening and bullet positions profit from curve steepening is found in US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

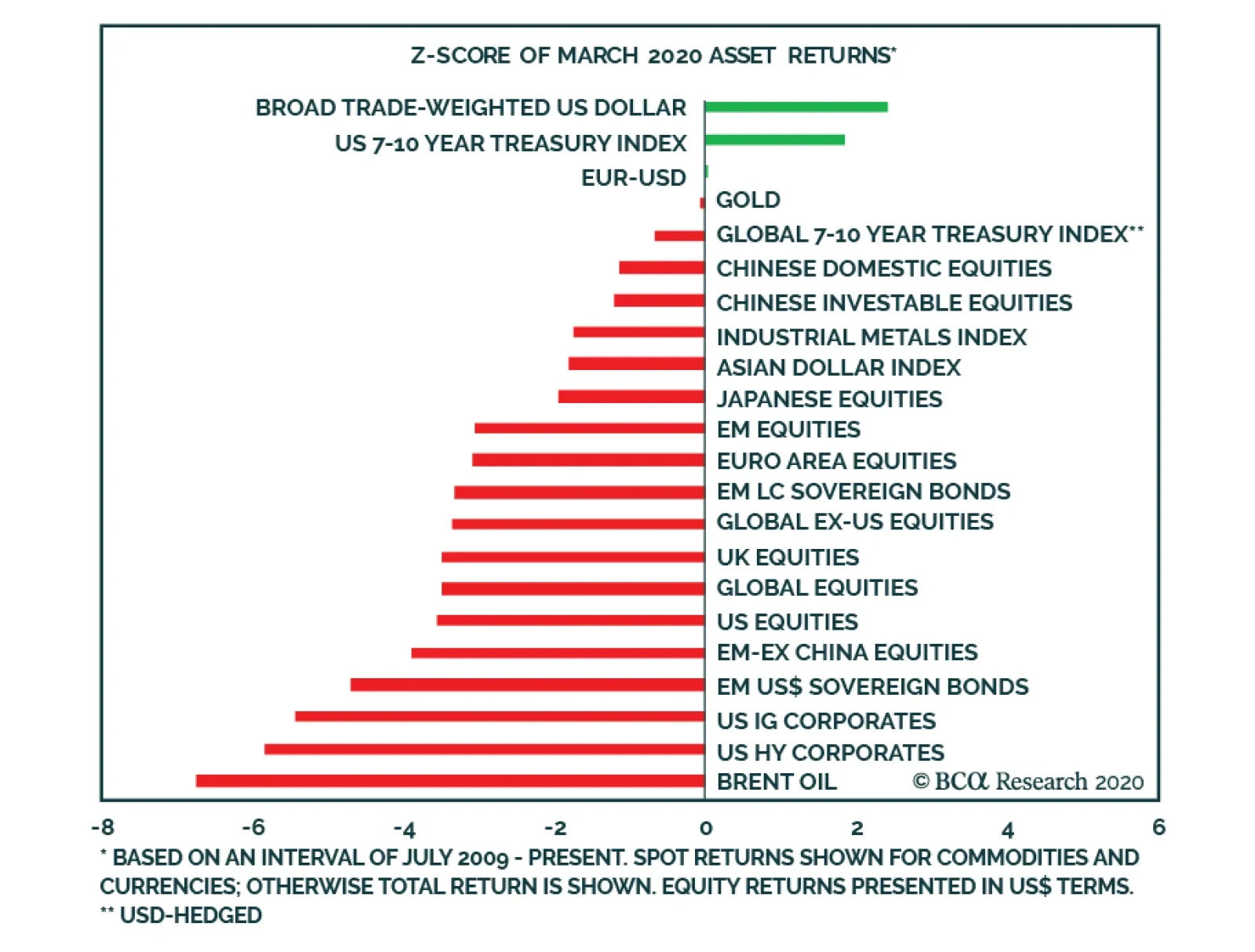

The chart above presents the March monthly returns of a variety of important financial assets, shown as the number of standard deviations from the average that has prevailed since the end of the Great Recession in 2009. Several points are noteworthy: The…

Highlights Please note that we published a Special Report early this week titled Brazilian Banks: Falling Angels, and an analysis on India. Please also note that we are publishing an analysis on Indonesia below. Given uncertainty over the depth and duration of the unfolding global recession, a sustainable equity bull run is now unlikely. It is still early to lift EM equity and EM credit allocations from underweight to overweight within global equity and global credit portfolios, respectively. EM currencies and EM fixed-income markets will remain under selling pressure. Feature The question investors now face is whether the recent rebound will endure for a few months or it will just be a bear market rebound that is already fading. BCA’s Emerging Market Strategy service believes it is the latter. EM and DM share prices will likely make new lows. A Tale Of Two Charts Chart I-1and I-2 overlay the current S&P 500 selloff with the market crashes of 1987 and 1929, respectively. The speed and ferocity of the current selloff is on a par with both. In 1987, following the 33% crash, share prices rebounded 14% but then relapsed without breaking below previous lows (Chart I-1). That was a hint that US share prices were entering a major bull market that indeed ensued. We do not know if the S&P 500 will make a lower low, but a retest of the recent lows is very likely. In 1929, US share prices collapsed by 36% over several weeks. Then, the overall index staged an 18% rebound within a couple of weeks, rolled over and plunged to new lows. The magnitude of the second downleg was 27% (Chart I-2). Chart I-1S&P 500: Now Versus 1987

S&P 500: Now Versus 1987

S&P 500: Now Versus 1987

Chart I-2S&P 500: Now Versus 1929

S&P 500: Now Versus 1929

S&P 500: Now Versus 1929

Fast forward to today, the S&P 500 plummeted 34% in a matter of only four weeks and then staged a 17.5% rebound in only a few days. We do not know if the S&P 500 will make a lower low, but a retest of the recent lows is very likely. In fact, we are assigning a higher probability to share prices in EM and DM breaking down to new lows than for the recent lows to hold. Chart I-3S&P 500: Now Versus 1929-32

S&P 500: Now Versus 1929-32

S&P 500: Now Versus 1929-32

Readers may question why we are comparing the current episode with the 1929 bear market. The argument against this comparison stresses that policymakers made numerous mistakes between 1929 and 1932, refusing to ease policy even after the crisis commenced. That led to debt deflation and a banking crisis, which in turn produced a vicious equity bear market of 85% lasting 3 years. At present, authorities around the world have reacted swiftly, providing enormous fiscal and monetary stimulus. We agree with this reasoning, but our point is as follows: Due to the US’s ongoing aggressive and timely policy response, stocks will avoid the protracted second phase of the 1930-‘32 bear market when share prices plummeted by another 80% (Chart I-3). Nonetheless, the US equity market could still repeat what occurred in the initial part of the 1929 bear market, as illustrated in Chart I-2 and Chart I-3. The Fundamentals The basis for our expectations of continued weakness in share prices is as follows: The selloff in the S&P 500 began from overbought and expensive levels (Chart I-4). The duration of the selloff so far has been only four weeks. We doubt that such a short, albeit vicious, selloff was enough to clear out valuation and positioning excesses. For example, even though by March 24 net long positions in US equity futures had dropped significantly, they were still above their 2011 and 2015/16 lows (Chart I-5). Chart I-4S&P 500: Correcting From Expensive Levels

S&P 500: Correcting From Expensive Levels

S&P 500: Correcting From Expensive Levels

Chart I-5Net Long Positions In US Equity Indexes Futures

Net Long Positions In US Equity Indexes Futures

Net Long Positions In US Equity Indexes Futures

Besides, US equity valuations are still elevated. The cyclically adjusted P/E ratio for the S&P 500 – based on operating profits – is 25 compared with its historical mean of 16.5, as demonstrated in the top panel of Chart I-4. While this valuation model does not take into account interest rates, our hunch is as follows: facing such high uncertainty over the profit outlook, investors will require higher than usual risk premiums to invest in equities. In short, the ongoing profit collapse and the extreme uncertainty over the cyclical outlook heralds a higher risk premium. The discount rate – which is the sum of the risk-free rate and risk premium – presently should not be lower than its average over the past 20 years. We are experiencing a sort of natural disaster, and there is little policymakers can do amid lockdowns. Natural disasters require time to play out, and financial markets are attempting to price in this downturn. Most stimulus measures taken worldwide to boost demand will only gain traction after the lockdowns are over. At the moment, global output and demand remain in freefall. The recovery will be hesitant and is unlikely to be V-shaped for two reasons: (1) social distancing measures will be eased only gradually; and (2) the lost household income and corporate profits from weeks and months of shutdowns will continue to weigh on consumer and business sentiment and their spending patterns for several months. China’s economy is a case in point. Both manufacturing and services PMIs for March posted readings in the 50-52 range. These are rather underwhelming numbers. Following stringent lockdowns in February when the level of economic output literally collapsed, only 52% of companies surveyed reported an improvement in their business activity/new orders in March relative to February. Chart I-6Our Reflation Confirming Indicator Is Downbeat

Our Reflation Confirming Indicator Is Downbeat

Our Reflation Confirming Indicator Is Downbeat

If true, these PMI readings imply a level of output and demand in China that is still well below March 2019 levels. It seems China has not been able to engineer a V-shaped recovery in demand and output. Therefore, the odds are that, outside China, economic activity will come back only slowly. This entails that some businesses will not reach their breakeven points anytime soon, and that their profits will be contracting for some time to come. We do not think this is reflected in today’s asset prices. Finally, our Reflation Confirming Indicator – which is composed of equally-weighted prices of industrial metals, platinum and US lumber – is pointing down (Chart I-6). Bottom Line: This bear market has been ferocious, but too short in duration. It is unlikely that share prices have already bottomed, given uncertainty over the depth and duration of the unfolding global recession. EM Versus DM: Stay Underweight Chart I-7EM Versus DM: Relative Equity Prices

EM Versus DM: Relative Equity Prices

EM Versus DM: Relative Equity Prices

EM stocks have failed to outperform DM equities in the recent rebound. As a result, EM versus DM relative share prices are testing new lows (Chart I-7). Odds are that EM will underperform DM in the coming weeks or months. Outside North Asian economies (China, Korea and Taiwan), EM countries have less capacity to deal with the COVID-19 pandemic than advanced countries. First, health care systems in developing countries are far less equipped to deal with the pandemic than DM ones. Chart I-8 shows the number of hospital beds per 1,000 people in India, Indonesia, Brazil and Mexico are significantly lower than in Europe and the US. Chart I-8Many EMs Have Poor Health Infrastructure

Downside Risks Prevail

Downside Risks Prevail

Second, EM ex-North Asian economies lack both the social safety net of Europe and the US’s capacity to inject large amounts of fiscal and monetary stimulus into the system. With the US dollar being the world reserve currency, the US has no problem monetizing its public debt and fiscal deficits. The same is true for the European Central Bank (ECB). If current account-deficit EM countries following in the footsteps of the US and monetize fiscal deficits/public debt, their currencies will likely depreciate. Last week, the South African central bank announced that it will buy local currency government bonds to cap their yields and inject liquidity into the system. This is of little help to foreign investors in domestic bonds because the rand has continued to sell off, eroding the US dollar value of their government bond holdings. Hence, the foreign investor exodus from the local currency bond market will likely continue. The same would be true for many other EM countries if they contemplate QE-type policies. Most stimulus measures taken worldwide to boost demand will only gain traction after the lockdowns are over. Third, unlike the Fed and the ECB, EM ex-North Asia central banks have limited capacity to alleviate funding stress for their companies. The Fed is also purchasing investment-grade corporate bonds and is setting up structures to channel credit to companies. All of this will marginally help ease financial and credit stress in the US. In contrast, central banks in EM ex-North Asia are unlikely to adopt similar policies on a comparable scale as the US. While DM countries do not mind seeing their currencies depreciate, authorities in many developing countries are fearful of further depreciation. The latter will inflict more stress on EM companies and banks that have large foreign currency debt. We will publish a report on EM foreign currency debt next week. Further, corporate bonds in DM are issued in local currency, allowing their central banks to purchase corporate bonds in unlimited quantities by creating money “out of thin air.” Chart I-9EM Performance Correlates With Commodities

EM Performance Correlates With Commodities

EM Performance Correlates With Commodities

In contrast, outside of China and Korea, the majority of EM corporate bonds are issued in US dollars. This means that to bring down their corporate US borrowing costs, central banks in developing countries need to spend their finite US dollar reserves. Finally, commodities prices are critical to EM financial markets’ absolute and relative performance (Chart I-9). The outlook for commodities prices remains dismal. As the global economy has experienced a sudden stop, demand for raw materials and energy has literally evaporated. Liquidity provisions by the Fed and other key central banks may at a certain point help financial assets but will not help commodities. The basis is that demand for equities and bonds is entirely driven by investors, but in the case of commodities a large share of demand comes from the real economy. In bad times like these, central banks’ liquidity provisions can at a certain point persuade investors to look through the recession and begin buying financial assets before the real economy bottoms. In the case of commodities, when real demand is collapsing, financial demand will not be able to revive commodities prices. Bottom Line: It is still early to lift EM equity and EM credit allocations from underweight to overweight within global equity and global credit portfolios, respectively. Technicals: Old Support = New Resistance? Calling tops and bottoms in financial markets is never easy. When formulating investment strategy it is helpful to examine both market price actions and other subtle clues that financial markets often provide. The global equity index and global industrial stocks have rebounded to levels that acted as supports during previous selloffs. We have detected the following patterns that suggest the recent rebound is facing major resistance, and new lower lows are likely: The global equity index and global industrial stocks have rebounded to levels that acted as supports during previous selloffs (Chart I-10). Unless these equity indexes decisively break above these lines, the odds favor retesting their recent lows or even falling to new lows. Many other equity indexes and individual stocks are also displaying similar technical patterns. The Korean won versus the US dollar as well as silver prices exhibit a similar technical profile (Chart I-11). Chart I-10Ominous Technical Signals

Ominous Technical Signals

Ominous Technical Signals

Chart I-11New Lows Ahead

New Lows Ahead

New Lows Ahead

Global materials have decisively broken below their long-term moving average that served as a major support in 2002, 2008 and 2015 (Chart I-12). The same multi-year moving average is now likely to act as a resistance. Hence, any rebound in global materials stocks – that extremely closely correlate with EM share prices – is very unlikely to prove durable until this support-turned-resistance level is decisively breached. US FAANGM (FB, AMZN, APPL, NFLX, GOOG, MSFT) equally-weighted stock prices have dropped below their 200-day moving average that served as a major support in recent years (Chart I-13). They did rebound but have not yet broken above the same line. Odds are that this line will become a resistance. If true, this will entail new lows in FAANGM stocks. Chart I-12Global Materials Broke Below Their Long-Term Defense Line

Global Materials Broke Below Their Long-Term Defense Line

Global Materials Broke Below Their Long-Term Defense Line

Chart I-13FAANGM: Previous Support Has Become New Resistance

FAANGM: Previous Support Has Become New Resistance

FAANGM: Previous Support Has Become New Resistance

Bottom Line: Various financial markets are exhibiting technical patterns consistent with retesting recent lows or making lower lows. Stay put. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Indonesia: A Fallen Angel Chart II-1Indonesian Equities Are In Freefall In Absolute & Relative Terms

Indonesian Equities Are In Freefall In Absolute & Relative Terms

Indonesian Equities Are In Freefall In Absolute & Relative Terms

Indonesian stock prices are in freefall - both in absolute terms and relative to EM - with no visible support (Chart II-1). We recommend that investors maintain an underweight position in both Indonesian equities and fixed-income and continue to short the rupiah versus the US dollar. We explain the reasoning behind this recommendation below. First, the key vulnerability of Indonesian financial markets is that they had been supported by massive foreign inflows stirred by falling US interest rates, despite deteriorating domestic fundamentals and falling commodities prices. We discussed this at length in our previous reports. However, the COVID-19 pandemic has brought these weak fundamentals to light. The latter have overshadowed falling US interest rates (Chart II-2) triggering an exodus of foreign portfolio capital and a plunge in the exchange rate. Currency depreciation has in turn mounted foreign investors losses resulting in a vicious feedback loop. As of the end of February, foreigners held about 37% of local currency bonds. Meanwhile, they held 56% of equities as of last week. Ongoing currency weakness and continued jitters in global financial markets will likely generate more foreign capital outflows. Second, the Indonesian economy - both domestic demand and exports - were already weak even before the breakout of COVID-19 occurred (Chart II-3). Chart II-2Indonesia: Falling US Rates Stopped Mattering

Indonesia: Falling US Rates Stopped Mattering

Indonesia: Falling US Rates Stopped Mattering

Chart II-3Indonesia: Domestic Demand Was Weak Before COVID-19 Outbreak

Indonesia: Domestic Demand Was Weak Before COVID-19 Outbreak

Indonesia: Domestic Demand Was Weak Before COVID-19 Outbreak

Chart II-4Indonesia: Struggling Under High Lending Rates

Indonesia: Struggling Under High Lending Rates

Indonesia: Struggling Under High Lending Rates

With imposition of social distancing measures, output and nominal incomes will contract (Chart II-4). Third, the nation’s very underdeveloped health care system makes it more vulnerable to a pandemic compared to other mainstream EM countries. For example, the number of hospital beds per 1000 people - at 1.2 - is among the lowest within the mainstream EM universe. We discuss this issue for EM in greater detail in our most recent weekly report. In brief, it will take a longer time for this nation to overcome the pandemic and get its economy back on track. Fourth, Indonesia - as with many EM countries - is short on both social safety programs and fiscal stabilizers that are available in North Asian countries, Europe and the US. Moreover, the country lacks the administrative system needed to promptly execute fiscal stimulus. Besides, the economic stimulus announced by the Indonesian authorities is so far insufficient to meaningfully moderate the economic blow. The government announced a fiscal stimulus that barely amounts to 1% of GDP. This will do little to counter the recession that the nation’s economy is now entering. On the monetary policy front, though the central bank has been cutting policy rates and injecting local currency liquidity into the system, this will only help reduce liquidity stress. It will not directly aid ailing households and small businesses suffering from an income shock. Critically, prime lending rates have not dropped despite dramatic cuts in policy rates (Chart II-4). Chart II-5Bank Stocks - Last Shoe To Drop - Are Unraveling Now

Bank Stocks - Last Shoe To Drop - Are Unraveling Now

Bank Stocks - Last Shoe To Drop - Are Unraveling Now

Meanwhile, the government’s decision to grant a debt servicing holiday to borrowers will only help temporarily. These borrowers will still need to repay their debts at some point down the line. Given the magnitude and uncertain duration of their income loss, there is no guarantee they will be in a position to service their debt after the pandemic is over. Eventually, Indonesian commercial banks will experience a large increase in non-performing loans (NPLs). Overall, the plunge in domestic demand combined with the fall in global trade and commodities prices entails that Indonesia is heading into its first recession since 1998. Given Indonesia has for many years been one of the darlings of EM investors, a recession in Indonesia and global flight to safety herald continued liquidation in its financial markets. Both local government bond yields and corporate US dollar bonds yields are breaking out. Rising borrowing costs amidst the recession will escalate the selloff in equities. Remarkably, non-financial stocks and small-caps have already fallen by 40% and 55% in US dollar terms, respectively (Chart II-5, top two panels). It was banks stocks – which comprise 35% of total market cap – that were holding up the overall index (Chart II-5, bottom panel). Given banks will likely experience rising defaults as discussed above, their share prices have more risk to the downside. Bottom Line: Absolute return investors should stay put on Indonesian risk assets for now. We maintain our short position on the rupiah versus the US dollar. EM-dedicated equity investors should keep underweighting Indonesian equities within an EM equity portfolio. Meanwhile, EM-dedicated fixed income investors should continue to underweight Indonesian local currency bonds as well as sovereign and corporate credit. Ayman Kawtharani Editor/Strategist ayman@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights The economic shutdown needed to exhaust the coronavirus pandemic must last much longer than is anticipated. For example, in Italy it must last 24 weeks. If the economy is reopened too soon, the pandemic will reignite in a second wave later this year, just as in 1918. Take the 12 percent profit in the tactical overweight to equities versus bonds and go neutral. Stay underweight European equities and euro area banks given their high sensitivity to the economy. Stay overweight US T-bonds versus German bunds and Swiss bonds. All high-quality bond yields will eventually reach the lower bound of -1 percent, making US T-bonds the most attractive in class. The euro is a structural overweight but a tactical neutral – because in equity market corrections the repatriation of foreign investments into domestic cash boosts the demand for dollars relative to the euro. Fractal trades: Go long Australia versus New Zealand. Short palladium versus nickel was closed at 32 percent profit. Feature “You’ve got to understand that you don’t make the timeline, the virus makes the timeline” – Dr. Anthony Fauci, Director of the National Institute of Allergy and Infectious Diseases It’s A Biological Crisis The coronavirus crisis is first and foremost a biological crisis. This makes it fundamentally different to the 2008 global financial crisis, the 2000 dot com bust, the 1990 Japanese crash, and the 1930s Great Depression – all of which were financial crises needing financial and economic cures. As such, the current crisis needs to be analysed very differently. Crucially, the financial and economic policy responses to the coronavirus crisis are only a palliative, not a cure. The cure is to exhaust the coronavirus pandemic. But to exhaust the pandemic without overburdening stretched healthcare systems will require shutting the economy for months. If the economy is reopened too soon, then the pandemic will reignite in a second and a possible third wave just as in 1918-19 (Chart of the Week). Chart I-1If The Economy Is Reopened Too Soon The Pandemic Will Reignite, Just As In 1918-19

If The Economy Is Reopened Too Soon The Pandemic Will Reignite, Just As In 1918-19

If The Economy Is Reopened Too Soon The Pandemic Will Reignite, Just As In 1918-19

The US fiscal stimulus package amounts to 10 percent of annual GDP. But if exhausting the pandemic requires a third of the economy to be shut for a third of the year, then the economy would lose one ninth, or 11 percent, of its annual output. Hence, despite the biggest fiscal boost of all time, the economy would end up shrinking (Chart I-2). Chart I-2Fiscal Stimulus Is Massive, But Might Not Be Enough

The Economy Must Shut For 24 Weeks

The Economy Must Shut For 24 Weeks