Fixed Income

The global risk-off phase will persist. It is too early to buy local-currency bonds in Mainstream EM, but it is not too late to sell EM sovereign and corporate credit (USD bonds).

Our Portfolio Allocation Summary for April 2026.

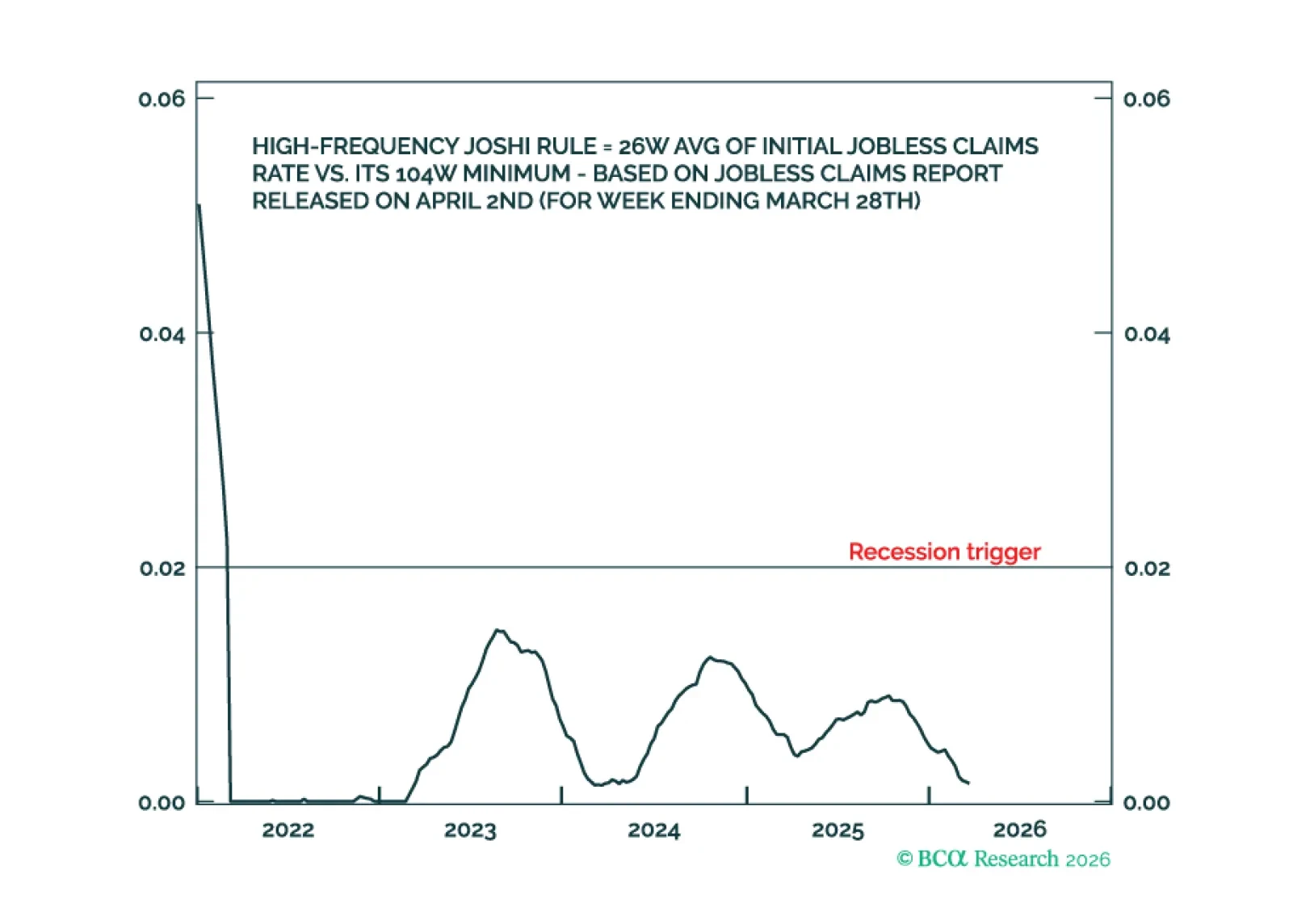

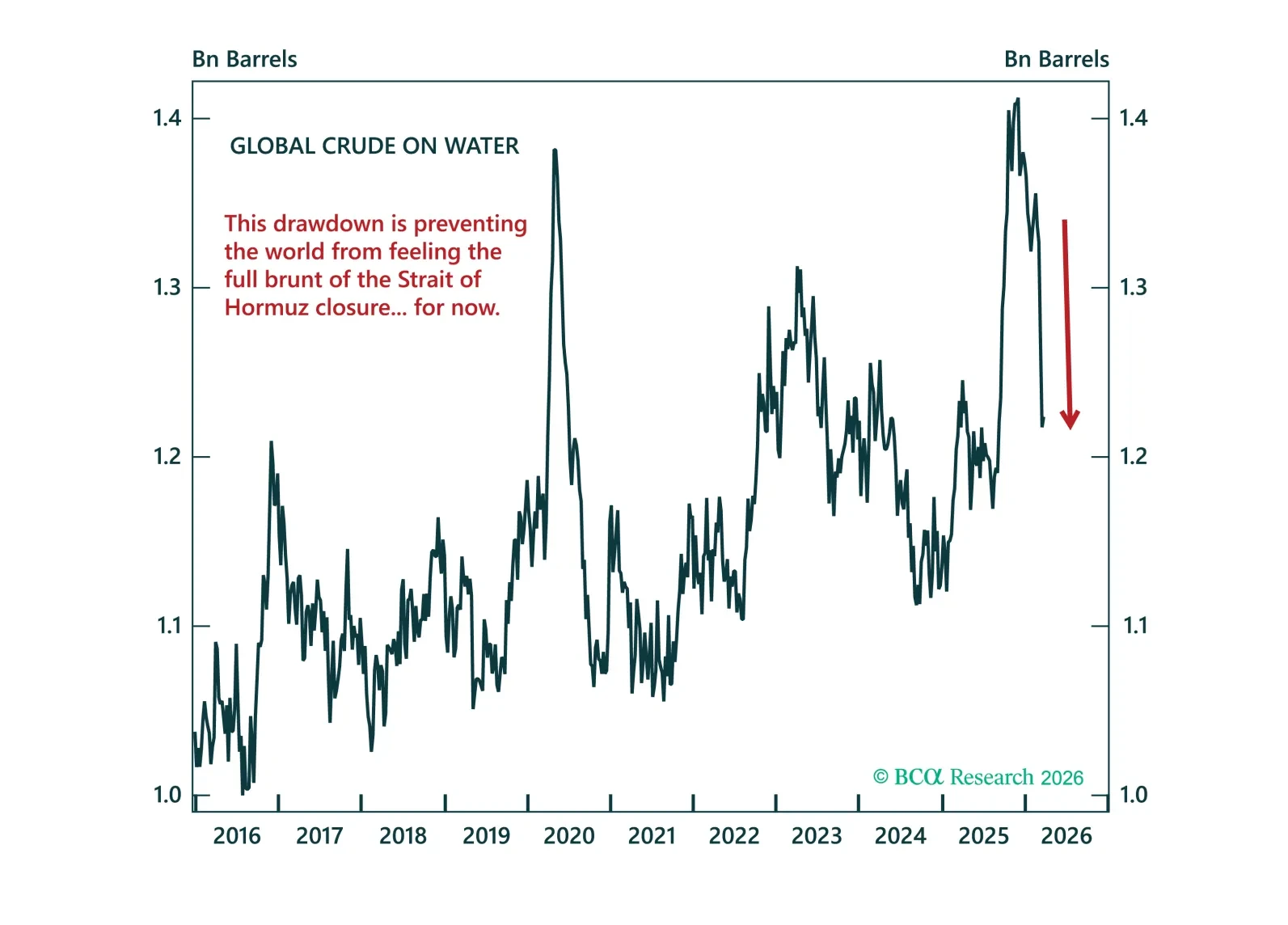

While the Middle East conflict’s inflationary impact is likely to persist, US recession risk is contained whereas non-US recession risk is more elevated. We discuss what this means for investment strategy. Plus, a new tactical trade is to underweight Utilities.

We are pleased to introduce our new Quarterly Investment Outlook, a joint publication bringing together the European Investment Strategy (EIS), Global Fixed Income Strategy (GFIS), and Foreign Exchange Strategy teams.

The main takeaway of the current edition is that investors should not add risk. Markets are still focused on inflation, but the binding constraint is growth: if the energy shock persists into mid-April, a rapid shift toward recession pricing will follow.

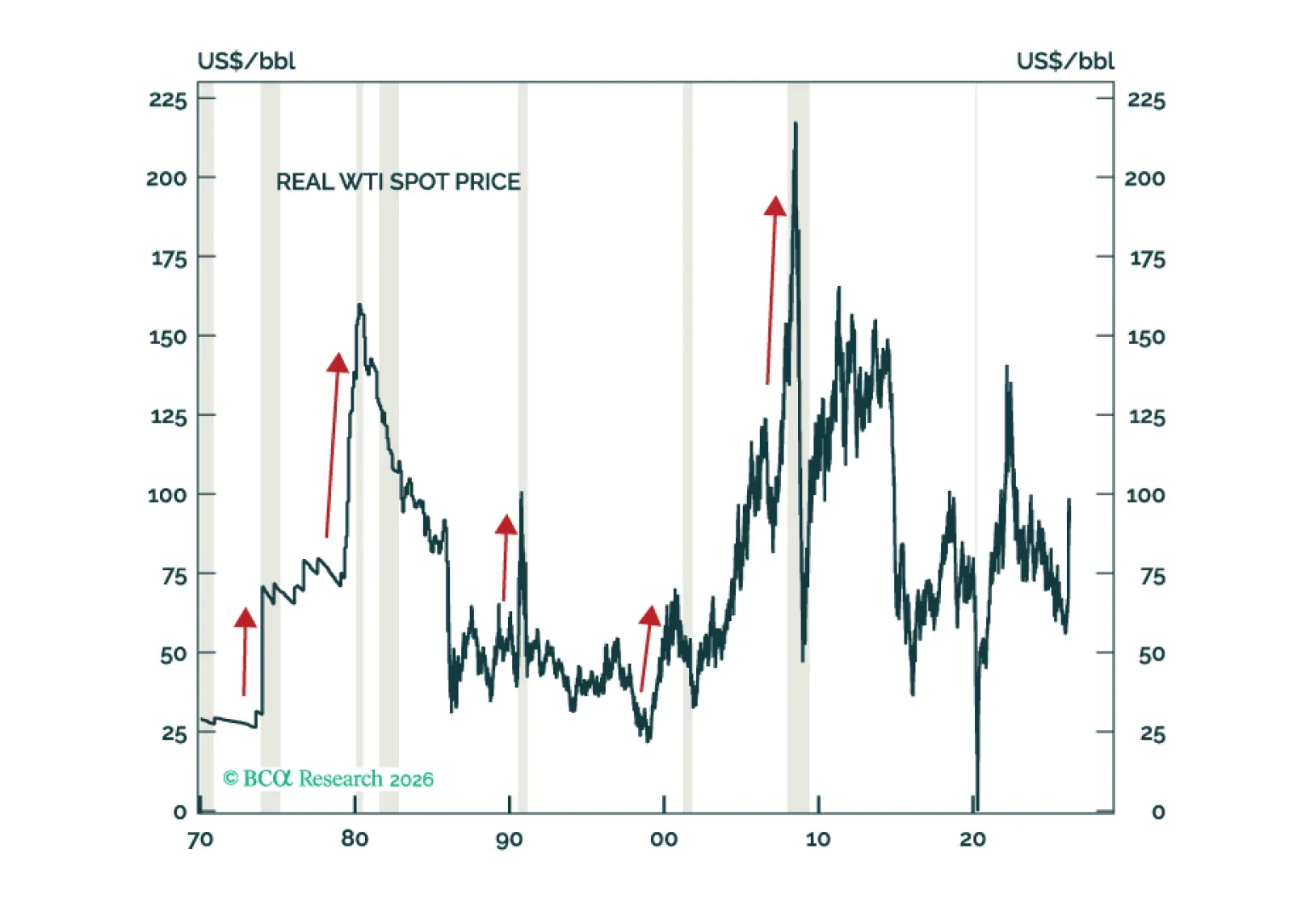

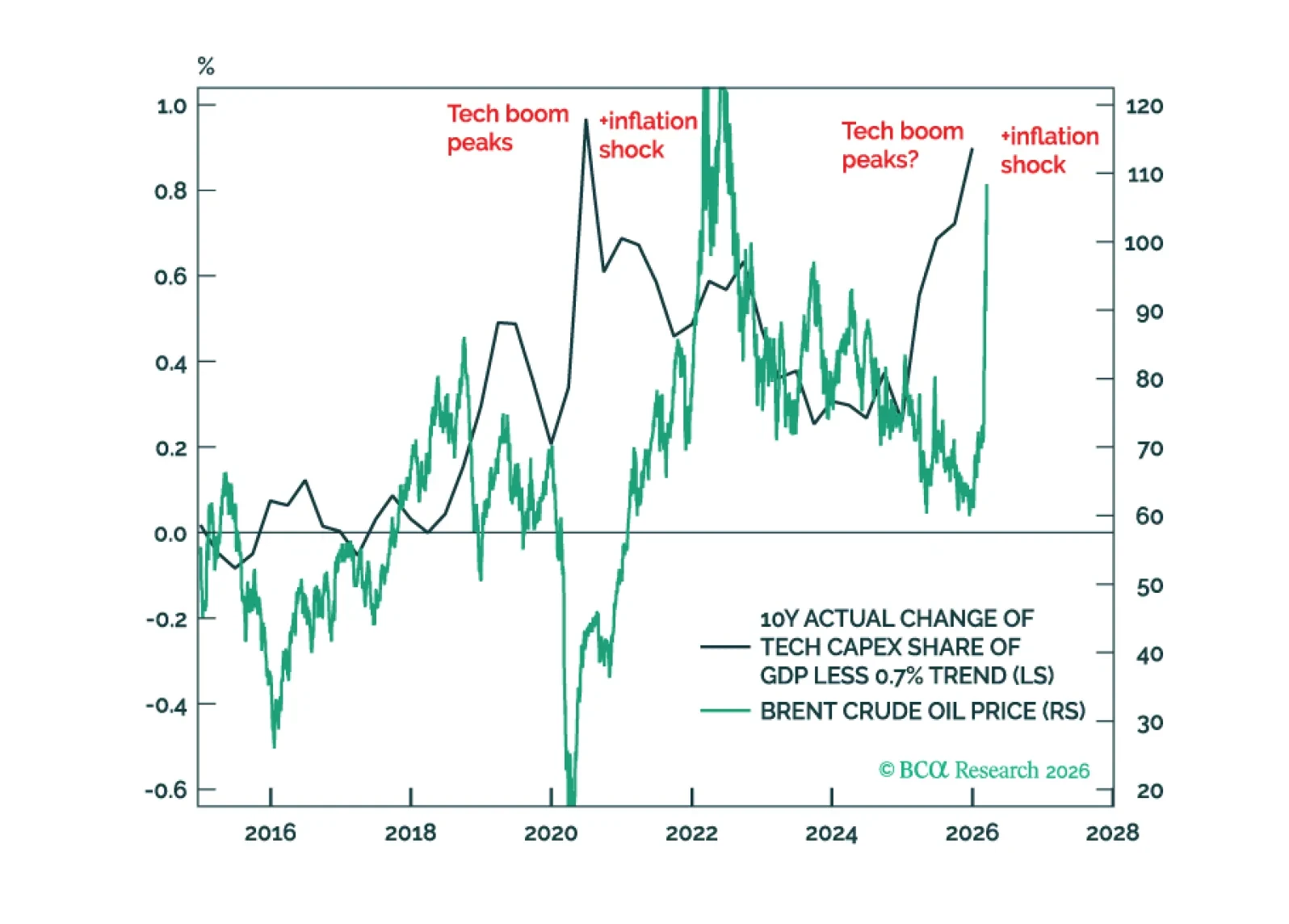

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

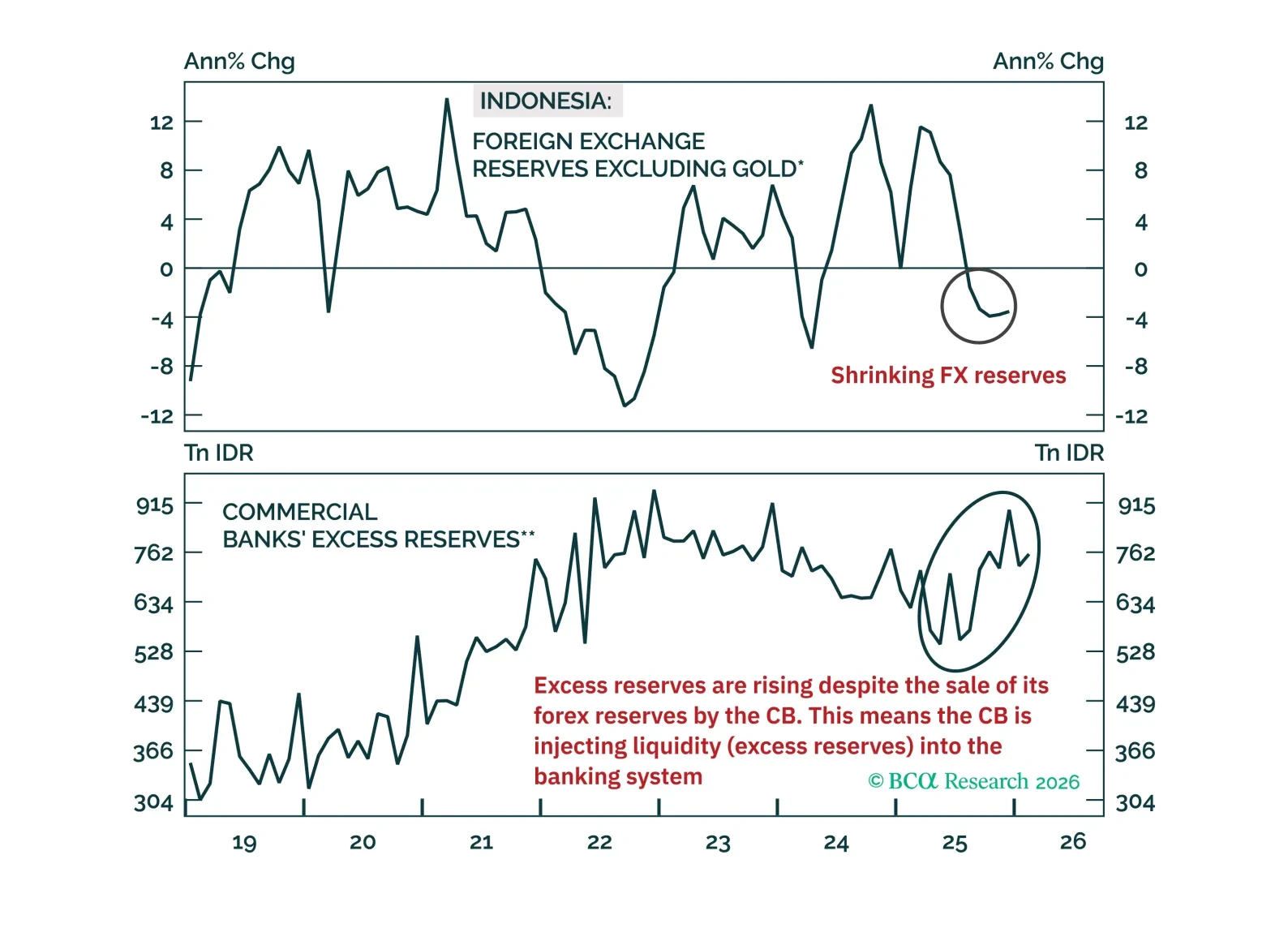

Indonesian rupiah will continue to plunge, and its local-currency bond yields will rise materially. Investors should short domestic bonds, currency unhedged.

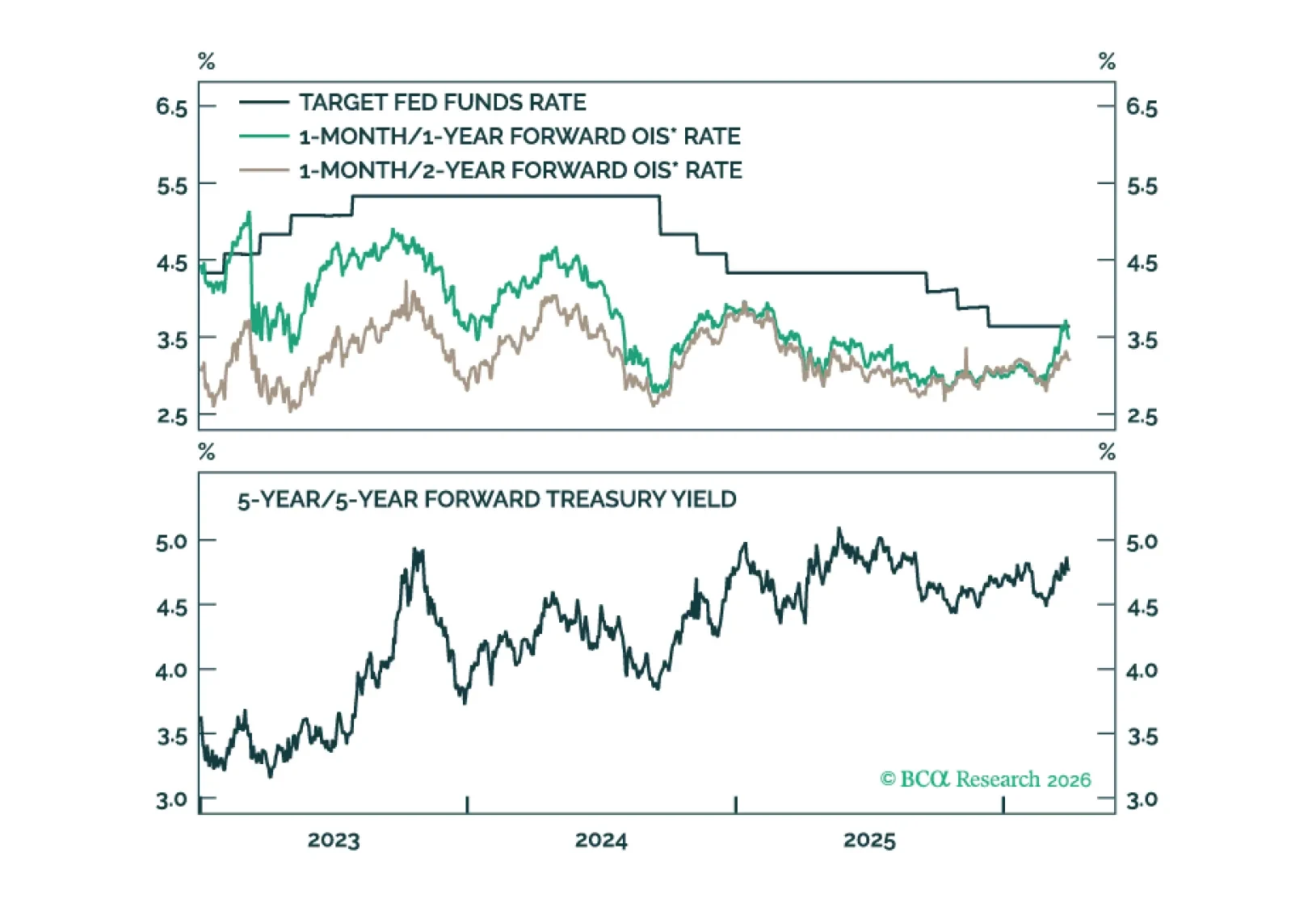

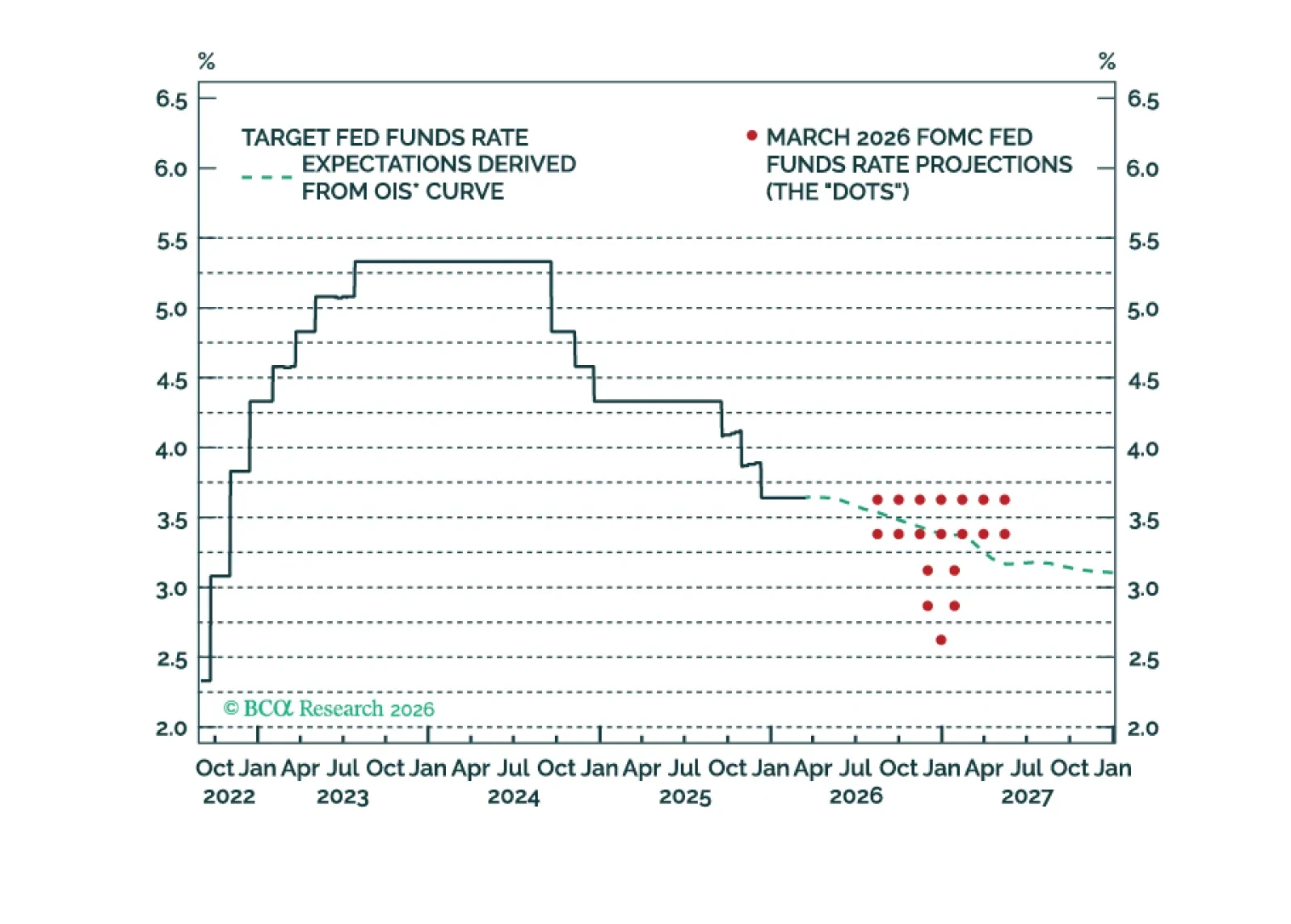

Forced to choose between growth and inflation, the Fed will save growth and the stock market rather than the 2 percent inflation target and the bond market.

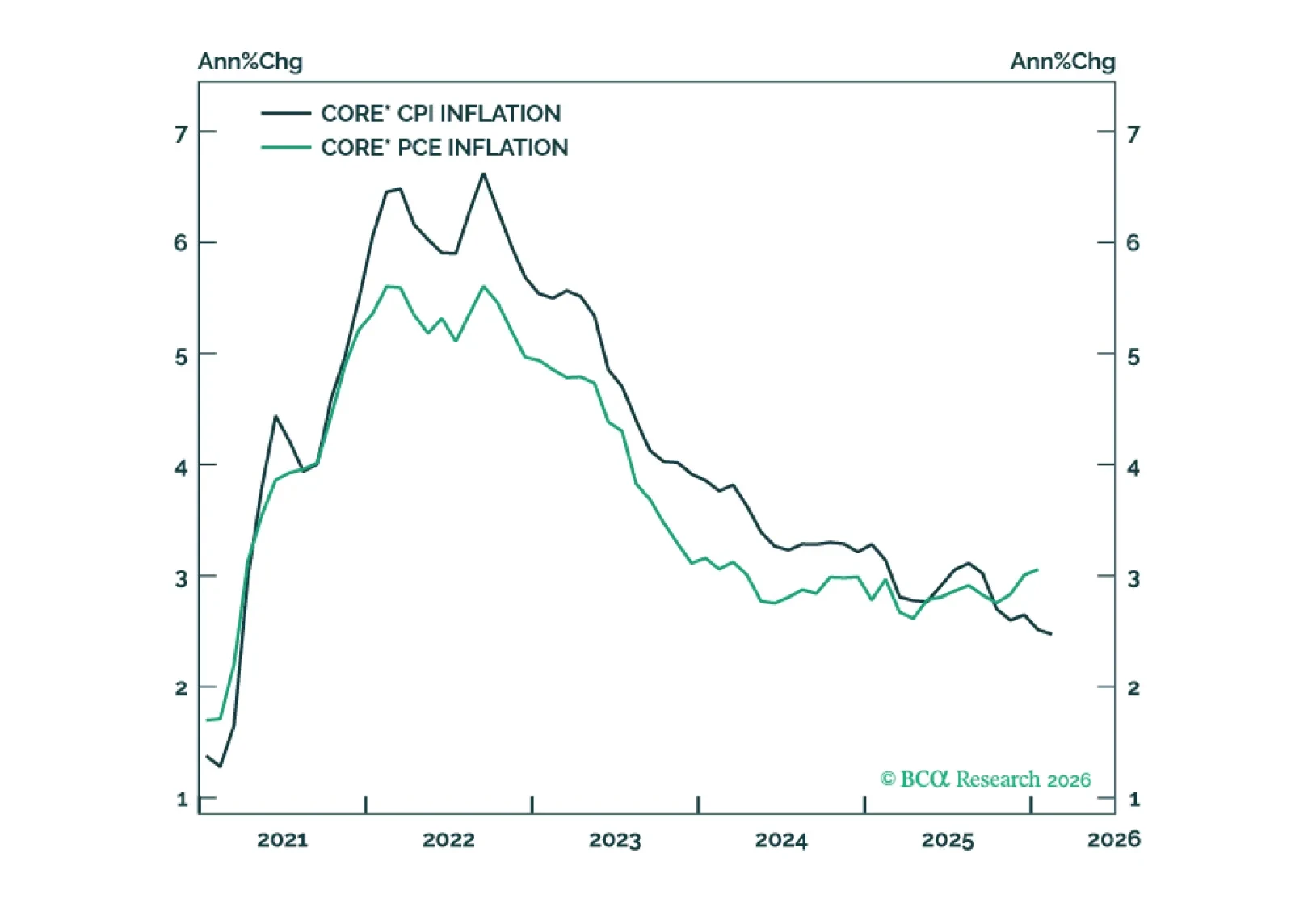

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

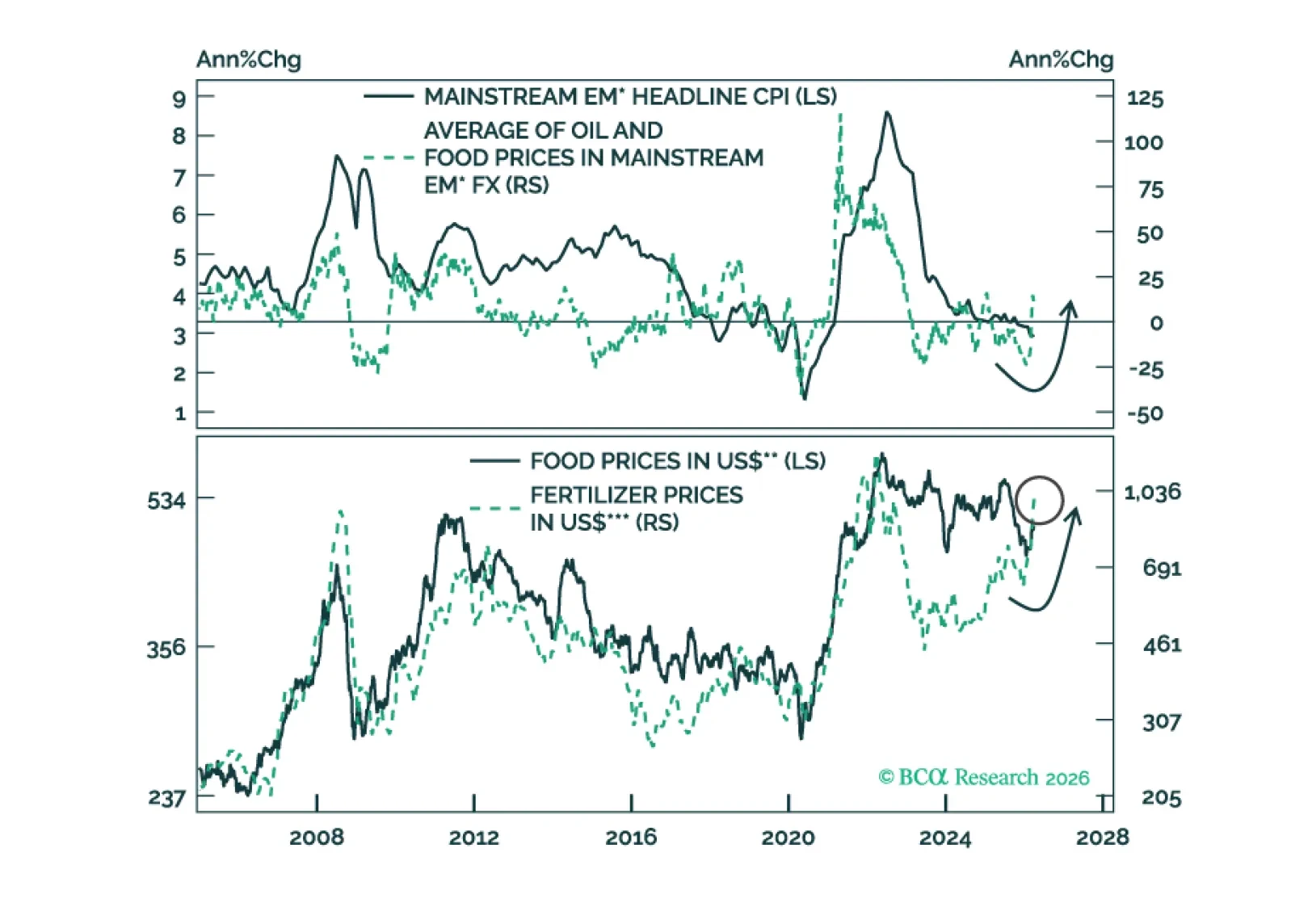

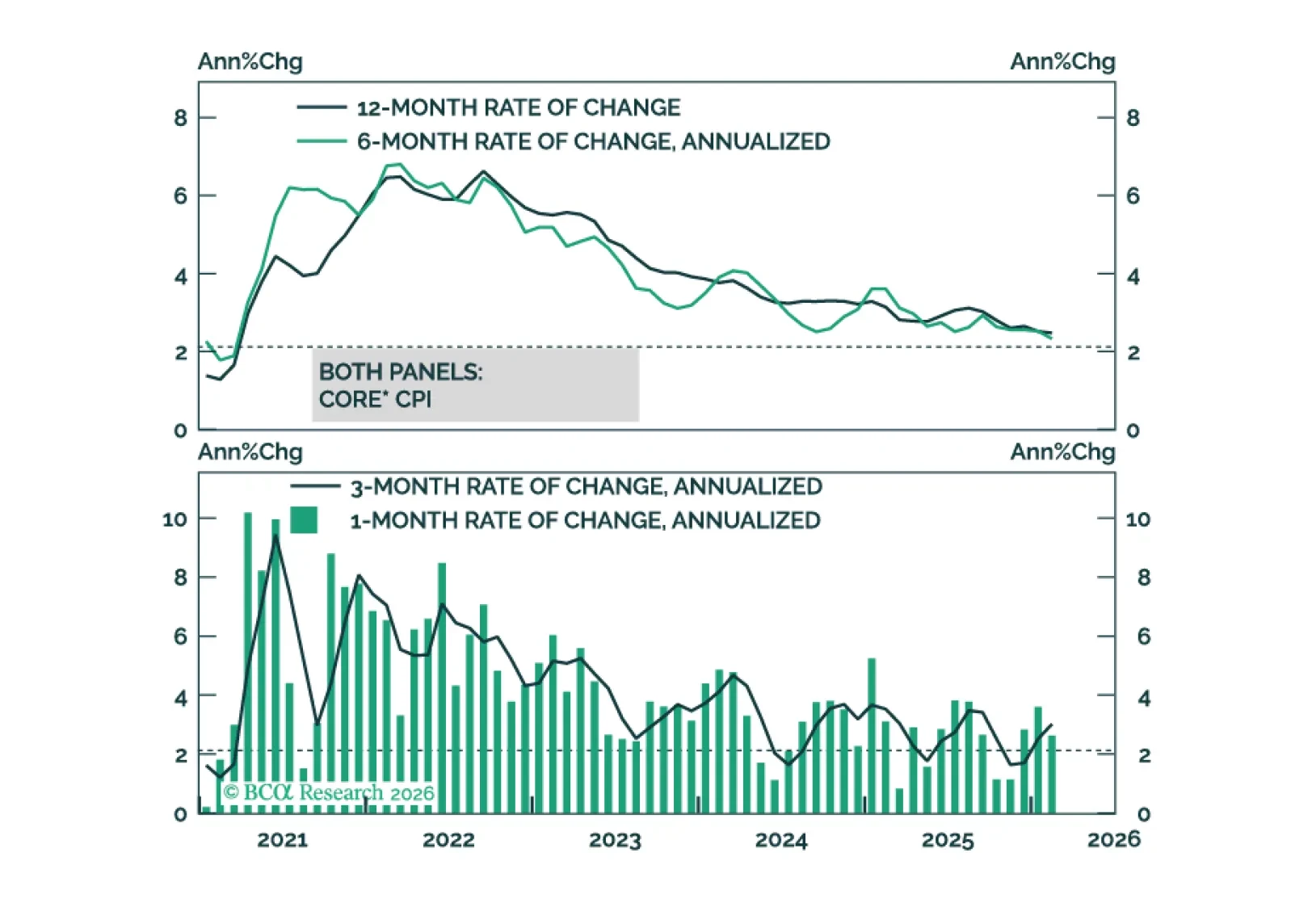

The recent oil price shock reinforces our view that inflation will surprise to the upside during the next few months but fall rapidly in H2 2026.