Fixed Income

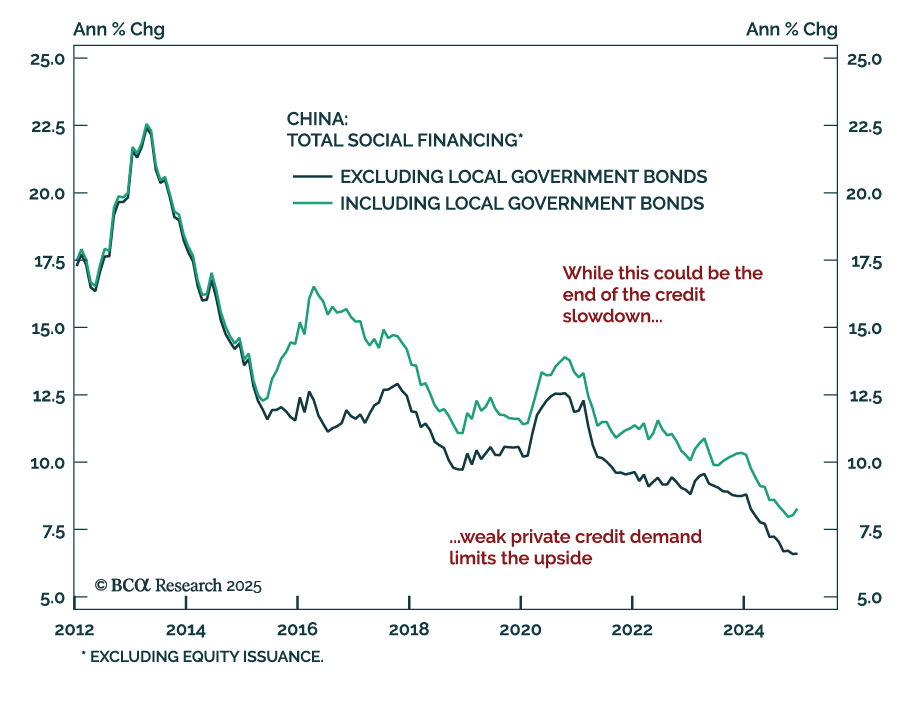

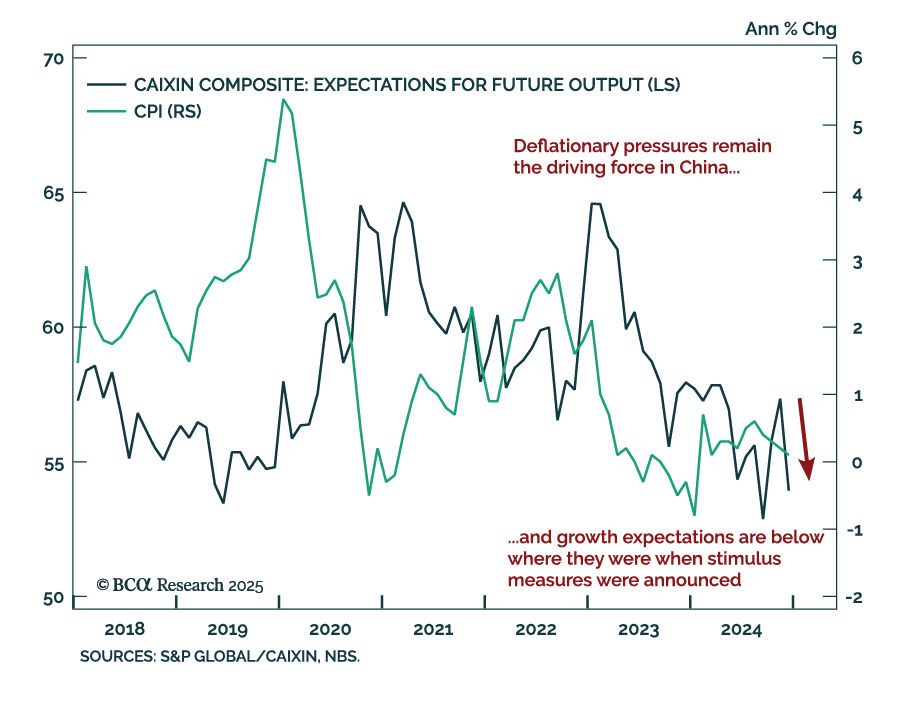

China’s monetary and credit data was relatively strong. New yuan loans increased more than expected, as did aggregate financing. M2 met estimates at 7.3% y/y. As was the case for trade in December, seasonality plays a big role in China around the…

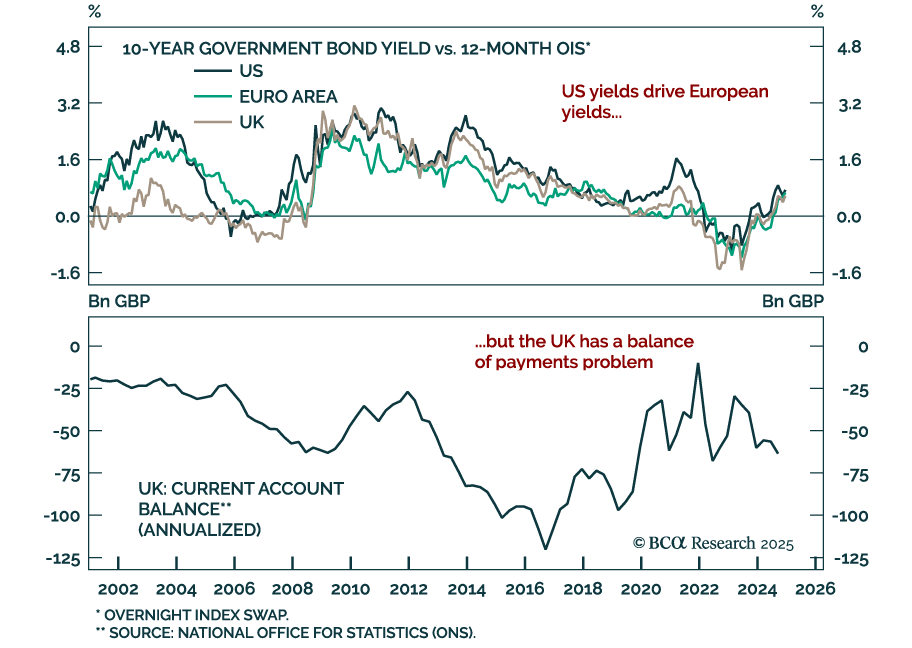

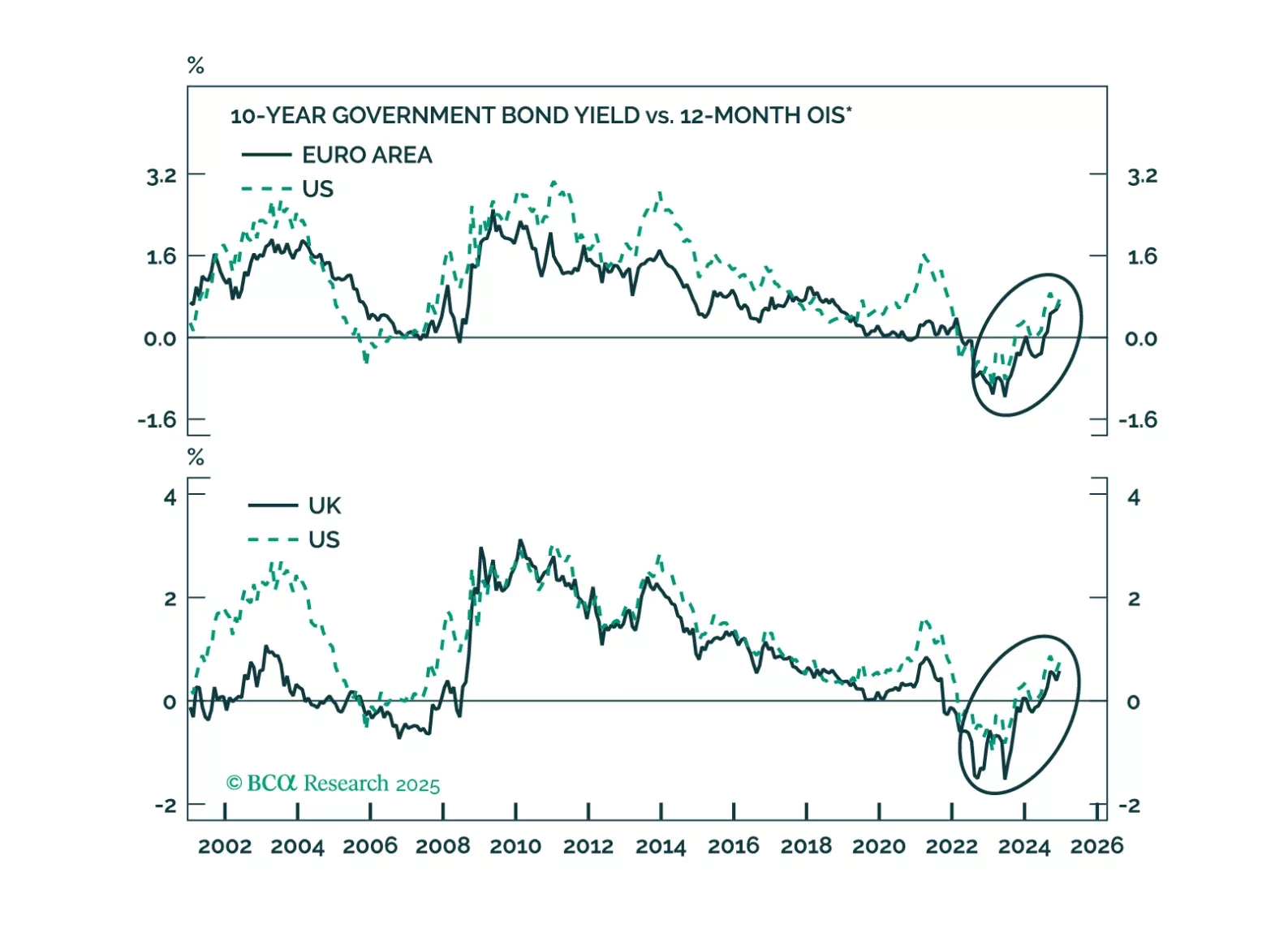

Our European Investment strategists looked at the developed markets bond selloff from a European perspective, focusing on Euro area and UK government bonds and currencies. The recent selloff in European bonds is driven primarily by surging US yields,…

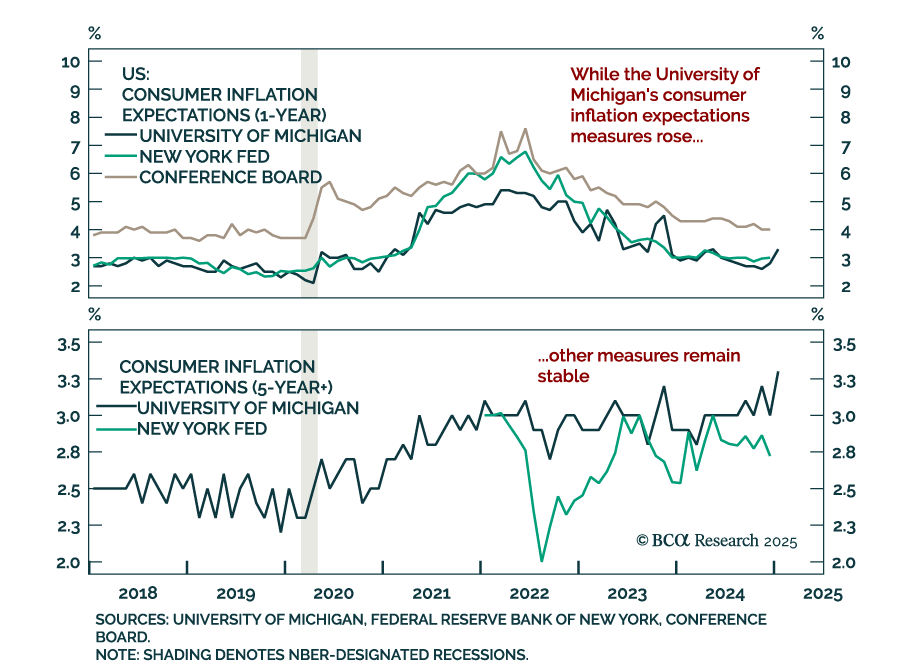

The preliminary January University of Michigan Consumer Sentiment Index missed estimates on Friday, driven by a cooling of consumer expectations. Worryingly, both the 1-year and 5-to-10 year inflation expectations ticked up to 3.3% from 2.8% and 3.0%,…

China’s December trade data was positive, with exports in USD terms rebounding to 10.7% y/y from 6.7% in November, and imports rebounding to 1.0% from -3.9%. Taken at face value, the numbers are positive for both the Chinese and global economies. However, our…

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

Thoughts on the increase in bond yields and this morning’s employment data.

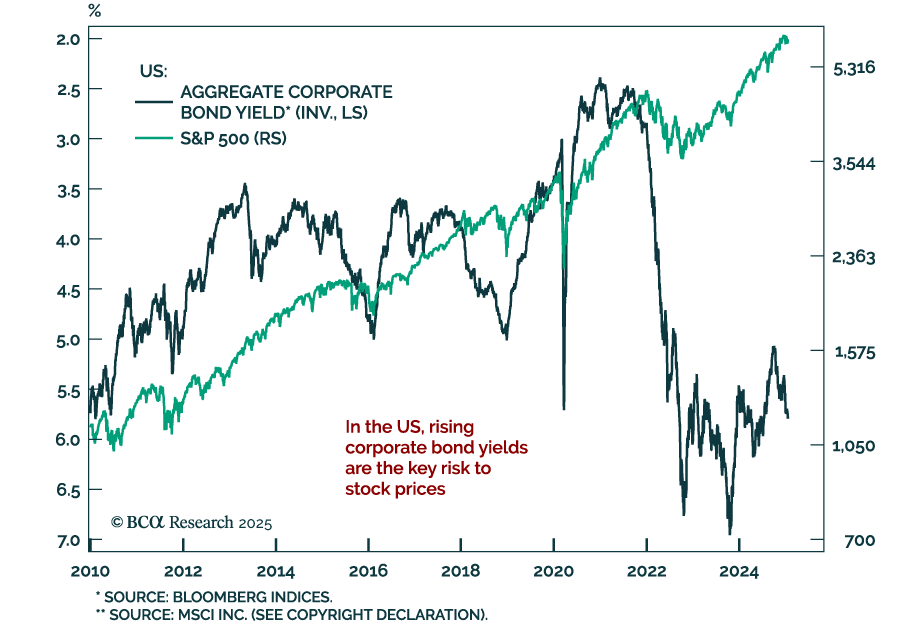

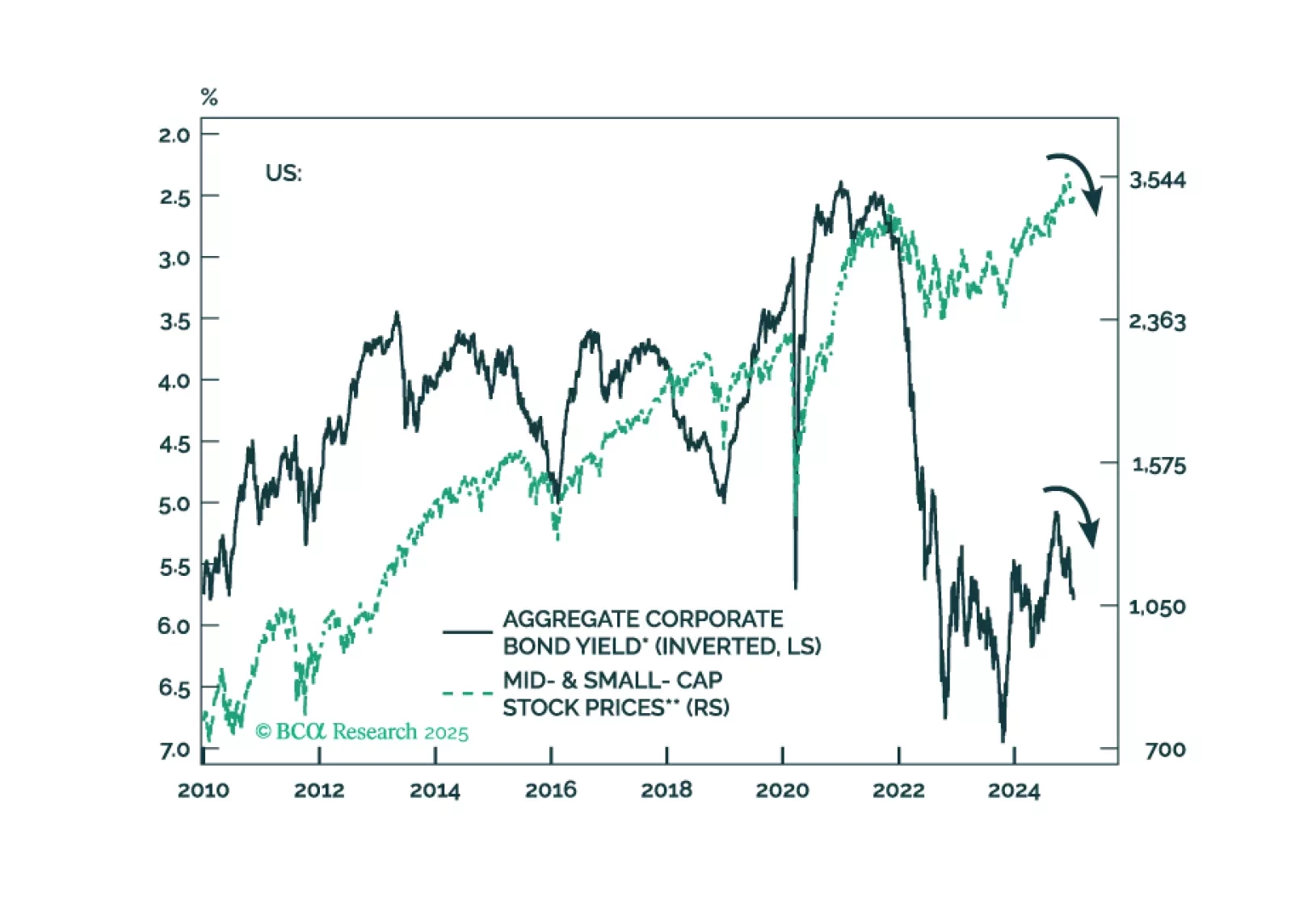

Our Chart Of The Week comes from Arthur Budaghyan, Chief Strategist for our Emerging Markets Strategy service. Arthur discusses the relationship between corporate bond yields and stock prices. Historically, US stocks suffer when US corporate bond yields…

Chinese December CPI and PPI releases show deflationary pressures are not abating. CPI slowed to a 0.1% y/y pace from 0.2% in November, while producer prices fell 2.3%. The Chinese economy has not meaningfully changed course since Beijing unveiled…

US bond yields will move higher, unleashing a storm in global financial markets. In the US, rising corporate bond yields will produce a selloff in share prices. In Mainstream EM, rising domestic and USD bond yields will weigh on share prices.

November factory orders in Germany widely missed estimates, falling by 5.4% m/m, worsening the 1.5% October decline. Excluding major orders, which often distort the overall picture, core new orders fell 1.7% y/y after growing 5.7% in October. The European…