Fixed Income

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

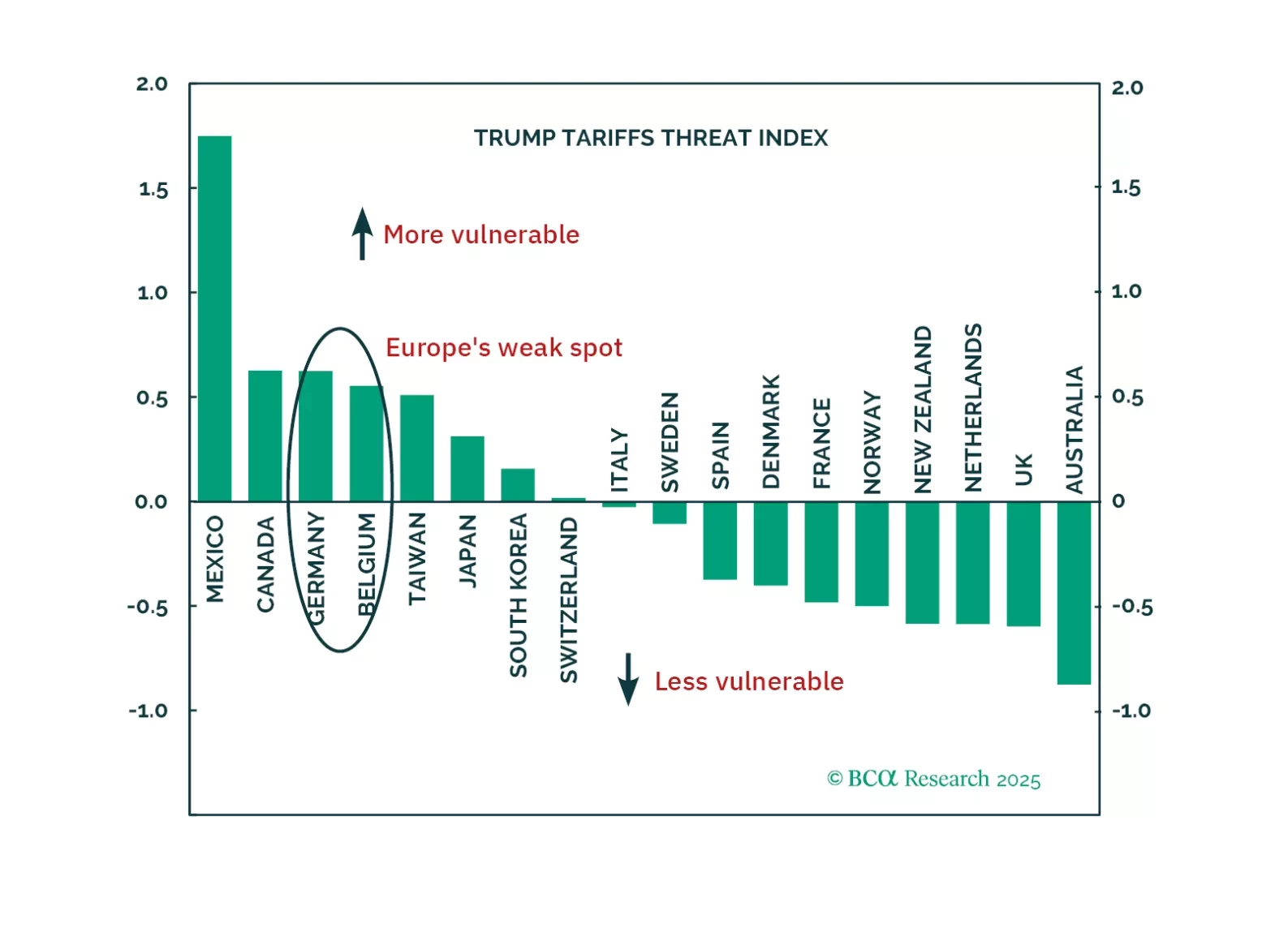

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

Today, we publish our Quarterly Model Bond Portfolio report. We review the performance of the portfolio in 2024 and discuss how to best position a global fixed income portfolio following the sharp rise in yields during the last months.