Fixed Income

We recently pointed to the UK Budget announcement as a pivotal event for UK assets. Following an initially positive reception, the market has turned and priced in further fiscal premia in UK assets, with both gilts and the pound selling off. While the…

The Fed’s preferred measure of inflation, core PCE, met expectations of a reacceleration to 0.3% month-on-month, and reached 2.7% year-over-year. The rest of the Personal Income and Outlays report showed solid consumption growth, although supported by a…

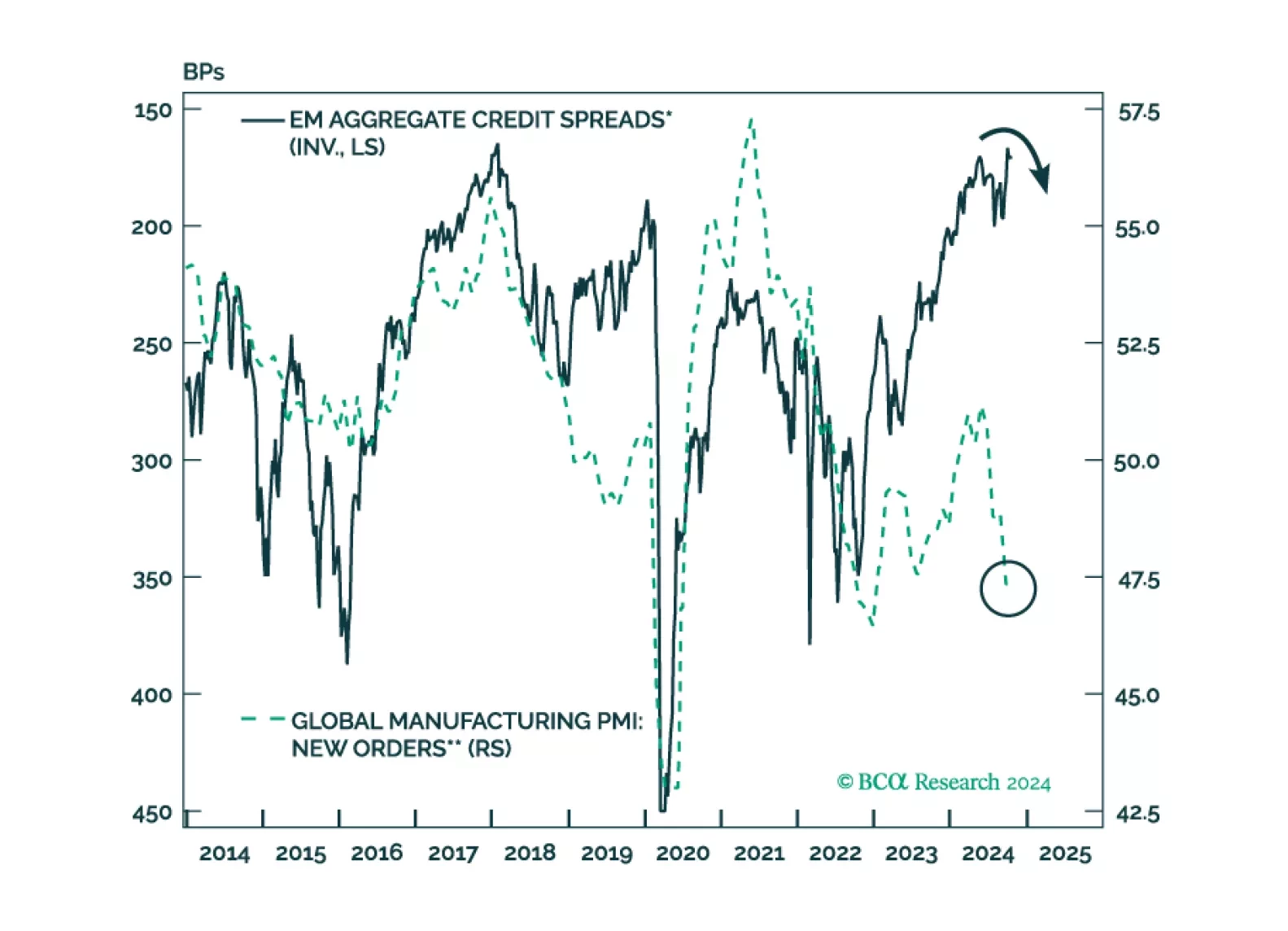

EM credit markets have recently defied the selloffs in EM equities, currencies, local currency bonds, and commodity prices. Such a decoupling is unusual. Resilient US growth and Fed easing are not sufficient to justify very low EM credit spreads.

Advanced Q3 GDP for the US met expectations, showing 2.8% quarterly annualized growth and a small deceleration from 3.0% in Q2. Importantly, growth remains above trend. The report was strong across the board except for housing. It also highlights that US…

Flash Q3 GDP estimates for the Euro Area beat expectations, accelerating to 0.4% quarterly growth from 0.2% last quarter. The momentum was spread across major countries, except for Italy. Meanwhile, the European Commission’s Economic Sentiment Index for…

As US consumers remain one of the few engines of global growth, our US Investment Strategy colleagues took a deep dive on consumer trends, augmented with comments from US banks’ earnings calls. Middle-aged consumers have fallen behind the young and old.…

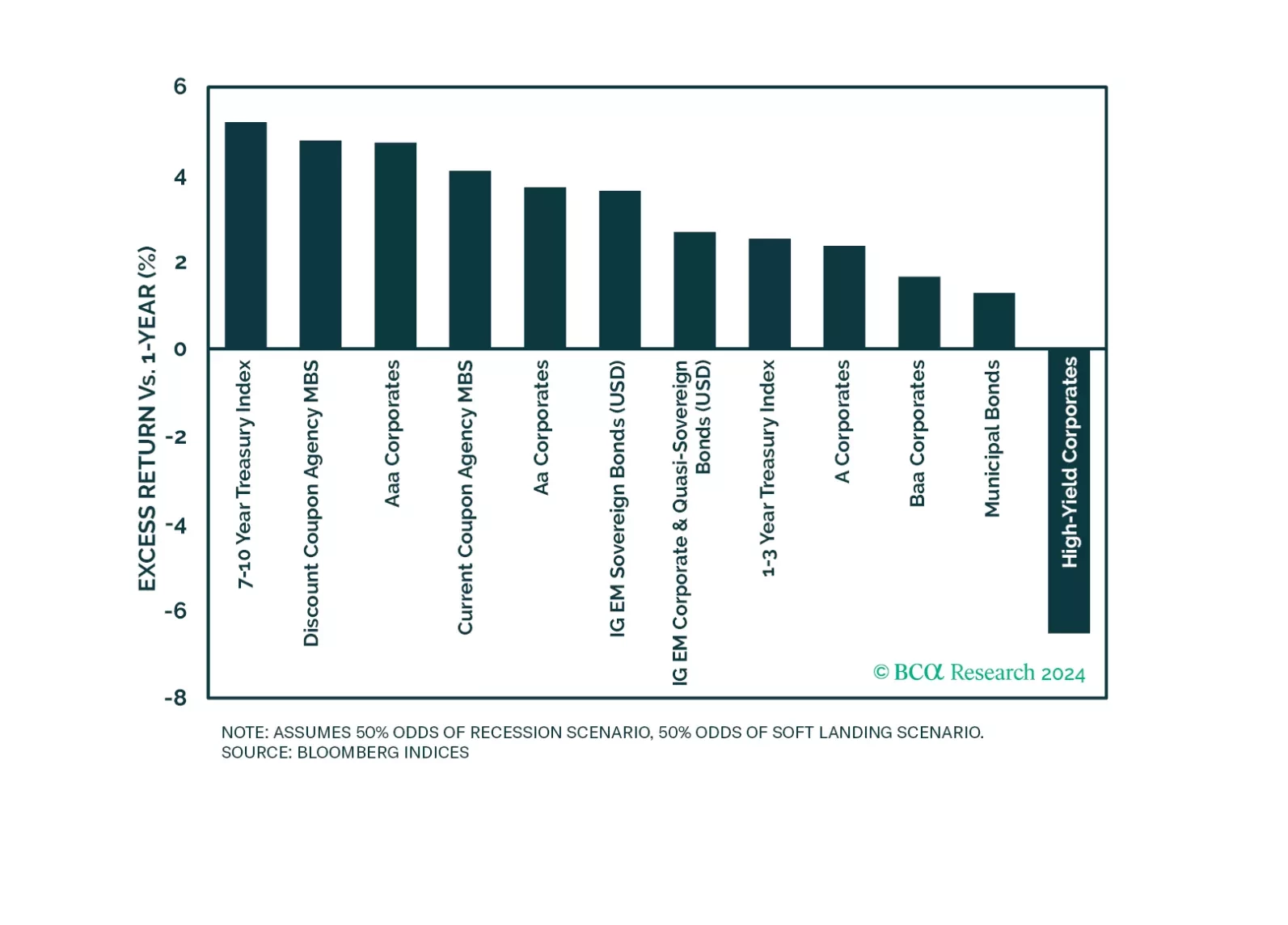

We update our 12-month return projections for different US fixed income sectors in soft-landing and recession scenarios.

For the past two weeks, oil has sold off amid a global spike in yields. Oil prices and Treasury yields tend to be positively correlated, as oil prices are a fast-moving component of inflation, driving the inflation expectations component of bond yields. …

While moving in the right direction, China’s latest stimulus measures are falling short of the mark to reflate the economy. The latest rumors extend this trend. News agencies reported discussions of a CNY 10 trillion bond issuance over three years. Six…

Job openings missed expectations at 7.44 million in September, a mild slowdown from August. The details of the JOLTS report were also negative, except for hirings which continue their June rebound. Meanwhile, consumer confidence for October data beat…