Fixed Income

Highlights Q3/2019 Performance Breakdown: Our recommended model bond portfolio underperformed the custom benchmark by -30bps during the third quarter of the year. Winners & Losers: The biggest underperformance came from underweight positions in U.S. Treasuries (-28bps) and Italian government bonds (-18bps) as yields plunged, dwarfing gains from overweights in corporate bonds in the U.S. (+11bps) and euro area (+4bps). Scenario Analysis For The Next Six Months: We are maintaining our current positioning, staying below-benchmark on duration while overweighting U.S. and euro area corporates vs. government debt. In our base case scenario, global growth will begin to stabilize but the Fed will deliver one more “insurance” rate cut by year-end, leading to corporate bond outperformance. Feature Global bond markets have enjoyed a powerful bull run throughout 2019, as yields have plummeted alongside weakening global growth and growing political uncertainty. Those two forces came to a head in the third quarter of the year, with U.S.-China trade tensions ratcheting up another notch after the imposition of higher U.S. tariffs in early August and global manufacturing PMI data moving into contraction territory – especially in the U.S. The result was a significant fall in government bond yields as markets discounted both lower inflation expectations and more aggressive monetary easing from global central banks, led by the Fed and ECB. The benchmark 10-year U.S. Treasury yield and 10-year German Bund yield plunged -40bps and -25bps, respectively, during the July-September period. Yet at the same time, global credit markets remained surprisingly stable, as the option-adjusted spread on the Bloomberg Barclays Global Corporates index was unchanged over the same three months. In this report, we review the performance of the BCA Global Fixed Income Strategy (GFIS) model bond portfolio during the eventful third quarter of 2019. We also present our updated scenario analysis, and total return projections, for the portfolio over the next six months. As a reminder to existing readers (and to new clients), the model portfolio is a part of our service that complements the usual macro analysis of global fixed income markets. The portfolio is how we communicate our opinion on the relative attractiveness between government bond and spread product sectors. This is done by applying actual percentage weightings to each of our recommendations within a fully invested hypothetical bond portfolio. Q3/2019 Model Portfolio Performance Breakdown: Good News On Credit Trumped By Bad News On Duration Chart of the WeekDuration Losses Dwarf Credit Gains In Q3/19

Duration Losses Dwarf Credit Gains In Q3/19

Duration Losses Dwarf Credit Gains In Q3/19

The total return for the GFIS model portfolio (hedged into U.S. dollars) in the third quarter was 2.0%, lagging the custom benchmark index by -30 bps (Chart of the Week).1 This brings the cumulative year-to-date total return of the portfolio to +7.8%, which has underperformed the benchmark by a disappointing –67bps. The Q3 drag on relative returns came entirely from the government bond side of the portfolio; specifically, the underweight allocation to U.S. Treasuries and Italian government bonds (Table 1). Those allocations reflected our views on overall portfolio duration (below benchmark) and a relative value consideration within European spread product (preferring corporates to Italy). Both those recommendations went against us as global bond yields dropped during Q3, with Italian yields collapsing (the benchmark 10-year yield was down –126bps) as investors chased any positive yield denominated in euros after the ECB signaled a new round of policy easing. The total return for the GFIS model portfolio (hedged into U.S. dollars) in the third quarter was 2.0%, lagging the custom benchmark index by -30 bps Table 1GFIS Model Bond Portfolio Q3/2019 Overall Return Attribution

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Providing some partial offset to the U.S. and Italy allocations were gains from overweight positions in government bonds in the U.K., Australia and Japan. More importantly, our overweights in corporate debt in the U.S. and euro area made a strong positive contribution to the performance of the portfolio. The bar charts showing the total and relative returns for each individual government bond market and spread product sector are presented in Charts 2 and 3. The most significant movers were: Chart 2GFIS Model Bond Portfolio Q3/2019 Government Bond Performance Attribution

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Chart 3GFIS Model Bond Portfolio Q3/2019 Spread Product Performance Attribution By Sector

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Biggest outperformers Overweight U.S. high-yield Ba-rated (+4bps) Overweight U.S. high-yield B-rated (+3bps) Overweight U.S. investment grade industrials (+3bps) Overweight Japanese government bonds with maturity of 5-7 years (+2bps) Overweight euro area corporates, both investment grade (+2bps) and high-yield (+2bps) Biggest underperformers Underweight U.S. government bonds with maturity beyond 10+ years (-15bps) Underweight Italy government bonds with maturity beyond 10+ years (-10bps) Underweight U.S. government bonds with maturity of 7-10 years (-5bps) Underweight Japanese government bonds with maturity beyond 10+ years (-4bps) Underweight U.S. government bonds with maturity of 3-5 years (-4bps) Chart 4 presents the ranked benchmark index returns of the individual countries and spread product sectors in the GFIS model bond portfolio for Q3/2019. The returns are hedged into U.S. dollars (we do not take active currency risk in this portfolio) and are adjusted to reflect duration differences between each country/sector and the overall custom benchmark index for the model portfolio. We have also color-coded the bars in each chart to reflect our recommended investment stance for each market during Q3/2019 (red for underweight, blue for overweight, gray for neutral).2 Ideally, we would look to see more blue bars on the left side of the chart where market returns are highest, and more red bars on the right side of the chart were returns are lowest. Chart 4Ranking The Winners & Losers From The Model Bond Portfolio In Q3/2019

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

One thing that stands out from Chart 4 is that every fixed income sector generated a positive return, except for EM USD-denominated corporates. This is a fascinating outcome given the sharp falls in risk-free government bond yields which typically would correlate to a selloff in risk assets and widening of credit spreads. The soothing balm of looser global monetary policy seems to have offset the impact of elevated uncertainty on trade and future economic growth, allowing both bond yields and credit spreads to stay low. The soothing balm of looser global monetary policy seems to have offset the impact of elevated uncertainty on trade and future economic growth, allowing both bond yields and credit spreads to stay low. We maintained an overweight stance on global spread product throughout Q3, as we felt that the monetary policy effect would continue to overwhelm uncertainty. We did, however, make some tactical adjustments to our duration stance after the U.S. raised tariffs on Chinese imports, upgrading to neutral on August 6th.3 We had felt that higher tariffs were a sign that a potential end to the U.S.-China trade conflict was now even less likely, which raised the odds of a potential risk-off financial market event that would temporarily push bond yields lower. We shifted back to a below-benchmark duration stance on September 17th, given signs of de-escalation in the trade dispute and, more importantly, some improvement evident in global leading economic indicators.4 Bottom Line: Our recommended model bond portfolio underperformed the custom benchmark index during the third quarter of the year, with the drag on performance from an underweight stance on U.S. Treasuries and Italian BTPs overwhelming the gains from corporate credit overweights in the U.S. and euro area. Future Drivers Of Portfolio Returns Looking ahead, the performance of the model bond portfolio will continue to be driven by two main factors: our below-benchmark duration bias and our overweight stance on global corporate debt versus government bonds. Chart 5Overall Portfolio Allocation: Overweight Credit

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

In terms of the specific high-level weightings in the model portfolio, we currently have a moderate overweight, equal to eight percentage points, on spread product versus government debt (Chart 5). This reflects a more constructive view on future global growth. Early leading economic indicators are starting to bottom out and global central bankers are maintaining a dovish policy bias despite low unemployment rates – both factors that will continue to benefit growth-sensitive assets like corporate debt. Early leading economic indicators are starting to bottom out and global central bankers are maintaining a dovish policy bias despite low unemployment rates – both factors that will continue to benefit growth-sensitive assets like corporate debt. We are maintaining our below-benchmark duration tilt at 0.6 years short of the custom benchmark (Chart 6). We recognize, however, that the underperformance from duration in the model portfolio will not begin to be clawed back until there are signs of a bottoming in widely-followed cyclical economic indicators like the U.S. ISM index and the German ZEW. We think that will happen given the uptick in our global leading economic indicator (LEI), but that may take a few more months to develop based on the usual lead time from the LEI to the survey data like the ISM. The hook up in the global LEI does still gives us more confidence that the big decline in global bond yields seen this year is over, especially if a potential truce in the U.S.-China trade war is soon reached, as our political strategists believe to be increasingly likely. Chart 6Overall Portfolio Duration: Moderately Below Benchmark

Overall Portfolio Duration: Moderately Below Benchmark

Overall Portfolio Duration: Moderately Below Benchmark

Turning to country allocation, we are sticking with overweights in countries where central banks are likely to be more dovish than the Fed over the next 6-12 months (Germany, France, the U.K., Japan, and Australia). We are staying underweight the U.S. where inflation expectations appear too low and Fed rate cut expectations look too extreme. The Italy underweight has become a trickier call. We have long viewed Italian debt as a growth-sensitive credit instrument rather than the yield-driven rates vehicle it became in Q3 as markets priced in fresh monetary easing measures from the ECB (including restarting government purchases). We will revisit our Italy views in an upcoming report but, until then, we will continue to view Italian BTPs within the context of our European spread product allocation. Thus, we are maintaining an overweight on euro area corporate debt (by 1% each in investment grade and high-yield) while having an equal-sized underweight (-2%) in Italian government bonds. Our combined positioning generates a portfolio that has “positive carry”, with a yield of 3.1% (hedged into U.S. dollars) that is +25bps over that of the custom benchmark index (Chart 7). That same portfolio, however, generates an estimated tracking error (excess volatility of the portfolio versus its benchmark) of 55bps - well below our self-imposed 100bps ceiling and still within the 40-60bps range we have targeted since the start of 2019 (Chart 8). Chart 7Portfolio Yield: Positive Carry From Credit

Portfolio Yield: Positive Carry From Credit

Portfolio Yield: Positive Carry From Credit

Chart 8Portfolio Risk Budget Usage: Cautious

Portfolio Risk Budget Usage: Cautious

Portfolio Risk Budget Usage: Cautious

Scenario Analysis & Return Forecasts In April 2018, we introduced a framework for estimating total returns for all government bond markets and spread product sectors, based on common risk factors.5 For credit, returns are estimated as a function of changes in the U.S. dollar, the Fed funds rate, oil prices and market volatility as proxied by the VIX index (Table 2A). For government bonds, non-U.S. yield changes are estimated using historical betas to changes in U.S. Treasury yields (Table 2B). Table 2AFactor Regressions Used To Estimate Spread Product Yield Changes

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Table 2BEstimated Government Bond Yield Betas To U.S. Treasuries

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

This framework allows us to conduct scenario analysis of projected returns for each asset class in the model bond portfolio by making assumptions on those individual risk factors. In Tables 3A & 3B, we present our three main scenarios for the next six months, defined by changes in the risk factors, and the expected performance of the model bond portfolio in each case. The scenarios, described below, all revolve around our expectation that the most important drivers of future market returns will continue to be the momentum of global growth and the path of U.S. monetary policy. The scenario inputs for the four main risk factors (the fed funds rate, the price of oil, the U.S. dollar and the VIX index) are shown visually in Chart 9. Table 3AScenario Analysis For The GFIS Model Bond Portfolio For The Next Six Months

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Table 3BU.S. Treasury Yield Assumptions For The 6-Month Forward Scenario Analysis

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Chart 9Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Base Case (Global Growth Bottoms): The Fed delivers one more -25bp rate cut by the end of 2019, the U.S. dollar weakens by -3%, oil prices rise by +10%, the VIX hovers around 15, and there is a bear-steepening of the UST curve. This is a scenario where the U.S. economy ends up avoiding recession and grows at roughly a trend-like pace. The Fed, however, still delivers one more “insurance” rate cut to mitigate the risk of low inflation expectations becoming more entrenched. Global growth is expected to bottom out as heralded by the global leading indicators. A truce (but not a full deal) is expected on the U.S.-China trade front, helping to moderately soften the U.S. dollar through reduced risk aversion. The model bond portfolio is expected to beat the benchmark index by +91bps in this case. Global Growth Strongly Rebounds: The Fed stays on hold, the U.S. dollar weakens by -5%, oil prices rise by +20%, the VIX declines to 12, there is a modest bear-steepening of the UST curve. In this tail-risk scenario, global growth starts to reaccelerate in lagged response to the global monetary easing seen this year, combined with some fiscal stimulus in major countries (China, the U.S., perhaps even Germany). The U.S. dollar weakens as global capital flows shift to markets which are more sensitive to global growth. The model bond portfolio is expected to beat the benchmark index by +106bps in this case. U.S. Downturn Intensifies: The Fed cuts rates by -75bps, the U.S. dollar is flat, oil prices fall by -15%, the VIX rises to 30; there is a bull-steepening of the UST curve. Under this tail-risk scenario, the current slowing of U.S. growth momentum gains speed, pushing the economy towards recession. The Fed cuts rates aggressively in response, helping weaken the U.S. dollar, but not before global risk assets sell off sharply to discount a worldwide recession. The model portfolio will underperform the benchmark by -38bps in this scenario. In terms of our conviction level among the main drivers of the model portfolio returns – duration allocation (across yield curves and countries) and asset allocation (credit versus government bonds) – we are most confident that credit returns will exceed those of sovereign debt over the next six months. In terms of our conviction level among the main drivers of the model portfolio returns – duration allocation (across yield curves and countries) and asset allocation (credit versus government bonds) – we are most confident that credit returns will exceed those of sovereign debt over the next six months. The underweight duration position, however, will also eventually begin to pay off if the message from the budding improvement in global leading economic indicators turns out to be correct. A collapse of the U.S.-China trade negotiations is the biggest threat to our base case, which would make the “U.S. Downturn Intensifies” scenario a more likely outcome. Bottom Line: We are maintaining our current positioning, staying below-benchmark on duration while overweighting U.S. and euro area corporates governments. In our base case scenario, global growth will begin to stabilize but the Fed will deliver one more “insurance” rate cut by year-end, leading to spread product outperformance. Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA, Research Analyst ray@bcaresearch.com Footnotes 1 The GFIS model bond portfolio custom benchmark index is the Bloomberg Barclays Global Aggregate Index, but with allocations to global high-yield corporate debt replacing very high quality spread product (i.e. AA-rated). We believe this to be more indicative of the typical internal benchmark used by global multi-sector fixed income managers. 2 Note that sectors where we made changes to our recommended weightings during Q3/2019 will have multiple colors in the respective bars in Chart 4. 3 Please see BCA Global Fixed Income Strategy Weekly Report, “Trade War Worries: Once More, With Feeling”, dated August 6, 2019, available at gfis.bcaresearch.com. 4 Please see BCA Global Fixed Income Strategy Weekly Report, “The World Is Not Ending: Return To Below-Benchmark Portfolio Duration”, dated September 17, 2019, available at gfis.bcaresearch.com. 5 Please see BCA Global Fixed Income Strategy Weekly Report, “GFIS Model Bond Portfolio Q1/2018 Performance Review: A Rough Start”, dated April 10th 2018, available at gfis.bcareseach.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Q3/2019 GFIS Model Bond Portfolio Performance Review: More Duration/Credit Divergence

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Chart 1Contagion?

Contagion?

Contagion?

Until last week, global growth weakness had been wholly confined to the manufacturing sector. But the drop to 52.6 in September’s Non-Manufacturing PMI (from 56.4 in August) raises the specter of contagion from manufacturing into the broader U.S. economy. A further drop would be consistent with an economy headed toward recession, and run contrary to the 2015/16 roadmap that has been our base case (Chart 1). We think it is still premature to abandon the 2015/16 episode as an appropriate comparable for the current period. For one thing, the hard economic data paint a rosier picture than the PMI surveys. Industrial production and core durable goods new orders are up 2.5% and 2.3% (annualized), respectively, during the past 3 months. These data have helped drive the economic surprise index above zero, an event that usually coincides with rising yields (bottom panel). The divergence between soft and hard data makes it clear that trade uncertainties are so far having a greater impact on business sentiment than on actual production, but history tells us that these divergences don’t last long. Some positive news on the trade front will be required during the next few months to raise business sentiment and push bond yields higher. Stay tuned. Feature Investment Grade: Overweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

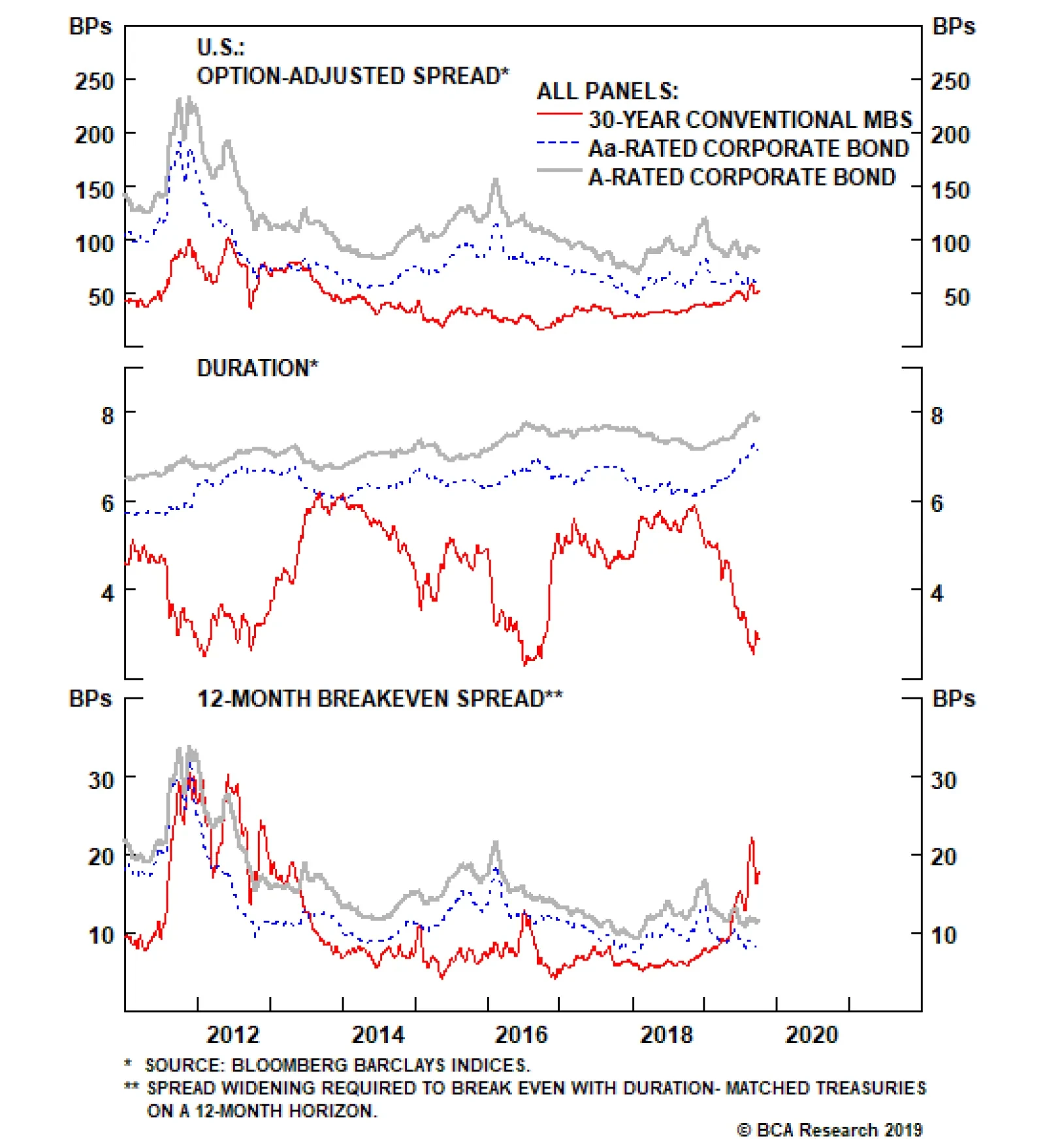

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 42 basis points in September, before giving back 37 bps in the first week of October. We consider three main factors in our credit cycle analysis: (i) corporate balance sheet health, (ii) monetary conditions, and (iii) valuation. At present, the chief conundrum for investors is that while corporate balance sheet health is weak, the monetary environment is extraordinarily accommodative.1 On balance sheets, our top-down measure of gross leverage is elevated and rising (Chart 2). In contrast, interest coverage ratios remain solid, propped up by the Fed’s accommodative stance. With inflation expectations still very low, the Fed can maintain its “easy money” policy for some time yet. This will ensure that interest coverage stays solid and that bank lending standards continue to ease (bottom panel). This is an environment where corporate bond spreads should tighten. How low can spreads go? Our assessment of reasonable spread targets for the current environment suggests that Aaa, Aa and A-rated spreads are already fully valued, while Baa-rated spreads are 13 bps cheap (panels 2 & 3).2 We recommend focusing investment grade corporate bond exposure on the Baa credit tier, and subbing some Agency MBS into your portfolio in place of corporate bonds rated A or higher. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

Crunch Time

Crunch Time

Table 3BCorporate Sector Risk Vs. Reward*

Crunch Time

Crunch Time

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

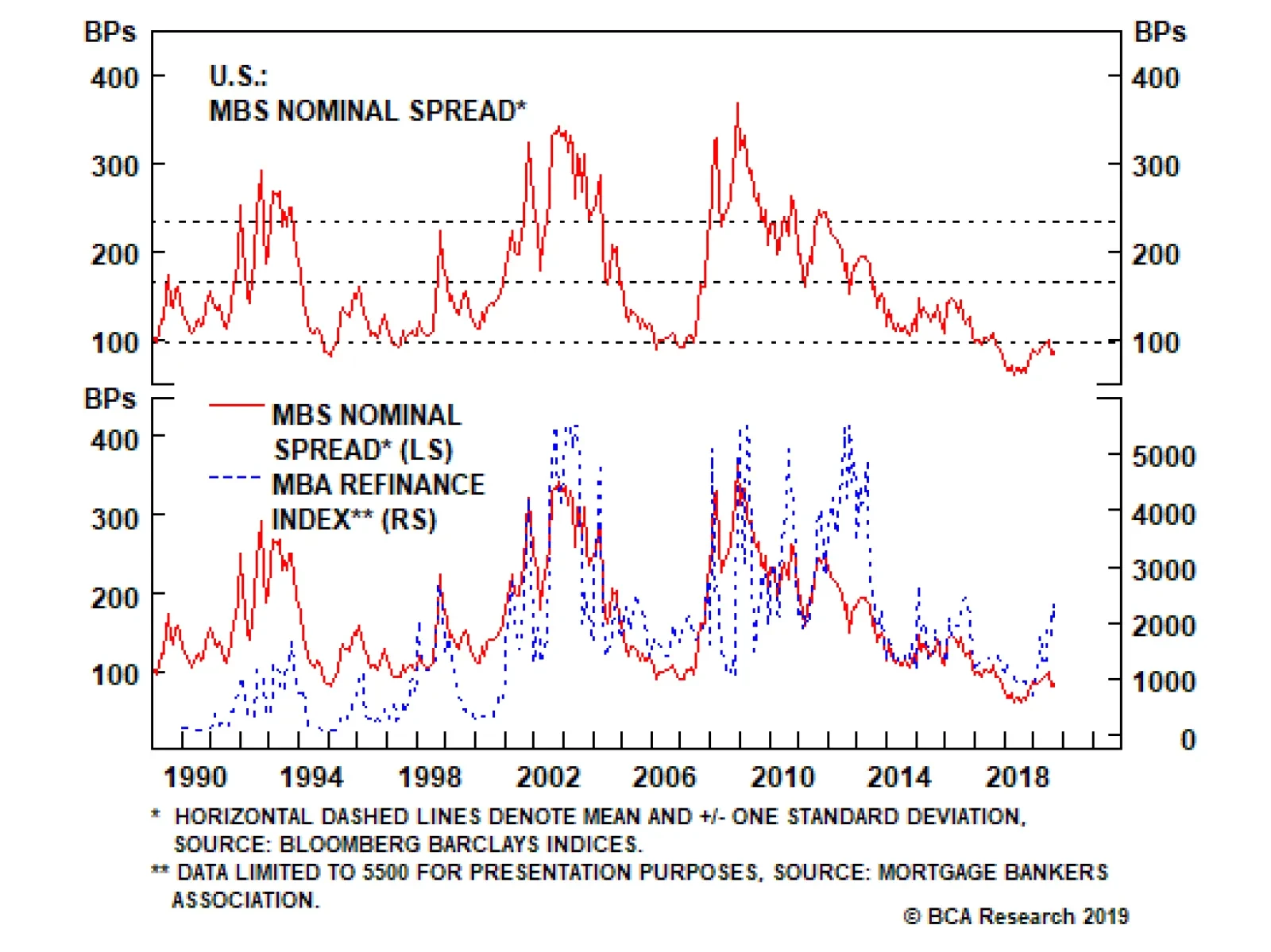

High-Yield outperformed the duration-equivalent Treasury index by 66 basis points in September, before giving back 117 bps in the first week of October. The junk index’s option-adjusted spread (OAS) has been fairly stable for most of the year, but the sector has become increasingly attractive from a risk/reward perspective.3 This is because the index’s negatively convex nature has caused its average duration to fall alongside declining Treasury yields. Chart 3 shows that while the index OAS has been rangebound, the 12-month breakeven spread has widened considerably.4 In other words, while junk expected returns have been stable, those expected returns now come with considerably less risk. As a result, the junk index OAS looks increasingly attractive relative to our spread target.5 Specifically, we now view the junk index OAS as 171 bps cheap (panel 3). Falling index duration also explains the divergence between quality spreads and the index OAS. Many have observed that the spread differential between Caa and Ba-rated junk bonds has widened in recent months, while the overall index OAS has been stable (panel 4). However, the divergence evaporates when we look at 12-month breakeven spreads instead of OAS (bottom panel). MBS: Neutral Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 24 basis points in September, before giving back 25 bps in the first week of October. MBS have underperformed Treasuries by 31 bps, year-to-date. The conventional 30-year zero volatility spread held flat at 82 bps in September, as a 3 bps increase in expected prepayment losses (option cost) was offset by a 3 bps tightening in the option-adjusted spread (OAS). In last week’s report, we recommended favoring Agency MBS over Aaa, Aa and A-rated corporate bonds.6 We have three main reasons for this recommendation. First, expected compensation is competitive. The conventional 30-year MBS OAS is now 57 bps. This is above the pre-crisis average (Chart 4), and only 4 bps below the spread offered by a Aa-rated corporate bond. Aaa, Aa and A-rated corporate bond spreads also all look expensive relative to our targets. Second, risk-adjusted compensation heavily favors MBS. The 12-month breakeven spread for a conventional 30-year MBS is 21 bps. This compares to 6 bps, 8 bps and 12 bps for Aaa, Aa and A-rated corporates, respectively. Finally, the macro environment for MBS remains supportive. Mortgage lending standards have barely eased since the financial crisis (bottom panel), and most people have already had at least one opportunity to refinance their mortgage. This burnout will keep refi activity low, and MBS spreads tight (panel 2), going forward. Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

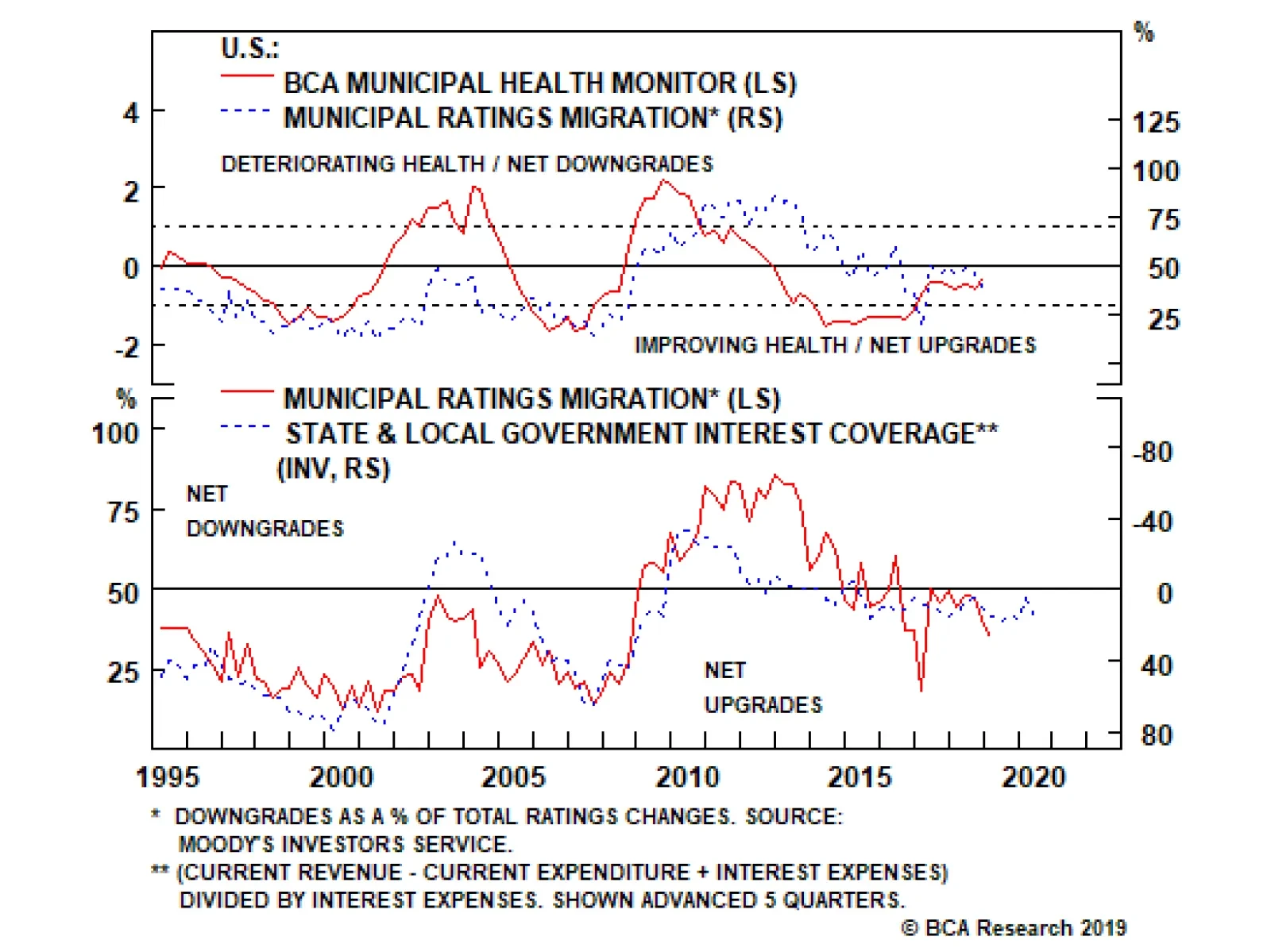

The Government-Related index outperformed the duration-equivalent Treasury index by 10 basis points in September, bringing year-to-date excess returns up to +163 bps. September returns were concentrated in the Foreign Agency sub-sector. These securities outperformed the Treasury benchmark by 55 bps on the month, bringing year-to-date excess returns up to +197 bps. Sovereign bonds underperformed duration-equivalent Treasuries by 6 bps in September, dragging year-to-date excess returns down to +436 bps. Local Authority and Domestic Agency debt underperformed by 1 bp and 2 bps on the month, respectively. Meanwhile, Supranationals bested the Treasury benchmark by a single basis point. Sovereign debt remains very expensive relative to equivalently-rated U.S. corporate credit (Chart 5). While the sector would benefit if the Fed’s dovish pivot eventually results in a weaker dollar, U.S. corporate bonds would also perform well in such an environment. Given the much more attractive starting point for U.S. corporate bond spreads, we find it difficult to recommend sovereign debt as an alternative. While sovereign debt in general looks expensive. USD-denominated Mexican sovereign bonds continue to look attractive relative to U.S. corporates (bottom panel). Investors should favor Mexican sovereigns within an otherwise underweight allocation to the sector as a whole. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 10 basis points in September, dragging year-to-date excess returns down to -57 bps (before adjusting for the tax advantage). We recommended upgrading municipal bonds from neutral to overweight in last week’s report.7 We based the decision on the increasing attractiveness of yield ratios, despite an underlying credit environment that remains supportive for munis. Municipal bond yields failed to keep pace with falling Treasury yields in recent months, and now look quite attractive as a result (Chart 6). The average Aaa-rated Municipal / Treasury (M/T) yield ratio rose 4% in September and is now back above 90%. This is well above the 81% average that prevailed in the late stages of the previous cycle, between mid-2006 and mid-2007. In fact, Aaa M/T yield ratios for every maturity are now above average pre-crisis levels. Though yield ratios still look best at the long-end of the Aaa curve (panel 2), we now recommend owning munis in place of Treasuries across the entire maturity spectrum. Fundamentally, state & local government balance sheets remain solid. We showed in last week’s report that our Municipal Health Monitor is in “improving health” territory, and noted that state & local government interest coverage is positive (bottom panel). Both of those trends are consistent with muni ratings upgrades continuing to outnumber downgrades going forward. Treasury Curve: Maintain A Barbell Curve Positioning Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve bear-steepened in September, and then bull-steepened sharply last week. All in all, the 2/10 Treasury slope is +12 bps, 12 bps steeper than it was at the end of August. The 5/30 slope is +67 bps, 10 bps steeper than at the end of August. Our fair value models (see Appendix B) continue to show that bullets are expensive relative to barbells across the entire Treasury curve. In particular, 5-year and 7-year maturities look very expensive compared to the short and long ends of the curve. Notice that the 2/5/10 butterfly spread, the spread between the 5-year bullet and a duration-matched 2/10 barbell, remains negative despite the recent 2/10 steepening (Chart 7). We have shown in prior research that the 5-year and 7-year maturities are the most highly correlated with our 12-month Fed Funds Discounter. Our discounter is currently at -74 bps, meaning that the market is priced for nearly three more Fed rate cuts during the next 12 months (top panel). We expect fewer cuts than that, and as such, think the Discounter is more likely to rise. 5-year and 7-year maturities would underperform the rest of the curve in that scenario. We also continue to hold our short position in the February 2020 fed funds futures contract. That contract is currently priced for 2 more rate cuts during the next 3 FOMC meetings. That outcome is possible, but our base case economic outlook is more consistent with 1 further cut, likely occurring this month. TIPS: Overweight Chart 8Inflation Compensation

Inflation Compensation

Inflation Compensation

TIPS underperformed the duration-equivalent nominal Treasury index by 38 basis points in September, dragging year-to-date excess returns down to -142 bps. The 10-year TIPS breakeven inflation rate fell 3 bps in September, and then another 2 bps last week. It currently sits at 1.51%, well below levels consistent with the Fed’s target. The divergence between the actual inflation data and inflation expectations is becoming increasingly stark. Trimmed mean PCE inflation has been fluctuating around the Fed’s target for most of the year (Chart 8). However, long-maturity TIPS breakeven inflation rates remain stubbornly low, nowhere near the 2.3% - 2.5% range that is consistent with the Fed’s target. As we have pointed out in prior research, it can take time for expectations to adapt to a changing macro environment.8 That being said, the 10-year TIPS breakeven inflation rate is currently 43 bps too low according to our Adaptive Expectations Model, a model whose primary input is 10-year trailing core inflation (panel 4). It is highly likely that the Fed will have to tolerate some overshoot of its 2% inflation target in order to re-anchor inflation expectations near desired levels. We anticipate that the committee will do so, and we maintain our view that long-dated TIPS breakevens will move above 2.3% before the end of the cycle. ABS: Underweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 2 basis points in September, dragging year-to-date excess returns down to +72 bps. The index option-adjusted spread for Aaa-rated ABS widened 2 bps on the month. It currently sits at 36 bps, very close to its minimum pre-crisis level (Chart 9). ABS also appear unattractive on a risk/reward basis, as both Aaa-rated auto loans and credit cards have moved into the “Avoid” quadrant of our Excess Return Bond Map (Appendix C). The Map uses each bond sector’s spread, duration and volatility to calculate the likelihood of earning or losing 100 bps of excess return versus Treasuries on a 12-month horizon. At present, the Map shows that ABS offer poor expected return for their level of risk. In addition to poor valuation, the ABS sector’s credit fundamentals are shifting in a negative direction. Household interest payments continue to trend up, suggesting a higher delinquency rate in the future (panel 3). Meanwhile, senior loan officers continue to tighten lending standards for both credit cards and auto loans. Tighter lending standards usually coincide with rising delinquencies (bottom panel). All in all, the combination of poor value and deteriorating credit quality leads us to recommend an underweight allocation to consumer ABS. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 9 basis points in September, bringing year-to-date excess returns up to +227 bps. The index option-adjusted spread for non-agency Aaa-rated CMBS held flat on the month, before widening 4 bps last week. It currently sits at 75 bps, below average pre-crisis levels but above levels seen in 2018 (Chart 10). The macro outlook for commercial real estate is somewhat unfavorable, with lenders tightening loan standards (panel 4) amidst falling demand (bottom panel). Commercial real estate prices have accelerated of late, but are still not keeping pace with CMBS spreads (panel 3). Despite the poor fundamental picture, our Excess Return Bond Map shows that CMBS offer a reasonably attractive risk/reward trade-off compared to other bond sectors (see Appendix C). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 2 basis points in September, bringing year-to-date excess returns up to +90 bps. The index option-adjusted spread held flat on the month, before widening by 5 bps last week. It currently sits at 61 bps. The Excess Return Bond Map in Appendix C shows that Agency CMBS offer high potential return compared to other low-risk spread products. Appendix A - The Golden Rule Of Bond Investing We follow a two-step process to formulate recommendations for bond portfolio duration. First, we determine the change in the federal funds rate that is priced into the yield curve for the next 12 months. Second, we decide – based on our assessments of the economy and Fed policy – whether the change in the fed funds rate will exceed or fall short of what is priced into the curve. Most of the time, a correct answer to this question leads to the appropriate duration call. We call this framework the Golden Rule Of Bond Investing, and we demonstrated its effectiveness in the U.S. Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018, available at usbs.bcaresearch.com. Chart 11 illustrates the Golden Rule’s track record by showing that the Bloomberg Barclays Treasury Master Index tends to outperform cash when rate hikes fall short of 12-month expectations, and vice-versa. Chart 11The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

At present, the market is priced for 74 basis points of cuts during the next 12 months. We anticipate fewer rate cuts over that time horizon, and therefore anticipate that below-benchmark portfolio duration positions will profit. We can also use our Golden Rule framework to make 12-month total return and excess return forecasts for the Bloomberg Barclays Treasury index under different scenarios for the fed funds rate. Excess returns are relative to the Bloomberg Barclays Cash index. To forecast total returns we first calculate the 12-month fed funds rate surprise in each scenario by comparing the assumed change in the fed funds rate to the current value of our 12-month discounter. This rate hike surprise is then mapped to an expected change in the Treasury index yield using a regression based on the historical relationship between those two variables. Finally, we apply the expected change in index yield to the current characteristics (yield, duration and convexity) of the Treasury index to estimate total returns on a 12-month horizon. The below tables present those results, along with 95% confidence intervals. Excess returns are calculated by subtracting assumed cash returns in each scenario from our total return projections.

Crunch Time

Crunch Time

Crunch Time

Crunch Time

Appendix B - Butterfly Strategy Valuation The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com U.S. Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of +48 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 48 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As of October 4, 2019)

Crunch Time

Crunch Time

Table 5Butterfly Strategy Valuation: Standardized Residuals (As of October 4, 2019)

Crunch Time

Crunch Time

Table 6

Crunch Time

Crunch Time

Appendix C - Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the U.S. fixed income market. The Map employs volatility-adjusted breakeven spread analysis to show how likely it is that a given sector will earn/lose money during the subsequent 12 months. The Map does not incorporate any macroeconomic view. The horizontal axis of the Map shows the number of days of average spread widening required for each sector to lose 100 bps versus a position in duration-matched Treasuries. Sectors plotting further to the left require more days of average spread widening and are therefore less likely to see losses. The vertical axis shows the number of days of average spread tightening required for each sector to earn 100 bps in excess of duration-matched Treasuries. Sectors plotting further toward the top require fewer days of spread tightening and are therefore more likely to earn 100 bps of excess return. Chart 12Excess Return Bond Map (As Of October 4, 2019)

Crunch Time

Crunch Time

Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Weekly Report, “Corporate Bond Investors Should Not Fight The Fed”, dated September 17, 2019, available at usbs.bcaresearch.com 2 For more details on how we arrive at our spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 3 Please see U.S. Bond Strategy Weekly Report, “Corporate Bond Investors Should Not Fight The Fed”, dated September 17, 2019, available at usbs.bcaresearch.com 4 The 12-month breakeven spread is the spread widening required to break even with a duration-matched position in Treasuries on a 12-month horizon. It can be approximated by OAS divided by duration. 5 For more details on how we arrive at our spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 6 Please see U.S. Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com 7 Please see U.S. Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com 8 Please see U.S. Bond Strategy Weekly Report, “Adaptive Expectations In The TIPS Market”, dated November 20, 2018, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

Brief Market Overview The S&P 500 convulsed last week, as a slew of weaker-than-expected data shattered investors’ confidence in the longevity of the business and profit cycles. Importantly, both ISM surveys declined month-over-month, arguing that the manufacturing sector’s ails are infecting services industries (second panel, Chart 1). Chart 1The U.S. Dollar Is The Key Indicator To Monitor

The U.S. Dollar Is The Key Indicator To Monitor

The U.S. Dollar Is The Key Indicator To Monitor

The “In Fed We Trust” doctrine will get severely tested in upcoming weeks. The Federal Reserve’s reaction function to the poor data took center stage with bond investors pricing a 75% probability of a rate cut in late October. However, our four factor EPS growth model continues to predict that earnings will remain weak for the rest of 2019 (not shown). Thus, next year’s 10% EPS growth is wishful thinking and profit growth will begin to bottom in Q1/2020 at the earliest. Absent profit growth, stocks will have to face reality and continue to drift lower. Importantly, the U.S. dollar – the great reflator – is the key determinant of both profit and global economic growth in coming quarters. The third panel of Chart 1 shows that currently that are no advanced economy central banks that have a policy rate higher than the Fed. Historically, this has been U.S. dollar bullish and has weighed on SPX momentum (trade-weighted U.S. dollar shown inverted, bottom panel, Chart 1). It remains to be seen if aggressive Fed easing can change this relationship, stave off recession and engineer a soft landing. U.S. Equity Strategy’s view remains intact that things will get worse before they get better and therefore a cautious overall U.S. equity market stance is still warranted on a cyclical 9-12 month time horizon. NIPA VS. SPX Profit Margins On the eve of earnings season, we decided to delve deeper into corporate profits and margins, and tally where we are in the cycle, specifically with regard to profit margin drivers. To start off, we compare overall economy profits, as measured by the NIPA accounts, with SPX earnings (Chart 2). While a lot of ink has been spent on this topic and the differences between these two profit measures are more or less well recognized and understood, Kenneth A. Petrick’s commentary on the issue is worth re-reading. Without going into much detail, according to Petrick four key reasons explain the differences between NIPA and S&P 500 profits: “coverage, changing shares, industry representation and accounting principles”.1 What interests us is the leading property of NIPA profits. Importantly, NIPA profits have peaked in advance of SPX earnings in the previous three cycles. Economy-wide profits may have already peaked this cycle, warning that the SPX earnings juggernaut is long in the tooth (top panel, Chart 2). Chart 2Earnings Fatigue

Earnings Fatigue

Earnings Fatigue

Given that NIPA profits include a broader universe of firms, small and medium enterprise (SME) profits are weighing on the overall NIPA number. The recent drubbing in economically hypersensitive S&P 400 (mid-caps) and S&P 600 (small-caps) profit estimates confirms this SME profit deterioration and forewarns that SPX profits are likely running out of fuel. While the SPX has not cracked yet courtesy of the heavyweight S&P software index, the Value Line Arithmetic (VLA, gauging the average stock) and Value Line Geometric (VLG, gauging the median stock) indexes appear to have peaked and correspond better to the NIPA profits as these indexes are broad-based are not market capitalization weighted (bottom panel, Chart 3). Chart 3Top Chart Of The Year

Top Chart Of The Year

Top Chart Of The Year

Worryingly for the S&P 500, the VLG index is an excellent leading indicator of the SPX. Based on empirical evidence, it has led the SPX tops in the past three cycles, making it a serious contender for our “Chart Of The Year” award (top panel, Chart 3). Not only have NIPA profits likely crested, but NIPA profit margins are in steep retreat and have definitively peaked. Similar to earnings, NIPA margins lead SPX profit margins (top panel, Chart 4). Importantly, the delta between the two margin gauges is surprisingly wide. This margin gap now sits nearly three standard deviations above the historical mean and has only been wider during the dotcom bubble (bottom panel, Chart 4). Our sense is that such an acute divergence is unsustainable and will likely narrow via a mean reversion in SPX margins. Chart 4Mind The Gap

Mind The Gap

Mind The Gap

Primary Margin Drivers Taking a deeper dive into traditional margin drivers is instructive. We use SPX margins since 1960 and prior to that we have used reconstructed SPX earnings divided by U.S. GDP (gauging SPX sales) to recreate a longer-term equity market profit margin proxy. The primary net-profit margin drivers are: Interest rates, Tax rates, Labor costs / Globalization, And corporate pricing power. Globalization has been another significant profit margin booster in the U.S. As countries are more outward looking, trade flourishes and openness to trade allows the free flow of capital to take advantage of profit maximizing projects. The bond bull market since the early 1980s has been a clear contributor to the secular advance in profits margins. Interest rates cut both ways and the big rise in long-term bond yields post World War II ate into margins. If the bond bull market is ending, then interest rates will start eating into margins anew (interest rates shown inverted, top panel, Chart 5). Intuitively, taxes and margins are also inversely correlated (tax rate shown inverted, bottom panel, Chart 5). Following the 2018 fiscal easing package, the effective corporate tax rate is now hovering in the mid-teens and explains the jump to all-time highs in SPX margins. We doubt corporate tax rates will drop further. At best, taxes will be margin-neutral in the coming years. Rising labor input costs squeeze margins and declining wages boost corporate profit margins. While labor’s share of income tentatively peaked in 1980, the late-1990s is this series’ ultimate peak and since then, it has been in a steady decline (employee compensation shown inverted, second panel, Chart 5). This labor input cost suppression has likely run its course and given that the U.S. economy is at full employment, wage inflation should also start denting margins. Globalization has been another significant profit margin booster in the U.S. As countries are more outward looking, trade flourishes and openness to trade allows the free flow of capital to take advantage of profit maximizing projects. Following the end of the Great Recession and similar to the Great Depression, de-globalization has commenced (third panel, Chart 5). Chart 5Primary...

Primary...

Primary...

Clearly, the Sino-U.S. war has accentuated and accelerated the inward movement of countries including Korea and Japan, and has had negative knock on effects on trade as evidenced by the now nearly two-year old global growth deceleration. The longer the U.S./China trade war remains unresolved, the deeper the cracks in the foundations of global trade. Such a backdrop is negative for profit margins, as inward looking countries prevent capital from being allocated most efficiently. Moreover, the uprooting of supply chains due to the trade war hurts margins and the redeployment of equipment in different jurisdictions will weigh on margins at a time when final demand suffers a setback. Corporate pricing power is deteriorating, which will negatively impact profit margins, given that they are joined at the hip. The current global manufacturing recession is wreaking havoc on selling prices around the world as a number of countries are experiencing outright producer price deflation. To compete, the U.S. corporate sector is doomed to suffer the same fate, which is depressing our Corporate Pricing Power proxy, an indicator composed of 60 top-down sector price series (bottom panel, Chart 6). Chart 6...And Secondary Profit Margin Drivers

...And Secondary Profit Margin Drivers

...And Secondary Profit Margin Drivers

Secondary Margin Drivers The ability of the overall corporate sector to lift prices is largely a function of firming final demand (i.e. volumes) and a falling greenback for the 40% of SPX sales that are international. This leads us to two secondary profit margin drivers: The trade-weighted U.S. dollar, And the yield curve. The ability of the overall corporate sector to lift prices is largely a function of firming final demand (i.e. volumes) and a falling greenback for the 40% of SPX sales that are international. Thus, not only is S&P 500 revenue growth and the trade-weighted U.S. dollar tightly inversely correlated, but also the same holds true for the greenback and profit margins (U.S. dollar shown inverted, top panel, Chart 6). Given that the U.S. dollar refuses to fall and is breaking out according to some Federal Reserve trade-weighted indexes, the path of least resistance for profit margins points south. The yield curve is related to the primary “interest rate” driver discussed above, but its most important signal concerns the business cycle. Empirically, profit margins mean revert at the onset of recession (yield curve shown advanced, middle panel, Chart 6). As a reminder, parts of the yield curve inverted last December, signaling that a corporate profit margin squeeze is looming. Income Inequality And Margins Finally, we make an interesting geopolitical observation. Rising profit margins are synonymous with wealth accruing to the top 1% of U.S. families and vice versa. This relationship dates back to the late-1920s, as far back as our dataset goes. Using Piketty and Saez data excluding capital gains it is clear that profit margin expansion accentuates income inequality (Chart 7).2 Chart 7Income Inequality And Margins

Income Inequality And Margins

Income Inequality And Margins

Rising profit margins lead to rising profits. Because families at the top of the income distribution are more often than not business owners, income disparities are the widest when margins are in overshoot territory. Eventually this income chasm comes to a head and potentially explains the rise of populism. Income re-distribution is therefore a rising probability event in the coming decades.3 Bottom Line: Unequivocally, all six key drivers we have identified (interest rates, tax rates, labor costs / globalization, corporate pricing power, yield curve and the U.S. dollar) are firing warning shots that profit margins have peaked and a “catch down” phase of SPX margins to NIPA margins is in store in the coming quarters. Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com Footnotes 1 https://apps.bea.gov/scb/pdf/national/niparel/2001/0401cpm.pdf 2 https://eml.berkeley.edu/~saez/TabFig2017.xls 3 Please see BCA Geopolitical Strategy Special Report, “The End Of The Anglo-Saxon Economy?” dated April 13, 2016, available at gps.bcaresearch.com.

Highlights MARKET FORECASTS

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Investment Strategy: Markets have entered a “show me” phase. Better economic data and meaningful progress on the trade negotiations will be necessary for stocks to move sustainably higher. We think both preconditions will be realized. Until then, risk assets could come under pressure. Global Asset Allocation: Investors should overweight stocks relative to bonds over a 12-month horizon, but maintain higher-than-normal cash positions in the near term as a hedge against downside risks. Equities: EM and European stocks will outperform once global growth bottoms out. Cyclical sectors, including financials, will also start to outperform defensives when the growth cycle turns. Bonds: Central banks will remain dovish, but yields will nevertheless rise modestly on the back of stronger global growth. Favor high-yield corporate credit over government bonds. Currencies: As a countercyclical currency, the U.S. dollar should peak later this year. Commodities: Oil and industrial metals prices will move higher. Gold prices have entered a holding pattern, but should shine again late next year or in 2021 when inflation finally breaks out. Feature Dear Client, In lieu of this report, I hosted a webcast on Monday, October 7th at 10:00 AM EDT, where I discussed the major investment themes and views I see playing out for the rest of the year and beyond. Best regards, Peter Berezin, Chief Global Strategist I. Global Macro Outlook A Testing Phase For The Global Economy The global economy has reached a critical juncture. Growth has been slowing since early 2018, reaching what many would regard as “stall speed.” This is the point where economic weakness begins to feed on itself, potentially triggering a recession. Will the growth slowdown worsen? Our guess is that it won’t. Global financial conditions have eased significantly over the past four months, thanks in part to the dovish pivot by most central banks. Looser financial conditions usually bode well for global growth (Chart 1). Our global leading indicator has hooked up, mainly due to a marginal improvement in emerging markets’ data (Chart 2). Chart 1Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Chart 2Global LEI Has Moved Off Its Lows

Global LEI Has Moved Off Its Lows

Global LEI Has Moved Off Its Lows

An important question is whether the weakness in the manufacturing sector will spread to the much larger services sector. There is some evidence that this is happening, with yesterday’s weaker-than-expected ISM non-manufacturing release being the latest example. Nevertheless, the deceleration in service sector activity has been limited so far (Chart 3). Even in Germany, with its large manufacturing base, the service sector PMI remains in expansionary territory. This is a key difference with the 2001/02 and 2008/09 periods, when service sector activity collapsed in lockstep with manufacturing activity. Chart 3AThe Service Sector Has Softened Less Than Manufacturing (I)

The Service Sector Has Softened Less Than Manufacturing (I)

The Service Sector Has Softened Less Than Manufacturing (I)

Chart 3BThe Service Sector Has Softened Less Than Manufacturing (II)

The Service Sector Has Softened Less Than Manufacturing (II)

The Service Sector Has Softened Less Than Manufacturing (II)

The Drive-By Slowdown If one were to ask most investors the reasons behind the manufacturing slowdown, they would probably cite the trade war or the Chinese deleveraging campaign. These are both valid reasons, but there is a less well-known culprit: autos. According to WardsAuto, global auto sales fell by over 5% in the first half of the year, by far the biggest decline since the Great Recession (Chart 4). Production dropped by even more. Chart 4Weakness In The Auto Sector Has Exacerbated The Manufacturing Downturn

Weakness In The Auto Sector Has Exacerbated The Manufacturing Downturn

Weakness In The Auto Sector Has Exacerbated The Manufacturing Downturn

Chart 5U.S. Auto Demand Is Recovering

U.S. Auto Demand Is Recovering

U.S. Auto Demand Is Recovering

The weakness in the global auto sector reflects a variety of factors. New stringent emission requirements, expiring tax breaks, lagged effects from tighter auto loan lending standards, and trade tensions have all played a role. In addition, the decline in gasoline prices in 2015/16 probably brought forward some automobile purchases. This suggests that the 2015/16 global manufacturing downturn may have helped sow the seeds for the current one. The fact that automobile output is falling faster than sales is encouraging because it means that excess inventories are being worked off. U.S. auto loan lending standards have started to normalize, with banks reporting stronger demand for auto loans in the latest Senior Loan Officer Survey (Chart 5). In China, auto sales have troughed after having declined by as much as 14% earlier this year (Chart 6). The Chinese automobile ownership rate is a fifth of what it is in the U.S., a quarter of what it is in Japan, and a third of what it is in Korea (Chart 7). Given the low starting point, Chinese auto sales are likely to resume their secular uptrend. Chart 6Auto Sector In China Is Finding A Floor

Auto Sector In China Is Finding A Floor

Auto Sector In China Is Finding A Floor

Chart 7China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

The Trade War: Tracking Towards A Détente? Chart 8A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

Manufacturing cycles typically last about three years – 18 months of slowing growth followed by 18 months of rising growth (Chart 8). To the extent that the global manufacturing PMI peaked in the first half of 2018, we should be nearing the end of the current downturn. Of course, much depends on policy developments. As we go to press, high-level negotiations between the U.S. and China have resumed. While it is impossible to predict the outcome of these talks, it does appear that both sides have an incentive to de-escalate the trade conflict. President Trump gets much better marks from voters on his management of the economy than on anything else, including his handling of trade negotiations with China (Chart 9). A protracted trade war would hurt U.S. growth, while weakening the stock market. Both would undermine Trump’s re-election prospects. Chart 9Trump Gets Reasonably High Marks On His Handling Of The Economy, But Not Much Else

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Chart 10Who Will Win The 2020 Democratic Nomination?

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

China also wants to bolster growth. As difficult as it has been for the Chinese leadership to deal with Donald Trump, trying to secure a trade deal with him after he has been re-elected would be even more challenging. This would especially be the case if Trump thought that the Chinese had tried to sabotage his re-election bid. Even if Trump were to lose the election, it is not clear that China would end up with someone more pliant to deal with on trade matters. Does the Chinese government really want to negotiate over environmental standards and human rights with President Warren, who betting markets now think has a better chance of becoming the Democratic nominee than Joe Biden (Chart 10)? The Democrats’ initiative to impeach President Trump make a trade resolution somewhat more likely. First, it brings attention to Joe Biden’s (and his son’s) own dubious dealings in Ukraine, thus delivering a blow to China’s preferred U.S. presidential candidate. Second, it makes Trump more inclined to want to put the China spat behind him in order to focus his energies on domestic matters. More Chinese Stimulus? Strategically, China has a strong incentive to stimulate its economy in order to prop up growth and gain greater leverage in the trade negotiations. The Chinese credit impulse bottomed in late 2018. The impulse leads Chinese nominal manufacturing output and most other activity indicators by about nine months (Chart 11). So far, the magnitude of China’s credit/fiscal easing has come nowhere close to matching the stimulus that was unleashed on the economy both in 2015/16 and 2008/09. This is partly because the authorities are more worried about excessive debt levels today than they were back then, but it is also because the economy is in better shape. The shock from the trade war has not been nearly as bad as the Great Recession – recall that Chinese exports to the U.S. are only 2.7% of GDP in value-added terms. Unlike in 2015/16, when China lost over $1 trillion in external reserves, capital outflows have remained muted this time around (Chart 12). Chart 11Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Chart 12China: No Major Capital Outflows

China: No Major Capital Outflows

China: No Major Capital Outflows

Better-than-expected Chinese PMI data released earlier this week offers a glimmer of hope. Nevertheless, in light of the disappointing August activity numbers, China is likely to increase the pace of stimulus in the coming months. The authorities have already reduced bank reserve requirements. We expect them to cut policy rates further in the coming months. They will also front-load local government bond issuance, which should help boost infrastructure spending. European Growth Should Improve A pickup in global growth will help Europe later this year. Germany, with its trade-dependent economy, will benefit the most. Chart 13Spreads Have Come In Across Southern Europe

Spreads Have Come In Across Southern Europe

Spreads Have Come In Across Southern Europe

Chart 14Faster Money Growth Bodes Well For GDP Growth In The Euro Area

Faster Money Growth Bodes Well For GDP Growth In The Euro Area

Faster Money Growth Bodes Well For GDP Growth In The Euro Area

Falling sovereign spreads should also support Southern Europe (Chart 13). The Italian 10-year spread with German bunds has narrowed by almost a full percentage point since mid-August, taking the Italian 10-year yield down to 0.83%. Greek 10-year bonds are now yielding less than U.S. Treasurys (the Greek manufacturing PMI is currently the strongest in the world). With the ECB back in the market buying sovereign and corporate debt, borrowing rates should remain low. Euro area money growth, which leads GDP growth, has already picked up (Chart 14). Bank lending to the private sector should continue to accelerate. A modest serving of fiscal stimulus will also help. The European Commission estimates that the fiscal thrust in the euro area will increase by 0.5% of GDP in 2019 (Chart 15). Assuming, conservatively, a fiscal multiplier of one, this would boost euro area growth by half a percentage point. Owing to lags between changes in fiscal policy and their impact on the real economy, most of the gains to GDP growth will occur over the remainder of this year and in 2020. Chart 15Euro Area Fiscal Stimulus Will Also Boost Growth

Euro Area Fiscal Stimulus Will Also Boost Growth

Euro Area Fiscal Stimulus Will Also Boost Growth

Chart 17Brexit Angst: A Case Of Bremorse

Brexit Angst: A Case Of Bremorse

Brexit Angst: A Case Of Bremorse

Chart 16U.K.: Brexit Uncertainty Is Weighing On Growth

U.K.: Brexit Uncertainty Is Weighing On Growth

U.K.: Brexit Uncertainty Is Weighing On Growth

In the U.K., Brexit uncertainty continues to weigh on growth. U.K. business investment has been especially hard hit (Chart 16). Prime Minister Boris Johnson remains insistent that he will take the U.K. out of the EU with or without a deal at the end of October. We would downplay his bluster. The Supreme Court has already denied his attempt to shutter parliament. The public is having second thoughts about the desirability of Brexit (Chart 17). While we do not have a strong view on the exact plot twists in the Brexit saga, we maintain that the odds of a no-deal Brexit are low. This is good news for U.K. growth and the pound. Japan: Own Goal Recent Japanese data releases have not been encouraging: Machine tool orders declined by 37% year-over-year in August. Exports contracted by over 8%, with imports recording a drop of 12%. The September PMI print exposed further deterioration in manufacturing, with the index falling to 48.9 from 49.3 in August. In addition, industrial production contracted by more than expected in August, falling by 1% month-over-month, and close to 5% year-over-year. The ongoing uncertainty surrounding the U.S.-China trade negotiations, as well as Japan’s own tensions with neighboring South Korea, have also weighed on the Japanese economy. Japanese industrial activity will improve later this year as global growth rebounds. But the government has not helped growth prospects by raising the consumption tax on October 1st. While various offsets will blunt the full effect of the tax hike, it still amounts to unwarranted tightening in fiscal policy. Nominal GDP has barely increased since the early 1990s. What Japan needs are policies that boost nominal income. Such reflationary policies may be the only way to stabilize debt-to-GDP without pushing the economy back into a deflationary spiral.1 The U.S.: Hanging Tough Chart 18U.S. Has A Smaller Share Of Manufacturing Than Most Other Developed Economies

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

The U.S. economy has fared relatively well during the latest global economic downturn, partly because manufacturing represents a smaller share of GDP than in most other economies (Chart 18). According to the Atlanta Fed GDPNow model, real GDP is on track to rise at a trend-like pace of 1.8% in the third quarter (Chart 19). Personal consumption is set to increase by 2.5%, after having grown by 4.6% in the second quarter. Consumer spending should stay robust, supported by rising wage growth. The personal savings rate also remains elevated, which should help cushion households from any adverse shocks (Chart 20). Chart 19U.S. Growth Has Softened, But Is Still Close To Trend

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Residential investment finally looks as though it is turning the corner. Housing starts, building permits, and home sales have all picked up. Given the tight relationship between mortgage rates and homebuilding, construction activity should accelerate over the next few quarters (Chart 21). Low inventory and vacancy rates, rising household formation, and reasonable affordability all bode well for the housing market (Chart 22). Chart 20The Savings Rate Has (A Lot Of) Room To Drop, Judging From The Historical Relationship With Wealth

The Savings Rate Has (A Lot Of) Room To Drop, Judging From The Historical Relationship With Wealth

The Savings Rate Has (A Lot Of) Room To Drop, Judging From The Historical Relationship With Wealth

Chart 21U.S. Housing Will Rebound

U.S. Housing Will Rebound

U.S. Housing Will Rebound

Chart 22U.S. Housing: On A Solid Foundation

U.S. Housing: On A Solid Foundation

U.S. Housing: On A Solid Foundation

Chart 23U.S. Capex Plans Have Come Off Their Highs, But Are Nowhere Close to Recessionary Levels

U.S. Capex Plans Have Come Off Their Highs, But Are Nowhere Close to Recessionary Levels

U.S. Capex Plans Have Come Off Their Highs, But Are Nowhere Close to Recessionary Levels

In contrast to residential investment, business capex continues to be weighed down by the manufacturing recession, a strong dollar, and trade policy uncertainty. Core durable goods orders declined in August. Capex intention surveys have also weakened, although they remain well above recessionary levels (Chart 23). The ISM manufacturing index hit its lowest level since July 2009 in September. The internals of the report were not quite as bad as the headline. The new orders-to-inventories component, which leads the ISM by two months, moved back into positive territory. The weak ISM print also stands in contrast to the more upbeat Markit U.S. manufacturing PMI, which rose to its highest level since April. Statistically, the Markit PMI does a better job of tracking official measures of U.S. manufacturing output, factory orders, and employment than the ISM. Taking everything together, the U.S. economy is likely to see modestly stronger growth later this year, as the global manufacturing recession comes to an end, while strong consumer spending and an improving housing market bolster domestic demand. II. Financial Markets Global Asset Allocation Markets have entered a “show me” phase. Better economic data and meaningful progress on the trade negotiations will be necessary for stocks to move sustainably higher. As such, investors should maintain larger-than-normal cash positions for the time being to guard against downside risks. Chart 24Stocks Will Outperform Bonds If Growth Recovers

Stocks Will Outperform Bonds If Growth Recovers

Stocks Will Outperform Bonds If Growth Recovers

Fortunately, any pullback in risk asset prices is likely to be temporary. If trade tensions subside and global growth rebounds later this year, as we expect, stocks and spread product should handily outperform government bonds over a 12-month horizon (Chart 24). Admittedly, there are plenty of things that could upend this sanguine 12-month recommendation: Global growth could continue to deteriorate; the trade war could intensify; supply-side shocks could cause oil prices to spike up again; the U.K. could end up leaving the EU in a “hard Brexit” scenario; and last but not least, Elizabeth Warren or some other far-left candidate could end up becoming the next U.S. president. The key question for investors today is whether these risks have been fully discounted in financial markets. We think they have. Chart 25 shows our estimates for the global equity risk premium (ERP), calculated as the difference between the earnings yield and the real bond yield. Our calculations suggest that stocks still look quite cheap compared to bonds. Chart 25AEquity Risk Premia Remain Quite High (I)

Equity Risk Premia Remain Quite High (I)

Equity Risk Premia Remain Quite High (I)

Chart 25BEquity Risk Premia Remain Quite High (II)

Equity Risk Premia Remain Quite High (II)

Equity Risk Premia Remain Quite High (II)

One might protest that the ERP is high only because today’s ultra-low bond yields are reflecting very poor growth prospects. There is some truth to that claim, but not as much as one might think. While trend GDP growth has fallen in the U.S. over the past decade, bond yields have declined by even more. The gap between U.S. potential nominal GDP growth, as estimated by the Congressional Budget Office, and the 10-year Treasury yield is close to two percentage points, the highest since 1979 (Chart 26). Chart 26Bond Yields Have Fallen More Than Trend Nominal GDP Growth

Bond Yields Have Fallen More Than Trend Nominal GDP Growth

Bond Yields Have Fallen More Than Trend Nominal GDP Growth

At the global level, trend GDP growth has barely changed since 1980, largely because faster-growing emerging markets now make up a larger share of the global economy (Chart 27). For large multinational companies, global growth, rather than domestic growth, is the more relevant measure of economic momentum. Gauging Future Equity Returns A high ERP simply says that equities are attractive relative to bonds. To gauge the prospective return to stocks in absolute terms, one should look at the absolute level of valuations. Chart 27The Trend In Global Growth Has Remained Steady Thanks To Faster-Growing EM

chart 27

The Trend In Global Growth Has Remained Steady Thanks To Faster-Growing EM

The Trend In Global Growth Has Remained Steady Thanks To Faster-Growing EM

Chart 28S&P 500: All Of The Increase In Margins Has Occurred In The IT Sector

S&P 500: All Of The Increase In Margins Has Occurred In The IT Sector

S&P 500: All Of The Increase In Margins Has Occurred In The IT Sector

As we argued in a recent report entitled “TINA To The Rescue?,”2 the earnings yield can be used as a proxy for the expected real total return on equities. Empirically, the evidence seems to bear this out: Since 1950, the earnings yield on U.S. equities has averaged 6.7%, compared to a real total return of 7.2%. Today, the trailing and forward PE ratio for U.S. stocks stand at 21.1 and 17.4, respectively. Using a simple average of the two as a guide for future returns, U.S. stocks should deliver a long-term real total return of 5.2%. While this is below its historic average, it is still a fairly decent return. One might complain that this calculation overstates prospective equity returns because the U.S. earnings yield is temporarily inflated by abnormally high profit margins. The problem with this argument is that virtually all of the increase in S&P 500 margins has occurred in just one sector: technology. Outside of the tech sector, S&P 500 margins are not far from their historic average (Chart 28). If high IT margins reflect structural changes in the global economy – such as the emergence of “winner take all” companies that benefit from powerful network effects and monopolistic pricing power – they could remain elevated for the foreseeable future. Regional And Sector Equity Allocation The earnings yield is roughly two percentage points higher outside the U.S., suggesting that non-U.S. stocks will best their U.S. peers over the long haul. In the developed market space, Germany, Spain, and the U.K. appear especially cheap. In the EM realm, China, Korea, and Russia stand out as being very attractively priced (Chart 29). At the sector level, cyclical stocks look more appealing than defensives (Chart 30). Chart 29U.S. Stocks Appear Expensive Compared To Their Peers

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Chart 31Economic Growth Drives Stocks Over A 12-Month Horizon

Economic Growth Drives Stocks Over A 12-Month Horizon

Economic Growth Drives Stocks Over A 12-Month Horizon

Chart 30Cyclical Stocks Are More Attractive Than Defensives

Cyclical Stocks Are More Attractive Than Defensives

Cyclical Stocks Are More Attractive Than Defensives

Chart 32EM And Euro Area Equities Usually Outperform When Global Growth Improves

EM And Euro Area Equities Usually Outperform When Global Growth Improves

EM And Euro Area Equities Usually Outperform When Global Growth Improves

Valuations are useful mainly as a guide to long-term returns. Over a horizon of say, 12 months, cyclical factors – i.e., what happens to growth, interest rates, and exchange rates – matter more (Chart 31). Fortunately, our cyclical views generally line up with our valuation assessment. Stronger global growth, a weaker dollar, and rising commodity prices should benefit cyclical stocks relative to defensives. To the extent that EM and European stock markets have more of a cyclical sector skew than U.S. stocks, the former should end up outperforming (Chart 32). We would put financials on our list of sectors to upgrade by year end once global growth begins to reaccelerate. Falling bond yields have hurt bank profits (Chart 33). The drag on net interest margins should recede as yields start rising. European banks, which currently trade at only 7.6 times forward earnings, 0.6 times book value, and sport a hefty dividend yield of 6.3%, could fare particularly well (Chart 34). Chart 33AHigher Bond Yields And Steeper Yield Curves Will Benefit Financials (I)

Higher Bond Yields And Steeper Yield Curves Will Benefit Financials (I)

Higher Bond Yields And Steeper Yield Curves Will Benefit Financials (I)

Chart 33BHigher Bond Yields And Steeper Yield Curves Will Benefit Financials (II)

Higher Bond Yields And Steeper Yield Curves Will Benefit Financials (II)

Higher Bond Yields And Steeper Yield Curves Will Benefit Financials (II)

As Chart 35 illustrates, a bet on financials is similar to a bet on value stocks. Growth has trounced value over the past 12 years, but a bit of respite for value is in order over the next 12-to-18 months. Chart 34European Banks Are Attractive

European Banks Are Attractive

European Banks Are Attractive

Chart 35Is Value Turning The Corner?

Is Value Turning The Corner?

Is Value Turning The Corner?

Fixed Income Chart 36AYields Should Rise On Stronger Growth (I)

Yields Should Rise On Stronger Growth (I)

Yields Should Rise On Stronger Growth (I)

Dovish central banks and, for the time being, still-subdued inflation will help keep government bond yields in check over the next 12 months. Nevertheless, yields will still rise from currently depressed levels on the back of stronger global growth (Chart 36). Chart 36BYields Should Rise On Stronger Growth (II)

Yields Should Rise On Stronger Growth (II)

Yields Should Rise On Stronger Growth (II)

Bond yields tend to rise or fall depending on whether central banks adjust rates by more or less than is anticipated (Chart 37). Investors currently expect the Fed to cut rates by another 80 basis points over the next 12 months. While we think the Fed will bring down rates by 25 basis points on October 30th, we do not anticipate any further cuts beyond then. The cumulative 75 basis points in cuts during this easing cycle will be equivalent to the amount of easing delivered during the two mid-cycle slowdowns in the 1990s (1995/96 and 1998). All told, the U.S. 10-year Treasury yield is likely to move back into the low 2% range by the middle of 2020. Chart 37AStronger Economic Growth Will Put Upward Pressure On Government Bond Yields (I)

Stronger Economic Growth Will Put Upward Pressure On Government Bond Yields (I)

Stronger Economic Growth Will Put Upward Pressure On Government Bond Yields (I)

Chart 36BStronger Economic Growth Will Put Upward Pressure On Government Bond Yields (II)