Fixed Income

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 60 basis points in October, bringing year-to-date excess returns up to +429 bps. When gauging the outlook for corporate bonds, we consider three main factors as part of…

Highlights While the Caixin PMI is pointing to improving economic conditions, other data series still reflect weak growth. China’s business cycle is likely to bottom in Q1 of next year, rather than in Q4. The failure of Chinese stocks to significantly outperform the global benchmark and the continued underperformance of cyclical stocks underscore the near-term risks to equities if this month’s trade & manufacturing data disappoint. We continue to recommend a neutral tactical stance (0-3 months) towards Chinese equities versus global stocks, but expect them to outperform on a cyclical (6-12 month) time horizon after economic growth firmly bottoms. Feature Tables 1 and 2 on pages 2 and 3 highlight key developments in China’s economy and its financial markets over the past month. On the growth front, the data remains mixed: the strength in the October Caixin PMI and the September pickup in electricity production are positive signs, but other important datapoints still point to weak conditions. We continue to expect that China’s business cycle is likely to bottom in Q1 of next year, rather than in Q4. We continue to expect that growth will bottom in Q1 of next year, rather than in Q4. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Within financial markets, Chinese stocks have rallied in absolute terms over the past month in response to greatly increased odds of a trade truce between China and the US, but have failed to outperform the global benchmark. This, in combination with the continued underperformance of cyclical stocks, suggests that hard evidence of an economic improvement in China will be required before Chinese stocks begin to rise in relative terms. The risk of near-term underperformance is still present, especially if October’s hard trade and manufacturing data disappoint. We continue to recommend a neutral tactical stance (0-3 months) towards Chinese equities versus global stocks, but expect them to outperform on a cyclical (6-12 month) time horizon after economic growth firmly bottoms. In reference to Tables 1 and 2, we provide below several detailed observations concerning developments in China’s macro and financial market data: Chart 1Not Yet A Clear Change In Trend

Not Yet A Clear Change In Trend

Not Yet A Clear Change In Trend

The Bloomberg Li Keqiang index (LKI) ticked up in September, led by an improvement in electricity production. An improvement in the LKI in lockstep with a rising Caixin manufacturing PMI (discussed below) raises the odds that the Chinese economy may be bottoming earlier than we expect, but for now only modestly so. Chinese economic data is highly volatile, and Chart 1 shows that the improvement in the LKI is very muted when shown as a 3-month moving average. In addition, a slight improvement also occurred earlier this year, but proved to be a false signal. All told, for now we continue to expect that growth will bottom in Q1 of next year, rather than in Q4. Our leading indicator for the LKI was essentially flat in September on a smoothed basis, with sequential declines in M3 growth and the credit components of the indicator offsetting improvements in monetary conditions and M2. From a big picture perspective, the story of our LKI leading indicator remains unchanged: it continues to trend higher, at a much shallower pace than has been the case during previous easing cycles. The uptrend is the basis of our forecast that China’s growth will soon bottom, but the uncharacteristically shallow nature of the rise suggests that the eventual recovery will be modest. On a smoothed basis, Chinese residential floor space sold improved again in September, following a very significant rise in August. Over the past 12-18 months, we had emphasized that the double-digit pace of growth in China’s housing starts was unsustainable because it had entirely decoupled from the trend in sales (which have reliably led construction activity over the past decade). This gap disappeared over the summer due to a significant slowdown in starts, which is what we predicted would occur. However, the recent acceleration in floor space sold represents a legitimate fundamental improvement in the housing market, that for now is difficult to attribute to the recent drivers of housing demand (Chart 2).1 Still, investors should continue to watch China’s housing demand data closely over the coming few months, for further signs of a potential re-acceleration in housing construction. Investors need to see meaningful sequential improvements in China’s October trade and manufacturing data. The October improvement in China’s Caixin PMI was quite notable, as it appears to confirm the full one-point rise in the index that occurred in September and suggests that manufacturing in China’s private-sector is now durably expanding. Still, conflicting signals remain: the official PMI fell in October and remains below 50, and the significant September improvement in the Caixin PMI was not corroborated by an improvement in producer prices or nominal import growth (Chart 3). As PMIs are simply timely coincident indicators that do not generally have leading properties, investors will need to see meaningful sequential improvements in China’s October trade and manufacturing data in order to have confidence that the Caixin PMI improvement is not a false signal. Chart 2It Is Not Yet Apparent What Is Driving A Pickup In Housing Demand

It Is Not Yet Apparent What Is Driving A Pickup In Housing Demand

It Is Not Yet Apparent What Is Driving A Pickup In Housing Demand

Chart 3If The Caixin PMI Is Not A False Signal, A Hard Data Improvement Must Occur Soon

If The Caixin PMI Is Not A False Signal, A Hard Data Improvement Must Occur Soon

If The Caixin PMI Is Not A False Signal, A Hard Data Improvement Must Occur Soon

Chinese stocks have rallied 6-7% over the past month in absolute terms, but have modestly underperformed global equities. The rally in global stock prices has occurred largely in response to the mid-October announcement of a trade truce between China and the US. The failure of Chinese stocks to outperform during this period suggests hard evidence of an economic improvement in China will be required before Chinese stocks begin to outpace their global peers. At the regional equity level, the other notable development over the past month has been the continued outperformance of the MSCI Taiwan Index versus the global benchmark. Taiwan’s outperformance has been boosted by a rising TWD versus the dollar, but Taiwanese stocks have also outperformed in local currency terms. Taiwan province is highly exposed to global trade, and it is not surprising that equities have reacted positively to the prospect of a trade truce between the US and China. Further meaningful outperformance, however, will likely require a re-acceleration in Taiwanese exports, as export growth has merely halted its contraction (Chart 4). Within China’s investable equity market, cyclicals have underperformed defensives over the past month after having rallied significantly from late-August to mid-September (Chart 5). We noted in our October 30 Special Report that these cyclical sectors have historically been positively correlated with pro-cyclical macroeconomic and equity market variables,2 and their underperformance versus defensives is thus consistent with the failure of Chinese stocks in the aggregate to outperform global equities over the past month. In both cases, outperformance likely requires hard evidence of an upturn in China’s business cycle. Chart 4Export Growth Needs To Improve In Order To Expect Further Taiwanese Relative Outperformance

Export Growth Needs To Improve In Order To Expect Further Taiwanese Relative Outperformance

Export Growth Needs To Improve In Order To Expect Further Taiwanese Relative Outperformance

Chart 5Cyclical Underperformance Underscores The Near-Term Risks To Chinese Vs. Global Stocks

Cyclical Underperformance Underscores The Near-Term Risks To Chinese Vs. Global Stocks

Cyclical Underperformance Underscores The Near-Term Risks To Chinese Vs. Global Stocks

We do not take the rise in Chinese government bond yields as necessarily indicative of an imminent breakout in relative equity performance. Chart 6Chinese Relative Equity Performance Leads Bond Yields, Not The Other Way Around

Chinese Relative Equity Performance Leads Bond Yields, Not The Other Way Around

Chinese Relative Equity Performance Leads Bond Yields, Not The Other Way Around

Chinese 10-year government bond yields have risen roughly 15bps over the past month, and are now 30bps off of their mid-August low. Many market participants view Chinese government bond yields as a leading growth barometer, but 10-year yields have actually lagged Chinese investable stock performance over the past two years (Chart 6). As such, we do not take the rise in yields as necessarily indicative of an imminent breakout in relative equity performance. Chinese onshore corporate bond spreads have declined over the past month as government bond yields have been rising, continuing a pattern of negative correlation between the two that has prevailed since early-2018. A negative correlation between yields and corporate bond spreads is a normal relationship, and it suggests that spreads may narrow over the coming year if the Chinese economy bottoms in Q1, as we expect. Spreads remain elevated despite the substantial easing in monetary conditions that occurred last year, due to persistent concerns about rising onshore defaults. While we acknowledge that defaults are indeed occurring, we have argued on several occasions that the pace of defaults would have to be much faster in order for current spreads to be justified.3 We continue to recommend a long RMB-denominated position in China’s onshore corporate bond market. The RMB has appreciated over the past month in response to news of a likely trade truce between the US and China, with most of the rise having occurred versus the US dollar. USD-CNY is likely to sustainably trade below the 7 mark in a trade truce scenario, but how much further downside is possible in the near-term absent a re-acceleration in Chinese economic activity remains an open question. With the Fed very likely on hold for the next year, stronger than expected economic growth in China would likely catalyze a persistent selloff in USD-CNY barring a re-emergence of the Sino-US trade war. This, however, is not our base-case view, meaning that we expect modest post-deal strength in the RMB. Jonathan LaBerge, CFA Vice President Special Reports jonathanl@bcaresearch.com Jing Sima China Strategist JingS@bcaresearch.com Footnotes 1. Please see China Investment Strategy Special Report, “China’s Property Market: Where Will It Go From Here?” dated September 13, 2018. 2. Please see China Investment Strategy Weekly Report, “A Guide To Chinese Investable Equity Sector Performance,” dated October 30, 2019. 3. Please see China Investment Strategy Weekly Reports, “A Shaky Ladder,” dated June 13, 2018, "Investing In The Middle Of A Trade War,” dated September 19, 2018 and "2019 Key Views: Four Themes For China In The Coming Year,” dated December 5, 2018. Cyclical Investment Stance Equity Sector Recommendations

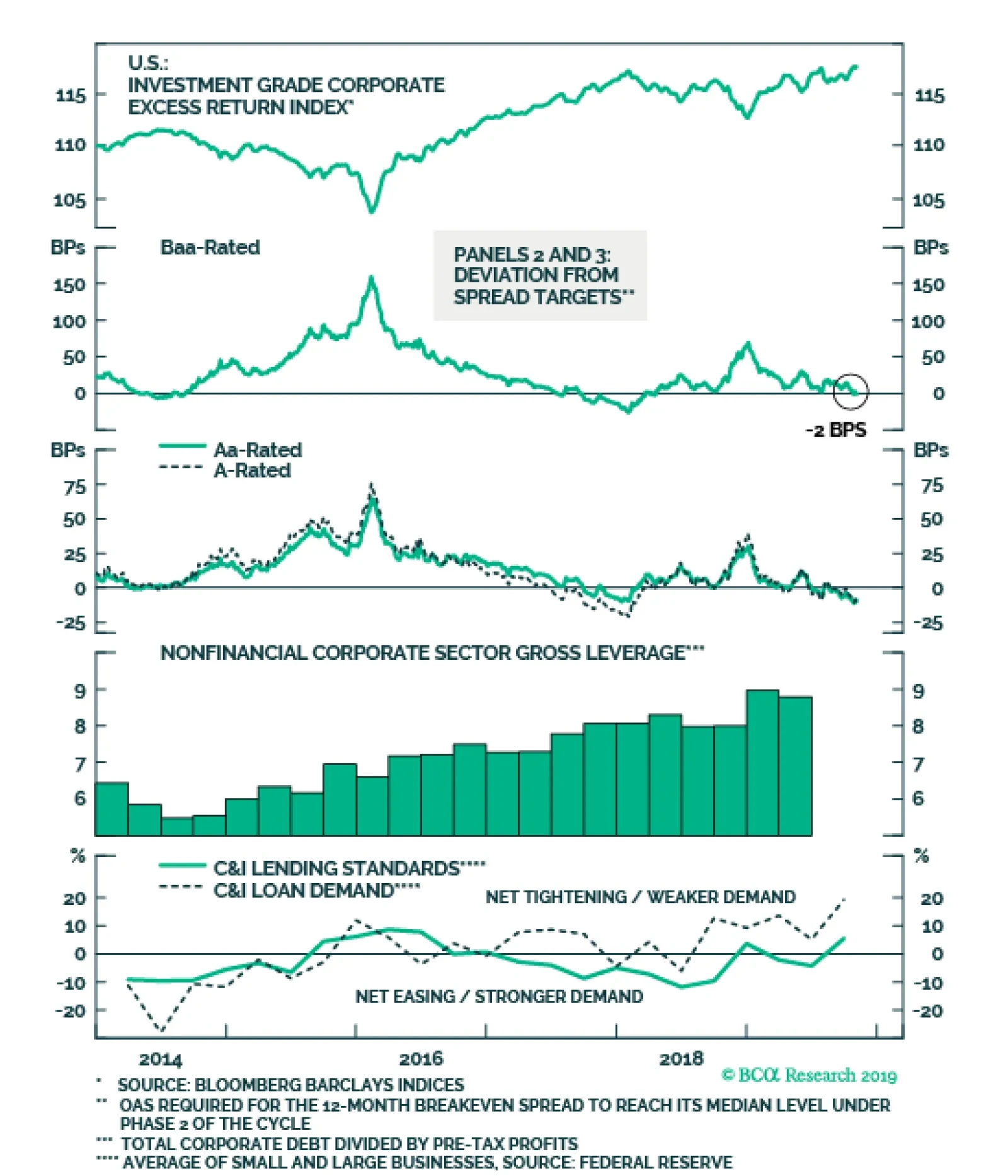

Highlights Chart 1The Fed Must Remain Dovish

The Fed Must Remain Dovish

The Fed Must Remain Dovish

Many were quick to label last week’s FOMC decision a “hawkish cut”. This is somewhat true in the near-term. The Fed lowered rates by 25 basis points while signaling that it doesn’t expect to have to cut more. But this focus on the near-term rate path misses the big picture. In the post-meeting press conference, Chairman Powell mentioned inflation expectations several different times. At one point, he called them “central” to the Fed’s framework and said “we need them to be anchored at a level that’s consistent with our symmetric 2 percent inflation goal.” As of today, the 5-year/5-year forward TIPS breakeven inflation rate is 1.69%, well short of the 2.3%-2.5% range that is consistent with the Fed’s goal (Chart 1). The Fed will take care to maintain an accommodative policy stance until inflation expectations are re-anchored. This will provide strong support for risk assets, and we recommend overweight positions in spread product versus Treasuries. We also expect that global growth will improve enough in the coming months for the Fed to keep its promise to stand pat. With the market still priced for 29 bps of cuts during the next 12 months, investors should keep portfolio duration low. Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 60 basis points in October, bringing year-to-date excess returns up to +429 bps. We consider three main factors in our credit cycle analysis: (i) corporate balance sheet health, (ii) monetary conditions and (iii) valuation.1 On balance sheets, our top-down measure of gross leverage is elevated and rising (Chart 2). In contrast, interest coverage ratios remain solid, propped up by the Fed’s accommodative stance. With inflation expectations still depressed, the Fed can maintain its “easy money” policy for some time yet. The Fed’s Senior Loan Officer survey shows that C&I lending standards tightened in Q3 (bottom panel). We expect the Fed’s accommodative stance to push standards back into “net easing” territory in Q4. But if standards continue to tighten, it could indicate that monetary conditions are not as accommodative as we think. For now, we see valuation as the main headwind for investment grade credit spreads. Spreads for all credit tiers are now below our targets, with the Baa tier looking less expensive than the others (panels 2 & 3).2 As a result, we advise only a neutral allocation to investment grade corporate bonds, with a preference for the Baa credit tier. We also recommend increasing exposure to Agency MBS in place of corporate bonds rated A or higher. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Fed Will Stay Supportive

The Fed Will Stay Supportive

Table 3BCorporate Sector Risk Vs. Reward*

The Fed Will Stay Supportive

The Fed Will Stay Supportive

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield performed in line with the duration-equivalent Treasury index in October, keeping year-to-date excess returns steady at +621 bps. The junk index’s option-adjusted spread (OAS) has been fairly stable for most of the year, but the sector has become increasingly attractive from a risk/reward perspective.3 This is because the index’s negatively convex nature has caused its average duration to fall alongside declining Treasury yields. Chart 3 shows that while the index OAS has been rangebound, the 12-month breakeven spread has widened considerably.4 In other words, while junk expected returns have been stable, those expected returns now come with considerably less risk. As a result, the junk index OAS looks increasingly attractive relative to our spread target.5 Specifically, we now view the junk index OAS as 141 bps cheap (panel 3). Falling index duration also explains the divergence between quality spreads and the index OAS. Many have observed that the spread differential between Caa and Ba-rated junk bonds has widened in recent months, while the overall index OAS has been stable (panel 4). However, the divergence evaporates when we look at 12-month breakeven spreads instead of OAS (bottom panel). MBS: Overweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 9 basis points in October, bringing year-to-date excess returns up to +3 bps. The conventional 30-year zero-volatility spread widened 4 bps on the month, as a 5 bps widening of the option-adjusted spread (OAS) was partially offset by a 1 bp decline in option cost (i.e. the expected losses from prepayments). This week we recommend upgrading Agency MBS from neutral to overweight, and in particular, we recommend favoring Agency MBS over corporate bonds rated A or higher. We have three main reasons for this recommendation.6 First, expected compensation is competitive. The conventional 30-year MBS OAS is now 53 bps. This is above its pre-crisis average (Chart 4), and only 4 bps below the spread offered by a Aa-rated corporate bond. All investment grade corporate bond credit tiers also look expensive relative to our spread targets. Second, risk-adjusted compensation heavily favors MBS. The Excess Return Bond Map in Appendix C shows that Agency MBS plot well to the right of investment grade corporates. This means that the sector is less likely to see losses versus Treasuries on a 12-month horizon. Finally, the macro environment for MBS remains supportive. Mortgage lending standards have barely eased since the financial crisis (bottom panel), and most people have already had at least one opportunity to refinance their mortgages. This burnout will keep refi activity low, and MBS spreads tight (panel 2). Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 20 basis points in October, bringing year-to-date excess returns up to +183 bps. Sovereign debt outperformed duration-equivalent Treasuries by 38 bps on the month, bringing year-to-date excess returns up to +475 bps. Local Authorities outperformed the Treasury benchmark by 9 bps, bringing year-to-date excess returns up to +220 bps. Meanwhile, Foreign Agencies outperformed by 63 bps, bringing year-to-date excess returns up to +261 bps. Domestic Agencies underperformed by 2 bps in October, dragging year-to-date excess returns down to +40 bps. Supranationals underperformed by 8 bps on the month, dragging year-to-date excess returns down to +31 bps. We continue to recommend an underweight allocation to USD-denominated sovereign bonds, given that spreads remain expensive compared to U.S. corporate credit (Chart 5). However, we noted in a recent report that Mexican and Saudi Arabian sovereigns look attractive on a risk/reward basis.7 This is also true for Foreign Agencies and Local Authorities, as shown in the Bond Map in Appendix C. Our Emerging Markets Strategy service also thinks that worries about Mexico’s fiscal position are overblown, and that bond yields embed too high of a risk premium (bottom panel).8 Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 7 basis points in October, dragging year-to-date excess returns down to -64 bps (before adjusting for the tax advantage). The average Aaa-rated Municipal / Treasury (M/T) yield ratio fell almost 2% in October, and currently sits at 85% (Chart 6). We recently upgraded municipal bonds from neutral to overweight.9 The decision was based on the fact that yield ratios had jumped significantly. Yield ratios continue to look attractive relative to average pre-crisis levels, especially at the long-end of the Aaa curve (panel 2). Specifically, 2-year and 5-year M/T yield ratios are close to average pre-crisis levels at 73% and 77%, respectively. Meanwhile, M/T yield ratios for longer maturities are all above average pre-crisis levels. M/T yield ratios for 10-year, 20-year and 30-year maturities are 86%, 94% and 97%, respectively. Fundamentally, state & local government balance sheets remain solid. Our Municipal Health Monitor remains in “improving health” territory and state & local government interest coverage has improved considerably in recent quarters (bottom panel). Both of these trends are consistent with muni ratings upgrades continuing to outnumber downgrades going forward. Treasury Curve: Maintain A Barbell Curve Positioning Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve steepened considerably in October, as short-dated yields came under downward pressure even as long-maturity yields edged higher. The 2/10 Treasury slope steepened 12 bps on the month, and currently sits at 17 bps. The 5/30 slope steepened 9 bps on the month, and currently sits at 66 bps (Chart 7). Last week’s report discussed the outlook for the 2/10 Treasury slope on a 6-12 month horizon.10 We considered the main macro factors that influence the slope of the yield curve: Fed policy, wage growth, inflation expectations and the neutral fed funds rate. We concluded that the 2/10 slope has room to steepen during the next few months, as the Fed holds down the front-end of the curve in an effort to re-anchor inflation expectations. However, we see the 2/10 slope remaining in a range between 0 bps and 50 bps, owing to strong wage growth and downbeat neutral rate expectations. Despite the outlook for modest curve steepening, we continue to recommend holding a barbelled Treasury portfolio. Specifically, we favor holding a 2/30 barbell versus the 5-year bullet, in duration-matched terms. This position offers strong positive carry (bottom panel), due to the extreme overvaluation of the 5-year note, and looks attractive on our yield curve models (see Appendix B). TIPS: Overweight Chart 8Inflation Compensation

Inflation Compensation

Inflation Compensation

TIPS outperformed the duration-equivalent nominal Treasury index by 27 basis points in October, bringing year-to-date excess returns up to -64 bps. The 10-year TIPS breakeven inflation rate rose 1 bp on the month, and currently sits at 1.60%. The 5-year/5-year forward TIPS breakeven inflation rate fell 8 bps on the month, and currently sits at 1.69%. Both rates remain well below the 2.3%-2.5% range consistent with the Fed’s target. The divergence between the actual inflation data and inflation expectations is becoming increasingly stark. Trimmed mean PCE inflation has been fluctuating around the Fed’s target for most of the year (Chart 8). However, long-maturity TIPS breakeven inflation rates remain stubbornly low. As we have pointed out in prior research, it can take time for expectations to adapt to a changing macro environment.11 That being said, the 10-year TIPS breakeven rate is currently 32 bps too low according to our Adaptive Expectations Model, a model whose primary input is 10-year trailing core inflation (panel 4). It is highly likely that the Fed will have to tolerate some overshoot of its 2% inflation target in order to re-anchor inflation expectations near desired levels. We anticipate that the committee will do so, and maintain our view that long-dated TIPS breakevens will move above 2.3% before the end of the cycle. ABS: Underweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 5 basis points in October, dragging year-to-date excess returns down to +67 bps. The index option-adjusted spread for Aaa-rated ABS widened 5 bps on the month. It currently sits at 39 bps, 5 bps above its minimum pre-crisis level (Chart 9). Our Excess Return Bond Map (see Appendix C) shows that Aaa-rated consumer ABS rank among the most defensive U.S. spread products and also offer more expected return than other low-risk sectors such as Domestic Agency bonds and Supranationals. However, we remain wary of allocating too much to consumer ABS because credit trends continue to shift in the wrong direction. The consumer credit delinquency rate is still low, but has put in a clear bottom. The same is true for the household interest expense ratio (panel 3). Senior loan officers also continue to tighten lending standards for both credit cards and auto loans. Tighter lending standards usually coincide with rising delinquencies (bottom panel). All in all, our favorable outlook for global growth causes us to shy away from defensive spread products, and deteriorating ABS credit metrics are also a cause for concern. Stay underweight. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 6 basis points in October, bringing year-to-date excess returns up to +233 bps. The index option-adjusted spread for non-agency Aaa-rated CMBS was flat on the month. It currently sits at 73 bps, below its average pre-crisis level but somewhat above levels seen in 2018 (Chart 10). The macro outlook for commercial real estate (CRE) is somewhat unfavorable, with lenders tightening loan standards (panel 4) in an environment of tepid demand. The Fed’s Senior Loan Officer survey shows that banks saw slightly stronger demand for nonfarm nonresidential CRE loans in Q3, after four consecutive quarters of falling demand (bottom panel). CRE prices have accelerated of late, but are still not keeping pace with CMBS spreads (panel 3). Despite the poor fundamental picture, our Excess Return Bond Map shows that CMBS offer a reasonably attractive risk/reward trade-off compared to other bond sectors (see Appendix C). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 10 basis points in October, bringing year-to-date excess returns up to +100 bps. The index option-adjusted spread was flat on the month, and currently sits at 57 bps. The Excess Return Bond Map in Appendix C shows that Agency CMBS offer a compelling risk/reward trade-off. An overweight allocation to this high-rated sector remains appropriate. Appendix A: The Golden Rule Of Bond Investing We follow a two-step process to formulate recommendations for bond portfolio duration. First, we determine the change in the federal funds rate that is priced into the yield curve for the next 12 months. Second, we decide – based on our assessments of the economy and Fed policy – whether the change in the fed funds rate will exceed or fall short of what is priced into the curve. Most of the time, a correct answer to this question leads to the appropriate duration call. We call this framework the Golden Rule Of Bond Investing, and we demonstrated its effectiveness in the U.S. Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018, available at usbs.bcaresearch.com. Chart 11 illustrates the Golden Rule’s track record by showing that the Bloomberg Barclays Treasury Master Index tends to outperform cash when rate hikes fall short of 12-month expectations, and vice-versa. Chart 11The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

At present, the market is priced for 29 basis points of cuts during the next 12 months. We anticipate a flat fed funds rate over that time horizon, and therefore anticipate that below-benchmark portfolio duration positions will profit. We can also use our Golden Rule framework to make 12-month total return and excess return forecasts for the Bloomberg Barclays Treasury index under different scenarios for the fed funds rate. Excess returns are relative to the Bloomberg Barclays Cash index. To forecast total returns we first calculate the 12-month fed funds rate surprise in each scenario by comparing the assumed change in the fed funds rate to the current value of our 12-month discounter. This rate hike surprise is then mapped to an expected change in the Treasury index yield using a regression based on the historical relationship between those two variables. Finally, we apply the expected change in index yield to the current characteristics (yield, duration and convexity) of the Treasury index to estimate total returns on a 12-month horizon. The below tables present those results, along with 95% confidence intervals. Excess returns are calculated by subtracting assumed cash returns in each scenario from our total return projections.

The Fed Will Stay Supportive

The Fed Will Stay Supportive

The Fed Will Stay Supportive

The Fed Will Stay Supportive

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com U.S. Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuations: Raw Residuals In Basis Points (As Of November 1, 2019)

The Fed Will Stay Supportive

The Fed Will Stay Supportive

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of November 1, 2019)

The Fed Will Stay Supportive

The Fed Will Stay Supportive

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 48 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 48 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Fed Will Stay Supportive

The Fed Will Stay Supportive

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the U.S. bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 12Excess Return Bond Map (As Of November 1, 2019)

The Fed Will Stay Supportive

The Fed Will Stay Supportive

Ryan Swift U.S. Bond Strategist rswift@bcaresearch.com Jeremie Peloso Research Analyst jeremiep@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Weekly Report, “Corporate Bond Investors Should Not Fight The Fed”, dated September 17, 2019, available at usbs.bcaresearch.com 2 For details on how we arrive at our spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 3 Please see U.S. Bond Strategy Weekly Report, “Crisis Of Confidence”, dated October 22, 2019, available at usbs.bcaresearch.com 4 The 12-month breakeven spread is the spread widening required to break even with a duration-matched position in Treasuries on a 12-month horizon. It can be approximated by OAS divided by duration. 5 For details on how we arrive at our spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 6 Please see U.S. Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com 7 Please see U.S. Bond Strategy Weekly Report, “A Perspective On Risk And Reward”, dated October 15, 2019, available at usbs.bcaresearch.com 8 Please see Emerging Markets Strategy Weekly Report, “Country Insights: Malaysia, Mexico & Central Europe”, dated October 31, 2019, available at ems.bcaresearch.com 9 Please see U.S. Bond Strategy Weekly Report, “Two Themes and Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com 10 Please see U.S. Bond Strategy Weekly Report, “Position For Modest Curve Steepening”, dated October 29, 2019, available at usbs.bcaresearch.com 11 Please see U.S. Bond Strategy Weekly Report, “Adaptive Expectations In The TIPS Market”, dated November 20, 2018, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

The key question for asset allocators over coming months will be when (or, perhaps, whether) the global manufacturing cycle will turn up. This would trigger a move into more cyclically sensitive markets, for example euro zone equities and Emerging Market assets. It would push up commodity prices and government bond yields, and lead to a weakening of the U.S. dollar. Recommended Allocation

Monthly Portfolio Update: Looking For The Turning-Point

Monthly Portfolio Update: Looking For The Turning-Point

Chart 1First Inklings Of A Pick-Up?

First Inklings Of A Pick-Up?

First Inklings Of A Pick-Up?

For now, the evidence of this turning-point remains ambiguous, and so we hesitate to pull the trigger. BCA Research's calculation of the global OECD Leading Economic Indicator bottomed earlier this year and should lead to a pick-up in manufacturing activity soon (Chart 1). However, only in EM have the manufacturing PMIs bottomed (Chart 1, panel 2) and this was due mainly to a questionably strong September PMI in China which might be reversed when the latest data-point is published on October 1. In the euro zone, the best that one can say is that the PMIs have stopped falling but they remain at a low level (41.9 in Germany, for instance). Some market-based indicators also signal a pick-up – but not yet convincingly (Chart 2). Defensive currencies such as the U.S. dollar and yen have fallen a little against cyclical currencies like the Korean won and Australian dollar. Euro zone equities have shown some strength, especially in the beaten-down auto sector. The global stock-to-bond ratio looks to be about to break out of its recent range. And copper has bounced off its lows. But these moves could turn out to be just noise rather than the beginning of a trend. Chart 2Are Markets Sniffing Out A Turn?

Are Markets Sniffing Out A Turn?

Are Markets Sniffing Out A Turn?

Easier financial conditions are the most likely cause of a rebound. BCA Research's Financial Liquidity Index tends to lead both manufacturing activity and the relative performance of global stocks by around 12-18 months (Chart 3). With the dovish turn of central banks this year, the decline in long-term interest rates (the 10-year U.S. Treasury yield, even after its recent rebound, is only at 1.7% compared to 3.2% a year ago), the contraction in credit spreads, and a pick-up in money supply growth especially in the U.S. (where M2 is now growing 6.5% year-on-year), it would be surprising if these looser monetary conditions do not feed through into stronger activity over coming quarters. Chart 3Financial Liquidity Propels Growth

Financial Liquidity Propels Growth

Financial Liquidity Propels Growth

Chart 4Could Inflation Now Slow?

Could Inflation Now Slow?

Could Inflation Now Slow?

Indeed, one can easily imagine a scenario next year where growth rebounds but inflation slows (due to the lagged effect of this year’s weaker growth, Chart 4), allowing central banks to remain dovish for some time. This non-inflationary accelerating growth would be highly positive for risk assets and negative for the U.S. dollar. Chart 5 shows how various asset classes behaved in such an environment in the past. Chart 5How Assets Behaved Under Rising Growth/Falling Inflation

Monthly Portfolio Update: Looking For The Turning-Point

Monthly Portfolio Update: Looking For The Turning-Point

Easier financial conditions are the most likely cause of a rebound. There are some risks to this optimistic scenario, however. Chinese growth remains sluggish with, for example, imports – the most important factor as far as the rest of the world is concerned – falling by 8.5% year-on-year in September and showing no signs of recovery (Chart 6). The acceleration of Chinese credit growth in early 2019 has petered out since the summer and points to a much flatter recovery of activity than was the case in 2016 (Chart 7). A politburo meeting in late October could lead to monetary stimulus being ramped up but, for now, investors should not assume a big reflationary impulse from China. In the developed world, the biggest risk is that the slowdown in manufacturing spills over into employment, consumption, and services. There are some signs in the U.S. that companies are delaying hiring decisions: job openings have fallen, and the employment component of both the manufacturing and non-manufacturing ISMs points to a deterioration in the labor market (Chart 8). Growing CEO pessimism, presumably because of anemic earnings and the trade war, points to continuing weakness in capex and a further decline in activity indicators (Chart 9). Chart 6Chinese Growth Still Sluggish...

Chinese Growth Still Sluggish...

Chinese Growth Still Sluggish...

Chart 7...As Credit Growth Peters Out

...As Credit Growth Peters Out

...As Credit Growth Peters Out

Chart 8Are Firms Starting To Delay Hiring?

Are Firms Starting To Delay Hiring?

Are Firms Starting To Delay Hiring?

Chart 9CEOs Are Not Happy

CEOs Are Not Happy

CEOs Are Not Happy

Chart 10Stocks Should Outperform Cyclically

Stocks Should Outperform Cyclically

Stocks Should Outperform Cyclically

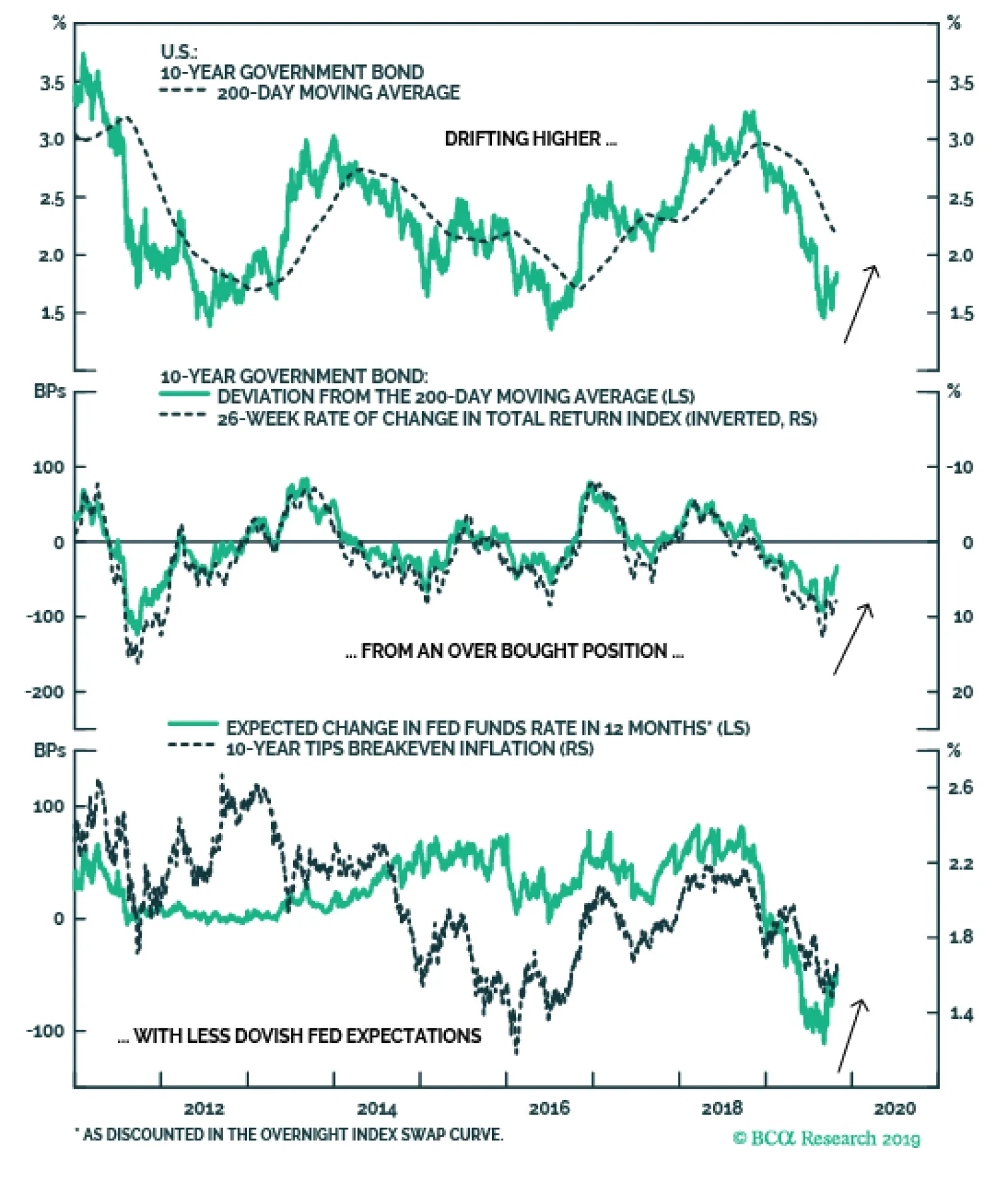

On balance, we still expect global growth to accelerate next year, and therefore global equities to outperform bonds over the next 12 months (Chart 10). But we want to have greater conviction for that view before we recommend more aggressive pro-cyclical tilts. We remain overweight equities versus bonds, but hedge the downside risk through an overweight in cash, and through tilts towards U.S. equities, and DM over EM equities. We continue to recommend hedging against the upside risk of greater Chinese stimulus and a strong rally in cyclical assets through an overweight in global Financials, Industrials, and Energy, and also through a neutral stance on Australian equities, which are a clean play on a Chinese rebound. We continue to look for the right timing to turn more positive on pure cyclical assets such as euro zone equities, and Emerging Markets. Fixed Income: A cyclical pick-up would imply that global government bond yields have further to rise (Chart 11). Our global fixed-income strategists have a short-term target for the 10-year U.S. Treasury yield of 2.1% (versus 1.7% now) and -0.2% for Bunds (-0.4% now), which would take yields back to their 200-day moving averages (Chart 12).1 We continue to recommend a moderate underweight on duration, and prefer TIPS to nominal bonds, since inflation breakevens imply that the Fed will miss its inflation target by 80 basis points a year on average over the next 10 years. In an environment of accelerating economic growth, credit (both investment grade and high-yield)should outperform in both the U.S. and Europe. The most attractive points on the credit curve are BBB-rated bonds in IG, and the riskiest bonds in HY. For more risk-averse investors, agency MBS currently offer an attractive yield pickup over quality corporate credits. Chart 11Growth Will Push Up Yields Further...

Growth Will Push Up Yields Further...

Growth Will Push Up Yields Further...

Chart 12...Initially To Their 200-Day Average

...Initially To Their 200-Day Average

...Initially To Their 200-Day Average

Equities: Any upside for U.S. equities must come from improved earnings performance. Throughout 2019, earnings have been beating overly pessimistic analysts’ forecasts and Q3 looks to be no exception, with EPS growth on track to be much stronger than the -5% year-on-year that analysts forecast going into the results season (Chart 13). Next year, nominal GDP growth of 4% and a weaker U.S. dollar should produce 7-8% EPS growth. But, with a forward PE of 17x and the Fed unlikely to boost the multiple by further rate cuts, upside is limited. In the right economic environment (as described above), euro zone and EM stocks should do much better. We are currently neutral on euro zone equities, but the recent stronger performance by European banks gives us more confidence that we may be able to move to overweight soon (Chart 14). Similarly, our EM strategists have instituted a buy stop on the MSCI EM index and say they will go overweight EM equities if the index in USD terms rises 3% from its current level.2 Chart 13Analysts Are Too Pessimistic On Earnings

Monthly Portfolio Update: Looking For The Turning-Point

Monthly Portfolio Update: Looking For The Turning-Point

Currencies: The first inklings of U.S. dollar weakness over the past month suggest that it may, too, be sniffing out the start of a cyclical rebound, since it tends to be a very counter-cyclical currency (Chart 15). Going forward, relative interest rates are also unlikely to be as bullish a force for the U.S. dollar as they have been in the past few years. For now, we are neutral on the U.S. dollar on a trade-weighted basis, but do see it depreciating against the Australian dollar and the euro over the next 12 months. The British pound has already risen to take into account the lesser probability of a no-deal Brexit, and we would not expect it to move much either way until the General Election result is clear. There are some risks to the optimistic scenario: Chinese growth remains sluggish, and there are signs that U.S. companies are delaying hiring decisions. Chart 14First Signs Of Euro Banks Recovering?

First Signs Of Euro Banks Recovering?

First Signs Of Euro Banks Recovering?

Chart 15Recovery Would Be Dollar Bearish

Recovery Would Be Dollar Bearish

Recovery Would Be Dollar Bearish

Commodities: Industrial metals prices have bottomed out in recent months, in line with Chinese leading indicators (Chart 16). But we will need to see greater Chinese stimulus before we become more positive. Crude oil has moved largely in a range for the past six months, with tightness in supply offset by some weakness in demand, especially from developed economies (Chart 17). With demand likely to pick up in line with the global economy, and supply still constrained by the Saudi/Russia production pact and geopolitical disturbances, our energy strategists see Brent crude averaging $66 a barrel in Q4 and $70 in 2020, versus $60 now. Chart 16Not Enough China Stimulus For Metals To Bounce

Not Enough China Stimulus For Metals To Bounce

Not Enough China Stimulus For Metals To Bounce

Chart 17Oil Kept Down By Weak Demand

Oil Kept Down By Weak Demand

Oil Kept Down By Weak Demand

As last year, the Global Asset Allocation service will not publish a Q1 Quarterly in mid-December. Instead, we will send clients on November 22 our annual report of the conversation between Mr and Ms X and BCA Research’s managing editors. This report will detail BCA's house views on the outlook for the macro environment and investment markets in 2020. We will publish GAA Monthly Portfolio Outlooks on the first business days of December and January. Garry Evans Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com Footnotes 1Please see Global Fixed Income Strategy Weekly Report “Big Mo(mentum) Is Turning Positive,” dated 29 October 2019, available at gfis.bcaresearch.com. 2For an explanation, please see the Emerging Markets Strategy Weekly Report " EM Local Bonds: A New Normal?" dated 24 October 2019, available at ems.bcaresearch.com. Recommended Asset Allocation Model Portfolio (USD Terms)

Analysis on Mexico and Central Europe is available on pages 6 and 10, respectively. Highlights Deflationary pressures have been intensifying in Malaysia and the central bank will be forced to cut its policy rate. To play this theme, we recommend receiving 2-year swap rates. In Mexico, pieces are falling into place for stocks to outperform the EM equity benchmark on a sustainable basis. We are also keeping an overweight allocation on Mexican sovereign credit and local currency bonds. In Central Europe (CE), inflation will continue to rise as both labor shortages and ultra-accommodative monetary and fiscal policies promote strong domestic demand. We are downgrading our allocation of CE local currency bonds from overweight to neutral. Malaysia: Besieged By Deflationary Pressures Malaysian interest rates appear elevated given the state of its economy. Deflationary pressures have been intensifying and the central bank will be forced to cut its policy rate. The Malaysian economy continues to face strong deflationary pressures. To play this theme, we recommend receiving 2-year swap rates. We are also upgrading our recommended allocation to Malaysian local currency and U.S. dollar government bonds for dedicated EM fixed-income portfolios from neutral to overweight. The Malaysian economy continues to face strong deflationary pressures, requiring significant rate cuts by the central bank: Chart I-1 shows that the GDP deflator is flirting with deflation, and nominal GDP growth has slowed to the level of commercial banks’ average lending rates. Falling nominal growth amid elevated corporate and household debt levels is an extremely toxic mix (Chart I-2, top panel). Notably, debt-servicing costs for the private sector – both businesses and households – are high at 13.5% of GDP and are also rising (Chart I-2, bottom panel). Chart I-1The Malaysian Economy Is Flirting With Deflation

The Malaysian Economy Is Flirting With Deflation

The Malaysian Economy Is Flirting With Deflation

Chart I-2High Leverage & Debt Servicing Costs Among Businesses & Households

High Leverage & Debt Servicing Costs Among Businesses & Households

High Leverage & Debt Servicing Costs Among Businesses & Households

Crucially, real borrowing costs are elevated. In real terms, the prime lending rate stands at 5% when deflated by the GDP deflator, and at 3% when deflated by headline CPI. Notably, private credit growth (outstanding business and household loans) has plunged to a 15-year low (Chart I-3), underscoring that real borrowing costs are excessive. Chart I-3Malaysia: Credit Growth Is In Freefall

Malaysia: Credit Growth Is In Freefall

Malaysia: Credit Growth Is In Freefall

Chart I-4Malaysia's Corporate Sector Is Struggling

Malaysia's Corporate Sector Is Struggling

Malaysia's Corporate Sector Is Struggling

Malaysia’s corporate sector is struggling. The manufacturing PMI is below the critical 50 threshold and is showing no signs of recovery. Listed companies’ profits are shrinking (Chart I-4, top panel). Poor corporate profitability is prompting cutbacks in capex spending (Chart I-4, middle and bottom panels) and weighing on employment and wages. The household sector has been retrenching; retail sales have been contracting and personal vehicle sales have been shrinking (Chart I-5). The property market – in particular the residential sub-sector – is still in recession. Property sales and starts are falling, and property prices are flirting with deflation (Chart I-6). Critically, monetary policy easing and exchange rate depreciation are the only levers available to policymakers to reflate the economy. Fiscal policy is constrained as the budget deficit is already large at 3.4% of GDP, and public debt is elevated. Prime Minister Mahathir Mohamad is in fact aiming to reduce the total national debt (including off-balance-sheet debt) back to the government’s ceiling of 54% of GDP (from 80% currently). Chart I-5Malaysian Households Are Retrenching

Malaysian Households Are Retrenching

Malaysian Households Are Retrenching

Chart I-6Malaysia's Property Sector Is In A Downturn

Malaysia's Property Sector Is In A Downturn

Malaysia's Property Sector Is In A Downturn

Bottom Line: The Malaysian economy is besieged by deflationary pressures and requires lower borrowing costs. The central bank will deliver rate cuts in the coming months. Investment Recommendations A new trade idea: receive 2-year swap rates as a bet on rate cuts by the central bank. Consistently, for dedicated EM bond portfolios, we are upgrading local currency and U.S. dollar-denominated government bonds from neutral to overweight. Chart I-7Overweight Malaysian Local Currency And U.S. Dollar Government Bonds

Overweight Malaysian Local Currency And U.S. Dollar Government Bonds

Overweight Malaysian Local Currency And U.S. Dollar Government Bonds

While we are downbeat on the ringgit versus the U.S. dollar, Malaysian domestic bonds will likely outperform the EM GBI index in common currency terms on a total return basis (Chart I-7, top panel). The same is true for excess returns on the country’s sovereign credit (Chart I-7, bottom panel). The basis for the ringgit’s more moderate depreciation, especially in comparison with other EM currencies, is as follows: First, foreigners have reduced their holdings of local currency bonds. The share of foreign ownership has declined from 36% in 2015 to 22% now of total outstanding local domestic bonds in the past 4 years (Chart I-8). Hence, currency depreciation will not trigger large foreign capital outflows. Second, the trade balance is in surplus and improving. This will provide a cushion for the ringgit. Finally, the ringgit is cheap in real effective terms which also limits the potential downside (Chart I-9). Dedicated EM equity portfolios should keep a neutral allocation on Malaysian stocks. We are taking profits on our long Malaysian small-cap stocks relative to the EM small-cap index position. This recommendation has generated a 6.6% gain since its initiation on December 14, 2018. Chart I-8Foreigners' Share Of Local Currency Bonds Has Dropped

Foreigners' Share Of Local Currency Bonds Has Dropped

Foreigners' Share Of Local Currency Bonds Has Dropped

Chart I-9The Ringgit Is Cheap

The Ringgit Is Cheap

The Ringgit Is Cheap

Ayman Kawtharani Editor/Strategist ayman@bcaresearch.com Mexico: Raising Our Conviction On Equity Outperformance Mexican local currency bonds, as well as sovereign and corporate credit, have been one of our highest conviction overweights for some time. These positions have played out very well (Chart II-1). Presently, pieces are falling into place for Mexican stocks to outperform the EM equity benchmark on a sustainable basis. First, long-lasting outperformance by Mexican local currency bonds and corporate credit will lead to the stock market’s outperformance relative to the EM benchmark. Chart II-2 shows that when Mexican local currency bond and corporate dollar bond yields fall relative to their EM peers, the Bolsa tends to outperform. In brief, a relative decline in the cost of capital will eventually translate into relative equity outperformance. Chart II-1Mexico Vs. EM: Domestic Bonds And Credit Markets

Mexico Vs. EM: Domestic Bonds And Credit Markets

Mexico Vs. EM: Domestic Bonds And Credit Markets

Chart II-2Mexico: Relative Stock Prices Are Correlated With Relative Cost Of Capital

Mexico: Relative Stock Prices Are Correlated With Relative Cost Of Capital

Mexico: Relative Stock Prices Are Correlated With Relative Cost Of Capital

Second – as discussed in detail in our previous Special Report – market worries about Mexico’s fiscal position are overblown, especially relative to other developing nations such as Brazil and South Africa. Orthodox fiscal and monetary policies, as well as low public debt, warrant a lower risk premium in Mexico, both in absolute terms and relative to other EM countries. Moreover, market participants and credit agencies have overstated the precariousness of Pemex’s debt and financing requirements. Pemex U.S. dollar bond yields have been falling steadily compared to EM aggregate corporate bond yields since the announcements of policies aimed at supporting the company’s debt sustainability. We have discussed Pemex’s financial sustainability and its effect on public finances in past reports.1 Third, having cut rates twice since September, the Central Bank of Mexico (Banxico) has embarked on a rate cutting cycle. This is positive for stock prices, as it implies higher equity valuations and will eventually put a floor under the economy. Given that both core and headline inflation have fallen within the target bands, this gives the monetary authorities more room to reduce interest rates. Banxico members have been vocal about their desire to cut rates further, which is being foreshadowed by the swap market (Chart II-3, top panel). Given that both core and headline inflation have fallen within the target bands, this gives the monetary authorities more room to reduce interest rates. The slowdown in the domestic economy and Andrés Manuel López Obrador’ (AMLO) administration’s tight fiscal policy will enable and encourage Banxico to further ease monetary policy (Chart II-3, bottom panel). Fourth, another positive market catalyst for Mexican equities is the ongoing outperformance of EM consumer staples versus the overall EM index. Consumer staples have a large 35% share of the overall Mexico MSCI stock index, while this sector in the EM MSCI benchmark accounts for only 7%. Therefore, durable outperformance by consumer staples often hints at a relative cyclical outperformance for the Mexican bourse (Chart II-4). Chart II-3Mexico: Continue Betting On Lower Rates

Mexico: Continue Betting On Lower Rates

Mexico: Continue Betting On Lower Rates

Chart II-4Mexican Equities Are A Play On Consumer Staples

Mexican Equities Are A Play On Consumer Staples

Mexican Equities Are A Play On Consumer Staples

Chart II-5Mexican Stocks Offer Reasonable Value

Mexican Stocks Offer Reasonable Value

Mexican Stocks Offer Reasonable Value

Finally, Mexican equities are not expensive. Chart II-5 illustrates that according to our cyclically-adjusted P/E ratios, Mexican stocks offer good value in both absolute terms and relative to EM overall. We continue to believe AMLO’s administration is proving to be a pragmatic government with the aim of reducing rent-seeking activities and addressing structural issues such as poverty, corruption and crime. These policies will be positive for the economy over the long run and share prices will move higher in anticipation. Bottom Line: We are reiterating our overweight allocation on Mexican sovereign credit and domestic local currency bonds within their respective EM benchmarks. With further rate cuts on the horizon, yet upside risks to EM local currency bond yields, we continue to recommend a curve steepening trade in Mexico: receiving 2-year and paying 10-year swap rates. We now have high conviction that Mexican share prices will stage a cyclical outperformance relative to their EM peers. The bottom panel of Chart II-4 on page 8 illustrates that Mexican stocks seem to have formed a major bottom and are about to begin outperforming the EM equity benchmark. Dedicated EM equity managers should have a large overweight allocation to Mexican stocks. Our recommendation of favoring small-caps over large-cap companies in Mexico has been very profitable since we argued for this trade last November. We are taking a 12.9% profit on this position and recommend keeping an overweight allocation to both Mexican large- and small-caps within an EM equity portfolio. Juan Egaña Research Associate juane@bcaresearch.com Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Central Europe: An Inflationary Enclave In Deflationary Europe Our macroeconomic theme for Central European (CE) economies – Hungary, Poland and the Czech Republic, elaborated in the linked report, has been as follows: Inflation will continue to rise as both labor shortages and ultra-accommodative monetary as well as fiscal policies in CE promote strong domestic demand. CE economies have stood out as an inflationary enclave in Europe. Notably, CE economies have stood out as an inflationary enclave in Europe. Going forward, inflation will continue to rise across this region, despite the ongoing contraction in European manufacturing. First, Hungary’s and Poland’s central banks are behind the curve – they remain reluctant to hike rates amid rampantly rising inflation within overheating economies (Chart III-1). In turn, real policy rates across CE are becoming more negative and will promote robust money and credit growth (Chart III-2). Chart III-1CE Central Banks Are Behind The Curve

CE Central Banks Are Behind The Curve

CE Central Banks Are Behind The Curve

Chart III-2Low Real Rates Promote Rampant Credit Growth

Low Real Rates Promote Rampant Credit Growth

Low Real Rates Promote Rampant Credit Growth

Policymakers are justifying stimulative policies by stressing ongoing woes in the Europe-wide manufacturing downturn. Yet, they are paying little attention to genuine inflationary pressures in their own economies. Most notably in Hungary, the National Bank of Hungary (NBH) has been aggressively suppressing its policy rate and engaging in a corporate QE program, despite rising inflation and an overheating economy. Similarly, the National Bank of Poland (NBP) seems inclined to cut rates sooner rather than later. On the other end of the spectrum though, the Czech National Bank (CNB) is the only CE central bank to have embarked on a rate hiking cycle over the past 18 months. Going forward, the CNB looks most likely to normalize rates by continuing its hiking cycle. This development will favor rate differentials between it and the rest of CE. As such, we remain long the CZK versus both the HUF and PLN (Chart III-3). Chart III-3Favor CZK Versus PLN & HUF

Favor CZK Versus PLN & HUF

Favor CZK Versus PLN & HUF

Chart III-4Germany's Manufacturing Cycles And CE Inflation

Germany's Manufacturing Cycles And CE Inflation

Germany's Manufacturing Cycles And CE Inflation

Second, European manufacturing cycles have historically defined CE inflation trends, with time lags of around 12 to 18 months. However, this time around, the euro area manufacturing recession will not translate into slower CE inflation and growth dynamics (Chart III-4). Above all, booming credit induced by real negative borrowing costs has incentivized robust domestic demand in general and construction activity in particular in CE. In addition, employment growth remains strong and double-digit wage growth has supported strong consumer spending (Chart III-5). As a result, manufacturing production volumes have remained relatively resilient in Hungary and Poland, even as manufacturing output volumes in both Germany and the broader euro area have been contracting (Chart III-6). Chart III-5Strong Domestic Demand In CE…

bca.ems_wr_2019_10_31_s3_c5

bca.ems_wr_2019_10_31_s3_c5

Chart III-6...Entails Divergences In Manufacturing With Euro Area

...Entails Divergences In Manufacturing With Euro Area

...Entails Divergences In Manufacturing With Euro Area

Third, inflationary pressures in CE are both acute and genuine. Wage growth has been rising faster than productivity growth across the region, leading to surging unit labor costs (Chart III-7). Mounting wage pressures reflect widespread labor shortages. Further, output gaps in these economies have turned positive, which has historically been a precursor of inflationary pressures. Finally, fiscal policy in CE will remain very expansionary, supporting strong business and consumer demand. Bottom Line: Super-accommodative monetary and fiscal policies have led to a classic case of overheating within CE, particularly in Hungary and Poland, and less so in the Czech Republic. Chart III-7Genuine Inflationary Pressures In Central Europe

Genuine Inflationary Pressures In Central Europe

Genuine Inflationary Pressures In Central Europe

Chart III-8A Widening Current Account Deficit Is A Symptom Of Overheating

A Widening Current Account Deficit Is A Symptom Of Overheating

A Widening Current Account Deficit Is A Symptom Of Overheating

Investment Implications Deteriorating current accounts (Chart III-8), rising inflation and behind-the-curve central banks warrant further currency depreciation in both Hungary and Poland. This is why we continue to recommend a short position on both the HUF and PLN versus the CZK. We are closing our Hungarian/euro area relative three-year swap rate trade with a loss of 87 basis points. Our expectation that the market would price in rate hikes in Hungary despite the central bank’s dovishness has not materialized. Investors should remain overweight CE equities within an EM portfolio due to strong domestic demand in these economies and no direct economic exposure to China. As we expect EM equities to underperform DM stocks, we continue to recommend underweighting CE versus the core European markets. We are downgrading our allocation to CE local currency bonds from overweight to neutral within an EM domestic bond portfolio. The primary reason is a risk of a selloff in core European rates. Anddrija Vesic Research Analyst andrija@bcaresearch.com Footnotes 1. Please see Emerging Markets Strategy, "Mexico: The Best Value In EM Fixed Income," dated April 23, 2019 and "Mexico: Crying Out For Policy Easing," dated September 5, 2019, available at ems.bcaresearch.com Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

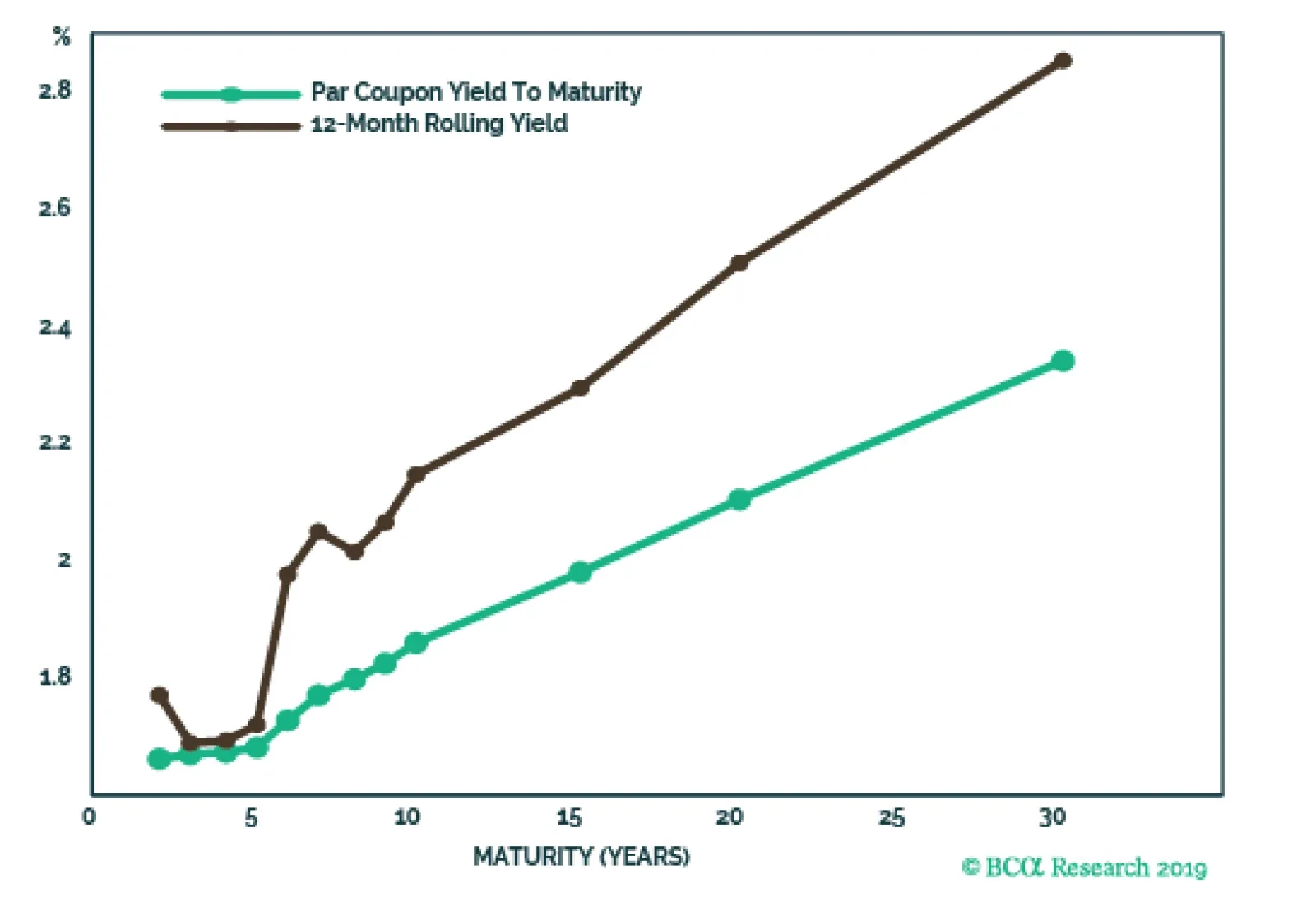

The first thing that sticks out in the chart above is that the 5-year note offers poor value. We also note that the curve steepens sharply beyond the 5-year maturity point, so maturities greater than 5 years benefit a lot from rolldown. The simple…

Highlights Declining uncertainty over policy, stabilizing growth in China and improvements in international liquidity, all will allow global economic activity to pick up in the months ahead. A weak dollar will reinforce this positive economic outlook; investors should favor pro-cyclical currencies such as the AUD, NZD and SEK. Bond yields will rise and stocks will outperform bonds on a 12- to 18-month basis. Cyclical stocks are more attractive than defensives. European stocks will outperform U.S. equities and European financials will shine. Copper is a promising buy; stay long the silver-to-gold ratio. Feature The outlook for risk assets and bond yields hinges on global economic activity. The S&P 500 has hit a new high, but our BCA Equity Scorecard Indicator remains non-committal towards stocks (Chart I-1). If global economic activity improves, the Scorecard will begin to flash a clear buy signal, but if growth deteriorates, the indicator will point towards sell. Chart I-1Stocks Could Go Either Way

Stocks Could Go Either Way

Stocks Could Go Either Way

Cautious optimism is in order. Politics, China, liquidity conditions and the dollar collectively will determine the global economic outlook. The liquidity backdrop has significantly improved, political uncertainty should recede and China will morph from a headwind to a modest tailwind. A weak dollar will indicate that the world is healing, and also will ease global financial conditions which will facilitate economic strength. We remain committed to a positive stance on equities on a 12- to 18-month horizon, and recommend below-benchmark duration in fixed-income portfolios. Cyclicals should outperform defensives, European banks offer an attractive tactical buying opportunity and European equities will outperform their U.S. counterparts. Heightened Risks… Chart I-2Risks To The Economy And Stocks

Risks To The Economy And Stocks

Risks To The Economy And Stocks

Many domestic indicators overstate the intrinsic fragility in the U.S. The Duncan LEI, which is the ratio of consumer durable spending and residential and business investment to final sales, has flattened. Therefore, the S&P 500 looks vulnerable and real GDP may contract (Chart I-2). CEO confidence and small business capex intentions warn of a looming retrenchment in household income (Chart I-2, bottom two panels). If consumer spending weakens, then a recession will be unavoidable. As worrisome as these indicators may be, we previously discussed that the major debt imbalances that often precede U.S. recessions are absent,1 the rebound in housing starts and homebuilding confidence is inconsistent with a restrictive monetary stance,2 and pipeline inflationary pressures are absent.3 Instead, business confidence and the Duncan LEI have been eroded by heightened political uncertainty and weak global manufacturing and trade. … Meet Receding Policy Uncertainty … The two biggest sources of policy uncertainty affecting markets, the Sino-U.S. trade war and Brexit, are diminishing. However, the U.S. election will continue to lurk in the background. Chart I-3Weaker Brexit Support = No Hard Brexit Support

Weaker Brexit Support = No Hard Brexit Support

Weaker Brexit Support = No Hard Brexit Support

Brexit Westminster and Britain’s Supreme Court have rebuked U.K. Prime Minister Boris Johnson’s threat of a “No-Deal” Brexit. Moreover, parliamentary support for his latest plan, which essentially keeps Northern Ireland’s economy within the EU, indicates that the probability of a “No-Deal” Brexit has collapsed to less than 5%. This assessment is reinforced by the delay of Brexit to January 31, 2020. An election is scheduled for December 12 and the chance of a new referendum to vet the deal is escalating. According to Matt Gertken, BCA’s Geopolitical Strategist, an election does not increase the risk of a hard Brexit. Meanwhile, support for Brexit is near its lowest point since the June 2016 referendum (Chart I-3). Thus, a new plebiscite would not favor a “No Deal” Brexit. Sino-U.S. Trade War Chart I-4Why The Trade-War Ceasefire?

Why The Trade-War Ceasefire?

Why The Trade-War Ceasefire?

The trade war truce will also greatly diminish economic uncertainty. Uncertainty created by the China-U.S. conflict accentuated the collapse in business confidence and capex intentions. The “phase one deal” announced earlier this month will likely materialize. The White House’s tactical retreat on trade is tied to U.S. President Donald Trump’s desire for a second term. He cannot risk inflicting further economic pain on his base of constituents. Weekly earnings are decreasing for workers in swing states located in the industrial rust belt, especially in those areas that Trump carried in 2016 (Chart I-4). Those swing states are most affected by the slowdown in the global manufacturing and trade sectors. Beijing is also motivated to agree to truce due to its soft economy and deflationary pressures. An easing in trade uncertainty will be positive for the domestic economy. China’s willingness to replace Carrie Lam, the embattled Chief Executive of Hong Kong, and to withdraw the extradition bill at the heart of the protests confirms its eagerness to come to an agreement with the U.S. China’s readiness to make a deal is also made evident by its increasing imports of U.S. agricultural products (Chart I-4, bottom panel). Ultimately, the U.S. will not implement tariffs in December on $160 billion of Chinese shipments. Consequently, investors and businesses should become less concerned about the chances of a worsening trade war. Moreover, chances are growing of a decrease (but not a complete annulation) of the previously imposed U.S. tariffs on China. … And A Q1 2020 Acceleration In Global Growth Global economic activity will improve in Q1 2020 because the drag from China will dissipate and global liquidity conditions will improve. Many activity indicators increasingly reflect these fundamental supports. China China’s economy has reached a new low point: Q3 annual GDP growth is at a 27-year low of 6%, capital spending is weak, industrial production and profits show little life, the labor market is soft, and imports and exports continue to contract. However, a turn in policy has materialized, which will protect the domestic economy. Moreover, this summer’s Politburo and State Council statements showed an increased willingness to reflate the economy. The global economy will accelerate in Q1 2020. Credit creation has stabilized and monetary conditions have eased (Chart I-5). Faced with producer price inflation of -1.2% and employment PMIs of 47.3 and 48.2 in the manufacturing and non-manufacturing sectors, respectively, authorities have allowed the credit impulse to improve to 26% of GDP from a low of 23.8%. In accordance with this new policy direction, the drag from the shadow banking system’s contraction will slow considerably, thanks to a stabilization in both the growth rate of deposits of non-depository financial institutions and the issuance of bonds by small financial institutions. Additionally, the emission of local government bonds will accelerate. Beijing has also meaningfully eased fiscal policy, which is its preferred reflationary tool. Policymakers have cut taxes by 2.8% of GDP in the past two years. The marginal propensity of households to consume is trying to bottom (Chart I-5, bottom). If history is a guide, the acceleration in the rate of change of public-sector capex will fuel this turnaround in China’s marginal propensity to consume, and push up BCA’s China Activity Indicator (Chart I-6). Chart I-5Overlooked Chinese Improvements

Overlooked Chinese Improvements

Overlooked Chinese Improvements

Chart I-6Public Investment Matters

Public Investment Matters

Public Investment Matters

Chart I-7A Bottom In Chinese Exports Growth?

A Bottom In Chinese Exports Growth?

A Bottom In Chinese Exports Growth?

China’s economy is unlikely to bounce back as violently as in 2009, 2012 or 2016. Authorities are much more circumspect in their use of credit to reflate the economy than they were previously. Moreover, the regulatory environment will prevent a boom in the shadow banking system. Nonetheless, the fiscal push and the end of the decline in aggregate credit growth will allow the Chinese economy to stabilize and maybe pick up a bit. Therefore, China will move from a large headwind to a slight tailwind for global activity (Chart I-7, top panel). Mounting public capex also points toward a modest global recovery (Chart I-7, middle panel). Finally, the upturn in our Chinese reflation indicator, which incorporates both fiscal and monetary policy, points to a re-acceleration in U.S. capex intentions (Chart I-7, bottom panel). Global Liquidity Global liquidity conditions continue to improve and the global economy should soon respond within normal policy lags. 95% of central banks are loosening policy, which normally leads to an escalation in global activity (Chart I-8). The dominant central banks (the Federal Reserve, the European Central Bank and the Bank of Japan) will not tighten anytime soon. Inflation expectations in the U.S., the euro area and Japan stand at 1.9%, 1.1%, and 0.2%, respectively, well below levels consistent with a 2% inflation target. Moreover, U.S. core CPI has been perky, but both the ISM and the performance of transportation equities relative to utilities indicate that a deceleration in inflation is imminent (Chart I-9). Salaries are not yet inflationary either because U.S. real wages are growing in line with productivity (Chart I-9, bottom panel). In the euro area and Japan, realized core inflation remains at 1.0% and 0.5%, respectively, and supports the dovish message emanating from inflation expectations. Chart I-8Easier Global Policy Is Important

Easier Global Policy Is Important

Easier Global Policy Is Important

Chart I-9If Inflation Peaks, The U.S. Economy Will Breath A Sigh Of Relief

If Inflation Peaks, The U.S. Economy Will Breath A Sigh Of Relief

If Inflation Peaks, The U.S. Economy Will Breath A Sigh Of Relief

Liquidity indicators are reflecting this accommodative policy setting. The growth of U.S. and European bank deposits has reaccelerated from 2.5% to 6%, a development linked to the exit of a soft patch (Chart I-10). Moreover, BCA’s U.S. Financial Liquidity Indicator is still moving higher and flashing a resurgence in the BCA Global Leading Economic Indicator (LEI), the ISM Manufacturing Index, commodity prices, and EM export prices (Chart I-11). Finally, U.S. and global excess money reinforce the message of BCA’s U.S. Financial liquidity Indicator (Chart I-12). Chart I-10Deposits Suggest The Worst Of The Slowdown Is Behind Us

Deposits Suggest The Worst Of The Slowdown Is Behind Us

Deposits Suggest The Worst Of The Slowdown Is Behind Us

Chart I-11Continued Pick-Up In Financial Liquidity

Continued Pick-Up In Financial Liquidity

Continued Pick-Up In Financial Liquidity

The Fed will add to the supply of global liquidity by tackling the repo market’s seize-up. Depleting excess reserves and mounting financing needs among primary dealers resulted in the September surge in the Secured Overnight Financing Rate (SOFR). The Fed announced three weeks ago it would buy $60 billion per month of T-Bills and T-Notes, which will lead to a climbing stock of excess reserves. Higher excess reserves create a weaker dollar, stronger EM currencies and firming global PMIs (Chart I-13). Ultimately, EM currency strength eases EM financial conditions, which supports global growth (Chart I-13, bottom panel). Chart I-12Excess Liquidity Is Accelerating

Excess Liquidity Is Accelerating

Excess Liquidity Is Accelerating

Chart I-13U.S. Excess Reserves Will Grow Again

U.S. Excess Reserves Will Grow Again

U.S. Excess Reserves Will Grow Again

Borrowing activity in Advanced Economies is showing signs of life. Bank credit is already responding to the drop in global yields, and global corporate bond issuance in September 2019 rose to $434 billion. In the U.S., new issues of corporate bonds have also reaccelerated (Chart I-14). Global Growth Indicators Crucial indicators of global economic activity are picking up on this improving fundamental backdrop. The list includes: A sharp takeoff in the annualized three-month rate of change of capital goods orders in the U.S., the Eurozone and Japan (Chart I-15, top panel). Improvement in this indicator precedes progress in the annual growth rate of orders and in capex itself. Chart I-14Borrowers Are Responding To Easier Financial Conditions

Borrowers Are Responding To Easier Financial Conditions

Borrowers Are Responding To Easier Financial Conditions

Chart I-15Some Green Shoots Are Coming Through

Some Green Shoots Are Coming Through

Some Green Shoots Are Coming Through

Chart I-16Positive Market Signals

Positive Market Signals

Positive Market Signals

A significant upturn in the Philly Fed, Empire State, and Richmond Fed manufacturing surveys for October, which sends a positive signal for the ISM Manufacturing Index (Chart I-15, second panel). Moreover, the new orders and employment components of these surveys indicate that cyclical sectors of the economy will recover and the recent deterioration in employment conditions will be fleeting. A rebound in BCA’s EM economic diffusion index, which incorporates 23 variables. Such an increase usually precedes inflections in global industrial production (Chart I-15, bottom panel). An acceleration – both in absolute and relative terms - in the annual appreciation of Taiwanese stocks. A strong and outperforming Taiwanese equity market is a harbinger of firmer PMIs (Chart I-16, top two panels). A solid performance of EM carry trades financed in yen, European luxury equities, and the relative performance of global semiconductors, materials and industrial stocks, which signal stronger global PMIs (Chart I-16, bottom three panels). Bottom Line: The global economy will accelerate in Q1 2020. A melting probability of a “No-Deal” Brexit and a truce in the Sino-U.S. trade war will allow global uncertainty to recede. Concurrently, China’s economic slowdown is ending and global liquidity conditions are improving. The Dollar As The Arbiter Of Growth Chart I-17The Dollar Is A Counter-Cyclical Currency

The Dollar Is A Counter-Cyclical Currency

The Dollar Is A Counter-Cyclical Currency

The dollar faces potent headwinds. The greenback is a countercyclical currency; a business cycle upswing and a weak USD go hand in hand (Chart I-17). The tightness of this relationship results from a powerful feedback loop: weak growth boosts the dollar, but the dollar’s strength foments additional economic slowdown. Global liquidity and activity indicators signal a weaker dollar because they point toward an economic recovery. BCA’s U.S. Financial Liquidity Index, which foresaw a deceleration in the greenback’s rate of appreciation, is calling for an outright depreciation (Chart I-18, top panel). The expanding holdings of securities on U.S. commercial banks’ balance sheets (a key measure of liquidity) corroborates this message. According to a model based on the U.S., Eurozone, Japanese and Chinese broad money supply, the USD should significantly depreciate in the coming 12 months (Chart I-18, third panel). Finally, our EM Economic Diffusion Index validates pressures on the greenback, especially against commodity currencies (Chart I-18, bottom two panels). Chart I-18Liquidity And Growth Indicators Point To A Weaker Dollar

Liquidity And Growth Indicators Point To A Weaker Dollar

Liquidity And Growth Indicators Point To A Weaker Dollar