Fixed Income

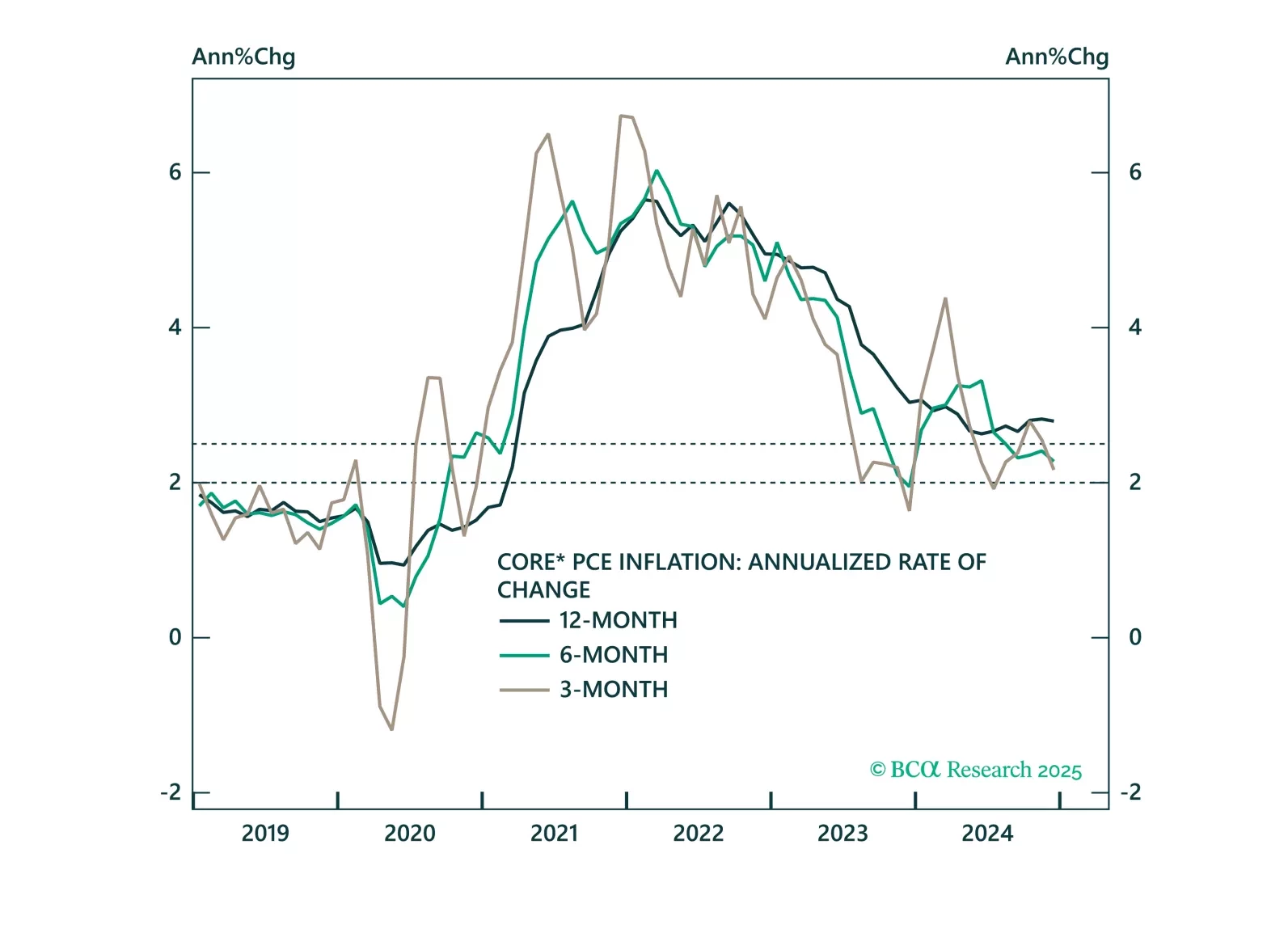

Core PCE inflation came in soft this morning and is tracking well below the Fed’s 2025 forecast. We highlight three upside risks to inflation and preview next week’s employment report.

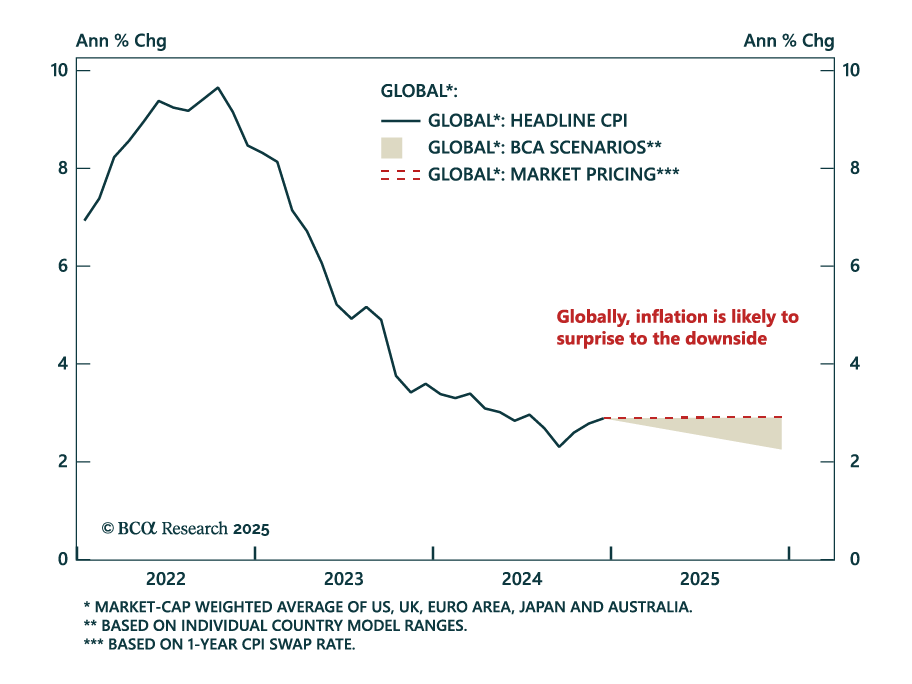

Our Global Fixed Income strategists assessed the risk of a second wave of inflation, and discussed the opportunities within the inflation-linked bond (ILB) market. Global disinflation remains on track, though energy prices and tariffs pose upside risks.…

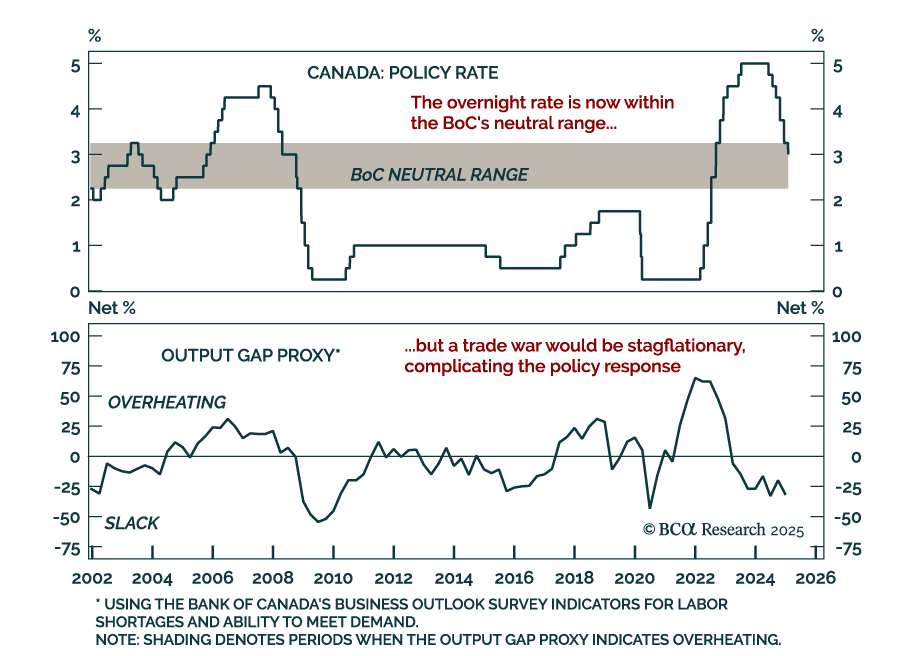

The Bank of Canada cut by 25 bps to 3% as expected, and announced the end of quantitative tightening. This sixth consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC assessed…

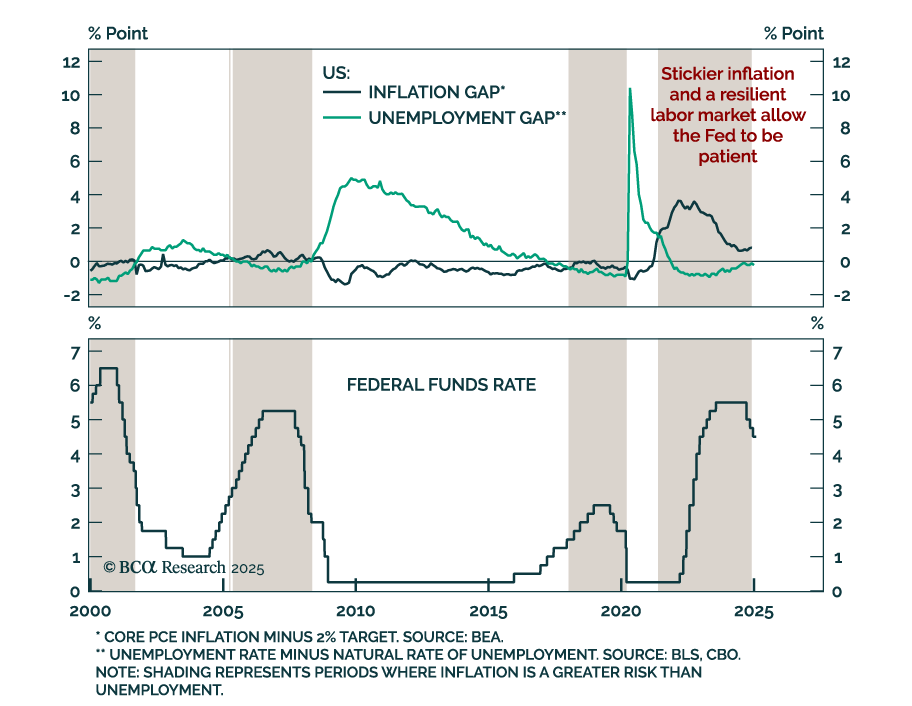

The Federal Reserve kept rates on hold in its 4.25%-to-4.5% range, as expected. The main change in the statement was the removal of the reference to progress towards the Fed’s 2% target, leaving instead a simple mention that inflation “remains somewhat…

Jay Powell didn’t say much at this afternoon’s FOMC press conference, and monetary policy will continue to take a back seat to fiscal for the next few months.

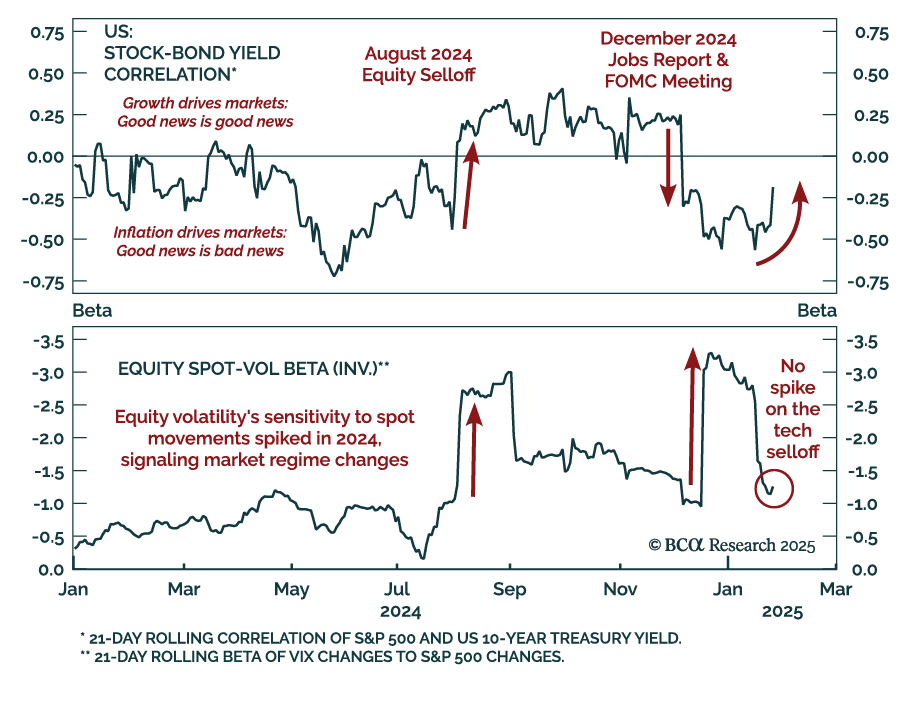

Monday’s selloff was orderly and concentrated in the tech sector. The price action was a classic risk-off response, where both stock prices and bond yields decreased. While the VIX increased, the equity spot-vol beta, volatility’s sensitivity to spot price…

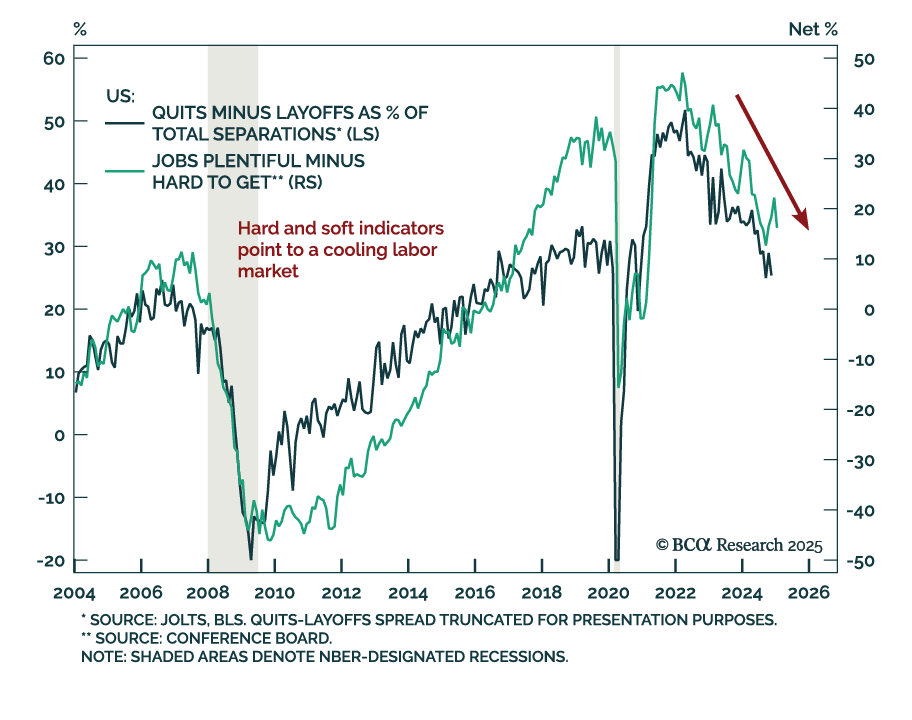

The January Conference Board Consumer Confidence index missed estimates, decreasing to 104.1 from an upwardly-revised 109.5 in December. The decrease was driven by both the present situation and expectations subcomponents. The labor differential, the…

Despite the choppy price action of the last few weeks, equity sentiment remains elevated. Surveys of investor sentiment remain at the top end of the bullish spectrum, and the S&P 500 is trading over 22x forward earnings, levels only seen in the…

The January ZEW index for Germany missed estimates, with expectations falling to 10.3 from 15.7 in December. However, the euro area level index ticked up to 18 from 17 a month prior. Measures of current conditions also rose. The lack of momentum for…

Our Emerging Markets strategists put together a hypothetical conversation between President Trump and Treasury Secretary nominee Scott Bessent on what economic policy would look like for the Trump 2.0 administration. Secretary Bessent is expected…