Fixed Income

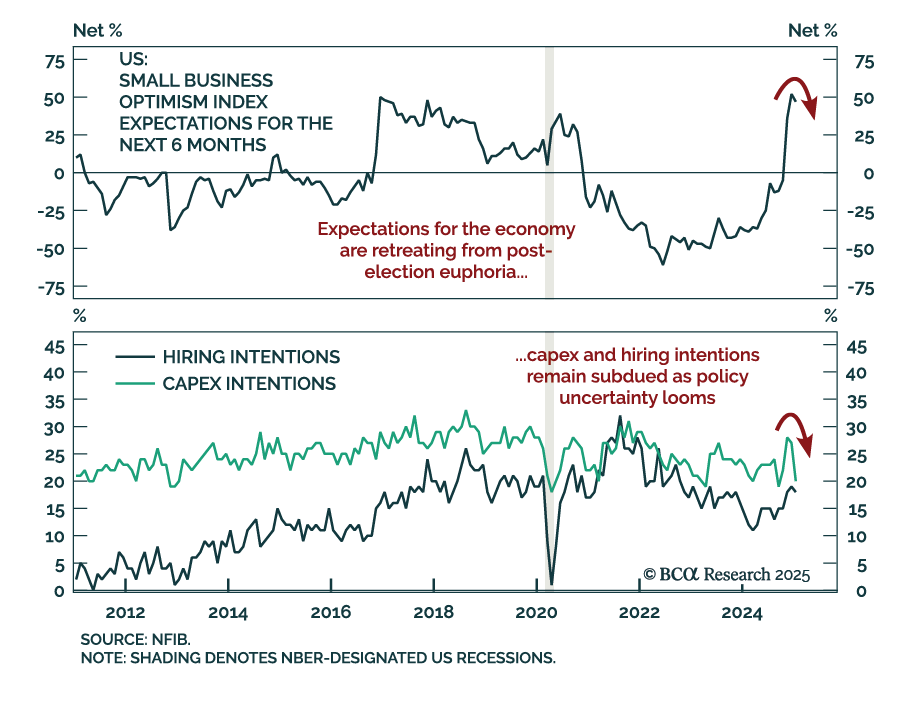

The January NFIB Small Business Optimism Index decreased more than expected to 102.8 from 105.1. After reaching near all-time highs in the wake of the election, expectations pulled back somewhat as uncertainty took center stage. The decline was…

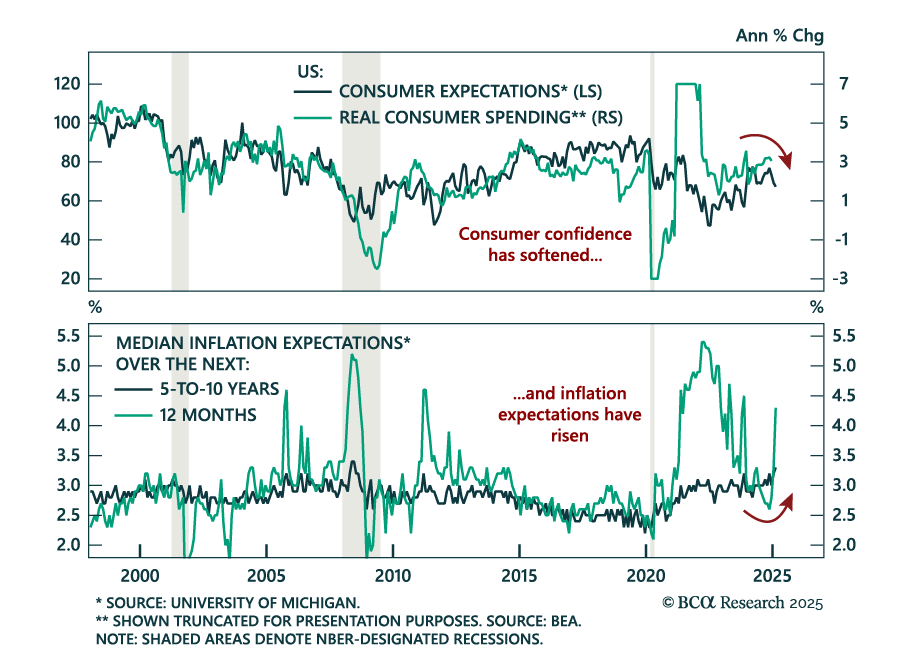

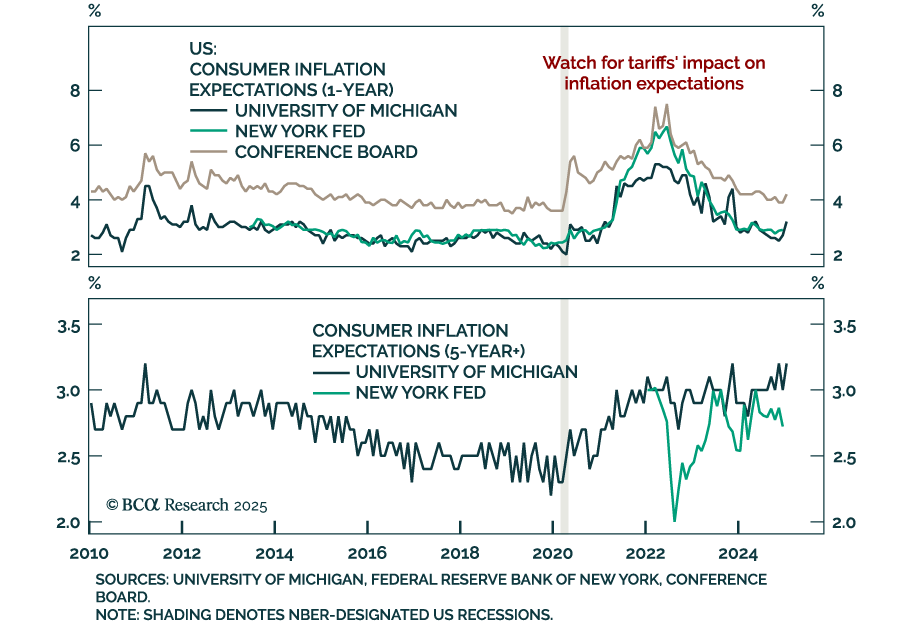

The preliminary February University of Michigan Consumer Sentiment Index missed estimates, falling to 67.8 from 71.1 in January. The decrease came from both expectations and the assessment of current conditions. Measures of 1-year and 5-10 year inflation…

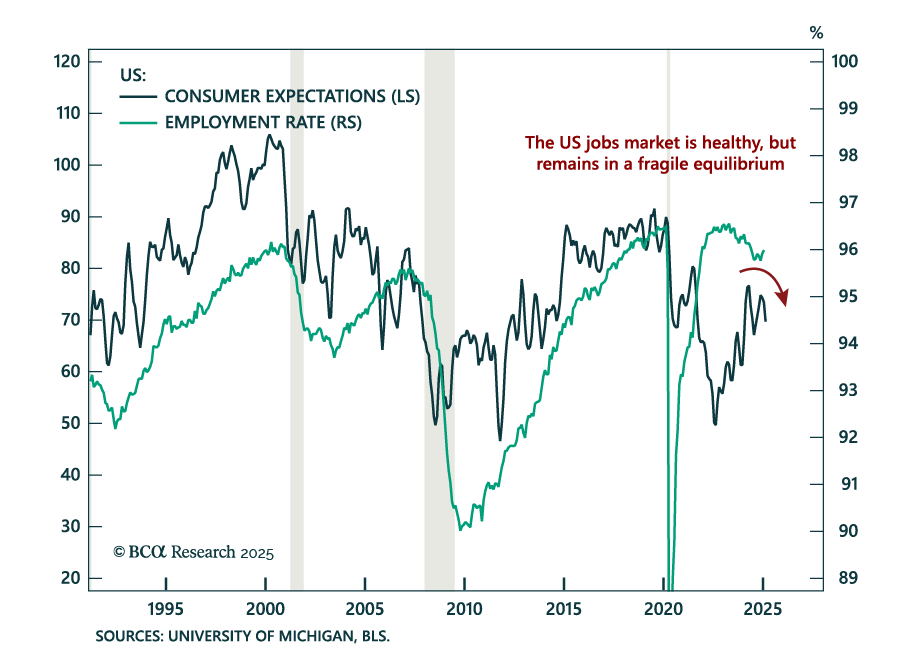

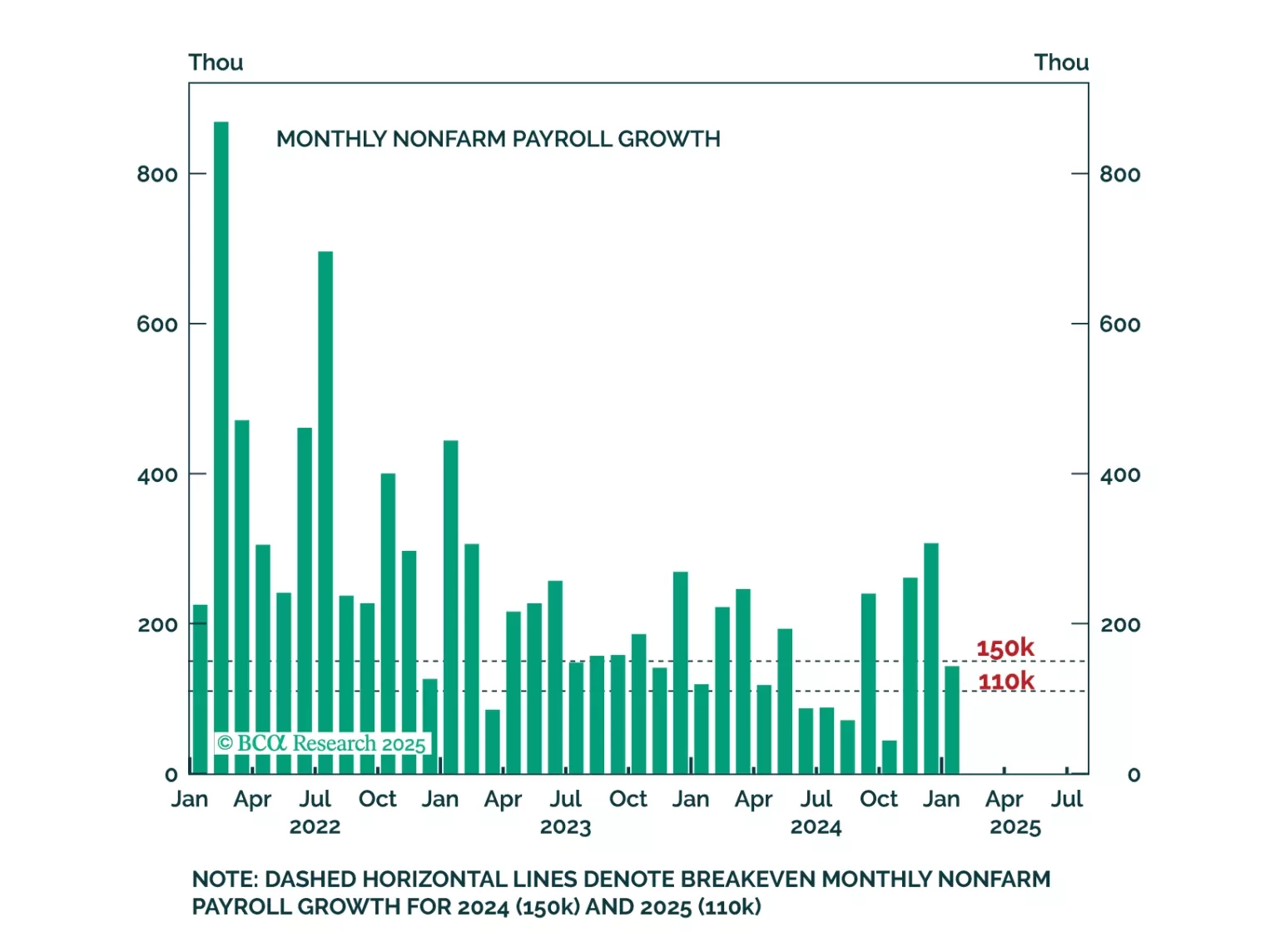

The January US jobs report was solid, reflecting a healthy labor market. Payrolls rose by less than expected at 143k, down from an upwardly-revised 307k in December, leaving the 3-month moving average at 237k. The unemployment rate ticked down 0.1% to 4.0%…

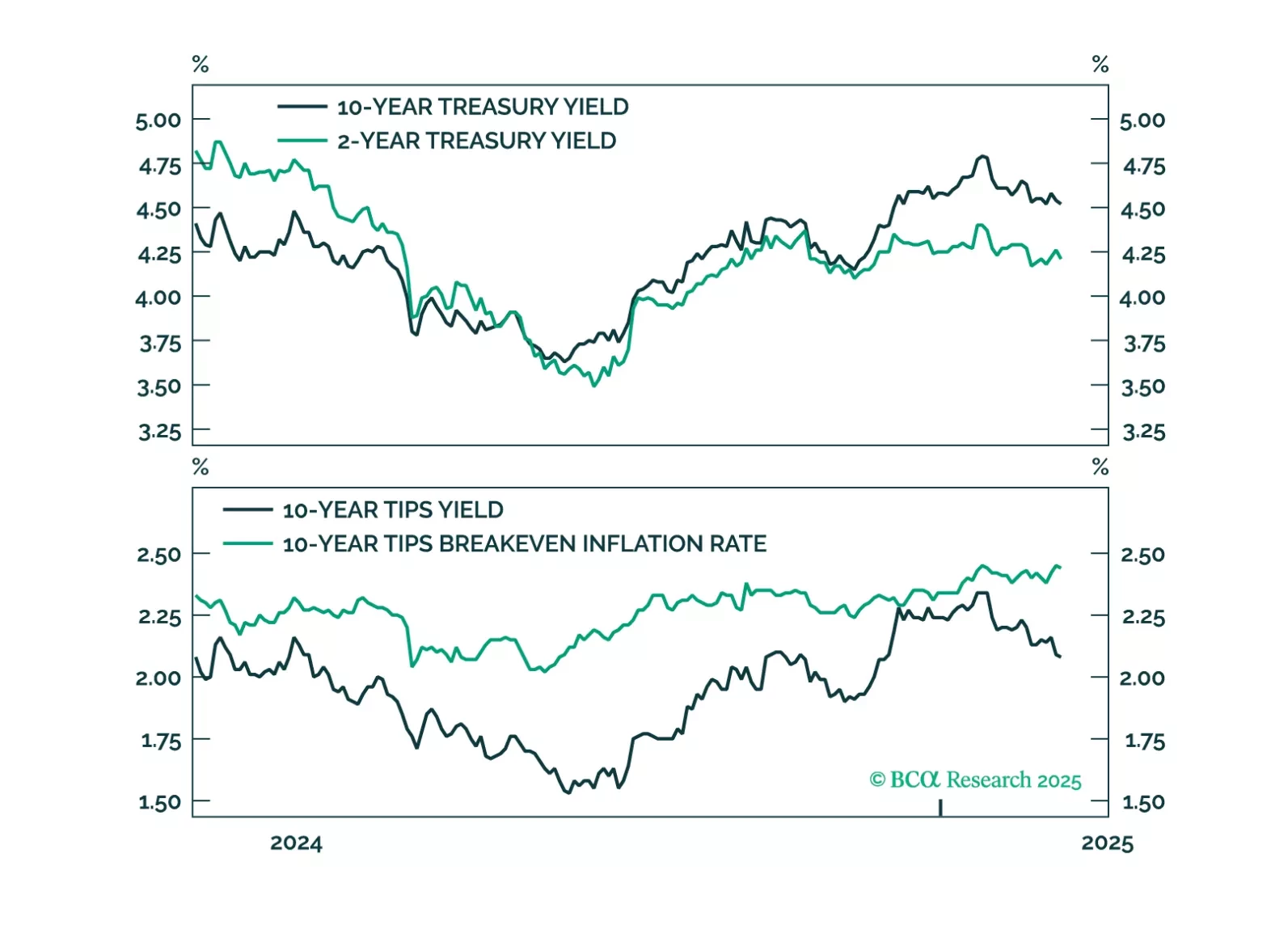

Some thoughts on this morning's employment data and Treasury Secretary Bessent's recent attempts to talk down the 10-year Treasury yield.

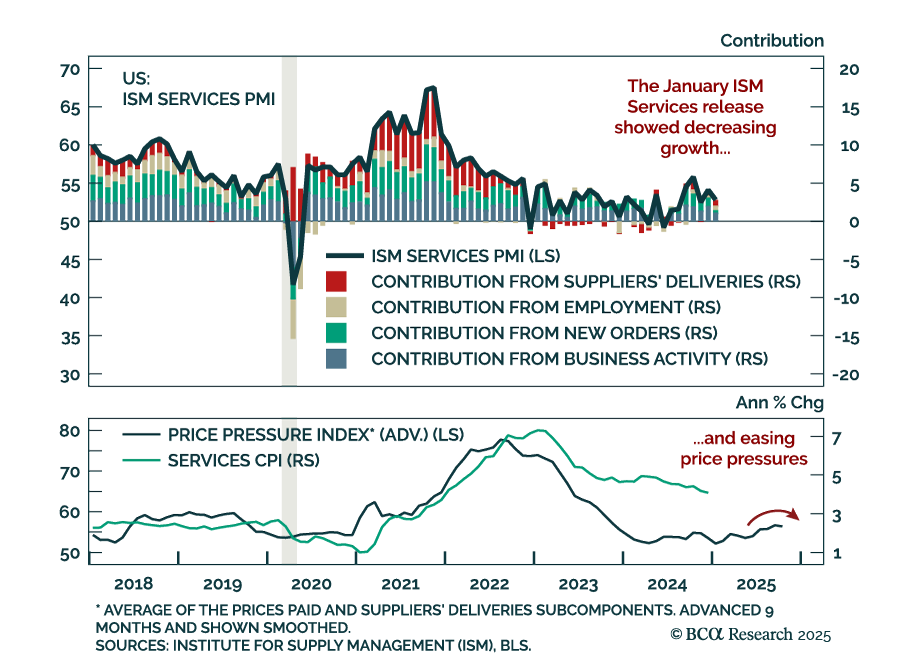

The January ISM Services missed estimates, decreasing to 52.8 from 54.0 in December. The move was driven by activity components, while employment and suppliers’ delivery times increased. Additionally, the prices paid measure decreased, reversing the…

Our Portfolio Allocation Summary for January 2025.

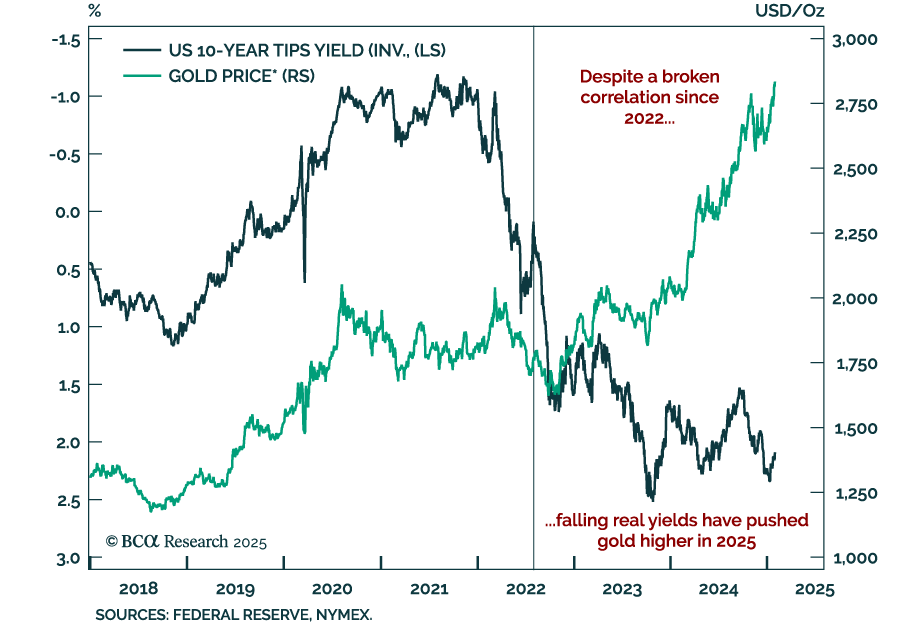

While the US dollar has outperformed every single DM currency in the past few months, the only monetary asset it did not outperform is gold. The greenback is up between 5-10% against DM currencies since September of last year, but down by more than 8% vs.…

Trade tensions muddy the outlook for global central banks. The 2010s were an era of low growth and low inflation that called for easy monetary policy. The post-COVID era has been marked by overheating and high inflation calling for tight policy. The second…

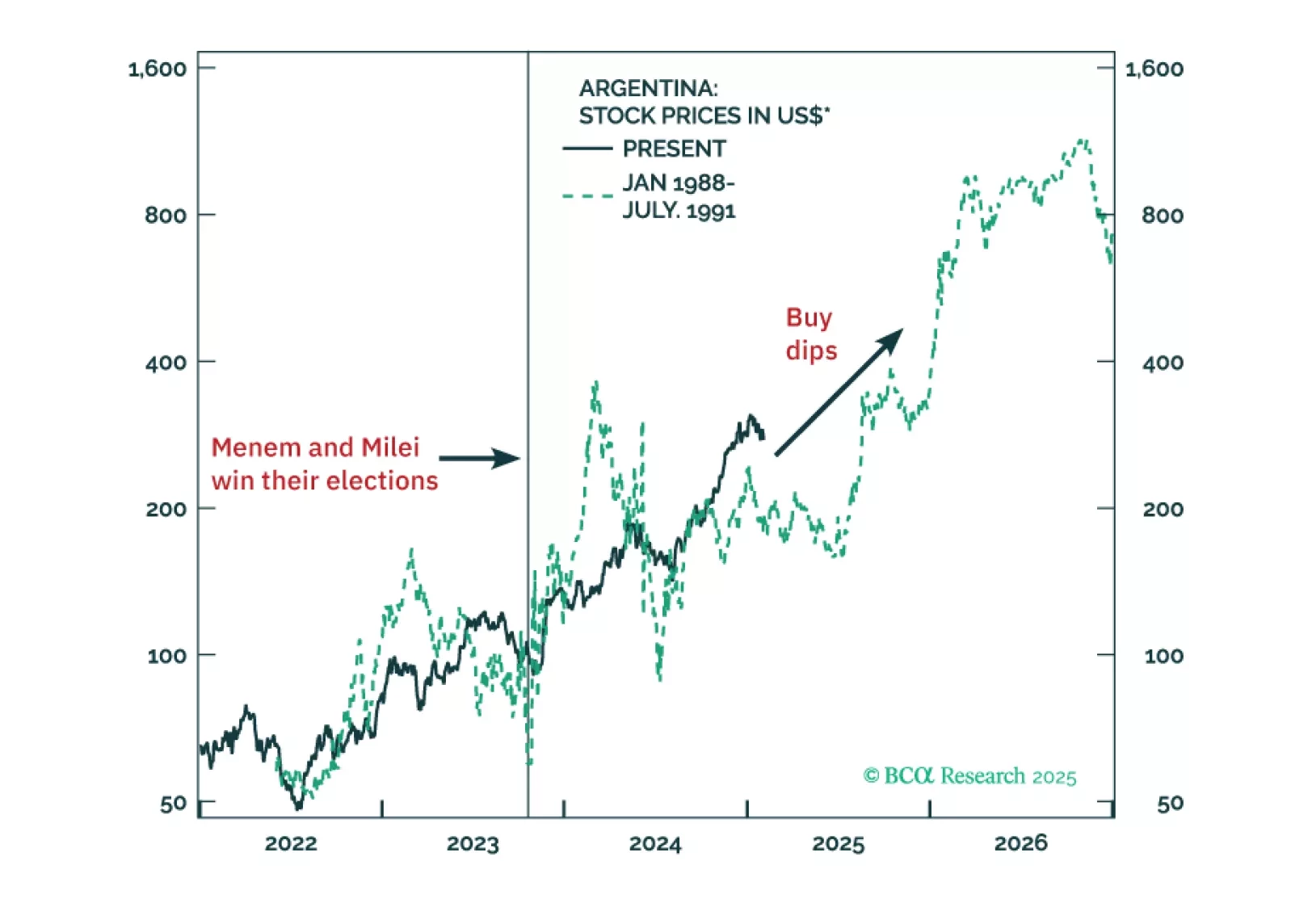

Argentina is entering a regime shift from the traditional short boom-bust cycles of the past 50 years. Profound structural reforms will result in a productivity boom, leading to a more durable economic expansion while keeping with the disinflation trend. Authorities will likely lift capital and currency controls in the second quarter of this year. All in all, odds are that Argentinian assets have entered a multi-year bull market.

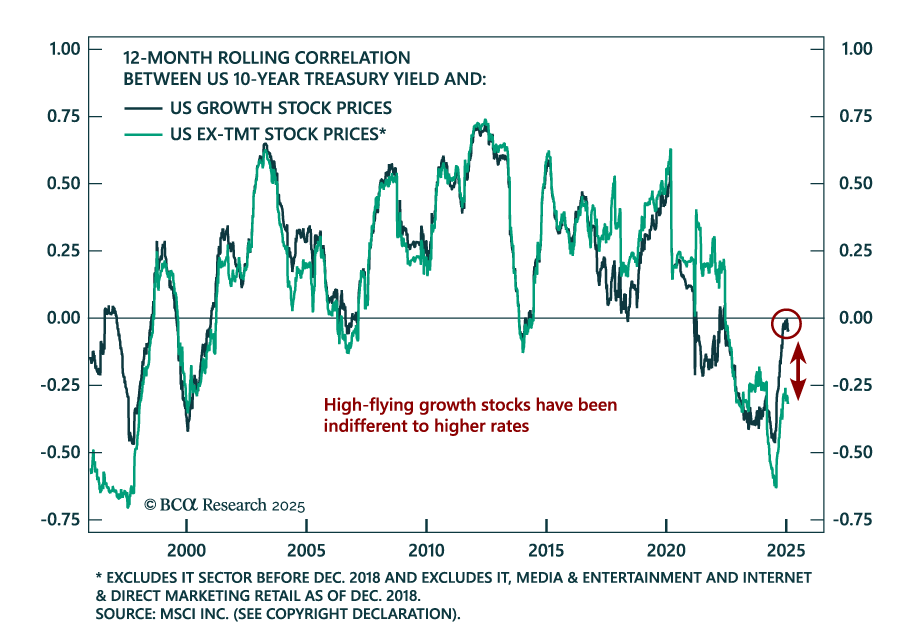

Our Chart Of The Week comes from Arthur Budaghyan, Chief Strategist of our Emerging Markets and China Investment Strategy services. Arthur highlights an important dichotomy in the US stock-bond yield correlation. In the past 12 months, US growth stocks…