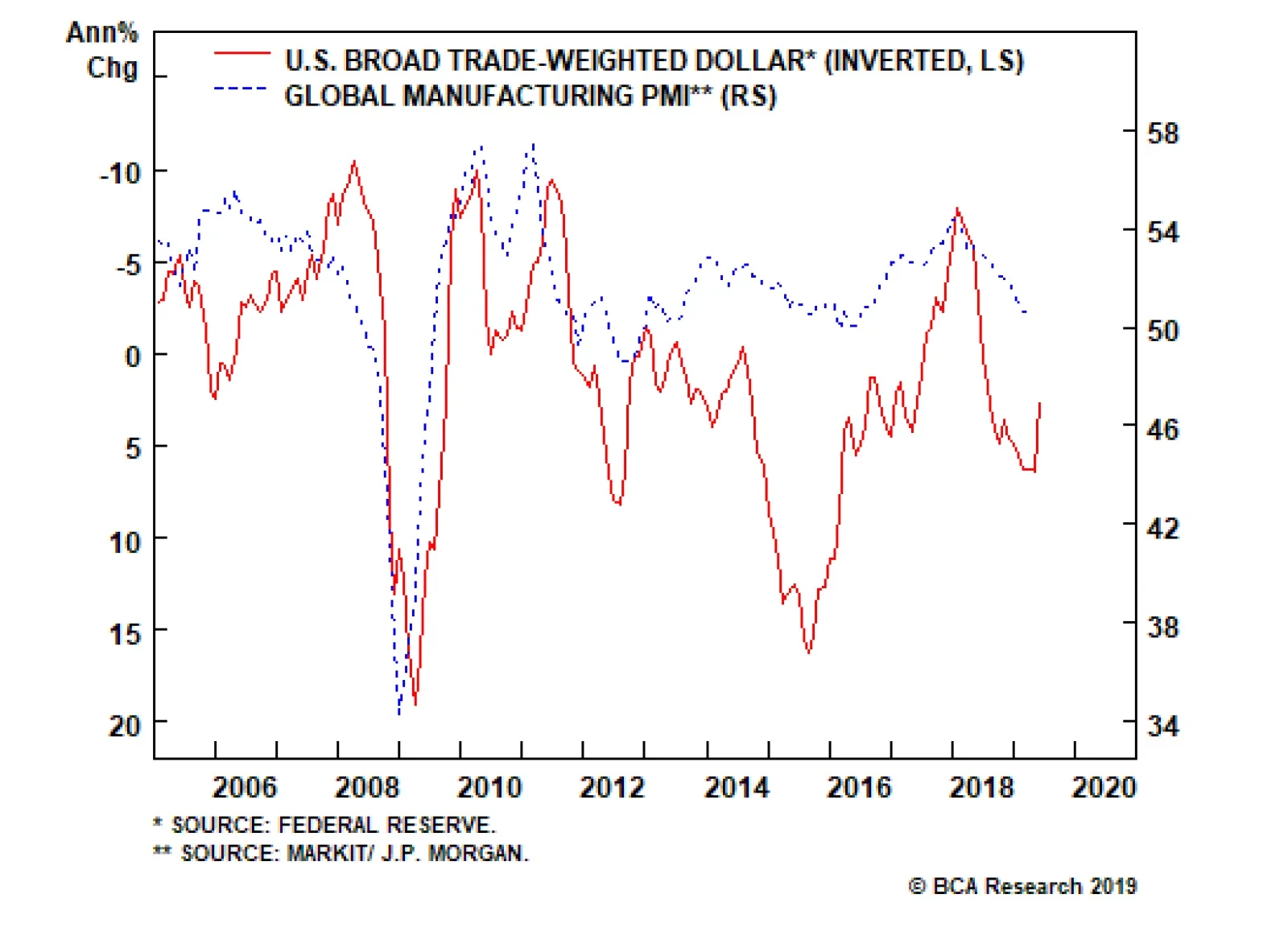

HighlightsU.S. inflation is on a structural uptrend. Monetary and fiscal policy, populism, and demographics will tend to push inflation higher over the coming decade.How can investors protect portfolios against inflation risk? We look at periods of rising inflation to determine which assets were the best inflation hedge.We find that the level of inflation is very important in determining which assets work best.When inflation is rising and high, or very high, the best inflation hedges at the asset class level are commodities and U.S. TIPS.When inflation is very high, gold is the best commodity to hold and defensive sectors will minimize losses in an equity portfolio.However, hedges have a cost. Allocating a large percentage of a portfolio to inflation hedges will be a drag on returns. Investors should opt for a low allocation to hedges now, and increase to a medium level when inflation rises further.FeatureSome 38 years have passed since the last time the U.S. suffered from double-digit inflation. The Federal Reserve reform of 1979, championed by Paul Volcker, changed the way the Fed approached monetary policy by putting a focus on controlling money growth.1 The reform gave way to almost four decades of relatively controlled inflation, which persists today.But times are changing. While most of today’s investors have never experienced anything other than periods of tame inflation, BCA expects that rising inflation will be a major driving force of asset returns over the coming decade.2 The main reasons behind this view are the following:A rethink in the monetary policy framework: At its most recent meeting, the FOMC openly discussed the idea of a price-level target, implying that it would be open to the economy running hot to compensate for the past 10 years of below-target inflation (Chart I-1A, top panel).Procyclical fiscal policy: The U.S. is conducting expansionary fiscal policy while the economy is at near-full employment (Chart I-1A, middle panel). The last time this happened in the U.S., during the 1960s, high inflation followed, as the fiscal boost made the economy run substantially above capacity.Waning Fed independence: President Trump has openly questioned the hiking campaign undertaken by the Fed. Moreover, he has tried to nominate Fed governors with dovish tendencies. Historically around the world, a lack of central bank independence has often led to higher inflation rates (Chart I-1A, bottom panel).Peak in globalization: Globalization accelerated significantly in the 1990s and 2000s, flooding the global economy with cheap labor (Chart I-1B, top panel). However, we believe that globalization has peaked. Instead, populism and protectionism will be the dominant paradigms for years to come, reducing the cheap pool of workers and goods previously available.Demographics: The population in the U.S. is set to age in coming years (Chart I-1B, middle panel). As the percentage of U.S. retirees increases, the number of spenders relative to savers will begin to rise (Chart I-1B, bottom panel). Higher spending and lower savings in the economy should create upward pressure on inflation. Chart I-1AStructural Forces Point To Higher Inflation In The Coming Decade (I)

Structural Forces Point To Higher Inflation In The Coming Decade (I)

Structural Forces Point To Higher Inflation In The Coming Decade (I)

Chart I-1BStructural Forces Point To Higher Inflation In The Coming Decade (II)

Structural Forces Point To Higher Inflation In The Coming Decade (II)

Structural Forces Point To Higher Inflation In The Coming Decade (II)

If our view is correct, how should investors allocate their money?We attempt to answer this question by evaluating the performance of five major asset classes during periods when inflation was rising. Furthermore, we look into sub-asset class performance to determine how investors should position themselves within each asset class to take advantage of an inflationary environment.In our asset-class analysis, we use a data sample starting in 1973 and we limit ourselves to five publicly traded assets that have adequate history: global equities, U.S. Treasuries, U.S. real estate (REITs), U.S. inflation-linked bonds,3 and commodities. We compare asset classes according to their Sharpe ratios: average annualized excess returns divided by annualized volatilities.4 BCA expects that rising inflation will be a major driving force of asset returns over the coming decade.In our sub-asset class analysis, we analyze global equity sectors, international vs U.S. equities, and individual commodities. In some of the sections in our sub-asset class analysis, our sample is slightly reduced due to lack of historical data. Moreover, since in some instances all sectors have negative returns, we compare sub-asset classes according to their excess returns only.We base our analysis on the U.S. Consumer Price Index, given that most of the assets in our sample are U.S. based. We opt for this measure because it tends to track the living expenses for most U.S. citizens and it is the preferred measure to index defined-benefit payments.Finally, we decompose the periods of rising inflation into four quartiles in order to examine whether the level of inflation has any impact on the performance of each asset. Chart I-2 and Table I-1 show the different ranges we use for our analysis as well as a description of the typical economic and monetary policy environments in each of them.

Chart I-2

Chart I-

Summary Of ResultsTable I-2 shows the summary of our results. For a detailed explanation on how each asset class and sub-asset class behaves as inflation rises, please see the Asset Class section and the Sub-Asset Class section below.

Chart I-

Which assets perform best when inflation is rising?Rising inflation affects assets very differently, and is especially dependent on how high inflation is.Global equities performed positively when inflation was rising and low or mild, but they were one of the worst-performing assets when inflation was rising and high or very high. Importantly, equities underperformed U.S. Treasuries in periods of both high and very high inflation.Commodities and U.S. TIPS were the best performers when inflation was high or very high.U.S. REITs were not a good inflation hedge.Which global equity sectors perform best when inflation is rising?Energy and materials outperformed when inflation was high.Every single sector had negative excess returns when inflation was very high, but defensive sectors such as utilities, healthcare, and telecommunications5 minimized losses.Which commodities perform best when inflation is rising?With the exception of energy, most commodities had subpar excess returns when inflation was in the first two quartiles.Industrial metals outperformed when inflation was high.Gold and silver outperformed when inflation was very high. Additionally, gold had consistent returns and low volatility.What is the cost of inflation hedging?To answer this question, we construct four portfolios with different levels of inflation hedging:Benchmark (no inflation hedging): 60% equities / 40% bonds.Low Inflation Hedging: 50% equities / 40% bonds / 5% TIPS / 5% commoditiesMedium Inflation Hedging: 40% equities / 30% bonds / 15% TIPS / 15 % commoditiesPure Inflation Hedging: 50% TIPS / 50% commodities. At the asset-class level, investors should allocate to commodities and U.S. TIPS to hedge inflation. Chart I-3Inflation Hedging Comes At A Cost

Inflation Hedging Comes At A Cost

Inflation Hedging Comes At A Cost

While increased inflation hedging provides better performance when inflation is high and rising, these hedges are costly to hold when inflation is at lower ranges or when it is falling (Chart I-3, panels 1 & 2). However, adding moderate inflation hedging (low or medium) to a portfolio achieved the right balance between cost and protection, and ultimately improved risk-adjusted returns over the whole sample (Chart I-3, panel 3).What about absolute returns? The benchmark outperformed over the whole sample. However, the low and medium inflation hedging did not lag far behind, while avoiding the big drawdowns of high inflation periods (Chart I-3, panel 4).Investment ImplicationsHigh inflation may return to the U.S. over the next decade. Therefore, inflation hedging should be a key consideration when constructing a portfolio. Based on our results, our recommendations are the following:1. At the asset-class level, investors should allocate to commodities and U.S. TIPS to hedge inflation.2. However, these hedges are costly to hold as they will create a drag on returns in periods when inflation is not high or very high. Therefore, a low allocation to inflation hedges is warranted now.3. Inflation will probably start to pick up in the 2020s. A medium allocation to inflation hedges will then be appropriate.4. When inflation is high (3.3%-4.9%), investors should overweight energy and materials in their equity portfolios. Likewise, they should overweight industrial metals and energy within a commodity portfolio.5. When inflation is very high (4.9% or more), investors should overweight defensive sectors in their equity portfolio to minimize losses. Moreover, investors should overweight gold within a commodity portfolio.Asset ClassesGlobal EquitiesThe relationship between equity returns and rising inflation depends on how high inflation is, with outstanding performance when inflation is rising but low or mild, and poor performance as it gets higher (Chart II-1, top panel).

Chart II-1

This relationship can be explained by the interaction between interest rates, inflation, earnings, and valuations:Earnings growth was usually slightly negative when inflation was recovering from low levels. However, given that interest rates were very low in this environment and growth expectations were high, multiple expansion boosted equity returns (Chart II-1, bottom panel).When inflation was mild, the Fed typically started to raise rates, resulting in a declining multiple. However, equities had the best performance in this range thanks to very high earnings growth – a result of the economy growing strongly due to a healthy level of inflation.When inflation climbed into the high or very high range, earnings growth was usually positive but beginning to slow, as high inflation weighed on growth. Meanwhile the multiple started to decline rapidly due to rising interest rates and declining growth expectations.With the exception of the mild inflation range, the return profile of equities during inflationary periods was similar to its normal profile: negative skew and excess kurtosis (Table II-1). However, the consistency of returns decreased at higher levels of inflation, with only 45% of months with positive returns when inflation was rising and in its highest quartile.

Chart II-

U.S. Treasuries

Chart II-2

U.S. Treasuries reacted in a similar fashion to equities when inflation was rising (Chart II-2). However, while Treasuries underperformed equities when inflation was low or mild, they actually outperformed equities when inflation was high or very high. This was in part due to the fact that at higher inflation ranges, U.S. Treasuries offer a higher coupon return when rates are high, at least partially counteracting losses from falling prices.The steady stream of cash flows from the coupons helped Treasuries achieve positive returns roughly two-thirds of the time at the highest levels of inflation (Table II-2). However, this consistency in returns came at a cost: very high inflation resulted in negative skew and high excess kurtosis. Therefore, while Treasuries provided frequent positive returns when inflation was very high, they were prone to violent selloffs.

Chart II-

U.S. REITs

Chart II-3

While REITs had high risk-adjusted returns when inflation was rising but mild, much like equities they had subpar performance in every other quartile and particularly poor performance when inflation was high or very high (Chart II-3). These results confirm our previous research showing that REITs performance is very similar to that of equities.6The return consistency for REITs was generally poor in inflationary periods, with the second-lowest percentage of positive return of any asset class (Table II-3). Moreover, REIT returns had excess kurtosis and negative skew throughout all inflation quartiles.

Chart II-

Commodity Futures

Chart II-4

Commodities performed positively in every quartile, and did particularly well when inflation was mild (Chart II-4, top panel). However, total return and price return were very different due to the behavior of the roll and collateral return:Total risk-adjusted returns were lower than spot risk-adjusted returns when inflation was low and rising. This happened because during these periods, commodity supply was high relative to demand, as the economy was recovering from a deflationary shock. Thus, there was an incentive for producers to conserve inventories, making the futures curve upward-sloping (contango). Thus, roll return was negative (Chart II-4, bottom panel).When inflation was in the upper two quartiles, total risk-adjusted returns were much higher than risk-adjusted spot returns. This was because high inflation was the product of supply shocks. These supply shocks resulted in a downward-sloping futures curve (backwardation), which, in turn, resulted in a positive roll return. Additionally, high rates during these regimes contributed to a high collateral return.Commodities provided good return consistency during inflationary periods, with roughly 60% of positive return months in the upper two inflation quartiles (Table II-4). The skew of returns was neutral or positive in the top two quartiles. This means that although volatility was high for commodities, extreme return movements were normally positive.

Chart II-

U.S. Inflation-Protected Bonds

Chart II-5

While inflation-protected bonds provided meager returns when inflation was rising but in the mild range, they provided excellent performance at the highest levels of inflation (Chart II-5). Moreover, this high Sharpe ratio was not just simply the result of low volatility, since U.S. TIPS had excess returns of 4.6% when inflation was high and 5.7% when inflation was very high.7The return profile of inflation-protected bonds during inflationary periods was also attractive in our testing period. Average skew was positive, while kurtosis was relatively low (Table II-5). The percentage of positive months across all quartiles was also the highest of all asset classes, with a particularly high share of positive returns in the periods of highest inflation.

Chart II-

Sub-Asset ClassesGlobal Equity Sectors

Chart III-1

For the sector analysis, we looked at information technology, financials, energy, materials, utilities, healthcare, and telecommunications. We excluded industrials, consumer discretionary, and consumer staples given that they do not have adequate back data.Once again, we separate rising inflation periods into four quartiles, arriving at the following results:When inflation was low, information technology had the best excess returns while utilities had the worst (Chart III-1, panel 1). This matches our observations at the asset class level, as IT is highly responsive to changes in the valuation multiple.When inflation was mild, energy had the best performance, followed by information technology (Chart III-1, panel 2). Meanwhile, financials had the worst performance, as rates were normally rising in these periods.When inflation was high, sectors highly correlated with commodity prices such as energy and materials outperformed. Meanwhile, IT was the worst performer (Chart III-1, panel 3).When inflation was very high, every sector had negative excess returns. Overall, investing in energy minimized losses (Chart III-1, panel 4). However, this performance was in part attributable to the oil spikes of the 1970s. Alternatively, defensive sectors such as utilities, telecommunications, and healthcare also minimized losses. International vs U.S. Equities

Chart III-2

How do equities outside of the U.S. behave when inflation is rising? While the high share of U.S. equities in the global index causes U.S. equities to be the main driver of global stock prices, is it possible to improve returns in inflationary environments by overweighting international equities?The answer once again depends on the level of inflation. When inflation was rising but low, U.S. stocks outperformed global ex-U.S. equities in both common currency and local currency terms (Chart III-2, panel 1). This was in part due to the inherent tech bias in U.S. stocks. Additionally, the low level of inflation was often accompanied by slowing global growth in our sample, helping the U.S. dollar.When inflation was mild, U.S. stocks once again outperformed international stocks in both local and common currency terms, though to a lesser degree (Chart III-2, panel 2). The dollar was roughly flat in this environmentU.S. stocks started to have negative excess returns when inflation was high (Chart III-2, panel 3). On the other hand international equities had positive excess returns in dollar terms, partly because of their energy and material bias and partly because the dollar was generally weak in this period.U.S. equities outperformed global ex-U.S. equities by a small margin when inflation was very high, given that defensive sectors such as telecommunication were over-represented in the U.S. index (Chart III-2, panel 4). The dollar was roughly flat in this period. Individual Commodities

Chart III-3

Our analysis above confirmed that commodities were one of the best assets to hold when inflation was rising. However, which commodity performed best?8Total return for every commodity was lower than spot return when inflation was low (Chart III-3, panel 1). This was due to the upward-sloping term structure of the futures curve (contango), resulting in a negative roll yield. In this range, energy had the best performance, followed by industrial metals. Precious metals had negative excess returns.When inflation was mild, energy had the best performance of any commodity by far (Chart III-3, panel 2). Precious and industrial metals had low but positive excess returns in this period.When inflation was high, industrial metals had the highest excess returns, followed by energy (Chart III-3, panel 3).We omit energy for the last quartile since there is not enough data available. Overall, when inflation was very high, both gold and silver had the highest excess returns (Chart III-3, panel 4). However, gold’s return volatility was much lower, while it also had positive returns 64% of the time compared to 52% for silver.Other AssetsU.S. Direct Real Estate Chart IV-1Direct Real Estate Is A Good Inflation Hedge

Direct Real Estate Is A Good Inflation Hedge

Direct Real Estate Is A Good Inflation Hedge

Our asset-class analysis confirmed that public real estate (REITs) as an asset class offered poor risk-adjusted returns during inflationary periods. But how did direct real estate perform?We analyzed direct real estate separately from all other assets because of a couple of issues:Our return dataset is available only on a quarterly basis, versus a monthly basis for the rest of the assets in our sample. Even when annualized, volatility is not directly comparable when using data with different frequencies.The NCREIF Real Estate Index that we used is a broad aggregate, which is not investable. Individual property prices might differ from this aggregate.Finally, real estate returns are measured on an appraisal basis. Appraisal-based indices are not reflective of real transactions. Moreover, prices tend to be sticky. To attenuate this issue we unsmoothed the capital returns by removing return autocorrelation.Overall, the Sharpe ratio of direct real estate was solid throughout the first three quartiles of rising inflation (Chart IV-1, top panel). There is not enough data available for the fourth quartile. However, judging by the performance of U.S. housing in the 1970s from OECD, risk-adjusted returns when inflation was very high was likely positive (Chart IV-1, bottom panel). Cash Chart IV-2Very High Inflation Erodes The Value Of Cash

Very High Inflation Erodes The Value Of Cash

Very High Inflation Erodes The Value Of Cash

Cash (investing in a 3-month U.S. Treasury bill) outperformed inflation over our sample. (Chart IV-2, top panel). Moreover, cash provided positive real returns when inflation was mild, or high, or when it was decreasing (Chart IV-2, bottom panel). However, cash was not a good inflation hedge at the highest inflation quartile, with an average annualized real loss of almost 2%. Juan Manuel Correa OssaSenior Analystjuanc@bcaresearch.com Footnotes1 Please see Carl E. Walsh, “October 6, 1979,” FRSBF Economic Letter, 2004:35, (December 3, 2004).2 Please see Global Investment Strategy Special Report, “1970s-Style Inflation: Could it Happen Again? (Part 1), ” dated August 10, 2018, available at gis.bcaresearch.com and Global Investment Strategy Special Report, “1970s-Style Inflation: Could it Happen Again? (Part 2),” dated August 24, 2018, available at gis.bcaresearch.com.3 We use a synthetic TIPS series for data prior to 1997. For details on the methodology, please see: Kothari, S.P. and Shanken, Jay A., “Asset Allocation with Inflation-Protected Bonds,” Financial Analysts Journal, Vol. 60, No. 1, pp. 54-70, January/February 2004. Jay A., “Asset Allocation with Inflation-Protected Bonds,” Financial Analysts Journal, Vol. 60, No. 1, pp. 54-70, January/February 2004.4 Excess returns are defined as asset return relative to a 3-month Treasury bill.5 Sector classification does not take into account GICS changes prior to December 2018. 6 Please see Global Asset Allocation Strategy Special Report "REITS Vs Direct: How To Get Exposure To Real Estate," dated September 15, 2016, available at gaa.bcaresearch.com.7 It is important to note that the synthetic TIPS series does not completely match actual TIPS series for the periods where they overlap. Specifically, volatility is significantly higher in the synthetic series. Thus, results should be taken as approximations.8 We decompose the returns into the same 4 quartiles to answer this question. However, due to lower data availability, we start our sample in 1978 instead of 1973. Moreover, our sample for energy is smaller beginning in 1983. This mainly reduces the amount of data available at the upper quartile.